Taxation Law Assignment: Capital Gain Tax, Cost and Capital Allowance

VerifiedAdded on 2022/10/12

|11

|2959

|13

Homework Assignment

AI Summary

This assignment report focuses on the capital gain regulations applicable in Australia, referencing the Income Tax Assessment Act 1936 and 1997. It addresses the calculation of capital gain tax and capital allowance through a case study involving Jasmine, an Australian resident selling assets after retirement, and John, a business owner. The report examines the tax implications of selling a residential house, car, business (including equipment and goodwill), furniture, and paintings, considering relevant exemptions and regulations. It also calculates the cost and capital allowance for a CNC machine imported by John's manufacturing business, including associated expenses like travel and installation costs. The analysis considers the tax treatment of different asset types, including depreciating and non-depreciating assets, and provides detailed calculations for capital gain and capital allowance based on the provided case study.

Taxation Law

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Introduction...................................................................................................................3

Question 1- Capital gain tax.........................................................................................4

Question 2- Calculation of cost and capital allowance.................................................7

Conclusion....................................................................................................................9

Bibliography................................................................................................................10

2

Introduction...................................................................................................................3

Question 1- Capital gain tax.........................................................................................4

Question 2- Calculation of cost and capital allowance.................................................7

Conclusion....................................................................................................................9

Bibliography................................................................................................................10

2

Introduction

This report is concerned with the capital gain regulations applicable in Australia.

Rules and regulations in relation to capital gain tax in Australia are regulated with the

help of income tax assessment act 1936 and income tax assessment Act 1997.

Income Tax Act 1936 was established for the purpose of governing tax regulations

and over the period of time there have been various changes made in this act and all

the new methods are now generally added in income tax assessment Act 1997

(Australian Taxation Office, 2019). Capital gain tax can be defined as the tax

applicable on earnings gained by a person by selling capital assets. There are

various types of capital assets on which rules and regulations of the Income Tax Act

will be applied with respect to capital gain such as machinery, property, building,

shares, land, etc. The main focus of this report will be on identifying the problems

associated with the provided case study and calculating the amount of capital gain

and capital gain tax. In addition to capital gain tax this report will also be calculating

the amount of capital allowance that can be recorded in the business owned by John

in the second question.

3

This report is concerned with the capital gain regulations applicable in Australia.

Rules and regulations in relation to capital gain tax in Australia are regulated with the

help of income tax assessment act 1936 and income tax assessment Act 1997.

Income Tax Act 1936 was established for the purpose of governing tax regulations

and over the period of time there have been various changes made in this act and all

the new methods are now generally added in income tax assessment Act 1997

(Australian Taxation Office, 2019). Capital gain tax can be defined as the tax

applicable on earnings gained by a person by selling capital assets. There are

various types of capital assets on which rules and regulations of the Income Tax Act

will be applied with respect to capital gain such as machinery, property, building,

shares, land, etc. The main focus of this report will be on identifying the problems

associated with the provided case study and calculating the amount of capital gain

and capital gain tax. In addition to capital gain tax this report will also be calculating

the amount of capital allowance that can be recorded in the business owned by John

in the second question.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Question 1- Capital gain tax

The taxpayer under consideration in this report is Jasmine who is an Australian

resident. Jasmine was born in the United Kingdom and she is 65 years old at the

time of income tax assessment. According to the provided information she is moving

back to United Kingdom after taking retirement from her business as a cleaner. She

is selling all the assets that she had acquired in Australia before moving back to

United Kingdom. Selling of Australian assets will be covered under income tax

assessment act of Australia and it will give rise to capital gain in the hand of

Jasmine. The main focus of this section will be on calculating the amount of capital

gain with respect to different assets sold by Jasmine.

1. Sale of Residential house

In the given scenario Jasmin is selling out to home purchased by Jasmine in 1981

which was primarily used residential purposes from the date of its purchase. Cost of

this house in the year 1981 was $40000 and it can be sold now at $650000.

