Analysis of Capital Gains Tax (CGT) and Fringe Benefits Tax (FBT)

VerifiedAdded on 2023/06/07

|12

|2898

|474

Report

AI Summary

This report provides legal advice on Capital Gains Tax (CGT) consequences for FY2018, focusing on pre-CGT assets, disposal of assets, and CGT event A1 under ITAA 1997. It examines the implications of selling a land block, antique bed, painting, shares, and violin, detailing the applicability of CGT based on purchase dates and asset types. The report also discusses Fringe Benefits Tax (FBT) concerning car fringe benefits, loan fringe benefits, and expense fringe benefits provided to an employee, Jasmine, by her employer, Rapid Heat, explaining the calculation of FBT liabilities and available deductions. The analysis includes statutory formulas, benchmark interest rates, and relevant sections of the FBTAA 1986 and ITAA 1997.

Taxation Theory, Practice & Law

[Pick the date]

STUDENT NAME/ID

[Pick the date]

STUDENT NAME/ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

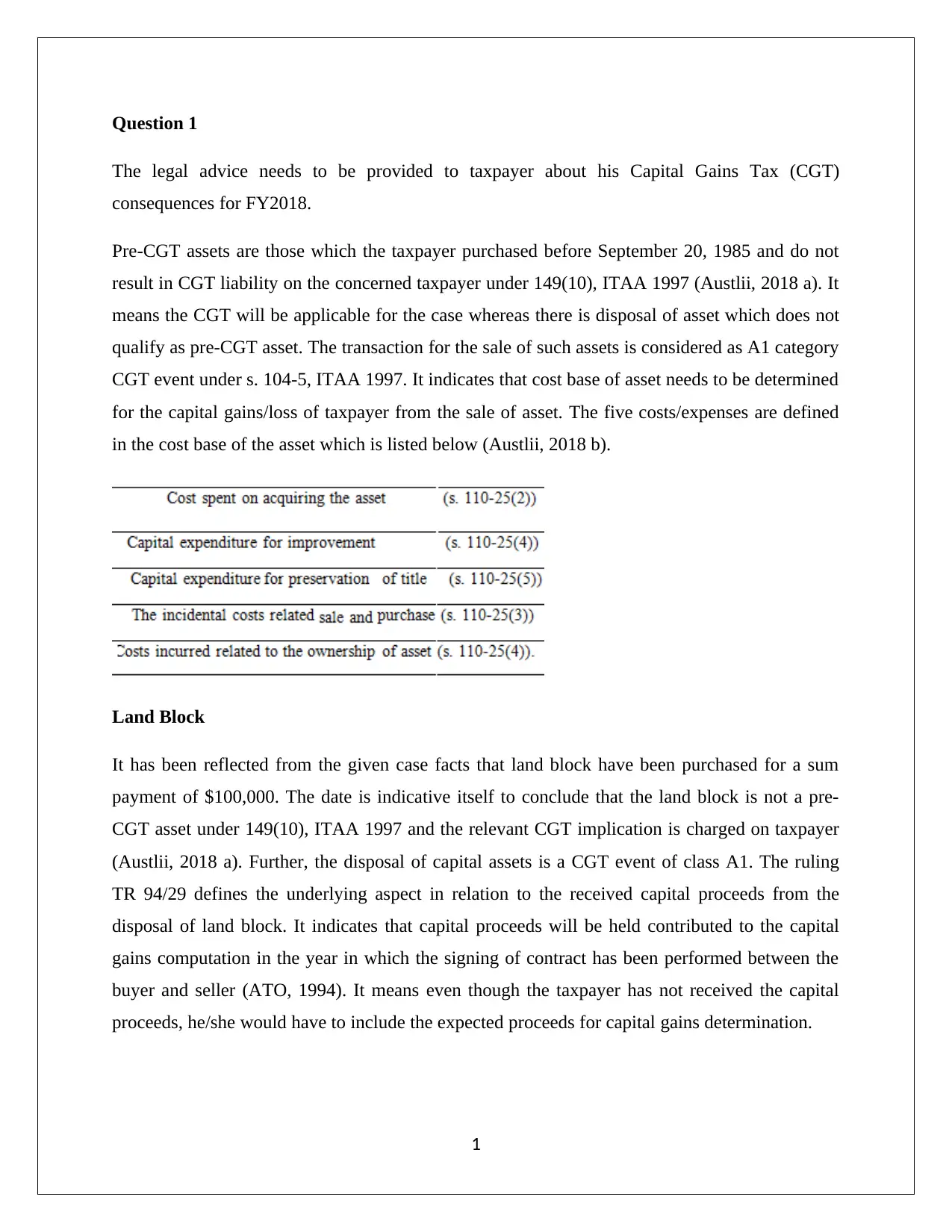

Question 1

The legal advice needs to be provided to taxpayer about his Capital Gains Tax (CGT)

consequences for FY2018.

Pre-CGT assets are those which the taxpayer purchased before September 20, 1985 and do not

result in CGT liability on the concerned taxpayer under 149(10), ITAA 1997 (Austlii, 2018 a). It

means the CGT will be applicable for the case whereas there is disposal of asset which does not

qualify as pre-CGT asset. The transaction for the sale of such assets is considered as A1 category

CGT event under s. 104-5, ITAA 1997. It indicates that cost base of asset needs to be determined

for the capital gains/loss of taxpayer from the sale of asset. The five costs/expenses are defined

in the cost base of the asset which is listed below (Austlii, 2018 b).

