Taxation Law 11: Capital Gains, Depreciation, and Tax Concessions

VerifiedAdded on 2022/11/10

|12

|2821

|413

Homework Assignment

AI Summary

This document presents a comprehensive solution to a taxation law assignment, addressing key concepts such as capital gains tax (CGT), depreciation, and small business concessions. The solution analyzes various scenarios, including the sale of a main residence, personal use assets (PUAs) like cars and furniture, and the application of small business CGT concessions. It also examines the treatment of collectables like paintings. The assignment further delves into depreciation rules, specifically concerning depreciating assets like an industrial CNC machine, and the associated costs including purchase price, installation, and improvements. The solution references relevant sections of the Income Tax Assessment Act 1997 (ITAA 1997) and case law to support its arguments, providing a detailed and practical understanding of taxation principles.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the university

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the university

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Answer A:..............................................................................................................................2

Answer B:...............................................................................................................................2

Answer C:...............................................................................................................................3

Answer D:..............................................................................................................................4

Answer E:...............................................................................................................................5

Answer to question 2:.................................................................................................................6

Issus:.......................................................................................................................................6

Law:........................................................................................................................................6

Application:............................................................................................................................7

Conclusion:............................................................................................................................9

References:...............................................................................................................................10

Table of Contents

Answer to question 1:.................................................................................................................2

Answer A:..............................................................................................................................2

Answer B:...............................................................................................................................2

Answer C:...............................................................................................................................3

Answer D:..............................................................................................................................4

Answer E:...............................................................................................................................5

Answer to question 2:.................................................................................................................6

Issus:.......................................................................................................................................6

Law:........................................................................................................................................6

Application:............................................................................................................................7

Conclusion:............................................................................................................................9

References:...............................................................................................................................10

2TAXATION LAW

Answer to question 1:

Answer A:

Capital gains represents the meaning of the term capital where the non-income gains

are not held as income. Capital gains represents the realisation of the asset where the gain do

not originate from conducting any kind of business activities or conducting any form of

isolated business venture (O’Connell 2017). There is an explanation that is given to the

taxpayer that assets which is acquired or the any other occurrence of events on or following

20/9/85 is considered for CGT. The word pre and post-CGT is applied prior to or following

that date. CGT event A1 under “sec 104-10”, involves the sale of CGT asset. This event is

applied on CGT assets purchased following 19/9/85.

The taxpayer can claim exemption from CGT derived from the main residence under

“Div-118-B, ITAA 1997”. The broad rule “sec 118-110” declares that a capital gain or loss

happening to the main dwelling of the taxpayer is simply omitted under this rule (Bain and

Boccabella 2019).

Jasmine by paying a sum of $40,000 in 1981 purchased a home for her-self that she

used as her main residence. While taking the decision of moving back to UK, Jasmine sold

her main dwelling for $650,000 that mainly used for her residence purpose. The disposal of

house is led to “CGT event A1” under “sec 104-10, ITAA 1997”. Jasmine has however,

purchased the asset before 1981. The asset is a pre-CGT asset because it was prior to

introducing CGT regime. The capital gains earned by Jasmine from selling her home is

exempted in this situation.

Answer B:

Apart from the collectable the personal use asset represents those assets that is bought

for private delight and use under “sec 108-20, ITAA 1997” (McCluskey 2018). “Sec 108-20

Answer to question 1:

Answer A:

Capital gains represents the meaning of the term capital where the non-income gains

are not held as income. Capital gains represents the realisation of the asset where the gain do

not originate from conducting any kind of business activities or conducting any form of

isolated business venture (O’Connell 2017). There is an explanation that is given to the

taxpayer that assets which is acquired or the any other occurrence of events on or following

20/9/85 is considered for CGT. The word pre and post-CGT is applied prior to or following

that date. CGT event A1 under “sec 104-10”, involves the sale of CGT asset. This event is

applied on CGT assets purchased following 19/9/85.

The taxpayer can claim exemption from CGT derived from the main residence under

“Div-118-B, ITAA 1997”. The broad rule “sec 118-110” declares that a capital gain or loss

happening to the main dwelling of the taxpayer is simply omitted under this rule (Bain and

Boccabella 2019).

