Taxation Case Studies: Analysis of Capital Gains and Fringe Benefits

VerifiedAdded on 2020/07/22

|10

|2781

|51

Case Study

AI Summary

This document presents a detailed analysis of five taxation case studies. The first case examines capital gains tax, calculating profit/loss from asset sales and determining tax liabilities based on holding periods. The second case focuses on fringe benefits tax, specifically loan fringe benefits, calculating taxable value based on interest rate differences. The third case study explores tax avoidance strategies through profit-sharing agreements within a family, considering income clubbing and loss carry-forward. The fourth case analyzes a tax avoidance scheme involving employment contracts and deeds, emphasizing the legality of tax planning. The fifth case examines timber sales and the applicability of taxation rulings, determining tax implications for non-forestry operations. Each case includes critical analysis, supporting evidence, and conclusions, providing a comprehensive understanding of various tax-related scenarios.

TAXATION CASE STUDIES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction.................................................................................................................................1

Critical analysis:..........................................................................................................................1

Supporting Evidence:..................................................................................................................1

Conclusion:.................................................................................................................................2

Question 2........................................................................................................................................2

Introduction.................................................................................................................................2

Critical analysis:..........................................................................................................................2

Supportive evidence:...................................................................................................................3

Conclusion:.................................................................................................................................4

Question 3........................................................................................................................................4

Introduction.................................................................................................................................4

Critical analysis...........................................................................................................................4

Supporting evidence:...................................................................................................................4

Conclusion...................................................................................................................................5

Question 4........................................................................................................................................5

Introduction:................................................................................................................................5

Critical analysis:..........................................................................................................................5

Supporting evidence:...................................................................................................................5

Conclusion:.................................................................................................................................6

Question 5........................................................................................................................................6

Introduction.................................................................................................................................6

Critical analysis:..........................................................................................................................6

Supporting Evidence...................................................................................................................6

Conclusions.................................................................................................................................7

Introduction.................................................................................................................................1

Critical analysis:..........................................................................................................................1

Supporting Evidence:..................................................................................................................1

Conclusion:.................................................................................................................................2

Question 2........................................................................................................................................2

Introduction.................................................................................................................................2

Critical analysis:..........................................................................................................................2

Supportive evidence:...................................................................................................................3

Conclusion:.................................................................................................................................4

Question 3........................................................................................................................................4

Introduction.................................................................................................................................4

Critical analysis...........................................................................................................................4

Supporting evidence:...................................................................................................................4

Conclusion...................................................................................................................................5

Question 4........................................................................................................................................5

Introduction:................................................................................................................................5

Critical analysis:..........................................................................................................................5

Supporting evidence:...................................................................................................................5

Conclusion:.................................................................................................................................6

Question 5........................................................................................................................................6

Introduction.................................................................................................................................6

Critical analysis:..........................................................................................................................6

Supporting Evidence...................................................................................................................6

Conclusions.................................................................................................................................7