Land Block

It has been reflected from the given case facts that land block have been purchased for a sum

payment of $100,000. The date is indicative itself to conclude that the land block is not a pre-

CGT asset under 149(10), ITAA 1997 and the relevant CGT implication is charged on taxpayer

(Austlii, 2018 a). Further, the disposal of capital assets is a CGT event of class A1. The ruling

TR 94/29 defines the underlying aspect in relation to the received capital proceeds from the

disposal of land block. It indicates that capital proceeds will be held contributed to the capital

gains computation in the year in which the signing of contract has been performed between the

buyer and seller (ATO, 1994). It means even though the taxpayer has not received the capital

proceeds, he/she would have to include the expected proceeds for capital gains determination.

1

The legal advice needs to be provided to taxpayer about his Capital Gains Tax (CGT)

consequences for FY2018.

Pre-CGT assets are those which the taxpayer purchased before September 20, 1985 and do not

result in CGT liability on the concerned taxpayer under 149(10), ITAA 1997 (Austlii, 2018 a). It

means the CGT will be applicable for the case whereas there is disposal of asset which does not

qualify as pre-CGT asset. The transaction for the sale of such assets is considered as A1 category

CGT event under s. 104-5, ITAA 1997. It indicates that cost base of asset needs to be determined

for the capital gains/loss of taxpayer from the sale of asset. The five costs/expenses are defined

in the cost base of the asset which is listed below (Austlii, 2018 b).

Land Block

It has been reflected from the given case facts that land block have been purchased for a sum

payment of $100,000. The date is indicative itself to conclude that the land block is not a pre-

CGT asset under 149(10), ITAA 1997 and the relevant CGT implication is charged on taxpayer

(Austlii, 2018 a). Further, the disposal of capital assets is a CGT event of class A1. The ruling

TR 94/29 defines the underlying aspect in relation to the received capital proceeds from the

disposal of land block. It indicates that capital proceeds will be held contributed to the capital

gains computation in the year in which the signing of contract has been performed between the

buyer and seller (ATO, 1994). It means even though the taxpayer has not received the capital

proceeds, he/she would have to include the expected proceeds for capital gains determination.

1

Further, the capital gains from the disposal of land block will be considered as long term capital

gains and is liable for 50% rebate for CGT consequences. The capital gains are long term as the

holding period for this asset has been higher than 1 year (Barkoczy, 2017).

Antique Bed

It has been reflected from the given case facts that antique bed has been purchased for a sum

payment of $3,500 in the year 1986. The date is indicative itself to conclude that the antique bed

is not a pre-CGT asset under 149(10), ITAA 1997 and the relevant CGT implication is charged

on taxpayer (Austlii, 2018 a). Further, the disposal of capital assets is a CGT event of class A1

and therefore, the basic procedure of calculation for capital gains/losses will be adopted which is

used for class A1 event (Barkoczy, 2017). However, it is noteworthy that the antique bed is part

of the collectables and hence, the necessary condition used for treating the collectables for CGT

taxation would be checked.

It is essential that the antique item must be bought at price in excess of $500 for the applicability

of CGT on the capital gains derived from disposal of the asset. Here, the taxpayer bought the

antique bed for $3,500 which is significantly higher than the amount required to satisfy the

necessary condition (Barkoczy, 2017). Hence, CGT implication is charged on her. The capital

expense of $1500has been paid by taxpayer in order to enhance the quality of bed by installing

the interlined mattresses. The carried forwarded loss from the disposal of sculpture has been

adjusted from the current year’s capital gains. Further, the capital gains from the disposal of

antique bed will be considered as long term capital gains and is liable for 50% rebate for CGT

2

gains and is liable for 50% rebate for CGT consequences. The capital gains are long term as the

holding period for this asset has been higher than 1 year (Barkoczy, 2017).

Antique Bed

It has been reflected from the given case facts that antique bed has been purchased for a sum

payment of $3,500 in the year 1986. The date is indicative itself to conclude that the antique bed

is not a pre-CGT asset under 149(10), ITAA 1997 and the relevant CGT implication is charged

on taxpayer (Austlii, 2018 a). Further, the disposal of capital assets is a CGT event of class A1

and therefore, the basic procedure of calculation for capital gains/losses will be adopted which is

used for class A1 event (Barkoczy, 2017). However, it is noteworthy that the antique bed is part

of the collectables and hence, the necessary condition used for treating the collectables for CGT

taxation would be checked.

It is essential that the antique item must be bought at price in excess of $500 for the applicability

of CGT on the capital gains derived from disposal of the asset. Here, the taxpayer bought the

antique bed for $3,500 which is significantly higher than the amount required to satisfy the

necessary condition (Barkoczy, 2017). Hence, CGT implication is charged on her. The capital

expense of $1500has been paid by taxpayer in order to enhance the quality of bed by installing

the interlined mattresses. The carried forwarded loss from the disposal of sculpture has been

adjusted from the current year’s capital gains. Further, the capital gains from the disposal of

antique bed will be considered as long term capital gains and is liable for 50% rebate for CGT

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

consequences. The capital gains are long term as the holding period for this asset has been higher

than 1 year (Gilders, et. al., 2015).

Painting

The disposal of the famous painting by the taxpayer does not create any CGT implication on her

as the aspect regarding the purchasing date of the painting indicates that taxpayer has been

purchased before September 20, 1985. Therefore, CGT implication is exempted as painting

belongs to category of pre-CGT asset which are immune to CGT taxation as per the highlights of

s. 149-10, ITAA 1997 (Austlii, 2018 a).

