Financial Analysis: Capital Budgeting and Cost of Capital for GOGreen

VerifiedAdded on 2022/10/15

|11

|2768

|98

Report

AI Summary

This report presents a detailed financial analysis focused on capital budgeting and the cost of capital. The first part of the report involves a capital budgeting analysis, where the after-tax cash flows, payback period, Net Present Value (NPV), and Profitability Index (PI) are calculated to evaluate the financial viability of an equipment upgrade proposal for GOGreen Motors. The analysis includes sensitivity analysis considering a change in variable costs. The second part of the report delves into the cost of capital for Grainwaves Ltd., determining the appropriate costs for debt, preference shares, and ordinary equity shares. The Weighted Average Cost of Capital (WACC) is then calculated, providing insights into the company's overall cost of financing. The report provides recommendations based on the financial analysis, supporting informed investment decisions.

Part A

Use of Capital Budgeting

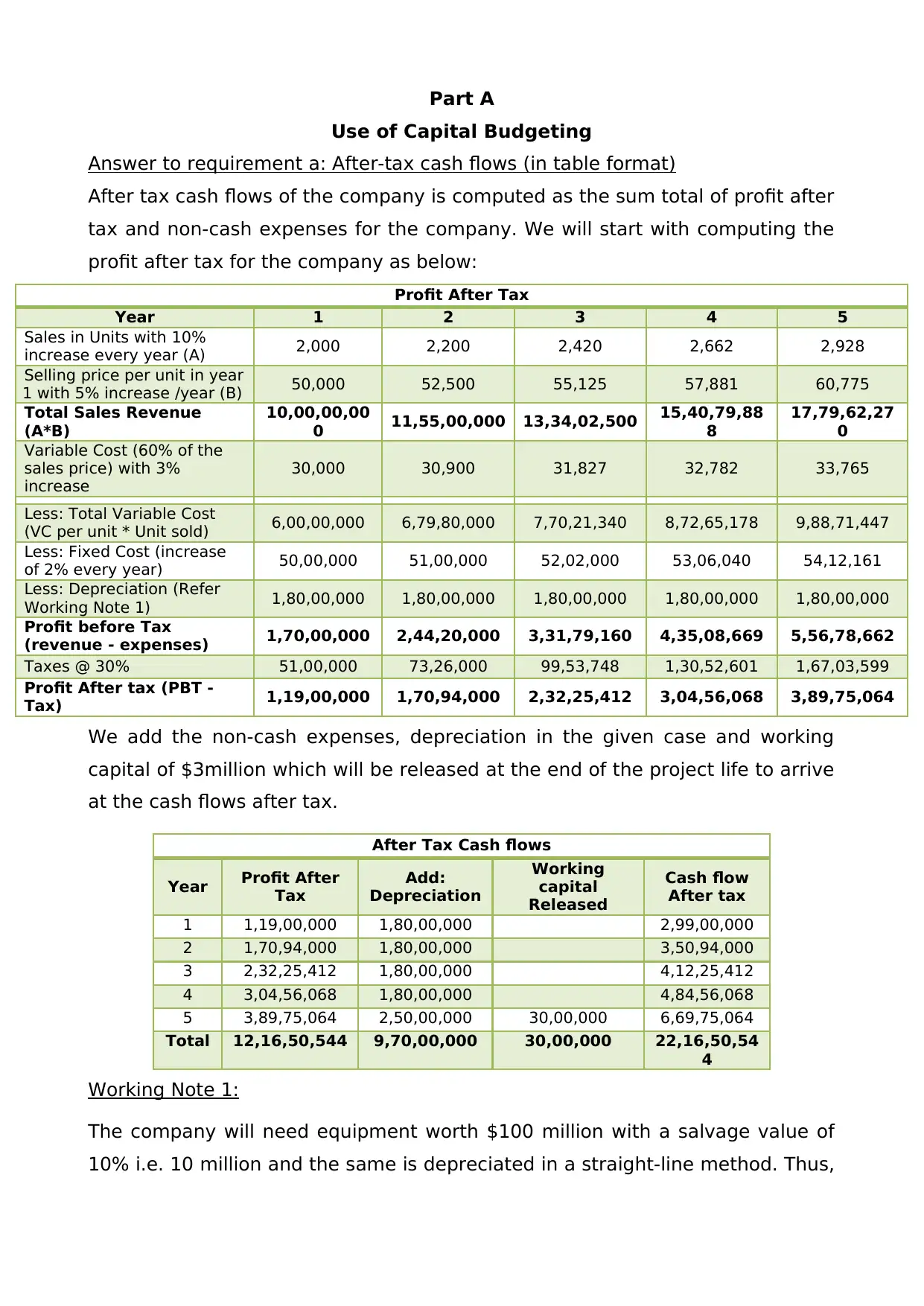

Answer to requirement a: After-tax cash flows (in table format)

After tax cash flows of the company is computed as the sum total of profit after

tax and non-cash expenses for the company. We will start with computing the

profit after tax for the company as below:

Profit After Tax

Year 1 2 3 4 5

Sales in Units with 10%

increase every year (A) 2,000 2,200 2,420 2,662 2,928

Selling price per unit in year

1 with 5% increase /year (B) 50,000 52,500 55,125 57,881 60,775

Total Sales Revenue

(A*B)

10,00,00,00

0 11,55,00,000 13,34,02,500 15,40,79,88

8

17,79,62,27

0

Variable Cost (60% of the

sales price) with 3%

increase

30,000 30,900 31,827 32,782 33,765

Less: Total Variable Cost

(VC per unit * Unit sold) 6,00,00,000 6,79,80,000 7,70,21,340 8,72,65,178 9,88,71,447

Less: Fixed Cost (increase

of 2% every year) 50,00,000 51,00,000 52,02,000 53,06,040 54,12,161

Less: Depreciation (Refer

Working Note 1) 1,80,00,000 1,80,00,000 1,80,00,000 1,80,00,000 1,80,00,000

Profit before Tax

(revenue - expenses) 1,70,00,000 2,44,20,000 3,31,79,160 4,35,08,669 5,56,78,662

Taxes @ 30% 51,00,000 73,26,000 99,53,748 1,30,52,601 1,67,03,599

Profit After tax (PBT -

Tax) 1,19,00,000 1,70,94,000 2,32,25,412 3,04,56,068 3,89,75,064

We add the non-cash expenses, depreciation in the given case and working

capital of $3million which will be released at the end of the project life to arrive

at the cash flows after tax.

After Tax Cash flows

Year Profit After

Tax

Add:

Depreciation

Working

capital

Released

Cash flow

After tax

1 1,19,00,000 1,80,00,000 2,99,00,000

2 1,70,94,000 1,80,00,000 3,50,94,000

3 2,32,25,412 1,80,00,000 4,12,25,412

4 3,04,56,068 1,80,00,000 4,84,56,068

5 3,89,75,064 2,50,00,000 30,00,000 6,69,75,064

Total 12,16,50,544 9,70,00,000 30,00,000 22,16,50,54

4

Working Note 1:

The company will need equipment worth $100 million with a salvage value of

10% i.e. 10 million and the same is depreciated in a straight-line method. Thus,

Use of Capital Budgeting

Answer to requirement a: After-tax cash flows (in table format)

After tax cash flows of the company is computed as the sum total of profit after

tax and non-cash expenses for the company. We will start with computing the

profit after tax for the company as below:

Profit After Tax

Year 1 2 3 4 5

Sales in Units with 10%

increase every year (A) 2,000 2,200 2,420 2,662 2,928

Selling price per unit in year

1 with 5% increase /year (B) 50,000 52,500 55,125 57,881 60,775

Total Sales Revenue

(A*B)

10,00,00,00

0 11,55,00,000 13,34,02,500 15,40,79,88

8

17,79,62,27

0

Variable Cost (60% of the

sales price) with 3%

increase

30,000 30,900 31,827 32,782 33,765

Less: Total Variable Cost

(VC per unit * Unit sold) 6,00,00,000 6,79,80,000 7,70,21,340 8,72,65,178 9,88,71,447

Less: Fixed Cost (increase

of 2% every year) 50,00,000 51,00,000 52,02,000 53,06,040 54,12,161

Less: Depreciation (Refer

Working Note 1) 1,80,00,000 1,80,00,000 1,80,00,000 1,80,00,000 1,80,00,000

Profit before Tax

(revenue - expenses) 1,70,00,000 2,44,20,000 3,31,79,160 4,35,08,669 5,56,78,662

Taxes @ 30% 51,00,000 73,26,000 99,53,748 1,30,52,601 1,67,03,599

Profit After tax (PBT -

Tax) 1,19,00,000 1,70,94,000 2,32,25,412 3,04,56,068 3,89,75,064

We add the non-cash expenses, depreciation in the given case and working

capital of $3million which will be released at the end of the project life to arrive

at the cash flows after tax.

