ACC 515 - Capital Investment Decision & Financial Ratio Analysis

VerifiedAdded on 2023/06/03

|16

|2551

|97

Report

AI Summary

This report provides a detailed financial analysis of AMP Limited, including a comparative analysis of WAACC and capital structure against Commonwealth Bank, key financial ratio analysis covering liquidity, solvency, profitability, efficiency, and investor ratios, and an assessment of material risks faced by the business. The report evaluates a proposed capital investment using payback period, net present value (NPV), and profitability index methods, including sensitivity analysis by varying sales by 20%. Additionally, it compares two investment options using annualized cost. The analysis concludes with recommendations based on the financial metrics and risk assessment.

ACC 515

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Part A.........................................................................................................................................3

(i)............................................................................................................................................3

(ii)...........................................................................................................................................5

A.........................................................................................................................................5

B.........................................................................................................................................6

C.........................................................................................................................................8

(iii)..........................................................................................................................................8

Part B........................................................................................................................................10

References................................................................................................................................16

Part A.........................................................................................................................................3

(i)............................................................................................................................................3

(ii)...........................................................................................................................................5

A.........................................................................................................................................5

B.........................................................................................................................................6

C.........................................................................................................................................8

(iii)..........................................................................................................................................8

Part B........................................................................................................................................10

References................................................................................................................................16

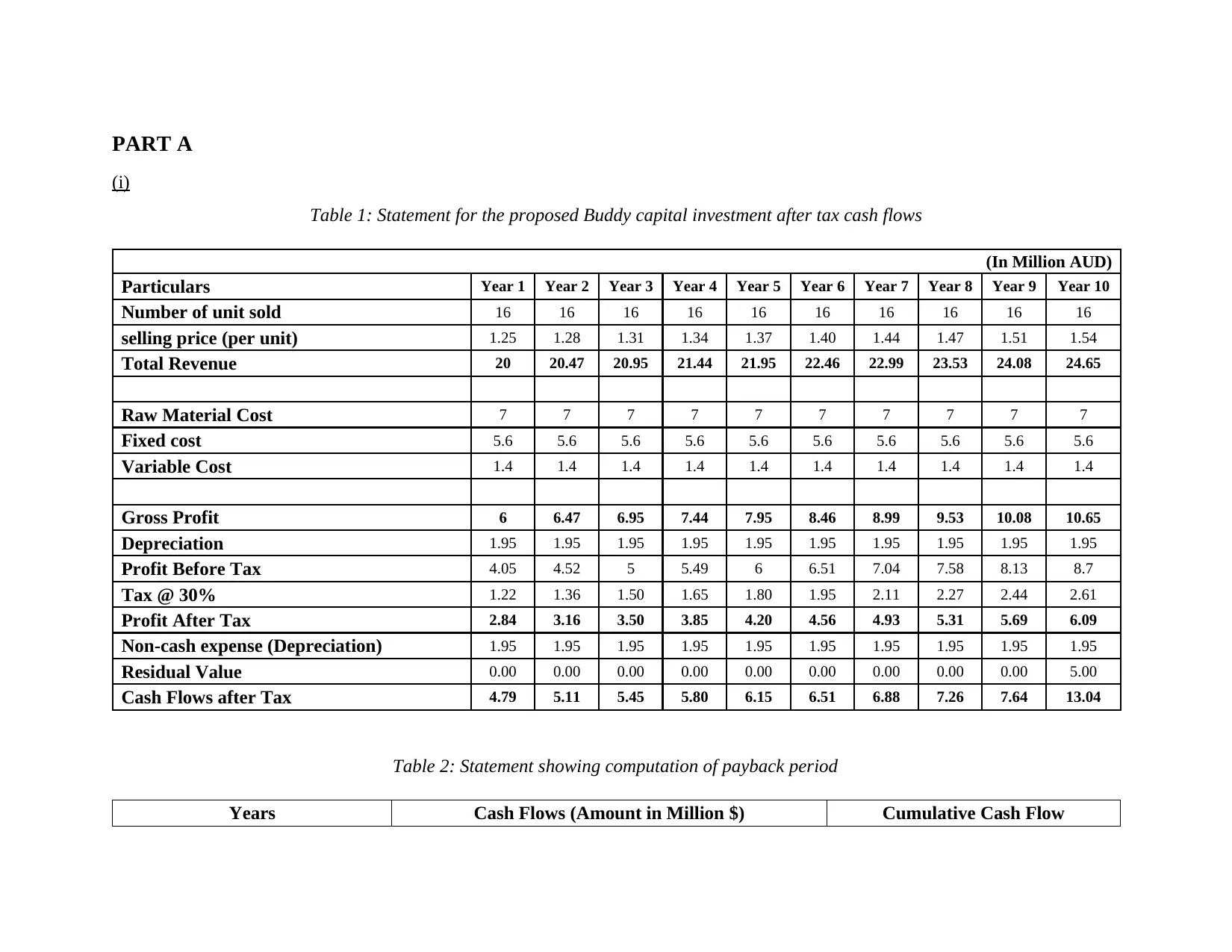

PART A

(i)

Table 1: Statement for the proposed Buddy capital investment after tax cash flows

(In Million AUD)

Particulars Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10

Number of unit sold 16 16 16 16 16 16 16 16 16 16

selling price (per unit) 1.25 1.28 1.31 1.34 1.37 1.40 1.44 1.47 1.51 1.54

Total Revenue 20 20.47 20.95 21.44 21.95 22.46 22.99 23.53 24.08 24.65

Raw Material Cost 7 7 7 7 7 7 7 7 7 7

Fixed cost 5.6 5.6 5.6 5.6 5.6 5.6 5.6 5.6 5.6 5.6

Variable Cost 1.4 1.4 1.4 1.4 1.4 1.4 1.4 1.4 1.4 1.4

Gross Profit 6 6.47 6.95 7.44 7.95 8.46 8.99 9.53 10.08 10.65

Depreciation 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95

Profit Before Tax 4.05 4.52 5 5.49 6 6.51 7.04 7.58 8.13 8.7

Tax @ 30% 1.22 1.36 1.50 1.65 1.80 1.95 2.11 2.27 2.44 2.61

Profit After Tax 2.84 3.16 3.50 3.85 4.20 4.56 4.93 5.31 5.69 6.09

Non-cash expense (Depreciation) 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95

Residual Value 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 5.00

Cash Flows after Tax 4.79 5.11 5.45 5.80 6.15 6.51 6.88 7.26 7.64 13.04

Table 2: Statement showing computation of payback period

Years Cash Flows (Amount in Million $) Cumulative Cash Flow

(i)

Table 1: Statement for the proposed Buddy capital investment after tax cash flows

(In Million AUD)

Particulars Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10

Number of unit sold 16 16 16 16 16 16 16 16 16 16

selling price (per unit) 1.25 1.28 1.31 1.34 1.37 1.40 1.44 1.47 1.51 1.54

Total Revenue 20 20.47 20.95 21.44 21.95 22.46 22.99 23.53 24.08 24.65

Raw Material Cost 7 7 7 7 7 7 7 7 7 7

Fixed cost 5.6 5.6 5.6 5.6 5.6 5.6 5.6 5.6 5.6 5.6

Variable Cost 1.4 1.4 1.4 1.4 1.4 1.4 1.4 1.4 1.4 1.4

Gross Profit 6 6.47 6.95 7.44 7.95 8.46 8.99 9.53 10.08 10.65

Depreciation 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95

Profit Before Tax 4.05 4.52 5 5.49 6 6.51 7.04 7.58 8.13 8.7

Tax @ 30% 1.22 1.36 1.50 1.65 1.80 1.95 2.11 2.27 2.44 2.61

Profit After Tax 2.84 3.16 3.50 3.85 4.20 4.56 4.93 5.31 5.69 6.09

Non-cash expense (Depreciation) 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95

