HI6028 Taxation Law: Capital Gains and Fringe Benefit Tax Analysis

VerifiedAdded on 2023/06/08

|16

|3838

|364

Report

AI Summary

This report provides a detailed analysis of capital gains tax (CGT) and fringe benefit tax (FBT) based on a hypothetical client scenario. It addresses various CGT events related to the sale of vacant land, loss of an antique bed, sale of a painting, disposal of shares, and sale of a violin, determining the tax implications for each. Furthermore, the report examines the FBT liabilities for Rapid Heat Pty Ltd, considering car fringe benefits, expense payment fringe benefits, and car parking fringe benefits, ultimately calculating the net capital gains and FBT obligations for the relevant tax year. Desklib provides a platform for students to access similar solved assignments and past papers.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to Question 2:................................................................................................................5

Answer to question 2 B:...........................................................................................................10

References:...............................................................................................................................11

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to Question 2:................................................................................................................5

Answer to question 2 B:...........................................................................................................10

References:...............................................................................................................................11

2TAXATION LAW

Answer to question 1:

Introduction:

As stated in “section 102-20, ITAA 1997” capital gains or loss only happens due to

the CGT event. Referring to “section 104-10 (1), ITAA 1997” CGT event A1 happens when

the when the asset is disposed (Stiglitz and Rosengard 2015). The commissioner of taxation

in “FC of T v Sara Lee Household” expressed its opinion by stating that CGT event is

necessary when a contract is entered into by the taxpayer. Capital gains tax cannot be

regarded as the separate system of taxation, instead it forms the part of the income tax

regimes of the taxpayer.

Answer to A: Sale of Vacant Land:

Vacant land that is purchased by the taxpayer for the private or investment propose is

treated as the capital asset and will attract capital gains tax upon the disposal of vacant land

(Becker, Reimer and Rust 2015). The evidences suggest from the present situation that an

agreement was reached by the taxpayer for disposal of vacant land. The cost base of land was

$100,000 with other expenses such as water, council rate etc. was incurred by the taxpayer

that amounted to $20,000.

The interpretative view of ATO makes it clear that vacant land is treated is similar to

any other capital asset for CGT purpose. According to the ATO the holders of vacant land

should maintain the record of date when the land was acquired and expenses incurred while

acquiring the land (Faccio and Xu 2015). The expenses include the council rates and

insurance on loan. Case facts obtained reveals that outlays on water, local council rates and

land taxes were incurred during the period of ownership. The ATO does not allows claiming

deductions for such expenses however they can be added up with the cost base of vacant land

to determine the CGT while disposing the land.

Answer to question 1:

Introduction:

As stated in “section 102-20, ITAA 1997” capital gains or loss only happens due to

the CGT event. Referring to “section 104-10 (1), ITAA 1997” CGT event A1 happens when

the when the asset is disposed (Stiglitz and Rosengard 2015). The commissioner of taxation

in “FC of T v Sara Lee Household” expressed its opinion by stating that CGT event is

necessary when a contract is entered into by the taxpayer. Capital gains tax cannot be

regarded as the separate system of taxation, instead it forms the part of the income tax

regimes of the taxpayer.

Answer to A: Sale of Vacant Land:

Vacant land that is purchased by the taxpayer for the private or investment propose is

treated as the capital asset and will attract capital gains tax upon the disposal of vacant land

(Becker, Reimer and Rust 2015). The evidences suggest from the present situation that an

agreement was reached by the taxpayer for disposal of vacant land. The cost base of land was

$100,000 with other expenses such as water, council rate etc. was incurred by the taxpayer

that amounted to $20,000.