According to the rules and regulations provided in the Income Tax Act, all the assets

that were purchased before 1985 are exempt from capital gain tax. It can be said

that provisions of capital gain tax will not be applicable if the property is purchased

before 1985. This regulation is also provided the type of assets that are exempt from

capital gain such as car, furniture, houses, etc. therefore it can be said that house

purchased before 1985 is exempt from liability of capital gain tax. In the given

scenario Jasmin has purchased the house in 1981 i.e. before 1985 (Australian

Taxation Office, 2019). This sale of asset will not attract any kind of capital gain due

to exemption provided by Income Tax Act.

Note- in this scenario it should be considered that any person that is resident of

Australia required to pay tax in Australia on capital gain even if such person is selling

assets outside the country. Jasmine is not liable to pay tax only because the asset

was purchased before 1985.

2. Sale of Car

According to the provided case study, Jasmine is considering selling a car that was

purchased in the year 2011 at the cost of $31000. Currently worth of this car is

around 10000 and it can be considered as its selling price. Treatment of loss and

profit on assets used for the personal purpose is provided in section 102.5 of Income

Tax Act applicable in Australia. According to this section spelling of any asset that is

used for personal use would not attract any capital gain tax. Therefore any capital

gain arising out of sale of personal assets will not be taxable. In addition to that loss

arising out of selling personal assets will not be carried forward in future and such

loss can be set off against any other capital tax payable. The definition of personal

assets provided in the section includes a car.

In the given scenario car purchased by Jasmine is assumed to be used for as other

specific use of suggested has not been provided in the case study (Australian

Taxation Office, 2019). According to the applicable rules and regulations loss on the

sale of the car will not be carried forward in future and such loss can also not be set

off against any other capital tax payable. Therefore there will be no treatment of this

transaction in tax return prepared by Jasmine during the financial year.

4

The taxpayer under consideration in this report is Jasmine who is an Australian

resident. Jasmine was born in the United Kingdom and she is 65 years old at the

time of income tax assessment. According to the provided information she is moving

back to United Kingdom after taking retirement from her business as a cleaner. She

is selling all the assets that she had acquired in Australia before moving back to

United Kingdom. Selling of Australian assets will be covered under income tax

assessment act of Australia and it will give rise to capital gain in the hand of

Jasmine. The main focus of this section will be on calculating the amount of capital

gain with respect to different assets sold by Jasmine.

1. Sale of Residential house

In the given scenario Jasmin is selling out to home purchased by Jasmine in 1981

which was primarily used residential purposes from the date of its purchase. Cost of

this house in the year 1981 was $40000 and it can be sold now at $650000.

According to the rules and regulations provided in the Income Tax Act, all the assets

that were purchased before 1985 are exempt from capital gain tax. It can be said

that provisions of capital gain tax will not be applicable if the property is purchased

before 1985. This regulation is also provided the type of assets that are exempt from

capital gain such as car, furniture, houses, etc. therefore it can be said that house

purchased before 1985 is exempt from liability of capital gain tax. In the given

scenario Jasmin has purchased the house in 1981 i.e. before 1985 (Australian

Taxation Office, 2019). This sale of asset will not attract any kind of capital gain due

to exemption provided by Income Tax Act.

Note- in this scenario it should be considered that any person that is resident of

Australia required to pay tax in Australia on capital gain even if such person is selling

assets outside the country. Jasmine is not liable to pay tax only because the asset

was purchased before 1985.

2. Sale of Car

According to the provided case study, Jasmine is considering selling a car that was

purchased in the year 2011 at the cost of $31000. Currently worth of this car is

around 10000 and it can be considered as its selling price. Treatment of loss and

profit on assets used for the personal purpose is provided in section 102.5 of Income

Tax Act applicable in Australia. According to this section spelling of any asset that is

used for personal use would not attract any capital gain tax. Therefore any capital

gain arising out of sale of personal assets will not be taxable. In addition to that loss

arising out of selling personal assets will not be carried forward in future and such

loss can be set off against any other capital tax payable. The definition of personal

assets provided in the section includes a car.

