Managerial Finance Report: Portfolio Analysis and Capital Budgeting

VerifiedAdded on 2020/02/03

|16

|4254

|64

Report

AI Summary

This report provides a comprehensive analysis of managerial finance, focusing on portfolio construction and capital investment appraisal. It begins by examining the financial performance of Tesco Plc and J. Sainsbury Plc, two major UK retail companies, using various financial ratios such as current ratio, quick ratio, gross margin, net profit margin, ROCE, gearing ratios, price/earnings ratio, EPS, dividend payout ratio, and inventory turnover. The analysis includes graphical presentations and recommendations for improving the performance of a poorly performing business. The report also delves into capital investment appraisal techniques, applying methods like payback period, net present value (NPV), and internal rate of return (IRR) to evaluate potential investment projects. It highlights the limitations of both financial ratio analysis and investment appraisal techniques, providing a balanced perspective on their application in financial decision-making. The report aims to assist a Chief Financial Officer in portfolio construction and to guide investment decisions for a manufacturing concern, Midway Limited (ML), by comparing different capital budgeting tools and project evaluations.

MANAGERIAL FINANCE

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION................................................................................................................................3

QUESTION: 1 PORTFOLIO...............................................................................................................3

Calculation of ratio and its analysis through graphical presentation...............................................3

Recommendation to poorly performing business............................................................................7

Limitations of financial ratios..........................................................................................................8

QUESTION: 2 CAPITAL INVESTMENT APPRAISALS.................................................................9

Application of different investment appraisal techniques...............................................................9

Limitations of using investment appraisal techniques...................................................................12

CONCLUSION..................................................................................................................................13

REFERENCES...................................................................................................................................14

2

INTRODUCTION................................................................................................................................3

QUESTION: 1 PORTFOLIO...............................................................................................................3

Calculation of ratio and its analysis through graphical presentation...............................................3

Recommendation to poorly performing business............................................................................7

Limitations of financial ratios..........................................................................................................8

QUESTION: 2 CAPITAL INVESTMENT APPRAISALS.................................................................9

Application of different investment appraisal techniques...............................................................9

Limitations of using investment appraisal techniques...................................................................12

CONCLUSION..................................................................................................................................13

REFERENCES...................................................................................................................................14

2

Table of figures

Figure 1 Calculation of cash flows from project A..............................................................................9

Figure 2 Calculation of cash flows from project B............................................................................10

Figure 3 Calculation of payback period.............................................................................................10

Figure 4 Calculation of net present value...........................................................................................11

Figure 5 Calculation of internal rate of return....................................................................................11

3

Figure 1 Calculation of cash flows from project A..............................................................................9

Figure 2 Calculation of cash flows from project B............................................................................10

Figure 3 Calculation of payback period.............................................................................................10

Figure 4 Calculation of net present value...........................................................................................11

Figure 5 Calculation of internal rate of return....................................................................................11

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

In the present times of wide market volatility and fierce level of competition, it becomes

essential for the establishments to manage their funds in an effective manner. The present project

highlights the financial performance analysis of two well-known retail stores of UK, Tesco Plc and

J. Sainsbury Plc. The central aim of evaluation and examination of both the company’s performance

is to suggest Ross Hill Ltd’s Chief Financial Officer for his portfolio construction. Moreover, many-

times, companies are also require to make investment in various capital projects like introduction of

new product, acquisition of advanced technology, upgraded machinery etc. Henceforth, the report

will apply different capital budgeting tools i.e. payback period, net present value and internal rate of

return to suggest Midway Limited (ML) about the best project.

QUESTION: 1 PORTFOLIO

Calculation of ratio and its analysis through graphical presentation

Ratio calculation attached in Appendix

Tesco Plc is one of the largest UK-based retail organizations that operate in 12 countries around

the world, but still, it generates around 86% of total turnover from UK. On the other side, J

Sainsbury is operating in the market through more than 1200 supermarkets and convenience stores.

Both the company’s financial performance has been analyzed here as under:

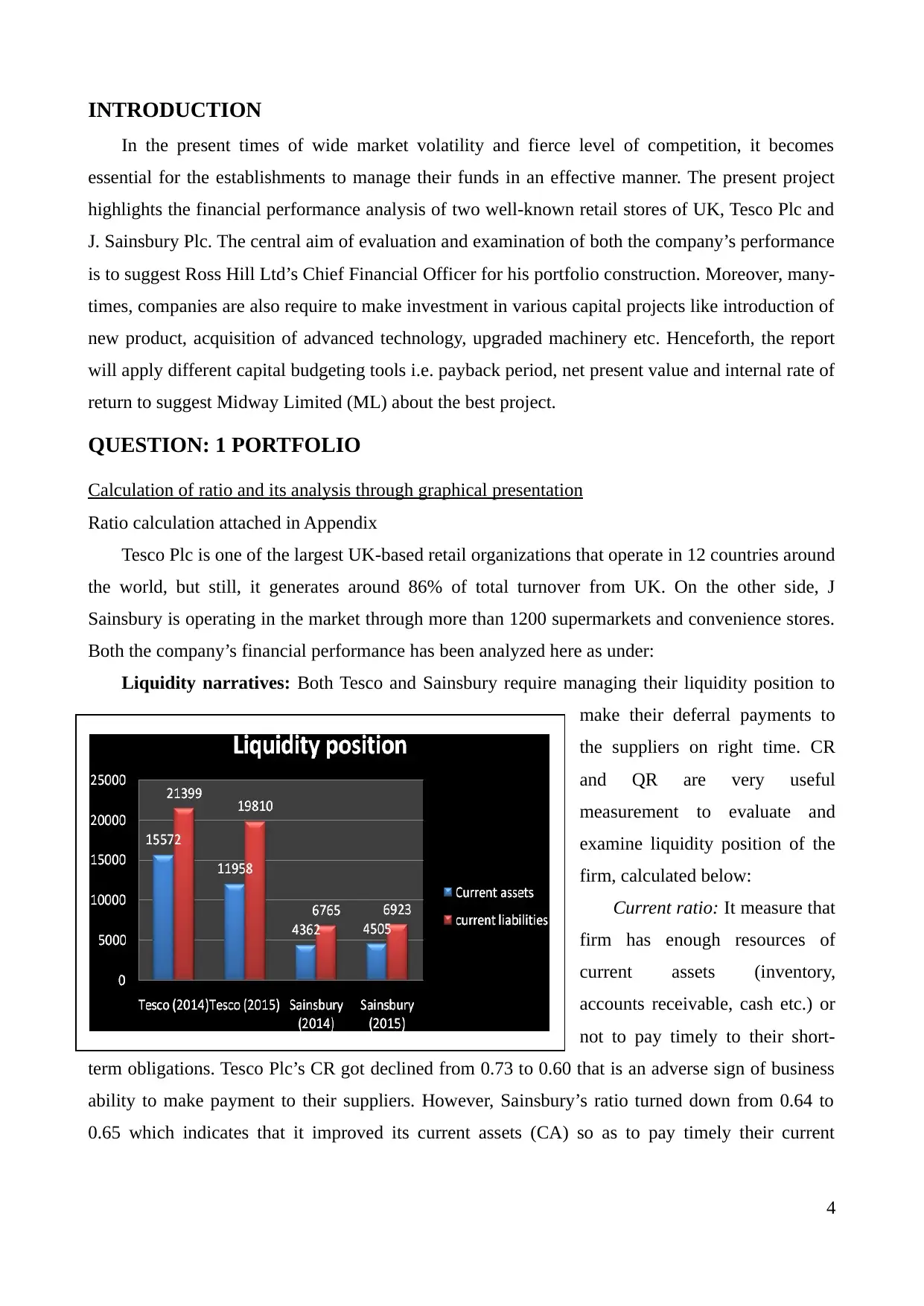

Liquidity narratives: Both Tesco and Sainsbury require managing their liquidity position to

make their deferral payments to

the suppliers on right time. CR

and QR are very useful

measurement to evaluate and

examine liquidity position of the

firm, calculated below:

Current ratio: It measure that

firm has enough resources of

current assets (inventory,

accounts receivable, cash etc.) or

not to pay timely to their short-

term obligations. Tesco Plc’s CR got declined from 0.73 to 0.60 that is an adverse sign of business

ability to make payment to their suppliers. However, Sainsbury’s ratio turned down from 0.64 to

0.65 which indicates that it improved its current assets (CA) so as to pay timely their current

4

In the present times of wide market volatility and fierce level of competition, it becomes

essential for the establishments to manage their funds in an effective manner. The present project

highlights the financial performance analysis of two well-known retail stores of UK, Tesco Plc and

J. Sainsbury Plc. The central aim of evaluation and examination of both the company’s performance

is to suggest Ross Hill Ltd’s Chief Financial Officer for his portfolio construction. Moreover, many-

times, companies are also require to make investment in various capital projects like introduction of

new product, acquisition of advanced technology, upgraded machinery etc. Henceforth, the report

will apply different capital budgeting tools i.e. payback period, net present value and internal rate of

return to suggest Midway Limited (ML) about the best project.

QUESTION: 1 PORTFOLIO

Calculation of ratio and its analysis through graphical presentation

Ratio calculation attached in Appendix

Tesco Plc is one of the largest UK-based retail organizations that operate in 12 countries around

the world, but still, it generates around 86% of total turnover from UK. On the other side, J

Sainsbury is operating in the market through more than 1200 supermarkets and convenience stores.

Both the company’s financial performance has been analyzed here as under:

Liquidity narratives: Both Tesco and Sainsbury require managing their liquidity position to

make their deferral payments to

the suppliers on right time. CR

and QR are very useful

measurement to evaluate and

examine liquidity position of the

firm, calculated below:

Current ratio: It measure that

firm has enough resources of

current assets (inventory,

accounts receivable, cash etc.) or

not to pay timely to their short-

term obligations. Tesco Plc’s CR got declined from 0.73 to 0.60 that is an adverse sign of business

ability to make payment to their suppliers. However, Sainsbury’s ratio turned down from 0.64 to

0.65 which indicates that it improved its current assets (CA) so as to pay timely their current

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

liabilities (CL) especially creditors. 2:1 is considered as idle industrial ratio thus, it becomes clear

that none of both these company has achieved target ratio to maintain their liquidity position.

Quick ratio: It measure liquidity position without taking into account closing inventory

balance. Tesco’s QR came down to 0.45 whereas Sainsbury’s ratio enhanced to 0.51 indicates that it

is comparatively more able to make deferral payments to suppliers on right time. Further, 1:1 is

considered as industrial benchmark, henceforth, it can be suggested to the both the companies to

maximize their CA and minimize their CL to achieve set standard.

Profitability narratives: The aim of both the retail firms is to generate greater yield on

turnover. Moreover, being an investor, Ross Hill Ltd’s CFO will be definitely interested to ensure

maximum possibility of return on their potential investment. Profitability ratios are the essential

tools that assist investors to examine that which company is more able to pay better return to the

investors, conducted hereunder:

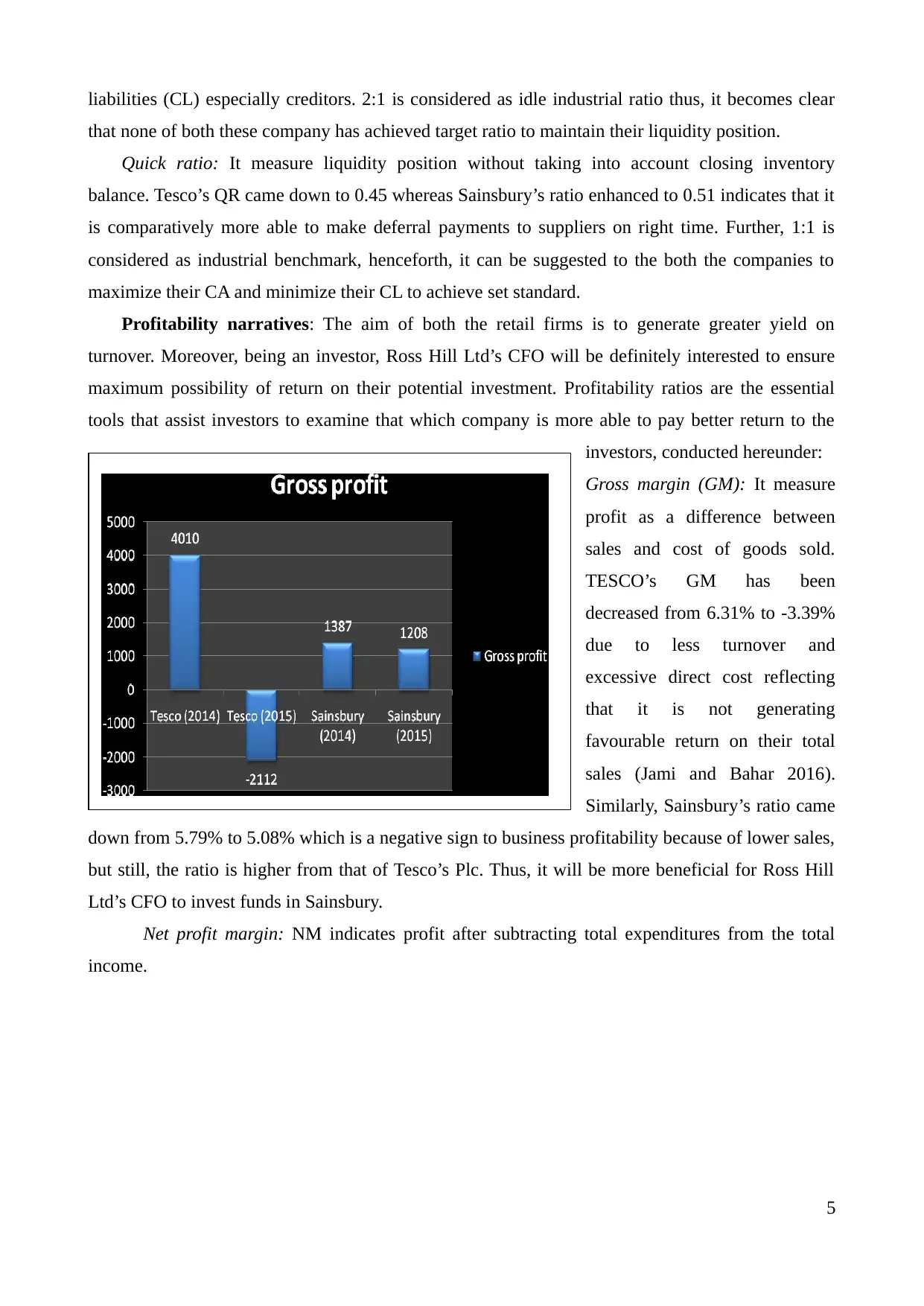

Gross margin (GM): It measure

profit as a difference between

sales and cost of goods sold.