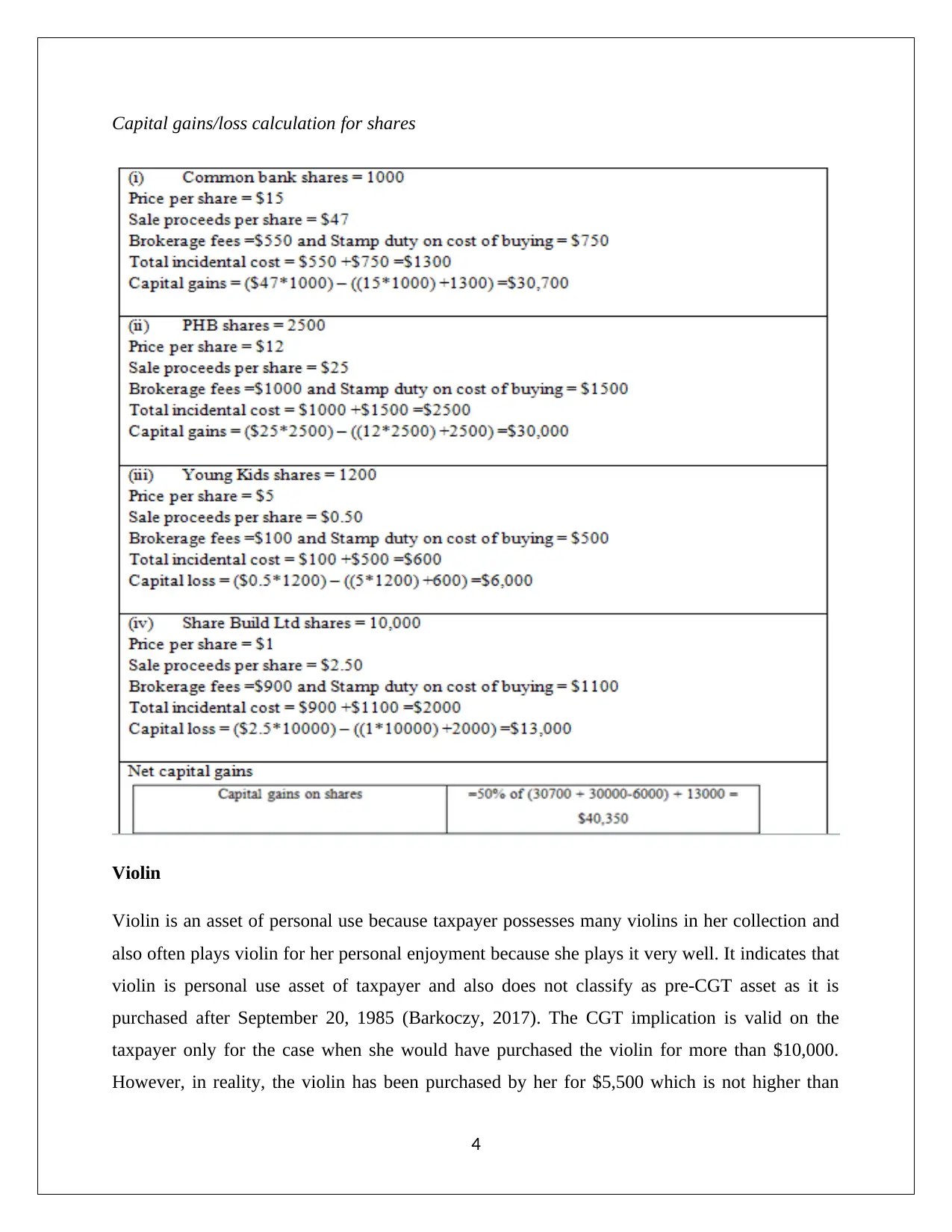

Shares

It is evident from that all the shares have been purchased by the taxpayer after September 20,

1985 which implies that CGT will be imposed because the shares are not belonged to pre-CGT

asset under 149(10), ITAA 1997 (Krever, 2017). Moreover, it is apparent that holding period for

the initial three assets tends to exceed one year and thus, 50% rebate will be applicable on the

long term capital gains and the fourth shares does not show holding period higher than a year and

hence, rebate will not be applicable on the short term capital gains.

3

than 1 year (Gilders, et. al., 2015).

Painting

The disposal of the famous painting by the taxpayer does not create any CGT implication on her

as the aspect regarding the purchasing date of the painting indicates that taxpayer has been

purchased before September 20, 1985. Therefore, CGT implication is exempted as painting

belongs to category of pre-CGT asset which are immune to CGT taxation as per the highlights of

s. 149-10, ITAA 1997 (Austlii, 2018 a).

Shares

It is evident from that all the shares have been purchased by the taxpayer after September 20,

1985 which implies that CGT will be imposed because the shares are not belonged to pre-CGT

asset under 149(10), ITAA 1997 (Krever, 2017). Moreover, it is apparent that holding period for

the initial three assets tends to exceed one year and thus, 50% rebate will be applicable on the

long term capital gains and the fourth shares does not show holding period higher than a year and

hence, rebate will not be applicable on the short term capital gains.

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Capital gains/loss calculation for shares

Violin

Violin is an asset of personal use because taxpayer possesses many violins in her collection and

also often plays violin for her personal enjoyment because she plays it very well. It indicates that

violin is personal use asset of taxpayer and also does not classify as pre-CGT asset as it is

purchased after September 20, 1985 (Barkoczy, 2017). The CGT implication is valid on the

taxpayer only for the case when she would have purchased the violin for more than $10,000.

However, in reality, the violin has been purchased by her for $5,500 which is not higher than

4

Violin

Violin is an asset of personal use because taxpayer possesses many violins in her collection and

also often plays violin for her personal enjoyment because she plays it very well. It indicates that

violin is personal use asset of taxpayer and also does not classify as pre-CGT asset as it is

purchased after September 20, 1985 (Barkoczy, 2017). The CGT implication is valid on the

taxpayer only for the case when she would have purchased the violin for more than $10,000.

