Capella University BUS-FP3062: Capital Budgeting Techniques Report

VerifiedAdded on 2022/08/22

|7

|1116

|19

Homework Assignment

AI Summary

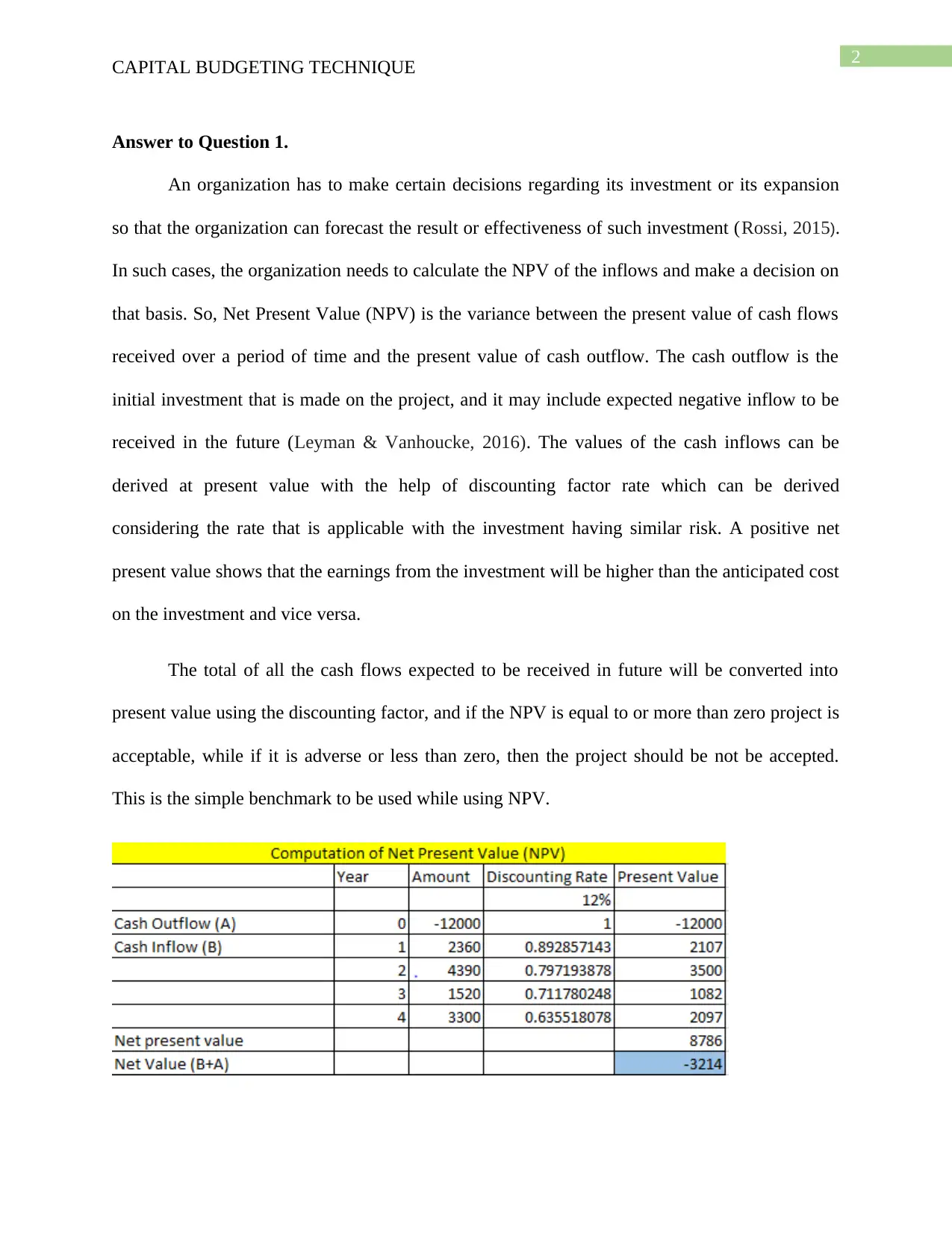

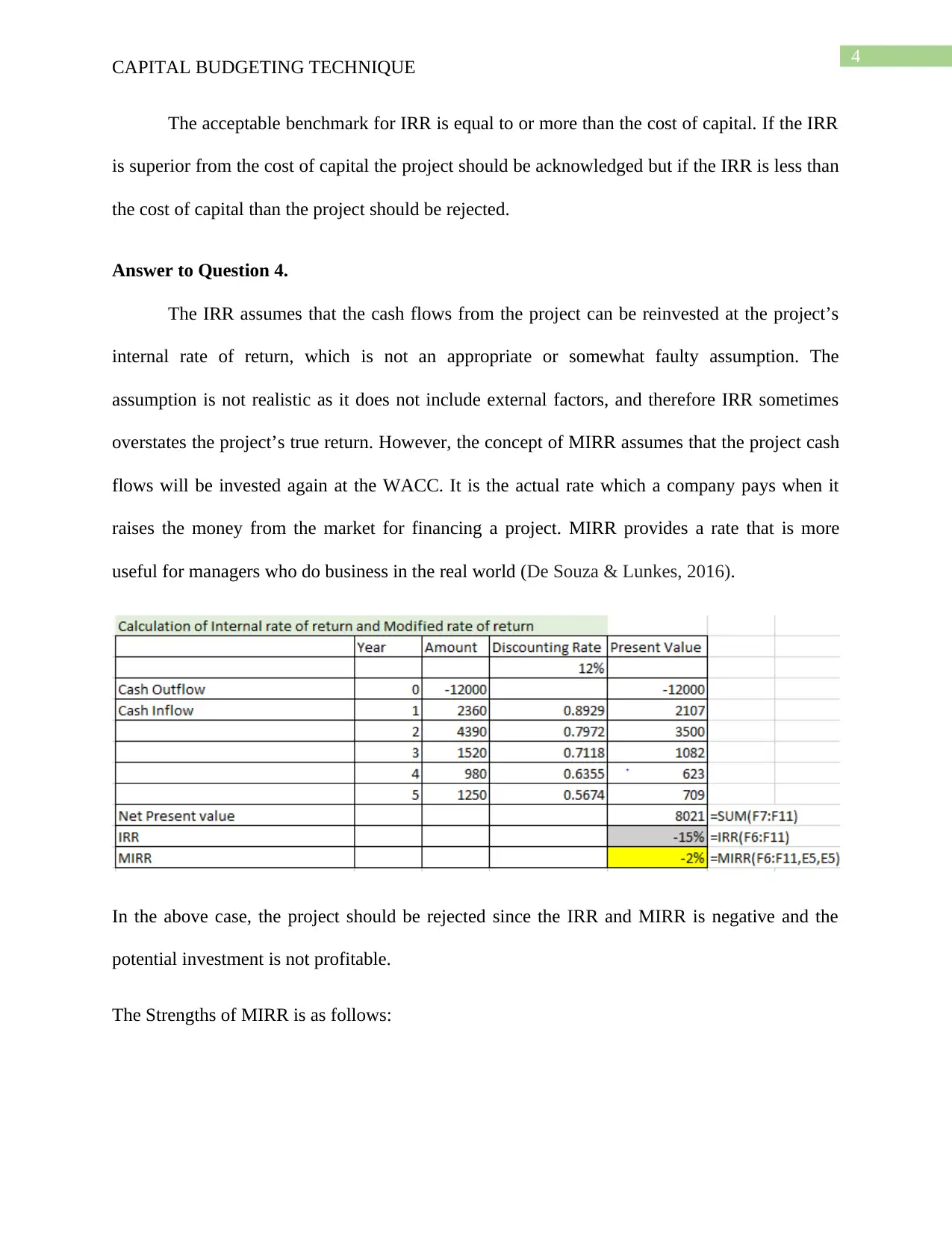

This document provides a comprehensive analysis of capital budgeting techniques, addressing key concepts such as Net Present Value (NPV), Internal Rate of Return (IRR), Modified Internal Rate of Return (MIRR), payback period, and discounted payback period. The assignment explores how organizations evaluate investments and make decisions regarding projects, including the expansion of facilities and the purchase of new equipment. The analysis includes detailed explanations of each technique, its application, and its limitations, providing a solid understanding of financial decision-making processes. Furthermore, the document highlights the importance of considering the time value of money and the impact of external factors on investment returns, emphasizing the practical application of these techniques in real-world scenarios. The document also includes a comparison of IRR and MIRR, highlighting the strengths and weaknesses of each approach and their implications for accurate project evaluation. This assignment is contributed by a student to be published on the website Desklib. Desklib is a platform which provides all the necessary AI based study tools for students.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.