Corporate Financial Management: Capital Budgeting Techniques Analysis

VerifiedAdded on 2019/11/12

|10

|2546

|282

Report

AI Summary

This report delves into various capital budgeting techniques crucial for corporate financial management. It begins by explaining sensitivity analysis, a method used to assess the impact of changes in key variables on investment outcomes. The report then explores scenario analysis, which evaluates project viability under different economic and market conditions, considering optimistic, moderate, and conservative scenarios. Break-even analysis is also examined, highlighting how companies determine the sales level needed to cover costs and achieve profitability, with a focus on cost-volume-profit analysis. Finally, the report discusses simulation techniques, particularly the Monte Carlo approach, for modeling uncertainties in cash flows and aiding in investment appraisal. The report concludes by emphasizing the significance of these techniques in managing risk and making sound capital budgeting decisions, essential for the financial health and sustainable growth of a business enterprise. The references include the work of various authors in the field of finance and capital budgeting.

Corporate Financial Management

1 | P a g e

1 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Sensitivity analysis......................................................................................................................................3

Scenario Analysis........................................................................................................................................4

Break-Even Analysis...................................................................................................................................5

Simulation techniques.................................................................................................................................6

Conclusion...................................................................................................................................................8

2 | P a g e

Sensitivity analysis......................................................................................................................................3

Scenario Analysis........................................................................................................................................4

Break-Even Analysis...................................................................................................................................5

Simulation techniques.................................................................................................................................6

Conclusion...................................................................................................................................................8

2 | P a g e

Under the different tools and techniques of capital budgeting, the management of the company

considers the various capital outlays that it has under its proposals. The main exercise that is

involved in the overall process of capital budgeting is to correlate the various benefits that are to

be achieved over the period of time and consistency of performance that helps in maximizing the

overall objective of the business. Management has to analyze risk as a key function of financial

management. As it is generally seen that the long term investment decisions tend to be

complicated in nature, there exist a high vulnerability of external risk and uncertainty. As the

acquisition of business Assets and resources are the activities which are continuous and nature,

therefore management should utilise their expertise in order to evaluate correct and fair valuation

of business enterprise. In the current assignment, the analyst discussed over different concepts

that are in relation to utilisation of capital budgeting techniques and a business enterprise. Some

of them are discussed as follows -

Sensitivity analysis – Approach of investing in assets related to business are the major reasons

for growth and development of the business enterprise. The company with the objective of

achieving long term goals with timely approach must take efficient decision on the part of capital

investments. Growth and development of the business organization are not only achieved

through the purchase of new machinery and equipment but also expanding business operations

through developing new products and services. Before investing and placing money into a

project it is greatly required to understand and evaluate the associated risk, business strengths

and weaknesses (Жамойда & Мацюк, 2011). Though risk cannot be completely avoided, but it

should be minimised to acceptable business appetite. For this purpose management of the

business, the organization must conduct sensitivity analysis as a part of capital budgeting

technique in order to evaluate the possible risk and effectiveness of investment opportunities

(Bennouna, et. al., 2010).

Sensitivity analysis as a part of capital budgeting techniques supports the business managers to

evaluate the uncertain situations. As in a General scenario business activities are based on

forecasts which are determined on the basis of certain assumptions and estimates. The technique

of sensitivity analysis focuses on the part wherein the impact on the financial part of the

company is visualised while making changes in assumptions and business estimates. The tool of