After Tax Cash flows

Year Profit After

Tax

Add:

Depreciation

Working

capital

Released

Cash flow

After tax

1 1,19,00,000 1,80,00,000 2,99,00,000

2 1,70,94,000 1,80,00,000 3,50,94,000

3 2,32,25,412 1,80,00,000 4,12,25,412

4 3,04,56,068 1,80,00,000 4,84,56,068

5 3,89,75,064 2,50,00,000 30,00,000 6,69,75,064

Total 12,16,50,544 9,70,00,000 30,00,000 22,16,50,54

4

Working Note 1:

The company will need equipment worth $100 million with a salvage value of

10% i.e. 10 million and the same is depreciated in a straight-line method. Thus,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

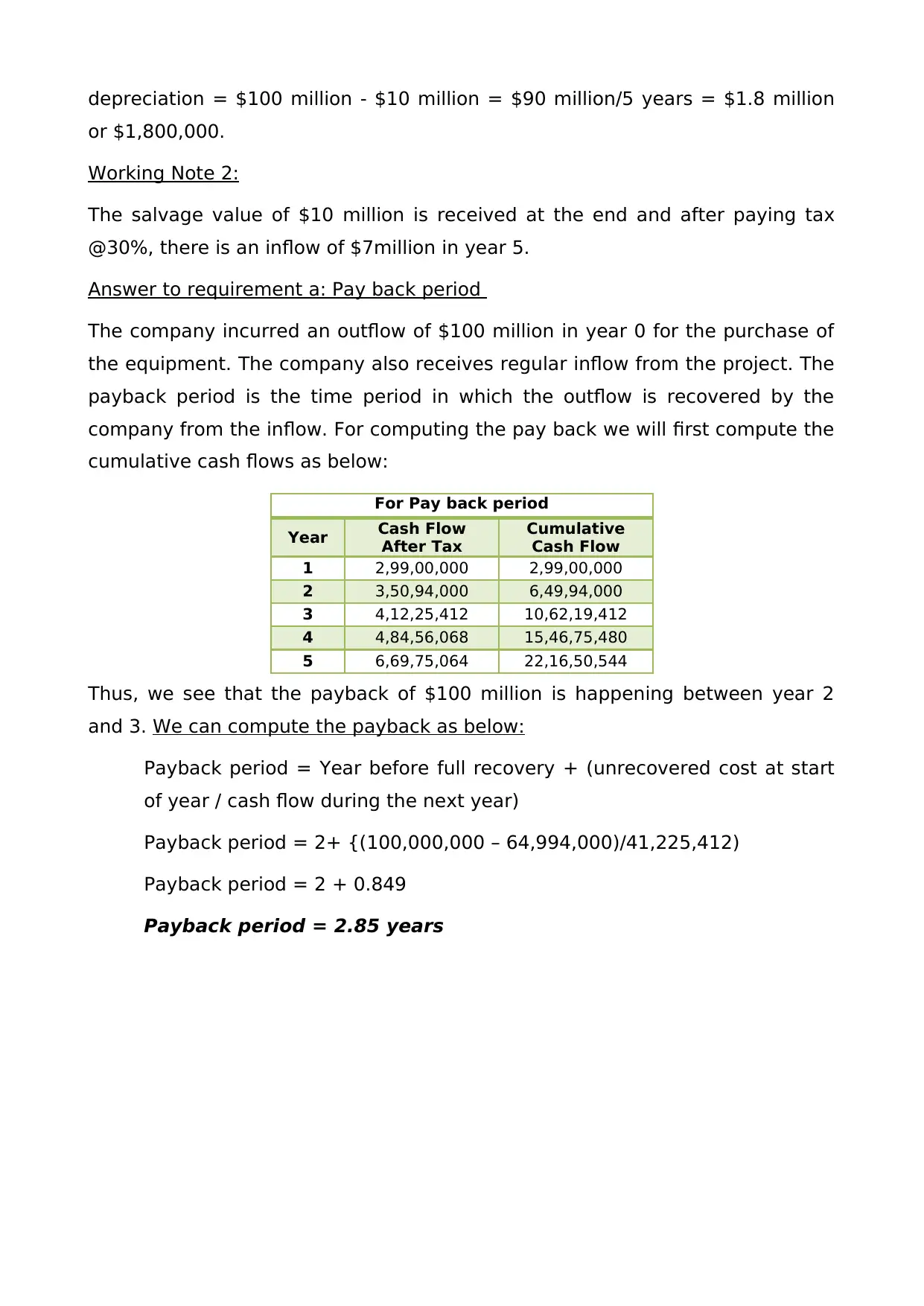

depreciation = $100 million - $10 million = $90 million/5 years = $1.8 million

or $1,800,000.

Working Note 2:

The salvage value of $10 million is received at the end and after paying tax

@30%, there is an inflow of $7million in year 5.

Answer to requirement a: Pay back period

The company incurred an outflow of $100 million in year 0 for the purchase of

the equipment. The company also receives regular inflow from the project. The

payback period is the time period in which the outflow is recovered by the

company from the inflow. For computing the pay back we will first compute the

cumulative cash flows as below:

For Pay back period

Year Cash Flow

After Tax

Cumulative

Cash Flow

1 2,99,00,000 2,99,00,000

2 3,50,94,000 6,49,94,000

3 4,12,25,412 10,62,19,412

4 4,84,56,068 15,46,75,480

5 6,69,75,064 22,16,50,544

Thus, we see that the payback of $100 million is happening between year 2

and 3. We can compute the payback as below:

Payback period = Year before full recovery + (unrecovered cost at start

of year / cash flow during the next year)

Payback period = 2+ {(100,000,000 – 64,994,000)/41,225,412)

Payback period = 2 + 0.849

Payback period = 2.85 years

or $1,800,000.

Working Note 2:

The salvage value of $10 million is received at the end and after paying tax

@30%, there is an inflow of $7million in year 5.

Answer to requirement a: Pay back period

The company incurred an outflow of $100 million in year 0 for the purchase of

the equipment. The company also receives regular inflow from the project. The

payback period is the time period in which the outflow is recovered by the

company from the inflow. For computing the pay back we will first compute the

cumulative cash flows as below:

For Pay back period

Year Cash Flow

After Tax

Cumulative

Cash Flow

1 2,99,00,000 2,99,00,000

2 3,50,94,000 6,49,94,000

3 4,12,25,412 10,62,19,412

4 4,84,56,068 15,46,75,480

5 6,69,75,064 22,16,50,544

Thus, we see that the payback of $100 million is happening between year 2

and 3. We can compute the payback as below:

Payback period = Year before full recovery + (unrecovered cost at start

of year / cash flow during the next year)

Payback period = 2+ {(100,000,000 – 64,994,000)/41,225,412)

