Financial Management Report: Capital Structure, Equity & Investment

VerifiedAdded on 2020/11/12

|20

|6390

|130

Report

AI Summary

This report delves into financial management principles, examining the cost of capital and capital structure of Kadlex Plc, the equity finance strategies of Lexbel Plc, and investment appraisal techniques relevant to Happy Meal Limited. It includes detailed calculations of the Weighted Average Cost of Capital (WACC) for Kadlex Plc, analyzing the impact of proposed capital structure changes. The report also explores equity finance through a right issue for Lexbel PLC, evaluating different issue prices and their effects on share value. Furthermore, it assesses investment appraisal techniques such as ARR, IRR, and NPV, evaluating their benefits and drawbacks. The analysis extends to agency problems, short-termism, and their effects on bankruptcy, providing a comprehensive overview of financial management concepts and their practical implications.

FINANCIAL MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

Question 1- Cost of Capital and Capital Structure:.........................................................................1

(a) Calculation of Book Value and Market Value cost of Capital (WACC) for Kadlex Plc: 2

(b) Kadlex Plc revised cost of capital after proposed changes with finance director proposal:. 3

(c) Critical analysis of integrating new capital:......................................................................3

(d) Effect of Short-termism on Agency Problem and Bankruptcy:........................................4

Question 2- Long term finance: Equity finance:..............................................................................4

(a) Right Issue: ......................................................................................................................4

(b) Scrip Dividends:...............................................................................................................9

Question 3- Investment Appraisal Techniques..............................................................................10

(a) Determination of economic feasibility of project using following investment appraisal

techniques:............................................................................................................................11

(b) Benefits and Drawbacks of various Investment Appraisal techniques:..........................15

CONCLUSION..............................................................................................................................16

REFERENCES .............................................................................................................................17

INTRODUCTION...........................................................................................................................1

Question 1- Cost of Capital and Capital Structure:.........................................................................1

(a) Calculation of Book Value and Market Value cost of Capital (WACC) for Kadlex Plc: 2

(b) Kadlex Plc revised cost of capital after proposed changes with finance director proposal:. 3

(c) Critical analysis of integrating new capital:......................................................................3

(d) Effect of Short-termism on Agency Problem and Bankruptcy:........................................4

Question 2- Long term finance: Equity finance:..............................................................................4

(a) Right Issue: ......................................................................................................................4

(b) Scrip Dividends:...............................................................................................................9

Question 3- Investment Appraisal Techniques..............................................................................10

(a) Determination of economic feasibility of project using following investment appraisal

techniques:............................................................................................................................11

(b) Benefits and Drawbacks of various Investment Appraisal techniques:..........................15

CONCLUSION..............................................................................................................................16

REFERENCES .............................................................................................................................17

INTRODUCTION

Financial Management is the study of planning, controlling and organizing the finances

of an organisation (Allen, Hemming and Potter, 2013). This report takes capital structure, equity

finance and investment appraisal techniques into consideration of Kadlex Plc, Lexbel Plc and

Happy Meal Limited respectively. It also evaluates the benefits and drawbacks of scrip dividends

and appraisal techniques like ARR, IRR and NPV.

Question 1- Cost of Capital and Capital Structure:

Cost of Capital and Capital structure are an important concept for any organization as they help

in determining the proportion in which the debt and equity must be taken so as to derive

maximum benefit at lowest cost possible. Kadlex plc wants to review its capital structure in order

to minimise its cost of capital (WACC). The following calculations have been worked out to

achieve the same:

Step 1: Calculation of growth (g)

Years

1 21 pence

2 23 pence

3 25 pence

4 27 pence

5 28 pence

S0*(1+g)n = Sn where, g is growth, n denotes number of years, S0 denotes first dividend and Sn

denotes last dividend. [In the above table the number of years will be taken as 4 instead of 5 as

the dividend has increased 4 times between Year 1 and Year 5.]

S0*(1+g)n = Sn

=> 21*(1+g)4=28

=> (1+g)4=28/21

=> (1+g)4=1.3333

=> (1+g)= (1.333)0.25

=> g= (1)- ( 1.0757) = 0.0757 or 7.57%

1

Financial Management is the study of planning, controlling and organizing the finances

of an organisation (Allen, Hemming and Potter, 2013). This report takes capital structure, equity

finance and investment appraisal techniques into consideration of Kadlex Plc, Lexbel Plc and

Happy Meal Limited respectively. It also evaluates the benefits and drawbacks of scrip dividends

and appraisal techniques like ARR, IRR and NPV.

Question 1- Cost of Capital and Capital Structure:

Cost of Capital and Capital structure are an important concept for any organization as they help

in determining the proportion in which the debt and equity must be taken so as to derive

maximum benefit at lowest cost possible. Kadlex plc wants to review its capital structure in order

to minimise its cost of capital (WACC). The following calculations have been worked out to

achieve the same:

Step 1: Calculation of growth (g)

Years

1 21 pence

2 23 pence

3 25 pence

4 27 pence

5 28 pence

S0*(1+g)n = Sn where, g is growth, n denotes number of years, S0 denotes first dividend and Sn

denotes last dividend. [In the above table the number of years will be taken as 4 instead of 5 as

the dividend has increased 4 times between Year 1 and Year 5.]

