Taxation Report: Capital Gains Tax and Fringe Benefit Tax Analysis

VerifiedAdded on 2020/12/29

|16

|2943

|65

Report

AI Summary

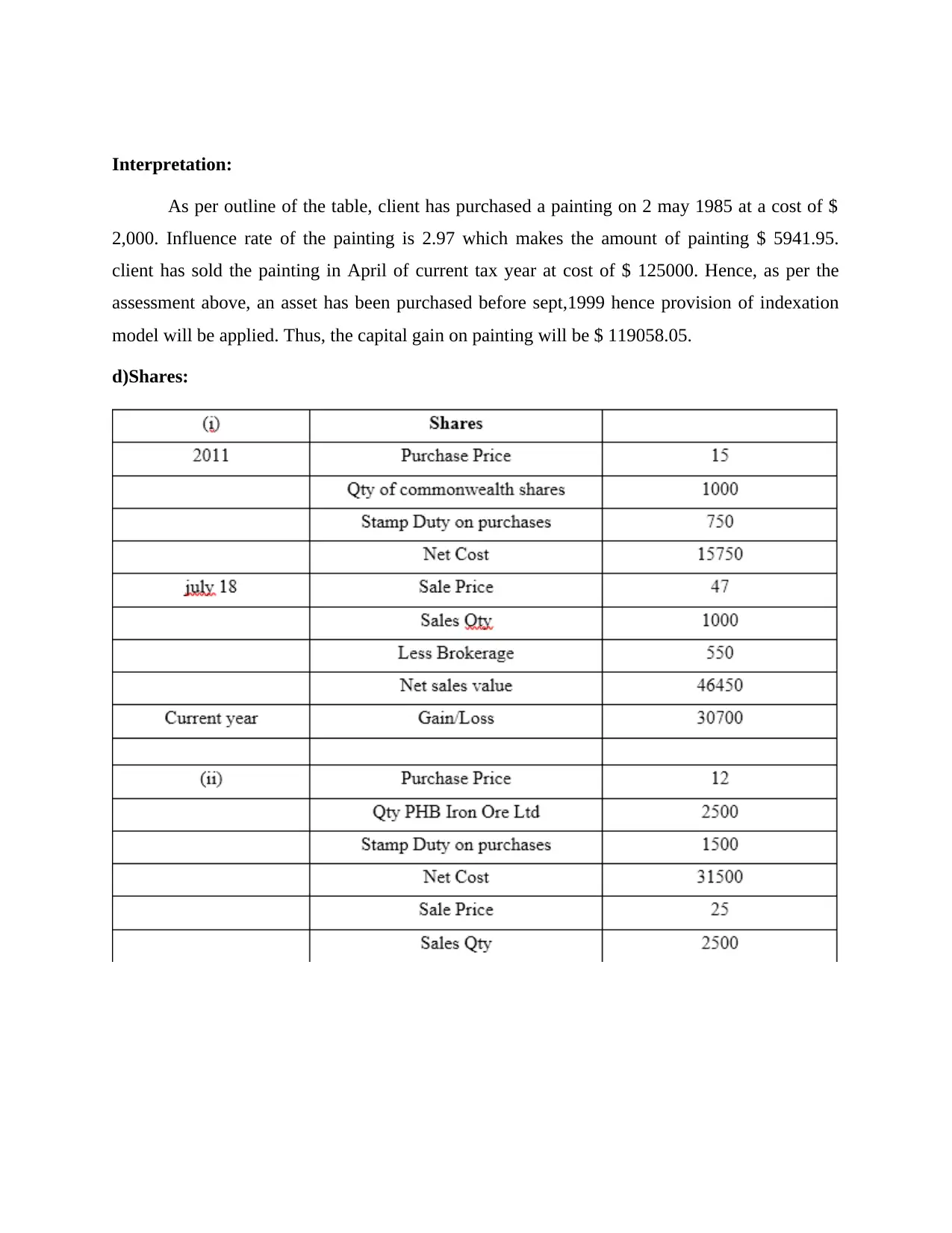

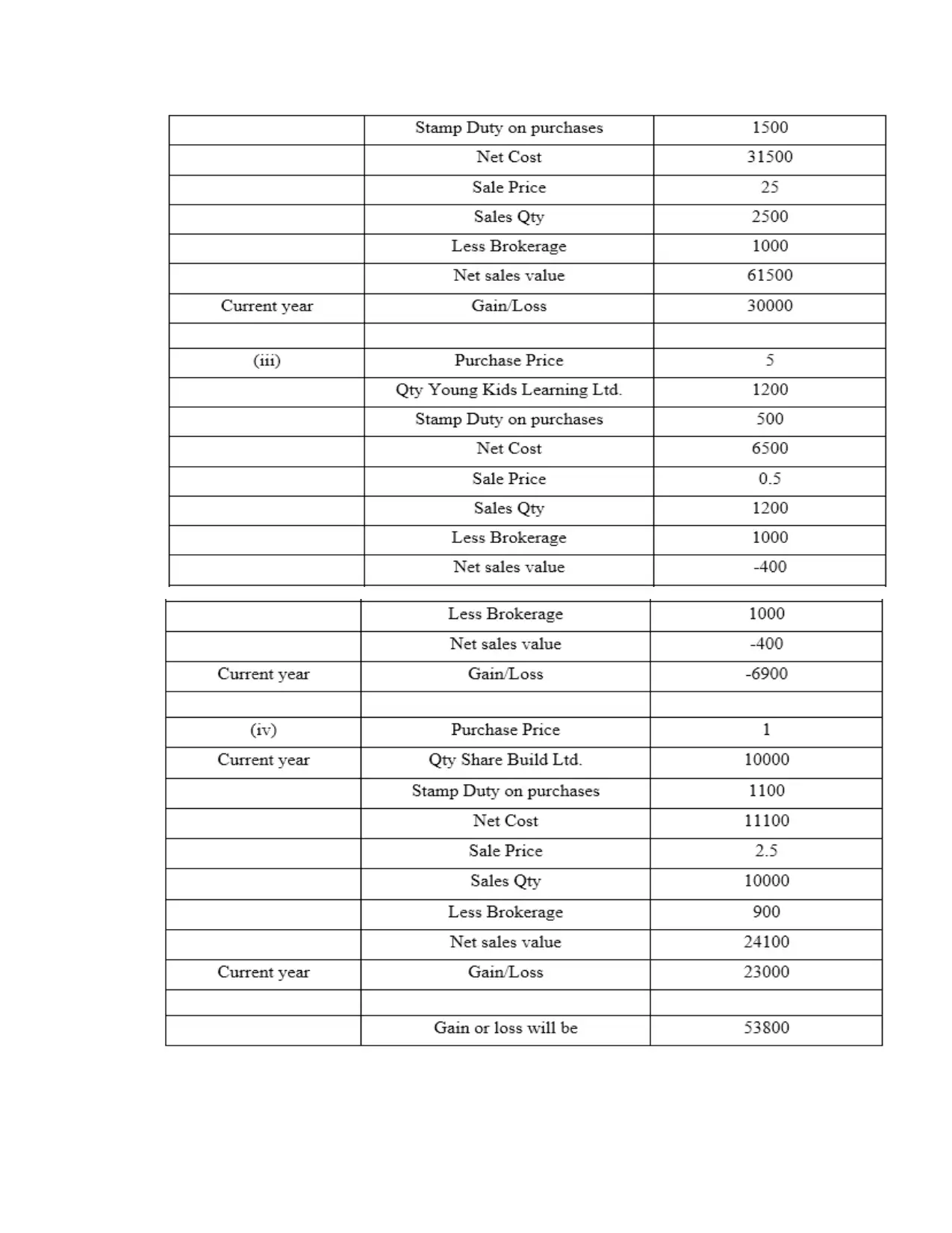

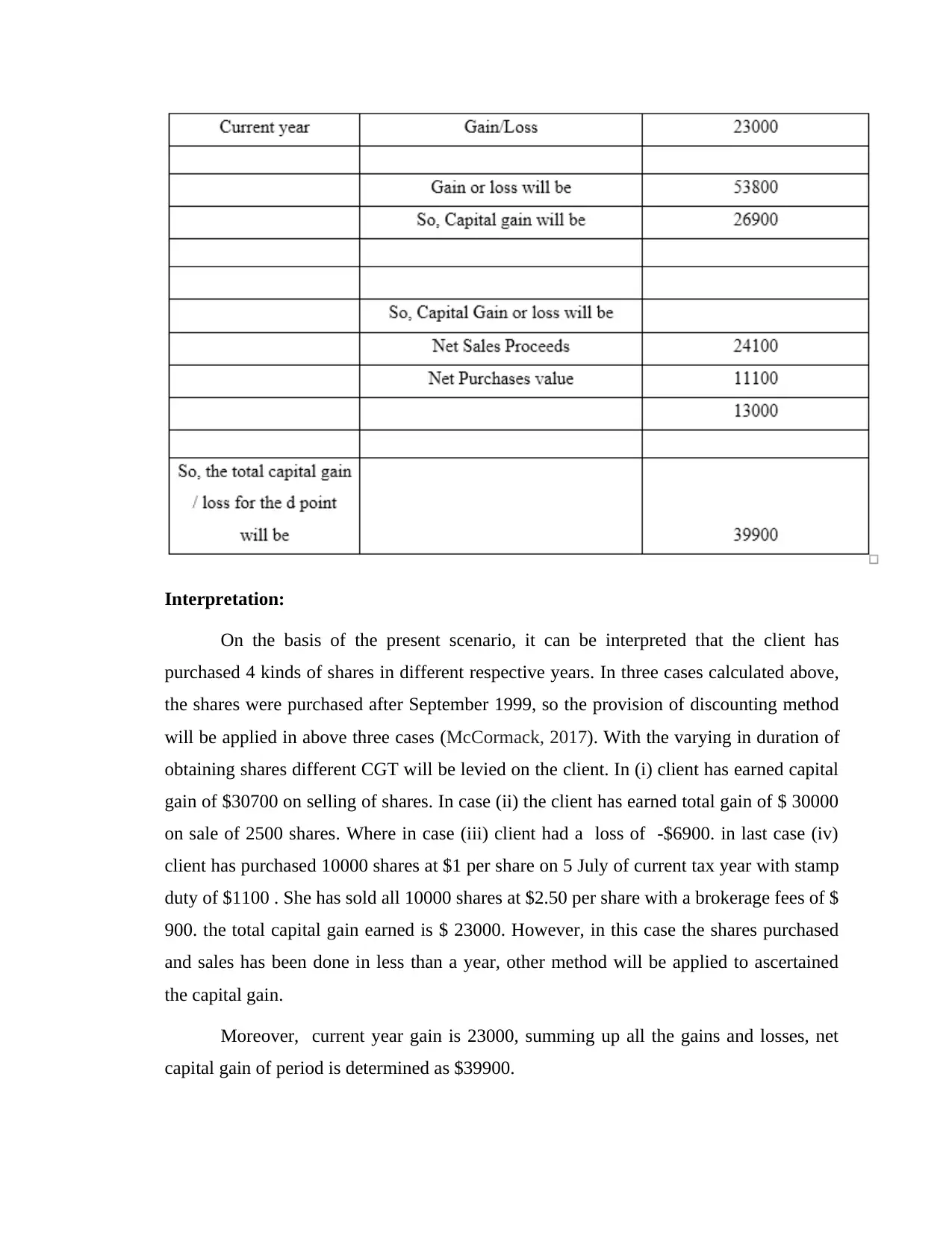