In the given scenario car purchased by Jasmine is assumed to be used for as other

specific use of suggested has not been provided in the case study (Australian

Taxation Office, 2019). According to the applicable rules and regulations loss on the

sale of the car will not be carried forward in future and such loss can also not be set

off against any other capital tax payable. Therefore there will be no treatment of this

transaction in tax return prepared by Jasmine during the financial year.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3. Sale of business

As it is already discussed that to Jasmine was operating a cleaning business and

she is retiring from this business and moving to the United Kingdom. The provided

information Jasmine has found a buyer for her business. Such a buyer has agreed to

pay a price of $125000 for entire business. Out of this $125000, $65000 are paid

against acquisition of all equipment and 60000 are being paid for the purpose of

goodwill during the purchase of business. Currently the cost of equipment in

business is estimated to be $75000.

An income tax ruling was provided in the year 1999 which specified the accounting

Income Tax treatment with respect to Goodwill acquired during the process of

merger and acquisition or selling of the business. According to this ruling, the

definition of capital assets includes goodwill and capital gain tax will be charged on

selling goodwill to the new buyer. It is a fact that Goodwill is not a tangible asset and

it is only provided for the brand name of the business that is being sold. Still Goodwill

will be considered as a capital asset as it will help the new owner to generate

revenue in future (Australian Taxation Office, 2019).

In addition to that, any loss arising out of the sale of depreciable assets at the time of

sale of business will not be charged to capital gain. Similarly any loss arising out of

such assets cannot be carried forward or adjusted with any other capital gain. On the

basis of provided ruling it can be said that loss of 15000 arising out of sale of

business equipment so will not be set off against any other capital gain. In addition to

that sale of goodwill worth $60000 will be charged to capital gain at the end of

financial year in which business is sold.

4. Sale of furniture

Section 102.5 of Income Tax Act has already been discussed in the scenario where

selling her personal car. According to the section, any assert that is used for

personal purpose is not taxable under the rules and regulations of the Income Tax

Assessment Act. In the given scenario has sold her furniture foreign aggregate

amount of $5000. The overall cost of these assets is not accessible but it was

provided that none of the assets that are sold in this arrangement has a cost of more

than $2000 (Australian Taxation Office, 2019).

It can be said that the furniture sold by Jasmine is used for personal purpose as

nothing specific is provided with respect to the use of such asset. After consideration

of given case study and section 102.5 it can be said that there will be no capital gain

loss or profit on sale of furniture that is used for personal use by Jasmine.

5. Sale of paintings

Jasmine has a number of paintings in her possession and she is selling all the

paintings at the price of $35,000. All according to the provided information all of

these paintings were purchased by her from second-hand shops and markets.

According to the recollection of jasmine, none of these paintings were worth more

than $500 with an exception of one painting. One of the painting out of the paintings

sold by Jasmine was directly purchased from an artist. The cost price of this painting

was $1000 and it is currently being sold at $5000.

5

As it is already discussed that to Jasmine was operating a cleaning business and

she is retiring from this business and moving to the United Kingdom. The provided

information Jasmine has found a buyer for her business. Such a buyer has agreed to

pay a price of $125000 for entire business. Out of this $125000, $65000 are paid

against acquisition of all equipment and 60000 are being paid for the purpose of

goodwill during the purchase of business. Currently the cost of equipment in

business is estimated to be $75000.

An income tax ruling was provided in the year 1999 which specified the accounting

Income Tax treatment with respect to Goodwill acquired during the process of

merger and acquisition or selling of the business. According to this ruling, the

definition of capital assets includes goodwill and capital gain tax will be charged on

selling goodwill to the new buyer. It is a fact that Goodwill is not a tangible asset and

it is only provided for the brand name of the business that is being sold. Still Goodwill

will be considered as a capital asset as it will help the new owner to generate

revenue in future (Australian Taxation Office, 2019).

In addition to that, any loss arising out of the sale of depreciable assets at the time of

sale of business will not be charged to capital gain. Similarly any loss arising out of

such assets cannot be carried forward or adjusted with any other capital gain. On the

basis of provided ruling it can be said that loss of 15000 arising out of sale of

business equipment so will not be set off against any other capital gain. In addition to

that sale of goodwill worth $60000 will be charged to capital gain at the end of

financial year in which business is sold.

