Capital Budgeting in Finance: Methods, Techniques, and Analysis Report

VerifiedAdded on 2020/02/19

|9

|2706

|105

Report

AI Summary

This report provides a comprehensive overview of capital budgeting, a crucial process in financial planning for companies. It explores the importance of capital budgeting, including its role in forecasting cash flows and setting long-term strategic goals. The report discusses various methods such as Net Present Value (NPV) and Internal Rate of Return (IRR), providing examples and calculations to illustrate their application. It also delves into the limitations of capital budgeting, such as ignoring non-quantifiable factors and the inherent uncertainty of future market conditions. Furthermore, the report examines techniques like sensitivity analysis, scenario analysis, breakeven analysis, and simulation analysis, explaining their functionalities and significance in financial decision-making. The report emphasizes the role of these techniques in assessing risk, understanding the impact of variable changes, and making informed investment choices.

CAPITAL BUDGETING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

Decisions are to be taken for many things in the company the matter can be major or minor.

The responsibility of decision making lies in the hands of the management. The management

is wholly responsible for the results of that decision making. Some of the examples where

decision making is required are acceptance or repentance of a special order, investment

decision, borrowing decision etc (Berman, Knight and Case, n.d.)..

We know that a company cannot survive without funds, whether small in nature or big.

Therefore, it is important to carry out proper financial planning. A company needs several

assets in order to grow, expand and earn profits but before investing in such asset it is

important to know whether it is worth funding cash for these or not. This decision can be

taken with the help of a method known as capital budgeting (Bruner, Eades and Schill, 2017).

Capital budgeting plays a major role in financial planning and therefore, it has its own

importance. The importance of capital budgeting are (TULSIAN, 2016)-

1. This process helps to forecast the future cash inflows and outflows of a company

which further helps to decide about the acceptance of a particular project.

2. The process of decision making is carried out at all the levels of the organisation and

this process begins when there is an idea of a new project till this project is concluded.

Hence, it is required at every time of the company’s working.

3. A company can grow, expand and compete well only when it has the ability to

develop long term strategic goals. However, capital budgeting is a process which is

helpful in setting these goals.

4. There are huge expenditures incurred in a company but it is always important to

monitor and analyse the benefits of spending funds, this becomes easier with the help

of the capital budgeting expenditure.

Capital budgeting is used by many companies as it is beneficial in taking long term

decisions. However, this process also has certain limitation which a company should

know before its adoption (Clarke and Clarke, 1990)-

1. Markets are dynamic in nature; therefore we can never now about the risk and

uncertainty that may arise. Capital budgeting ignore the risk element and the

uncertainty element (Fairhurst, 2015).

2. Capital budgeting takes into consideration certain financial factor, it complete ignore

the non quantifiable factor such as reputation of the company, employee morale etc.

3. There is no guarantee that the decision taken through this process will be correct

because capital budgeting is a process which takes future into consideration and no

one is capable enough to predict the future (Taylor, 2008).

4. The capital investment decisions can also be limited by urgency.

Capital budgeting involves various methods and techniques. Firstly, let us now

understand the method involved in capital budgeting-

Decisions are to be taken for many things in the company the matter can be major or minor.

The responsibility of decision making lies in the hands of the management. The management

is wholly responsible for the results of that decision making. Some of the examples where

decision making is required are acceptance or repentance of a special order, investment

decision, borrowing decision etc (Berman, Knight and Case, n.d.)..

We know that a company cannot survive without funds, whether small in nature or big.

Therefore, it is important to carry out proper financial planning. A company needs several

assets in order to grow, expand and earn profits but before investing in such asset it is

important to know whether it is worth funding cash for these or not. This decision can be

taken with the help of a method known as capital budgeting (Bruner, Eades and Schill, 2017).

Capital budgeting plays a major role in financial planning and therefore, it has its own

importance. The importance of capital budgeting are (TULSIAN, 2016)-

1. This process helps to forecast the future cash inflows and outflows of a company

which further helps to decide about the acceptance of a particular project.

2. The process of decision making is carried out at all the levels of the organisation and

this process begins when there is an idea of a new project till this project is concluded.

Hence, it is required at every time of the company’s working.

3. A company can grow, expand and compete well only when it has the ability to

develop long term strategic goals. However, capital budgeting is a process which is

helpful in setting these goals.

4. There are huge expenditures incurred in a company but it is always important to

monitor and analyse the benefits of spending funds, this becomes easier with the help

of the capital budgeting expenditure.

Capital budgeting is used by many companies as it is beneficial in taking long term

decisions. However, this process also has certain limitation which a company should

know before its adoption (Clarke and Clarke, 1990)-

1. Markets are dynamic in nature; therefore we can never now about the risk and

uncertainty that may arise. Capital budgeting ignore the risk element and the

uncertainty element (Fairhurst, 2015).

2. Capital budgeting takes into consideration certain financial factor, it complete ignore

the non quantifiable factor such as reputation of the company, employee morale etc.

3. There is no guarantee that the decision taken through this process will be correct

because capital budgeting is a process which takes future into consideration and no

one is capable enough to predict the future (Taylor, 2008).