The interpretative view of ATO makes it clear that vacant land is treated is similar to

any other capital asset for CGT purpose. According to the ATO the holders of vacant land

should maintain the record of date when the land was acquired and expenses incurred while

acquiring the land (Faccio and Xu 2015). The expenses include the council rates and

insurance on loan. Case facts obtained reveals that outlays on water, local council rates and

land taxes were incurred during the period of ownership. The ATO does not allows claiming

deductions for such expenses however they can be added up with the cost base of vacant land

to determine the CGT while disposing the land.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

Answer to B: Antique Bed:

The explanation of collectables is given under “section 108-10(2) of the ITAA

1997”. As per “section 108-10(2), ITAA 1997” collectables refers to the artwork, jewellery,

antiques or coin that are kept by the taxpayer for their own use and satisfaction. There are

certain rules that is applicable on collectables (Tan, Braithwaite and Reinhart 2016). Capital

gains and losses made from collectables that costs less than $500 will be excluded. The case

study provides that the taxpayer held an antique bed but the antique bed was stole from the

house of taxpayer. In the insurance list the antique bed did not formed the part of the taxpayer

specified items which resulted the insurance company in paying the taxpayer a sum of

$11,000.

CGT event C1 takes place under “section 104-20(1), ITAA 1997” when the asset is

lost or destroyed that is owned to the taxpayer (Snape and De Souza 2016). Receipt of

compensation from such asset give rise to CGT event C1. Similarly the compensation

received by the taxpayer from the insurance company relating to the loss of antique bed gave

rise to CGT event C1.

Answer to C: Painting

Capital gains tax is usually applied on the assets that is acquired or on after 20

September 1985. It is worth mentioning that Pre-CGT and Post CGT is generally used to

refer the assets that is obtained or events that taking place before or after that date (Robin

2017). For an individual taxpayer it is necessary to work out the capital proceeds from the

CGT events. The primary step of ascertaining whether the transaction will attract CGT is to

ascertain the whether the CGT event has taken place.

Answer to B: Antique Bed:

The explanation of collectables is given under “section 108-10(2) of the ITAA

1997”. As per “section 108-10(2), ITAA 1997” collectables refers to the artwork, jewellery,

antiques or coin that are kept by the taxpayer for their own use and satisfaction. There are

certain rules that is applicable on collectables (Tan, Braithwaite and Reinhart 2016). Capital

gains and losses made from collectables that costs less than $500 will be excluded. The case

study provides that the taxpayer held an antique bed but the antique bed was stole from the

house of taxpayer. In the insurance list the antique bed did not formed the part of the taxpayer

specified items which resulted the insurance company in paying the taxpayer a sum of

$11,000.

CGT event C1 takes place under “section 104-20(1), ITAA 1997” when the asset is

lost or destroyed that is owned to the taxpayer (Snape and De Souza 2016). Receipt of

compensation from such asset give rise to CGT event C1. Similarly the compensation

received by the taxpayer from the insurance company relating to the loss of antique bed gave

rise to CGT event C1.

Answer to C: Painting

Capital gains tax is usually applied on the assets that is acquired or on after 20

September 1985. It is worth mentioning that Pre-CGT and Post CGT is generally used to

refer the assets that is obtained or events that taking place before or after that date (Robin

2017). For an individual taxpayer it is necessary to work out the capital proceeds from the

CGT events. The primary step of ascertaining whether the transaction will attract CGT is to

ascertain the whether the CGT event has taken place.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

The painting was bought by the taxpayer from the well-known Australian Artist on 2nd

May 1985 for the sum of $2000. With the rise in the value of the painting it was sold for

$125,000 in auction on 3rd April in current tax year. The painting can be classified as the Pre-

CGT asset because it was acquired before the introduction of CGT on 20th September 1985

(Maley 2018). Therefore, the capital gains made from the paintings will be exempted from

CGT.

Answer to D: Shares:

Shares that are held by the taxpayer in company are treated as CGT asset. On the

happening of CGT event, capital gains tax is applied to determine the net capital gains or

shares from the sale of shares (Johnston 2017). As understood the taxpayer reported capital

gains from the disposal of PHB Ltd shares, Build Ltd and Common Ltd shares. But also

reports net capital loss from the sale of Young Kinds shares. The capital loss can be offset

against the capital gains made from the sale of shares.

