S Plc: Investment Appraisal, CVP Analysis, and Sourcing Strategies

VerifiedAdded on 2023/06/16

|20

|4051

|454

Report

AI Summary

This business report delves into capital investment appraisal for S Plc, a computer games company. It defines the significance of the capital investment appraisal process, drafts a cash flow analysis statement, identifies the payback period for a new investment, and assesses the viability using the net present value (NPV) approach. The report also describes the logic behind the NPV method and its association with the cost of capital, assesses the internal rate of return (IRR), and states reasons why NPV is considered a better approach than IRR. Furthermore, it critically evaluates equity issues versus bank loans for long-term finance, presents a cost-volume-profit (CVP) analysis, and examines the consequences of price level changes on CVP analysis. Finally, the report distinguishes categories of suppliers, compares single and multiple sourcing benefits, and explains cross-sourcing and its benefits to the buyer, providing a comprehensive overview of financial and strategic considerations for S Plc. Desklib provides a platform to access similar solved assignments.

Business Report

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK...............................................................................................................................................3

A......................................................................................................................................................3

1. Defining the significance of capital investment appraisal process..........................................3

2. Drafting cash flow analysis statement.....................................................................................3

3. Identifying payback period for the new investment................................................................4

4. Assessing the viability of proposed investment using net present value approach.................5

5. Describing the logic behind the net present value method and its association with cost of

capital...........................................................................................................................................6

6. Assessing internal rate of return..............................................................................................6

8. Stating reasons due to which NPV considered as better approach over IRR..........................7

B).....................................................................................................................................................7

Critically evaluating an equity issue with bank loan for all its long-term finance requirements 7

C).....................................................................................................................................................7

1. Presenting CVP analysis referring given scenario...................................................................7

2. What are the consequences pertaining to CVP analysis when price level changes.................7

D).....................................................................................................................................................8

1) Distinguishing the categories of suppliers...............................................................................8

2) Comparing the benefits of single and multiple sourcing with regards to procurement..........8

3) Explaining cross-sourcing and its benefit to the buyer...........................................................8

INTRODUCTION...........................................................................................................................3

TASK...............................................................................................................................................3

A......................................................................................................................................................3

1. Defining the significance of capital investment appraisal process..........................................3

2. Drafting cash flow analysis statement.....................................................................................3

3. Identifying payback period for the new investment................................................................4

4. Assessing the viability of proposed investment using net present value approach.................5

5. Describing the logic behind the net present value method and its association with cost of

capital...........................................................................................................................................6

6. Assessing internal rate of return..............................................................................................6

8. Stating reasons due to which NPV considered as better approach over IRR..........................7

B).....................................................................................................................................................7

Critically evaluating an equity issue with bank loan for all its long-term finance requirements 7

C).....................................................................................................................................................7

1. Presenting CVP analysis referring given scenario...................................................................7

2. What are the consequences pertaining to CVP analysis when price level changes.................7

D).....................................................................................................................................................8

1) Distinguishing the categories of suppliers...............................................................................8

2) Comparing the benefits of single and multiple sourcing with regards to procurement..........8

3) Explaining cross-sourcing and its benefit to the buyer...........................................................8

CONCLUSION................................................................................................................................8

REFERENCES..............................................................................................................................10

REFERENCES..............................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

In the dynamic business arena, success of business unit is highly influenced from

decisions undertaken by manager. There are several tools and techniques which manager can

undertake for assessing or evaluating business opportunities. Thus, it is an accountability of

manager to undertaken competent investment decisions which aid in the growth and profitability

of firm. The present report is based on S Plc which deals in computer games and now with the

motive to attain success company is planning to add new line. In this, report will provide deeper

understanding about the manner in which capital budgeting tools aid in investment decision

making or selection. Further, it also highlights the contribution of cost, volume and profit

relationship pertaining to financial decision making. Report also presents how bank loan source

is cheaper source in comparison to equity issuance. It also depicts the categories of suppliers

which S Plc can employ for the purpose of procurement.

TASK

A

1. Defining the significance of capital investment appraisal process

Capital budgeting may be defined as a process which emphasizes on the selection of

project which aid in firm’s value. According to the given case scenario, S plc is planning to

include new line of computer game which requires initial investment of £1300000. In this regard,

capital budgeting tools are considered as highly significant as it helps in creating both

accountability and measurability. In other words, by applying investment appraisal tools such as

payback period, NPV and IRR S Plc can assess whether long term investment will maximize

shareholder’s wealth or not (Kengatharan, 2018). In addition to this, concerned tools and

techniques assist in evaluating risk and profitability, associated with the potential investment, to

the large extent.