S0*(1+g)n = Sn

=> 21*(1+g)4=28

=> (1+g)4=28/21

=> (1+g)4=1.3333

=> (1+g)= (1.333)0.25

=> g= (1)- ( 1.0757) = 0.0757 or 7.57%

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

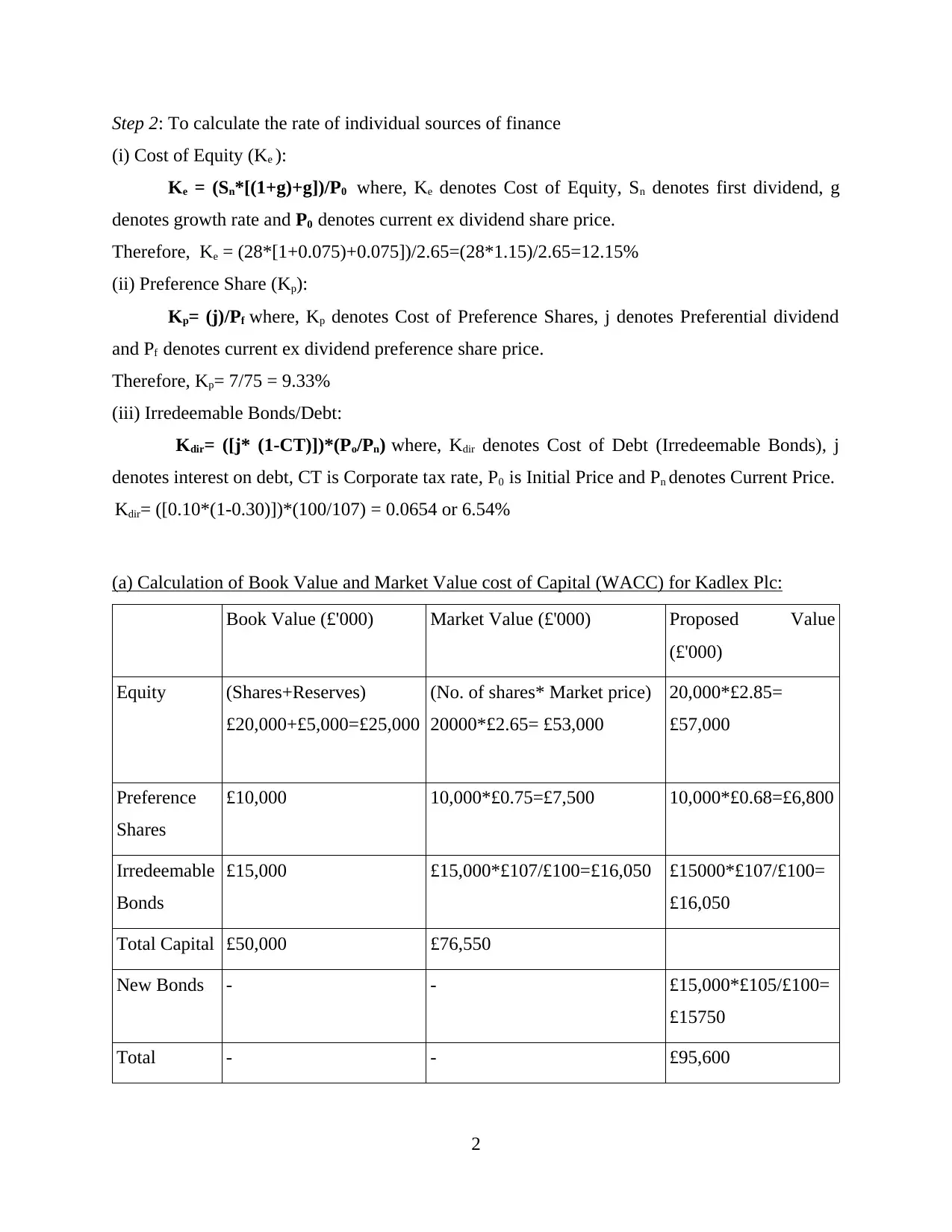

Step 2: To calculate the rate of individual sources of finance

(i) Cost of Equity (Ke ):

Ke = (Sn*[(1+g)+g])/P0 where, Ke denotes Cost of Equity, Sn denotes first dividend, g

denotes growth rate and P0 denotes current ex dividend share price.

Therefore, Ke = (28*[1+0.075)+0.075])/2.65=(28*1.15)/2.65=12.15%

(ii) Preference Share (Kp):

Kp= (j)/Pf where, Kp denotes Cost of Preference Shares, j denotes Preferential dividend

and Pf denotes current ex dividend preference share price.

Therefore, Kp= 7/75 = 9.33%

(iii) Irredeemable Bonds/Debt:

Kdir= ([j* (1-CT)])*(Po/Pn) where, Kdir denotes Cost of Debt (Irredeemable Bonds), j

denotes interest on debt, CT is Corporate tax rate, P0 is Initial Price and Pn denotes Current Price.

Kdir= ([0.10*(1-0.30)])*(100/107) = 0.0654 or 6.54%

(a) Calculation of Book Value and Market Value cost of Capital (WACC) for Kadlex Plc:

Book Value (£'000) Market Value (£'000) Proposed Value

(£'000)

Equity (Shares+Reserves)

£20,000+£5,000=£25,000

(No. of shares* Market price)

20000*£2.65= £53,000

20,000*£2.85=

£57,000

Preference

Shares

£10,000 10,000*£0.75=£7,500 10,000*£0.68=£6,800

Irredeemable

Bonds

£15,000 £15,000*£107/£100=£16,050 £15000*£107/£100=

£16,050

Total Capital £50,000 £76,550

New Bonds - - £15,000*£105/£100=

£15750

Total - - £95,600

2

(i) Cost of Equity (Ke ):

Ke = (Sn*[(1+g)+g])/P0 where, Ke denotes Cost of Equity, Sn denotes first dividend, g

denotes growth rate and P0 denotes current ex dividend share price.

Therefore, Ke = (28*[1+0.075)+0.075])/2.65=(28*1.15)/2.65=12.15%

(ii) Preference Share (Kp):

Kp= (j)/Pf where, Kp denotes Cost of Preference Shares, j denotes Preferential dividend

and Pf denotes current ex dividend preference share price.

Therefore, Kp= 7/75 = 9.33%

(iii) Irredeemable Bonds/Debt:

Kdir= ([j* (1-CT)])*(Po/Pn) where, Kdir denotes Cost of Debt (Irredeemable Bonds), j

denotes interest on debt, CT is Corporate tax rate, P0 is Initial Price and Pn denotes Current Price.

Kdir= ([0.10*(1-0.30)])*(100/107) = 0.0654 or 6.54%

(a) Calculation of Book Value and Market Value cost of Capital (WACC) for Kadlex Plc:

Book Value (£'000) Market Value (£'000) Proposed Value

(£'000)

Equity (Shares+Reserves)

£20,000+£5,000=£25,000

(No. of shares* Market price)