3 | P a g e

considers the various capital outlays that it has under its proposals. The main exercise that is

involved in the overall process of capital budgeting is to correlate the various benefits that are to

be achieved over the period of time and consistency of performance that helps in maximizing the

overall objective of the business. Management has to analyze risk as a key function of financial

management. As it is generally seen that the long term investment decisions tend to be

complicated in nature, there exist a high vulnerability of external risk and uncertainty. As the

acquisition of business Assets and resources are the activities which are continuous and nature,

therefore management should utilise their expertise in order to evaluate correct and fair valuation

of business enterprise. In the current assignment, the analyst discussed over different concepts

that are in relation to utilisation of capital budgeting techniques and a business enterprise. Some

of them are discussed as follows -

Sensitivity analysis – Approach of investing in assets related to business are the major reasons

for growth and development of the business enterprise. The company with the objective of

achieving long term goals with timely approach must take efficient decision on the part of capital

investments. Growth and development of the business organization are not only achieved

through the purchase of new machinery and equipment but also expanding business operations

through developing new products and services. Before investing and placing money into a

project it is greatly required to understand and evaluate the associated risk, business strengths

and weaknesses (Жамойда & Мацюк, 2011). Though risk cannot be completely avoided, but it

should be minimised to acceptable business appetite. For this purpose management of the

business, the organization must conduct sensitivity analysis as a part of capital budgeting

technique in order to evaluate the possible risk and effectiveness of investment opportunities

(Bennouna, et. al., 2010).

Sensitivity analysis as a part of capital budgeting techniques supports the business managers to

evaluate the uncertain situations. As in a General scenario business activities are based on

forecasts which are determined on the basis of certain assumptions and estimates. The technique

of sensitivity analysis focuses on the part wherein the impact on the financial part of the

company is visualised while making changes in assumptions and business estimates. The tool of

3 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

sensitivity analysis evaluates the possible risk while determining the various variables that place

an effect on the performance of the investment and associated net benefits. Various effects on

changes made in the variable while conducting internal rate of return technique and net present

value technique are analyzed and reported as a part of sensitivity analysis. The analyst using this

report identifies various possible risk event and their resulted outcome and consequences if the

above risk materialized (Correia & Cramer, 2008).

Using this approach overall project feasibility is determined. Using net present value technique

as a part of capital budgeting approach various independent variables are needed to be changed

in order to determine the possible risk. Some of these variables are -

Expected revenue

Budgeted selling price

Budgeted cost of the investment

Initial cost of the project

Rate of return

Interest to be paid on loan etc

For instance, sensitivity analysis taken as part of capital budgeting techniques and calculation, it

changes one part of the estimates that have been forecasted on the initial stage and accordingly

the changes in results are to be evaluated. For example, in the case while taking projected cash

flow for the next 10 years to determine the net present value of the investment the business

organization took 8 % projected cost of capital. In this situation analysis, the analyst has three

variables which can be changed accordingly to notice the effective change in the net present

value of the project (Carmichael & Balatbat, 2008). There can be a variation witnessed over the

period of time in the variables of time duration, the rate of cost of capital, and projected inflows.

Scenario Analysis

Scenario Analysis is an analysis of Net Present Value (NPV) or Internal Rate of Return (IRR) of

a forecast under various important scenarios, based on industry, firm economic factors, and

macro-economic factors. It is a process of considering various future uncertain events by

considering their alternative predictable outcomes. When future projection is made scenario

4 | P a g e

an effect on the performance of the investment and associated net benefits. Various effects on

changes made in the variable while conducting internal rate of return technique and net present

value technique are analyzed and reported as a part of sensitivity analysis. The analyst using this

report identifies various possible risk event and their resulted outcome and consequences if the

above risk materialized (Correia & Cramer, 2008).

Using this approach overall project feasibility is determined. Using net present value technique

as a part of capital budgeting approach various independent variables are needed to be changed

in order to determine the possible risk. Some of these variables are -

Expected revenue

Budgeted selling price

Budgeted cost of the investment

Initial cost of the project

Rate of return

Interest to be paid on loan etc

For instance, sensitivity analysis taken as part of capital budgeting techniques and calculation, it

changes one part of the estimates that have been forecasted on the initial stage and accordingly

the changes in results are to be evaluated. For example, in the case while taking projected cash

flow for the next 10 years to determine the net present value of the investment the business

organization took 8 % projected cost of capital. In this situation analysis, the analyst has three

variables which can be changed accordingly to notice the effective change in the net present

value of the project (Carmichael & Balatbat, 2008). There can be a variation witnessed over the

period of time in the variables of time duration, the rate of cost of capital, and projected inflows.