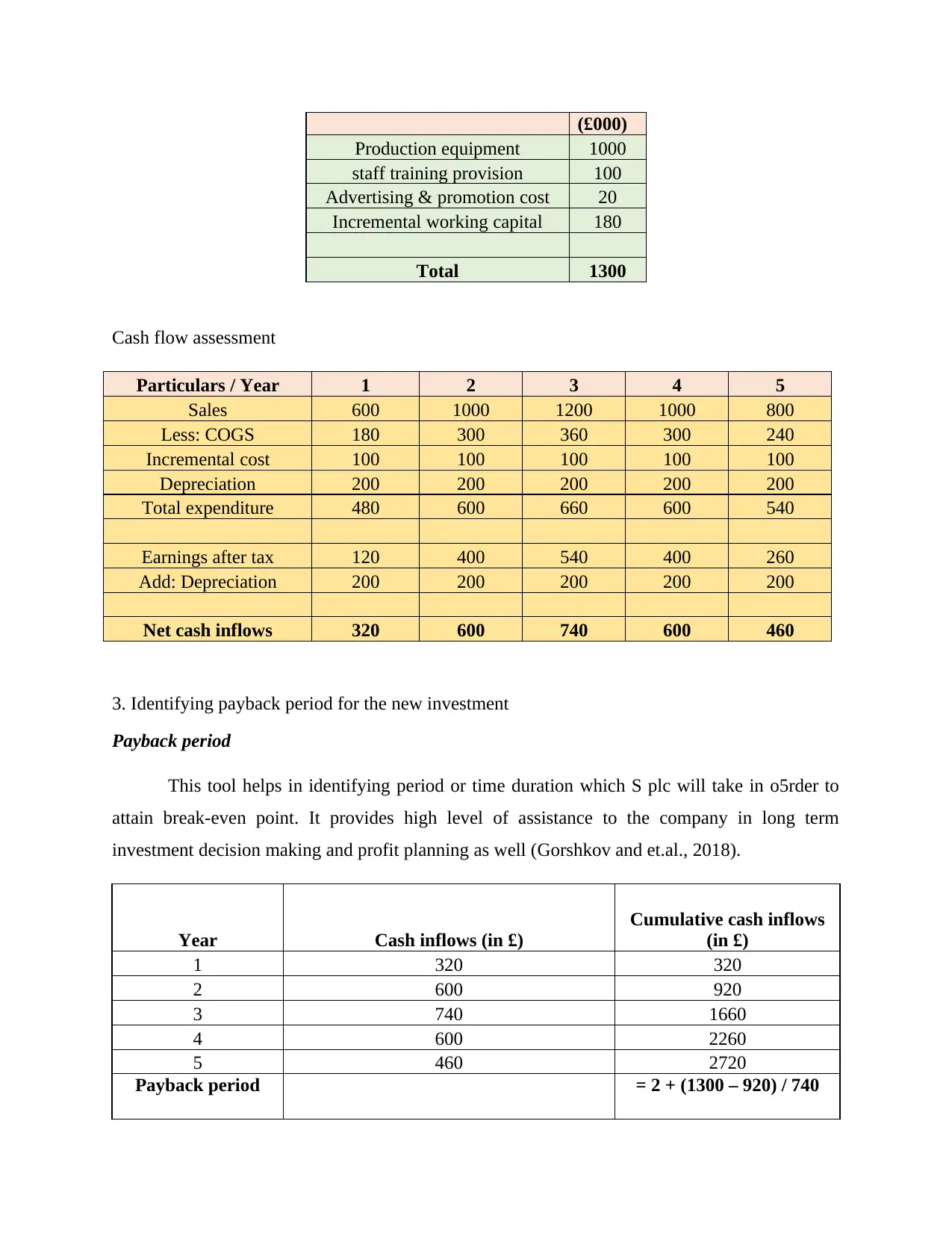

2. Drafting cash flow analysis statement

Initial investment

Particulars Figures

In the dynamic business arena, success of business unit is highly influenced from

decisions undertaken by manager. There are several tools and techniques which manager can

undertake for assessing or evaluating business opportunities. Thus, it is an accountability of

manager to undertaken competent investment decisions which aid in the growth and profitability

of firm. The present report is based on S Plc which deals in computer games and now with the

motive to attain success company is planning to add new line. In this, report will provide deeper

understanding about the manner in which capital budgeting tools aid in investment decision

making or selection. Further, it also highlights the contribution of cost, volume and profit

relationship pertaining to financial decision making. Report also presents how bank loan source

is cheaper source in comparison to equity issuance. It also depicts the categories of suppliers

which S Plc can employ for the purpose of procurement.