20000*£2.65= £53,000

20,000*£2.85=

£57,000

Preference

Shares

£10,000 10,000*£0.75=£7,500 10,000*£0.68=£6,800

Irredeemable

Bonds

£15,000 £15,000*£107/£100=£16,050 £15000*£107/£100=

£16,050

Total Capital £50,000 £76,550

New Bonds - - £15,000*£105/£100=

£15750

Total - - £95,600

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

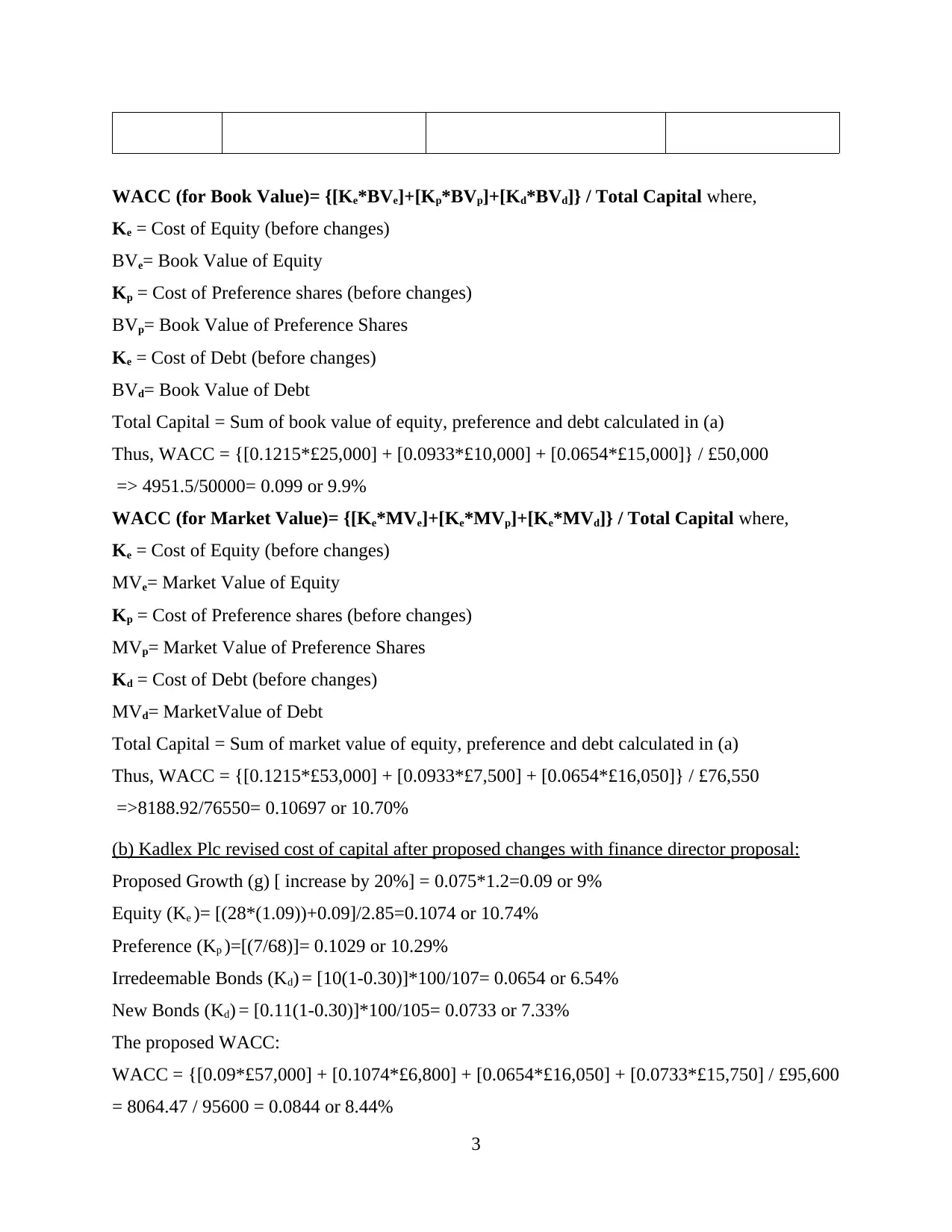

WACC (for Book Value)= {[Ke*BVe]+[Kp*BVp]+[Kd*BVd]} / Total Capital where,

Ke = Cost of Equity (before changes)

BVe= Book Value of Equity

Kp = Cost of Preference shares (before changes)

BVp= Book Value of Preference Shares

Ke = Cost of Debt (before changes)

BVd= Book Value of Debt

Total Capital = Sum of book value of equity, preference and debt calculated in (a)

Thus, WACC = {[0.1215*£25,000] + [0.0933*£10,000] + [0.0654*£15,000]} / £50,000

=> 4951.5/50000= 0.099 or 9.9%

WACC (for Market Value)= {[Ke*MVe]+[Ke*MVp]+[Ke*MVd]} / Total Capital where,

Ke = Cost of Equity (before changes)

MVe= Market Value of Equity

Kp = Cost of Preference shares (before changes)

MVp= Market Value of Preference Shares

Kd = Cost of Debt (before changes)

MVd= MarketValue of Debt

Total Capital = Sum of market value of equity, preference and debt calculated in (a)

Thus, WACC = {[0.1215*£53,000] + [0.0933*£7,500] + [0.0654*£16,050]} / £76,550

=>8188.92/76550= 0.10697 or 10.70%

(b) Kadlex Plc revised cost of capital after proposed changes with finance director proposal:

Proposed Growth (g) [ increase by 20%] = 0.075*1.2=0.09 or 9%

Equity (Ke )= [(28*(1.09))+0.09]/2.85=0.1074 or 10.74%

Preference (Kp )=[(7/68)]= 0.1029 or 10.29%

Irredeemable Bonds (Kd) = [10(1-0.30)]*100/107= 0.0654 or 6.54%

New Bonds (Kd) = [0.11(1-0.30)]*100/105= 0.0733 or 7.33%

The proposed WACC:

WACC = {[0.09*£57,000] + [0.1074*£6,800] + [0.0654*£16,050] + [0.0733*£15,750] / £95,600

= 8064.47 / 95600 = 0.0844 or 8.44%

3

Ke = Cost of Equity (before changes)

BVe= Book Value of Equity

Kp = Cost of Preference shares (before changes)

BVp= Book Value of Preference Shares

Ke = Cost of Debt (before changes)

BVd= Book Value of Debt

Total Capital = Sum of book value of equity, preference and debt calculated in (a)

Thus, WACC = {[0.1215*£25,000] + [0.0933*£10,000] + [0.0654*£15,000]} / £50,000

=> 4951.5/50000= 0.099 or 9.9%

WACC (for Market Value)= {[Ke*MVe]+[Ke*MVp]+[Ke*MVd]} / Total Capital where,

Ke = Cost of Equity (before changes)

MVe= Market Value of Equity

Kp = Cost of Preference shares (before changes)

MVp= Market Value of Preference Shares

Kd = Cost of Debt (before changes)

MVd= MarketValue of Debt

Total Capital = Sum of market value of equity, preference and debt calculated in (a)