Residual Value 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 5.00

Cash Flows after Tax 4.79 5.11 5.45 5.80 6.15 6.51 6.88 7.26 7.64 13.04

Table 2: Statement showing computation of payback period

Years Cash Flows (Amount in Million $) Cumulative Cash Flow

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

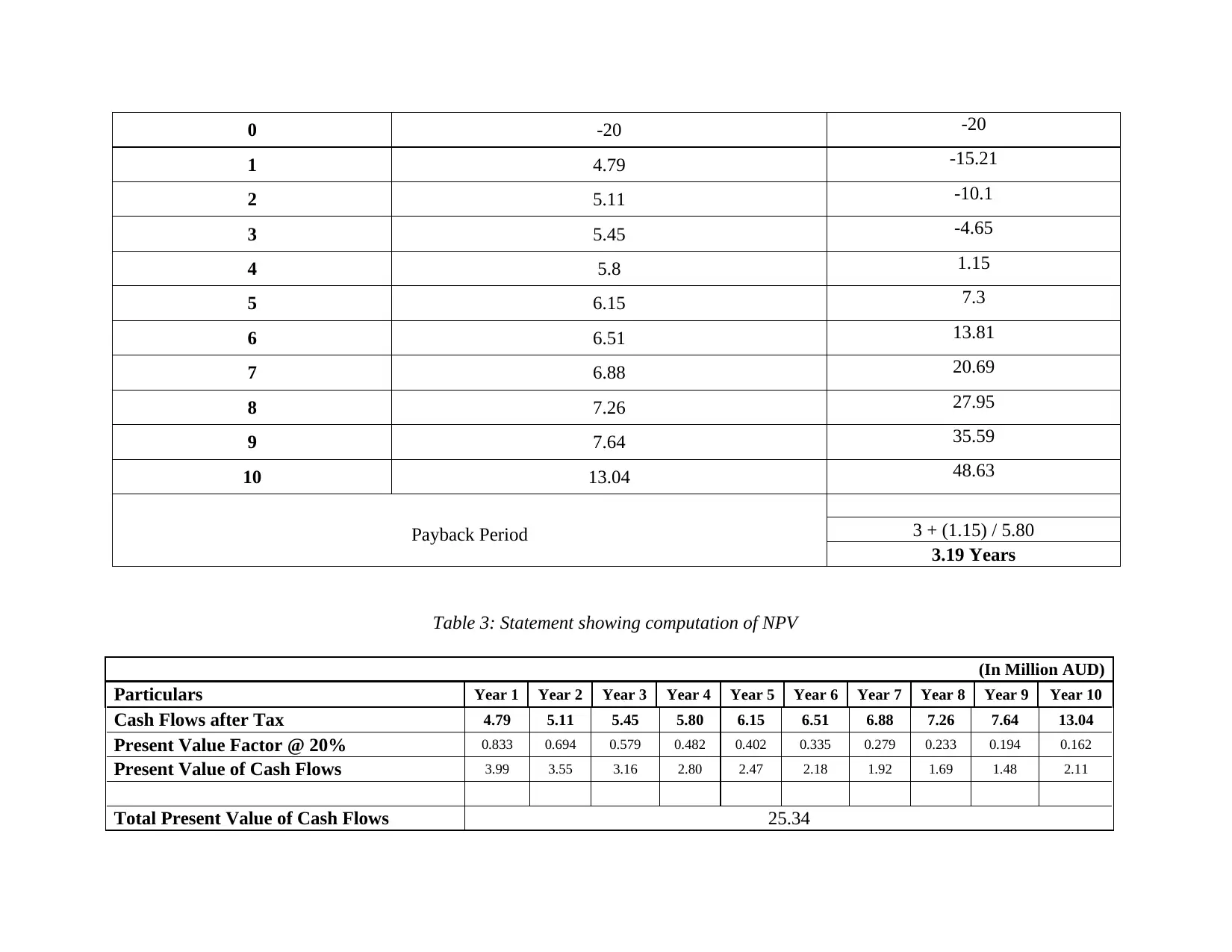

0 -20 -20

1 4.79 -15.21

2 5.11 -10.1

3 5.45 -4.65

4 5.8 1.15

5 6.15 7.3

6 6.51 13.81

7 6.88 20.69

8 7.26 27.95

9 7.64 35.59

10 13.04 48.63

Payback Period 3 + (1.15) / 5.80

3.19 Years

Table 3: Statement showing computation of NPV

(In Million AUD)

Particulars Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10

Cash Flows after Tax 4.79 5.11 5.45 5.80 6.15 6.51 6.88 7.26 7.64 13.04

Present Value Factor @ 20% 0.833 0.694 0.579 0.482 0.402 0.335 0.279 0.233 0.194 0.162

Present Value of Cash Flows 3.99 3.55 3.16 2.80 2.47 2.18 1.92 1.69 1.48 2.11

Total Present Value of Cash Flows 25.34

1 4.79 -15.21

2 5.11 -10.1

3 5.45 -4.65

4 5.8 1.15

5 6.15 7.3

6 6.51 13.81

7 6.88 20.69

8 7.26 27.95

9 7.64 35.59

10 13.04 48.63

Payback Period 3 + (1.15) / 5.80

3.19 Years

Table 3: Statement showing computation of NPV

(In Million AUD)

Particulars Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10

Cash Flows after Tax 4.79 5.11 5.45 5.80 6.15 6.51 6.88 7.26 7.64 13.04

Present Value Factor @ 20% 0.833 0.694 0.579 0.482 0.402 0.335 0.279 0.233 0.194 0.162