Scenario Analysis

Scenario Analysis is an analysis of Net Present Value (NPV) or Internal Rate of Return (IRR) of

a forecast under various important scenarios, based on industry, firm economic factors, and

macro-economic factors. It is a process of considering various future uncertain events by

considering their alternative predictable outcomes. When future projection is made scenario

4 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

analysis is considered to be a main factor. Then the various observations have been made

regarding the future outcome and several developments have made to change the predictable

outcomes. Scenario analysis is not based on the past data or historical data of the company. In

scenario analysis the analyst expects that the past observations not remain same in the

foreseeable future (Dedi & Orsag, 2007). Every scenario combines optimistic, predictable

situations which affects the working of the company in the near future.

Scenario Analysis is plotted to permit improved decision making and planning by considering

the various possible outcomes. In financial sector, financial institution might use scenario

analysis to predict various possible situations for the economy (e.g. aggressive growth, moderate

growth, conservative growth) and for the market returns (for stocks, bonds, cash and cash

equivalents) in all of the scenarios. Financial institutions also made scenario analysis to predict

the return on investments. Scenario planning starts by dividing the knowledge into two broad

areas: 1 component we consider uncertain or unknowable and 2 things we believe we know

anything about (Khamees, et. al., 2010). It is the process of estimating the predictable value of

the portfolio after a stipulated period of time, assuming that the securities in the portfolio has

changed or key factors change such as change in the rate of interest on securities.

There are many perspective of scenario analysis. A most and common method is to determine the

risk of the portfolio by computing the standard deviation of monthly or daily returns of the

portfolio. A consumer or group of person can use scenario analysis to examine the various

financial possibilities of purchasing a product. Mathematics and Statistics plays an important role

in the scenario analysis. Most managers use scenario analysis in their company is for framing a

plan or in a decision making process to determine the best situation for maximizing the profits of

the business and they also use this analysis to determine the worst possible outcome and

anticipate operational losses and effective problems (Adair, 2011). This analysis also used in

determining the net present value of the business in the near future.

Break-Even Analysis

Break even analysis is that analysis which determine the point at which sales of the company

equals the cost associated with receiving the revenue. In alternate way we can say that break-

even is that point where profit of the company is zero. Entities used Break even analysis to

5 | P a g e

regarding the future outcome and several developments have made to change the predictable

outcomes. Scenario analysis is not based on the past data or historical data of the company. In

scenario analysis the analyst expects that the past observations not remain same in the

foreseeable future (Dedi & Orsag, 2007). Every scenario combines optimistic, predictable

situations which affects the working of the company in the near future.

Scenario Analysis is plotted to permit improved decision making and planning by considering

the various possible outcomes. In financial sector, financial institution might use scenario

analysis to predict various possible situations for the economy (e.g. aggressive growth, moderate

growth, conservative growth) and for the market returns (for stocks, bonds, cash and cash

equivalents) in all of the scenarios. Financial institutions also made scenario analysis to predict

the return on investments. Scenario planning starts by dividing the knowledge into two broad

areas: 1 component we consider uncertain or unknowable and 2 things we believe we know

anything about (Khamees, et. al., 2010). It is the process of estimating the predictable value of

the portfolio after a stipulated period of time, assuming that the securities in the portfolio has

changed or key factors change such as change in the rate of interest on securities.

There are many perspective of scenario analysis. A most and common method is to determine the

risk of the portfolio by computing the standard deviation of monthly or daily returns of the

portfolio. A consumer or group of person can use scenario analysis to examine the various

financial possibilities of purchasing a product. Mathematics and Statistics plays an important role

in the scenario analysis. Most managers use scenario analysis in their company is for framing a

plan or in a decision making process to determine the best situation for maximizing the profits of

the business and they also use this analysis to determine the worst possible outcome and

anticipate operational losses and effective problems (Adair, 2011). This analysis also used in

determining the net present value of the business in the near future.