However, in reality, the violin has been purchased by her for $5,500 which is not higher than

4

$10,000 and thus, the necessary condition is not satiated and hence, CGT implication will not

have occurred for taxpayer for this case.

Total Capital Gains subject to CGT

It has been resulted from the disposal of block of land, share, and antique bed.

Question 2

(a) Benefits of personal nature of employee which are provided by the employer in kind and not

cash are termed as fringe benefits. The taxation of such fringe benefits is described in details

in “Fringe Benefits Tax Assessment Act 1986.” One of the main characteristic of Fringe

Benefits Tax (FBT) is that the tax burden is only applicable on the employer and the

employee despite being the person who has utilized the fringe benefit is free from FBT

liabilities. The various factors related to three fringe benefits which are provided to Jasmine

by employer Rapid Heat are discussed below.

Car Fringe Benefit

The imperative condition for the car fringe benefits is defined in s. 7 FBTAA 1986 which refers

that employer should extend the car availability to employee for the utilization of personal nature

purposes. Further, it is noteworthy that car fringe benefits will not be given to employee when

the employer has given a car to employee only for office related travelling. In such cases, the

employer is not having any liability of FBT as there is no car fringe benefit (Nethercott,

Richardson and Devos, 2016).

Rapid Heat or Rapid Heat Pty Ltd: Employer

Jasmine: Employee

Company has issued a car to Jasmine with the consent that Jasmine can utilize the given car to

complete the personal nature work. Also, the car is being available to Jasmine on the day on

which the car is issued to her by Rapid Heat (May 1, 2017). FBT liability does not rise on

5

have occurred for taxpayer for this case.

Total Capital Gains subject to CGT

It has been resulted from the disposal of block of land, share, and antique bed.

Question 2

(a) Benefits of personal nature of employee which are provided by the employer in kind and not

cash are termed as fringe benefits. The taxation of such fringe benefits is described in details

in “Fringe Benefits Tax Assessment Act 1986.” One of the main characteristic of Fringe

Benefits Tax (FBT) is that the tax burden is only applicable on the employer and the

employee despite being the person who has utilized the fringe benefit is free from FBT

liabilities. The various factors related to three fringe benefits which are provided to Jasmine

by employer Rapid Heat are discussed below.

Car Fringe Benefit

The imperative condition for the car fringe benefits is defined in s. 7 FBTAA 1986 which refers

that employer should extend the car availability to employee for the utilization of personal nature

purposes. Further, it is noteworthy that car fringe benefits will not be given to employee when

the employer has given a car to employee only for office related travelling. In such cases, the

employer is not having any liability of FBT as there is no car fringe benefit (Nethercott,

Richardson and Devos, 2016).

Rapid Heat or Rapid Heat Pty Ltd: Employer

Jasmine: Employee

Company has issued a car to Jasmine with the consent that Jasmine can utilize the given car to

complete the personal nature work. Also, the car is being available to Jasmine on the day on

which the car is issued to her by Rapid Heat (May 1, 2017). FBT liability does not rise on

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Jasmine and all the FBT liability will be charged on Rapid Heat only. Therefore, the objective

here is to find the net FBT liability that needs to be satisfied by Rapid Heat on the account of car

fringe benefits. As the provisions of s. 9 FBTAA 1986 defines that statutory formula should be

used to find the net taxable value of car fringe benefits based on the below highlighted factors

(Woellner, 2017).

The capital value of car is a function of purchased price of car and the incurred expenses on

minor repairing which are paid by the employer. Deduct minor repair expense from

acquisition price of car so as to determine the capital value.

Further, the car is said to be available to employee even if the car is out for maintenance

or/and for minor repairing. This period is 5 days when car is left at garage for minor

repairing and would not be removed from the net available days of car.

Similarly, the car will be said available for use even if the car is parked at the parking area of

the employees or else the employee has parked it at the airport and went out of the city. This

period is 10 days in present case which would not be removed from the net available days of

car (Sadiq, et.al., 2015).

The available days of utilization will be the time period starting from the day when the

employee has received the car to the assessment years end day which is March 31, 2018 for

the given circumstances. The total days between these periods are 335 days.

GST is applied on car and thus, the gross up factor is 2.0808 (TYPE I goods) considering the

tax year 2017/2018.

The net FBT payable for car fringe benefits will be. 47% which is the applicable FBT rate for

tax year 2018 and it is a variable that might change every year by ATO.