Jasmine by paying a sum of $40,000 in 1981 purchased a home for her-self that she

used as her main residence. While taking the decision of moving back to UK, Jasmine sold

her main dwelling for $650,000 that mainly used for her residence purpose. The disposal of

house is led to “CGT event A1” under “sec 104-10, ITAA 1997”. Jasmine has however,

purchased the asset before 1981. The asset is a pre-CGT asset because it was prior to

introducing CGT regime. The capital gains earned by Jasmine from selling her home is

exempted in this situation.

Answer B:

Apart from the collectable the personal use asset represents those assets that is bought

for private delight and use under “sec 108-20, ITAA 1997” (McCluskey 2018). “Sec 108-20

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

(2), ITAA 1997” provides the example of PUA’s this includes the boats, household goods,

furniture etc. Most notably within “sec 108-20 (1)” any kind of capital loss arising from sale

of PUA’s should be ignored in this situation by taxpayer.

There was a car which Jasmine has purchased for $31,000 in 2011. The now worth

just about $10k when Jasmine undertook the decision of selling it. In this situation, the car is

personal use asset for Jasmine within “sec 108-20 (2), ITAA 1997”. This is because Jasmine

has purchased the car for her private usage (Prince 2016). As a result, when Jasmine sold the

car, a “CGT event A1” happened within “sec 104-10 (1)”. Upon selling the car Jasmine

realised capital loss. As per the rule given within “sec 108-20 (2), ITAA 1997” capital loss

realised by Jasmine should be ignored.

Answer C:

“Div 152, ITAA 1997” says that small business is given concessions for CGT events that

happen on or following 21/9/1999 (Prince 2016). When it is noticed that a CGT asset meets

the “active asset test” there are four types of concessions given to small business. This

includes;

a. Under “section 152-10” a small business entity or the partner in the SBE; or

b. Under “section 152-10 & 152-15, ITAA 1997”, any kind of business taxpayer that

has the net amount of CGT asset and any other related entities is not greater than $6

million (Evans, Minas and Lim 2015).

The four types of small business concessions are as follows;

a. Under “Subdivision 152-B”, exemption from capital gains is permitted for assets that

is owned for 15 years.

b. Within “Subdivision 152-C”, there is a reduction of capital gain by 50% is allowed to

taxpayer.

(2), ITAA 1997” provides the example of PUA’s this includes the boats, household goods,

furniture etc. Most notably within “sec 108-20 (1)” any kind of capital loss arising from sale

of PUA’s should be ignored in this situation by taxpayer.

There was a car which Jasmine has purchased for $31,000 in 2011. The now worth

just about $10k when Jasmine undertook the decision of selling it. In this situation, the car is

personal use asset for Jasmine within “sec 108-20 (2), ITAA 1997”. This is because Jasmine

has purchased the car for her private usage (Prince 2016). As a result, when Jasmine sold the

car, a “CGT event A1” happened within “sec 104-10 (1)”. Upon selling the car Jasmine

realised capital loss. As per the rule given within “sec 108-20 (2), ITAA 1997” capital loss

realised by Jasmine should be ignored.

Answer C:

“Div 152, ITAA 1997” says that small business is given concessions for CGT events that

happen on or following 21/9/1999 (Prince 2016). When it is noticed that a CGT asset meets

the “active asset test” there are four types of concessions given to small business. This

includes;

a. Under “section 152-10” a small business entity or the partner in the SBE; or

b. Under “section 152-10 & 152-15, ITAA 1997”, any kind of business taxpayer that

has the net amount of CGT asset and any other related entities is not greater than $6

million (Evans, Minas and Lim 2015).

The four types of small business concessions are as follows;

a. Under “Subdivision 152-B”, exemption from capital gains is permitted for assets that

is owned for 15 years.

b. Within “Subdivision 152-C”, there is a reduction of capital gain by 50% is allowed to

taxpayer.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

c. Under “Subdivision 152-D”, taxpayers can obtain the exemption relating to retirement

capital gains (Ingles 2019).

d. Within “Subdivision 152-E”, taxpayers are permitted roll-over relief for assets

replacement

As it is understood that Jasmine is leaving Australia to move UK on permanent basis,

she is also selling her small business of cleaning that she started herself. She finally finds a

buyer who agrees to take the business for $125,000. The assets were sold for $65000 while

the goodwill for $60,000. While for her business goodwill, its sale has contributed to “CGT

event C1” because the business was Jasmine was stopped permanently when she ceased

operations. Jasmine business is satisfying the active asset test under “sec 152-35” and her

business qualifies as SBE under “sec 152-10”. Furthermore, her CGT assets of business does

not worth more than $6 million under “sec 152-10 and 152-15”. Jasmine here obtain a

retirement exemption from the capital gains under “Subdiv 152-D, ITAA 1997”.