4. The capital investment decisions can also be limited by urgency.

Capital budgeting involves various methods and techniques. Firstly, let us now

understand the method involved in capital budgeting-

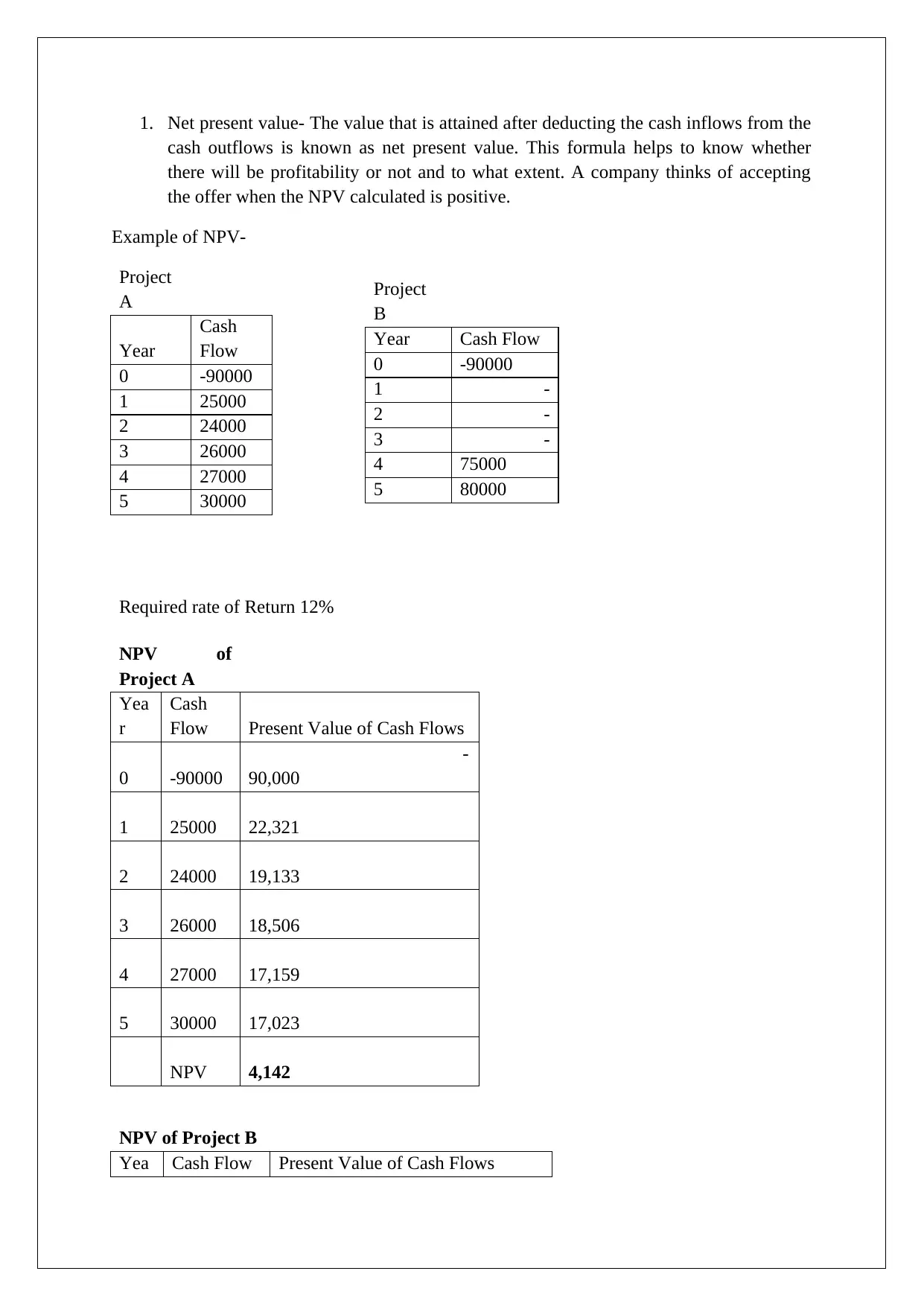

1. Net present value- The value that is attained after deducting the cash inflows from the

cash outflows is known as net present value. This formula helps to know whether

there will be profitability or not and to what extent. A company thinks of accepting

the offer when the NPV calculated is positive.

Example of NPV-

Project

A

Year

Cash

Flow

0 -90000

1 25000

2 24000

3 26000

4 27000

5 30000

Required rate of Return 12%

NPV of

Project A

Yea

r

Cash

Flow Present Value of Cash Flows

0 -90000

-

90,000

1 25000 22,321

2 24000 19,133

3 26000 18,506

4 27000 17,159

5 30000 17,023

NPV 4,142

NPV of Project B

Yea Cash Flow Present Value of Cash Flows

Project

B

Year Cash Flow

0 -90000

1 -

2 -

3 -

4 75000

5 80000

cash outflows is known as net present value. This formula helps to know whether

there will be profitability or not and to what extent. A company thinks of accepting

the offer when the NPV calculated is positive.