Payback period = 2 + 0.849

Payback period = 2.85 years

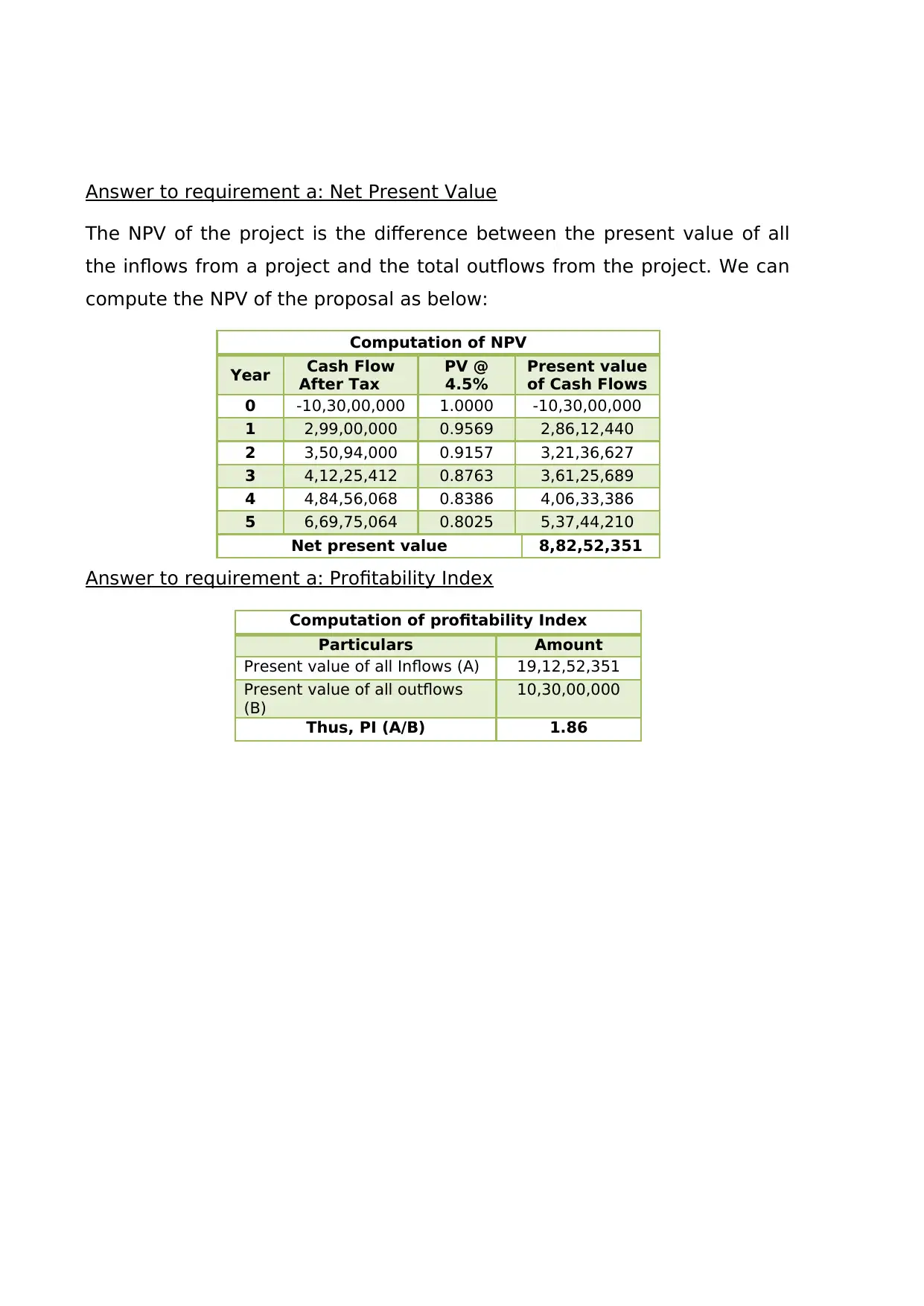

Answer to requirement a: Net Present Value

The NPV of the project is the difference between the present value of all

the inflows from a project and the total outflows from the project. We can

compute the NPV of the proposal as below:

Computation of NPV

Year Cash Flow

After Tax

PV @

4.5%

Present value

of Cash Flows

0 -10,30,00,000 1.0000 -10,30,00,000

1 2,99,00,000 0.9569 2,86,12,440

2 3,50,94,000 0.9157 3,21,36,627

3 4,12,25,412 0.8763 3,61,25,689

4 4,84,56,068 0.8386 4,06,33,386

5 6,69,75,064 0.8025 5,37,44,210

Net present value 8,82,52,351

Answer to requirement a: Profitability Index

Computation of profitability Index

Particulars Amount

Present value of all Inflows (A) 19,12,52,351

Present value of all outflows

(B)

10,30,00,000

Thus, PI (A/B) 1.86

The NPV of the project is the difference between the present value of all

the inflows from a project and the total outflows from the project. We can

compute the NPV of the proposal as below:

Computation of NPV

Year Cash Flow

After Tax

PV @

4.5%

Present value

of Cash Flows

0 -10,30,00,000 1.0000 -10,30,00,000

1 2,99,00,000 0.9569 2,86,12,440

2 3,50,94,000 0.9157 3,21,36,627

3 4,12,25,412 0.8763 3,61,25,689

4 4,84,56,068 0.8386 4,06,33,386

5 6,69,75,064 0.8025 5,37,44,210

Net present value 8,82,52,351

Answer to requirement a: Profitability Index

Computation of profitability Index

Particulars Amount

Present value of all Inflows (A) 19,12,52,351

Present value of all outflows

(B)

10,30,00,000

Thus, PI (A/B) 1.86

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

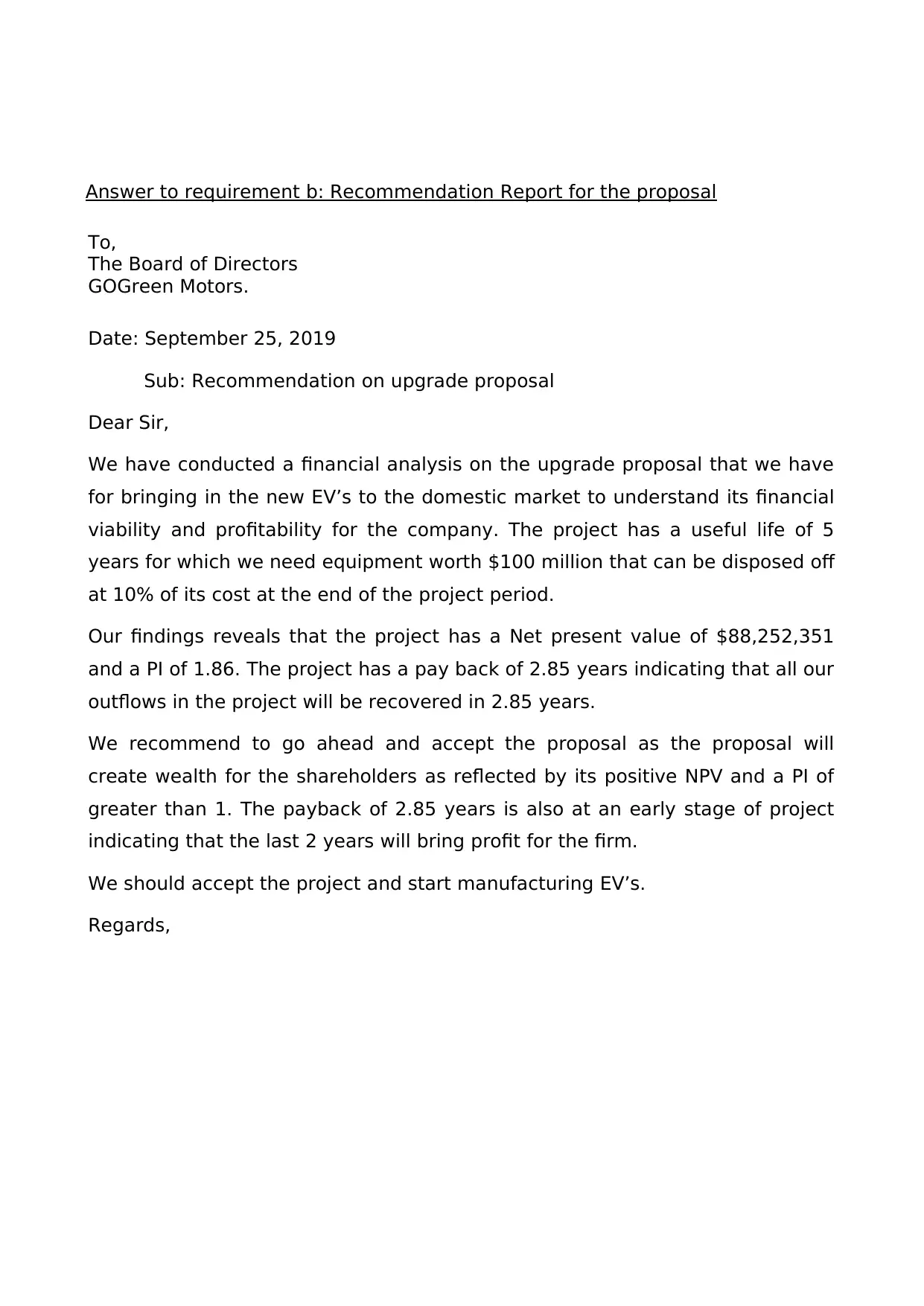

Answer to requirement b: Recommendation Report for the proposal

To,

The Board of Directors

GOGreen Motors.

Date: September 25, 2019

Sub: Recommendation on upgrade proposal

Dear Sir,

We have conducted a financial analysis on the upgrade proposal that we have

for bringing in the new EV’s to the domestic market to understand its financial

viability and profitability for the company. The project has a useful life of 5

years for which we need equipment worth $100 million that can be disposed off

at 10% of its cost at the end of the project period.

Our findings reveals that the project has a Net present value of $88,252,351

and a PI of 1.86. The project has a pay back of 2.85 years indicating that all our

outflows in the project will be recovered in 2.85 years.