Answer D:

Within the “sec 118-10 (3), ITAA 1997” gains must be ignored by the taxpayer when

an acquisition of PUA’s is made for lower than $10,000. This is because the first element of

the personal use asset cost base is not satisfied by the taxpayer. Jasmine is found to have sold

the furniture for $5,000 that has the cost base of greater than $2,000. When the furniture was

sold by Jasmine a “CGT event A1” happened under “sec 104-10 (1), ITAA 1997” because

the asset was the post-CGT asset (Dougla and Pejoska 2017). Furthermore, capital gains

realised by Jasmine from the furniture must be ignored under “sec 118-10 (3), ITAA 1997”,

because it was purchased for lower than $10,000. The first element of cost base of asset is not

met under this situation by Jasmine.

c. Under “Subdivision 152-D”, taxpayers can obtain the exemption relating to retirement

capital gains (Ingles 2019).

d. Within “Subdivision 152-E”, taxpayers are permitted roll-over relief for assets

replacement

As it is understood that Jasmine is leaving Australia to move UK on permanent basis,

she is also selling her small business of cleaning that she started herself. She finally finds a

buyer who agrees to take the business for $125,000. The assets were sold for $65000 while

the goodwill for $60,000. While for her business goodwill, its sale has contributed to “CGT

event C1” because the business was Jasmine was stopped permanently when she ceased

operations. Jasmine business is satisfying the active asset test under “sec 152-35” and her

business qualifies as SBE under “sec 152-10”. Furthermore, her CGT assets of business does

not worth more than $6 million under “sec 152-10 and 152-15”. Jasmine here obtain a

retirement exemption from the capital gains under “Subdiv 152-D, ITAA 1997”.

Answer D:

Within the “sec 118-10 (3), ITAA 1997” gains must be ignored by the taxpayer when

an acquisition of PUA’s is made for lower than $10,000. This is because the first element of

the personal use asset cost base is not satisfied by the taxpayer. Jasmine is found to have sold

the furniture for $5,000 that has the cost base of greater than $2,000. When the furniture was

sold by Jasmine a “CGT event A1” happened under “sec 104-10 (1), ITAA 1997” because

the asset was the post-CGT asset (Dougla and Pejoska 2017). Furthermore, capital gains

realised by Jasmine from the furniture must be ignored under “sec 118-10 (3), ITAA 1997”,

because it was purchased for lower than $10,000. The first element of cost base of asset is not

met under this situation by Jasmine.