Present Value of Cash Flows 3.99 3.55 3.16 2.80 2.47 2.18 1.92 1.69 1.48 2.11

Total Present Value of Cash Flows 25.34

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

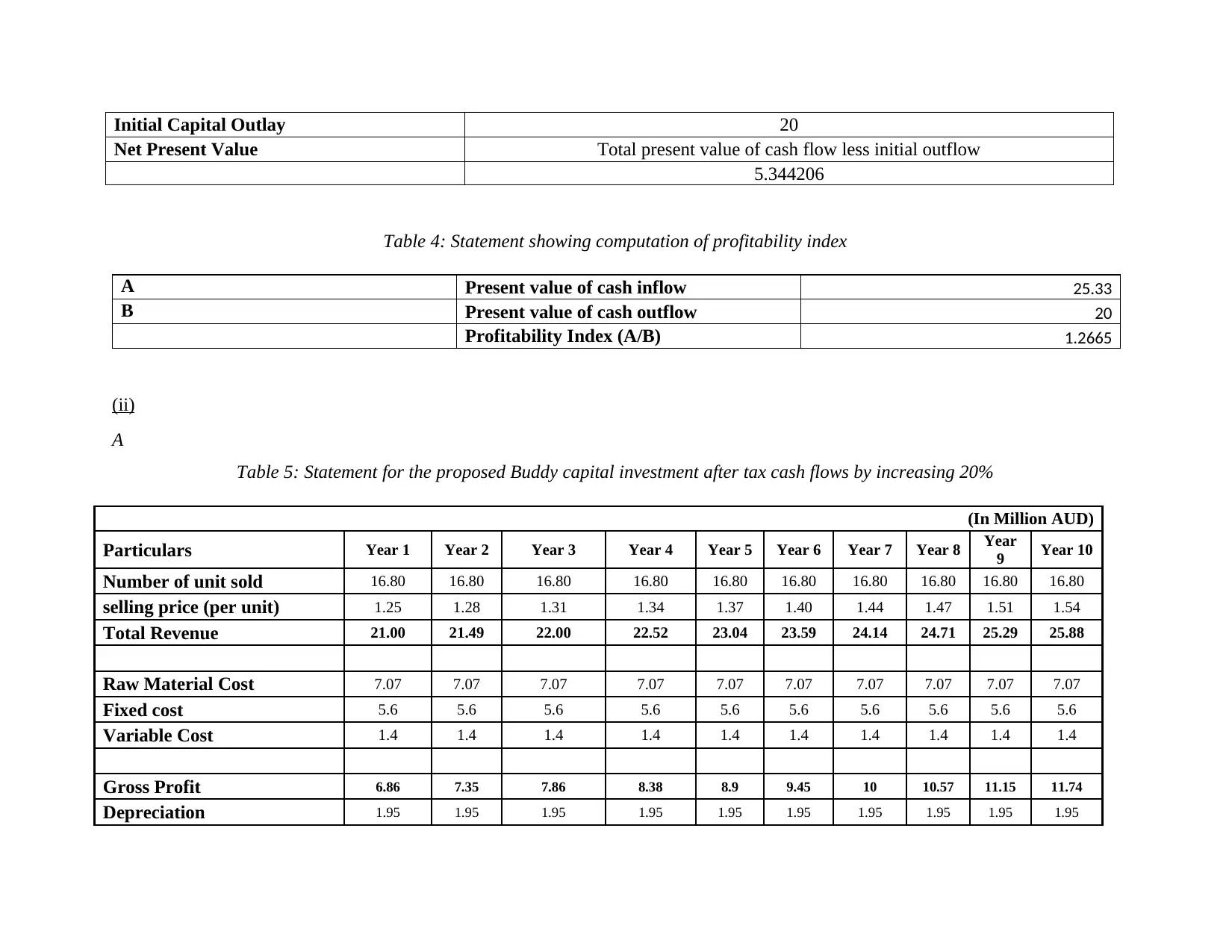

Initial Capital Outlay 20

Net Present Value Total present value of cash flow less initial outflow

5.344206

Table 4: Statement showing computation of profitability index

A Present value of cash inflow 25.33

B Present value of cash outflow 20

Profitability Index (A/B) 1.2665

(ii)

A

Table 5: Statement for the proposed Buddy capital investment after tax cash flows by increasing 20%

(In Million AUD)

Particulars Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year

9 Year 10

Number of unit sold 16.80 16.80 16.80 16.80 16.80 16.80 16.80 16.80 16.80 16.80

selling price (per unit) 1.25 1.28 1.31 1.34 1.37 1.40 1.44 1.47 1.51 1.54

Total Revenue 21.00 21.49 22.00 22.52 23.04 23.59 24.14 24.71 25.29 25.88

Raw Material Cost 7.07 7.07 7.07 7.07 7.07 7.07 7.07 7.07 7.07 7.07

Fixed cost 5.6 5.6 5.6 5.6 5.6 5.6 5.6 5.6 5.6 5.6

Variable Cost 1.4 1.4 1.4 1.4 1.4 1.4 1.4 1.4 1.4 1.4

Gross Profit 6.86 7.35 7.86 8.38 8.9 9.45 10 10.57 11.15 11.74

Depreciation 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95

Net Present Value Total present value of cash flow less initial outflow

5.344206

Table 4: Statement showing computation of profitability index

A Present value of cash inflow 25.33

B Present value of cash outflow 20

Profitability Index (A/B) 1.2665

(ii)

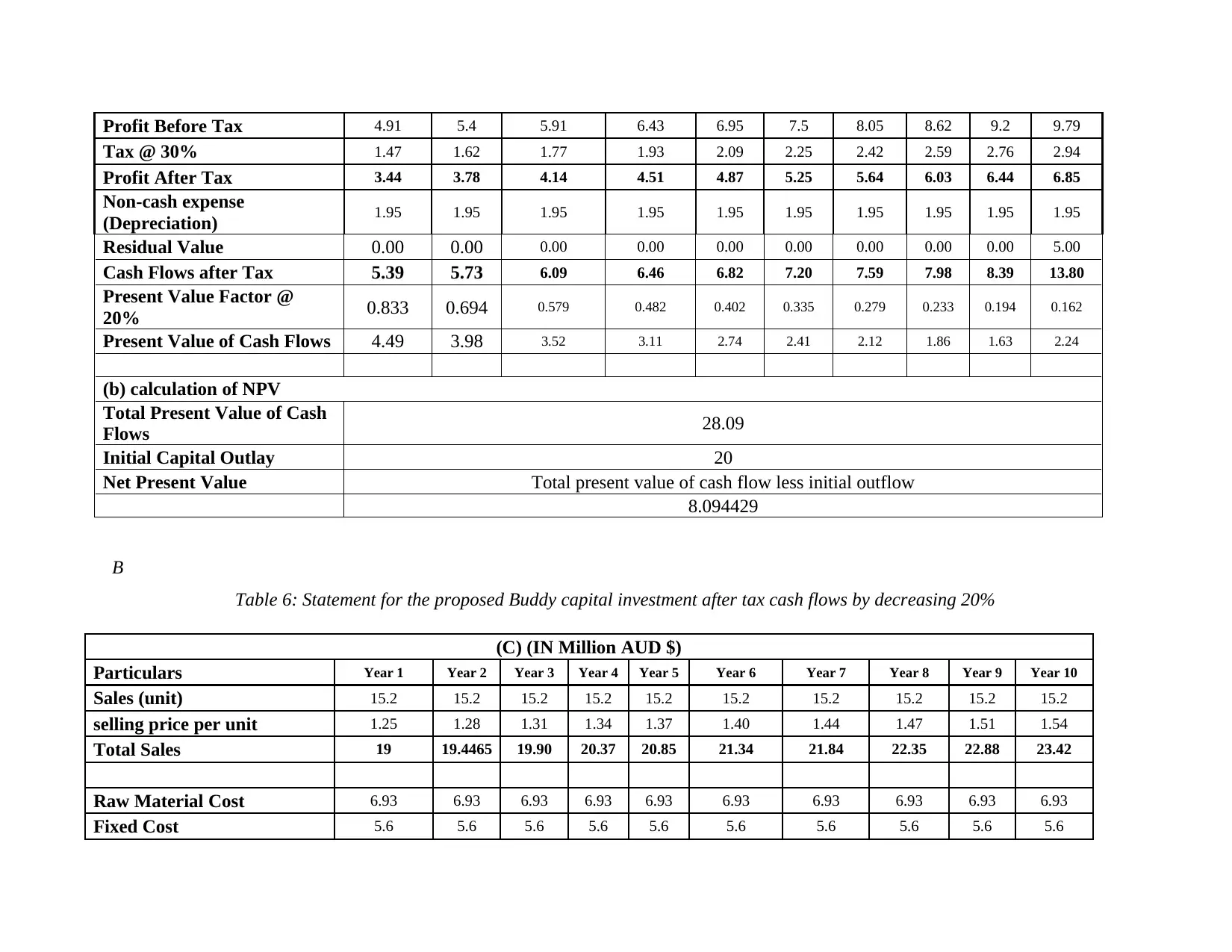

A

Table 5: Statement for the proposed Buddy capital investment after tax cash flows by increasing 20%