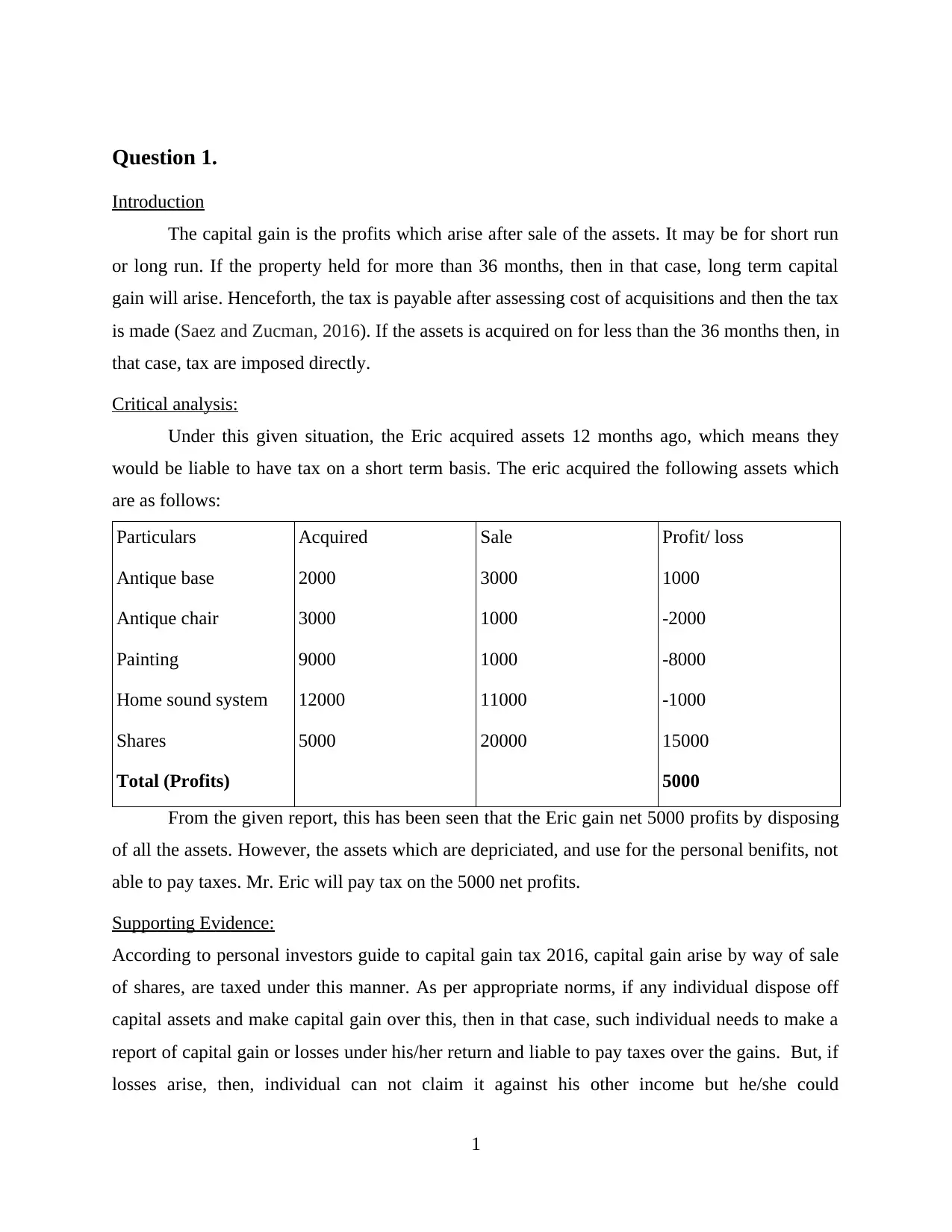

Question 1.

Introduction

The capital gain is the profits which arise after sale of the assets. It may be for short run

or long run. If the property held for more than 36 months, then in that case, long term capital

gain will arise. Henceforth, the tax is payable after assessing cost of acquisitions and then the tax

is made (Saez and Zucman, 2016). If the assets is acquired on for less than the 36 months then, in

that case, tax are imposed directly.

Critical analysis:

Under this given situation, the Eric acquired assets 12 months ago, which means they

would be liable to have tax on a short term basis. The eric acquired the following assets which

are as follows:

Particulars Acquired Sale Profit/ loss

Antique base 2000 3000 1000

Antique chair 3000 1000 -2000

Painting 9000 1000 -8000

Home sound system 12000 11000 -1000

Shares 5000 20000 15000

Total (Profits) 5000

From the given report, this has been seen that the Eric gain net 5000 profits by disposing

of all the assets. However, the assets which are depriciated, and use for the personal benifits, not

able to pay taxes. Mr. Eric will pay tax on the 5000 net profits.

Supporting Evidence:

According to personal investors guide to capital gain tax 2016, capital gain arise by way of sale

of shares, are taxed under this manner. As per appropriate norms, if any individual dispose off

capital assets and make capital gain over this, then in that case, such individual needs to make a

report of capital gain or losses under his/her return and liable to pay taxes over the gains. But, if

losses arise, then, individual can not claim it against his other income but he/she could

1

Introduction

The capital gain is the profits which arise after sale of the assets. It may be for short run

or long run. If the property held for more than 36 months, then in that case, long term capital

gain will arise. Henceforth, the tax is payable after assessing cost of acquisitions and then the tax

is made (Saez and Zucman, 2016). If the assets is acquired on for less than the 36 months then, in

that case, tax are imposed directly.

Critical analysis:

Under this given situation, the Eric acquired assets 12 months ago, which means they

would be liable to have tax on a short term basis. The eric acquired the following assets which

are as follows:

Particulars Acquired Sale Profit/ loss

Antique base 2000 3000 1000

Antique chair 3000 1000 -2000

Painting 9000 1000 -8000

Home sound system 12000 11000 -1000

Shares 5000 20000 15000

Total (Profits) 5000

From the given report, this has been seen that the Eric gain net 5000 profits by disposing

of all the assets. However, the assets which are depriciated, and use for the personal benifits, not

able to pay taxes. Mr. Eric will pay tax on the 5000 net profits.