TESCO’s GM has been

decreased from 6.31% to -3.39%

due to less turnover and

excessive direct cost reflecting

that it is not generating

favourable return on their total

sales (Jami and Bahar 2016).

Similarly, Sainsbury’s ratio came

down from 5.79% to 5.08% which is a negative sign to business profitability because of lower sales,

but still, the ratio is higher from that of Tesco’s Plc. Thus, it will be more beneficial for Ross Hill

Ltd’s CFO to invest funds in Sainsbury.

Net profit margin: NM indicates profit after subtracting total expenditures from the total

income.

5

that none of both these company has achieved target ratio to maintain their liquidity position.

Quick ratio: It measure liquidity position without taking into account closing inventory

balance. Tesco’s QR came down to 0.45 whereas Sainsbury’s ratio enhanced to 0.51 indicates that it

is comparatively more able to make deferral payments to suppliers on right time. Further, 1:1 is

considered as industrial benchmark, henceforth, it can be suggested to the both the companies to

maximize their CA and minimize their CL to achieve set standard.

Profitability narratives: The aim of both the retail firms is to generate greater yield on

turnover. Moreover, being an investor, Ross Hill Ltd’s CFO will be definitely interested to ensure

maximum possibility of return on their potential investment. Profitability ratios are the essential

tools that assist investors to examine that which company is more able to pay better return to the

investors, conducted hereunder:

Gross margin (GM): It measure

profit as a difference between

sales and cost of goods sold.

TESCO’s GM has been

decreased from 6.31% to -3.39%

due to less turnover and

excessive direct cost reflecting

that it is not generating

favourable return on their total

sales (Jami and Bahar 2016).

Similarly, Sainsbury’s ratio came

down from 5.79% to 5.08% which is a negative sign to business profitability because of lower sales,

but still, the ratio is higher from that of Tesco’s Plc. Thus, it will be more beneficial for Ross Hill

Ltd’s CFO to invest funds in Sainsbury.

Net profit margin: NM indicates profit after subtracting total expenditures from the total

income.

5

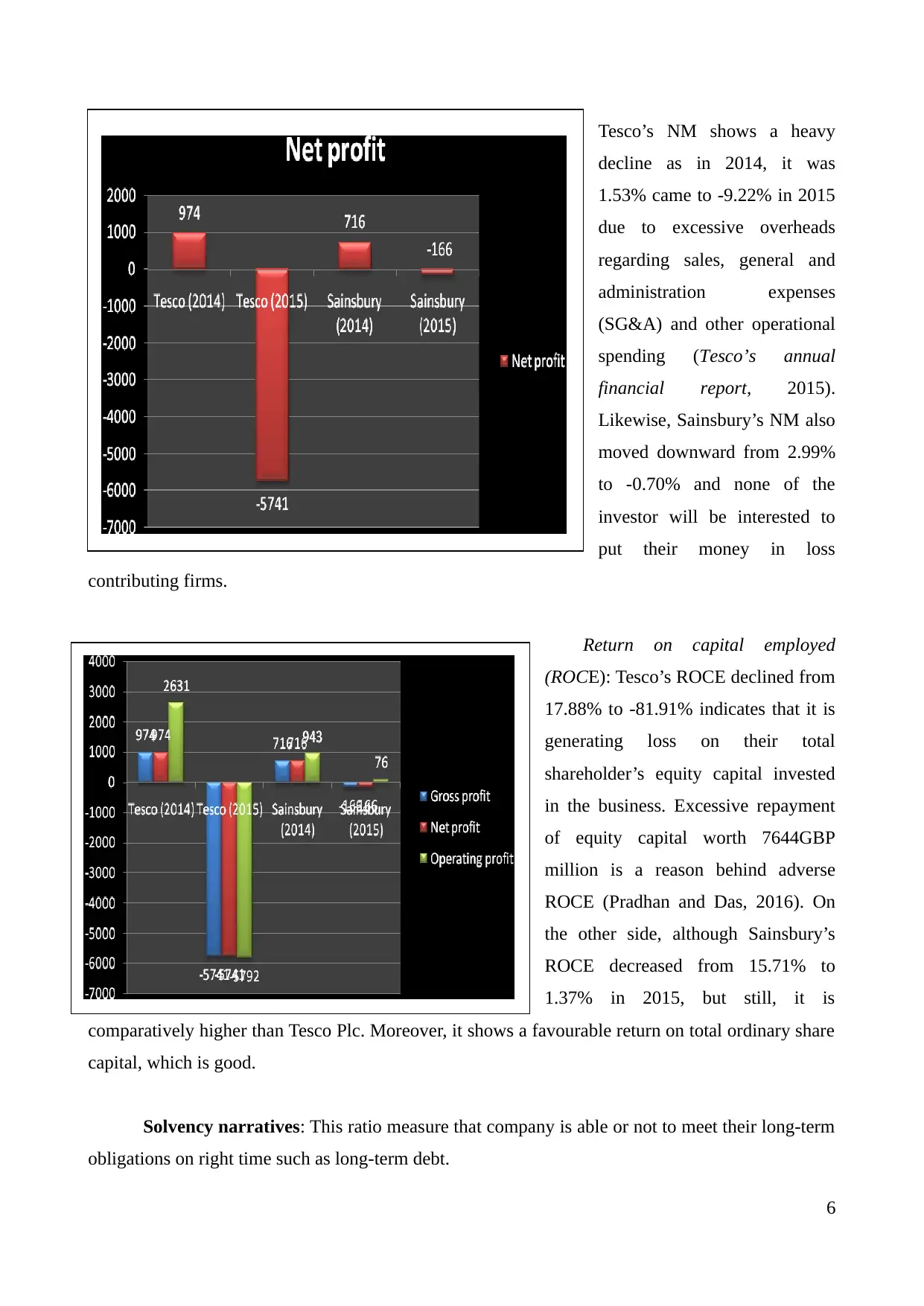

Tesco’s NM shows a heavy

decline as in 2014, it was

1.53% came to -9.22% in 2015

due to excessive overheads

regarding sales, general and

administration expenses

(SG&A) and other operational

spending (Tesco’s annual

financial report, 2015).

Likewise, Sainsbury’s NM also

moved downward from 2.99%

to -0.70% and none of the

investor will be interested to

put their money in loss

contributing firms.

Return on capital employed

(ROCE): Tesco’s ROCE declined from

17.88% to -81.91% indicates that it is

generating loss on their total

shareholder’s equity capital invested

in the business. Excessive repayment

of equity capital worth 7644GBP

million is a reason behind adverse

ROCE (Pradhan and Das, 2016). On

the other side, although Sainsbury’s

ROCE decreased from 15.71% to

1.37% in 2015, but still, it is

comparatively higher than Tesco Plc. Moreover, it shows a favourable return on total ordinary share

capital, which is good.

Solvency narratives: This ratio measure that company is able or not to meet their long-term

obligations on right time such as long-term debt.