Example of NPV-

Project

A

Year

Cash

Flow

0 -90000

1 25000

2 24000

3 26000

4 27000

5 30000

Required rate of Return 12%

NPV of

Project A

Yea

r

Cash

Flow Present Value of Cash Flows

0 -90000

-

90,000

1 25000 22,321

2 24000 19,133

3 26000 18,506

4 27000 17,159

5 30000 17,023

NPV 4,142

NPV of Project B

Yea Cash Flow Present Value of Cash Flows

Project

B

Year Cash Flow

0 -90000

1 -

2 -

3 -

4 75000

5 80000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

r

0 -90000 -90000

1 - -

2 - -

3 - -

4 75000 47,664

5 80000 45,394

NPV 3,058

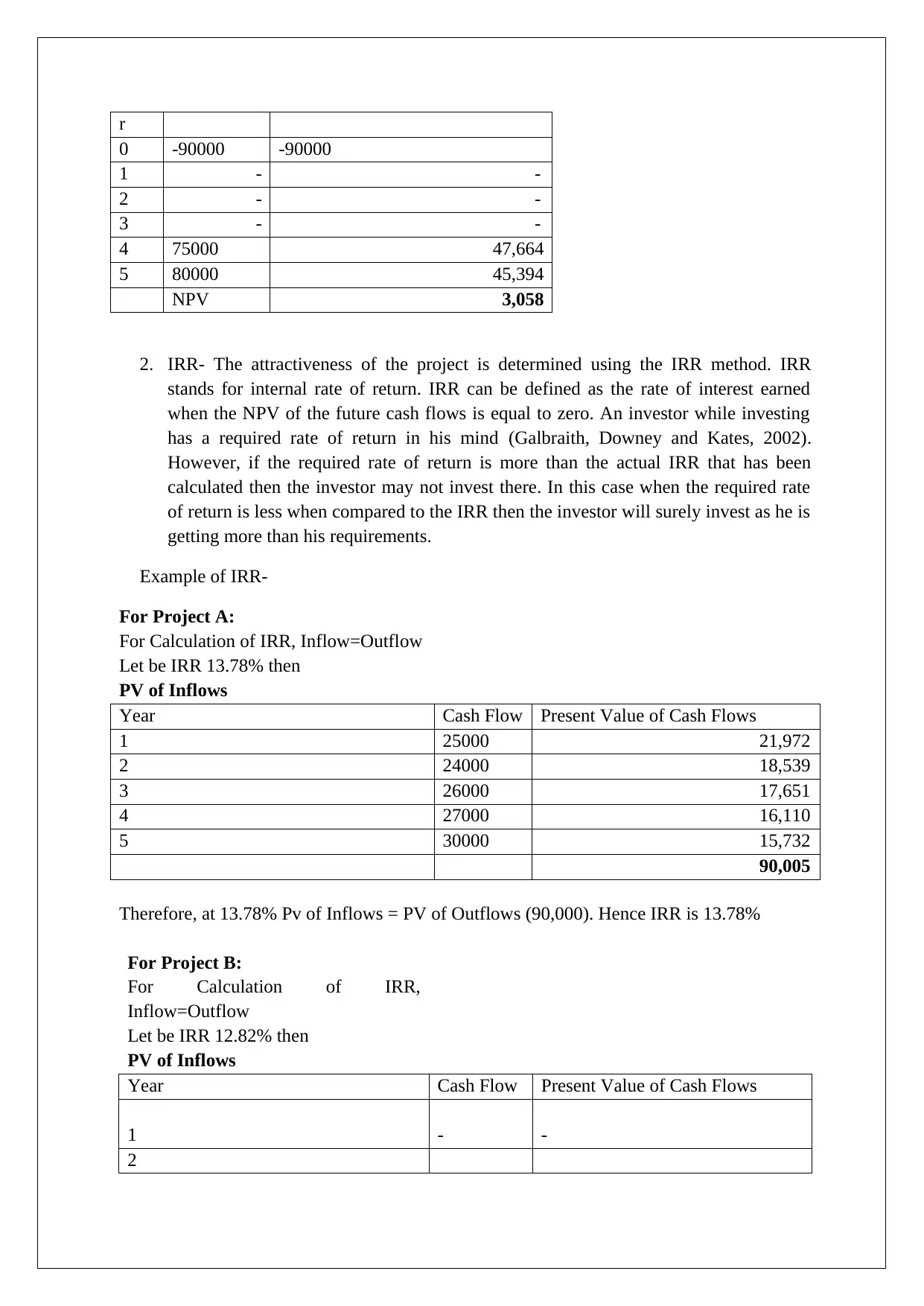

2. IRR- The attractiveness of the project is determined using the IRR method. IRR

stands for internal rate of return. IRR can be defined as the rate of interest earned

when the NPV of the future cash flows is equal to zero. An investor while investing

has a required rate of return in his mind (Galbraith, Downey and Kates, 2002).

However, if the required rate of return is more than the actual IRR that has been

calculated then the investor may not invest there. In this case when the required rate

of return is less when compared to the IRR then the investor will surely invest as he is

getting more than his requirements.

