Analysis of Capital Budgeting Techniques for Financial Projects

VerifiedAdded on 2021/06/14

|16

|1675

|53

Homework Assignment

AI Summary

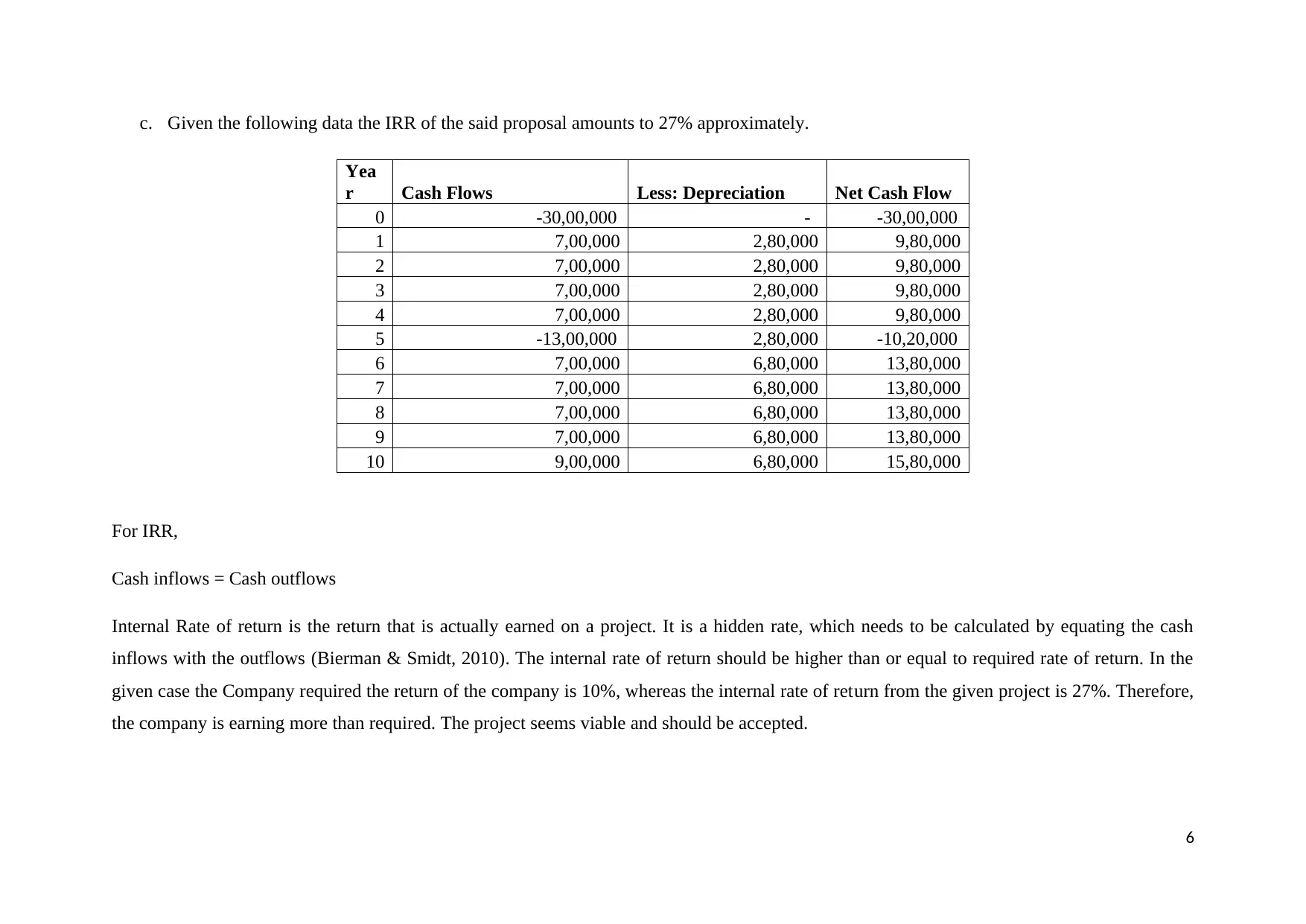