6

decline as in 2014, it was

1.53% came to -9.22% in 2015

due to excessive overheads

regarding sales, general and

administration expenses

(SG&A) and other operational

spending (Tesco’s annual

financial report, 2015).

Likewise, Sainsbury’s NM also

moved downward from 2.99%

to -0.70% and none of the

investor will be interested to

put their money in loss

contributing firms.

Return on capital employed

(ROCE): Tesco’s ROCE declined from

17.88% to -81.91% indicates that it is

generating loss on their total

shareholder’s equity capital invested

in the business. Excessive repayment

of equity capital worth 7644GBP

million is a reason behind adverse

ROCE (Pradhan and Das, 2016). On

the other side, although Sainsbury’s

ROCE decreased from 15.71% to

1.37% in 2015, but still, it is

comparatively higher than Tesco Plc. Moreover, it shows a favourable return on total ordinary share

capital, which is good.

Solvency narratives: This ratio measure that company is able or not to meet their long-term

obligations on right time such as long-term debt.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

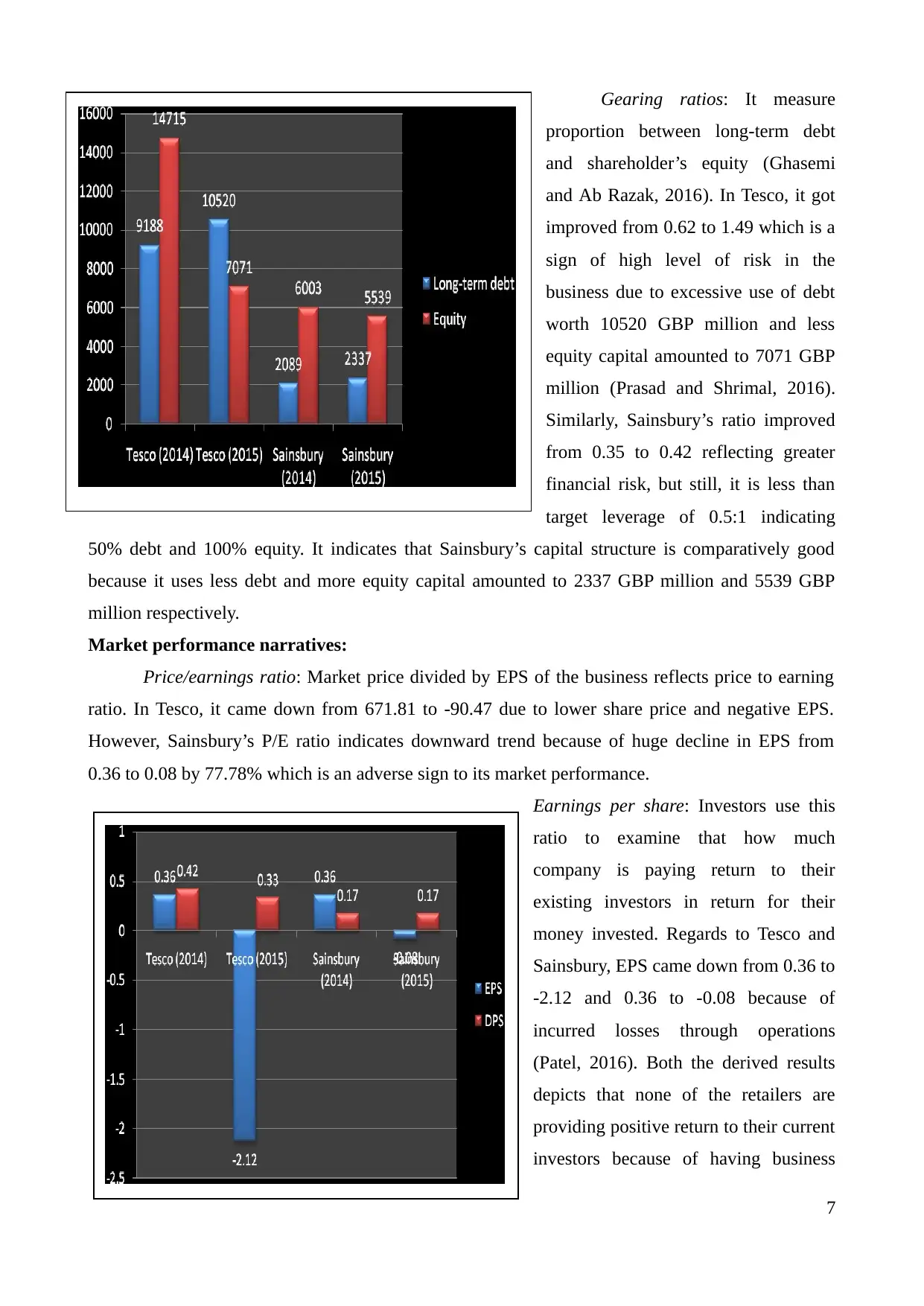

Gearing ratios: It measure

proportion between long-term debt

and shareholder’s equity (Ghasemi

and Ab Razak, 2016). In Tesco, it got

improved from 0.62 to 1.49 which is a

sign of high level of risk in the

business due to excessive use of debt

worth 10520 GBP million and less

equity capital amounted to 7071 GBP

million (Prasad and Shrimal, 2016).

Similarly, Sainsbury’s ratio improved

from 0.35 to 0.42 reflecting greater

financial risk, but still, it is less than

target leverage of 0.5:1 indicating

50% debt and 100% equity. It indicates that Sainsbury’s capital structure is comparatively good

because it uses less debt and more equity capital amounted to 2337 GBP million and 5539 GBP

million respectively.

Market performance narratives:

Price/earnings ratio: Market price divided by EPS of the business reflects price to earning

ratio. In Tesco, it came down from 671.81 to -90.47 due to lower share price and negative EPS.

However, Sainsbury’s P/E ratio indicates downward trend because of huge decline in EPS from

0.36 to 0.08 by 77.78% which is an adverse sign to its market performance.

Earnings per share: Investors use this

ratio to examine that how much

company is paying return to their

existing investors in return for their

money invested. Regards to Tesco and

Sainsbury, EPS came down from 0.36 to

-2.12 and 0.36 to -0.08 because of

incurred losses through operations

(Patel, 2016). Both the derived results

depicts that none of the retailers are

providing positive return to their current

investors because of having business

7

proportion between long-term debt

and shareholder’s equity (Ghasemi

and Ab Razak, 2016). In Tesco, it got

improved from 0.62 to 1.49 which is a

sign of high level of risk in the

business due to excessive use of debt

worth 10520 GBP million and less

equity capital amounted to 7071 GBP

million (Prasad and Shrimal, 2016).

Similarly, Sainsbury’s ratio improved

from 0.35 to 0.42 reflecting greater

financial risk, but still, it is less than

target leverage of 0.5:1 indicating

50% debt and 100% equity. It indicates that Sainsbury’s capital structure is comparatively good

because it uses less debt and more equity capital amounted to 2337 GBP million and 5539 GBP

million respectively.

Market performance narratives:

Price/earnings ratio: Market price divided by EPS of the business reflects price to earning

ratio. In Tesco, it came down from 671.81 to -90.47 due to lower share price and negative EPS.

However, Sainsbury’s P/E ratio indicates downward trend because of huge decline in EPS from

0.36 to 0.08 by 77.78% which is an adverse sign to its market performance.