5TAXATION LAW

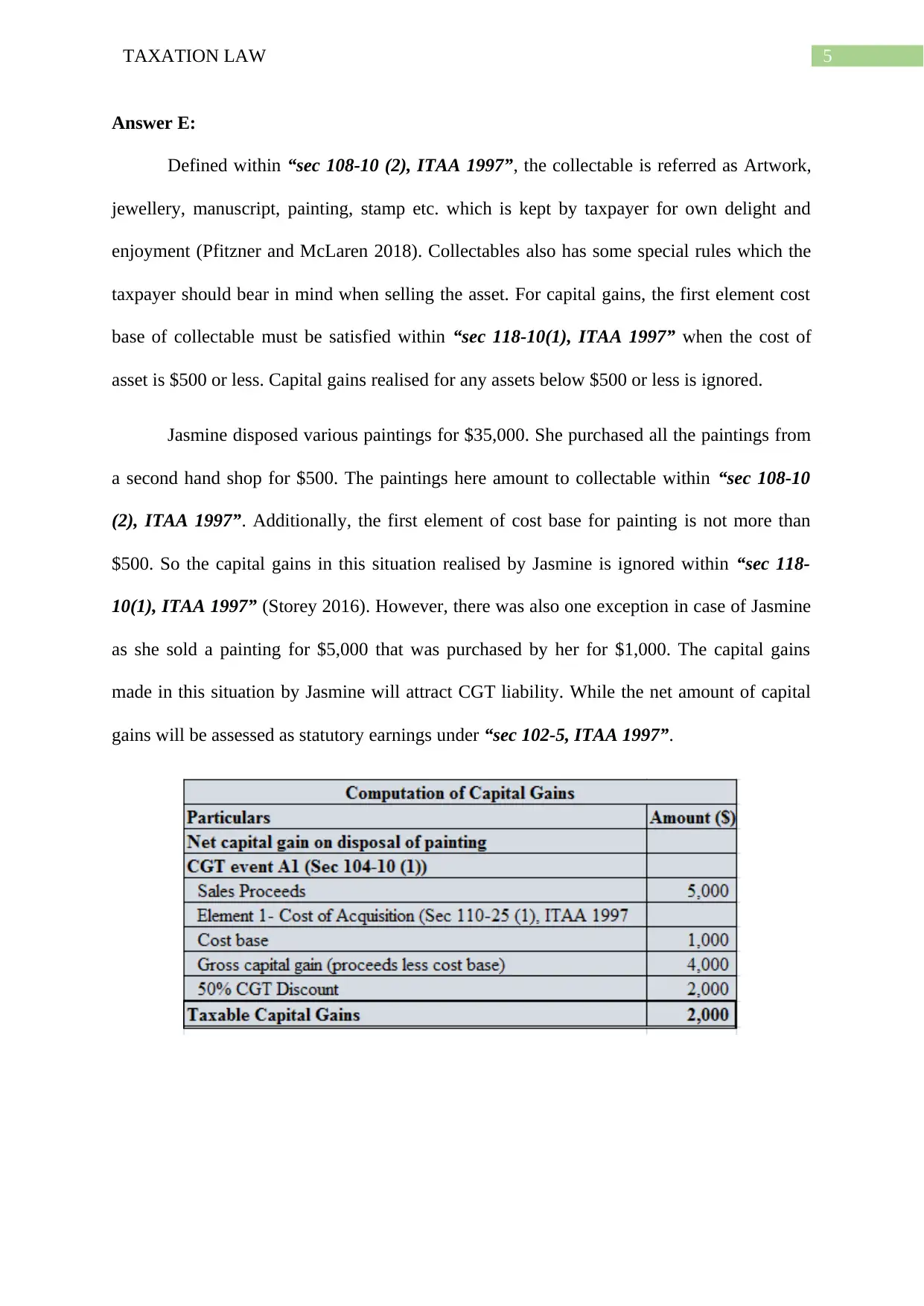

Answer E:

Defined within “sec 108-10 (2), ITAA 1997”, the collectable is referred as Artwork,

jewellery, manuscript, painting, stamp etc. which is kept by taxpayer for own delight and

enjoyment (Pfitzner and McLaren 2018). Collectables also has some special rules which the

taxpayer should bear in mind when selling the asset. For capital gains, the first element cost

base of collectable must be satisfied within “sec 118-10(1), ITAA 1997” when the cost of

asset is $500 or less. Capital gains realised for any assets below $500 or less is ignored.

Jasmine disposed various paintings for $35,000. She purchased all the paintings from

a second hand shop for $500. The paintings here amount to collectable within “sec 108-10

(2), ITAA 1997”. Additionally, the first element of cost base for painting is not more than

$500. So the capital gains in this situation realised by Jasmine is ignored within “sec 118-

10(1), ITAA 1997” (Storey 2016). However, there was also one exception in case of Jasmine

as she sold a painting for $5,000 that was purchased by her for $1,000. The capital gains

made in this situation by Jasmine will attract CGT liability. While the net amount of capital

gains will be assessed as statutory earnings under “sec 102-5, ITAA 1997”.

Answer E:

Defined within “sec 108-10 (2), ITAA 1997”, the collectable is referred as Artwork,

jewellery, manuscript, painting, stamp etc. which is kept by taxpayer for own delight and

enjoyment (Pfitzner and McLaren 2018). Collectables also has some special rules which the

taxpayer should bear in mind when selling the asset. For capital gains, the first element cost

base of collectable must be satisfied within “sec 118-10(1), ITAA 1997” when the cost of

asset is $500 or less. Capital gains realised for any assets below $500 or less is ignored.

Jasmine disposed various paintings for $35,000. She purchased all the paintings from

a second hand shop for $500. The paintings here amount to collectable within “sec 108-10

(2), ITAA 1997”. Additionally, the first element of cost base for painting is not more than

$500. So the capital gains in this situation realised by Jasmine is ignored within “sec 118-

10(1), ITAA 1997” (Storey 2016). However, there was also one exception in case of Jasmine

as she sold a painting for $5,000 that was purchased by her for $1,000. The capital gains

made in this situation by Jasmine will attract CGT liability. While the net amount of capital

gains will be assessed as statutory earnings under “sec 102-5, ITAA 1997”.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

Answer to question 2:

Issus:

The concerned issue here is the claim for depreciation based on the capital cost of

depreciating asset used by taxpayer for generating earnings under “sec 40-25, ITAA 1997”.