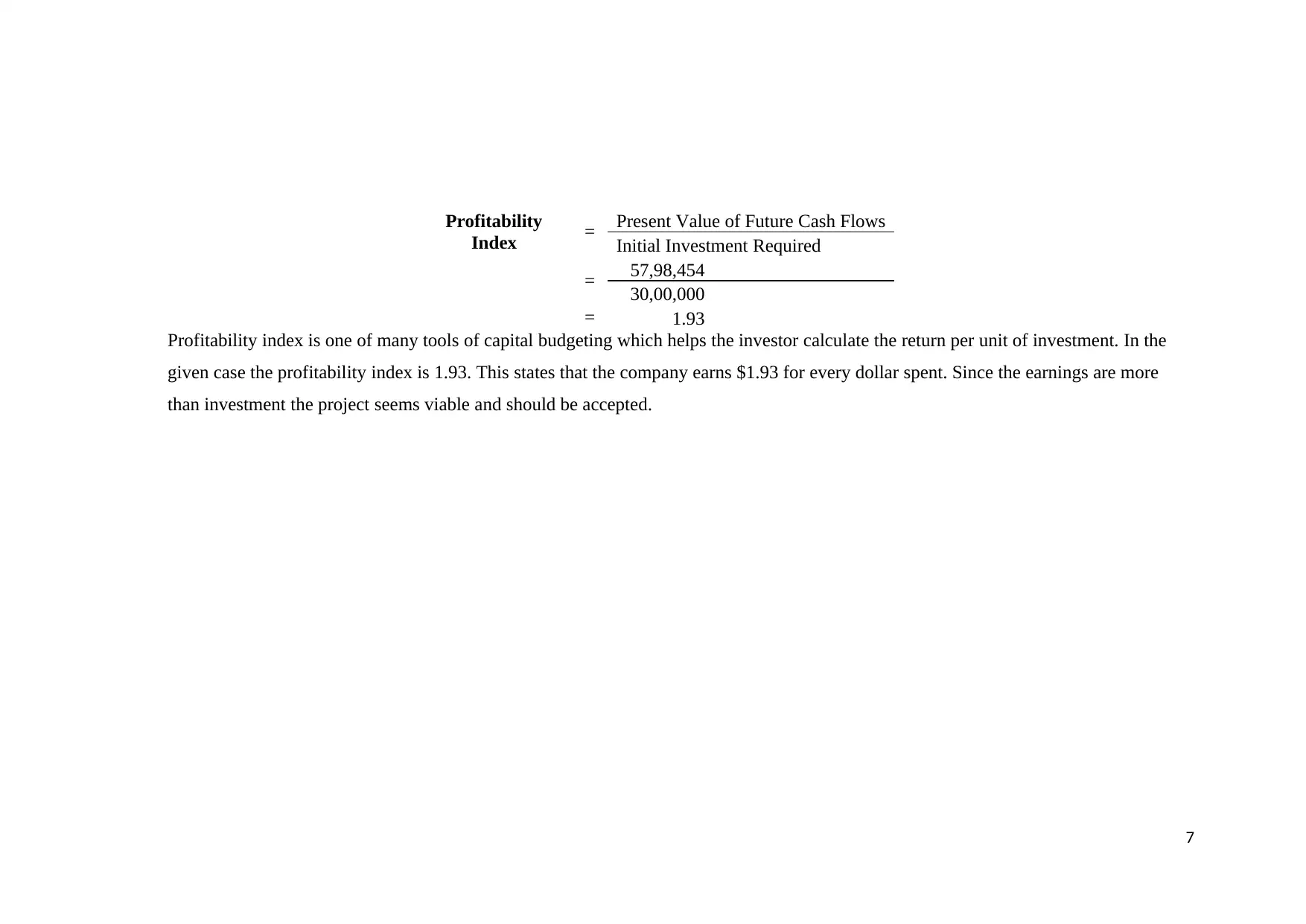

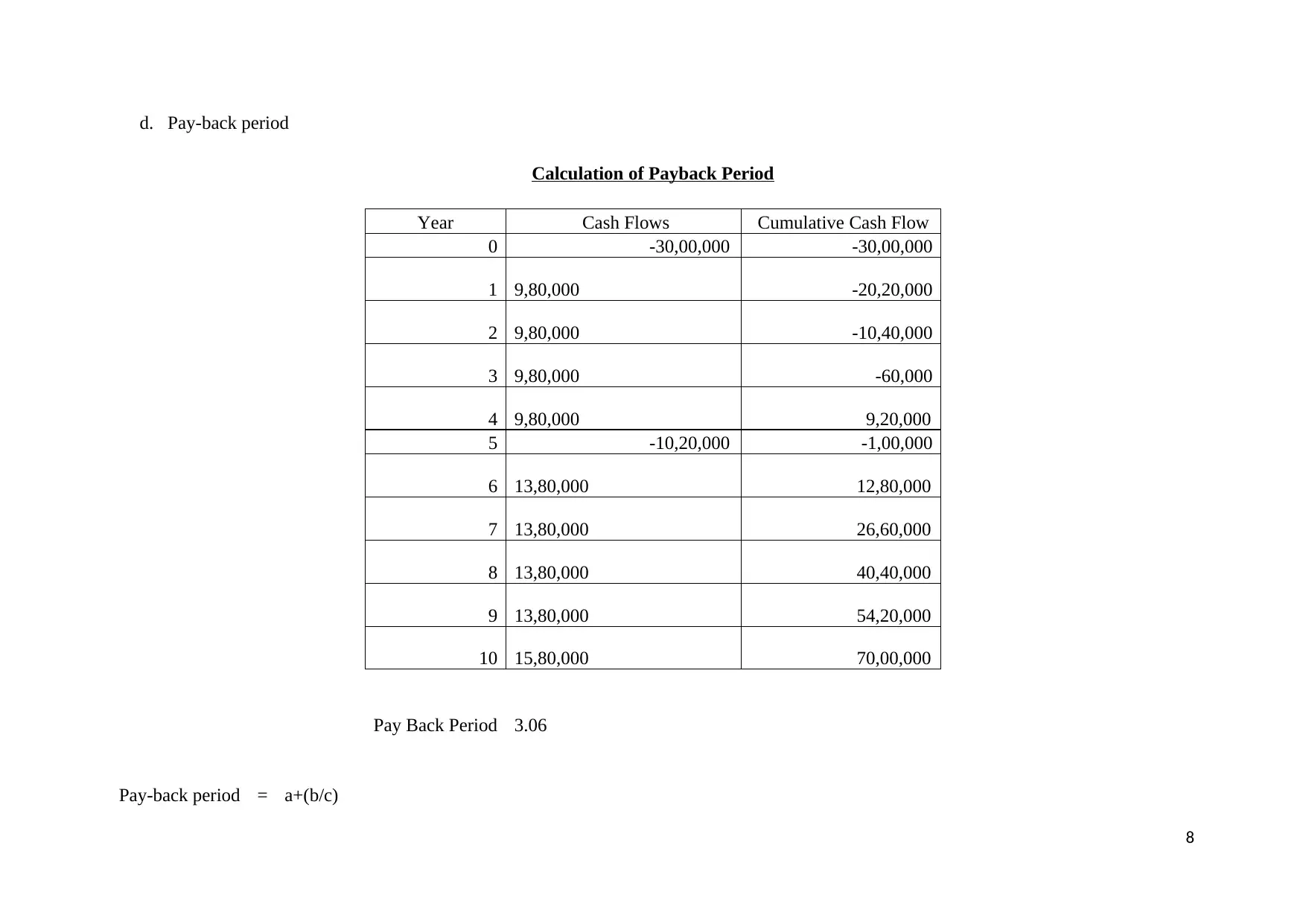

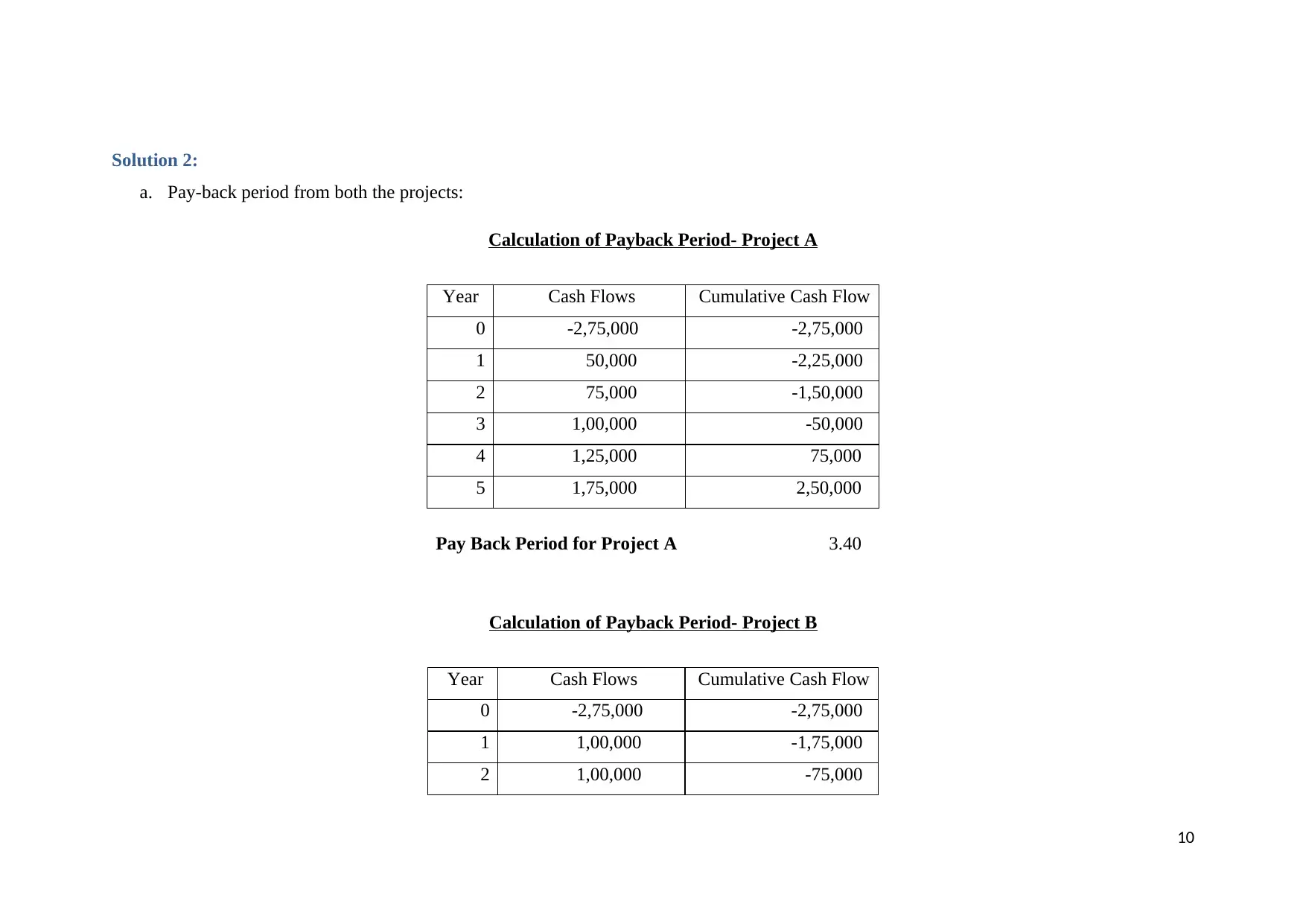

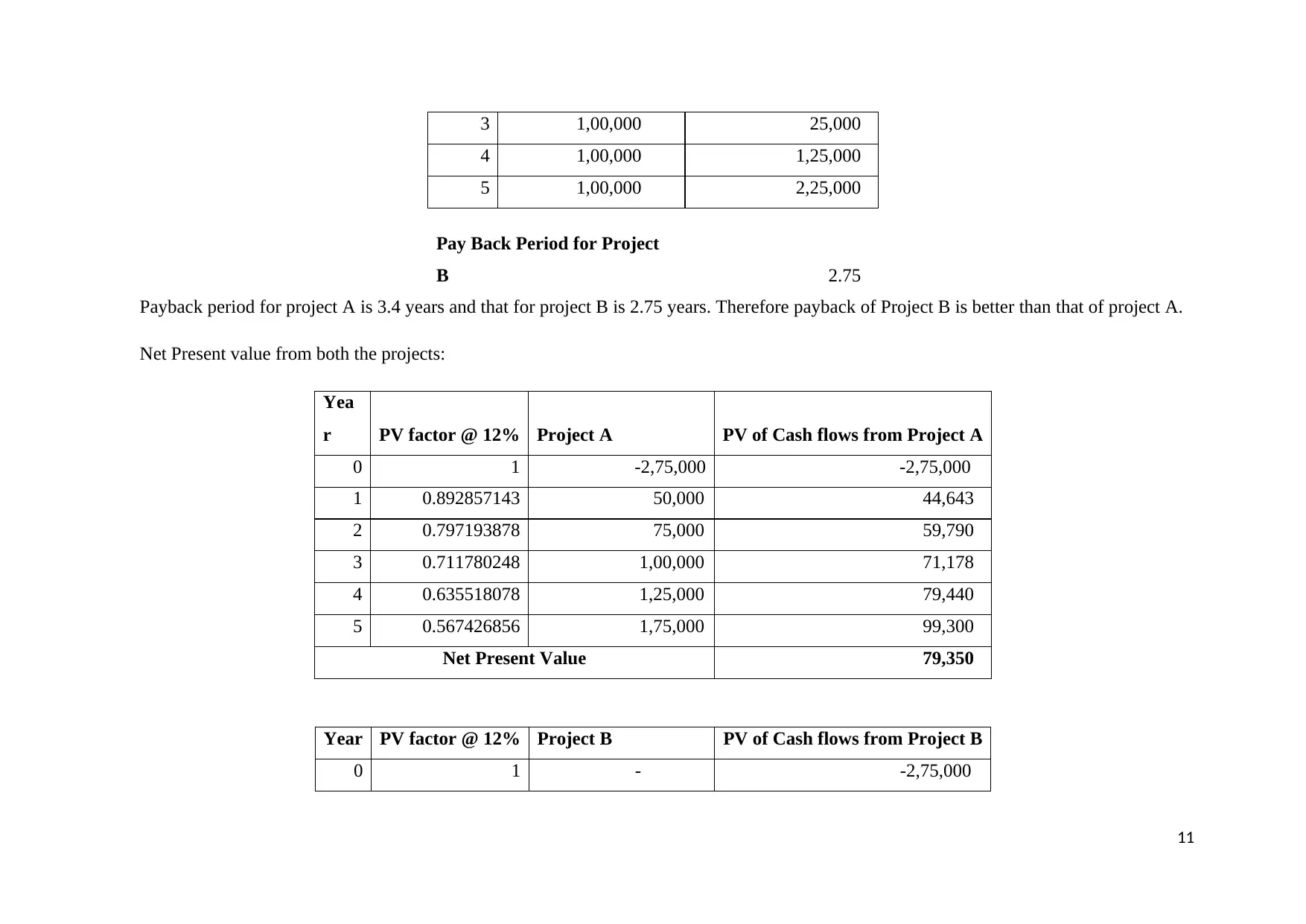

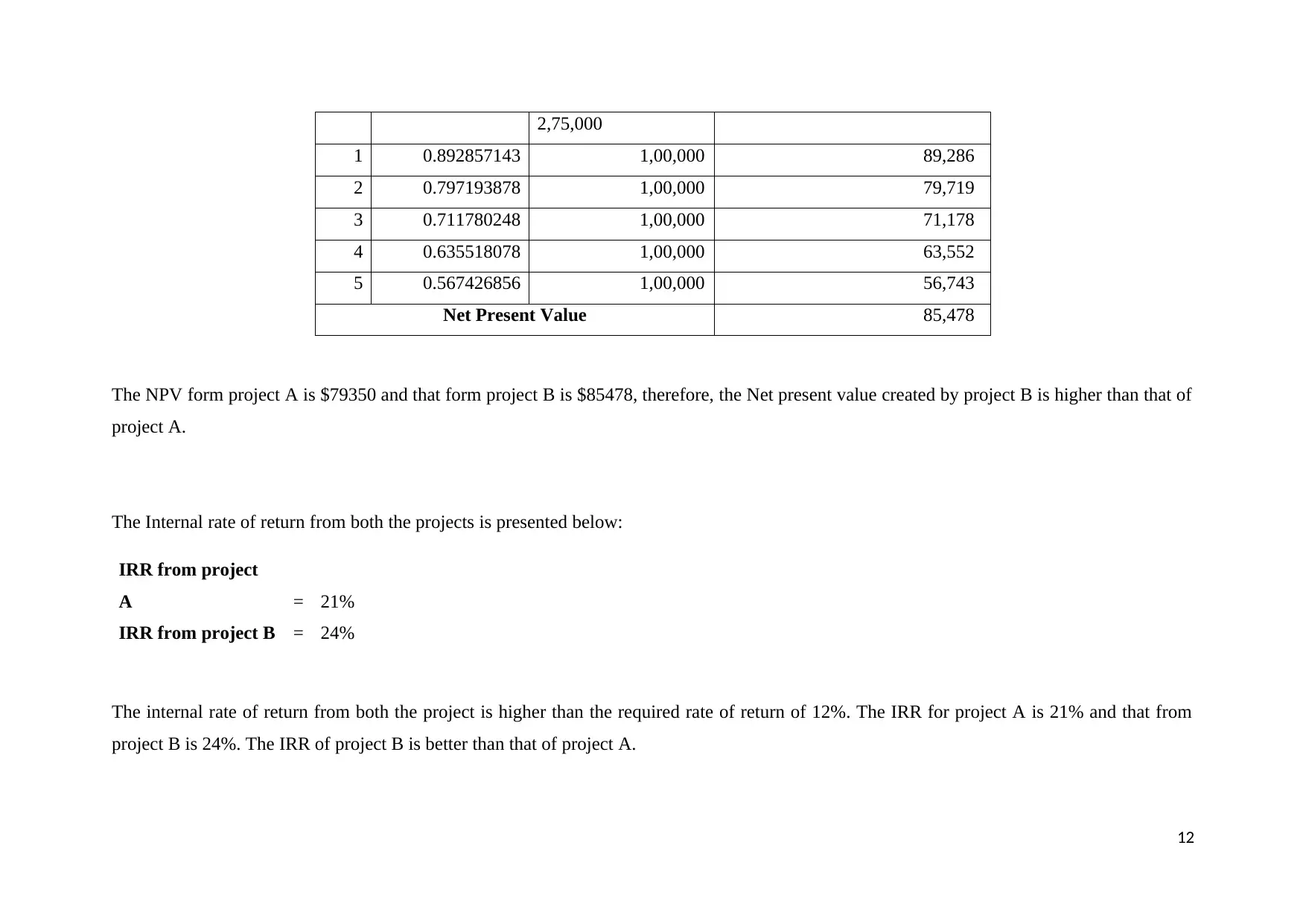

This assignment analyzes two financial projects using capital budgeting techniques. Solution 1 calculates the Net Present Value (NPV), Internal Rate of Return (IRR), Profitability Index, and Payback Period for a new plant investment, concluding the project is viable. Solution 2 compares two projects (A and B), calculating their payback periods, NPVs, and IRRs. The analysis reveals that Project B has a higher NPV and IRR, and a shorter payback period, making it the preferred choice. The assignment highlights the importance of these capital budgeting tools in evaluating investment opportunities and making informed financial decisions. The document also includes a bibliography citing relevant finance resources.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.