Break-Even Analysis

Break even analysis is that analysis which determine the point at which sales of the company

equals the cost associated with receiving the revenue. In alternate way we can say that break-

even is that point where profit of the company is zero. Entities used Break even analysis to

5 | P a g e

determine the level of units which company has to sell in order to cover their total fixed costs.

Break even analysis concept deals with the contribution margin of the product. The contribution

is the difference between the sales and the total variable costs. And the contribution margin is the

difference of selling price and total variable cost per unit (Verma, et. al., 2009). Break even

analysis plays a vital role in determining the practical application of cost related functions. It

consist three factors, i.e sales volume, cost and profit. The aim of this analysis is to classify the

between sales volume and total costs of the company. It is also known as cost-volume-profit-

analysis. It helps in understanding the operating condition that exists when an entity ‘break-

even’. This is also known as no profit no loss point.

This analysis has very useful to the company and the executives of the company takes

forecasting decisions and make future planning by considering the break-even of the company.

In break-even analysis a break even chart has made by the managerial economists, company

executives and government agencies in order to find the break-even point. In the break even

chart total fixed cost, total revenue and total variable cost are shown separately (Bierman Jr &

Smidt, 2012). This break even chart shows the level of profit or loss to the entity at various levels

of activity.

In the situation of term loans, the institutions which have a business of finance have to find out

the possibility that the person who took the loan can repay the loan. In such case they had to find

the level of break-even point not only the total cost of the company are required but also the full

debt of the person. That level of break-even is called cash break-even. A firm has to decide the

most economical course of production both at planning level and expansion level. The break-

even analysis is the most helpful in determining the best course of action. For management, the

best use of break-even analysis is that they present a microscopic picture of the profit of the

company and it helps in determining the business model of the company. Despite some

limitations break even analysis has its own utility in managerial decision making. Considering

the above technique as a part of the management tool for the purpose of taking short term

decision it is considered highly worthwhile. Utilising this approach into current business

condition works out as an additional advantage for a business manager to incorporate the

fluctuations and changes that exist in the external micro environment due to its flexible

behaviour (James, et. al., 2010).

6 | P a g e

Break even analysis concept deals with the contribution margin of the product. The contribution

is the difference between the sales and the total variable costs. And the contribution margin is the

difference of selling price and total variable cost per unit (Verma, et. al., 2009). Break even

analysis plays a vital role in determining the practical application of cost related functions. It

consist three factors, i.e sales volume, cost and profit. The aim of this analysis is to classify the

between sales volume and total costs of the company. It is also known as cost-volume-profit-

analysis. It helps in understanding the operating condition that exists when an entity ‘break-

even’. This is also known as no profit no loss point.

This analysis has very useful to the company and the executives of the company takes

forecasting decisions and make future planning by considering the break-even of the company.

In break-even analysis a break even chart has made by the managerial economists, company

executives and government agencies in order to find the break-even point. In the break even

chart total fixed cost, total revenue and total variable cost are shown separately (Bierman Jr &

Smidt, 2012). This break even chart shows the level of profit or loss to the entity at various levels

of activity.

In the situation of term loans, the institutions which have a business of finance have to find out

the possibility that the person who took the loan can repay the loan. In such case they had to find

the level of break-even point not only the total cost of the company are required but also the full

debt of the person. That level of break-even is called cash break-even. A firm has to decide the

most economical course of production both at planning level and expansion level. The break-

even analysis is the most helpful in determining the best course of action. For management, the

best use of break-even analysis is that they present a microscopic picture of the profit of the

company and it helps in determining the business model of the company. Despite some

limitations break even analysis has its own utility in managerial decision making. Considering

the above technique as a part of the management tool for the purpose of taking short term

decision it is considered highly worthwhile. Utilising this approach into current business

condition works out as an additional advantage for a business manager to incorporate the

fluctuations and changes that exist in the external micro environment due to its flexible

behaviour (James, et. al., 2010).