Answer to E: Violin:

The definition of personal use asset stated under “section 108-20 (2)” refers to the

asset that are non-collectables. These personal use assets are held for the personal enjoyment

and usage by the taxpayer. They include the electrical goods, household items, furniture and

boats. The personal use assets under “section 108-20 (3)” does not include the land buildings

(Chardon, Brimble and Freudenberg 2017). An explanation stated under “section 118-10

(3)” states that capital gains derived from personal use asset that has the cost of $10,000 or

less is excluded from CGT.

The cost base of the violin that was kept for the taxpayer personal use amounted to

$5,500. The violin was later sold for $12,000. Mentioning the elucidation of “section 118-10

(3)” capital gains derived from personal use asset that has the cost of $10,000 or less is

The painting was bought by the taxpayer from the well-known Australian Artist on 2nd

May 1985 for the sum of $2000. With the rise in the value of the painting it was sold for

$125,000 in auction on 3rd April in current tax year. The painting can be classified as the Pre-

CGT asset because it was acquired before the introduction of CGT on 20th September 1985

(Maley 2018). Therefore, the capital gains made from the paintings will be exempted from

CGT.

Answer to D: Shares:

Shares that are held by the taxpayer in company are treated as CGT asset. On the

happening of CGT event, capital gains tax is applied to determine the net capital gains or

shares from the sale of shares (Johnston 2017). As understood the taxpayer reported capital

gains from the disposal of PHB Ltd shares, Build Ltd and Common Ltd shares. But also

reports net capital loss from the sale of Young Kinds shares. The capital loss can be offset

against the capital gains made from the sale of shares.

Answer to E: Violin:

The definition of personal use asset stated under “section 108-20 (2)” refers to the

asset that are non-collectables. These personal use assets are held for the personal enjoyment

and usage by the taxpayer. They include the electrical goods, household items, furniture and

boats. The personal use assets under “section 108-20 (3)” does not include the land buildings

(Chardon, Brimble and Freudenberg 2017). An explanation stated under “section 118-10

(3)” states that capital gains derived from personal use asset that has the cost of $10,000 or

less is excluded from CGT.

The cost base of the violin that was kept for the taxpayer personal use amounted to

$5,500. The violin was later sold for $12,000. Mentioning the elucidation of “section 118-10

(3)” capital gains derived from personal use asset that has the cost of $10,000 or less is

5TAXATION LAW

excluded from CGT (Barnes 2018). Hence, capital gains made from sale of violin should be

disregarded by the taxpayer.

excluded from CGT (Barnes 2018). Hence, capital gains made from sale of violin should be

disregarded by the taxpayer.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