(In Million AUD)

Particulars Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year

9 Year 10

Number of unit sold 16.80 16.80 16.80 16.80 16.80 16.80 16.80 16.80 16.80 16.80

selling price (per unit) 1.25 1.28 1.31 1.34 1.37 1.40 1.44 1.47 1.51 1.54

Total Revenue 21.00 21.49 22.00 22.52 23.04 23.59 24.14 24.71 25.29 25.88

Raw Material Cost 7.07 7.07 7.07 7.07 7.07 7.07 7.07 7.07 7.07 7.07

Fixed cost 5.6 5.6 5.6 5.6 5.6 5.6 5.6 5.6 5.6 5.6

Variable Cost 1.4 1.4 1.4 1.4 1.4 1.4 1.4 1.4 1.4 1.4

Gross Profit 6.86 7.35 7.86 8.38 8.9 9.45 10 10.57 11.15 11.74

Depreciation 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95

Profit Before Tax 4.91 5.4 5.91 6.43 6.95 7.5 8.05 8.62 9.2 9.79

Tax @ 30% 1.47 1.62 1.77 1.93 2.09 2.25 2.42 2.59 2.76 2.94

Profit After Tax 3.44 3.78 4.14 4.51 4.87 5.25 5.64 6.03 6.44 6.85

Non-cash expense

(Depreciation) 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95

Residual Value 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 5.00

Cash Flows after Tax 5.39 5.73 6.09 6.46 6.82 7.20 7.59 7.98 8.39 13.80

Present Value Factor @

20% 0.833 0.694 0.579 0.482 0.402 0.335 0.279 0.233 0.194 0.162

Present Value of Cash Flows 4.49 3.98 3.52 3.11 2.74 2.41 2.12 1.86 1.63 2.24

(b) calculation of NPV

Total Present Value of Cash

Flows 28.09

Initial Capital Outlay 20

Net Present Value Total present value of cash flow less initial outflow

8.094429

B

Table 6: Statement for the proposed Buddy capital investment after tax cash flows by decreasing 20%

(C) (IN Million AUD $)

Particulars Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10

Sales (unit) 15.2 15.2 15.2 15.2 15.2 15.2 15.2 15.2 15.2 15.2

selling price per unit 1.25 1.28 1.31 1.34 1.37 1.40 1.44 1.47 1.51 1.54

Total Sales 19 19.4465 19.90 20.37 20.85 21.34 21.84 22.35 22.88 23.42

Raw Material Cost 6.93 6.93 6.93 6.93 6.93 6.93 6.93 6.93 6.93 6.93

Fixed Cost 5.6 5.6 5.6 5.6 5.6 5.6 5.6 5.6 5.6 5.6

Tax @ 30% 1.47 1.62 1.77 1.93 2.09 2.25 2.42 2.59 2.76 2.94

Profit After Tax 3.44 3.78 4.14 4.51 4.87 5.25 5.64 6.03 6.44 6.85

Non-cash expense

(Depreciation) 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95

Residual Value 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 5.00

Cash Flows after Tax 5.39 5.73 6.09 6.46 6.82 7.20 7.59 7.98 8.39 13.80

Present Value Factor @

20% 0.833 0.694 0.579 0.482 0.402 0.335 0.279 0.233 0.194 0.162

Present Value of Cash Flows 4.49 3.98 3.52 3.11 2.74 2.41 2.12 1.86 1.63 2.24

(b) calculation of NPV

Total Present Value of Cash

Flows 28.09

Initial Capital Outlay 20

Net Present Value Total present value of cash flow less initial outflow

8.094429

B

Table 6: Statement for the proposed Buddy capital investment after tax cash flows by decreasing 20%

(C) (IN Million AUD $)

Particulars Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10

Sales (unit) 15.2 15.2 15.2 15.2 15.2 15.2 15.2 15.2 15.2 15.2

selling price per unit 1.25 1.28 1.31 1.34 1.37 1.40 1.44 1.47 1.51 1.54

Total Sales 19 19.4465 19.90 20.37 20.85 21.34 21.84 22.35 22.88 23.42

Raw Material Cost 6.93 6.93 6.93 6.93 6.93 6.93 6.93 6.93 6.93 6.93

Fixed Cost 5.6 5.6 5.6 5.6 5.6 5.6 5.6 5.6 5.6 5.6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