We recommend to go ahead and accept the proposal as the proposal will

create wealth for the shareholders as reflected by its positive NPV and a PI of

greater than 1. The payback of 2.85 years is also at an early stage of project

indicating that the last 2 years will bring profit for the firm.

We should accept the project and start manufacturing EV’s.

Regards,

To,

The Board of Directors

GOGreen Motors.

Date: September 25, 2019

Sub: Recommendation on upgrade proposal

Dear Sir,

We have conducted a financial analysis on the upgrade proposal that we have

for bringing in the new EV’s to the domestic market to understand its financial

viability and profitability for the company. The project has a useful life of 5

years for which we need equipment worth $100 million that can be disposed off

at 10% of its cost at the end of the project period.

Our findings reveals that the project has a Net present value of $88,252,351

and a PI of 1.86. The project has a pay back of 2.85 years indicating that all our

outflows in the project will be recovered in 2.85 years.

We recommend to go ahead and accept the proposal as the proposal will

create wealth for the shareholders as reflected by its positive NPV and a PI of

greater than 1. The payback of 2.85 years is also at an early stage of project

indicating that the last 2 years will bring profit for the firm.

We should accept the project and start manufacturing EV’s.

Regards,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

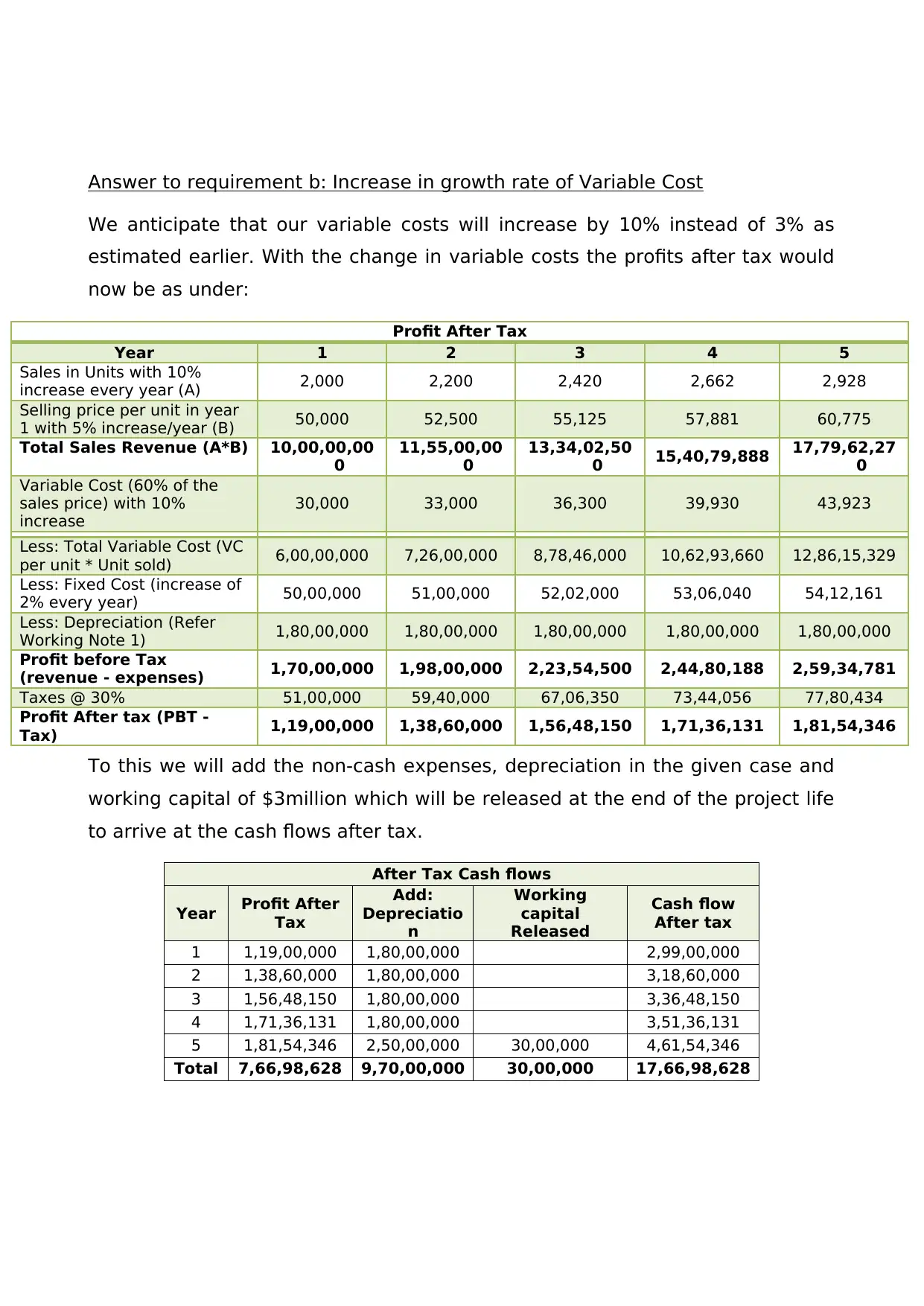

Answer to requirement b: Increase in growth rate of Variable Cost

We anticipate that our variable costs will increase by 10% instead of 3% as

estimated earlier. With the change in variable costs the profits after tax would

now be as under:

Profit After Tax

Year 1 2 3 4 5

Sales in Units with 10%

increase every year (A) 2,000 2,200 2,420 2,662 2,928

Selling price per unit in year

1 with 5% increase/year (B) 50,000 52,500 55,125 57,881 60,775

Total Sales Revenue (A*B) 10,00,00,00

0

11,55,00,00

0

13,34,02,50

0 15,40,79,888 17,79,62,27

0

Variable Cost (60% of the

sales price) with 10%

increase

30,000 33,000 36,300 39,930 43,923

Less: Total Variable Cost (VC

per unit * Unit sold) 6,00,00,000 7,26,00,000 8,78,46,000 10,62,93,660 12,86,15,329

Less: Fixed Cost (increase of

2% every year) 50,00,000 51,00,000 52,02,000 53,06,040 54,12,161

Less: Depreciation (Refer

Working Note 1) 1,80,00,000 1,80,00,000 1,80,00,000 1,80,00,000 1,80,00,000

Profit before Tax

(revenue - expenses) 1,70,00,000 1,98,00,000 2,23,54,500 2,44,80,188 2,59,34,781

Taxes @ 30% 51,00,000 59,40,000 67,06,350 73,44,056 77,80,434

Profit After tax (PBT -

Tax) 1,19,00,000 1,38,60,000 1,56,48,150 1,71,36,131 1,81,54,346

To this we will add the non-cash expenses, depreciation in the given case and

working capital of $3million which will be released at the end of the project life

to arrive at the cash flows after tax.

After Tax Cash flows

Year Profit After

Tax

Add:

Depreciatio

n

Working

capital

Released

Cash flow

After tax

1 1,19,00,000 1,80,00,000 2,99,00,000

2 1,38,60,000 1,80,00,000 3,18,60,000

3 1,56,48,150 1,80,00,000 3,36,48,150

4 1,71,36,131 1,80,00,000 3,51,36,131

5 1,81,54,346 2,50,00,000 30,00,000 4,61,54,346

Total 7,66,98,628 9,70,00,000 30,00,000 17,66,98,628

We anticipate that our variable costs will increase by 10% instead of 3% as

estimated earlier. With the change in variable costs the profits after tax would

now be as under:

Profit After Tax

Year 1 2 3 4 5

Sales in Units with 10%

increase every year (A) 2,000 2,200 2,420 2,662 2,928

Selling price per unit in year

1 with 5% increase/year (B) 50,000 52,500 55,125 57,881 60,775

Total Sales Revenue (A*B) 10,00,00,00

0

11,55,00,00

0

13,34,02,50

0 15,40,79,888 17,79,62,27

0

Variable Cost (60% of the

sales price) with 10%

increase

30,000 33,000 36,300 39,930 43,923

Less: Total Variable Cost (VC

per unit * Unit sold) 6,00,00,000 7,26,00,000 8,78,46,000 10,62,93,660 12,86,15,329

Less: Fixed Cost (increase of

2% every year) 50,00,000 51,00,000 52,02,000 53,06,040 54,12,161

Less: Depreciation (Refer

Working Note 1) 1,80,00,000 1,80,00,000 1,80,00,000 1,80,00,000 1,80,00,000

Profit before Tax

(revenue - expenses) 1,70,00,000 1,98,00,000 2,23,54,500 2,44,80,188 2,59,34,781

Taxes @ 30% 51,00,000 59,40,000 67,06,350 73,44,056 77,80,434

Profit After tax (PBT -

Tax) 1,19,00,000 1,38,60,000 1,56,48,150 1,71,36,131 1,81,54,346

To this we will add the non-cash expenses, depreciation in the given case and

working capital of $3million which will be released at the end of the project life

to arrive at the cash flows after tax.