4. Sale of furniture

Section 102.5 of Income Tax Act has already been discussed in the scenario where

selling her personal car. According to the section, any assert that is used for

personal purpose is not taxable under the rules and regulations of the Income Tax

Assessment Act. In the given scenario has sold her furniture foreign aggregate

amount of $5000. The overall cost of these assets is not accessible but it was

provided that none of the assets that are sold in this arrangement has a cost of more

than $2000 (Australian Taxation Office, 2019).

It can be said that the furniture sold by Jasmine is used for personal purpose as

nothing specific is provided with respect to the use of such asset. After consideration

of given case study and section 102.5 it can be said that there will be no capital gain

loss or profit on sale of furniture that is used for personal use by Jasmine.

5. Sale of paintings

Jasmine has a number of paintings in her possession and she is selling all the

paintings at the price of $35,000. All according to the provided information all of

these paintings were purchased by her from second-hand shops and markets.

According to the recollection of jasmine, none of these paintings were worth more

than $500 with an exception of one painting. One of the painting out of the paintings

sold by Jasmine was directly purchased from an artist. The cost price of this painting

was $1000 and it is currently being sold at $5000.

5

According to the rules and regulations provided in section 118 of the income tax

assessment act, collectible goods are included in the definition of capital assets. In

addition to the collectible goods includes work of art, pictures, jewellery and other

collectible items. Paintings can be categorized as work of art, therefore, they will also

be considered as a capital asset for the purpose of capital gain rules and regulations.

Rules and regulations in relation to collectible have also provided that any collectible

that is purchased for a cost price of less than $500 is not required to be taxed under

capital gain rules and regulations (Australian Taxation Office, 2019). In addition to

that any loss arising out of sale of collectibles can be set off against profit earned

from sale of collectibles only. These losses can be carried forward but it will only be

set off against capital gain arising out of selling collectibles.

According to the provided information and rules and regulations of the income tax

assessment act, it can be said that paintings that are purchased by Jasmine from

second-hand market worth less than $500 will not be taxable. On the other hand

painting that is acquired directly from the artist at cost price of 1000 will be taxable in

the financial year in which it is sold. Rate of capital gain tax will be applied to the

profit earned on sale of that particular painting i.e. $4000 ($5000-$1000).

6

assessment act, collectible goods are included in the definition of capital assets. In

addition to the collectible goods includes work of art, pictures, jewellery and other

collectible items. Paintings can be categorized as work of art, therefore, they will also

be considered as a capital asset for the purpose of capital gain rules and regulations.

Rules and regulations in relation to collectible have also provided that any collectible

that is purchased for a cost price of less than $500 is not required to be taxed under

capital gain rules and regulations (Australian Taxation Office, 2019). In addition to

that any loss arising out of sale of collectibles can be set off against profit earned

from sale of collectibles only. These losses can be carried forward but it will only be

set off against capital gain arising out of selling collectibles.

According to the provided information and rules and regulations of the income tax

assessment act, it can be said that paintings that are purchased by Jasmine from

second-hand market worth less than $500 will not be taxable. On the other hand

painting that is acquired directly from the artist at cost price of 1000 will be taxable in

the financial year in which it is sold. Rate of capital gain tax will be applied to the

profit earned on sale of that particular painting i.e. $4000 ($5000-$1000).

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Question 2- Calculation of cost and capital allowance

According to the Income Tax assessment act 1997, any expense in a business

organization can be categorized into revenue expense and capital expenses.

Specific rules and regulations have been provided in this legislature with respect to

allowance on capital depreciation expenses that are directly attributable to fixed

assets i.e. expenses that are capital in nature. According to the applicable rules and

regulations, these capital expenses are required to be distributed throughout the life

of asset and are required to be charged in similar manner as depreciation (Australian

Taxation Office, 2019). All the assets on which depreciation is required to be

charged are called as depreciating Assets and there are some exceptions to

depreciating Assets on which depreciation is not required to be charged such as

land, trading stock, intangible assets, etc. Book value of depreciating assets will

decrease on a regular basis whereas book value of non-depreciating assets will not

be affected throughout its life unless and until there is a permanent decline in their

value.