6 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Simulation techniques

Simulation technique as a part of capital budgeting methodology provides a natural and logical

model in which various situations are analysed and a model is created for better decision making

process. Various conditions in the real life business structure are analysed in order to formulate

the better structuring of the future possible conditions. All aspects related to business are taken

into study to make the sample structure on a wider part. Various variables forming part of the

problems is identified that places an overall effect over the implementation part. The probable

uncertain behaviour and outcomes in form of cash outflows are analysed as part of simulation

techniques. Utilising the approach of Weingartner's Basic Horizon model as part of capital

budgeting technique expected return on the investment is to be computed. The management

utilising the simulation technique for its investment appraisal proposals is supported while

evaluating the portfolio and generating the same for the organisation (Kwak & Ingall, 2007). The

business can follow up the technique as presented by the Monte Carlo simulation approach in

order to identify the probable risk and uncertainty that exist while determining the accuracy in

the projected discounted cash flows associated with the project.

The current approach of simulation reduces the shortcomings and lacking that does exist in the

approach of scenario and sensitivity analysis. In spite of focusing on the impact on the

performance due the change in the variable the analyst in the current approach takes random

variable for each input and determines Net present value for each probable condition.

7 | P a g e

Simulation technique as a part of capital budgeting methodology provides a natural and logical

model in which various situations are analysed and a model is created for better decision making

process. Various conditions in the real life business structure are analysed in order to formulate

the better structuring of the future possible conditions. All aspects related to business are taken

into study to make the sample structure on a wider part. Various variables forming part of the

problems is identified that places an overall effect over the implementation part. The probable

uncertain behaviour and outcomes in form of cash outflows are analysed as part of simulation

techniques. Utilising the approach of Weingartner's Basic Horizon model as part of capital

budgeting technique expected return on the investment is to be computed. The management

utilising the simulation technique for its investment appraisal proposals is supported while

evaluating the portfolio and generating the same for the organisation (Kwak & Ingall, 2007). The

business can follow up the technique as presented by the Monte Carlo simulation approach in

order to identify the probable risk and uncertainty that exist while determining the accuracy in

the projected discounted cash flows associated with the project.

The current approach of simulation reduces the shortcomings and lacking that does exist in the

approach of scenario and sensitivity analysis. In spite of focusing on the impact on the

performance due the change in the variable the analyst in the current approach takes random

variable for each input and determines Net present value for each probable condition.