After Tax Cash flows

Year Profit After

Tax

Add:

Depreciatio

n

Working

capital

Released

Cash flow

After tax

1 1,19,00,000 1,80,00,000 2,99,00,000

2 1,38,60,000 1,80,00,000 3,18,60,000

3 1,56,48,150 1,80,00,000 3,36,48,150

4 1,71,36,131 1,80,00,000 3,51,36,131

5 1,81,54,346 2,50,00,000 30,00,000 4,61,54,346

Total 7,66,98,628 9,70,00,000 30,00,000 17,66,98,628

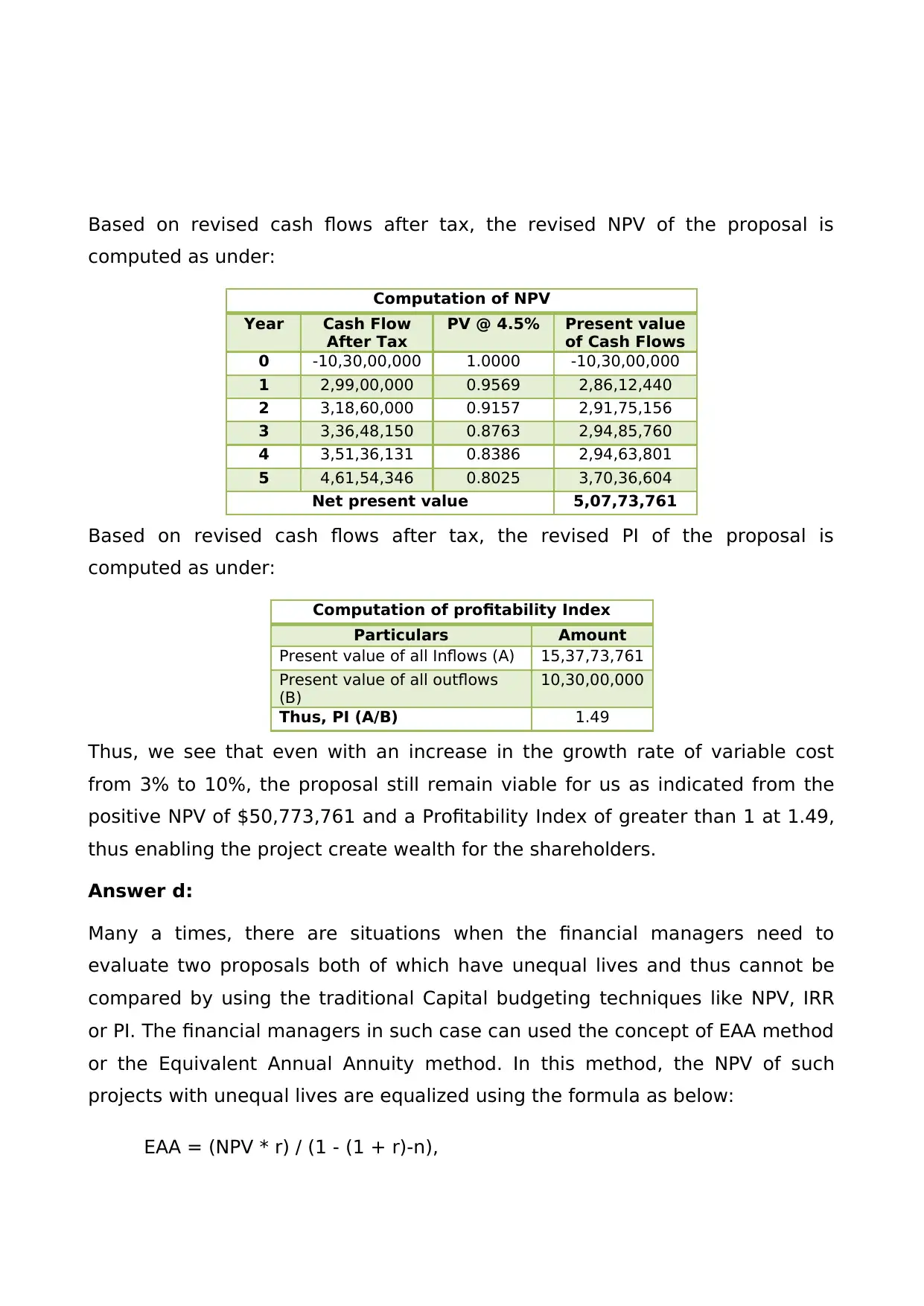

Based on revised cash flows after tax, the revised NPV of the proposal is

computed as under:

Computation of NPV

Year Cash Flow

After Tax

PV @ 4.5% Present value

of Cash Flows

0 -10,30,00,000 1.0000 -10,30,00,000

1 2,99,00,000 0.9569 2,86,12,440

2 3,18,60,000 0.9157 2,91,75,156

3 3,36,48,150 0.8763 2,94,85,760

4 3,51,36,131 0.8386 2,94,63,801

5 4,61,54,346 0.8025 3,70,36,604

Net present value 5,07,73,761

Based on revised cash flows after tax, the revised PI of the proposal is

computed as under:

Computation of profitability Index

Particulars Amount

Present value of all Inflows (A) 15,37,73,761

Present value of all outflows

(B)

10,30,00,000

Thus, PI (A/B) 1.49

Thus, we see that even with an increase in the growth rate of variable cost

from 3% to 10%, the proposal still remain viable for us as indicated from the

positive NPV of $50,773,761 and a Profitability Index of greater than 1 at 1.49,

thus enabling the project create wealth for the shareholders.

Answer d:

Many a times, there are situations when the financial managers need to

evaluate two proposals both of which have unequal lives and thus cannot be

compared by using the traditional Capital budgeting techniques like NPV, IRR

or PI. The financial managers in such case can used the concept of EAA method

or the Equivalent Annual Annuity method. In this method, the NPV of such

projects with unequal lives are equalized using the formula as below:

EAA = (NPV * r) / (1 - (1 + r)-n),

computed as under:

Computation of NPV

Year Cash Flow

After Tax

PV @ 4.5% Present value

of Cash Flows

0 -10,30,00,000 1.0000 -10,30,00,000

1 2,99,00,000 0.9569 2,86,12,440

2 3,18,60,000 0.9157 2,91,75,156

3 3,36,48,150 0.8763 2,94,85,760

4 3,51,36,131 0.8386 2,94,63,801

5 4,61,54,346 0.8025 3,70,36,604

Net present value 5,07,73,761

Based on revised cash flows after tax, the revised PI of the proposal is

computed as under:

Computation of profitability Index

Particulars Amount

Present value of all Inflows (A) 15,37,73,761

Present value of all outflows

(B)

10,30,00,000

Thus, PI (A/B) 1.49

Thus, we see that even with an increase in the growth rate of variable cost

from 3% to 10%, the proposal still remain viable for us as indicated from the

positive NPV of $50,773,761 and a Profitability Index of greater than 1 at 1.49,

thus enabling the project create wealth for the shareholders.

Answer d:

Many a times, there are situations when the financial managers need to

evaluate two proposals both of which have unequal lives and thus cannot be

compared by using the traditional Capital budgeting techniques like NPV, IRR

or PI. The financial managers in such case can used the concept of EAA method

or the Equivalent Annual Annuity method. In this method, the NPV of such

projects with unequal lives are equalized using the formula as below:

EAA = (NPV * r) / (1 - (1 + r)-n),

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

where r = required rate of return and n = project life. The managers should

select projects with higher EAA as that would create wealth for the

shareholders.