Calculation of the cost of the asset is also an important part of providing depreciation

on such asset as cost of asset includes any kind of installation cost for initiation cost.

In addition to that any cost that is incurred for bringing such asset into operation will

also be included in cost of asset (Australian Taxation Office, 2019). Such cost of

asset will be included in historical cost price of such asset that will be shown in

balance sheet.

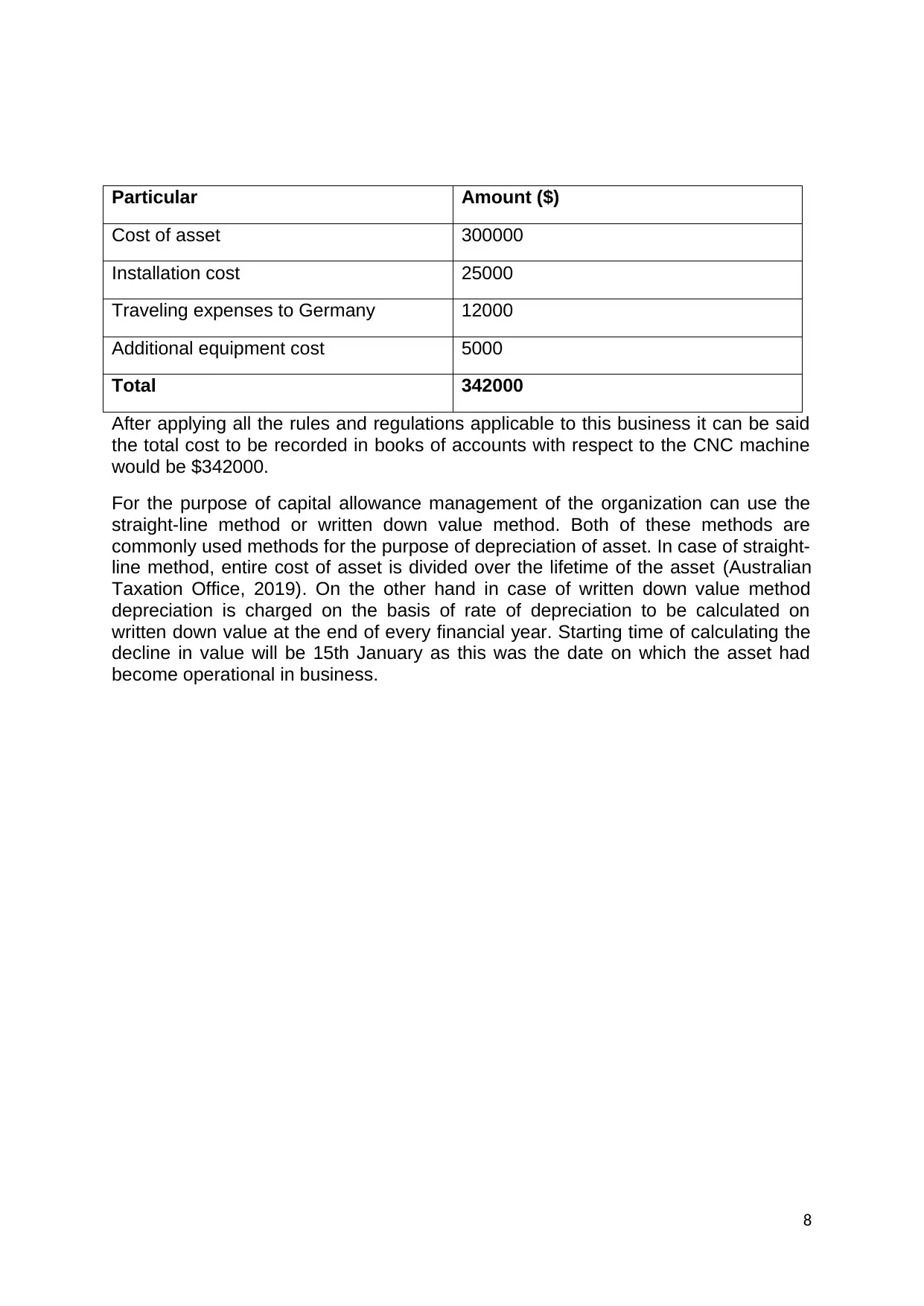

In the provided scenario John is an owner of a manufacturing organization that is in