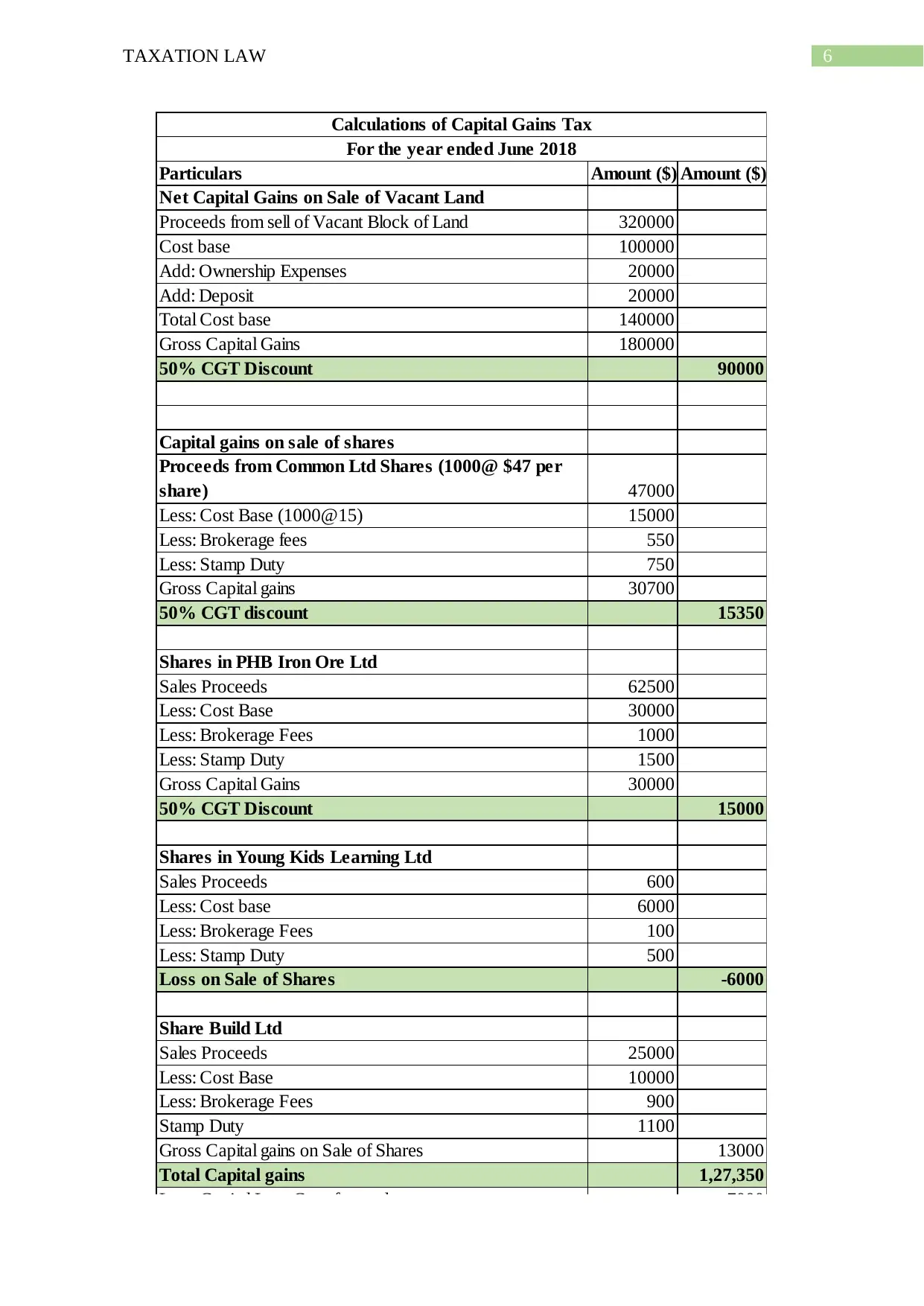

Particulars Amount ($) Amount ($)

Net Capital Gains on Sale of Vacant Land

Proceeds from sell of Vacant Block of Land 320000

Cost base 100000

Add: Ownership Expenses 20000

Add: Deposit 20000

Total Cost base 140000

Gross Capital Gains 180000

50% CGT Discount 90000

Capital gains on sale of shares

Proceeds from Common Ltd Shares (1000@ $47 per

share) 47000

Less: Cost Base (1000@15) 15000

Less: Brokerage fees 550

Less: Stamp Duty 750

Gross Capital gains 30700

50% CGT discount 15350

Shares in PHB Iron Ore Ltd

Sales Proceeds 62500

Less: Cost Base 30000

Less: Brokerage Fees 1000

Less: Stamp Duty 1500

Gross Capital Gains 30000

50% CGT Discount 15000

Shares in Young Kids Learning Ltd

Sales Proceeds 600

Less: Cost base 6000

Less: Brokerage Fees 100

Less: Stamp Duty 500

Loss on Sale of Shares -6000

Share Build Ltd

Sales Proceeds 25000

Less: Cost Base 10000

Less: Brokerage Fees 900

Stamp Duty 1100

Gross Capital gains on Sale of Shares 13000

Total Capital gains 1,27,350

Less: Capital Loss Carryforward 7000

Total Net Capital Gains 1,20,350

Calculations of Capital Gains Tax

For the year ended June 2018

Particulars Amount ($) Amount ($)