Supporting Evidence:

According to personal investors guide to capital gain tax 2016, capital gain arise by way of sale

of shares, are taxed under this manner. As per appropriate norms, if any individual dispose off

capital assets and make capital gain over this, then in that case, such individual needs to make a

report of capital gain or losses under his/her return and liable to pay taxes over the gains. But, if

losses arise, then, individual can not claim it against his other income but he/she could

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

implement it in order to reduce capital gain. As, per the tax norms, whole assets acquired on or

before 20 September, 1985, are liable to pay CGT unless specifically excluded:

Many of the personal assets are exempt from CGT, and it also does not apply to depreciating

assets used for the taxable aim (Evers, Miller and Spengel, 2015). Henceforth, the tax is not

payable on above mentioned depreciating personal assets.

Conclusion:

Under this report, this has been seen that capital gain tax is payable as per the norms of

the income tax laws. Firstly, there is a need to assess the disposing value and then reduce the cost

of acquisition in a better manner.

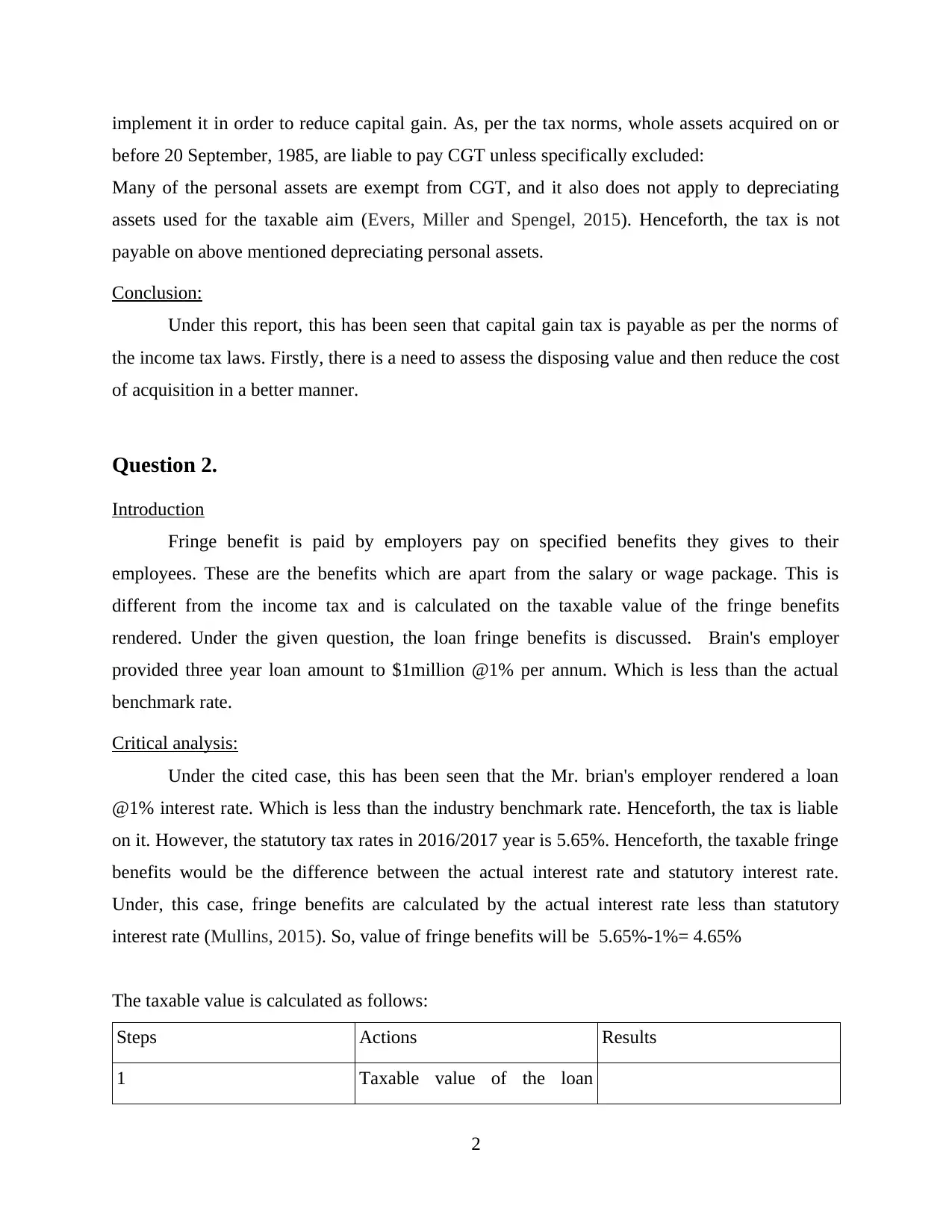

Question 2.