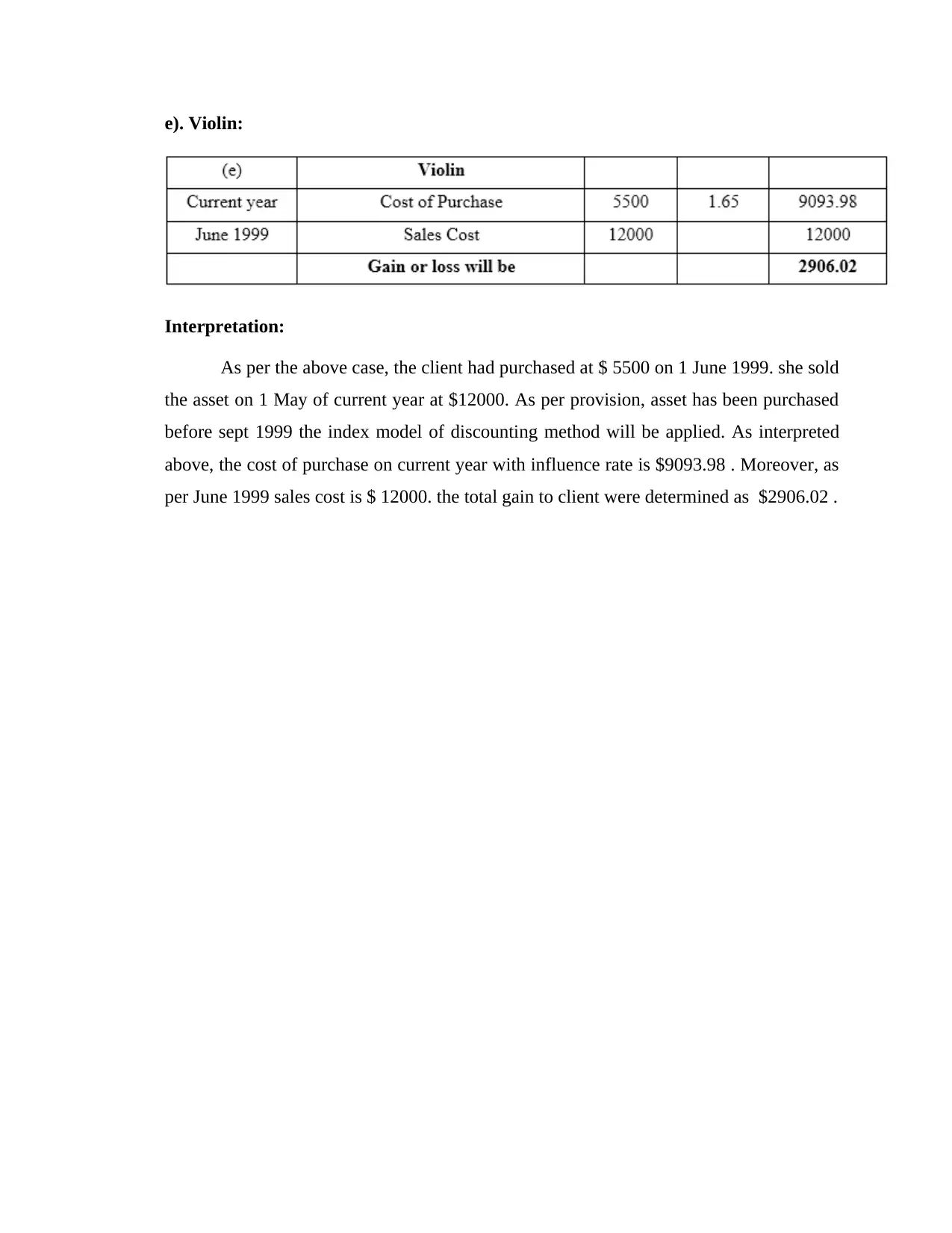

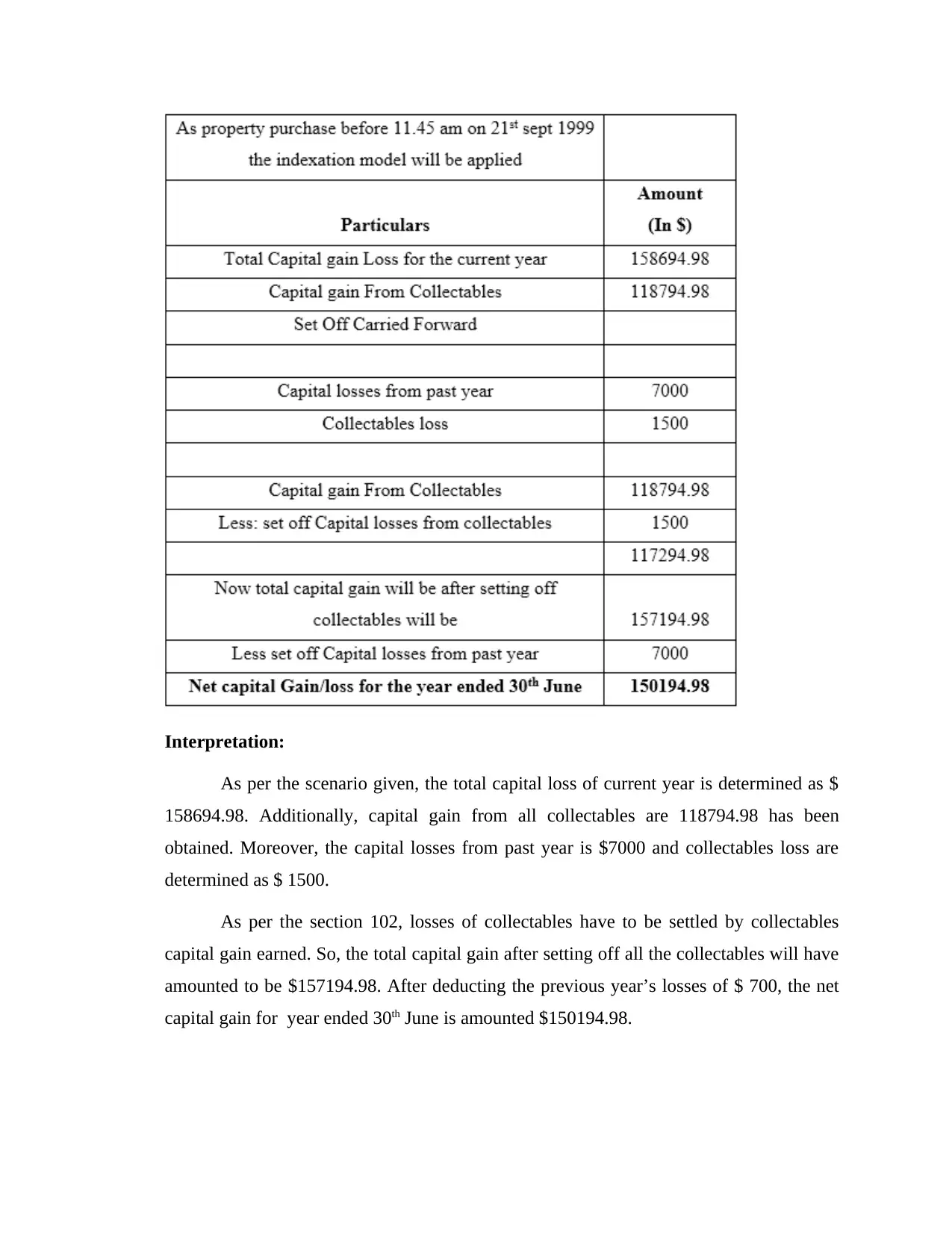

This report provides a detailed analysis of Australian taxation laws and practices, focusing on capital gains tax (CGT) and fringe benefit tax (FBT). It examines CGT implications on the sale and purchase of various assets, including vacant land, an antique bed, a painting, shares, and a violin, with detailed calculations to determine net capital gains or losses. The report also addresses fringe benefit tax (FBT) for the Rapid Heat company, specifically concerning car benefits, loan benefits, and heater benefits provided to an employee. It includes calculations to determine the taxable amount based on the Fringe Benefits Tax Assessment Act 1986, offering insights into the application of statutory formula and operating cost methods. The report further explains the determination of taxable value on car benefit, and loan benefit as per FBT assessment act. The report is a comprehensive guide to understanding the complexities of Australian taxation.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.