Net Capital Gains on Sale of Vacant Land

Proceeds from sell of Vacant Block of Land 320000

Cost base 100000

Add: Ownership Expenses 20000

Add: Deposit 20000

Total Cost base 140000

Gross Capital Gains 180000

50% CGT Discount 90000

Capital gains on sale of shares

Proceeds from Common Ltd Shares (1000@ $47 per

share) 47000

Less: Cost Base (1000@15) 15000

Less: Brokerage fees 550

Less: Stamp Duty 750

Gross Capital gains 30700

50% CGT discount 15350

Shares in PHB Iron Ore Ltd

Sales Proceeds 62500

Less: Cost Base 30000

Less: Brokerage Fees 1000

Less: Stamp Duty 1500

Gross Capital Gains 30000

50% CGT Discount 15000

Shares in Young Kids Learning Ltd

Sales Proceeds 600

Less: Cost base 6000

Less: Brokerage Fees 100

Less: Stamp Duty 500

Loss on Sale of Shares -6000

Share Build Ltd

Sales Proceeds 25000

Less: Cost Base 10000

Less: Brokerage Fees 900

Stamp Duty 1100

Gross Capital gains on Sale of Shares 13000

Total Capital gains 1,27,350

Less: Capital Loss Carryforward 7000

Total Net Capital Gains 1,20,350

Calculations of Capital Gains Tax

For the year ended June 2018

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

Answer to Question 2:

Issue:

The case study involves the issues that is associated with the fringe benefit tax

liability. The case would be addressing the issue of Rapid Heat Pty Ltd relating to the fringe

benefit tax consequences and by determining the fringe benefit tax liability for the income

year ended 31st March 2018.

Laws:

According to the ATO the fringe benefit tax is generally paid by the employer. An

individual is held as employer for the fringe benefit tax purpose given that a payment is made

to the employee, holder of the office or the director of company that are subjected to

withholding obligations, or if the employer provides the benefit in lieu of such payments

(Hodgson and Pearce 2015). As the employer an individual is required to pay the fringe

benefit tax notwithstanding whether the taxpayer is operating the business of sole trader,

corporation, trustee, partnership or government authority. The benefit provided is regardless

of whether the employer or any other party provides the fringe benefit. An individual is

accountable of paying the fringe benefit tax whether they are paying or not paying any other

taxes such as the income tax (Braverman, Marsden and Sadiq 2015). An individual taxpayer

can claim the deduction for income tax purpose for the expenses incurred in providing the

fringe benefit and the amount they pay to employee.

A fringe benefit signifies the payment that is made to the employee but it is different

from the salary or wages. As defined under the legislation of the FBT, a fringe benefit is

given to the employee based on their employment. This signifies that benefit is given to a

person because they are employee (White and Townsend 2018). The employee can be either

the future or former employee as well.

Answer to Question 2:

Issue:

The case study involves the issues that is associated with the fringe benefit tax

liability. The case would be addressing the issue of Rapid Heat Pty Ltd relating to the fringe

benefit tax consequences and by determining the fringe benefit tax liability for the income

year ended 31st March 2018.

Laws:

According to the ATO the fringe benefit tax is generally paid by the employer. An

individual is held as employer for the fringe benefit tax purpose given that a payment is made

to the employee, holder of the office or the director of company that are subjected to

withholding obligations, or if the employer provides the benefit in lieu of such payments

(Hodgson and Pearce 2015). As the employer an individual is required to pay the fringe

benefit tax notwithstanding whether the taxpayer is operating the business of sole trader,

corporation, trustee, partnership or government authority. The benefit provided is regardless

of whether the employer or any other party provides the fringe benefit. An individual is

accountable of paying the fringe benefit tax whether they are paying or not paying any other

taxes such as the income tax (Braverman, Marsden and Sadiq 2015). An individual taxpayer

can claim the deduction for income tax purpose for the expenses incurred in providing the

fringe benefit and the amount they pay to employee.

A fringe benefit signifies the payment that is made to the employee but it is different

from the salary or wages. As defined under the legislation of the FBT, a fringe benefit is

given to the employee based on their employment. This signifies that benefit is given to a

person because they are employee (White and Townsend 2018). The employee can be either

the future or former employee as well.