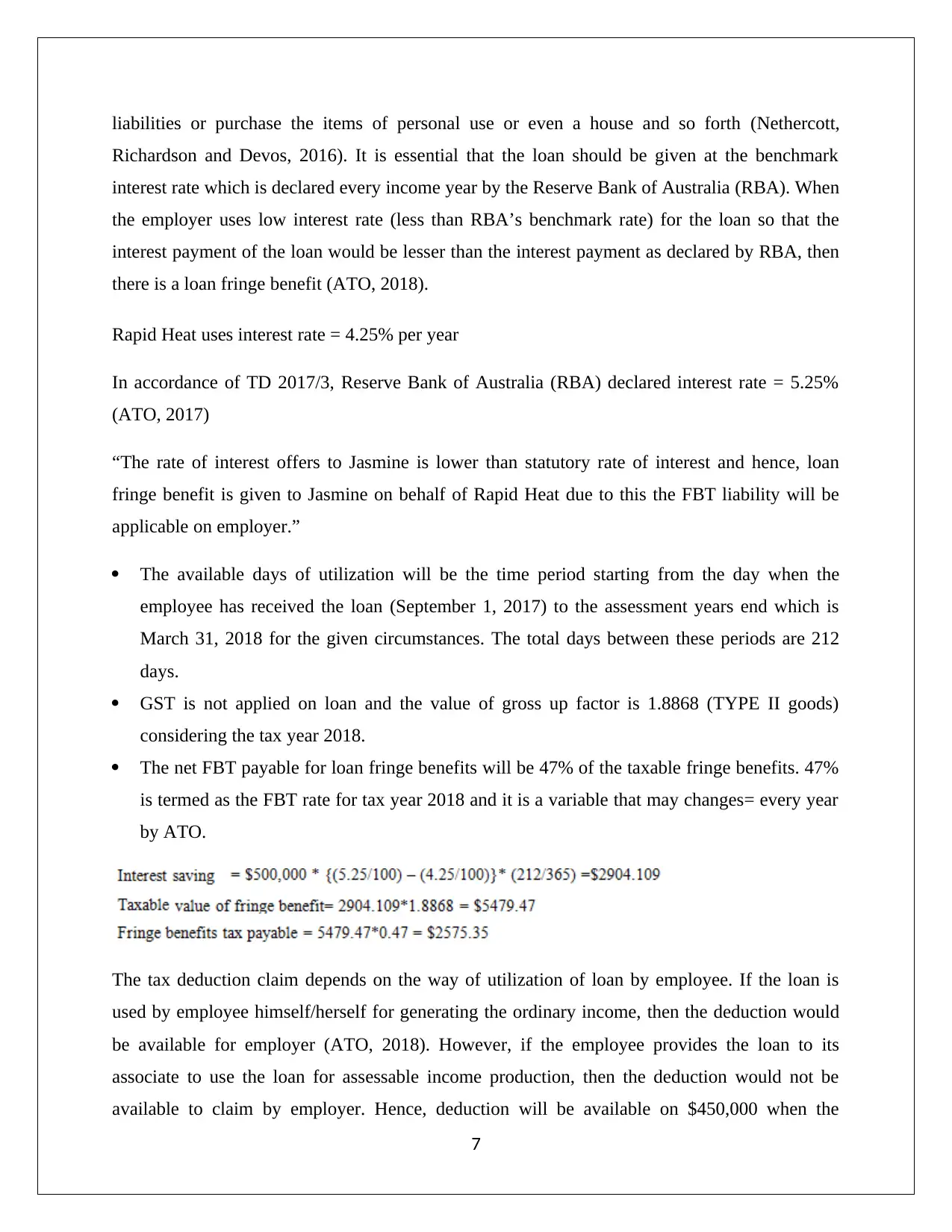

Loan Fringe Benefit

It is considered one of the common business practice in which the employer offers loan to

employee in order to provide them financial help so that the employee can complete the personal

6

here is to find the net FBT liability that needs to be satisfied by Rapid Heat on the account of car

fringe benefits. As the provisions of s. 9 FBTAA 1986 defines that statutory formula should be

used to find the net taxable value of car fringe benefits based on the below highlighted factors

(Woellner, 2017).

The capital value of car is a function of purchased price of car and the incurred expenses on

minor repairing which are paid by the employer. Deduct minor repair expense from

acquisition price of car so as to determine the capital value.

Further, the car is said to be available to employee even if the car is out for maintenance

or/and for minor repairing. This period is 5 days when car is left at garage for minor

repairing and would not be removed from the net available days of car.

Similarly, the car will be said available for use even if the car is parked at the parking area of

the employees or else the employee has parked it at the airport and went out of the city. This

period is 10 days in present case which would not be removed from the net available days of

car (Sadiq, et.al., 2015).

The available days of utilization will be the time period starting from the day when the

employee has received the car to the assessment years end day which is March 31, 2018 for

the given circumstances. The total days between these periods are 335 days.

GST is applied on car and thus, the gross up factor is 2.0808 (TYPE I goods) considering the

tax year 2017/2018.

The net FBT payable for car fringe benefits will be. 47% which is the applicable FBT rate for

tax year 2018 and it is a variable that might change every year by ATO.

Loan Fringe Benefit

It is considered one of the common business practice in which the employer offers loan to

employee in order to provide them financial help so that the employee can complete the personal

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

liabilities or purchase the items of personal use or even a house and so forth (Nethercott,

Richardson and Devos, 2016). It is essential that the loan should be given at the benchmark

interest rate which is declared every income year by the Reserve Bank of Australia (RBA). When

the employer uses low interest rate (less than RBA’s benchmark rate) for the loan so that the

interest payment of the loan would be lesser than the interest payment as declared by RBA, then

there is a loan fringe benefit (ATO, 2018).

Rapid Heat uses interest rate = 4.25% per year

In accordance of TD 2017/3, Reserve Bank of Australia (RBA) declared interest rate = 5.25%

(ATO, 2017)

“The rate of interest offers to Jasmine is lower than statutory rate of interest and hence, loan

fringe benefit is given to Jasmine on behalf of Rapid Heat due to this the FBT liability will be

applicable on employer.”

The available days of utilization will be the time period starting from the day when the

employee has received the loan (September 1, 2017) to the assessment years end which is

March 31, 2018 for the given circumstances. The total days between these periods are 212

days.

GST is not applied on loan and the value of gross up factor is 1.8868 (TYPE II goods)

considering the tax year 2018.

The net FBT payable for loan fringe benefits will be 47% of the taxable fringe benefits. 47%

is termed as the FBT rate for tax year 2018 and it is a variable that may changes= every year

by ATO.