Introduction

Fringe benefit is paid by employers pay on specified benefits they gives to their

employees. These are the benefits which are apart from the salary or wage package. This is

different from the income tax and is calculated on the taxable value of the fringe benefits

rendered. Under the given question, the loan fringe benefits is discussed. Brain's employer

provided three year loan amount to $1million @1% per annum. Which is less than the actual

benchmark rate.

Critical analysis:

Under the cited case, this has been seen that the Mr. brian's employer rendered a loan

@1% interest rate. Which is less than the industry benchmark rate. Henceforth, the tax is liable

on it. However, the statutory tax rates in 2016/2017 year is 5.65%. Henceforth, the taxable fringe

benefits would be the difference between the actual interest rate and statutory interest rate.

Under, this case, fringe benefits are calculated by the actual interest rate less than statutory

interest rate (Mullins, 2015). So, value of fringe benefits will be 5.65%-1%= 4.65%

The taxable value is calculated as follows:

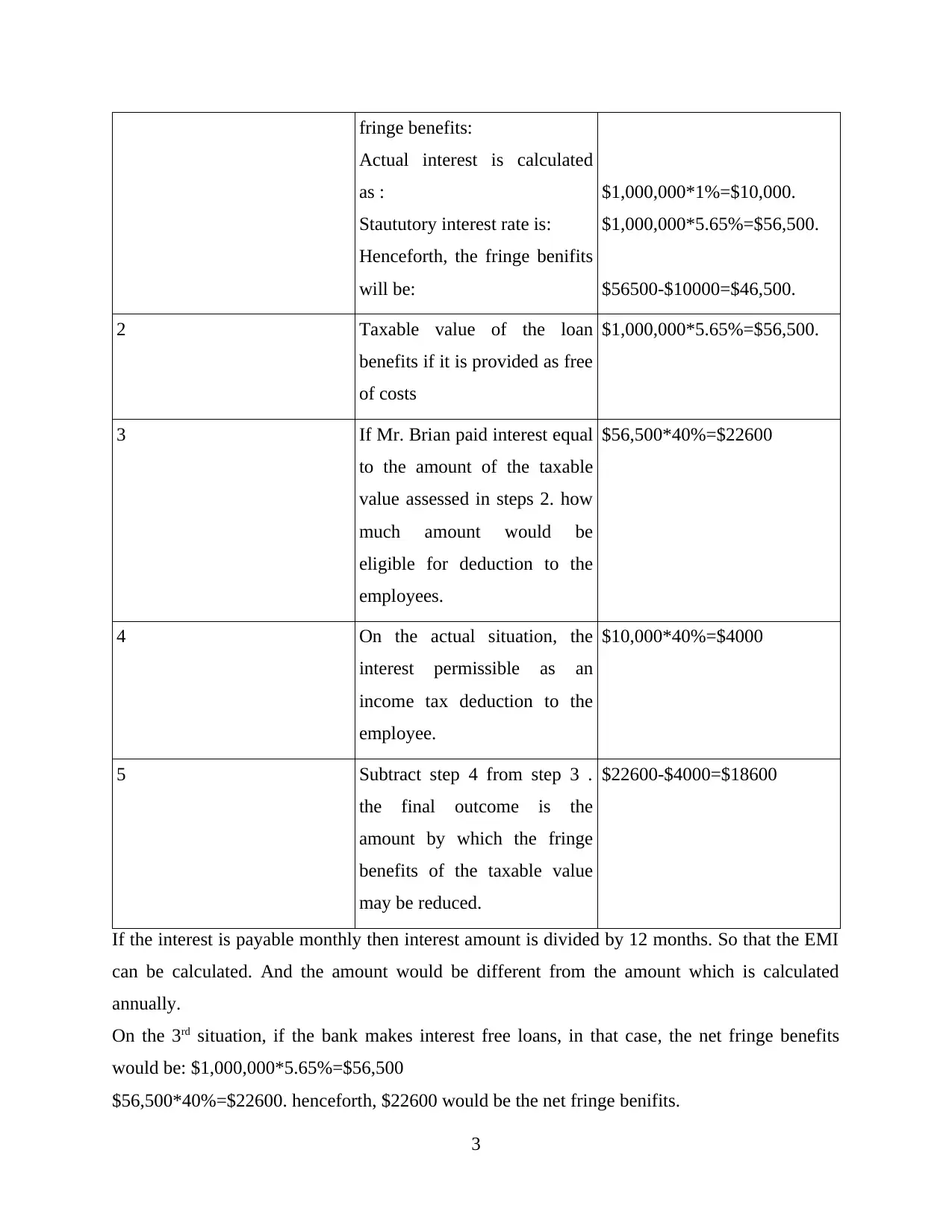

Steps Actions Results

1 Taxable value of the loan

2

before 20 September, 1985, are liable to pay CGT unless specifically excluded:

Many of the personal assets are exempt from CGT, and it also does not apply to depreciating

assets used for the taxable aim (Evers, Miller and Spengel, 2015). Henceforth, the tax is not

payable on above mentioned depreciating personal assets.

Conclusion:

Under this report, this has been seen that capital gain tax is payable as per the norms of

the income tax laws. Firstly, there is a need to assess the disposing value and then reduce the cost

of acquisition in a better manner.

Question 2.

Introduction

Fringe benefit is paid by employers pay on specified benefits they gives to their

employees. These are the benefits which are apart from the salary or wage package. This is

different from the income tax and is calculated on the taxable value of the fringe benefits

rendered. Under the given question, the loan fringe benefits is discussed. Brain's employer

provided three year loan amount to $1million @1% per annum. Which is less than the actual

benchmark rate.

Critical analysis:

Under the cited case, this has been seen that the Mr. brian's employer rendered a loan

@1% interest rate. Which is less than the industry benchmark rate. Henceforth, the tax is liable

on it. However, the statutory tax rates in 2016/2017 year is 5.65%. Henceforth, the taxable fringe

benefits would be the difference between the actual interest rate and statutory interest rate.

Under, this case, fringe benefits are calculated by the actual interest rate less than statutory

interest rate (Mullins, 2015). So, value of fringe benefits will be 5.65%-1%= 4.65%

The taxable value is calculated as follows:

Steps Actions Results

1 Taxable value of the loan

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

fringe benefits:

Actual interest is calculated

as :

Staututory interest rate is:

Henceforth, the fringe benifits

will be:

$1,000,000*1%=$10,000.

$1,000,000*5.65%=$56,500.

$56500-$10000=$46,500.

2 Taxable value of the loan

benefits if it is provided as free

of costs

$1,000,000*5.65%=$56,500.

3 If Mr. Brian paid interest equal

to the amount of the taxable

value assessed in steps 2. how

much amount would be

eligible for deduction to the

employees.

$56,500*40%=$22600

4 On the actual situation, the

interest permissible as an

income tax deduction to the

employee.

$10,000*40%=$4000

5 Subtract step 4 from step 3 .

the final outcome is the

amount by which the fringe

benefits of the taxable value

may be reduced.

$22600-$4000=$18600

If the interest is payable monthly then interest amount is divided by 12 months. So that the EMI

can be calculated. And the amount would be different from the amount which is calculated

annually.

On the 3rd situation, if the bank makes interest free loans, in that case, the net fringe benefits

would be: $1,000,000*5.65%=$56,500

$56,500*40%=$22600. henceforth, $22600 would be the net fringe benifits.

3

Actual interest is calculated

as :

Staututory interest rate is:

Henceforth, the fringe benifits

will be:

$1,000,000*1%=$10,000.

$1,000,000*5.65%=$56,500.

$56500-$10000=$46,500.

2 Taxable value of the loan

benefits if it is provided as free

of costs

$1,000,000*5.65%=$56,500.

3 If Mr. Brian paid interest equal

to the amount of the taxable

value assessed in steps 2. how

much amount would be

eligible for deduction to the

employees.

$56,500*40%=$22600

4 On the actual situation, the

interest permissible as an

income tax deduction to the

employee.

$10,000*40%=$4000

5 Subtract step 4 from step 3 .

the final outcome is the

amount by which the fringe

benefits of the taxable value

may be reduced.

$22600-$4000=$18600

If the interest is payable monthly then interest amount is divided by 12 months. So that the EMI

can be calculated. And the amount would be different from the amount which is calculated

annually.

On the 3rd situation, if the bank makes interest free loans, in that case, the net fringe benefits

would be: $1,000,000*5.65%=$56,500

$56,500*40%=$22600. henceforth, $22600 would be the net fringe benifits.

3

Supportive evidence:

As per the fringe benefits tax policy, FB taxable value is the amount under which the

notional amount of interest exceeds the actual amount of interest falling on the loan. Every loan

is to be considered separately.

Conclusion:

Fringe benefits are the benefits which have been allotted by the employer to the

employee, and on behalf on this, the employee paid tax on the fringe benefits taxable amount.