8TAXATION LAW

As per the “section 7, FBTAA 1986” a benefit that most commonly occurs is the car

fringe benefit when the employer gives or makes the car available for the employee’s private

use (Pearce and Hodgson 2015). The employer makes the car available for the employee

personal use actually when the car is available for the private purpose of the employee. A car

is treated available for the personal use during any day when the car is either used by the

employee for private purpose or the employer makes the car available to the employee’s

private use.

When the car is kept at the garage at employees home, the car is treated to be

available for the private use of the employee irrespective of whether they have the permission

to use. The federal court in “FC of T v Lunney (1958)” passed its verdict by explaining that

travel to and from the place of work should be viewed as private use of car (Young and Miles

2015). When the car is kept in the workshop for the extensive repairs then it is not available

for the employee’s private use. Conversely, the car is regarded to be available for the

employee private use when the car is for the routine service or maintenance. The employer

can compute the taxable value of the car fringe benefit by using either the statutory method or

the operating cost method.

As stated in “Subdivision B 22A, FBTAA 1986” whenever the employer reimburse

the employee relating to the expenses that they occur it give rise to the expense payment

fringe benefit (Shields and North-Samardzic 2015). The expense payment fringe benefit

happens in two ways. Generally when the employer reimburses the expense that is incurred

by employee or they pay the third party in satisfaction of the expenditure that is incurred by

the employee. In either of the above stated cases the expense can be business or private

expense or the combination of both. The taxable value of the expense payment fringe benefit

represents the amount that the employer reimburses or pays the employee. The concessional

rates rules can be applied to determine the taxable value of the fringe benefit.

As per the “section 7, FBTAA 1986” a benefit that most commonly occurs is the car

fringe benefit when the employer gives or makes the car available for the employee’s private

use (Pearce and Hodgson 2015). The employer makes the car available for the employee

personal use actually when the car is available for the private purpose of the employee. A car

is treated available for the personal use during any day when the car is either used by the

employee for private purpose or the employer makes the car available to the employee’s

private use.

When the car is kept at the garage at employees home, the car is treated to be

available for the private use of the employee irrespective of whether they have the permission

to use. The federal court in “FC of T v Lunney (1958)” passed its verdict by explaining that

travel to and from the place of work should be viewed as private use of car (Young and Miles

2015). When the car is kept in the workshop for the extensive repairs then it is not available

for the employee’s private use. Conversely, the car is regarded to be available for the

employee private use when the car is for the routine service or maintenance. The employer

can compute the taxable value of the car fringe benefit by using either the statutory method or

the operating cost method.

As stated in “Subdivision B 22A, FBTAA 1986” whenever the employer reimburse

the employee relating to the expenses that they occur it give rise to the expense payment

fringe benefit (Shields and North-Samardzic 2015). The expense payment fringe benefit

happens in two ways. Generally when the employer reimburses the expense that is incurred

by employee or they pay the third party in satisfaction of the expenditure that is incurred by

the employee. In either of the above stated cases the expense can be business or private

expense or the combination of both. The taxable value of the expense payment fringe benefit

represents the amount that the employer reimburses or pays the employee. The concessional

rates rules can be applied to determine the taxable value of the fringe benefit.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

Very broadly speaking under “Sub-Division B 39C, FBTAA 1986” a fringe benefit

relating to car parking can happen during any day when the employer offers the employee

with a car parking space exclusively for the employee use (Seymour 2017). Precisely, fringe

benefit relating to the car parking happens during the fringe benefit year given that all the

below stated conditions are met. This includes;

a. The parking of car is made near the primary place of employee’s employment during

that day.

b. The car is parked for no less than four hours during that day.

c. The car is leased, owned or controlled by the employee or the car the provided to

employee.

d. The car is parked at the place or leased by or under the control of the employer

e. The car is inside the one kilometre area of premises or there is an existence of the

commercial parking station that charges fees for all day parking.