Earnings per share: Investors use this

ratio to examine that how much

company is paying return to their

existing investors in return for their

money invested. Regards to Tesco and

Sainsbury, EPS came down from 0.36 to

-2.12 and 0.36 to -0.08 because of

incurred losses through operations

(Patel, 2016). Both the derived results

depicts that none of the retailers are

providing positive return to their current

investors because of having business

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

losses.

Dividend payout ratio: Tesco Plc’s dividend payout ratio got decreased from 116.67 to -

15.57% in 2015 whilst Sainsbury’s ratio got decreased came down from 47.22% to -212.50%. Less

DPS to 0.17 is the main reason behind lower DPR in Sainsbury.

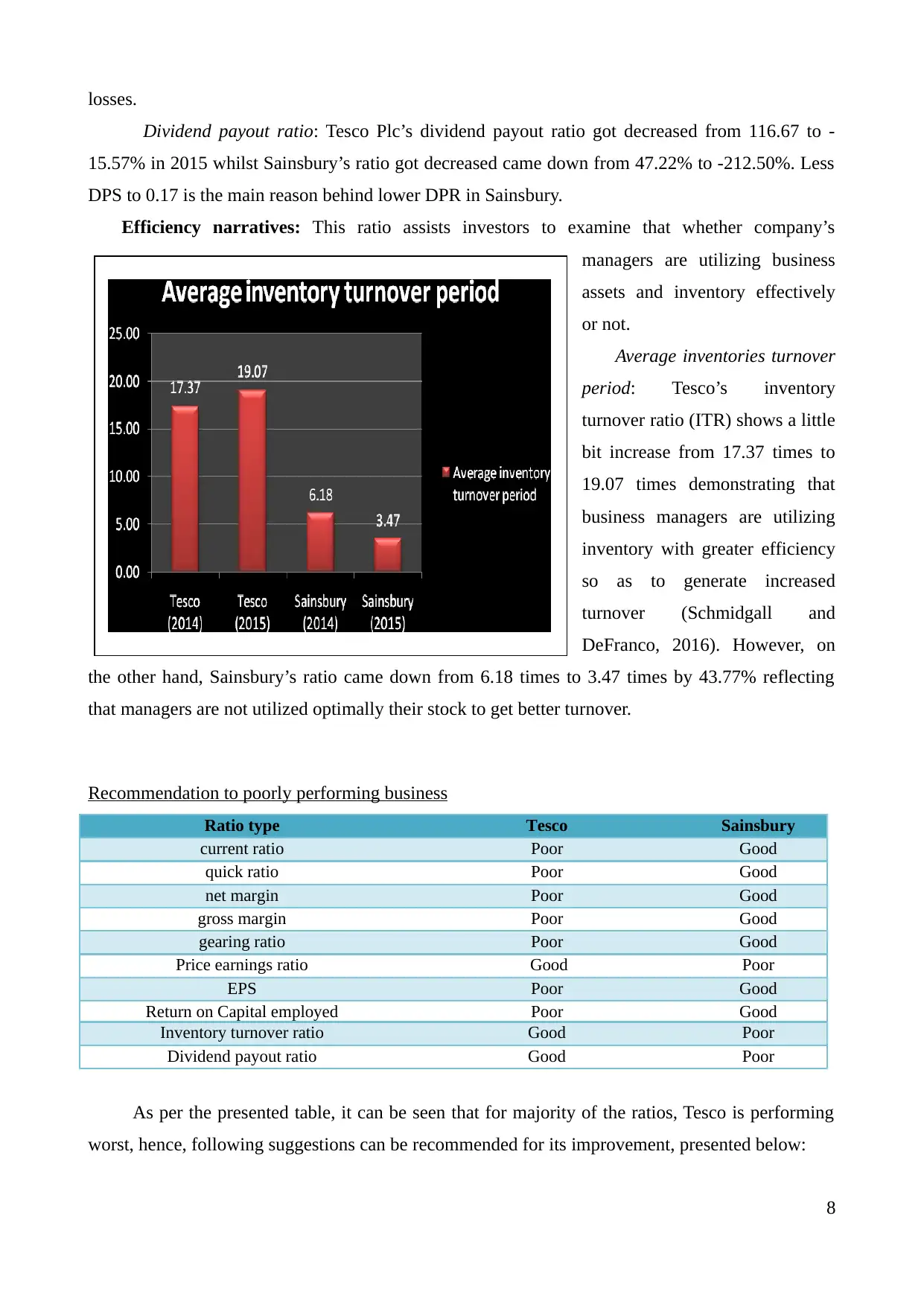

Efficiency narratives: This ratio assists investors to examine that whether company’s

managers are utilizing business

assets and inventory effectively

or not.

Average inventories turnover

period: Tesco’s inventory

turnover ratio (ITR) shows a little

bit increase from 17.37 times to

19.07 times demonstrating that

business managers are utilizing

inventory with greater efficiency

so as to generate increased

turnover (Schmidgall and

DeFranco, 2016). However, on

the other hand, Sainsbury’s ratio came down from 6.18 times to 3.47 times by 43.77% reflecting

that managers are not utilized optimally their stock to get better turnover.

Recommendation to poorly performing business

Ratio type Tesco Sainsbury

current ratio Poor Good

quick ratio Poor Good

net margin Poor Good

gross margin Poor Good

gearing ratio Poor Good

Price earnings ratio Good Poor

EPS Poor Good

Return on Capital employed Poor Good

Inventory turnover ratio Good Poor

Dividend payout ratio Good Poor

As per the presented table, it can be seen that for majority of the ratios, Tesco is performing

worst, hence, following suggestions can be recommended for its improvement, presented below:

8

Dividend payout ratio: Tesco Plc’s dividend payout ratio got decreased from 116.67 to -

15.57% in 2015 whilst Sainsbury’s ratio got decreased came down from 47.22% to -212.50%. Less

DPS to 0.17 is the main reason behind lower DPR in Sainsbury.

Efficiency narratives: This ratio assists investors to examine that whether company’s

managers are utilizing business

assets and inventory effectively

or not.

Average inventories turnover

period: Tesco’s inventory

turnover ratio (ITR) shows a little

bit increase from 17.37 times to

19.07 times demonstrating that

business managers are utilizing

inventory with greater efficiency

so as to generate increased

turnover (Schmidgall and

DeFranco, 2016). However, on

the other hand, Sainsbury’s ratio came down from 6.18 times to 3.47 times by 43.77% reflecting

that managers are not utilized optimally their stock to get better turnover.

Recommendation to poorly performing business

Ratio type Tesco Sainsbury

current ratio Poor Good

quick ratio Poor Good

net margin Poor Good

gross margin Poor Good

gearing ratio Poor Good

Price earnings ratio Good Poor

EPS Poor Good

Return on Capital employed Poor Good

Inventory turnover ratio Good Poor

Dividend payout ratio Good Poor

As per the presented table, it can be seen that for majority of the ratios, Tesco is performing

worst, hence, following suggestions can be recommended for its improvement, presented below:

8

- Liquidity position can be improved by maximizing their current assets, comprising

inventory, receivables, cash and at the same time, Tesco Plc also require to pay-off some of

current liabilities like overdraft and payables (Goldmann, 2017). Moreover, it also can be

improved through brining enhancement in cash flow generating activities, which in turn,

increase liquidity position to a major extent.