The tax deduction claim depends on the way of utilization of loan by employee. If the loan is

used by employee himself/herself for generating the ordinary income, then the deduction would

be available for employer (ATO, 2018). However, if the employee provides the loan to its

associate to use the loan for assessable income production, then the deduction would not be

available to claim by employer. Hence, deduction will be available on $450,000 when the

7

Richardson and Devos, 2016). It is essential that the loan should be given at the benchmark

interest rate which is declared every income year by the Reserve Bank of Australia (RBA). When

the employer uses low interest rate (less than RBA’s benchmark rate) for the loan so that the

interest payment of the loan would be lesser than the interest payment as declared by RBA, then

there is a loan fringe benefit (ATO, 2018).

Rapid Heat uses interest rate = 4.25% per year

In accordance of TD 2017/3, Reserve Bank of Australia (RBA) declared interest rate = 5.25%

(ATO, 2017)

“The rate of interest offers to Jasmine is lower than statutory rate of interest and hence, loan

fringe benefit is given to Jasmine on behalf of Rapid Heat due to this the FBT liability will be

applicable on employer.”

The available days of utilization will be the time period starting from the day when the

employee has received the loan (September 1, 2017) to the assessment years end which is

March 31, 2018 for the given circumstances. The total days between these periods are 212

days.

GST is not applied on loan and the value of gross up factor is 1.8868 (TYPE II goods)

considering the tax year 2018.

The net FBT payable for loan fringe benefits will be 47% of the taxable fringe benefits. 47%

is termed as the FBT rate for tax year 2018 and it is a variable that may changes= every year

by ATO.

The tax deduction claim depends on the way of utilization of loan by employee. If the loan is

used by employee himself/herself for generating the ordinary income, then the deduction would

be available for employer (ATO, 2018). However, if the employee provides the loan to its

associate to use the loan for assessable income production, then the deduction would not be

available to claim by employer. Hence, deduction will be available on $450,000 when the

7

holiday home acquired by Jasmine will generate ordinary income in terms of rent income while

the amount which she has offered to her husband will not considered for deduction even through

there is generation of dividend income which is assessable as per s. 6-5 ITAA 1997 (Woellner,

2017).

Expense Fringe Benefit

Expense fringe benefit is given to employee when there is payment of personal expense of

employee by the employer. When, the expenses are borne by employer in their own product

while extending it to the employee, then it is an internal expense fringe benefit (Barkoczy, 2017).

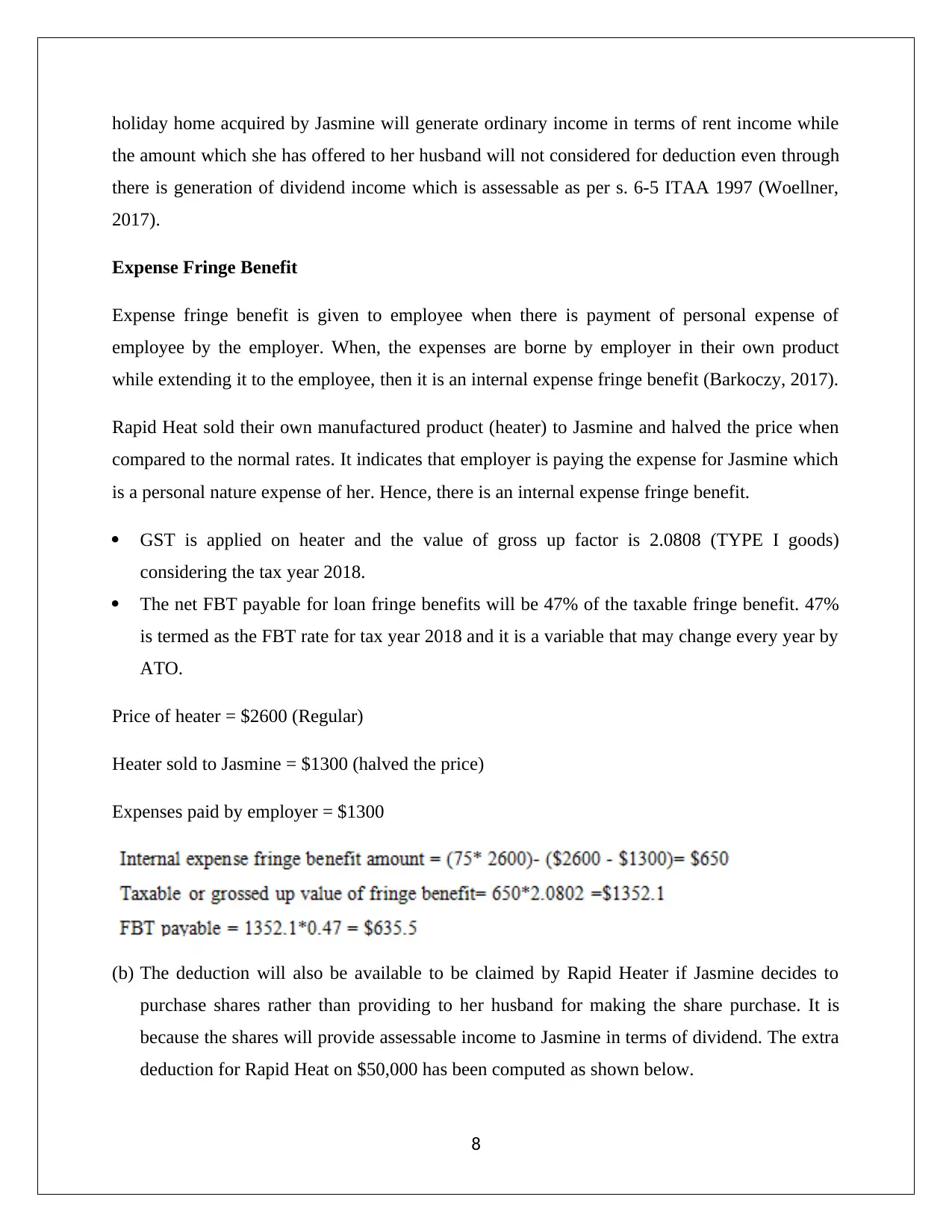

Rapid Heat sold their own manufactured product (heater) to Jasmine and halved the price when

compared to the normal rates. It indicates that employer is paying the expense for Jasmine which

is a personal nature expense of her. Hence, there is an internal expense fringe benefit.