As per the “Division 4 of the FBTAA 1986” when the employer provides the

employee with the loan and a lower interest rate is charged then in such a situation the loan

fringe benefit happens during the FBT year (Barkoczy 2016). A noteworthy fact of loan

fringe benefit is that the lower rate of interest is less than the statutory rate of interest. The

taxable value of the loan fringe benefit reflects the difference between the interests which

may have been accrued during the FBT year given the statutory rate of interest is applied on

the outstanding balance of the loan.

Application:

The situation from the case study provides that the Rapid Heat Pty Ltd is the

manufacturer of electric heaters and one of its employee, Jasmine is provided with the car as

majority of her work requires travelling. Quoting the instance of “FC of T v Lunney (1958)”

Very broadly speaking under “Sub-Division B 39C, FBTAA 1986” a fringe benefit

relating to car parking can happen during any day when the employer offers the employee

with a car parking space exclusively for the employee use (Seymour 2017). Precisely, fringe

benefit relating to the car parking happens during the fringe benefit year given that all the

below stated conditions are met. This includes;

a. The parking of car is made near the primary place of employee’s employment during

that day.

b. The car is parked for no less than four hours during that day.

c. The car is leased, owned or controlled by the employee or the car the provided to

employee.

d. The car is parked at the place or leased by or under the control of the employer

e. The car is inside the one kilometre area of premises or there is an existence of the

commercial parking station that charges fees for all day parking.

As per the “Division 4 of the FBTAA 1986” when the employer provides the

employee with the loan and a lower interest rate is charged then in such a situation the loan

fringe benefit happens during the FBT year (Barkoczy 2016). A noteworthy fact of loan

fringe benefit is that the lower rate of interest is less than the statutory rate of interest. The

taxable value of the loan fringe benefit reflects the difference between the interests which

may have been accrued during the FBT year given the statutory rate of interest is applied on

the outstanding balance of the loan.

Application:

The situation from the case study provides that the Rapid Heat Pty Ltd is the

manufacturer of electric heaters and one of its employee, Jasmine is provided with the car as

majority of her work requires travelling. Quoting the instance of “FC of T v Lunney (1958)”

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

the case study further adds on that the Jasmine use of car is not limited to work only as she

has the permission of using the car for private purpose as well (Fisher 2015). Citing the

“section 7, FBTAA 1986” a car fringe benefit arises for Rapid Heat Pty Ltd when the

company gave or made the car available for the Jasmine’s private use. The car fringe benefit

is given to the Jasmine based on her employment with Rapid Heat Pty Ltd. Therefore, Rapid

Heat Pty Ltd will be liable for the taxable value of the car fringe benefit during the FBT year.

Evidences gained suggest that the Jasmine used the car to travel 10,000 km and

occurred the expenses for conducting minor repair which was reimbursed by Rapid Heat Pty

Ltd. Based on “Subdivision B 22A, FBTAA 1986” the reimbursement by Rapid Heat Pty Ltd

relating to the expenses that Jasmine occurred on minor repair gave rise to the expense

payment fringe benefit (Foster 2016). In whichever of the above stated case the expense

incurred by Jasmine can be business or private expense or the combination of both. The

taxable value of the car repair expense payment fringe benefit represents the amount that the

Rapid Heat Pty Ltd reimburses or pays Jasmine. The concessional rates rules can be applied

by Rapid Heat Pty Ltd to determine the taxable value of the fringe benefit.

In the following part of the case it is noticed that Jasmine parked the car at the airport

when she was out of state. The car was further parked at the work station for another five

days due to scheduled repairs. Referring to “Sub-Division B 39C, FBTAA 1986” a fringe

benefit relating to car parking did not arise for Rapid Heat Pty Ltd (Young and Miles 2015).