TASK

A

1. Defining the significance of capital investment appraisal process

Capital budgeting may be defined as a process which emphasizes on the selection of

project which aid in firm’s value. According to the given case scenario, S plc is planning to

include new line of computer game which requires initial investment of £1300000. In this regard,

capital budgeting tools are considered as highly significant as it helps in creating both

accountability and measurability. In other words, by applying investment appraisal tools such as

payback period, NPV and IRR S Plc can assess whether long term investment will maximize

shareholder’s wealth or not (Kengatharan, 2018). In addition to this, concerned tools and

techniques assist in evaluating risk and profitability, associated with the potential investment, to

the large extent.

2. Drafting cash flow analysis statement

Initial investment

Particulars Figures

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(£000)

Production equipment 1000

staff training provision 100

Advertising & promotion cost 20

Incremental working capital 180

Total 1300

Cash flow assessment

Particulars / Year 1 2 3 4 5

Sales 600 1000 1200 1000 800

Less: COGS 180 300 360 300 240

Incremental cost 100 100 100 100 100

Depreciation 200 200 200 200 200

Total expenditure 480 600 660 600 540

Earnings after tax 120 400 540 400 260

Add: Depreciation 200 200 200 200 200

Net cash inflows 320 600 740 600 460

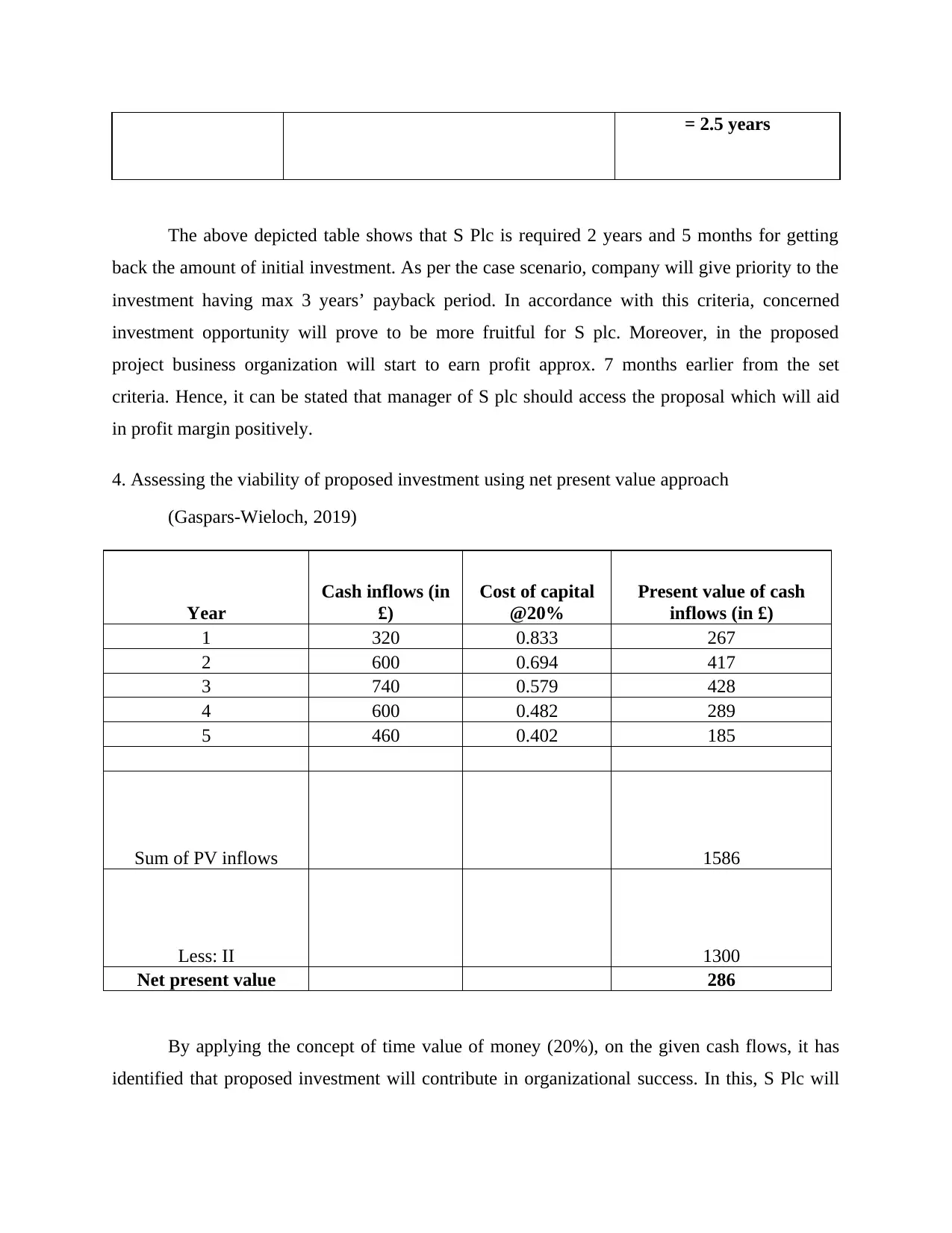

3. Identifying payback period for the new investment

Payback period

This tool helps in identifying period or time duration which S plc will take in o5rder to

attain break-even point. It provides high level of assistance to the company in long term

investment decision making and profit planning as well (Gorshkov and et.al., 2018).

Year Cash inflows (in £)

Cumulative cash inflows

(in £)

1 320 320

2 600 920

3 740 1660

4 600 2260

5 460 2720

Payback period = 2 + (1300 – 920) / 740

Production equipment 1000

staff training provision 100

Advertising & promotion cost 20

Incremental working capital 180

Total 1300

Cash flow assessment

Particulars / Year 1 2 3 4 5

Sales 600 1000 1200 1000 800

Less: COGS 180 300 360 300 240

Incremental cost 100 100 100 100 100

Depreciation 200 200 200 200 200

Total expenditure 480 600 660 600 540