Dust in manufacturing of motor vehicle parts and other accessories. Owner of the

organization has imported a CNC machine costing $300000 from Germany on 1st

November 2014. For the purpose of inspection John personally visited the CNC

machine manufacturing premises in order to check the quality of the machine. The

sole purpose of this visit to Germany was to import the machine in effective manner.

The total cost associated with this trip to Germany is estimated to be $12000.

Specialized installation is required for the purpose of installing the CNC machine

under consideration. This machine is required to be bolted down to the factory floor

and the overall cost of this installation is $25,000 and the process of installation is

completed on the 15th of January. This machine has not put into operation until the

date of installation. After this machine is put into manufacturing process after

installation process is completed but it was discovered that there are some

deficiencies in operational process of this machine. This machine will require an

additional guiding rod for efficiency of the machine. This installation was completed

on 1st February with a cost of $5000.

All the costs involved in bringing the assets to operation are to be including in the

total cost of the assets. In the given scenario trip to Germany was specifically for the

purpose of importing the machine, therefore, it is required to be included (Australian

Taxation Office, 2019). In addition to that installation cost is always included in cost

of asset as without installation such as it cannot be operational. Any cost incurred by

organisation for improving efficiency of asset is also a part of its cost. On the basis of

this assessment it can be said all of the cost incurred by John with respect to CNC

machine is required to be included in cost of asset. Statement showing cost of asset

will be as follows-

7

According to the Income Tax assessment act 1997, any expense in a business

organization can be categorized into revenue expense and capital expenses.

Specific rules and regulations have been provided in this legislature with respect to

allowance on capital depreciation expenses that are directly attributable to fixed

assets i.e. expenses that are capital in nature. According to the applicable rules and

regulations, these capital expenses are required to be distributed throughout the life

of asset and are required to be charged in similar manner as depreciation (Australian

Taxation Office, 2019). All the assets on which depreciation is required to be

charged are called as depreciating Assets and there are some exceptions to

depreciating Assets on which depreciation is not required to be charged such as

land, trading stock, intangible assets, etc. Book value of depreciating assets will

decrease on a regular basis whereas book value of non-depreciating assets will not

be affected throughout its life unless and until there is a permanent decline in their

value.

Calculation of the cost of the asset is also an important part of providing depreciation

on such asset as cost of asset includes any kind of installation cost for initiation cost.

In addition to that any cost that is incurred for bringing such asset into operation will

also be included in cost of asset (Australian Taxation Office, 2019). Such cost of

asset will be included in historical cost price of such asset that will be shown in

balance sheet.

In the provided scenario John is an owner of a manufacturing organization that is in

Dust in manufacturing of motor vehicle parts and other accessories. Owner of the

organization has imported a CNC machine costing $300000 from Germany on 1st

November 2014. For the purpose of inspection John personally visited the CNC

machine manufacturing premises in order to check the quality of the machine. The

sole purpose of this visit to Germany was to import the machine in effective manner.

The total cost associated with this trip to Germany is estimated to be $12000.

Specialized installation is required for the purpose of installing the CNC machine

under consideration. This machine is required to be bolted down to the factory floor

and the overall cost of this installation is $25,000 and the process of installation is

completed on the 15th of January. This machine has not put into operation until the

date of installation. After this machine is put into manufacturing process after

installation process is completed but it was discovered that there are some

deficiencies in operational process of this machine. This machine will require an

additional guiding rod for efficiency of the machine. This installation was completed

on 1st February with a cost of $5000.