The reason for this is that the parking of car was not made near the primary place of

employee’s employment during those 10 days. Neither the car was parked at the place that

was under the control of the employer. Therefore, Rapid Heat Pty Ltd will not be held liable

for the car parking fringe benefit in such circumstances.

the case study further adds on that the Jasmine use of car is not limited to work only as she

has the permission of using the car for private purpose as well (Fisher 2015). Citing the

“section 7, FBTAA 1986” a car fringe benefit arises for Rapid Heat Pty Ltd when the

company gave or made the car available for the Jasmine’s private use. The car fringe benefit

is given to the Jasmine based on her employment with Rapid Heat Pty Ltd. Therefore, Rapid

Heat Pty Ltd will be liable for the taxable value of the car fringe benefit during the FBT year.

Evidences gained suggest that the Jasmine used the car to travel 10,000 km and

occurred the expenses for conducting minor repair which was reimbursed by Rapid Heat Pty

Ltd. Based on “Subdivision B 22A, FBTAA 1986” the reimbursement by Rapid Heat Pty Ltd

relating to the expenses that Jasmine occurred on minor repair gave rise to the expense

payment fringe benefit (Foster 2016). In whichever of the above stated case the expense

incurred by Jasmine can be business or private expense or the combination of both. The

taxable value of the car repair expense payment fringe benefit represents the amount that the

Rapid Heat Pty Ltd reimburses or pays Jasmine. The concessional rates rules can be applied

by Rapid Heat Pty Ltd to determine the taxable value of the fringe benefit.

In the following part of the case it is noticed that Jasmine parked the car at the airport

when she was out of state. The car was further parked at the work station for another five

days due to scheduled repairs. Referring to “Sub-Division B 39C, FBTAA 1986” a fringe

benefit relating to car parking did not arise for Rapid Heat Pty Ltd (Young and Miles 2015).

The reason for this is that the parking of car was not made near the primary place of

employee’s employment during those 10 days. Neither the car was parked at the place that

was under the control of the employer. Therefore, Rapid Heat Pty Ltd will not be held liable

for the car parking fringe benefit in such circumstances.

11TAXATION LAW

In the other instances obtained it is noticed that Rapid Heat Pty Ltd provided Jasmine

with the loan of $500,000 for purchasing the holiday home at 4.25% interest rate. Citing the

“Division 4 of the FBTAA 1986” making of loan by Rapid Heat Pty Ltd to Jasmine gave rise

to the loan fringe benefit during the FBT year (Seymour 2017). The lower rate of interest that

is charged by Rapid Heat Pty Ltd is less than the statutory rate of interest. The taxable value

of the loan fringe benefit for Rapid Heat Pty Ltd reflects the difference between the interests

which may have been accrued during the FBT year given the statutory rate of interest is

applied on the outstanding balance of the loan.

Conclusion:

The above stated analysis can be concluded by stating that the benefit provided by

Rapid Heat Ltd constitute fringe benefit for Jasmine under “S 7, FBTAA 1986”. Rapid Heat

made the car available for employee’s private use and the other benefits that was provided

was in respect of the employment. Rapid Heat will be held taxable for the value of fringe

benefit under the “FBTAA 1997”.

In the other instances obtained it is noticed that Rapid Heat Pty Ltd provided Jasmine

with the loan of $500,000 for purchasing the holiday home at 4.25% interest rate. Citing the

“Division 4 of the FBTAA 1986” making of loan by Rapid Heat Pty Ltd to Jasmine gave rise

to the loan fringe benefit during the FBT year (Seymour 2017). The lower rate of interest that

is charged by Rapid Heat Pty Ltd is less than the statutory rate of interest. The taxable value

of the loan fringe benefit for Rapid Heat Pty Ltd reflects the difference between the interests

which may have been accrued during the FBT year given the statutory rate of interest is

applied on the outstanding balance of the loan.

Conclusion:

The above stated analysis can be concluded by stating that the benefit provided by

Rapid Heat Ltd constitute fringe benefit for Jasmine under “S 7, FBTAA 1986”. Rapid Heat

made the car available for employee’s private use and the other benefits that was provided

was in respect of the employment. Rapid Heat will be held taxable for the value of fringe

benefit under the “FBTAA 1997”.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.