Example of IRR-

For Project A:

For Calculation of IRR, Inflow=Outflow

Let be IRR 13.78% then

PV of Inflows

Year Cash Flow Present Value of Cash Flows

1 25000 21,972

2 24000 18,539

3 26000 17,651

4 27000 16,110

5 30000 15,732

90,005

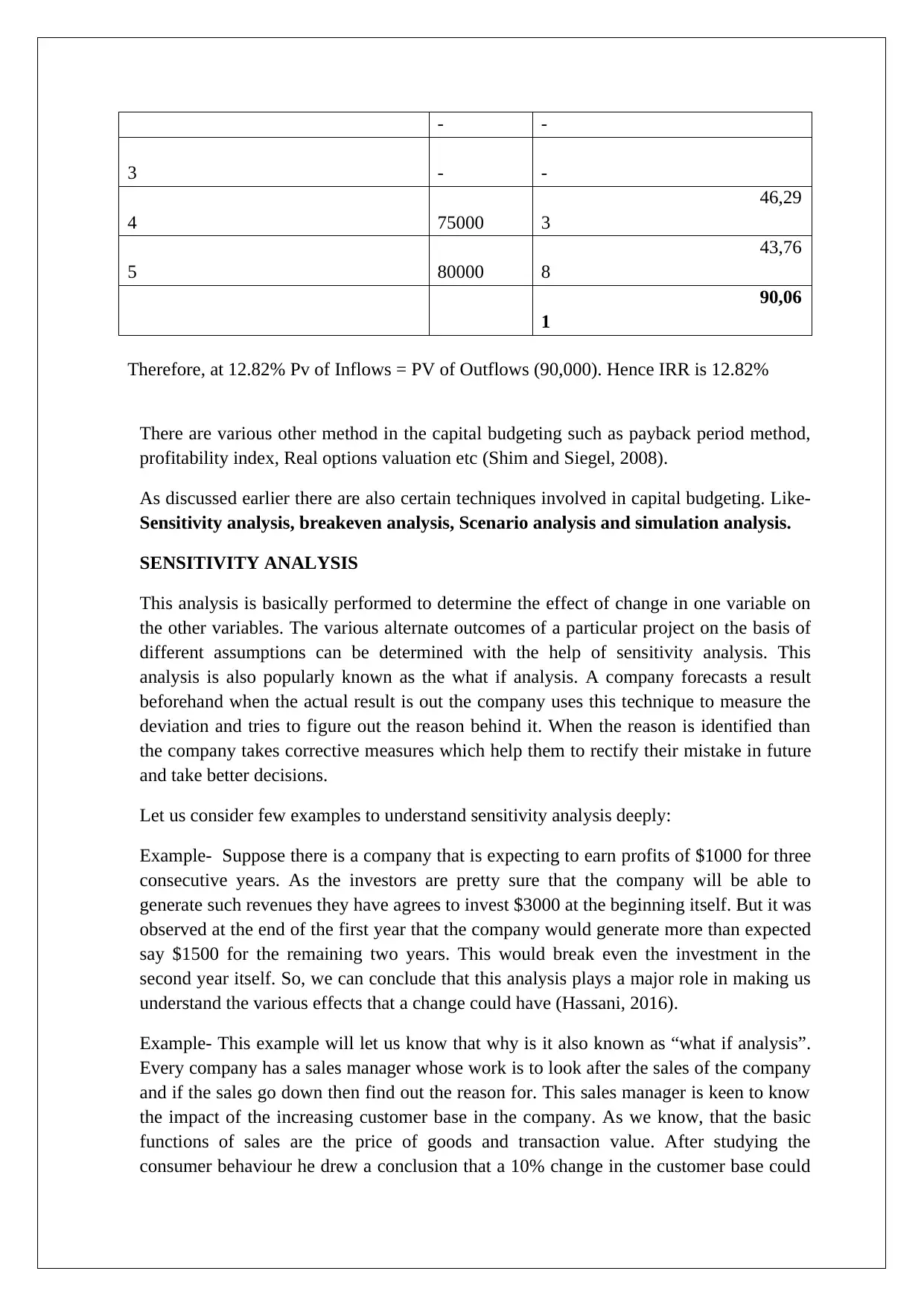

Therefore, at 13.78% Pv of Inflows = PV of Outflows (90,000). Hence IRR is 13.78%

For Project B:

For Calculation of IRR,

Inflow=Outflow

Let be IRR 12.82% then

PV of Inflows

Year Cash Flow Present Value of Cash Flows

1 - -

2

0 -90000 -90000

1 - -

2 - -

3 - -

4 75000 47,664

5 80000 45,394

NPV 3,058

2. IRR- The attractiveness of the project is determined using the IRR method. IRR

stands for internal rate of return. IRR can be defined as the rate of interest earned

when the NPV of the future cash flows is equal to zero. An investor while investing

has a required rate of return in his mind (Galbraith, Downey and Kates, 2002).

However, if the required rate of return is more than the actual IRR that has been

calculated then the investor may not invest there. In this case when the required rate

of return is less when compared to the IRR then the investor will surely invest as he is

getting more than his requirements.