GST is applied on heater and the value of gross up factor is 2.0808 (TYPE I goods)

considering the tax year 2018.

The net FBT payable for loan fringe benefits will be 47% of the taxable fringe benefit. 47%

is termed as the FBT rate for tax year 2018 and it is a variable that may change every year by

ATO.

Price of heater = $2600 (Regular)

Heater sold to Jasmine = $1300 (halved the price)

Expenses paid by employer = $1300

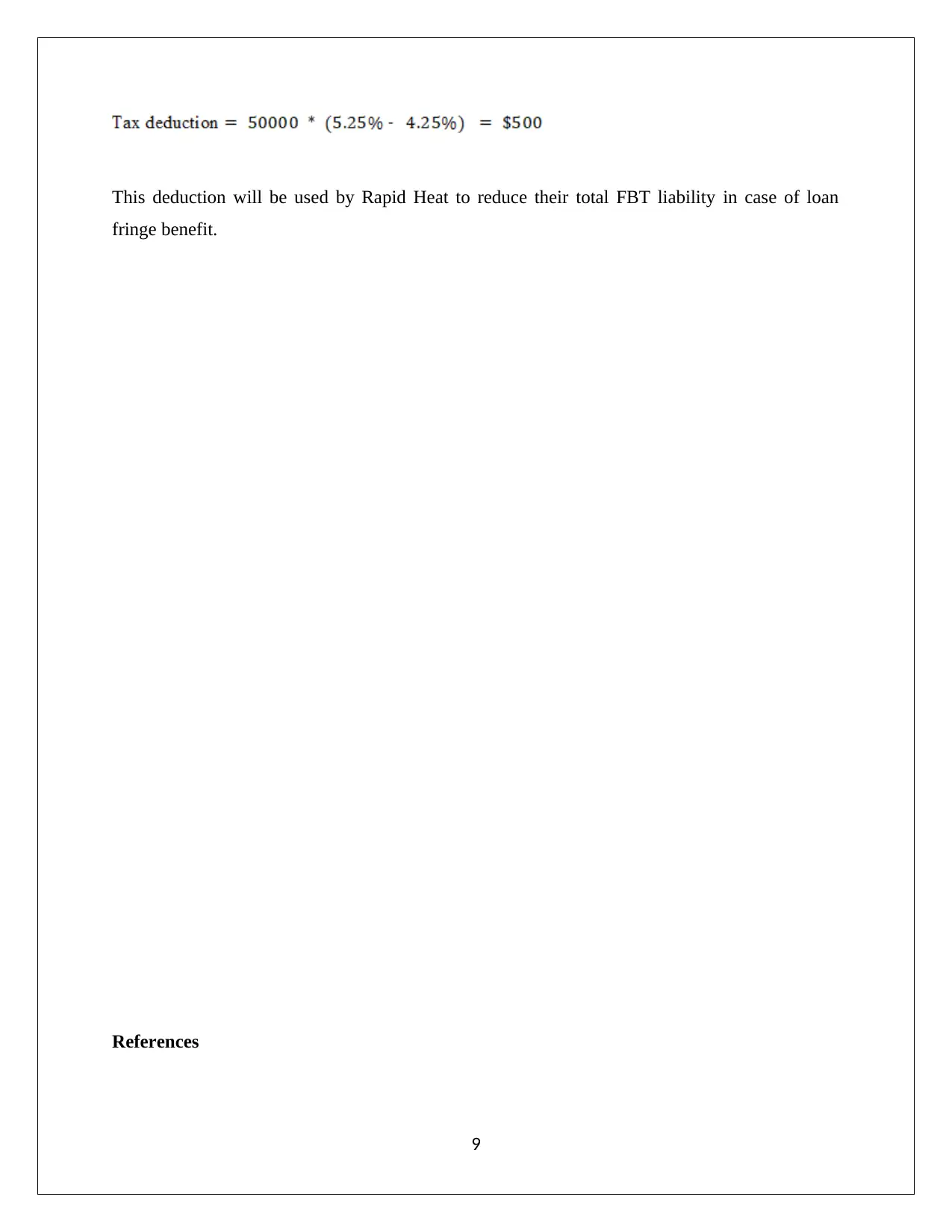

(b) The deduction will also be available to be claimed by Rapid Heater if Jasmine decides to

purchase shares rather than providing to her husband for making the share purchase. It is

because the shares will provide assessable income to Jasmine in terms of dividend. The extra

deduction for Rapid Heat on $50,000 has been computed as shown below.

8

the amount which she has offered to her husband will not considered for deduction even through

there is generation of dividend income which is assessable as per s. 6-5 ITAA 1997 (Woellner,

2017).

Expense Fringe Benefit

Expense fringe benefit is given to employee when there is payment of personal expense of

employee by the employer. When, the expenses are borne by employer in their own product

while extending it to the employee, then it is an internal expense fringe benefit (Barkoczy, 2017).

Rapid Heat sold their own manufactured product (heater) to Jasmine and halved the price when

compared to the normal rates. It indicates that employer is paying the expense for Jasmine which

is a personal nature expense of her. Hence, there is an internal expense fringe benefit.

GST is applied on heater and the value of gross up factor is 2.0808 (TYPE I goods)

considering the tax year 2018.