Earnings after tax 120 400 540 400 260

Add: Depreciation 200 200 200 200 200

Net cash inflows 320 600 740 600 460

3. Identifying payback period for the new investment

Payback period

This tool helps in identifying period or time duration which S plc will take in o5rder to

attain break-even point. It provides high level of assistance to the company in long term

investment decision making and profit planning as well (Gorshkov and et.al., 2018).

Year Cash inflows (in £)

Cumulative cash inflows

(in £)

1 320 320

2 600 920

3 740 1660

4 600 2260

5 460 2720

Payback period = 2 + (1300 – 920) / 740

= 2.5 years

The above depicted table shows that S Plc is required 2 years and 5 months for getting

back the amount of initial investment. As per the case scenario, company will give priority to the

investment having max 3 years’ payback period. In accordance with this criteria, concerned

investment opportunity will prove to be more fruitful for S plc. Moreover, in the proposed

project business organization will start to earn profit approx. 7 months earlier from the set

criteria. Hence, it can be stated that manager of S plc should access the proposal which will aid

in profit margin positively.

4. Assessing the viability of proposed investment using net present value approach

(Gaspars-Wieloch, 2019)

Year

Cash inflows (in

£)

Cost of capital

@20%

Present value of cash

inflows (in £)

1 320 0.833 267

2 600 0.694 417

3 740 0.579 428

4 600 0.482 289

5 460 0.402 185

Sum of PV inflows 1586

Less: II 1300

Net present value 286

By applying the concept of time value of money (20%), on the given cash flows, it has

identified that proposed investment will contribute in organizational success. In this, S Plc will

The above depicted table shows that S Plc is required 2 years and 5 months for getting

back the amount of initial investment. As per the case scenario, company will give priority to the

investment having max 3 years’ payback period. In accordance with this criteria, concerned

investment opportunity will prove to be more fruitful for S plc. Moreover, in the proposed

project business organization will start to earn profit approx. 7 months earlier from the set

criteria. Hence, it can be stated that manager of S plc should access the proposal which will aid

in profit margin positively.