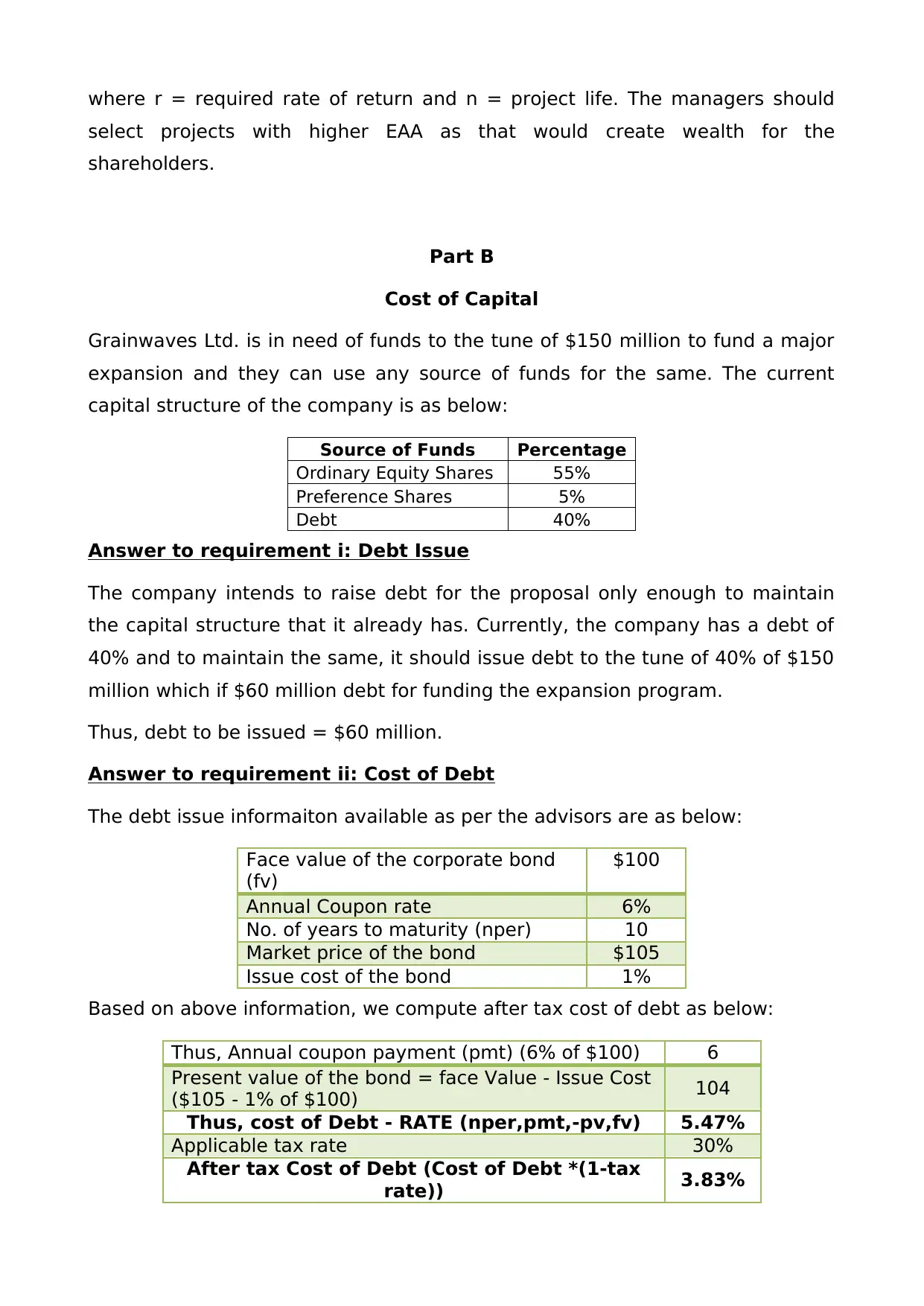

Part B

Cost of Capital

Grainwaves Ltd. is in need of funds to the tune of $150 million to fund a major

expansion and they can use any source of funds for the same. The current

capital structure of the company is as below:

Source of Funds Percentage

Ordinary Equity Shares 55%

Preference Shares 5%

Debt 40%

Answer to requirement i: Debt Issue

The company intends to raise debt for the proposal only enough to maintain

the capital structure that it already has. Currently, the company has a debt of

40% and to maintain the same, it should issue debt to the tune of 40% of $150

million which if $60 million debt for funding the expansion program.

Thus, debt to be issued = $60 million.

Answer to requirement ii: Cost of Debt

The debt issue informaiton available as per the advisors are as below:

Face value of the corporate bond

(fv)

$100

Annual Coupon rate 6%

No. of years to maturity (nper) 10

Market price of the bond $105

Issue cost of the bond 1%

Based on above information, we compute after tax cost of debt as below:

Thus, Annual coupon payment (pmt) (6% of $100) 6

Present value of the bond = face Value - Issue Cost

($105 - 1% of $100) 104

Thus, cost of Debt - RATE (nper,pmt,-pv,fv) 5.47%

Applicable tax rate 30%

After tax Cost of Debt (Cost of Debt *(1-tax

rate)) 3.83%

select projects with higher EAA as that would create wealth for the

shareholders.

Part B

Cost of Capital

Grainwaves Ltd. is in need of funds to the tune of $150 million to fund a major

expansion and they can use any source of funds for the same. The current

capital structure of the company is as below:

Source of Funds Percentage

Ordinary Equity Shares 55%

Preference Shares 5%

Debt 40%

Answer to requirement i: Debt Issue

The company intends to raise debt for the proposal only enough to maintain

the capital structure that it already has. Currently, the company has a debt of

40% and to maintain the same, it should issue debt to the tune of 40% of $150

million which if $60 million debt for funding the expansion program.

Thus, debt to be issued = $60 million.

Answer to requirement ii: Cost of Debt

The debt issue informaiton available as per the advisors are as below:

Face value of the corporate bond

(fv)

$100

Annual Coupon rate 6%

No. of years to maturity (nper) 10

Market price of the bond $105

Issue cost of the bond 1%

Based on above information, we compute after tax cost of debt as below:

Thus, Annual coupon payment (pmt) (6% of $100) 6

Present value of the bond = face Value - Issue Cost

($105 - 1% of $100) 104

Thus, cost of Debt - RATE (nper,pmt,-pv,fv) 5.47%

Applicable tax rate 30%

After tax Cost of Debt (Cost of Debt *(1-tax

rate)) 3.83%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

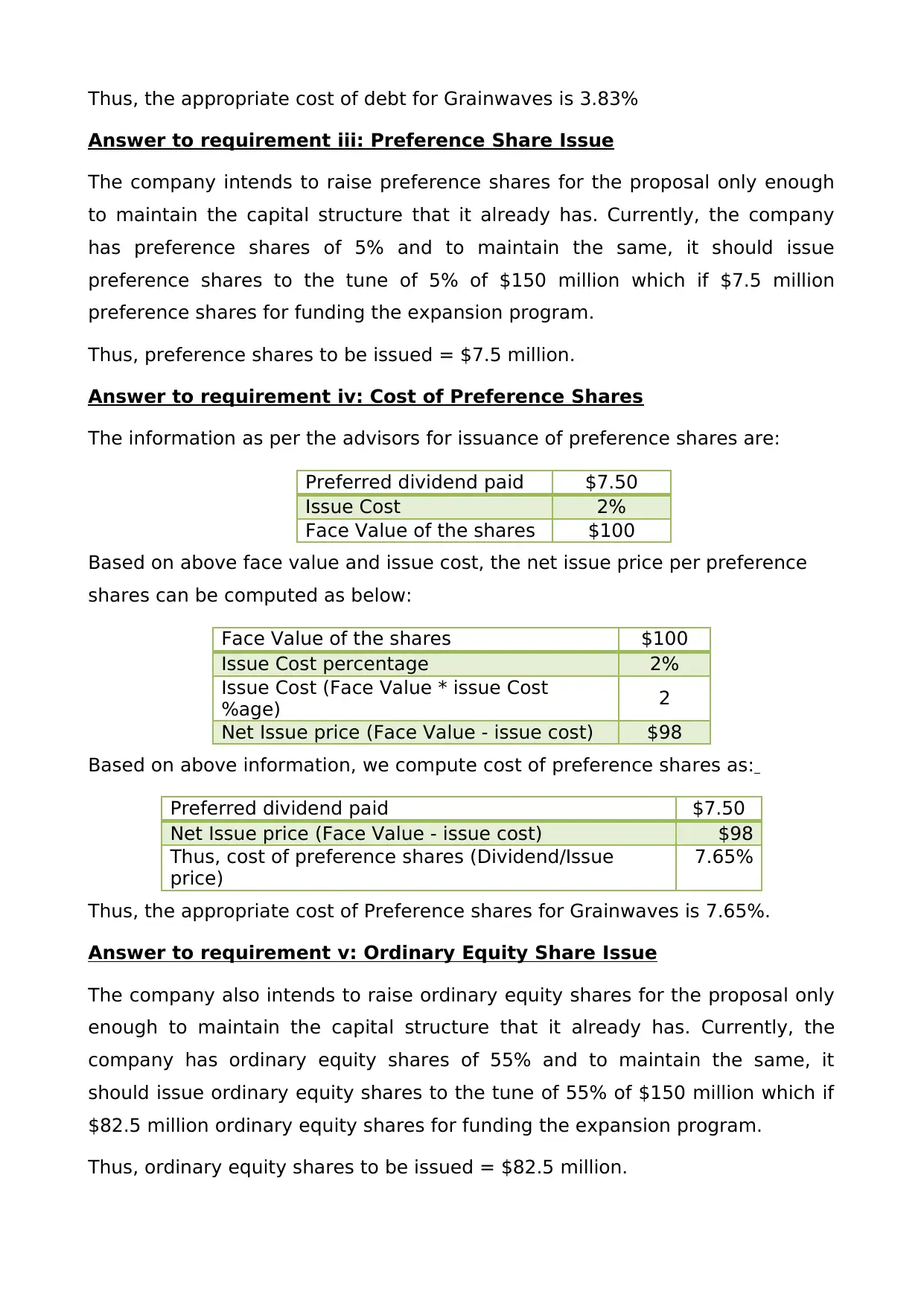

Thus, the appropriate cost of debt for Grainwaves is 3.83%

Answer to requirement iii: Preference Share Issue

The company intends to raise preference shares for the proposal only enough

to maintain the capital structure that it already has. Currently, the company

has preference shares of 5% and to maintain the same, it should issue

preference shares to the tune of 5% of $150 million which if $7.5 million

preference shares for funding the expansion program.