Law:

Referring to “division 40, ITAA 1997”, deduction is permitted for depreciation on the

basis of the cost of depreciating asset. The depreciating assets is primarily involved in the

production of taxpayer business income. Furthermore, an explanation that is contained within

the “division 40, ITAA 1997” covers the provision associated to the uniform capital

allowance that is mostly applied on wide variety of depreciating asset held by taxpayer

(Neutze 2016). “Sec 40-880” also includes the range of capital expenses that are allowed to

taxpayer in relation to the depreciating asset for claim purpose.

Most importantly within “sec 40.25 (1), ITAA 1997” which is also viewed as key

operative provision of capital allowance regime, permits the taxpayer with deduction from

the sum that is equivalent to “decline in value” (deprecation) of the “depreciating asset”

held for generating assessable income by the taxpayer during the year (Curtis 2016).

Deduction for depreciation purpose is also permitted to taxpayer when they start holding the

asset as installed ready for use.

The meaning of held relating to depreciating asset is given in “subsection 40-25 (1),

ITAA 1997”. Under this rule a deduction for depreciation of depreciating asset that is held by

taxpayer is permitted during the year. Usually, there will be the lawful owner of the asset that

begins to hold the asset and will be permitted for claiming deduction relating to depreciation

of the asset. In the meantime, “sec 40-30 (1), ITAA 1997” explains the depreciating asset as

that asset which only has limited useful life (Boadway and Tremblay 2016). These assets are

Answer to question 2:

Issus:

The concerned issue here is the claim for depreciation based on the capital cost of

depreciating asset used by taxpayer for generating earnings under “sec 40-25, ITAA 1997”.

Law:

Referring to “division 40, ITAA 1997”, deduction is permitted for depreciation on the

basis of the cost of depreciating asset. The depreciating assets is primarily involved in the

production of taxpayer business income. Furthermore, an explanation that is contained within

the “division 40, ITAA 1997” covers the provision associated to the uniform capital

allowance that is mostly applied on wide variety of depreciating asset held by taxpayer

(Neutze 2016). “Sec 40-880” also includes the range of capital expenses that are allowed to

taxpayer in relation to the depreciating asset for claim purpose.

Most importantly within “sec 40.25 (1), ITAA 1997” which is also viewed as key

operative provision of capital allowance regime, permits the taxpayer with deduction from

the sum that is equivalent to “decline in value” (deprecation) of the “depreciating asset”

held for generating assessable income by the taxpayer during the year (Curtis 2016).

Deduction for depreciation purpose is also permitted to taxpayer when they start holding the

asset as installed ready for use.

The meaning of held relating to depreciating asset is given in “subsection 40-25 (1),

ITAA 1997”. Under this rule a deduction for depreciation of depreciating asset that is held by

taxpayer is permitted during the year. Usually, there will be the lawful owner of the asset that

begins to hold the asset and will be permitted for claiming deduction relating to depreciation

of the asset. In the meantime, “sec 40-30 (1), ITAA 1997” explains the depreciating asset as

that asset which only has limited useful life (Boadway and Tremblay 2016). These assets are

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

generally anticipated to depreciate based on the time and usage. The meaning of the asset was

explained by court in “FCT v Wangaratta Wollen Mills Ltd (1969)” where a dye house was

held as plant, in contrast to the general situation with structure.

On the other hand, under “sec 40.60 (1)” says that the start begins when the taxpayer

commences holding the asset. The depreciating asset start time happens under “sec 40.60 (2),

ITAA 1997” when the first use is made by taxpayer for the taxable purpose as ready for use.

This implies that the depreciation of assets begins when the it is installed first as ready to use

by taxpayer. Most importantly within the “Subdiv 40-C” a depreciation is permitted for the

cost of the asset that is purchased by taxpayer for their usage in taxable purpose (Langham

and Paulsen 2017). For the depreciation purpose, not only does the purchase price is counted

but also the incidental cost that is involved in delivery and installation is included as well.

Any kind of minor expenditure that is reported by the taxpayer for removal or the

rearrangement of depreciating asset then the cost will be included into the cost base of the

asset.