Thus, WACC = {[0.1215*£53,000] + [0.0933*£7,500] + [0.0654*£16,050]} / £76,550

=>8188.92/76550= 0.10697 or 10.70%

(b) Kadlex Plc revised cost of capital after proposed changes with finance director proposal:

Proposed Growth (g) [ increase by 20%] = 0.075*1.2=0.09 or 9%

Equity (Ke )= [(28*(1.09))+0.09]/2.85=0.1074 or 10.74%

Preference (Kp )=[(7/68)]= 0.1029 or 10.29%

Irredeemable Bonds (Kd) = [10(1-0.30)]*100/107= 0.0654 or 6.54%

New Bonds (Kd) = [0.11(1-0.30)]*100/105= 0.0733 or 7.33%

The proposed WACC:

WACC = {[0.09*£57,000] + [0.1074*£6,800] + [0.0654*£16,050] + [0.0733*£15,750] / £95,600

= 8064.47 / 95600 = 0.0844 or 8.44%

3

(c) Critical analysis of integrating new capital:

The WACC for the proposal is 8.44% while the market share WACC is 10.70%. Therefore,

Kadlex Company will be able to save a cost of capital (10.70%-8.44%=) 2.26%. This means that

by integrating the proposed capital structure into the existing capital structure of Kadlex Plc, the

minimum weighted average cost of capital can be reduced by 2.26%. As Myers explains cost of

capital can make or break a firm, once this new capital structure has been geared Kadlex can

utilize 2.26% saved costs in other areas for effective allocation of resources such as purchasing

new machinery or any other kind of investment.

(d) Effect of Short-termism on Agency Problem and Bankruptcy:

Short-termism relates to a situation where a company tends to focus on short-term

projects or objectives for earning present profits at the expense of foregoing long-term earnings

or benefits. The following example provides a clear picture of Short-termism on Agency

Problem.

If a finance finance director has 20 million to invest and they are able to:

-in Year 1 get a return of 5 million

-in Year 3 get a return of 10 million

-in Year 5 get a return of 15 million

Of course most of the finance directors will go for the 5 million return because they will

get that money at the end of the first year. Since their jobs are not guaranteed they will look for

their own interests first instead for the company interest. This phenomenon is known as 'Agency

problem' where interests of shareholders are overlooked for personal growth and expansion by a

company. The effects of this phenomenon on bankruptcy and agency problem in a company can

be devastating. Unrelentingly chasing short-term profits can create a gap between the aim of a

company and its operations, as short-termism is caused when managers tend to overuse their

equity funds, the company may not be able to provide dividends and interest payments to their

creditors thus going bankrupt.

Question 2- Long term finance: Equity finance:

(a) Right Issue:

A company may face a situation where the invested capital is not sufficient to carry out

its operational activities on a regular basis. Apart from meeting working capital requirements,

4

The WACC for the proposal is 8.44% while the market share WACC is 10.70%. Therefore,

Kadlex Company will be able to save a cost of capital (10.70%-8.44%=) 2.26%. This means that

by integrating the proposed capital structure into the existing capital structure of Kadlex Plc, the

minimum weighted average cost of capital can be reduced by 2.26%. As Myers explains cost of

capital can make or break a firm, once this new capital structure has been geared Kadlex can

utilize 2.26% saved costs in other areas for effective allocation of resources such as purchasing

new machinery or any other kind of investment.

(d) Effect of Short-termism on Agency Problem and Bankruptcy:

Short-termism relates to a situation where a company tends to focus on short-term

projects or objectives for earning present profits at the expense of foregoing long-term earnings

or benefits. The following example provides a clear picture of Short-termism on Agency

Problem.

If a finance finance director has 20 million to invest and they are able to:

-in Year 1 get a return of 5 million

-in Year 3 get a return of 10 million

-in Year 5 get a return of 15 million

Of course most of the finance directors will go for the 5 million return because they will

get that money at the end of the first year. Since their jobs are not guaranteed they will look for

their own interests first instead for the company interest. This phenomenon is known as 'Agency

problem' where interests of shareholders are overlooked for personal growth and expansion by a

company. The effects of this phenomenon on bankruptcy and agency problem in a company can

be devastating. Unrelentingly chasing short-term profits can create a gap between the aim of a

company and its operations, as short-termism is caused when managers tend to overuse their

equity funds, the company may not be able to provide dividends and interest payments to their

creditors thus going bankrupt.

Question 2- Long term finance: Equity finance:

(a) Right Issue:

A company may face a situation where the invested capital is not sufficient to carry out

its operational activities on a regular basis. Apart from meeting working capital requirements,

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

this fresh capital may be required by the companies for the purpose of expansion and takeovers.

In case a company wants to expand its existing operations, it may adopt the method of Right

Issue. Right Issue helps a firm to raise fresh capital by inviting its existing shareholders to

purchase new shares, called right shares, offered by the company (Aubert and Grudnitski, 2011).

Under this method, existing shareholders get a right to purchase new shares at a discounted

market price on a predetermined future date. These rights act as a compensation to the current

shareholders for dilution of their shareholding value in future due to increase in equity capital.

The shareholders can exercise their right to fully subscribe new shares or sell their rights to

someone else before the date of right issue. They can also ignore these rights. Selling of rights

works in the same way as a shareholder selling a share of the company to someone else.

Lexbel PLC has decided to opt for a right issue in order to raise fresh capital worth

£180,000 to expand its existing operations. The financial director of Lexbel has suggested three

different right issue prices for this at £1.80, £1.60, £1.40. Current Market Price before rights

attached prevailed at £1.90. It has been decided by the management that the rate of return on

shareholder's fund shall remain unchanged at 20%.

Given Information:

Particulars Amount(£)

Existing Shareholder's Funds:

Ordinary shares of 50p each (given) 300000

Reserves (given) 400000

Total Shareholder's Funds 700000

In order to determine the number of shares to be issued, theoretical ex-right issue price,

expected earnings per share (EPS) and form of the issue for each right issue price, following

calculations were carried out:

1. Calculation of number of shares to be issued:

Number of shares to be issued = [Cash to be raised by Lexbel PLC/ Right issue price suggested

by Board]

(i) if right issue price is £1.80:

Number of existing shares of Lexbel PLC (given) = £300,000/0.5 = 600,000 shares

Cash raised by Lexbel (given) = £180,000

5

In case a company wants to expand its existing operations, it may adopt the method of Right

Issue. Right Issue helps a firm to raise fresh capital by inviting its existing shareholders to

purchase new shares, called right shares, offered by the company (Aubert and Grudnitski, 2011).

