HI6028 Taxation Law: Analysis of Capital Gains, Income & Case Law

VerifiedAdded on 2023/03/31

|6

|1891

|211

Homework Assignment

AI Summary

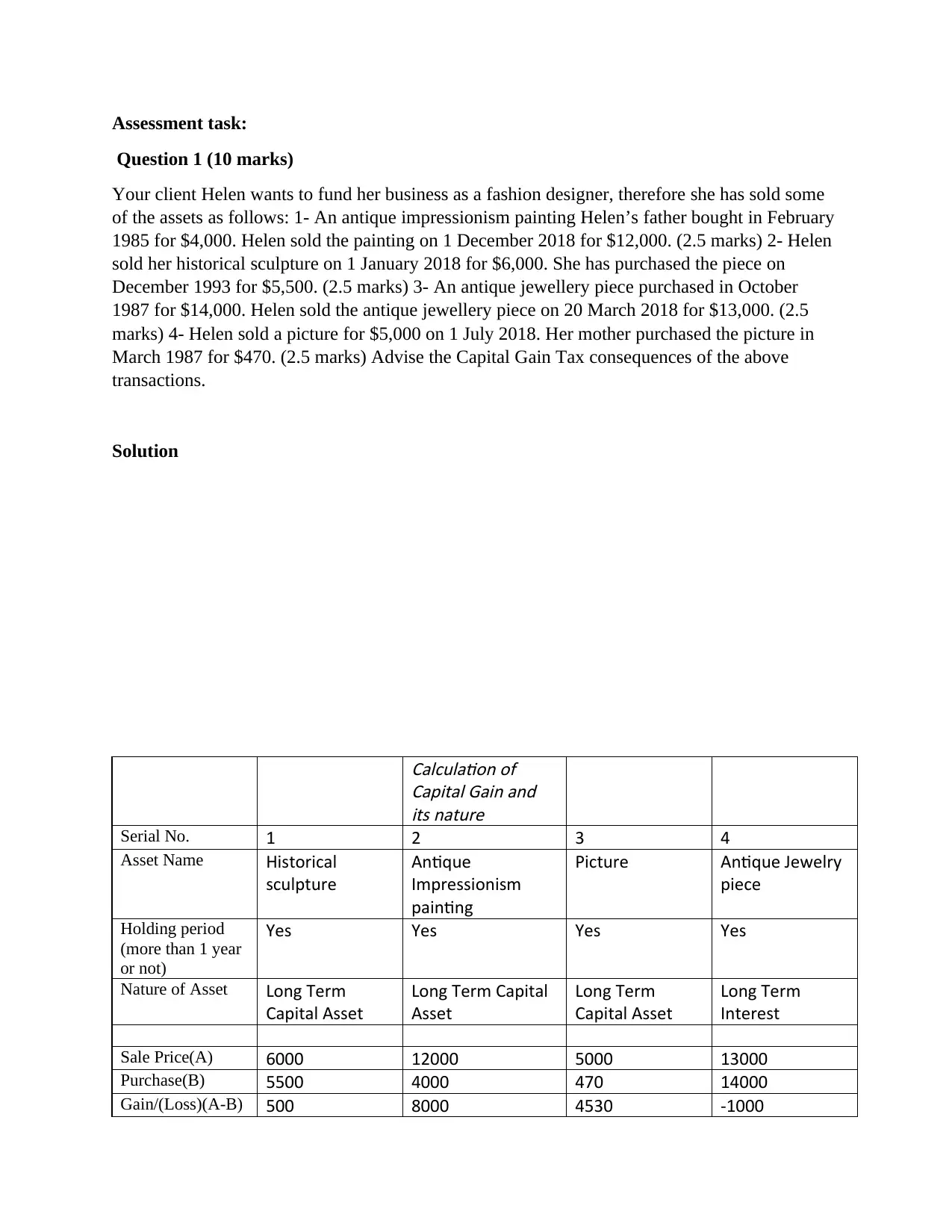

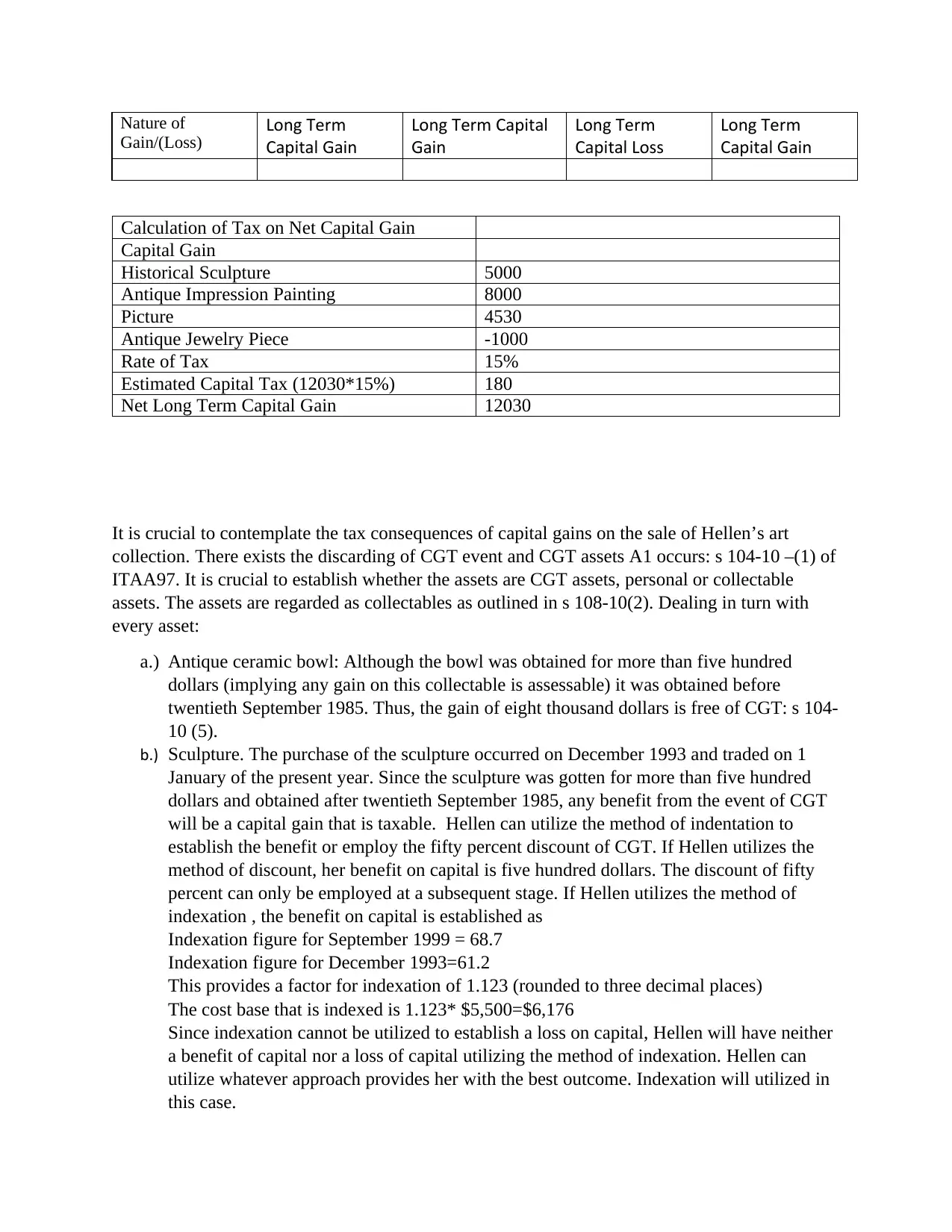

This assignment solution addresses several questions related to Australian taxation law. The first question analyzes the capital gains tax consequences of Helen selling various assets, including an antique painting, a historical sculpture, an antique jewelry piece, and a picture, providing calculations and legal references. The second question discusses whether payments to Barbara, an economist researcher, for writing a book and selling its copyright and manuscripts constitute income from personal exertion, considering scenarios with and without a prior contract, supported by case law. The third question examines the effect of a loan arrangement between Patrick and his son David on Patrick's assessable income, focusing on the tax implications of the interest paid, referencing statutory law.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.