Example of IRR-

For Project A:

For Calculation of IRR, Inflow=Outflow

Let be IRR 13.78% then

PV of Inflows

Year Cash Flow Present Value of Cash Flows

1 25000 21,972

2 24000 18,539

3 26000 17,651

4 27000 16,110

5 30000 15,732

90,005

Therefore, at 13.78% Pv of Inflows = PV of Outflows (90,000). Hence IRR is 13.78%

For Project B:

For Calculation of IRR,

Inflow=Outflow

Let be IRR 12.82% then

PV of Inflows

Year Cash Flow Present Value of Cash Flows

1 - -

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

- -

3 - -

4 75000

46,29

3

5 80000

43,76

8

90,06

1

Therefore, at 12.82% Pv of Inflows = PV of Outflows (90,000). Hence IRR is 12.82%

There are various other method in the capital budgeting such as payback period method,

profitability index, Real options valuation etc (Shim and Siegel, 2008).

As discussed earlier there are also certain techniques involved in capital budgeting. Like-

Sensitivity analysis, breakeven analysis, Scenario analysis and simulation analysis.

SENSITIVITY ANALYSIS

This analysis is basically performed to determine the effect of change in one variable on

the other variables. The various alternate outcomes of a particular project on the basis of

different assumptions can be determined with the help of sensitivity analysis. This

analysis is also popularly known as the what if analysis. A company forecasts a result

beforehand when the actual result is out the company uses this technique to measure the

deviation and tries to figure out the reason behind it. When the reason is identified than

the company takes corrective measures which help them to rectify their mistake in future

and take better decisions.

Let us consider few examples to understand sensitivity analysis deeply:

Example- Suppose there is a company that is expecting to earn profits of $1000 for three

consecutive years. As the investors are pretty sure that the company will be able to

generate such revenues they have agrees to invest $3000 at the beginning itself. But it was

observed at the end of the first year that the company would generate more than expected

say $1500 for the remaining two years. This would break even the investment in the

second year itself. So, we can conclude that this analysis plays a major role in making us

understand the various effects that a change could have (Hassani, 2016).

Example- This example will let us know that why is it also known as “what if analysis”.

Every company has a sales manager whose work is to look after the sales of the company

and if the sales go down then find out the reason for. This sales manager is keen to know

the impact of the increasing customer base in the company. As we know, that the basic

functions of sales are the price of goods and transaction value. After studying the

consumer behaviour he drew a conclusion that a 10% change in the customer base could

3 - -

4 75000

46,29

3

5 80000

43,76

8

90,06

1

Therefore, at 12.82% Pv of Inflows = PV of Outflows (90,000). Hence IRR is 12.82%

There are various other method in the capital budgeting such as payback period method,

profitability index, Real options valuation etc (Shim and Siegel, 2008).

As discussed earlier there are also certain techniques involved in capital budgeting. Like-

Sensitivity analysis, breakeven analysis, Scenario analysis and simulation analysis.

SENSITIVITY ANALYSIS

This analysis is basically performed to determine the effect of change in one variable on

the other variables. The various alternate outcomes of a particular project on the basis of

different assumptions can be determined with the help of sensitivity analysis. This

analysis is also popularly known as the what if analysis. A company forecasts a result

beforehand when the actual result is out the company uses this technique to measure the

deviation and tries to figure out the reason behind it. When the reason is identified than

the company takes corrective measures which help them to rectify their mistake in future

and take better decisions.

Let us consider few examples to understand sensitivity analysis deeply:

Example- Suppose there is a company that is expecting to earn profits of $1000 for three

consecutive years. As the investors are pretty sure that the company will be able to

generate such revenues they have agrees to invest $3000 at the beginning itself. But it was

observed at the end of the first year that the company would generate more than expected

say $1500 for the remaining two years. This would break even the investment in the

second year itself. So, we can conclude that this analysis plays a major role in making us

understand the various effects that a change could have (Hassani, 2016).

Example- This example will let us know that why is it also known as “what if analysis”.

Every company has a sales manager whose work is to look after the sales of the company

and if the sales go down then find out the reason for. This sales manager is keen to know

the impact of the increasing customer base in the company. As we know, that the basic

functions of sales are the price of goods and transaction value. After studying the

consumer behaviour he drew a conclusion that a 10% change in the customer base could

increase the revenues of the company by 5%. So this question “what if the customer base

increases by 10% ? is resolved using this approach (Holland and Torregrosa, 2008).

SCENARIO ANALYSIS

It is a very known fact that we cannot predict the happenings keeping in mind the

dynamic and uncertain nature of the markets today. The analyst should always consider

this analysis as analytical tool. The analyst usually uses the words best case, base case

and worst case in order to explain the outcomes. It is well understood by the words itself

that the best case is the one in which all the things go in the way in which the analyst

thought it to be whereas the worst case is just the opposite of the best case. Anything that

has the highest probability is considered as the base case. It is the task of the analyst to

identify the risk and also prevent the worst case scenario. However, it is a fact that the

analysis cannot provide the exact situation but it provides a rough idea so that further

steps can be taken with utmost care (Khan and Jain, 2014).