All the costs involved in bringing the assets to operation are to be including in the

total cost of the assets. In the given scenario trip to Germany was specifically for the

purpose of importing the machine, therefore, it is required to be included (Australian

Taxation Office, 2019). In addition to that installation cost is always included in cost

of asset as without installation such as it cannot be operational. Any cost incurred by

organisation for improving efficiency of asset is also a part of its cost. On the basis of

this assessment it can be said all of the cost incurred by John with respect to CNC

machine is required to be included in cost of asset. Statement showing cost of asset

will be as follows-

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Particular Amount ($)

Cost of asset 300000

Installation cost 25000

Traveling expenses to Germany 12000

Additional equipment cost 5000

Total 342000

After applying all the rules and regulations applicable to this business it can be said

the total cost to be recorded in books of accounts with respect to the CNC machine

would be $342000.

For the purpose of capital allowance management of the organization can use the

straight-line method or written down value method. Both of these methods are

commonly used methods for the purpose of depreciation of asset. In case of straight-

line method, entire cost of asset is divided over the lifetime of the asset (Australian

Taxation Office, 2019). On the other hand in case of written down value method

depreciation is charged on the basis of rate of depreciation to be calculated on

written down value at the end of every financial year. Starting time of calculating the

decline in value will be 15th January as this was the date on which the asset had

become operational in business.

8

Cost of asset 300000

Installation cost 25000

Traveling expenses to Germany 12000

Additional equipment cost 5000

Total 342000

After applying all the rules and regulations applicable to this business it can be said

the total cost to be recorded in books of accounts with respect to the CNC machine

would be $342000.

For the purpose of capital allowance management of the organization can use the

straight-line method or written down value method. Both of these methods are

commonly used methods for the purpose of depreciation of asset. In case of straight-

line method, entire cost of asset is divided over the lifetime of the asset (Australian

Taxation Office, 2019). On the other hand in case of written down value method

depreciation is charged on the basis of rate of depreciation to be calculated on

written down value at the end of every financial year. Starting time of calculating the

decline in value will be 15th January as this was the date on which the asset had

become operational in business.

8

Conclusion

On an overall evaluation of this report, it can be said that the main focus of this

report was on calculation of capital gain and value of fixed asset. The first question

of the report has been focused on calculation of capital gain with respect to

Australian resident that is leaving the country and selling off her assets. This report

has provided capital gain treatment for each and every asset that has been sold in

the market. The second question of the report is focused on identification of

elements that will be included in calculation of fixed and start time for calculating the

decline in value of asset.

9

On an overall evaluation of this report, it can be said that the main focus of this

report was on calculation of capital gain and value of fixed asset. The first question

of the report has been focused on calculation of capital gain with respect to

Australian resident that is leaving the country and selling off her assets. This report

has provided capital gain treatment for each and every asset that has been sold in

the market. The second question of the report is focused on identification of

elements that will be included in calculation of fixed and start time for calculating the

decline in value of asset.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

References

Anon., 2019. Cost base. [Online]

Available at: https://iknow.cch.com.au/topic/tlp702/overview/cost-base

Anon., n.d. What are capital allowances?. [Online]

Available at: https://www.freeagent.com/glossary/capital-allowances/

[Accessed 13 July 2016].

Anon., n.d. What are capital allowances?. [Online]

Available at: https://home.kpmg/ie/en/home/services/tax/corporate-tax/capital-allowances/capital-

allowances-explained.html

Australian Taxation Office, 2019. Company income tax return 1997. s.l.:Retrievable at:

https://www.ato.gov.au/Forms/Company-income-tax-return-1997/.

Australian Taxation Office, 2019. Cost base.

s.l.:https://www.ato.gov.au/General/Capital-gains-tax/Working-out-your-capital-gain-or-loss/Cost-

base/.

Australian Taxation Office, 2019. Depreciation and capital expenses and allowances.

s.l.:https://www.ato.gov.au/business/depreciation-and-capital-expenses-and-allowances/.

Australian Taxation Office, 2019. Elements of the cost base and reduced cost base.

s.l.:https://www.ato.gov.au/General/Capital-gains-tax/Working-out-your-capital-gain-or-loss/Cost-

base/Elements-of-the-cost-base-and-reduced-cost-base/.

Australian Taxation Office, 2019. Motor vehicle retail – new and used.

s.l.:https://www.ato.gov.au/Business/Small-business-benchmarks/In-detail/Benchmarks-by-

industry/Retail-trade/Motor-vehicle-retail---new-and-used/.