Under this method, existing shareholders get a right to purchase new shares at a discounted

market price on a predetermined future date. These rights act as a compensation to the current

shareholders for dilution of their shareholding value in future due to increase in equity capital.

The shareholders can exercise their right to fully subscribe new shares or sell their rights to

someone else before the date of right issue. They can also ignore these rights. Selling of rights

works in the same way as a shareholder selling a share of the company to someone else.

Lexbel PLC has decided to opt for a right issue in order to raise fresh capital worth

£180,000 to expand its existing operations. The financial director of Lexbel has suggested three

different right issue prices for this at £1.80, £1.60, £1.40. Current Market Price before rights

attached prevailed at £1.90. It has been decided by the management that the rate of return on

shareholder's fund shall remain unchanged at 20%.

Given Information:

Particulars Amount(£)

Existing Shareholder's Funds:

Ordinary shares of 50p each (given) 300000

Reserves (given) 400000

Total Shareholder's Funds 700000

In order to determine the number of shares to be issued, theoretical ex-right issue price,

expected earnings per share (EPS) and form of the issue for each right issue price, following

calculations were carried out:

1. Calculation of number of shares to be issued:

Number of shares to be issued = [Cash to be raised by Lexbel PLC/ Right issue price suggested

by Board]

(i) if right issue price is £1.80:

Number of existing shares of Lexbel PLC (given) = £300,000/0.5 = 600,000 shares

Cash raised by Lexbel (given) = £180,000

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Therefore, number of shares to be issued = £180,000/£1.80 = 100,000 shares

(ii) if right issue price is £1.60:

Number of existing shares of Lexbel PLC (given) = £300,000/0.5 = 600,000 shares

Cash raised by Lexbel (given) = £180,000

Therefore, number of shares to be issued = £180,000/£1.60 = 112,500 shares

(iii) if right issue price is £1.40:

Number of existing shares of Lexbel PLC (given) = £300,000/0.5 = 600,000 shares

Cash raised by Lexbel (given) = £180,000

Therefore, number of shares to be issued= £180,000/£1.40 = 128571.43 or 128572

shares.

2. Calculation of theoretical ex-right price:

(a) Step 1: Calculating Return on Shareholder's Funds:

Return on Shareholder's Funds @ 20% = total capital by return on shareholder's funds* rate of

return = £700,000* 0.20 = £140,000

(b) Step 2: Value of Lexbel PLC before Rights Issue:

Value of Lexbel PLC before Rights Issue = number of existing shares*current market price (ex-

div)

Note: Current Market Price (ex-div) of share means the prevailing market price of the share

before right issue or the rights attached to the share of a company.

(i) if right issue price is £1.80:

Number of existing shares of Lexbel PLC (given) = £300,000/0.5 = 600,000 shares

Current market price (ex-div) (given) = £1.90

Therefore, value of Lexbel PLC = 600,000*£1.90 = £1,140,000

(ii) if right issue price is £1.60:

Number of existing shares of Lexbel PLC (given) = £300,000/0.5 = 600,000 shares

Current market price (ex-div) (given) = £1.90

Therefore, Value of Lexbel PLC = 600,000*£1.90 = £1,140,000

(iii) if right issue price is £1.40:

Number of existing shares of Lexbel PLC (given) = £300,000/0.5 = 600,000 shares

6

(ii) if right issue price is £1.60:

Number of existing shares of Lexbel PLC (given) = £300,000/0.5 = 600,000 shares

Cash raised by Lexbel (given) = £180,000

Therefore, number of shares to be issued = £180,000/£1.60 = 112,500 shares

(iii) if right issue price is £1.40:

Number of existing shares of Lexbel PLC (given) = £300,000/0.5 = 600,000 shares

Cash raised by Lexbel (given) = £180,000

Therefore, number of shares to be issued= £180,000/£1.40 = 128571.43 or 128572

shares.

2. Calculation of theoretical ex-right price:

(a) Step 1: Calculating Return on Shareholder's Funds:

Return on Shareholder's Funds @ 20% = total capital by return on shareholder's funds* rate of

return = £700,000* 0.20 = £140,000

(b) Step 2: Value of Lexbel PLC before Rights Issue:

Value of Lexbel PLC before Rights Issue = number of existing shares*current market price (ex-

div)

Note: Current Market Price (ex-div) of share means the prevailing market price of the share

before right issue or the rights attached to the share of a company.

(i) if right issue price is £1.80:

Number of existing shares of Lexbel PLC (given) = £300,000/0.5 = 600,000 shares

Current market price (ex-div) (given) = £1.90

Therefore, value of Lexbel PLC = 600,000*£1.90 = £1,140,000

(ii) if right issue price is £1.60:

Number of existing shares of Lexbel PLC (given) = £300,000/0.5 = 600,000 shares

Current market price (ex-div) (given) = £1.90

Therefore, Value of Lexbel PLC = 600,000*£1.90 = £1,140,000

(iii) if right issue price is £1.40:

Number of existing shares of Lexbel PLC (given) = £300,000/0.5 = 600,000 shares

6

Current market price (ex-div) (given) = £1.90

Therefore, Value of Lexbel PLC = 600,000*£1.90 = £1,140,000

(c) Step 3: Value of Lexbel PLC after Rights Issue:

Value of Lexbel PLC after Rights Issue = Value of Lexbel PLC before right issue+ Cash to be

raised

(i) if right issue price is £1.80:

Value of Lexbel PLC before right issue = £1,140,000

Cash raised by Lexbel (given) = £180,000

Therefore, value of Lexbel PLC = £1,140,000+ £180,000 = £1,320,000

(ii) if right issue price is £1.60:

Value of Lexbel PLC before right issue = £1,140,000

Cash raised by Lexbel (given) = £180,000

Therefore, value of Lexbel PLC = £1,140,000+ £180,000 = £1,320,000

(iii) if right issue price is £1.40:

Value of Lexbel PLC before right issue = £1,140,000

Cash raised by Lexbel (given) = £180,000

Therefore, value of Lexbel PLC = £1,140,000+ £180,000 = £1,320,000

(d) Step 4: Theoretical Ex-Right Issue Price

Theoretical Ex-Rights price per share is the estimated market price of the share that it

will have after a right issue is carried out by the company, in theory. The actual ex-rights price

per share may be same or different from theoretical ex-right price of share.