We know that estimations are never accurate they always differ from the actual data. But

the analyst tries his best that his estimation falls close to the actual data. However, if there

are any confusions or uncertainties then the sensitivity analysis is not enough, it has to be

extended to scenario analysis (Saunders and Cornett, 2017). While performing scenario

analysis the analyst may use the sensitivity analysis also but there never arises situation

when an analyst requires scenario analysis information while carrying out sensitivity

analysis. Scenario analysis is basically done to analyse the uncertainties that may arise

and the impact of this uncertainty on a particular project. Scenario analysis and sensitivity

analysis goes hand in hand and are considered very vital part of the capital budgeting

process. These tools not only gives advise for the best investment plan but also saves

them from the dynamic nature and the risk involved in the market (Palepu, Healy and

Peek, 2016).

BREAKEVEN ANALYSIS

A company has to incur cost in order to manufacture and sell the product in the market.

Cost is included in the manufacturing process and even in the selling and distribution

process. These costs may be variable and fixed in nature. A company is said to earn

profits only when it has recovered the entire cost from customers. The level at which the

company only recovers the cost and does not have any profit or loss is known as the

breakeven point (Phillips, 2014). We can also say that the net income of the company will

be equal to zero in such a situation. There are two different formulas of breakeven point,

one helps to know about the breakeven point in units whereas the other gives the

breakeven point in term of volume of sale. A lower breakeven point is considered

beneficial for the company.

According to the accounting breakeven point, total cost will be equal to the total revenue

and net income will be equal to zero. The two formulas of breakeven point are shown

below (Reilly and Brown, 2012):

increases by 10% ? is resolved using this approach (Holland and Torregrosa, 2008).

SCENARIO ANALYSIS

It is a very known fact that we cannot predict the happenings keeping in mind the

dynamic and uncertain nature of the markets today. The analyst should always consider

this analysis as analytical tool. The analyst usually uses the words best case, base case

and worst case in order to explain the outcomes. It is well understood by the words itself

that the best case is the one in which all the things go in the way in which the analyst

thought it to be whereas the worst case is just the opposite of the best case. Anything that

has the highest probability is considered as the base case. It is the task of the analyst to

identify the risk and also prevent the worst case scenario. However, it is a fact that the

analysis cannot provide the exact situation but it provides a rough idea so that further

steps can be taken with utmost care (Khan and Jain, 2014).

We know that estimations are never accurate they always differ from the actual data. But

the analyst tries his best that his estimation falls close to the actual data. However, if there

are any confusions or uncertainties then the sensitivity analysis is not enough, it has to be

extended to scenario analysis (Saunders and Cornett, 2017). While performing scenario

analysis the analyst may use the sensitivity analysis also but there never arises situation

when an analyst requires scenario analysis information while carrying out sensitivity

analysis. Scenario analysis is basically done to analyse the uncertainties that may arise

and the impact of this uncertainty on a particular project. Scenario analysis and sensitivity

analysis goes hand in hand and are considered very vital part of the capital budgeting

process. These tools not only gives advise for the best investment plan but also saves

them from the dynamic nature and the risk involved in the market (Palepu, Healy and

Peek, 2016).

BREAKEVEN ANALYSIS

A company has to incur cost in order to manufacture and sell the product in the market.

Cost is included in the manufacturing process and even in the selling and distribution

process. These costs may be variable and fixed in nature. A company is said to earn

profits only when it has recovered the entire cost from customers. The level at which the

company only recovers the cost and does not have any profit or loss is known as the

breakeven point (Phillips, 2014). We can also say that the net income of the company will

be equal to zero in such a situation. There are two different formulas of breakeven point,

one helps to know about the breakeven point in units whereas the other gives the

breakeven point in term of volume of sale. A lower breakeven point is considered

beneficial for the company.

According to the accounting breakeven point, total cost will be equal to the total revenue

and net income will be equal to zero. The two formulas of breakeven point are shown

below (Reilly and Brown, 2012):

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Breakeven point (in units)= Fixed cost/ contribution per unit

Breakeven point (sales volume) = Fixed cost / Contribution margin

However, if the amount of depreciation is excluded from the fixed cost then we get the

cash breakeven point for the company.

In case of the financial breakeven analysis, the initial payment made towards the

investment is always equal to the future cash inflows and therefore, the NPV is zero,