Thus, preference shares to be issued = $7.5 million.

Answer to requirement iv: Cost of Preference Shares

The information as per the advisors for issuance of preference shares are:

Preferred dividend paid $7.50

Issue Cost 2%

Face Value of the shares $100

Based on above face value and issue cost, the net issue price per preference

shares can be computed as below:

Face Value of the shares $100

Issue Cost percentage 2%

Issue Cost (Face Value * issue Cost

%age) 2

Net Issue price (Face Value - issue cost) $98

Based on above information, we compute cost of preference shares as:

Preferred dividend paid $7.50

Net Issue price (Face Value - issue cost) $98

Thus, cost of preference shares (Dividend/Issue

price)

7.65%

Thus, the appropriate cost of Preference shares for Grainwaves is 7.65%.

Answer to requirement v: Ordinary Equity Share Issue

The company also intends to raise ordinary equity shares for the proposal only

enough to maintain the capital structure that it already has. Currently, the

company has ordinary equity shares of 55% and to maintain the same, it

should issue ordinary equity shares to the tune of 55% of $150 million which if

$82.5 million ordinary equity shares for funding the expansion program.

Thus, ordinary equity shares to be issued = $82.5 million.

Answer to requirement iii: Preference Share Issue

The company intends to raise preference shares for the proposal only enough

to maintain the capital structure that it already has. Currently, the company

has preference shares of 5% and to maintain the same, it should issue

preference shares to the tune of 5% of $150 million which if $7.5 million

preference shares for funding the expansion program.

Thus, preference shares to be issued = $7.5 million.

Answer to requirement iv: Cost of Preference Shares

The information as per the advisors for issuance of preference shares are:

Preferred dividend paid $7.50

Issue Cost 2%

Face Value of the shares $100

Based on above face value and issue cost, the net issue price per preference

shares can be computed as below:

Face Value of the shares $100

Issue Cost percentage 2%

Issue Cost (Face Value * issue Cost

%age) 2

Net Issue price (Face Value - issue cost) $98

Based on above information, we compute cost of preference shares as:

Preferred dividend paid $7.50

Net Issue price (Face Value - issue cost) $98

Thus, cost of preference shares (Dividend/Issue

price)

7.65%

Thus, the appropriate cost of Preference shares for Grainwaves is 7.65%.

Answer to requirement v: Ordinary Equity Share Issue

The company also intends to raise ordinary equity shares for the proposal only

enough to maintain the capital structure that it already has. Currently, the

company has ordinary equity shares of 55% and to maintain the same, it

should issue ordinary equity shares to the tune of 55% of $150 million which if

$82.5 million ordinary equity shares for funding the expansion program.

Thus, ordinary equity shares to be issued = $82.5 million.

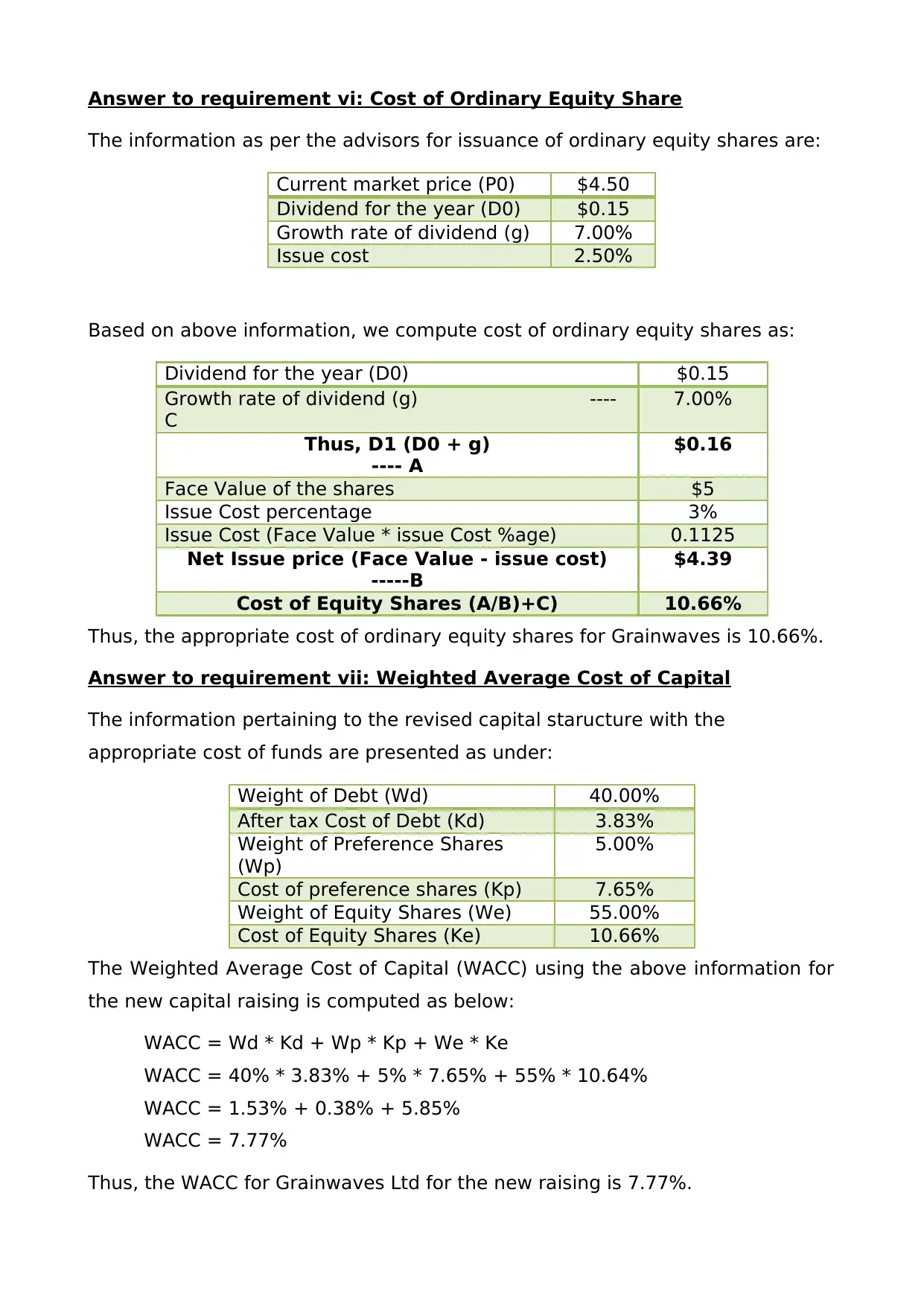

Answer to requirement vi: Cost of Ordinary Equity Share

The information as per the advisors for issuance of ordinary equity shares are:

Current market price (P0) $4.50

Dividend for the year (D0) $0.15

Growth rate of dividend (g) 7.00%

Issue cost 2.50%

Based on above information, we compute cost of ordinary equity shares as:

Dividend for the year (D0) $0.15

Growth rate of dividend (g) ----

C

7.00%

Thus, D1 (D0 + g)

---- A

$0.16

Face Value of the shares $5

Issue Cost percentage 3%

Issue Cost (Face Value * issue Cost %age) 0.1125

Net Issue price (Face Value - issue cost)

-----B

$4.39

Cost of Equity Shares (A/B)+C) 10.66%

Thus, the appropriate cost of ordinary equity shares for Grainwaves is 10.66%.