The net FBT payable for loan fringe benefits will be 47% of the taxable fringe benefit. 47%

is termed as the FBT rate for tax year 2018 and it is a variable that may change every year by

ATO.

Price of heater = $2600 (Regular)

Heater sold to Jasmine = $1300 (halved the price)

Expenses paid by employer = $1300

(b) The deduction will also be available to be claimed by Rapid Heater if Jasmine decides to

purchase shares rather than providing to her husband for making the share purchase. It is

because the shares will provide assessable income to Jasmine in terms of dividend. The extra

deduction for Rapid Heat on $50,000 has been computed as shown below.

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

This deduction will be used by Rapid Heat to reduce their total FBT liability in case of loan

fringe benefit.

References

9

fringe benefit.

References

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ATO, (1994) Taxation Ruling –TR 94/29 [Online]. Available at: Income tax: capital gains tax

consequences of a contract for the sale of land falling through.

https://www.ato.gov.au/law/view/document?DocID=TXR/TR9429/NAT/ATO/

00001&PiT=99991231235958 (Accessed: 24 September 2018)

ATO, (2017) Taxation Determination –TD 2017/3 [Online].

http://law.ato.gov.au/atolaw/view.htm?docid=%22TXD%2FTD20173%2FNAT%2FATO

%2F00001%22 (Accessed: 24 September 2018)

ATO, (2018) Loan Fringe Benefits

https://www.ato.gov.au/General/Fringe-benefits-tax-(FBT)/Types-of-fringe-benefits/Loan-

fringe-benefits/ (Accessed: 24 September 2018)

Austlii, (2018 a) Income Tax Assessment Act 1997- SECT 149.10 [Online]. Available at:

http://www5.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s149.10.html (Accessed: 24

September 2018)

Austlii, (2018 b) Income Tax Assessment Act 1997- SECT 110.25.General Rules About Cost

Base [Online]. Available at:

http://www5.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s104.5.html (Accessed: 24

September 2018)

Barkoczy, S. (2017) Foundation of Taxation Law 2017. 9th ed. Sydney: Oxford University Press.

Deutsch, R., Freizer, M., Fullerton, I., Hanley, P., and Snape, T. (2015) Australian tax handbook.

8th ed. Pymont: Thomson Reuters.

Gilders, F., Taylor, J., Walpole, M., Burton, M. and Ciro, T. (2016) Understanding taxation law

2016. 9th ed. Sydney: LexisNexis/Butterworths.

Krever, R. (2016) Australian Taxation Law Cases 2017. 2nd ed. Brisbane: THOMSON

LAWBOOK Company.

Nethercott, L., Richardson, G., & Devos, K. (2016) Australian Taxation Study Manual 2016. 8th

ed. Sydney: Oxford University Press.

10

consequences of a contract for the sale of land falling through.

https://www.ato.gov.au/law/view/document?DocID=TXR/TR9429/NAT/ATO/

00001&PiT=99991231235958 (Accessed: 24 September 2018)

ATO, (2017) Taxation Determination –TD 2017/3 [Online].

http://law.ato.gov.au/atolaw/view.htm?docid=%22TXD%2FTD20173%2FNAT%2FATO

%2F00001%22 (Accessed: 24 September 2018)

ATO, (2018) Loan Fringe Benefits

https://www.ato.gov.au/General/Fringe-benefits-tax-(FBT)/Types-of-fringe-benefits/Loan-

fringe-benefits/ (Accessed: 24 September 2018)

Austlii, (2018 a) Income Tax Assessment Act 1997- SECT 149.10 [Online]. Available at:

http://www5.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s149.10.html (Accessed: 24

September 2018)

Austlii, (2018 b) Income Tax Assessment Act 1997- SECT 110.25.General Rules About Cost

Base [Online]. Available at:

http://www5.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s104.5.html (Accessed: 24

September 2018)

Barkoczy, S. (2017) Foundation of Taxation Law 2017. 9th ed. Sydney: Oxford University Press.

Deutsch, R., Freizer, M., Fullerton, I., Hanley, P., and Snape, T. (2015) Australian tax handbook.

8th ed. Pymont: Thomson Reuters.

Gilders, F., Taylor, J., Walpole, M., Burton, M. and Ciro, T. (2016) Understanding taxation law

2016. 9th ed. Sydney: LexisNexis/Butterworths.

Krever, R. (2016) Australian Taxation Law Cases 2017. 2nd ed. Brisbane: THOMSON

LAWBOOK Company.

Nethercott, L., Richardson, G., & Devos, K. (2016) Australian Taxation Study Manual 2016. 8th

ed. Sydney: Oxford University Press.

10

Reuters, T. (2017) Australian Tax Legislation (2017). 4th ed. Sydney. THOMSON REUTERS.

Sadiq, K., Coleman, C., Hanegbi, R., Jogarajan, S., Krever, R., Obst, W., and Ting, A.

(2015) Principles of Taxation Law 2015. 7th ed. Pymont: Thomson Reuters.

Woellner, R., Barkoczy, S., Murphy, S. and Pinto, D. (2017). Australian Taxation Law Select

Legislation and Commentary Curtin 2017. 2nd ed. Sydney: Oxford University Press Australia.

11

Sadiq, K., Coleman, C., Hanegbi, R., Jogarajan, S., Krever, R., Obst, W., and Ting, A.

(2015) Principles of Taxation Law 2015. 7th ed. Pymont: Thomson Reuters.

Woellner, R., Barkoczy, S., Murphy, S. and Pinto, D. (2017). Australian Taxation Law Select

Legislation and Commentary Curtin 2017. 2nd ed. Sydney: Oxford University Press Australia.

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.