- Tesco Plc’s managers need to increase their revenue by offering quality services at

affordable prices, so as to generate more turnovers. While, on the other hand, operational

expenditures comprising both direct and indirect i.e. SG&A and overheads need to be

controlled through regular monitoring and controlling by departmental managers. Moreover,

comparison of actual results with targets is also a better way to make better decisions for

increasing net return (Sarkar, 2016).

- Through getting more yield through daily operations, not only Tesco Plc but also Sainsbury

will be able to give favourable return to the investors to satisfy their return expectations.

Further, it also assists company to maximize their ROCE and profitability position.

- Long-term financial risk can be minimized by Tesco Plc through repayment of some debt

and generating more capital through issuance of ordinary shares (Singh, 2016).

Limitations of financial ratios

Although, ratio analysis is considered as best tool to evaluate and examine performance over

the period, but still, it employs certain drawbacks that are enumerated underneath:

Based on historical results: All the ratios computed above use historical results whereas being

an investor, Ross Hill Ltd’s CFO will be surely interested in knowing future results so as to make

sure himself about better return on their future investment. Thus, it is one of the main limitations of

the financial ratio analysis as is based on historical outcome and does not provide any assistance to

forecast future outcome (Pant, 2013).

Quantitative technique: All the ratios i.e. liquidity, solvency, profitability and efficiency use

quantitative and numerical data whilst in the real market, investors are also interested in other

business activities that cannot be measured in figures. In such case, ratio analysis does not offer any

help to the investors that is also its disadvantage.

Inflation: Inflation rate greatly affects business cost and revenue, which in turn, influenced net

results. However, profitability ratios does not measure the impact of varying inflation rate on their

net yield, which is also a drawback for the Ross Hill Ltd’s CFO because he cannot determine the

impact of market volatility on both the Tesco and Sainsbury’s net earnings (Schmidgall and

DeFranco, 2016).

9

inventory, receivables, cash and at the same time, Tesco Plc also require to pay-off some of

current liabilities like overdraft and payables (Goldmann, 2017). Moreover, it also can be

improved through brining enhancement in cash flow generating activities, which in turn,

increase liquidity position to a major extent.

- Tesco Plc’s managers need to increase their revenue by offering quality services at

affordable prices, so as to generate more turnovers. While, on the other hand, operational

expenditures comprising both direct and indirect i.e. SG&A and overheads need to be

controlled through regular monitoring and controlling by departmental managers. Moreover,

comparison of actual results with targets is also a better way to make better decisions for

increasing net return (Sarkar, 2016).

- Through getting more yield through daily operations, not only Tesco Plc but also Sainsbury

will be able to give favourable return to the investors to satisfy their return expectations.

Further, it also assists company to maximize their ROCE and profitability position.

- Long-term financial risk can be minimized by Tesco Plc through repayment of some debt

and generating more capital through issuance of ordinary shares (Singh, 2016).

Limitations of financial ratios

Although, ratio analysis is considered as best tool to evaluate and examine performance over

the period, but still, it employs certain drawbacks that are enumerated underneath:

Based on historical results: All the ratios computed above use historical results whereas being

an investor, Ross Hill Ltd’s CFO will be surely interested in knowing future results so as to make

sure himself about better return on their future investment. Thus, it is one of the main limitations of

the financial ratio analysis as is based on historical outcome and does not provide any assistance to

forecast future outcome (Pant, 2013).

Quantitative technique: All the ratios i.e. liquidity, solvency, profitability and efficiency use

quantitative and numerical data whilst in the real market, investors are also interested in other

business activities that cannot be measured in figures. In such case, ratio analysis does not offer any

help to the investors that is also its disadvantage.

Inflation: Inflation rate greatly affects business cost and revenue, which in turn, influenced net

results. However, profitability ratios does not measure the impact of varying inflation rate on their

net yield, which is also a drawback for the Ross Hill Ltd’s CFO because he cannot determine the

impact of market volatility on both the Tesco and Sainsbury’s net earnings (Schmidgall and

DeFranco, 2016).

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting techniques and principles: Although both the companies operate in retail industry,

but still, data which they report in their annual accounts may be differ due to follow-up of

distinguish accounting principles, conventions, policies and rules. It directly influenced the reported

figures in the financial statement and quality of ratio analysis, which in turn, affect investor’s

decisions.

Operational change: Financial ratio analysis in Tesco and Sainsbury having differences in

internal business conditions, operational structure, system and processes and corporate strategies

and goals may lead to take harmful investment decisions. For instance, out of these companies, if

any one follows low-cost strategy and then it will definitely willing to accept lower GM so as to

attract larger market share (Ghasemi and Ab Razak, 2016).. In such case, profitability evaluation

may lead to take misleading decisions.

Difficult to interpret: It will not be easy for Ross Hill Ltd’s CFO to say a particular ratio good

or bad because of no idle set. For instance, although improvements in assets inventory turnover

ratio is a good sign of managerial efficiency, but still, it is not decided that at what level, it will be

considered as idle. As a result, interpretation of ratio becomes very difficult for the investor.

QUESTION: 2 CAPITAL INVESTMENT APPRAISALS

According to the given scenario, Midway Limited (ML) is a manufacturing concern that has an

opportunity available in the market to invest funds in one of two mutually exclusive projects about

machinery purchase. It is a type of capital expenditures which comprises both risk and return

possibility, therefore, in order to make better and viable decision, ML require to examine the risk-

return relationship in both the projects and thereby identify the best among these. Investment

appraisal techniques are of great importance that assists companies to evaluate project viability,

portfolio decision and identify the value that a project can generate in future. Here, both the

discounting and non-discounting techniques are applying to identify the most viable or profitable

proposal available to ML, executed below:

Application of different investment appraisal techniques

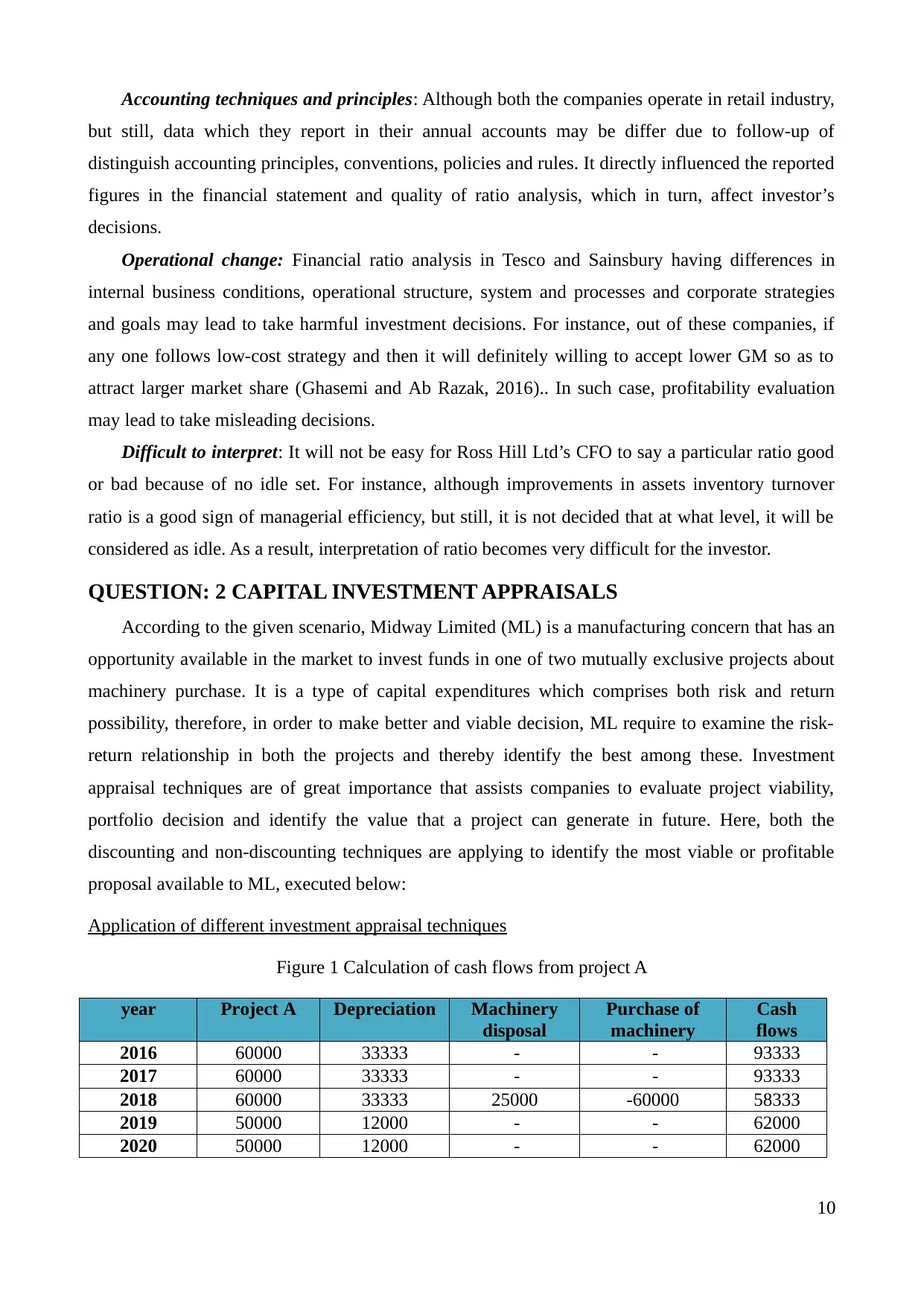

Figure 1 Calculation of cash flows from project A

year Project A Depreciation Machinery

disposal

Purchase of

machinery

Cash

flows

2016 60000 33333 - - 93333

2017 60000 33333 - - 93333

2018 60000 33333 25000 -60000 58333

2019 50000 12000 - - 62000

2020 50000 12000 - - 62000

10

but still, data which they report in their annual accounts may be differ due to follow-up of

distinguish accounting principles, conventions, policies and rules. It directly influenced the reported

figures in the financial statement and quality of ratio analysis, which in turn, affect investor’s

decisions.

Operational change: Financial ratio analysis in Tesco and Sainsbury having differences in

internal business conditions, operational structure, system and processes and corporate strategies

and goals may lead to take harmful investment decisions. For instance, out of these companies, if

any one follows low-cost strategy and then it will definitely willing to accept lower GM so as to

attract larger market share (Ghasemi and Ab Razak, 2016).. In such case, profitability evaluation

may lead to take misleading decisions.

Difficult to interpret: It will not be easy for Ross Hill Ltd’s CFO to say a particular ratio good

or bad because of no idle set. For instance, although improvements in assets inventory turnover

ratio is a good sign of managerial efficiency, but still, it is not decided that at what level, it will be

considered as idle. As a result, interpretation of ratio becomes very difficult for the investor.

QUESTION: 2 CAPITAL INVESTMENT APPRAISALS

According to the given scenario, Midway Limited (ML) is a manufacturing concern that has an

opportunity available in the market to invest funds in one of two mutually exclusive projects about

machinery purchase. It is a type of capital expenditures which comprises both risk and return

possibility, therefore, in order to make better and viable decision, ML require to examine the risk-

return relationship in both the projects and thereby identify the best among these. Investment

appraisal techniques are of great importance that assists companies to evaluate project viability,

portfolio decision and identify the value that a project can generate in future. Here, both the

discounting and non-discounting techniques are applying to identify the most viable or profitable

proposal available to ML, executed below:

Application of different investment appraisal techniques

Figure 1 Calculation of cash flows from project A

year Project A Depreciation Machinery

disposal

Purchase of

machinery

Cash

flows

2016 60000 33333 - - 93333

2017 60000 33333 - - 93333

2018 60000 33333 25000 -60000 58333

2019 50000 12000 - - 62000

2020 50000 12000 - - 62000

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2021 40000 12000 - - 52000

Total 320000

Depreciation = (Initial investment – Residual/scrap value)/Estimated project life