Theoretical Ex-Rights price per share = value of Lexbel PLC after right issue/ total number of

shares

Total Number of Shares = Existing shares + New Shares

Theoretical Ex-Rights price under three given scenarios is shown below:

(i) if right issue price is £1.80:

Value of Lexbel PLC after right issue = £1,132,000

Total Number of shares = 600,000+ 100,000 = 700,000 shares

Therefore, Theoretical Ex-Rights price = £1,132,000/700,000 = £1.89

7

Therefore, Value of Lexbel PLC = 600,000*£1.90 = £1,140,000

(c) Step 3: Value of Lexbel PLC after Rights Issue:

Value of Lexbel PLC after Rights Issue = Value of Lexbel PLC before right issue+ Cash to be

raised

(i) if right issue price is £1.80:

Value of Lexbel PLC before right issue = £1,140,000

Cash raised by Lexbel (given) = £180,000

Therefore, value of Lexbel PLC = £1,140,000+ £180,000 = £1,320,000

(ii) if right issue price is £1.60:

Value of Lexbel PLC before right issue = £1,140,000

Cash raised by Lexbel (given) = £180,000

Therefore, value of Lexbel PLC = £1,140,000+ £180,000 = £1,320,000

(iii) if right issue price is £1.40:

Value of Lexbel PLC before right issue = £1,140,000

Cash raised by Lexbel (given) = £180,000

Therefore, value of Lexbel PLC = £1,140,000+ £180,000 = £1,320,000

(d) Step 4: Theoretical Ex-Right Issue Price

Theoretical Ex-Rights price per share is the estimated market price of the share that it

will have after a right issue is carried out by the company, in theory. The actual ex-rights price

per share may be same or different from theoretical ex-right price of share.

Theoretical Ex-Rights price per share = value of Lexbel PLC after right issue/ total number of

shares

Total Number of Shares = Existing shares + New Shares

Theoretical Ex-Rights price under three given scenarios is shown below:

(i) if right issue price is £1.80:

Value of Lexbel PLC after right issue = £1,132,000

Total Number of shares = 600,000+ 100,000 = 700,000 shares

Therefore, Theoretical Ex-Rights price = £1,132,000/700,000 = £1.89

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

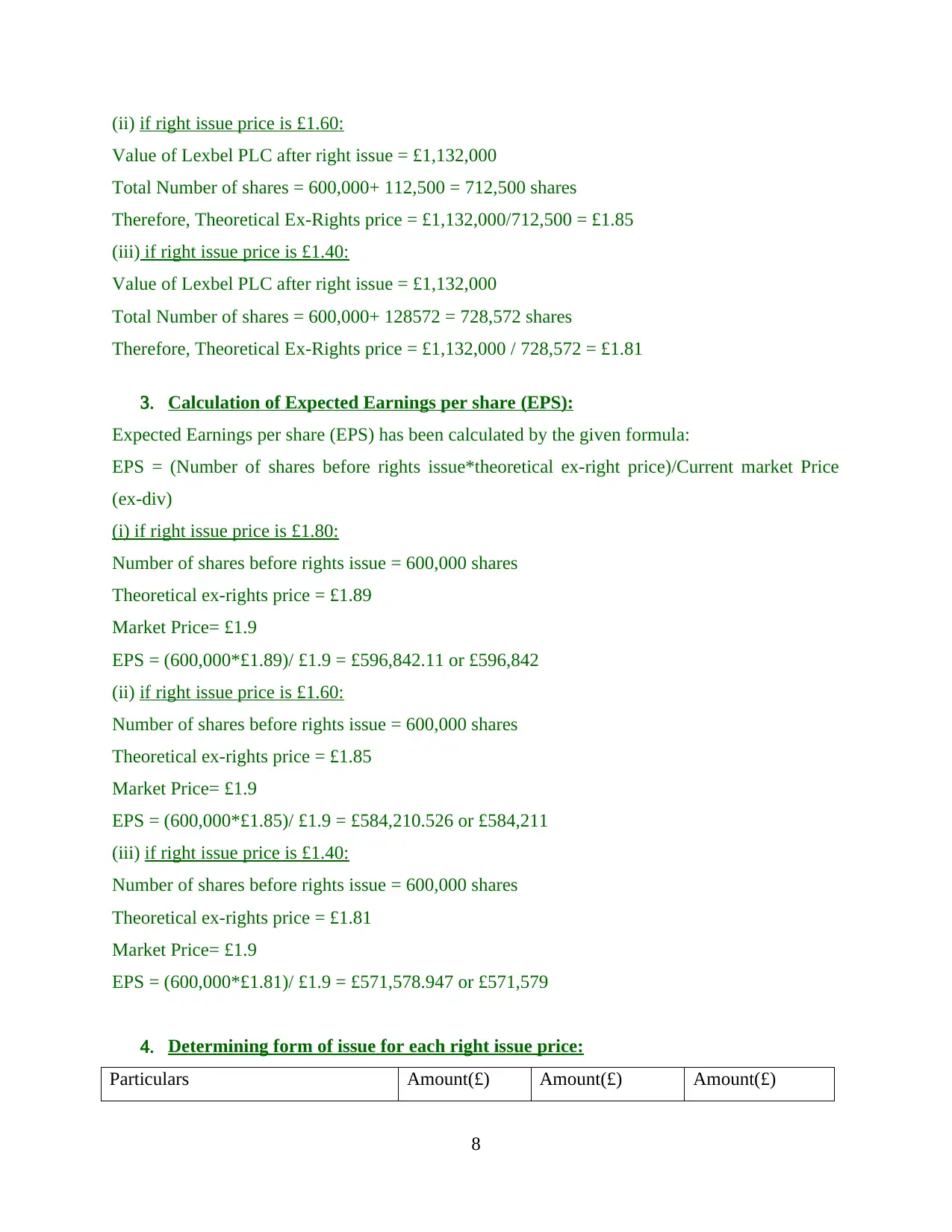

(ii) if right issue price is £1.60:

Value of Lexbel PLC after right issue = £1,132,000

Total Number of shares = 600,000+ 112,500 = 712,500 shares

Therefore, Theoretical Ex-Rights price = £1,132,000/712,500 = £1.85

(iii) if right issue price is £1.40:

Value of Lexbel PLC after right issue = £1,132,000

Total Number of shares = 600,000+ 128572 = 728,572 shares

Therefore, Theoretical Ex-Rights price = £1,132,000 / 728,572 = £1.81

3. Calculation of Expected Earnings per share (EPS):

Expected Earnings per share (EPS) has been calculated by the given formula:

EPS = (Number of shares before rights issue*theoretical ex-right price)/Current market Price

(ex-div)

(i) if right issue price is £1.80:

Number of shares before rights issue = 600,000 shares

Theoretical ex-rights price = £1.89

Market Price= £1.9

EPS = (600,000*£1.89)/ £1.9 = £596,842.11 or £596,842

(ii) if right issue price is £1.60:

Number of shares before rights issue = 600,000 shares

Theoretical ex-rights price = £1.85

Market Price= £1.9

EPS = (600,000*£1.85)/ £1.9 = £584,210.526 or £584,211

(iii) if right issue price is £1.40:

Number of shares before rights issue = 600,000 shares

Theoretical ex-rights price = £1.81

Market Price= £1.9

EPS = (600,000*£1.81)/ £1.9 = £571,578.947 or £571,579

4. Determining form of issue for each right issue price:

Particulars Amount(£) Amount(£) Amount(£)

8

Value of Lexbel PLC after right issue = £1,132,000

Total Number of shares = 600,000+ 112,500 = 712,500 shares

Therefore, Theoretical Ex-Rights price = £1,132,000/712,500 = £1.85

(iii) if right issue price is £1.40:

Value of Lexbel PLC after right issue = £1,132,000

Total Number of shares = 600,000+ 128572 = 728,572 shares

Therefore, Theoretical Ex-Rights price = £1,132,000 / 728,572 = £1.81

3. Calculation of Expected Earnings per share (EPS):

Expected Earnings per share (EPS) has been calculated by the given formula:

EPS = (Number of shares before rights issue*theoretical ex-right price)/Current market Price

(ex-div)

(i) if right issue price is £1.80:

Number of shares before rights issue = 600,000 shares

Theoretical ex-rights price = £1.89

Market Price= £1.9

EPS = (600,000*£1.89)/ £1.9 = £596,842.11 or £596,842

(ii) if right issue price is £1.60:

Number of shares before rights issue = 600,000 shares

Theoretical ex-rights price = £1.85

Market Price= £1.9

EPS = (600,000*£1.85)/ £1.9 = £584,210.526 or £584,211

(iii) if right issue price is £1.40:

Number of shares before rights issue = 600,000 shares

Theoretical ex-rights price = £1.81

Market Price= £1.9

EPS = (600,000*£1.81)/ £1.9 = £571,578.947 or £571,579

4. Determining form of issue for each right issue price:

Particulars Amount(£) Amount(£) Amount(£)

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

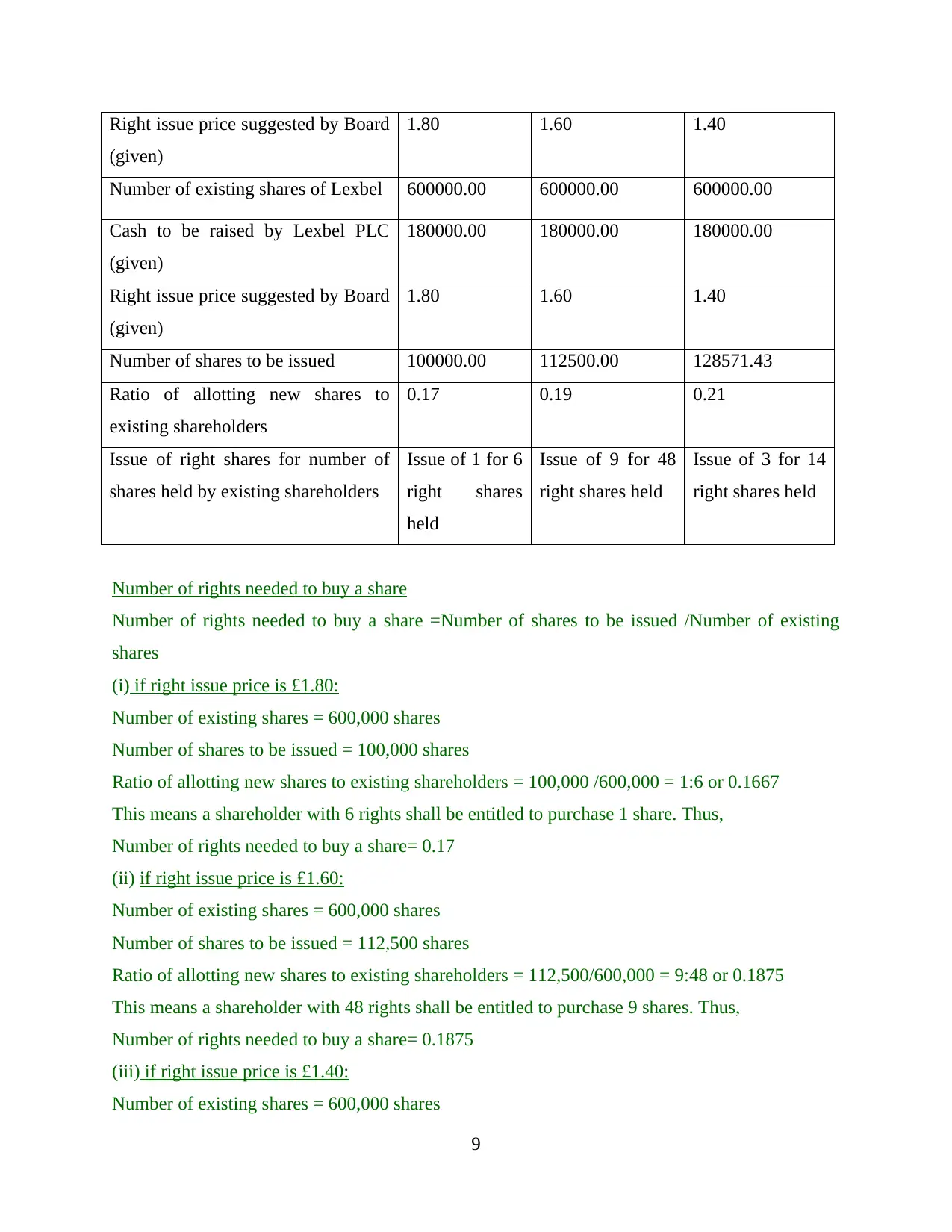

Right issue price suggested by Board

(given)

1.80 1.60 1.40

Number of existing shares of Lexbel 600000.00 600000.00 600000.00

Cash to be raised by Lexbel PLC

(given)

180000.00 180000.00 180000.00

Right issue price suggested by Board

(given)