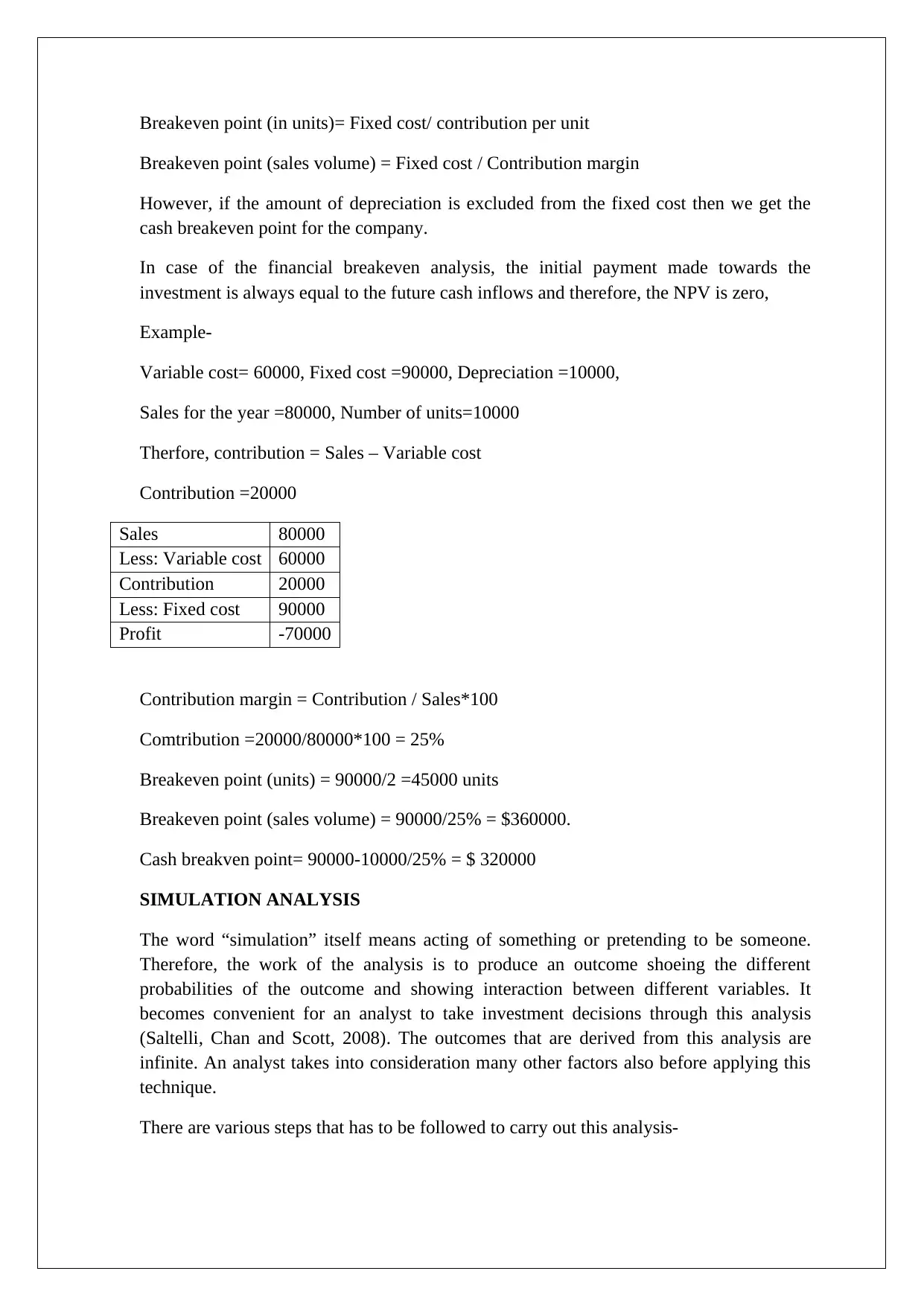

Example-

Variable cost= 60000, Fixed cost =90000, Depreciation =10000,

Sales for the year =80000, Number of units=10000

Therfore, contribution = Sales – Variable cost

Contribution =20000

Sales 80000

Less: Variable cost 60000

Contribution 20000

Less: Fixed cost 90000

Profit -70000

Contribution margin = Contribution / Sales*100

Comtribution =20000/80000*100 = 25%

Breakeven point (units) = 90000/2 =45000 units

Breakeven point (sales volume) = 90000/25% = $360000.

Cash breakven point= 90000-10000/25% = $ 320000

SIMULATION ANALYSIS

The word “simulation” itself means acting of something or pretending to be someone.

Therefore, the work of the analysis is to produce an outcome shoeing the different

probabilities of the outcome and showing interaction between different variables. It

becomes convenient for an analyst to take investment decisions through this analysis

(Saltelli, Chan and Scott, 2008). The outcomes that are derived from this analysis are

infinite. An analyst takes into consideration many other factors also before applying this

technique.

There are various steps that has to be followed to carry out this analysis-

Breakeven point (sales volume) = Fixed cost / Contribution margin

However, if the amount of depreciation is excluded from the fixed cost then we get the

cash breakeven point for the company.

In case of the financial breakeven analysis, the initial payment made towards the

investment is always equal to the future cash inflows and therefore, the NPV is zero,

Example-

Variable cost= 60000, Fixed cost =90000, Depreciation =10000,

Sales for the year =80000, Number of units=10000

Therfore, contribution = Sales – Variable cost

Contribution =20000

Sales 80000

Less: Variable cost 60000

Contribution 20000

Less: Fixed cost 90000

Profit -70000

Contribution margin = Contribution / Sales*100

Comtribution =20000/80000*100 = 25%

Breakeven point (units) = 90000/2 =45000 units

Breakeven point (sales volume) = 90000/25% = $360000.

Cash breakven point= 90000-10000/25% = $ 320000

SIMULATION ANALYSIS

The word “simulation” itself means acting of something or pretending to be someone.

