Business Decision Making: NPV, Payback, and Financial Factors

VerifiedAdded on 2023/01/11

|7

|1358

|69

Essay

AI Summary

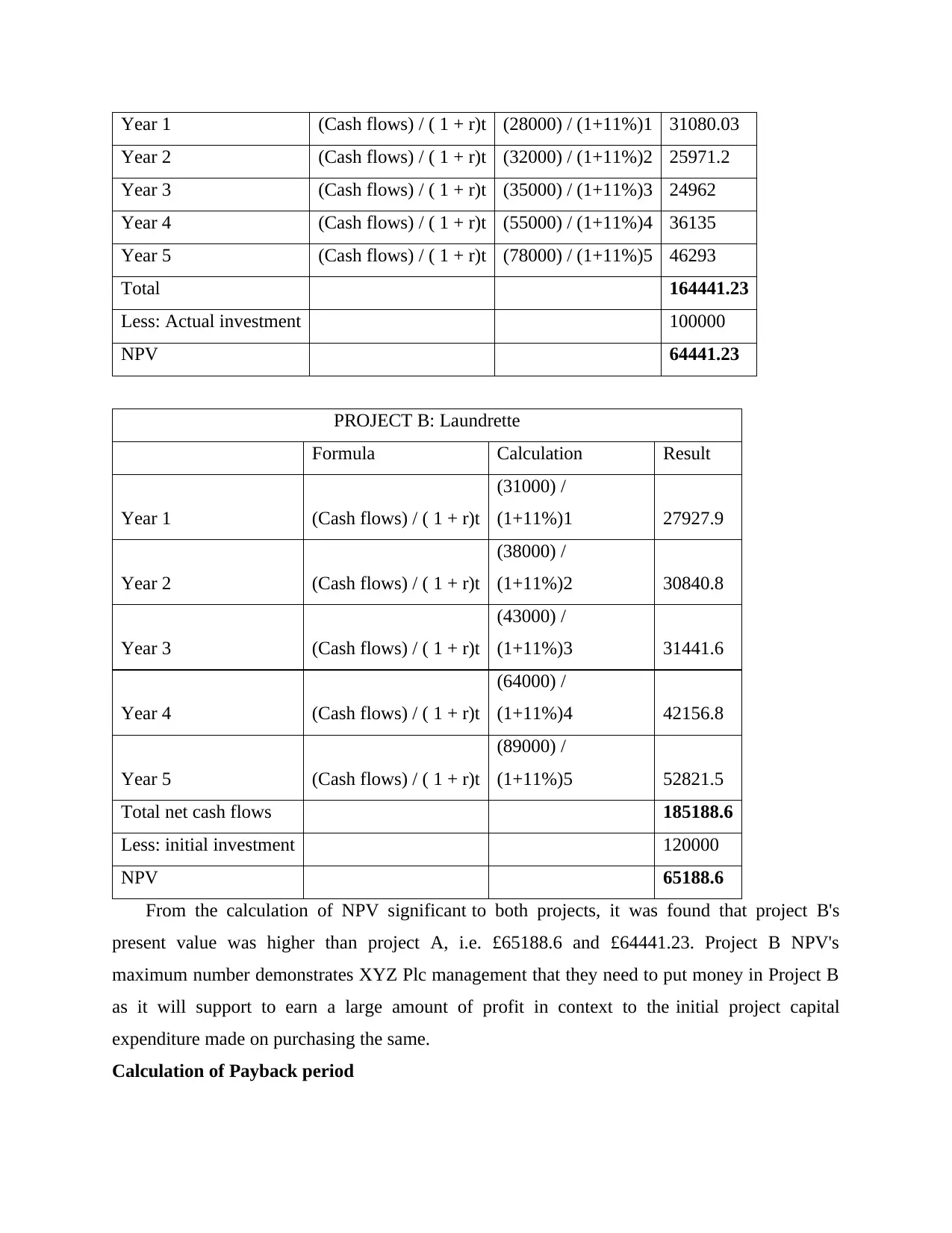

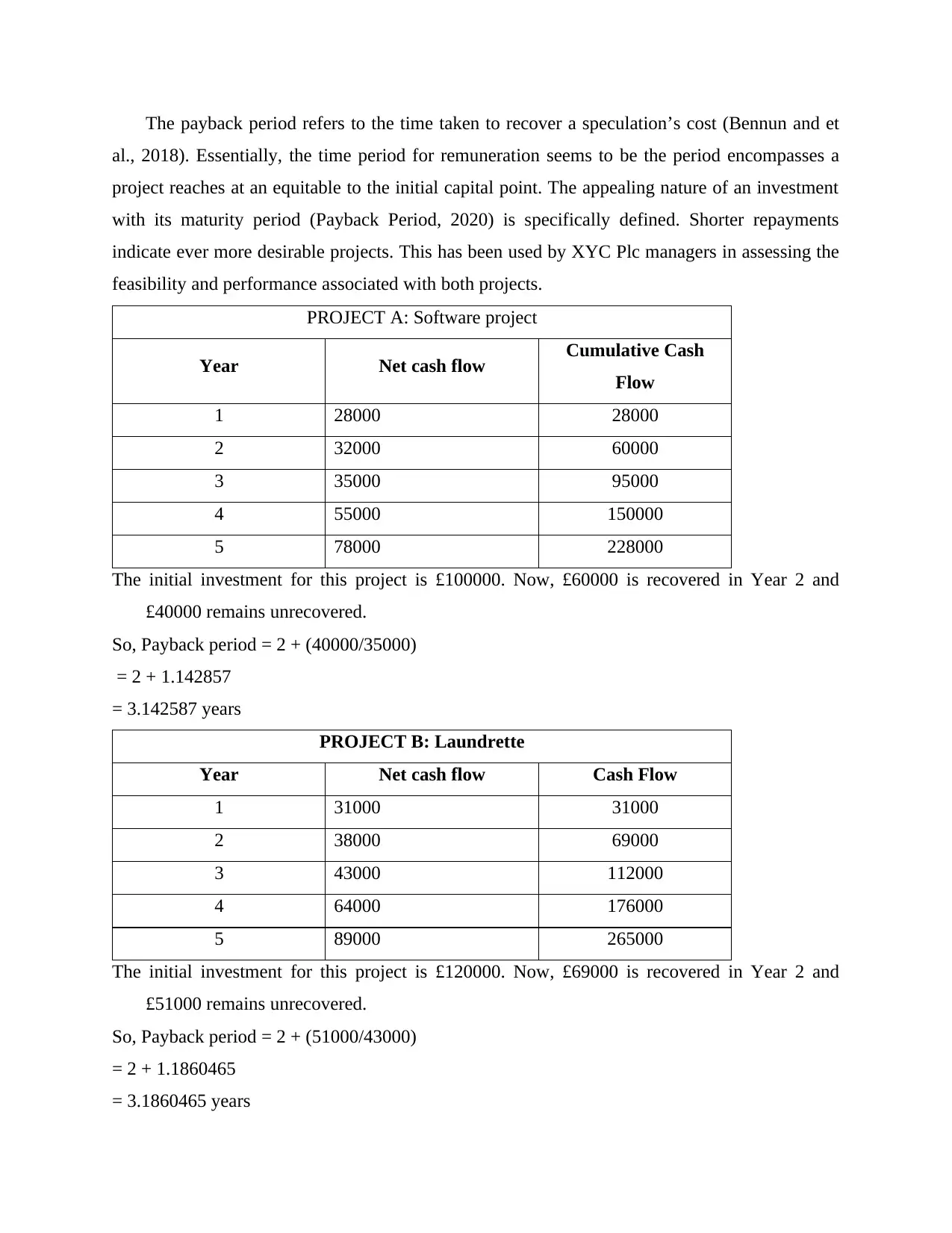

This essay examines business decision-making through the lens of capital budgeting techniques, specifically net present value (NPV) and payback period. It uses a case study of XYZ Plc, a budget chain restaurant considering investments in software or a laundrette project. The essay calculates and compares the NPV and payback periods for both projects, demonstrating how these techniques help in evaluating investment opportunities. It also discusses financial and non-financial factors influencing the decision, such as UK financial security and potential legislation. The conclusion recommends project B (laundrette) for better growth and success, based on the analysis. The essay emphasizes the importance of these techniques in making informed business decisions.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.