The employee must reduce fringe benefits taxable value to which the notional interest on loan

will be permissible as an income tax deduction to the employee (Brink, 2017). For proving the

deductibility, there is a need to make a declaration report made by the employee to the employer,

which clear the use of loan was put and the extent to which interest on the implement of loan was

allowable as a deduction.

Question 3

Introduction

Under the cited case, Jack and Jill borrowed money for buying rental property. They both were

agreeing to make a contract under which they agreed to share the profits in the ration of 90:10,

and the loss is to be bear by the Jack only. This contract made in order to avoid the tax liabilities.

In the last year, property arose $10000 loss.

Critical analysis

In the given case, they both made a contract for avoiding the tax liabilities. As, this has

been seen that Jill is the housewife who is a dependant lady hence, her income is to be clubbed

under the Jack assessment (McGuire, Wang, and Wilson, 2014). So, the covenant is made for

lowering the tax liabilities and the income is also covered under Jack. Hence forth, if the

property incurred the loss last year, then, in that case, such loss is to be carry forward for nest

year and this would be set off from the nest year or succeeding years profits (Capital gain tax on

property, 2017). If, they both decides to sell it, then any Capital gain or loss arise, then, it would

be assessed under the Jack capital gain head. As, his wife is the dependant lady and earn nothing.

She is not liable to pay tax over any capital gain but his husband would pay the entire capital

gain tax.

4

As per the fringe benefits tax policy, FB taxable value is the amount under which the

notional amount of interest exceeds the actual amount of interest falling on the loan. Every loan

is to be considered separately.

Conclusion:

Fringe benefits are the benefits which have been allotted by the employer to the

employee, and on behalf on this, the employee paid tax on the fringe benefits taxable amount.

The employee must reduce fringe benefits taxable value to which the notional interest on loan

will be permissible as an income tax deduction to the employee (Brink, 2017). For proving the

deductibility, there is a need to make a declaration report made by the employee to the employer,

which clear the use of loan was put and the extent to which interest on the implement of loan was

allowable as a deduction.

Question 3

Introduction

Under the cited case, Jack and Jill borrowed money for buying rental property. They both were

agreeing to make a contract under which they agreed to share the profits in the ration of 90:10,

and the loss is to be bear by the Jack only. This contract made in order to avoid the tax liabilities.

In the last year, property arose $10000 loss.

Critical analysis

In the given case, they both made a contract for avoiding the tax liabilities. As, this has

been seen that Jill is the housewife who is a dependant lady hence, her income is to be clubbed

under the Jack assessment (McGuire, Wang, and Wilson, 2014). So, the covenant is made for

lowering the tax liabilities and the income is also covered under Jack. Hence forth, if the

property incurred the loss last year, then, in that case, such loss is to be carry forward for nest

year and this would be set off from the nest year or succeeding years profits (Capital gain tax on

property, 2017). If, they both decides to sell it, then any Capital gain or loss arise, then, it would

be assessed under the Jack capital gain head. As, his wife is the dependant lady and earn nothing.

She is not liable to pay tax over any capital gain but his husband would pay the entire capital

gain tax.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Supporting evidence:

As per the tax laws of the country, one can not take the benefits for which he/ she did not

pay nothing. Hence, the tax is to be paid on the capital gain amount what they are going to

entitled. Henceforth, the tax is to be paid by Jack on CG.

Conclusion

From the given case, this has been concluded that tax is to be paid by Jack on the capital gain

what he earn form the assets. The last year loss is also set off form the capital gain arise for the

sale of the assets.

Question 4

Introduction:

According to Duke of Westminster's case which was based on tax avoidance. They executed a

deed of conveyance of covalent with his lad servant including national helpers, gardeners, etc.

Under a special deed, duke decided to pay some amount for the services which he was rendering

to him. In an written letter which was sent to the servants. In which, it was clearly mentioned that

Duke would pay remuneration on priority in addition to sums, if any, services performed by the

servant as a domestic helper. After analysing all situations Duke has decided to claim such

payment for a tax deduction in preparation for tax avoidance (Gallemore and Labro, 2015).

Critical analysis:

A deed is a known as a contract same as legal document which requires a mutual consents of

more than one people. It is normally used to grant a perfect ways to transfer of such property.

The basic relation among a deed and a contract is that, deed is a written agreement that must be

dully signed and get sealed under the presence of a third party. Like solicitor. An agreement must

be in writing, a dead is a contract which is not required to be unenforceable. In most of the cases,

a deed has a long term enforceable time duration as a easy contract.