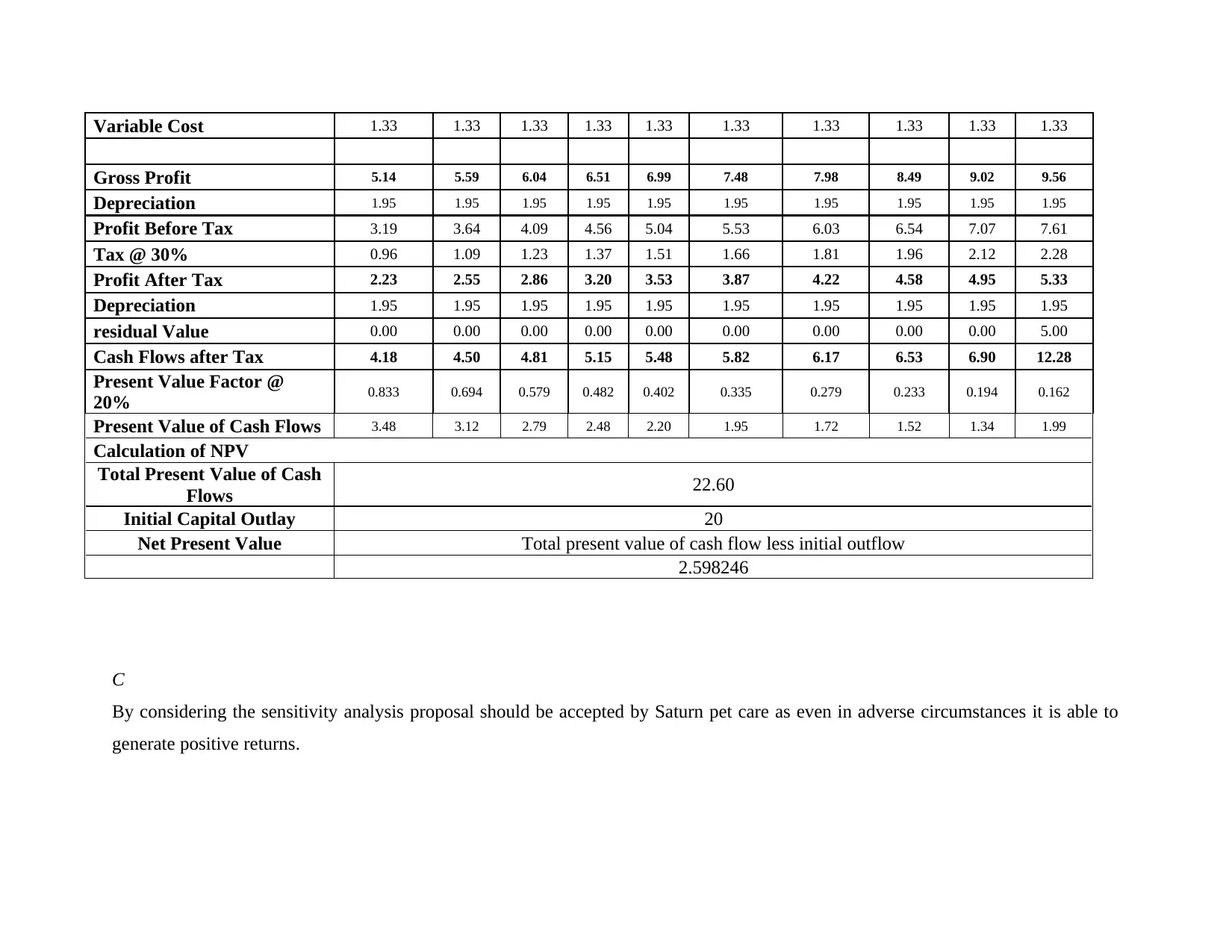

Variable Cost 1.33 1.33 1.33 1.33 1.33 1.33 1.33 1.33 1.33 1.33

Gross Profit 5.14 5.59 6.04 6.51 6.99 7.48 7.98 8.49 9.02 9.56

Depreciation 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95

Profit Before Tax 3.19 3.64 4.09 4.56 5.04 5.53 6.03 6.54 7.07 7.61

Tax @ 30% 0.96 1.09 1.23 1.37 1.51 1.66 1.81 1.96 2.12 2.28

Profit After Tax 2.23 2.55 2.86 3.20 3.53 3.87 4.22 4.58 4.95 5.33

Depreciation 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95

residual Value 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 5.00

Cash Flows after Tax 4.18 4.50 4.81 5.15 5.48 5.82 6.17 6.53 6.90 12.28

Present Value Factor @

20% 0.833 0.694 0.579 0.482 0.402 0.335 0.279 0.233 0.194 0.162

Present Value of Cash Flows 3.48 3.12 2.79 2.48 2.20 1.95 1.72 1.52 1.34 1.99

Calculation of NPV

Total Present Value of Cash

Flows 22.60

Initial Capital Outlay 20

Net Present Value Total present value of cash flow less initial outflow

2.598246

C

By considering the sensitivity analysis proposal should be accepted by Saturn pet care as even in adverse circumstances it is able to

generate positive returns.

Gross Profit 5.14 5.59 6.04 6.51 6.99 7.48 7.98 8.49 9.02 9.56

Depreciation 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95

Profit Before Tax 3.19 3.64 4.09 4.56 5.04 5.53 6.03 6.54 7.07 7.61

Tax @ 30% 0.96 1.09 1.23 1.37 1.51 1.66 1.81 1.96 2.12 2.28

Profit After Tax 2.23 2.55 2.86 3.20 3.53 3.87 4.22 4.58 4.95 5.33

Depreciation 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95 1.95

residual Value 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 5.00

Cash Flows after Tax 4.18 4.50 4.81 5.15 5.48 5.82 6.17 6.53 6.90 12.28

Present Value Factor @

20% 0.833 0.694 0.579 0.482 0.402 0.335 0.279 0.233 0.194 0.162

Present Value of Cash Flows 3.48 3.12 2.79 2.48 2.20 1.95 1.72 1.52 1.34 1.99

Calculation of NPV

Total Present Value of Cash

Flows 22.60

Initial Capital Outlay 20

Net Present Value Total present value of cash flow less initial outflow

2.598246

C

By considering the sensitivity analysis proposal should be accepted by Saturn pet care as even in adverse circumstances it is able to

generate positive returns.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

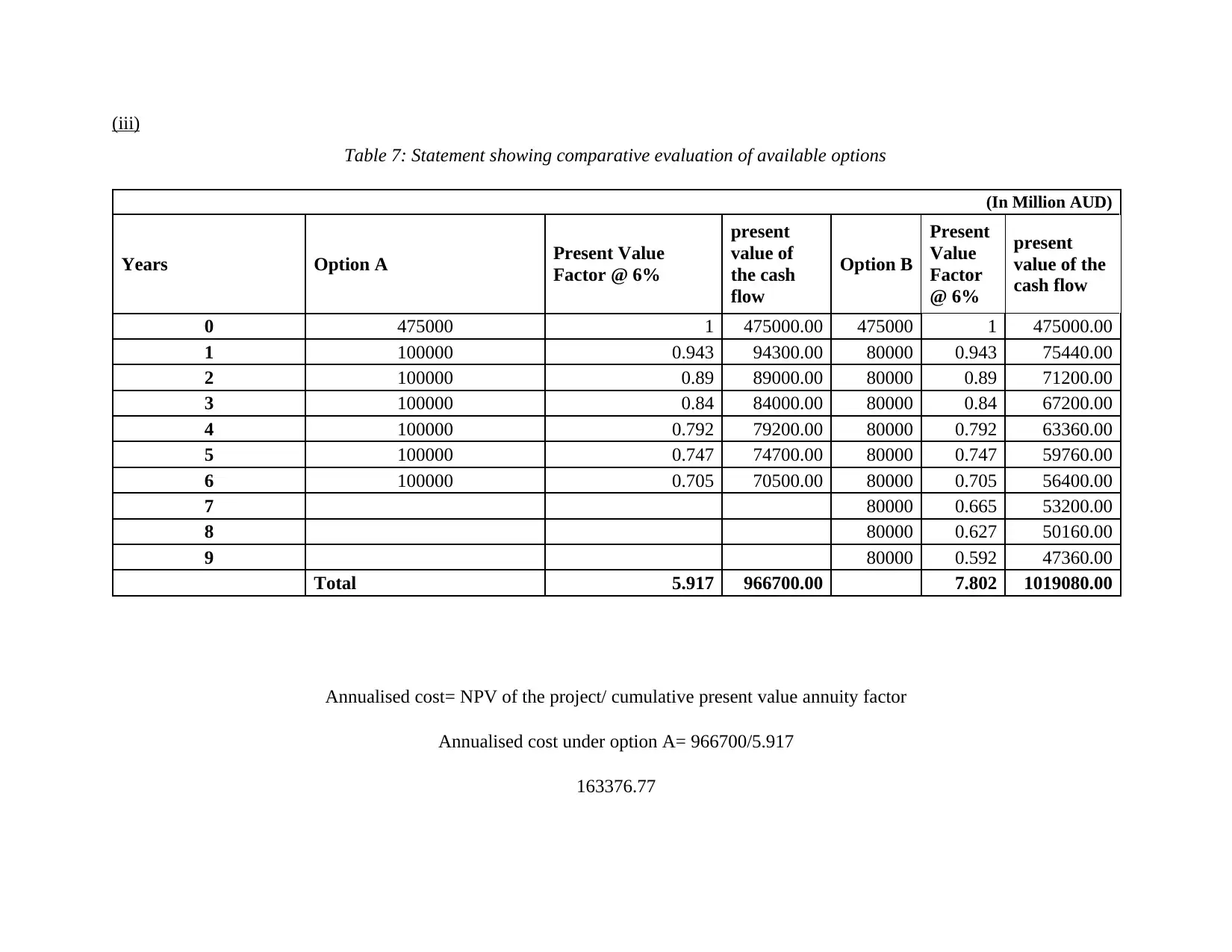

(iii)

Table 7: Statement showing comparative evaluation of available options

(In Million AUD)

