Investment Appraisal: Capital Budgeting and Strategic Control

VerifiedAdded on 2023/04/25

|7

|1609

|137

Report

AI Summary

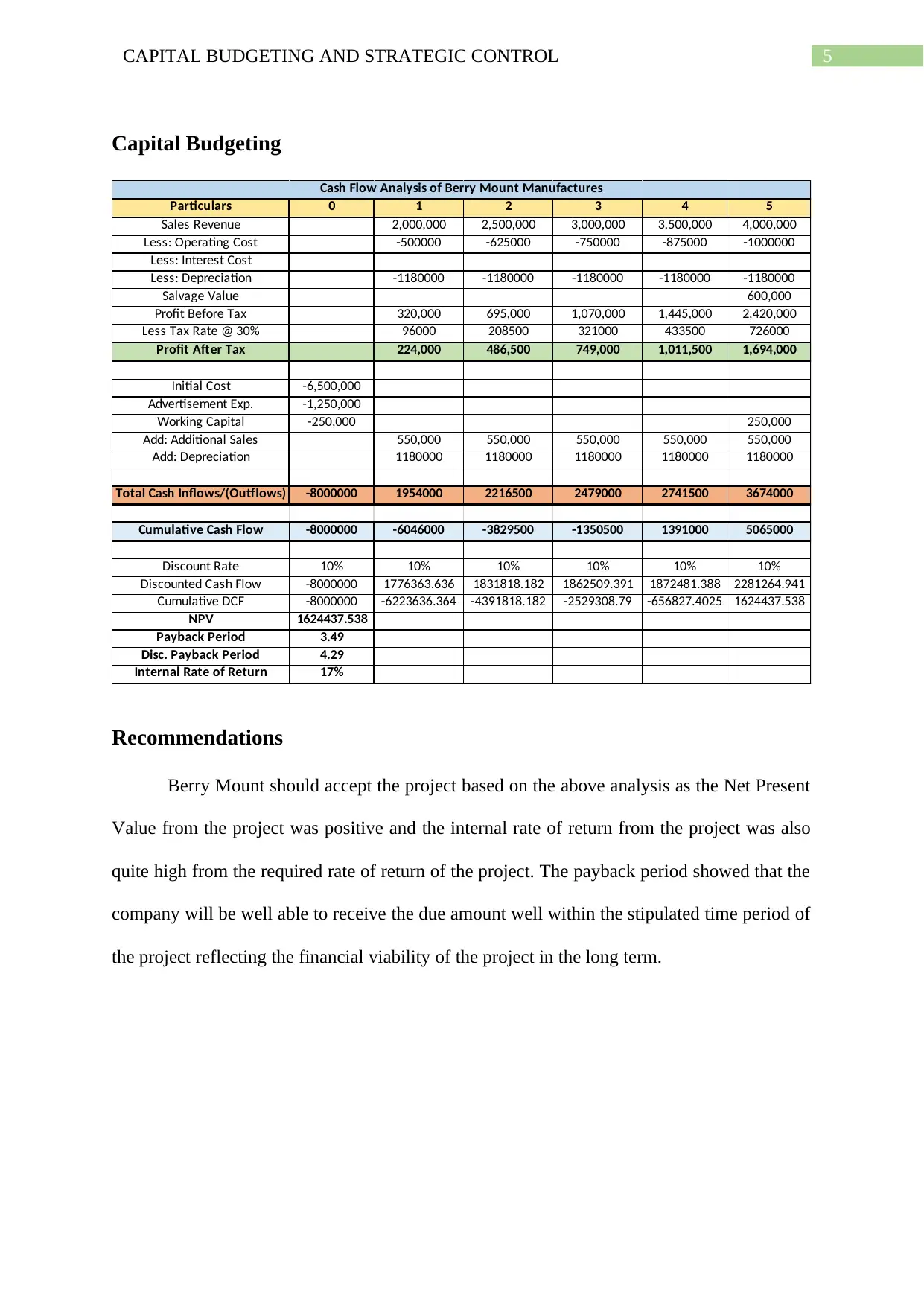

This report provides an overview of capital budgeting and strategic control, focusing on investment appraisal techniques. It discusses key concepts such as Net Present Value (NPV), payback period, discounted payback period, and profitability index. The report includes a cash flow analysis for Berry Mount Manufactures, demonstrating the application of these techniques. Sensitivity and scenario analyses are highlighted as crucial for assessing project viability under varying conditions. Ultimately, the report recommends that Berry Mount accept the project based on its positive NPV, high internal rate of return, and reasonable payback period, emphasizing the importance of comprehensive assessment in investment decision-making. Desklib offers a wealth of resources, including past papers and solved assignments, to aid students in mastering these complex financial concepts.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.