There are some specific rules in “sec 40-180” that helps the taxpayer in computing

the cost base under the first element (Sadiq 2019). The first element on majority of the

occasion includes the price which is paid by taxpayer for purchasing the depreciating asset.

Meanwhile, “sec 40-190” lay down the costs that are included in the second element such as

the capital improvement cost, installation cost, delivery cost occurred by the taxpayer for the

asset.

Application:

The case study puts forward that John has been operating a business of manufacturing

the certified BMW parts. John bought an industrial CNC machine that was imported from

Germany on 1st November 2014. The machine was installed in 15th January as ready for

generally anticipated to depreciate based on the time and usage. The meaning of the asset was

explained by court in “FCT v Wangaratta Wollen Mills Ltd (1969)” where a dye house was

held as plant, in contrast to the general situation with structure.

On the other hand, under “sec 40.60 (1)” says that the start begins when the taxpayer

commences holding the asset. The depreciating asset start time happens under “sec 40.60 (2),

ITAA 1997” when the first use is made by taxpayer for the taxable purpose as ready for use.

This implies that the depreciation of assets begins when the it is installed first as ready to use

by taxpayer. Most importantly within the “Subdiv 40-C” a depreciation is permitted for the

cost of the asset that is purchased by taxpayer for their usage in taxable purpose (Langham

and Paulsen 2017). For the depreciation purpose, not only does the purchase price is counted

but also the incidental cost that is involved in delivery and installation is included as well.

Any kind of minor expenditure that is reported by the taxpayer for removal or the

rearrangement of depreciating asset then the cost will be included into the cost base of the

asset.

There are some specific rules in “sec 40-180” that helps the taxpayer in computing

the cost base under the first element (Sadiq 2019). The first element on majority of the

occasion includes the price which is paid by taxpayer for purchasing the depreciating asset.

Meanwhile, “sec 40-190” lay down the costs that are included in the second element such as

the capital improvement cost, installation cost, delivery cost occurred by the taxpayer for the

asset.

Application:

The case study puts forward that John has been operating a business of manufacturing

the certified BMW parts. John bought an industrial CNC machine that was imported from

Germany on 1st November 2014. The machine was installed in 15th January as ready for

8TAXATION LAW

business usage. John paid a sum of $300,000 to purchase the machine. Mentioning “FCT v

Wangaratta Wollen Mills Ltd (1969)” the CNC machine here satisfies the meaning of

depreciating asset given in “sec 40.30 (1)” because it has the limited useful life and the CNC

machine is anticipated to fall in value based on the time of the usage (Langham and Paulsen

2017).

The taxpayer here John is permitted get the deduction for CNC Machine under “sec

40-25, ITAA 1997” because the asset is bought by John exclusively for the taxable purpose.

In other words, the asset here is purchased by him for use in business purpose. Within “sec

40-60 (1)” the start time for depreciation purpose is 15th January because John has installed

the machine as ready for business use (Neutze 2016). While to determine the decline in value

of asset in the situation of John “subdiv 40-C” is referred which explains that depreciation is

done on the basis of cost of depreciating asset. Within “sec 40.180, ITAA 1997” the purchase

price paid by John for acquiring the CNC machine will be included inside the first element

cost base.