Years Option A Present Value

Factor @ 6%

present

value of

the cash

flow

Option B

Present

Value

Factor

@ 6%

present

value of the

cash flow

0 475000 1 475000.00 475000 1 475000.00

1 100000 0.943 94300.00 80000 0.943 75440.00

2 100000 0.89 89000.00 80000 0.89 71200.00

3 100000 0.84 84000.00 80000 0.84 67200.00

4 100000 0.792 79200.00 80000 0.792 63360.00

5 100000 0.747 74700.00 80000 0.747 59760.00

6 100000 0.705 70500.00 80000 0.705 56400.00

7 80000 0.665 53200.00

8 80000 0.627 50160.00

9 80000 0.592 47360.00

Total 5.917 966700.00 7.802 1019080.00

Annualised cost= NPV of the project/ cumulative present value annuity factor

Annualised cost under option A= 966700/5.917

163376.77

Table 7: Statement showing comparative evaluation of available options

(In Million AUD)

Years Option A Present Value

Factor @ 6%

present

value of

the cash

flow

Option B

Present

Value

Factor

@ 6%

present

value of the

cash flow

0 475000 1 475000.00 475000 1 475000.00

1 100000 0.943 94300.00 80000 0.943 75440.00

2 100000 0.89 89000.00 80000 0.89 71200.00

3 100000 0.84 84000.00 80000 0.84 67200.00

4 100000 0.792 79200.00 80000 0.792 63360.00

5 100000 0.747 74700.00 80000 0.747 59760.00

6 100000 0.705 70500.00 80000 0.705 56400.00

7 80000 0.665 53200.00

8 80000 0.627 50160.00

9 80000 0.592 47360.00

Total 5.917 966700.00 7.802 1019080.00

Annualised cost= NPV of the project/ cumulative present value annuity factor

Annualised cost under option A= 966700/5.917

163376.77

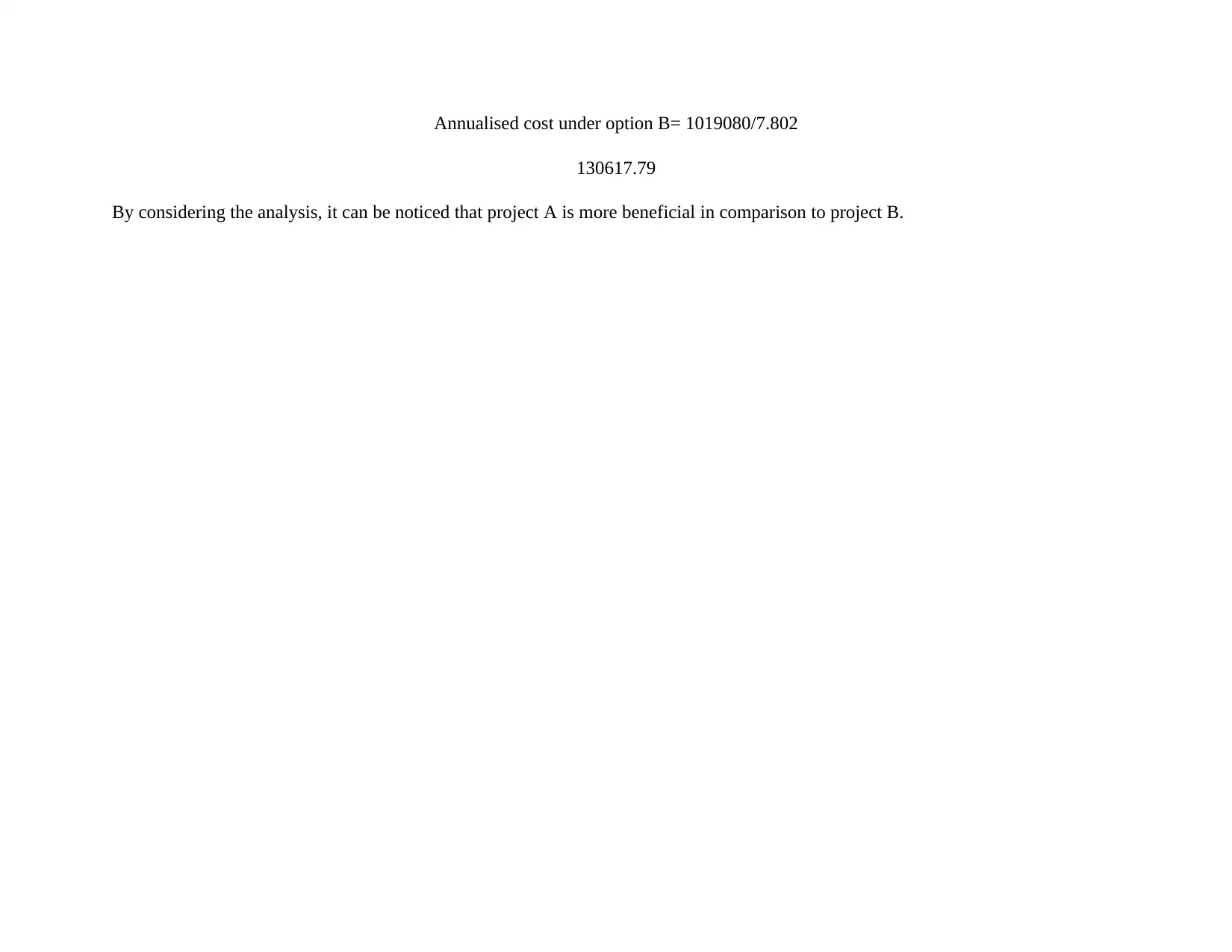

Annualised cost under option B= 1019080/7.802

130617.79

By considering the analysis, it can be noticed that project A is more beneficial in comparison to project B.

130617.79

By considering the analysis, it can be noticed that project A is more beneficial in comparison to project B.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