Machine 1 = (£125000-£25000)/3 year

= £33333

Machine X = (£60000 – Nil)/5 year

= £12000

Figure 2 Calculation of cash flows from project B

Year Project B Depreciation Cash flows

2016 20000 20833 40833

2017 30000 20833 50833

2018 40000 20833 60833

2019 70000 20833 90833

2020 80000 20833 100833

2021 65000 20833 85833

Total 305000

Machine 2 = (£125000 - nil)/6 year

= £20833

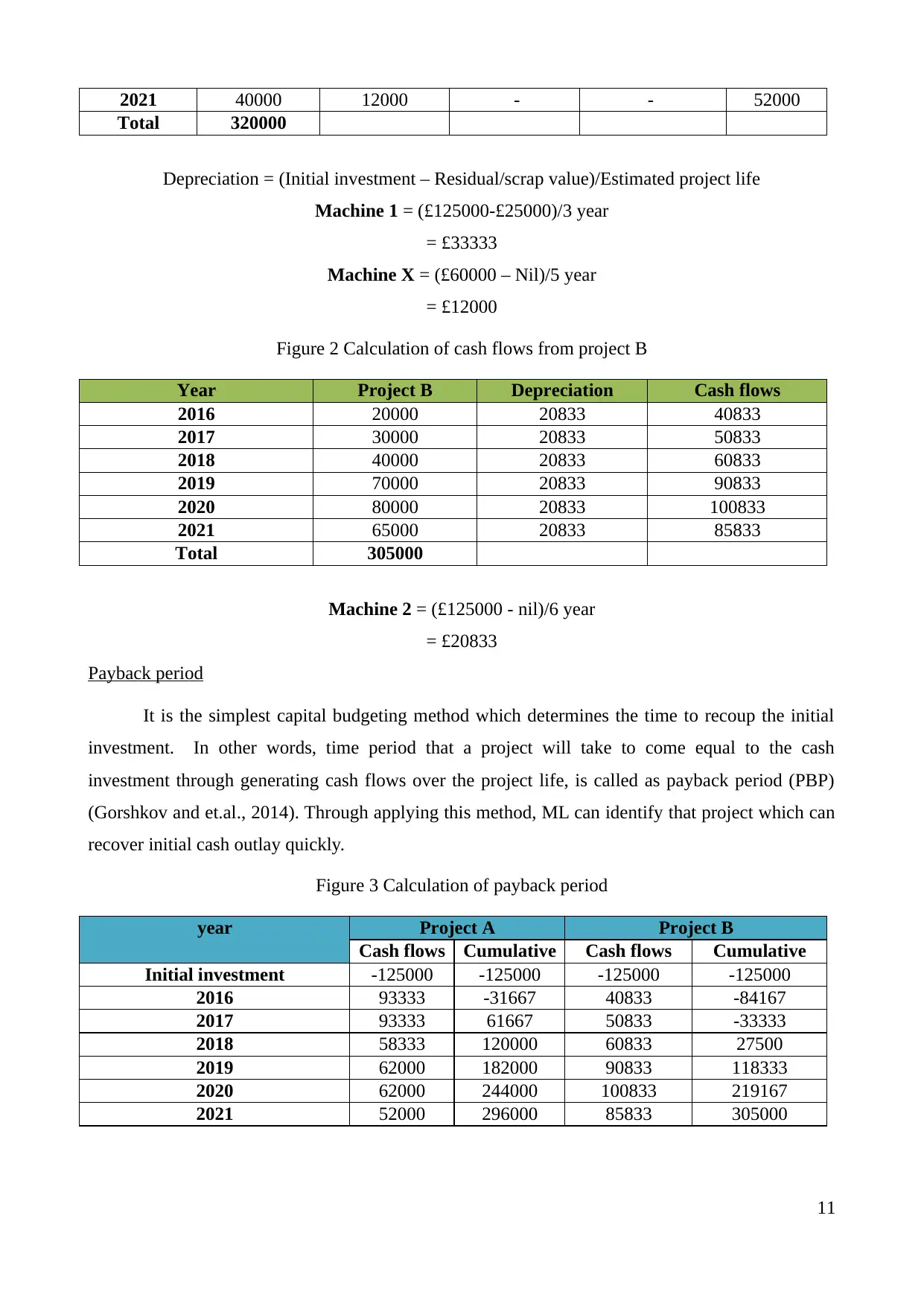

Payback period

It is the simplest capital budgeting method which determines the time to recoup the initial

investment. In other words, time period that a project will take to come equal to the cash

investment through generating cash flows over the project life, is called as payback period (PBP)

(Gorshkov and et.al., 2014). Through applying this method, ML can identify that project which can

recover initial cash outlay quickly.

Figure 3 Calculation of payback period

year Project A Project B

Cash flows Cumulative Cash flows Cumulative

Initial investment -125000 -125000 -125000 -125000

2016 93333 -31667 40833 -84167

2017 93333 61667 50833 -33333

2018 58333 120000 60833 27500

2019 62000 182000 90833 118333

2020 62000 244000 100833 219167

2021 52000 296000 85833 305000

11

Total 320000

Depreciation = (Initial investment – Residual/scrap value)/Estimated project life

Machine 1 = (£125000-£25000)/3 year

= £33333

Machine X = (£60000 – Nil)/5 year

= £12000

Figure 2 Calculation of cash flows from project B

Year Project B Depreciation Cash flows

2016 20000 20833 40833

2017 30000 20833 50833

2018 40000 20833 60833

2019 70000 20833 90833

2020 80000 20833 100833

2021 65000 20833 85833

Total 305000

Machine 2 = (£125000 - nil)/6 year

= £20833

Payback period

It is the simplest capital budgeting method which determines the time to recoup the initial

investment. In other words, time period that a project will take to come equal to the cash

investment through generating cash flows over the project life, is called as payback period (PBP)

(Gorshkov and et.al., 2014). Through applying this method, ML can identify that project which can

recover initial cash outlay quickly.

Figure 3 Calculation of payback period

year Project A Project B

Cash flows Cumulative Cash flows Cumulative

Initial investment -125000 -125000 -125000 -125000

2016 93333 -31667 40833 -84167

2017 93333 61667 50833 -33333

2018 58333 120000 60833 27500

2019 62000 182000 90833 118333

2020 62000 244000 100833 219167

2021 52000 296000 85833 305000

11

PBP (A) = 1 year + (£31667/£93333)

= 1.34 year OR 1 year 4 months

PBP (B) = 2 year + (£3333/£60833)

= 2.55 year OR 2 year 6.5 months

Net present value

The present value of expected cash inflows (CI) net of project cost is called as net present

value (NPV) (Götze, Northcott and Schuster, 2015). This method is considered as best method to

determine project viability because it discounts all the forecasted CI of the capital projects to reflect

their current worth or value. The main reason behind this is it believes that the worth of money that

receives today is more valuable than amount received in later years mainly due to inflation. Thus,

this technique use an appropriate rate of discounting factor based on the cost of capital to determine

the current value of all the projected cash inflows during project life (Leyman and Vanhoucke,

2017).

Figure 4 Calculation of net present value

Year Project A Project B Discounted

value @20%

PV of cash

flows

PV of cash

flows

2016 93333 40833 0.8333 77777.77778 34027.78

2017 93333 50833 0.6944 64814.81481 35300.93

2018 58333 60833 0.5787 33757.71605 35204.48

2019 62000 90833 0.4823 29899.69136 43804.66

2020 62000 100833 0.4019 24916.40947 40522.66

2021 52000 85833 0.3349 17414.69479 28745.41

Total discounted values 248581.1043 217605.9

Less: Initial project

investment

125000 125000

Net present value (NPV) 123581.1043 92605.9

Internal rate of return (IRR)

It is also a useful method that assists ML to determine the most worthy projects among

various alternatives available (Lakew and Rao, 2015). IRR is a rate at which project will give nil

return (NPV- zero), in other words, both discounted value of cash inflows and initial investment

comes equal.

Figure 5 Calculation of internal rate of return

Year Project A Project B

Initial investment -125000 -125000

2016 60000 40833

12

= 1.34 year OR 1 year 4 months

PBP (B) = 2 year + (£3333/£60833)

= 2.55 year OR 2 year 6.5 months

Net present value

The present value of expected cash inflows (CI) net of project cost is called as net present

value (NPV) (Götze, Northcott and Schuster, 2015). This method is considered as best method to

determine project viability because it discounts all the forecasted CI of the capital projects to reflect

their current worth or value. The main reason behind this is it believes that the worth of money that

receives today is more valuable than amount received in later years mainly due to inflation. Thus,

this technique use an appropriate rate of discounting factor based on the cost of capital to determine

the current value of all the projected cash inflows during project life (Leyman and Vanhoucke,

2017).

Figure 4 Calculation of net present value

Year Project A Project B Discounted

value @20%

PV of cash

flows

PV of cash

flows

2016 93333 40833 0.8333 77777.77778 34027.78

2017 93333 50833 0.6944 64814.81481 35300.93

2018 58333 60833 0.5787 33757.71605 35204.48

2019 62000 90833 0.4823 29899.69136 43804.66

2020 62000 100833 0.4019 24916.40947 40522.66

2021 52000 85833 0.3349 17414.69479 28745.41

Total discounted values 248581.1043 217605.9

Less: Initial project

investment

125000 125000

Net present value (NPV) 123581.1043 92605.9

Internal rate of return (IRR)

It is also a useful method that assists ML to determine the most worthy projects among

various alternatives available (Lakew and Rao, 2015). IRR is a rate at which project will give nil

return (NPV- zero), in other words, both discounted value of cash inflows and initial investment

comes equal.

Figure 5 Calculation of internal rate of return

Year Project A Project B

Initial investment -125000 -125000

2016 60000 40833

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.