4. Assessing the viability of proposed investment using net present value approach

(Gaspars-Wieloch, 2019)

Year

Cash inflows (in

£)

Cost of capital

@20%

Present value of cash

inflows (in £)

1 320 0.833 267

2 600 0.694 417

3 740 0.579 428

4 600 0.482 289

5 460 0.402 185

Sum of PV inflows 1586

Less: II 1300

Net present value 286

By applying the concept of time value of money (20%), on the given cash flows, it has

identified that proposed investment will contribute in organizational success. In this, S Plc will

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

get £286000 after the period of five years. It shows that company is getting positive and higher

return in against to the initial investment made. As per overall evaluation company should go

with new line of computer game. This in turn helps it in getting the desired level of outcome or

success.

5. Describing the logic behind the net present value method and its association with cost of

capital

NPV method of investment appraisal represents difference which takes place between

present values of cash inflows and outflows. It provides high level of assistance to the manager

in taking appropriate decision about investment by analyzing profitability (Sarwary, 2020). NPV

and cost of capital is highly associated with each other. Moreover, cost capital (WACC) helps in

determining opportunity cost and thereby assists S Plc in selecting best alternative available for

investment purpose. NPV and WACC help company in assessing the whether concerned

opportunity prove to be beneficial or not (Bierman, 2020).

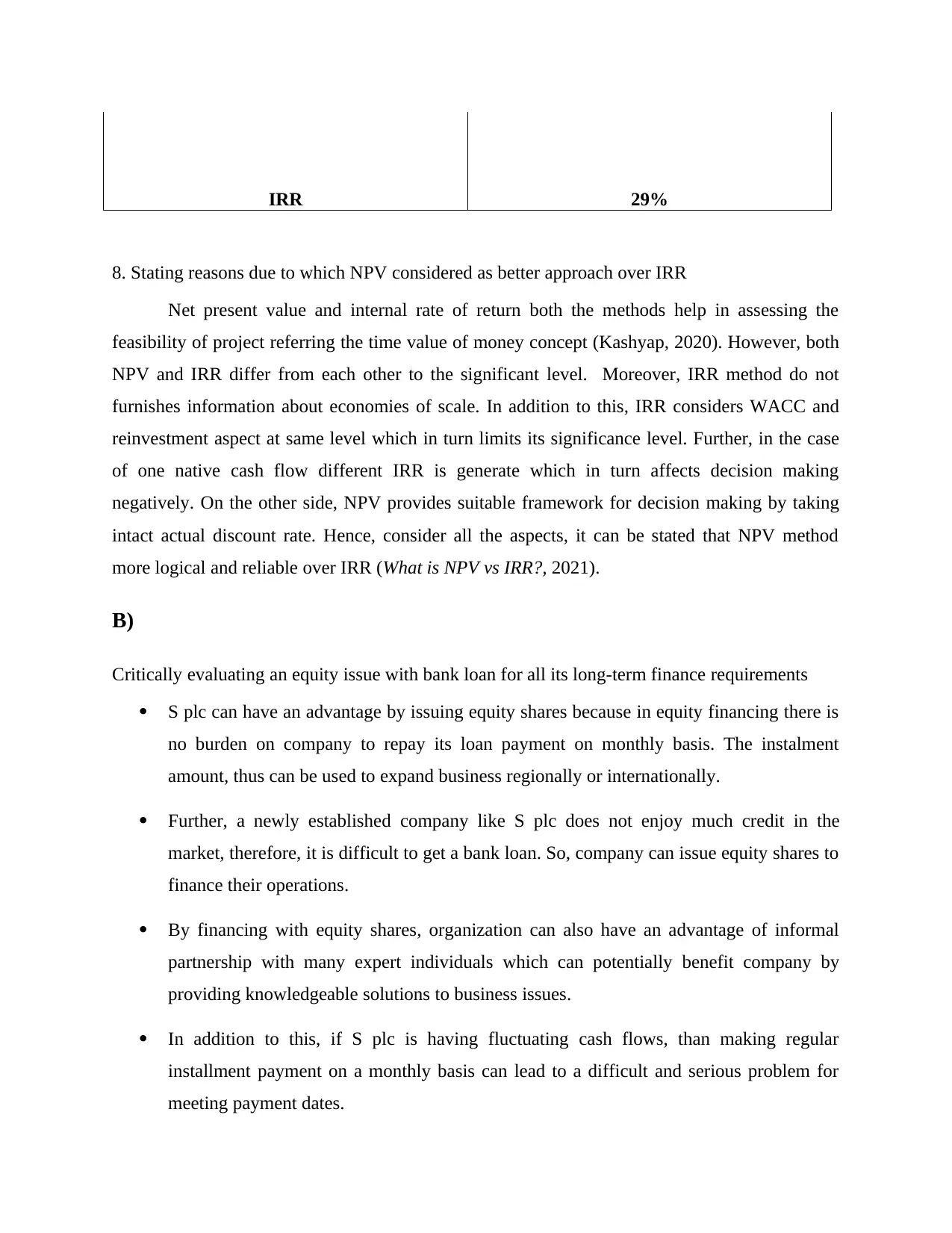

6. Assessing internal rate of return

Internal rate of return

This method is used by business unit for calculating the rate of return associated with the