7 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

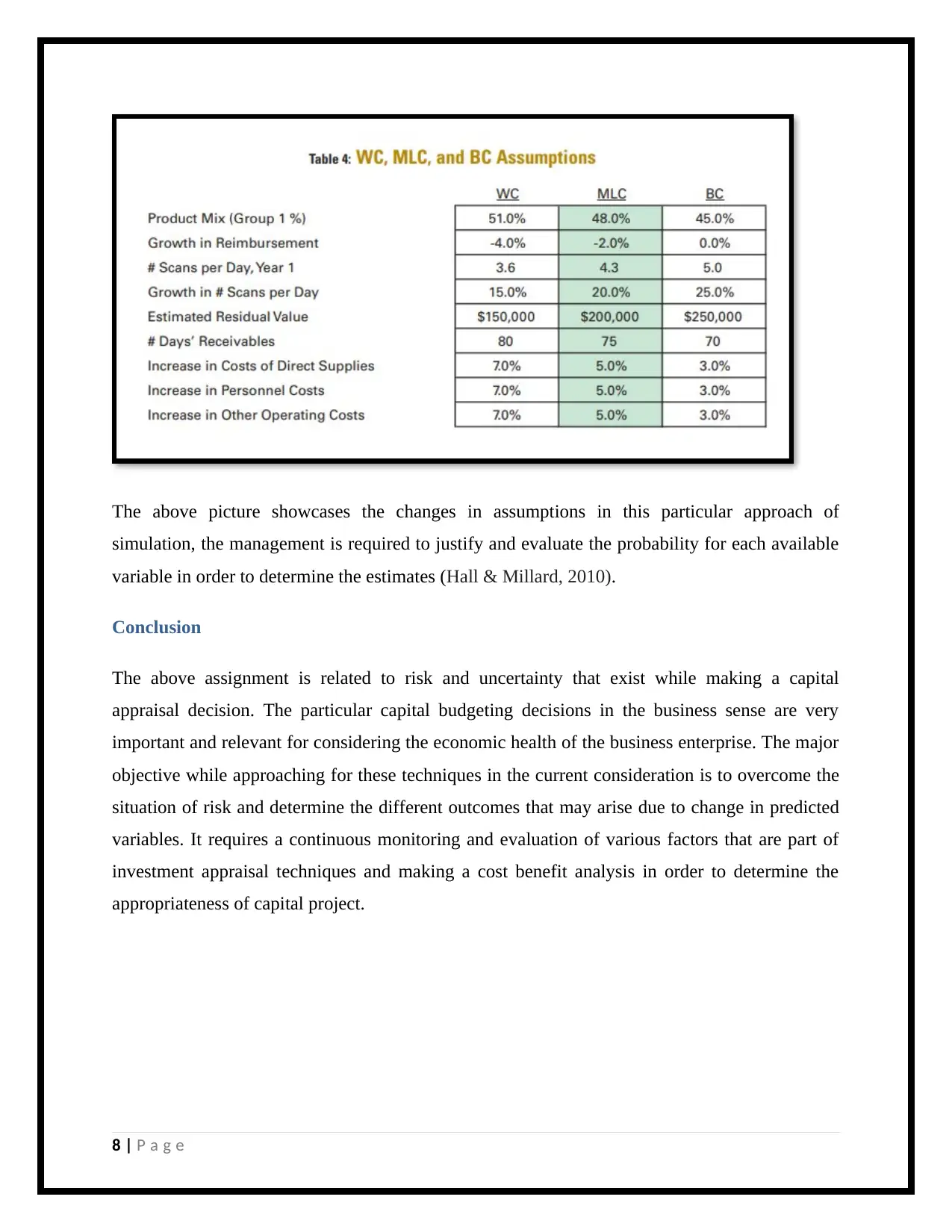

The above picture showcases the changes in assumptions in this particular approach of

simulation, the management is required to justify and evaluate the probability for each available

variable in order to determine the estimates (Hall & Millard, 2010).

Conclusion

The above assignment is related to risk and uncertainty that exist while making a capital

appraisal decision. The particular capital budgeting decisions in the business sense are very

important and relevant for considering the economic health of the business enterprise. The major

objective while approaching for these techniques in the current consideration is to overcome the

situation of risk and determine the different outcomes that may arise due to change in predicted

variables. It requires a continuous monitoring and evaluation of various factors that are part of

investment appraisal techniques and making a cost benefit analysis in order to determine the

appropriateness of capital project.

8 | P a g e

simulation, the management is required to justify and evaluate the probability for each available

variable in order to determine the estimates (Hall & Millard, 2010).

Conclusion

The above assignment is related to risk and uncertainty that exist while making a capital

appraisal decision. The particular capital budgeting decisions in the business sense are very

important and relevant for considering the economic health of the business enterprise. The major

objective while approaching for these techniques in the current consideration is to overcome the

situation of risk and determine the different outcomes that may arise due to change in predicted

variables. It requires a continuous monitoring and evaluation of various factors that are part of

investment appraisal techniques and making a cost benefit analysis in order to determine the

appropriateness of capital project.