Australian Taxation Office, 2019. Residential premises.

s.l.:https://www.ato.gov.au/business/gst/when-to-charge-gst-(and-when-not-to)/input-taxed-

sales/residential-premises/.

Australian Taxation Office, 2019. Sale of a business as a going concern – supporting information.

s.l.:https://www.ato.gov.au/General/ATO-advice-and-guidance/In-detail/Private-rulings/Supporting-

documents/GST/Sale-of-a-business-as-a-going-concern/.

Australian Taxation Office, 2019. Taxable Sales. s.l.:https://www.ato.gov.au/business/gst/when-to-

charge-gst-(and-when-not-to)/taxable-sales/.

Australian Taxation Office, 2019. The cost of a depreciating asset. s.l.:https://www.ato.gov.au/Print-

publications/Guide-to-depreciating-assets-2019/?page=10.

Gardiner, S., 2019. Tax depreciation. [Online]

Available at: https://www2.deloitte.com/ie/en/pages/deloitte-private/articles/tax-depreciation.html

Wilkins, M., 2019. What is Capital Allowance?. [Online]

Available at: http://blog.capitalclaims.com.au/property-tax-depreciation/what-is-capital-allowance

10

Anon., 2019. Cost base. [Online]

Available at: https://iknow.cch.com.au/topic/tlp702/overview/cost-base

Anon., n.d. What are capital allowances?. [Online]

Available at: https://www.freeagent.com/glossary/capital-allowances/

[Accessed 13 July 2016].

Anon., n.d. What are capital allowances?. [Online]

Available at: https://home.kpmg/ie/en/home/services/tax/corporate-tax/capital-allowances/capital-

allowances-explained.html

Australian Taxation Office, 2019. Company income tax return 1997. s.l.:Retrievable at:

https://www.ato.gov.au/Forms/Company-income-tax-return-1997/.

Australian Taxation Office, 2019. Cost base.

s.l.:https://www.ato.gov.au/General/Capital-gains-tax/Working-out-your-capital-gain-or-loss/Cost-

base/.

Australian Taxation Office, 2019. Depreciation and capital expenses and allowances.

s.l.:https://www.ato.gov.au/business/depreciation-and-capital-expenses-and-allowances/.

Australian Taxation Office, 2019. Elements of the cost base and reduced cost base.

s.l.:https://www.ato.gov.au/General/Capital-gains-tax/Working-out-your-capital-gain-or-loss/Cost-

base/Elements-of-the-cost-base-and-reduced-cost-base/.

Australian Taxation Office, 2019. Motor vehicle retail – new and used.

s.l.:https://www.ato.gov.au/Business/Small-business-benchmarks/In-detail/Benchmarks-by-

industry/Retail-trade/Motor-vehicle-retail---new-and-used/.

Australian Taxation Office, 2019. Residential premises.

s.l.:https://www.ato.gov.au/business/gst/when-to-charge-gst-(and-when-not-to)/input-taxed-

sales/residential-premises/.

Australian Taxation Office, 2019. Sale of a business as a going concern – supporting information.

s.l.:https://www.ato.gov.au/General/ATO-advice-and-guidance/In-detail/Private-rulings/Supporting-

documents/GST/Sale-of-a-business-as-a-going-concern/.

Australian Taxation Office, 2019. Taxable Sales. s.l.:https://www.ato.gov.au/business/gst/when-to-

charge-gst-(and-when-not-to)/taxable-sales/.

Australian Taxation Office, 2019. The cost of a depreciating asset. s.l.:https://www.ato.gov.au/Print-

publications/Guide-to-depreciating-assets-2019/?page=10.

Gardiner, S., 2019. Tax depreciation. [Online]

Available at: https://www2.deloitte.com/ie/en/pages/deloitte-private/articles/tax-depreciation.html

Wilkins, M., 2019. What is Capital Allowance?. [Online]

Available at: http://blog.capitalclaims.com.au/property-tax-depreciation/what-is-capital-allowance

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.