Supporting evidence:

According to the above mentioned case, the major issues lies on whether the deed of written

agreement would be seen or burned as under employment contract. Duke was not even paying

the gardeners and servants not weakly wages neither monthly salary that was mentioned under

the employment contract. Therefore, there is no any consideration is made towards the contract

which is said to be one of the major factors in the development of legally binding contract. In the

5

As per the tax laws of the country, one can not take the benefits for which he/ she did not

pay nothing. Hence, the tax is to be paid on the capital gain amount what they are going to

entitled. Henceforth, the tax is to be paid by Jack on CG.

Conclusion

From the given case, this has been concluded that tax is to be paid by Jack on the capital gain

what he earn form the assets. The last year loss is also set off form the capital gain arise for the

sale of the assets.

Question 4

Introduction:

According to Duke of Westminster's case which was based on tax avoidance. They executed a

deed of conveyance of covalent with his lad servant including national helpers, gardeners, etc.

Under a special deed, duke decided to pay some amount for the services which he was rendering

to him. In an written letter which was sent to the servants. In which, it was clearly mentioned that

Duke would pay remuneration on priority in addition to sums, if any, services performed by the

servant as a domestic helper. After analysing all situations Duke has decided to claim such

payment for a tax deduction in preparation for tax avoidance (Gallemore and Labro, 2015).

Critical analysis:

A deed is a known as a contract same as legal document which requires a mutual consents of

more than one people. It is normally used to grant a perfect ways to transfer of such property.

The basic relation among a deed and a contract is that, deed is a written agreement that must be

dully signed and get sealed under the presence of a third party. Like solicitor. An agreement must

be in writing, a dead is a contract which is not required to be unenforceable. In most of the cases,

a deed has a long term enforceable time duration as a easy contract.

Supporting evidence:

According to the above mentioned case, the major issues lies on whether the deed of written

agreement would be seen or burned as under employment contract. Duke was not even paying

the gardeners and servants not weakly wages neither monthly salary that was mentioned under

the employment contract. Therefore, there is no any consideration is made towards the contract

which is said to be one of the major factors in the development of legally binding contract. In the

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

case of agreement, the payment is made only in terms of tax deductible (Jiang and Shao, 2014).

If it is an yearly payment to gardener and servants. They Duke have only the right to claim tax

relief for the yearly payment or in the situation where the amount paid for those services

rendered in that particular year.

Conclusion:

The overall case recommended that tax avoidance can only be allowed as long as it follows

enactment law. Under this case the principles amount of that specific format of the agreement

can reduce the tax liabilities. If it get approved and claim for only annual year is made for the

payment.

Question 5

Introduction

The revenue generated via giving the land for producing timber. This is done by cutting

various pine trees. Under the cited case, it is found that Mr. Bill wants to clear its land. For that,

a company is paying him $1000 for 100 metre of timber. This comes under Taxation ruling 95/6,

primary production and forestry. Such ruling covers the receipts comes from the sale of timber

would make accessible income, whether they are from the forestry industry or not. The

deduction is also allowable on such income. Such ruling is covers the tax treatment of

transactions connected to timber which does not comes under the forest operations.

Critical analysis:

Under the give case, Mr. Bill does not engaged in forest operations but he ultimately

indulge in disposing the operations. Hence he is not liable to pay tax on the amount what he will

get from the company. Because, such activity does not covers the forest operations On the other

case, if Mr. bill will get $50000 lump sum amount, in that case, the this would be presumed to be

the assessable income (Jiang and Shao, 2014). As, such activity covers under forest operations,

and liable to pay taxes. Hence, both reflects different answer.

Supporting Evidence

This circumstances comes under taxation ruling, and this ruling is applicable to person

not occupied in forest operations who sale off timber. If any person receives royalties for

removing the trees form the land, does not comes under conducting forest operations if these are

not intentionally planted for the purpose of felling. Hence, not liable pay tax on assessable

6

If it is an yearly payment to gardener and servants. They Duke have only the right to claim tax

relief for the yearly payment or in the situation where the amount paid for those services

rendered in that particular year.

Conclusion:

The overall case recommended that tax avoidance can only be allowed as long as it follows

enactment law. Under this case the principles amount of that specific format of the agreement

can reduce the tax liabilities. If it get approved and claim for only annual year is made for the

payment.

Question 5

Introduction

The revenue generated via giving the land for producing timber. This is done by cutting

various pine trees. Under the cited case, it is found that Mr. Bill wants to clear its land. For that,

a company is paying him $1000 for 100 metre of timber. This comes under Taxation ruling 95/6,

primary production and forestry. Such ruling covers the receipts comes from the sale of timber

would make accessible income, whether they are from the forestry industry or not. The

deduction is also allowable on such income. Such ruling is covers the tax treatment of

transactions connected to timber which does not comes under the forest operations.