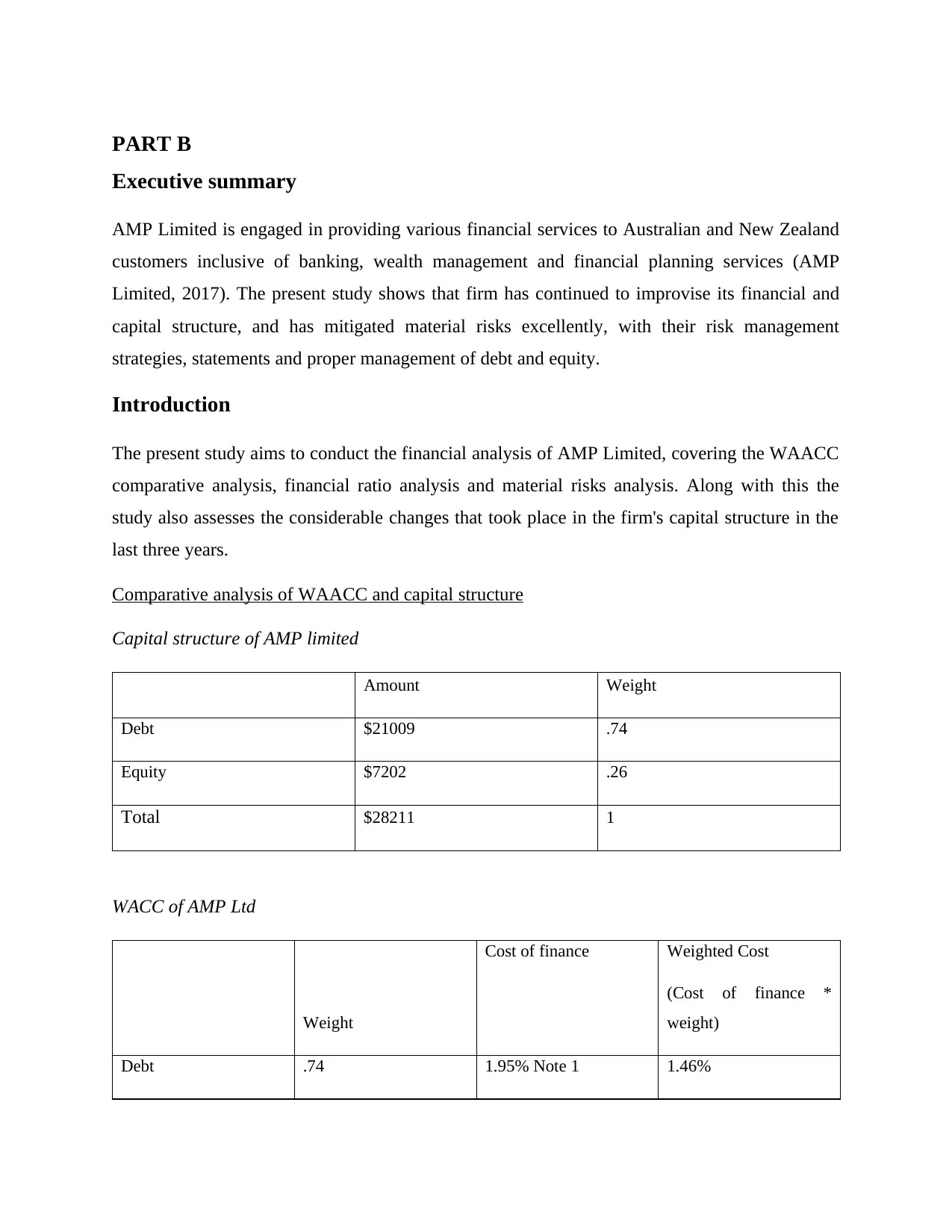

PART B

Executive summary

AMP Limited is engaged in providing various financial services to Australian and New Zealand

customers inclusive of banking, wealth management and financial planning services (AMP

Limited, 2017). The present study shows that firm has continued to improvise its financial and

capital structure, and has mitigated material risks excellently, with their risk management

strategies, statements and proper management of debt and equity.

Introduction

The present study aims to conduct the financial analysis of AMP Limited, covering the WAACC

comparative analysis, financial ratio analysis and material risks analysis. Along with this the

study also assesses the considerable changes that took place in the firm's capital structure in the

last three years.

Comparative analysis of WAACC and capital structure

Capital structure of AMP limited

Amount Weight

Debt $21009 .74

Equity $7202 .26

Total $28211 1

WACC of AMP Ltd

Weight

Cost of finance Weighted Cost

(Cost of finance *

weight)

Debt .74 1.95% Note 1 1.46%

Executive summary

AMP Limited is engaged in providing various financial services to Australian and New Zealand

customers inclusive of banking, wealth management and financial planning services (AMP

Limited, 2017). The present study shows that firm has continued to improvise its financial and

capital structure, and has mitigated material risks excellently, with their risk management

strategies, statements and proper management of debt and equity.

Introduction

The present study aims to conduct the financial analysis of AMP Limited, covering the WAACC

comparative analysis, financial ratio analysis and material risks analysis. Along with this the

study also assesses the considerable changes that took place in the firm's capital structure in the

last three years.

Comparative analysis of WAACC and capital structure

Capital structure of AMP limited

Amount Weight

Debt $21009 .74

Equity $7202 .26

Total $28211 1

WACC of AMP Ltd

Weight

Cost of finance Weighted Cost

(Cost of finance *

weight)

Debt .74 1.95% Note 1 1.46%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

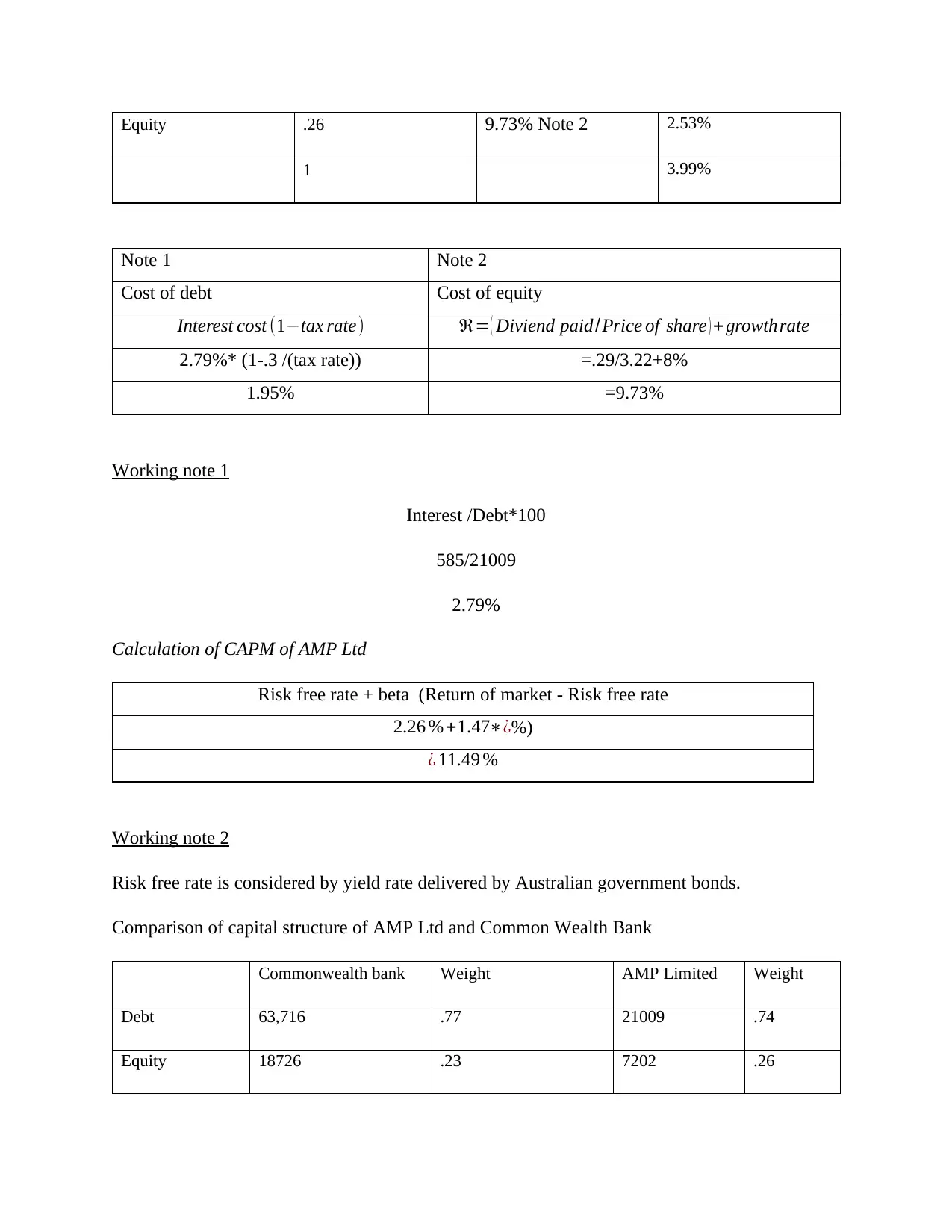

Equity .26 9.73% Note 2 2.53%

1 3.99%

Note 1 Note 2

Cost of debt Cost of equity

Interest cost (1−tax rate) ℜ= ( Diviend paid/Price of share ) + growthrate

2.79%* (1-.3 /(tax rate)) =.29/3.22+8%

1.95% =9.73%

Working note 1

Interest /Debt*100

585/21009

2.79%

Calculation of CAPM of AMP Ltd

Risk free rate + beta (Return of market - Risk free rate

2.26 % +1.47∗¿%)

¿ 11.49 %

Working note 2

Risk free rate is considered by yield rate delivered by Australian government bonds.