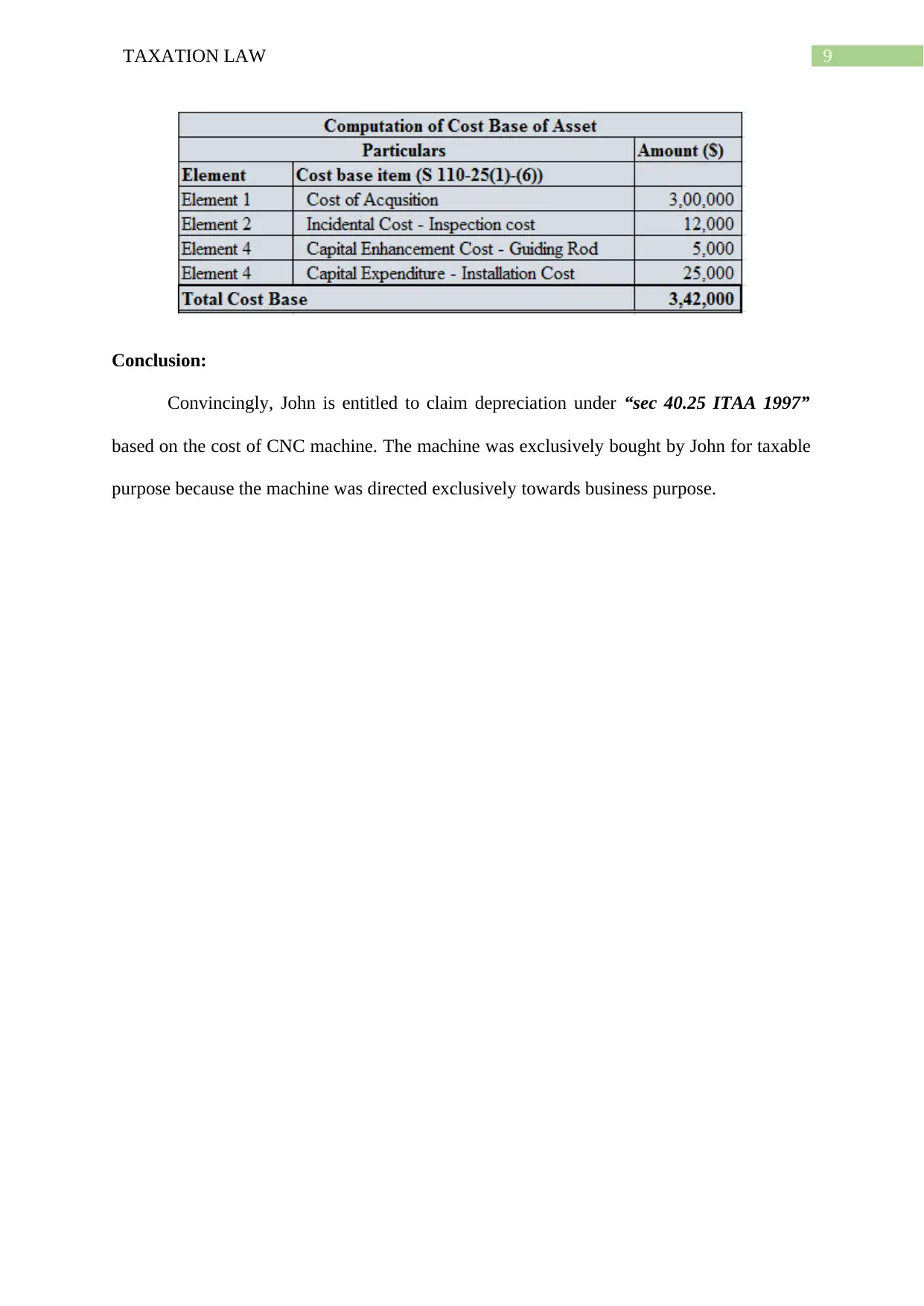

John during the year also reported that he spends additional cost of $25,000 for

installing the machine. Additionally, he incurred the travel cost of $12,000 for inspecting the

machine. On 1st February a guiding rod of $5,000 was also installed in the CNC machine as

this was aimed at improving the performance. Under “sec 40.190, ITAA 1997” these cost

will be included under the second element cost base of CNC machine. The overall cost base

of the machine for depreciation purpose is given below;

business usage. John paid a sum of $300,000 to purchase the machine. Mentioning “FCT v

Wangaratta Wollen Mills Ltd (1969)” the CNC machine here satisfies the meaning of

depreciating asset given in “sec 40.30 (1)” because it has the limited useful life and the CNC

machine is anticipated to fall in value based on the time of the usage (Langham and Paulsen

2017).

The taxpayer here John is permitted get the deduction for CNC Machine under “sec

40-25, ITAA 1997” because the asset is bought by John exclusively for the taxable purpose.

In other words, the asset here is purchased by him for use in business purpose. Within “sec

40-60 (1)” the start time for depreciation purpose is 15th January because John has installed

the machine as ready for business use (Neutze 2016). While to determine the decline in value

of asset in the situation of John “subdiv 40-C” is referred which explains that depreciation is

done on the basis of cost of depreciating asset. Within “sec 40.180, ITAA 1997” the purchase

price paid by John for acquiring the CNC machine will be included inside the first element

cost base.