Critical analysis:

Under the give case, Mr. Bill does not engaged in forest operations but he ultimately

indulge in disposing the operations. Hence he is not liable to pay tax on the amount what he will

get from the company. Because, such activity does not covers the forest operations On the other

case, if Mr. bill will get $50000 lump sum amount, in that case, the this would be presumed to be

the assessable income (Jiang and Shao, 2014). As, such activity covers under forest operations,

and liable to pay taxes. Hence, both reflects different answer.

Supporting Evidence

This circumstances comes under taxation ruling, and this ruling is applicable to person

not occupied in forest operations who sale off timber. If any person receives royalties for

removing the trees form the land, does not comes under conducting forest operations if these are

not intentionally planted for the purpose of felling. Hence, not liable pay tax on assessable

6

income. On the other hand, the income is received knowingly then, it is liable to pay tax, as the

operations would presumed to the forest operations.

Conclusions

From the cited case study, this has been observed that Mr bill is not carrying forest

operations under first phase, so the revenue earned by him would not liable to pay tax. While on

the other case, he receives $50000 for permitting logging company a right to remove timber,

which covers forest activity, hence liable to pay tax on that.

7

operations would presumed to the forest operations.

Conclusions

From the cited case study, this has been observed that Mr bill is not carrying forest

operations under first phase, so the revenue earned by him would not liable to pay tax. While on

the other case, he receives $50000 for permitting logging company a right to remove timber,

which covers forest activity, hence liable to pay tax on that.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals:

Saez, E. and Zucman, G., 2016. Wealth inequality in the United States since 1913: Evidence

from capitalized income tax data. The Quarterly Journal of Economics. 131(2). pp.519-

578.

Evers, L., Miller, H. and Spengel, C., 2015. Intellectual property box regimes: effective tax rates

and tax policy considerations. International Tax and Public Finance. 22(3), pp.502-530.

Mullins, C., 2015. Tax considerations of debit loans: business income tax. TAXtalk. 2015(55).

pp.58-59.

Brink, J., 2017. Taxable benefits provided to expatriate employees seconded in South Africa:

fringe benefits. Tax Breaks Newsletter. 2017(373). pp.5-8.

McGuire, S.T., Wang, D. and Wilson, R.J., 2014. Dual class ownership and tax avoidance. The

Accounting Review. 89(4). pp.1487-1516.

Gallemore, J. and Labro, E., 2015. The importance of the internal information environment for

tax avoidance. Journal of Accounting and Economics. 60(1). pp.149-167.

Jiang, Z. and Shao, S., 2014. Distributional effects of a carbon tax on Chinese households: A

case of Shanghai. Energy Policy. 73. pp.269-277.

Online

Capital gain tax on property. 2017. [Online]. Available

through:<http://www.which.co.uk/money/tax/capital-gains-tax/guides/capital-gains-tax-on-

property>. [Accessed on 18 th September, 2017].

8

Books and Journals:

Saez, E. and Zucman, G., 2016. Wealth inequality in the United States since 1913: Evidence

from capitalized income tax data. The Quarterly Journal of Economics. 131(2). pp.519-

578.

Evers, L., Miller, H. and Spengel, C., 2015. Intellectual property box regimes: effective tax rates

and tax policy considerations. International Tax and Public Finance. 22(3), pp.502-530.

Mullins, C., 2015. Tax considerations of debit loans: business income tax. TAXtalk. 2015(55).

pp.58-59.

Brink, J., 2017. Taxable benefits provided to expatriate employees seconded in South Africa:

fringe benefits. Tax Breaks Newsletter. 2017(373). pp.5-8.

McGuire, S.T., Wang, D. and Wilson, R.J., 2014. Dual class ownership and tax avoidance. The

Accounting Review. 89(4). pp.1487-1516.

Gallemore, J. and Labro, E., 2015. The importance of the internal information environment for

tax avoidance. Journal of Accounting and Economics. 60(1). pp.149-167.

Jiang, Z. and Shao, S., 2014. Distributional effects of a carbon tax on Chinese households: A

case of Shanghai. Energy Policy. 73. pp.269-277.

Online

Capital gain tax on property. 2017. [Online]. Available

through:<http://www.which.co.uk/money/tax/capital-gains-tax/guides/capital-gains-tax-on-

property>. [Accessed on 18 th September, 2017].

8

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.