Comparison of capital structure of AMP Ltd and Common Wealth Bank

Commonwealth bank Weight AMP Limited Weight

Debt 63,716 .77 21009 .74

Equity 18726 .23 7202 .26

1 3.99%

Note 1 Note 2

Cost of debt Cost of equity

Interest cost (1−tax rate) ℜ= ( Diviend paid/Price of share ) + growthrate

2.79%* (1-.3 /(tax rate)) =.29/3.22+8%

1.95% =9.73%

Working note 1

Interest /Debt*100

585/21009

2.79%

Calculation of CAPM of AMP Ltd

Risk free rate + beta (Return of market - Risk free rate

2.26 % +1.47∗¿%)

¿ 11.49 %

Working note 2

Risk free rate is considered by yield rate delivered by Australian government bonds.

Comparison of capital structure of AMP Ltd and Common Wealth Bank

Commonwealth bank Weight AMP Limited Weight

Debt 63,716 .77 21009 .74

Equity 18726 .23 7202 .26

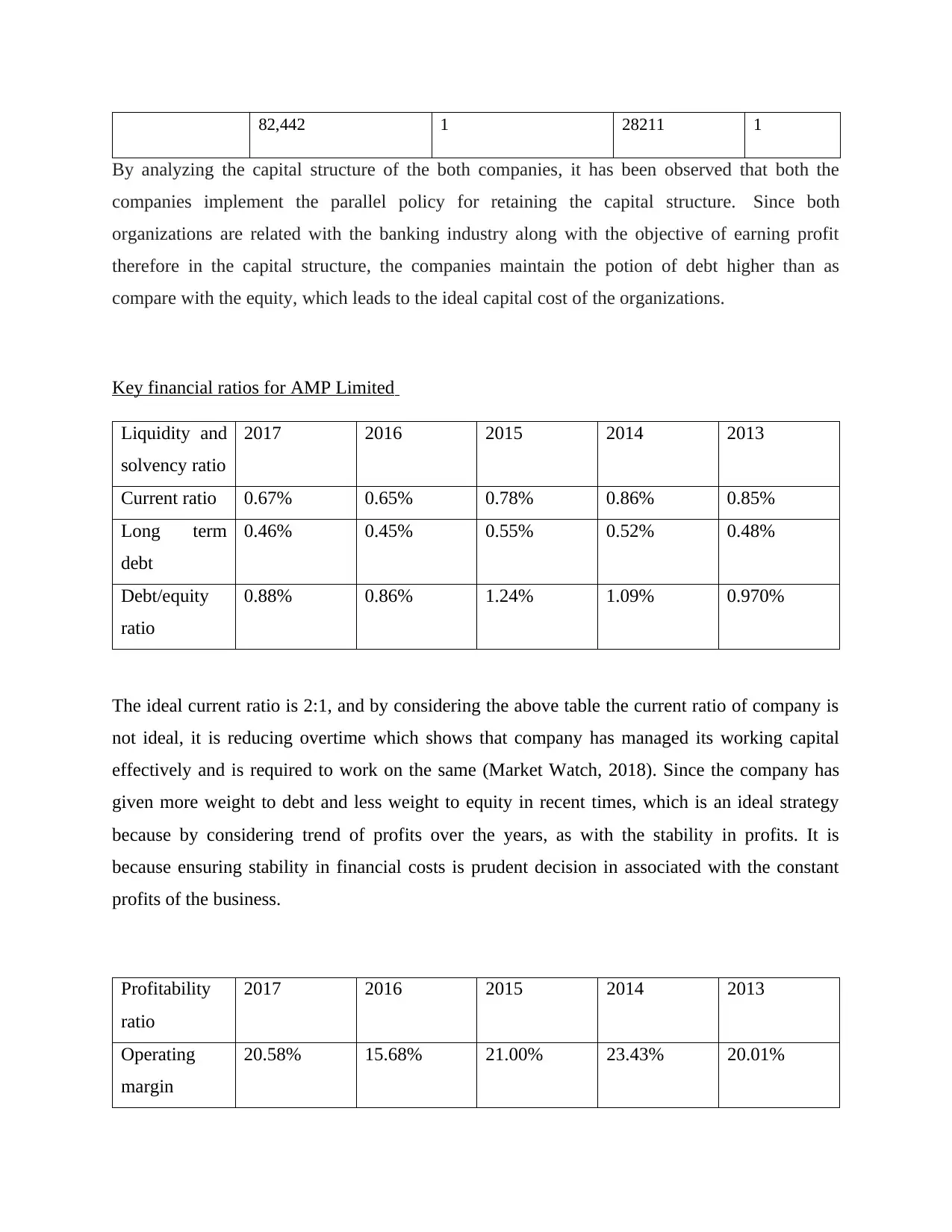

82,442 1 28211 1

By analyzing the capital structure of the both companies, it has been observed that both the

companies implement the parallel policy for retaining the capital structure. Since both

organizations are related with the banking industry along with the objective of earning profit

therefore in the capital structure, the companies maintain the potion of debt higher than as

compare with the equity, which leads to the ideal capital cost of the organizations.

Key financial ratios for AMP Limited

Liquidity and

solvency ratio

2017 2016 2015 2014 2013

Current ratio 0.67% 0.65% 0.78% 0.86% 0.85%

Long term

debt

0.46% 0.45% 0.55% 0.52% 0.48%

Debt/equity

ratio

0.88% 0.86% 1.24% 1.09% 0.970%

The ideal current ratio is 2:1, and by considering the above table the current ratio of company is

not ideal, it is reducing overtime which shows that company has managed its working capital

effectively and is required to work on the same (Market Watch, 2018). Since the company has

given more weight to debt and less weight to equity in recent times, which is an ideal strategy

because by considering trend of profits over the years, as with the stability in profits. It is

because ensuring stability in financial costs is prudent decision in associated with the constant

profits of the business.

Profitability

ratio

2017 2016 2015 2014 2013

Operating

margin

20.58% 15.68% 21.00% 23.43% 20.01%

By analyzing the capital structure of the both companies, it has been observed that both the

companies implement the parallel policy for retaining the capital structure. Since both

organizations are related with the banking industry along with the objective of earning profit

therefore in the capital structure, the companies maintain the potion of debt higher than as

compare with the equity, which leads to the ideal capital cost of the organizations.

Key financial ratios for AMP Limited

Liquidity and

solvency ratio

2017 2016 2015 2014 2013

Current ratio 0.67% 0.65% 0.78% 0.86% 0.85%

Long term

debt

0.46% 0.45% 0.55% 0.52% 0.48%

Debt/equity

ratio

0.88% 0.86% 1.24% 1.09% 0.970%

The ideal current ratio is 2:1, and by considering the above table the current ratio of company is

not ideal, it is reducing overtime which shows that company has managed its working capital

effectively and is required to work on the same (Market Watch, 2018). Since the company has

given more weight to debt and less weight to equity in recent times, which is an ideal strategy

because by considering trend of profits over the years, as with the stability in profits. It is

because ensuring stability in financial costs is prudent decision in associated with the constant

profits of the business.

Profitability

ratio

2017 2016 2015 2014 2013

Operating

margin

20.58% 15.68% 21.00% 23.43% 20.01%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.