John during the year also reported that he spends additional cost of $25,000 for

installing the machine. Additionally, he incurred the travel cost of $12,000 for inspecting the

machine. On 1st February a guiding rod of $5,000 was also installed in the CNC machine as

this was aimed at improving the performance. Under “sec 40.190, ITAA 1997” these cost

will be included under the second element cost base of CNC machine. The overall cost base

of the machine for depreciation purpose is given below;

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

Conclusion:

Convincingly, John is entitled to claim depreciation under “sec 40.25 ITAA 1997”

based on the cost of CNC machine. The machine was exclusively bought by John for taxable

purpose because the machine was directed exclusively towards business purpose.

Conclusion:

Convincingly, John is entitled to claim depreciation under “sec 40.25 ITAA 1997”

based on the cost of CNC machine. The machine was exclusively bought by John for taxable

purpose because the machine was directed exclusively towards business purpose.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

References:

Bain, K., and Boccabella, D. 2019. The Age of the Home Worker–Part 2: Calculation of

Home Occupancy Expense Deductions, Deduction Apportionment and Partial Loss of CGT

Main Residence Exemption. In Australian Tax Forum (Vol. 34, No. 1).

Boadway, R. and Tremblay, J.F., 2016. Modernizing Business Taxation. CD Howe Institute

Commentary, 452.

Curtis, V., 2016. Small Business For Dummies-Australia & New Zealand. John Wiley &

Sons.

Douglas, J. and Pejoska, A.L., 2017. Regulation and small business. Economic Round-up,

(2017), p.1.

Evans, C., Minas, J. and Lim, Y., 2015. Taxing personal capital gains in Australia: An

alternative way forward. Austl. Tax F., 30, p.735.

Ingles, D., 2019. Taxing Capital Income and the Z-Tax Solution. Tax and Transfer Policy

Institute-working paper, 6.

Kenny, P., 2018. Small business capital allowances.

Langham, J.A. and Paulsen, N., 2017. Invisible Taxation: Fantasy or Just Good Service

Design. Austl. Tax F., 32, p.129.

McCluskey, W., 2018. Property tax: An international comparative review. Routledge.

Neutze, D., 2016. Tax tips for small business.

O’Connell, A., 2017. Australia. In Capital Gains Taxation. Edward Elgar Publishing.

Pfitzner, D.M. and McLaren, J., 2018. Microbusinesses in Australia: a robust

definition. Australasian Accounting Business & Finance Journal, 12(3), pp.4-18.

References:

Bain, K., and Boccabella, D. 2019. The Age of the Home Worker–Part 2: Calculation of

Home Occupancy Expense Deductions, Deduction Apportionment and Partial Loss of CGT

Main Residence Exemption. In Australian Tax Forum (Vol. 34, No. 1).

Boadway, R. and Tremblay, J.F., 2016. Modernizing Business Taxation. CD Howe Institute

Commentary, 452.

Curtis, V., 2016. Small Business For Dummies-Australia & New Zealand. John Wiley &

Sons.

Douglas, J. and Pejoska, A.L., 2017. Regulation and small business. Economic Round-up,

(2017), p.1.

Evans, C., Minas, J. and Lim, Y., 2015. Taxing personal capital gains in Australia: An

alternative way forward. Austl. Tax F., 30, p.735.

Ingles, D., 2019. Taxing Capital Income and the Z-Tax Solution. Tax and Transfer Policy

Institute-working paper, 6.

Kenny, P., 2018. Small business capital allowances.

Langham, J.A. and Paulsen, N., 2017. Invisible Taxation: Fantasy or Just Good Service

Design. Austl. Tax F., 32, p.129.

McCluskey, W., 2018. Property tax: An international comparative review. Routledge.

Neutze, D., 2016. Tax tips for small business.

O’Connell, A., 2017. Australia. In Capital Gains Taxation. Edward Elgar Publishing.

Pfitzner, D.M. and McLaren, J., 2018. Microbusinesses in Australia: a robust

definition. Australasian Accounting Business & Finance Journal, 12(3), pp.4-18.

11TAXATION LAW

Prince, J.B., 2016. Tax for Australians for Dummies. John Wiley & Sons.

Sadiq, K., 2019. Australian Taxation Law Cases 2019. Thomson Reuters.

Storey, D.J., 2016. Understanding the small business sector. Routledge.

Prince, J.B., 2016. Tax for Australians for Dummies. John Wiley & Sons.

Sadiq, K., 2019. Australian Taxation Law Cases 2019. Thomson Reuters.

Storey, D.J., 2016. Understanding the small business sector. Routledge.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.