Therefore, the work of the analysis is to produce an outcome shoeing the different

probabilities of the outcome and showing interaction between different variables. It

becomes convenient for an analyst to take investment decisions through this analysis

(Saltelli, Chan and Scott, 2008). The outcomes that are derived from this analysis are

infinite. An analyst takes into consideration many other factors also before applying this

technique.

There are various steps that has to be followed to carry out this analysis-

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1. The first step is to analyse the relationship between the present value and the

parameters. As we know parameters are constant they act as a benchmark.

2. The probabilities are then assigned to the random variables depending on the

parameters.

3. Select any one variable randomly to which the probability has already been assigned.

4. Then the NPV should be calculated for the given set of variables.

5. Then NPV is calculated for the required outcomes. However, it is noticed that there is

not a particular outcome nut there are several outcomes.

All these four techniques are considered the most important part of the capital

budgeting process.

parameters. As we know parameters are constant they act as a benchmark.

2. The probabilities are then assigned to the random variables depending on the

parameters.

3. Select any one variable randomly to which the probability has already been assigned.

4. Then the NPV should be calculated for the given set of variables.

5. Then NPV is calculated for the required outcomes. However, it is noticed that there is

not a particular outcome nut there are several outcomes.

All these four techniques are considered the most important part of the capital

budgeting process.

REFERENCES:

Berman, K., Knight, J. and Case, J. (n.d.). Financial intelligence for HR professionals.

Bruner, R., Eades, K. and Schill, M. (2017). Case studies in finance. Dubuque, IA: McGraw-

Hill Education.

Clarke, R. and Clarke, R. (1990). Strategic financial management. Homewood, Ill.: R.D.

Irwin.

Fairhurst, D. (2015). Using Excel for Business Analysis A Guide to Financial Modelling

Fundamenta. John Wiley & Sons.

Galbraith, J., Downey, D. and Kates, A. (2002). Designing dynamic organizations. New

York: AMACOM.

Hassani, B. (2016). Scenario analysis in risk management. Cham: Springer International

Publishing.

Holland, J. and Torregrosa, D. (2008). Capital budgeting. [Washington, D.C.]: Congress of

the U.S., Congressional Budget Office.

Khan, M. and Jain, P. (2014). Financial management. New Delhi: McGraw Hill Education.

Palepu, K., Healy, P. and Peek, E. (2016). Business analysis and valuation. Andover,

Hampshire, United Kingdom: Cengage Learning EMEA.

Phillips, J. (2014). Capm / pmp. New York: McGraw Hill.

Reilly, F. and Brown, K. (2012). Investment analysis & portfolio management. Mason, OH:

South-Western Cengage Learning.

Saltelli, A., Chan, K. and Scott, E. (2008). Sensitivity analysis. Chichester: John Wiley &

Sons, Ltd.

Saunders, A. and Cornett, M. (2017). Financial institutions management. New York:

McGraw-Hill Education.

Shim, J. and Siegel, J. (2008). Financial management. Hauppauge, N.Y.: Barron's

Educational Series.

Taylor, S. (2008). Modelling financial time series. New Jersey: World Scientific.

TULSIAN, B. (2016). TULSIAN'S FINANCIAL MANAGEMENT FOR CA-IPC (GROUP-I).

[S.l.]: S CHAND & CO LTD.

Berman, K., Knight, J. and Case, J. (n.d.). Financial intelligence for HR professionals.

Bruner, R., Eades, K. and Schill, M. (2017). Case studies in finance. Dubuque, IA: McGraw-

Hill Education.

Clarke, R. and Clarke, R. (1990). Strategic financial management. Homewood, Ill.: R.D.

Irwin.

Fairhurst, D. (2015). Using Excel for Business Analysis A Guide to Financial Modelling

Fundamenta. John Wiley & Sons.

Galbraith, J., Downey, D. and Kates, A. (2002). Designing dynamic organizations. New

York: AMACOM.

Hassani, B. (2016). Scenario analysis in risk management. Cham: Springer International

Publishing.

Holland, J. and Torregrosa, D. (2008). Capital budgeting. [Washington, D.C.]: Congress of

the U.S., Congressional Budget Office.

Khan, M. and Jain, P. (2014). Financial management. New Delhi: McGraw Hill Education.

Palepu, K., Healy, P. and Peek, E. (2016). Business analysis and valuation. Andover,

Hampshire, United Kingdom: Cengage Learning EMEA.

Phillips, J. (2014). Capm / pmp. New York: McGraw Hill.

Reilly, F. and Brown, K. (2012). Investment analysis & portfolio management. Mason, OH:

South-Western Cengage Learning.

Saltelli, A., Chan, K. and Scott, E. (2008). Sensitivity analysis. Chichester: John Wiley &

Sons, Ltd.

Saunders, A. and Cornett, M. (2017). Financial institutions management. New York:

McGraw-Hill Education.

Shim, J. and Siegel, J. (2008). Financial management. Hauppauge, N.Y.: Barron's

Educational Series.

Taylor, S. (2008). Modelling financial time series. New Jersey: World Scientific.

TULSIAN, B. (2016). TULSIAN'S FINANCIAL MANAGEMENT FOR CA-IPC (GROUP-I).

[S.l.]: S CHAND & CO LTD.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.