Answer to requirement vii: Weighted Average Cost of Capital

The information pertaining to the revised capital staructure with the

appropriate cost of funds are presented as under:

Weight of Debt (Wd) 40.00%

After tax Cost of Debt (Kd) 3.83%

Weight of Preference Shares

(Wp)

5.00%

Cost of preference shares (Kp) 7.65%

Weight of Equity Shares (We) 55.00%

Cost of Equity Shares (Ke) 10.66%

The Weighted Average Cost of Capital (WACC) using the above information for

the new capital raising is computed as below:

WACC = Wd * Kd + Wp * Kp + We * Ke

WACC = 40% * 3.83% + 5% * 7.65% + 55% * 10.64%

WACC = 1.53% + 0.38% + 5.85%

WACC = 7.77%

Thus, the WACC for Grainwaves Ltd for the new raising is 7.77%.

The information as per the advisors for issuance of ordinary equity shares are:

Current market price (P0) $4.50

Dividend for the year (D0) $0.15

Growth rate of dividend (g) 7.00%

Issue cost 2.50%

Based on above information, we compute cost of ordinary equity shares as:

Dividend for the year (D0) $0.15

Growth rate of dividend (g) ----

C

7.00%

Thus, D1 (D0 + g)

---- A

$0.16

Face Value of the shares $5

Issue Cost percentage 3%

Issue Cost (Face Value * issue Cost %age) 0.1125

Net Issue price (Face Value - issue cost)

-----B

$4.39

Cost of Equity Shares (A/B)+C) 10.66%

Thus, the appropriate cost of ordinary equity shares for Grainwaves is 10.66%.

Answer to requirement vii: Weighted Average Cost of Capital

The information pertaining to the revised capital staructure with the

appropriate cost of funds are presented as under:

Weight of Debt (Wd) 40.00%

After tax Cost of Debt (Kd) 3.83%

Weight of Preference Shares

(Wp)

5.00%

Cost of preference shares (Kp) 7.65%

Weight of Equity Shares (We) 55.00%

Cost of Equity Shares (Ke) 10.66%

The Weighted Average Cost of Capital (WACC) using the above information for

the new capital raising is computed as below:

WACC = Wd * Kd + Wp * Kp + We * Ke

WACC = 40% * 3.83% + 5% * 7.65% + 55% * 10.64%

WACC = 1.53% + 0.38% + 5.85%

WACC = 7.77%

Thus, the WACC for Grainwaves Ltd for the new raising is 7.77%.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

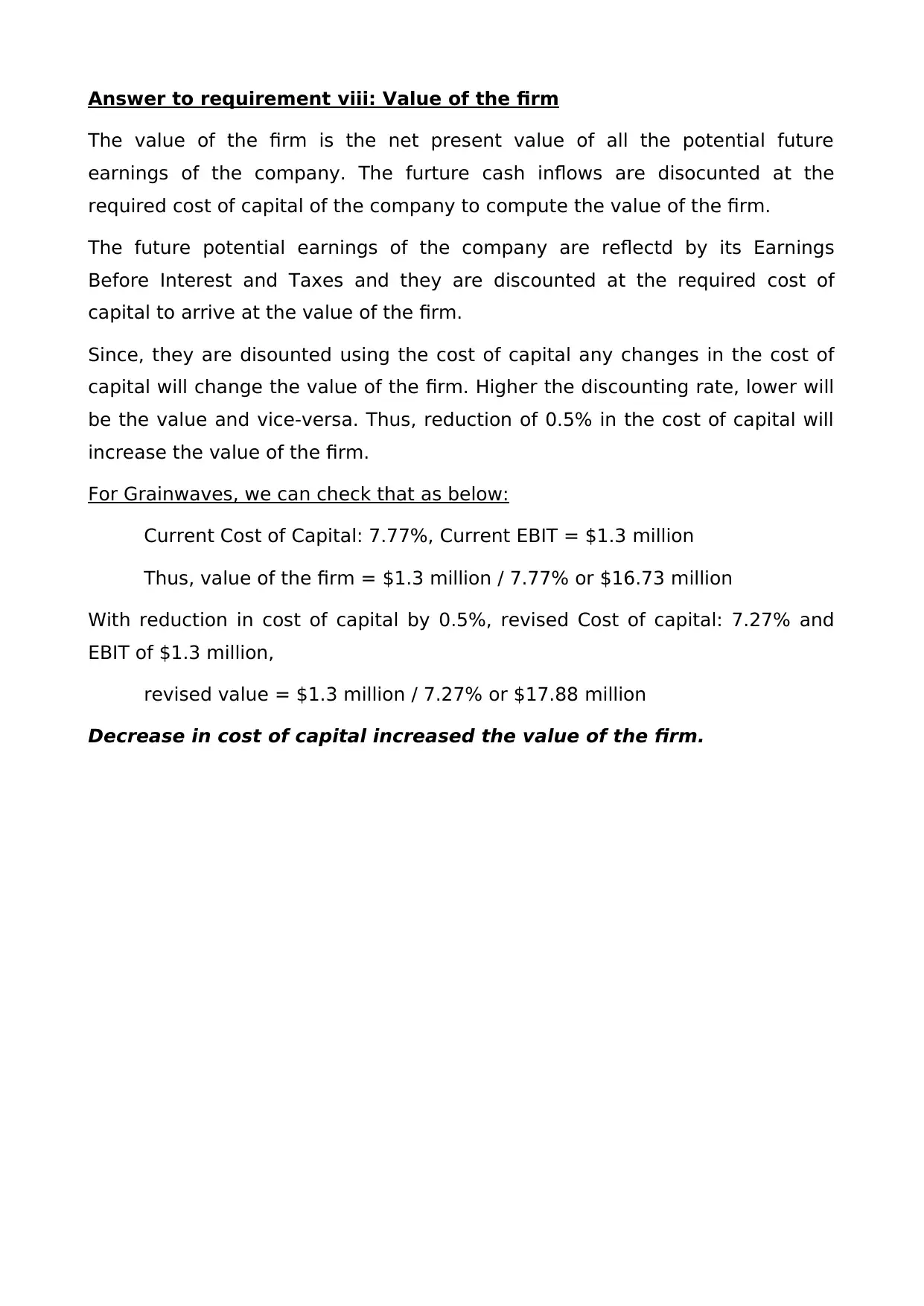

Answer to requirement viii: Value of the firm

The value of the firm is the net present value of all the potential future

earnings of the company. The furture cash inflows are disocunted at the

required cost of capital of the company to compute the value of the firm.

The future potential earnings of the company are reflectd by its Earnings

Before Interest and Taxes and they are discounted at the required cost of

capital to arrive at the value of the firm.

Since, they are disounted using the cost of capital any changes in the cost of

capital will change the value of the firm. Higher the discounting rate, lower will

be the value and vice-versa. Thus, reduction of 0.5% in the cost of capital will

increase the value of the firm.

For Grainwaves, we can check that as below:

Current Cost of Capital: 7.77%, Current EBIT = $1.3 million

Thus, value of the firm = $1.3 million / 7.77% or $16.73 million

With reduction in cost of capital by 0.5%, revised Cost of capital: 7.27% and

EBIT of $1.3 million,

revised value = $1.3 million / 7.27% or $17.88 million

Decrease in cost of capital increased the value of the firm.

The value of the firm is the net present value of all the potential future

earnings of the company. The furture cash inflows are disocunted at the

required cost of capital of the company to compute the value of the firm.

The future potential earnings of the company are reflectd by its Earnings

Before Interest and Taxes and they are discounted at the required cost of

capital to arrive at the value of the firm.

Since, they are disounted using the cost of capital any changes in the cost of

capital will change the value of the firm. Higher the discounting rate, lower will

be the value and vice-versa. Thus, reduction of 0.5% in the cost of capital will

increase the value of the firm.

For Grainwaves, we can check that as below:

Current Cost of Capital: 7.77%, Current EBIT = $1.3 million

Thus, value of the firm = $1.3 million / 7.77% or $16.73 million

With reduction in cost of capital by 0.5%, revised Cost of capital: 7.27% and

EBIT of $1.3 million,

revised value = $1.3 million / 7.27% or $17.88 million

Decrease in cost of capital increased the value of the firm.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

Atrill, P.(2009). Financial management for decision makers, 5th edn., England:

FT Prentice Hall.

Block, S. (2019). Foundations of financial management. New York: McGraw-Hill.

Atrill, P.(2009). Financial management for decision makers, 5th edn., England:

FT Prentice Hall.

Block, S. (2019). Foundations of financial management. New York: McGraw-Hill.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.