1.80 1.60 1.40

Number of shares to be issued 100000.00 112500.00 128571.43

Ratio of allotting new shares to

existing shareholders

0.17 0.19 0.21

Issue of right shares for number of

shares held by existing shareholders

Issue of 1 for 6

right shares

held

Issue of 9 for 48

right shares held

Issue of 3 for 14

right shares held

Number of rights needed to buy a share

Number of rights needed to buy a share =Number of shares to be issued /Number of existing

shares

(i) if right issue price is £1.80:

Number of existing shares = 600,000 shares

Number of shares to be issued = 100,000 shares

Ratio of allotting new shares to existing shareholders = 100,000 /600,000 = 1:6 or 0.1667

This means a shareholder with 6 rights shall be entitled to purchase 1 share. Thus,

Number of rights needed to buy a share= 0.17

(ii) if right issue price is £1.60:

Number of existing shares = 600,000 shares

Number of shares to be issued = 112,500 shares

Ratio of allotting new shares to existing shareholders = 112,500/600,000 = 9:48 or 0.1875

This means a shareholder with 48 rights shall be entitled to purchase 9 shares. Thus,

Number of rights needed to buy a share= 0.1875

(iii) if right issue price is £1.40:

Number of existing shares = 600,000 shares

9

(given)

1.80 1.60 1.40

Number of existing shares of Lexbel 600000.00 600000.00 600000.00

Cash to be raised by Lexbel PLC

(given)

180000.00 180000.00 180000.00

Right issue price suggested by Board

(given)

1.80 1.60 1.40

Number of shares to be issued 100000.00 112500.00 128571.43

Ratio of allotting new shares to

existing shareholders

0.17 0.19 0.21

Issue of right shares for number of

shares held by existing shareholders

Issue of 1 for 6

right shares

held

Issue of 9 for 48

right shares held

Issue of 3 for 14

right shares held

Number of rights needed to buy a share

Number of rights needed to buy a share =Number of shares to be issued /Number of existing

shares

(i) if right issue price is £1.80:

Number of existing shares = 600,000 shares

Number of shares to be issued = 100,000 shares

Ratio of allotting new shares to existing shareholders = 100,000 /600,000 = 1:6 or 0.1667

This means a shareholder with 6 rights shall be entitled to purchase 1 share. Thus,

Number of rights needed to buy a share= 0.17

(ii) if right issue price is £1.60:

Number of existing shares = 600,000 shares

Number of shares to be issued = 112,500 shares

Ratio of allotting new shares to existing shareholders = 112,500/600,000 = 9:48 or 0.1875

This means a shareholder with 48 rights shall be entitled to purchase 9 shares. Thus,

Number of rights needed to buy a share= 0.1875

(iii) if right issue price is £1.40:

Number of existing shares = 600,000 shares

9

Number of shares to be issued = 128,572 shares

Ratio of allotting new shares to existing shareholders = 128,572 /600,000 = 3:14 or 0.2143

This means a shareholder with 14 rights shall be entitled to purchase 3 shares. Thus,

Number of rights needed to buy a share= 0.2143

Therefore, value of one right = (£1.90-£1.80)/6= 0.467

The form of issue for each right issue price can be determined as follows:

For right issue price of £1.80, the number of shares that would be raised by the

company would be 1,00,000 shares. Hence, on a pro-rata basis, 1 new share will be

allotted for every 6 shares held by them (Brigham and Houston, 2012).

For right issue price of £1.60, the number shares of that would be raised by the

company would be 1,12,500 shares. Hence, on a pro-rata basis, 9 new shares will be

allotted for every 48 shares held by them.

For right issue price of £1.40, the number shares of that would be raised by the

company would be 128571 shares (rounded-off). Hence, on a pro-rata basis, 3 new

shares will be allotted for every 14 shares held by them.

5. Interpreting the results:

It can be concluded from the above calculations that the suggested right issue price of

£1.80 generates more Earnings Per Share (EPS) for Lexbel Plc worth $596,842 than other two

suggested issue prices with 1 share allotted to every 6 shares held by a shareholder it is

recommended to assume this price for right issue.

(b) Scrip Dividends:

As mentioned by the case, it has become common for the companies to offer their

shareholders a choice between a cash dividend and an equivalent scrip dividend (Brooks and

Mukherjee, 2013). Scrip dividends are a type of dividend payment method adopted by the

companies to pay their shareholders in form of shares instead of cash. A scrip issue and a scrip

dividend are two different concepts. Scrip dividends essentially relate to payment of dividend in

kind rather than cash whereas a scrip issue is a bonus issue of shares offered to the shareholders

of the company. The advantages and disadvantages of a scrip dividend from shareholders as well

as company's point of view have been enlisted below: Advantages of Scrip Dividend:

10

Ratio of allotting new shares to existing shareholders = 128,572 /600,000 = 3:14 or 0.2143

This means a shareholder with 14 rights shall be entitled to purchase 3 shares. Thus,

Number of rights needed to buy a share= 0.2143

Therefore, value of one right = (£1.90-£1.80)/6= 0.467

The form of issue for each right issue price can be determined as follows:

For right issue price of £1.80, the number of shares that would be raised by the

company would be 1,00,000 shares. Hence, on a pro-rata basis, 1 new share will be

allotted for every 6 shares held by them (Brigham and Houston, 2012).

For right issue price of £1.60, the number shares of that would be raised by the

company would be 1,12,500 shares. Hence, on a pro-rata basis, 9 new shares will be

allotted for every 48 shares held by them.

For right issue price of £1.40, the number shares of that would be raised by the

company would be 128571 shares (rounded-off). Hence, on a pro-rata basis, 3 new

shares will be allotted for every 14 shares held by them.

5. Interpreting the results:

It can be concluded from the above calculations that the suggested right issue price of

£1.80 generates more Earnings Per Share (EPS) for Lexbel Plc worth $596,842 than other two

suggested issue prices with 1 share allotted to every 6 shares held by a shareholder it is

recommended to assume this price for right issue.

(b) Scrip Dividends:

As mentioned by the case, it has become common for the companies to offer their

shareholders a choice between a cash dividend and an equivalent scrip dividend (Brooks and

Mukherjee, 2013). Scrip dividends are a type of dividend payment method adopted by the

companies to pay their shareholders in form of shares instead of cash. A scrip issue and a scrip

dividend are two different concepts. Scrip dividends essentially relate to payment of dividend in

kind rather than cash whereas a scrip issue is a bonus issue of shares offered to the shareholders

of the company. The advantages and disadvantages of a scrip dividend from shareholders as well

as company's point of view have been enlisted below: Advantages of Scrip Dividend:

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.