8 | P a g e

References

Adair, T., 2011. Corporate Finance Demystified 2/E. McGraw Hill Professional.

Bennouna, K., Meredith, G.G. and Marchant, T., 2010. Improved capital budgeting decision

making: evidence from Canada. Management decision, 48(2), pp.225-247.

Bierman Jr, H. and Smidt, S., 2012. The capital budgeting decision: economic analysis of

investment projects. Routledge.

Carmichael, D.G. and Balatbat, M.C., 2008. Probabilistic DCF analysis and capital budgeting

and investment—a survey. The Engineering Economist, 53(1), pp.84-102.

Correia, C. and Cramer, P., 2008. An analysis of cost of capital, capital structure and capital

budgeting practices: a survey of South African listed companies. Meditari accountancy

research, 16(2), pp.31-52.

Dedi, L. and Orsag, S., 2007. Capital budgeting practices: a survey of Croatian firms. South East

European Journal of Economics and Business, 2(1), pp.59-67.

Hall, J. and Millard, S., 2010. Capital budgeting practices used by selected listed South African

firms. South African Journal of Economic and Management Sciences, 13(1), pp.85-97.

James, L.K., Swinton, S.M. and Thelen, K.D., 2010. Profitability analysis of cellulosic energy

crops compared with corn. Agronomy Journal, 102(2), pp.675-687.

Khamees, B.A., Al-Fayoumi, N. and Al-Thuneibat, A.A., 2010. Capital budgeting practices in

the Jordanian industrial corporations. International journal of commerce and

management, 20(1), pp.49-63.

Kwak, Y.H. and Ingall, L., 2007. Exploring Monte Carlo simulation applications for project

management. Risk Management, 9(1), pp.44-57.

9 | P a g e

Adair, T., 2011. Corporate Finance Demystified 2/E. McGraw Hill Professional.

Bennouna, K., Meredith, G.G. and Marchant, T., 2010. Improved capital budgeting decision

making: evidence from Canada. Management decision, 48(2), pp.225-247.

Bierman Jr, H. and Smidt, S., 2012. The capital budgeting decision: economic analysis of

investment projects. Routledge.

Carmichael, D.G. and Balatbat, M.C., 2008. Probabilistic DCF analysis and capital budgeting

and investment—a survey. The Engineering Economist, 53(1), pp.84-102.

Correia, C. and Cramer, P., 2008. An analysis of cost of capital, capital structure and capital

budgeting practices: a survey of South African listed companies. Meditari accountancy

research, 16(2), pp.31-52.

Dedi, L. and Orsag, S., 2007. Capital budgeting practices: a survey of Croatian firms. South East

European Journal of Economics and Business, 2(1), pp.59-67.

Hall, J. and Millard, S., 2010. Capital budgeting practices used by selected listed South African

firms. South African Journal of Economic and Management Sciences, 13(1), pp.85-97.

James, L.K., Swinton, S.M. and Thelen, K.D., 2010. Profitability analysis of cellulosic energy

crops compared with corn. Agronomy Journal, 102(2), pp.675-687.

Khamees, B.A., Al-Fayoumi, N. and Al-Thuneibat, A.A., 2010. Capital budgeting practices in

the Jordanian industrial corporations. International journal of commerce and

management, 20(1), pp.49-63.

Kwak, Y.H. and Ingall, L., 2007. Exploring Monte Carlo simulation applications for project

management. Risk Management, 9(1), pp.44-57.

9 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Verma, S., Gupta, S. and Batra, R., 2009. A survey of capital budgeting practices in corporate

India. Vision, 13(3), pp.1-17.

Жамойда, О.А. and Мацюк, М.С., 2011. Sensitivity Analysis in Capital Budgeting.

10 | P a g e

India. Vision, 13(3), pp.1-17.

Жамойда, О.А. and Мацюк, М.С., 2011. Sensitivity Analysis in Capital Budgeting.

10 | P a g e

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.