concerned investment. IRR represents discounting rate where initial investment and present

value of cash flows become zero (Bierman, 2020). On the basis of this method, S Plc should

invest £1300000 in the new business opportunity. Moreover, concerned opportunity offers 29%

return which in turn considered as highly good for the organization.

Year Cash inflows

0 -1300

1 320

2 600

3 740

4 600

5 460

return in against to the initial investment made. As per overall evaluation company should go

with new line of computer game. This in turn helps it in getting the desired level of outcome or

success.

5. Describing the logic behind the net present value method and its association with cost of

capital

NPV method of investment appraisal represents difference which takes place between

present values of cash inflows and outflows. It provides high level of assistance to the manager

in taking appropriate decision about investment by analyzing profitability (Sarwary, 2020). NPV

and cost of capital is highly associated with each other. Moreover, cost capital (WACC) helps in

determining opportunity cost and thereby assists S Plc in selecting best alternative available for

investment purpose. NPV and WACC help company in assessing the whether concerned

opportunity prove to be beneficial or not (Bierman, 2020).

6. Assessing internal rate of return

Internal rate of return

This method is used by business unit for calculating the rate of return associated with the

concerned investment. IRR represents discounting rate where initial investment and present

value of cash flows become zero (Bierman, 2020). On the basis of this method, S Plc should

invest £1300000 in the new business opportunity. Moreover, concerned opportunity offers 29%

return which in turn considered as highly good for the organization.

Year Cash inflows

0 -1300

1 320

2 600

3 740

4 600

5 460

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

IRR 29%

8. Stating reasons due to which NPV considered as better approach over IRR

Net present value and internal rate of return both the methods help in assessing the

feasibility of project referring the time value of money concept (Kashyap, 2020). However, both

NPV and IRR differ from each other to the significant level. Moreover, IRR method do not

furnishes information about economies of scale. In addition to this, IRR considers WACC and

reinvestment aspect at same level which in turn limits its significance level. Further, in the case

of one native cash flow different IRR is generate which in turn affects decision making

negatively. On the other side, NPV provides suitable framework for decision making by taking

intact actual discount rate. Hence, consider all the aspects, it can be stated that NPV method

more logical and reliable over IRR (What is NPV vs IRR?, 2021).

B)

Critically evaluating an equity issue with bank loan for all its long-term finance requirements

S plc can have an advantage by issuing equity shares because in equity financing there is

no burden on company to repay its loan payment on monthly basis. The instalment

amount, thus can be used to expand business regionally or internationally.

Further, a newly established company like S plc does not enjoy much credit in the

market, therefore, it is difficult to get a bank loan. So, company can issue equity shares to

finance their operations.

By financing with equity shares, organization can also have an advantage of informal

partnership with many expert individuals which can potentially benefit company by

providing knowledgeable solutions to business issues.

In addition to this, if S plc is having fluctuating cash flows, than making regular

installment payment on a monthly basis can lead to a difficult and serious problem for

meeting payment dates.

8. Stating reasons due to which NPV considered as better approach over IRR

Net present value and internal rate of return both the methods help in assessing the

feasibility of project referring the time value of money concept (Kashyap, 2020). However, both

NPV and IRR differ from each other to the significant level. Moreover, IRR method do not

furnishes information about economies of scale. In addition to this, IRR considers WACC and

reinvestment aspect at same level which in turn limits its significance level. Further, in the case

of one native cash flow different IRR is generate which in turn affects decision making

negatively. On the other side, NPV provides suitable framework for decision making by taking

intact actual discount rate. Hence, consider all the aspects, it can be stated that NPV method

more logical and reliable over IRR (What is NPV vs IRR?, 2021).

B)

Critically evaluating an equity issue with bank loan for all its long-term finance requirements

S plc can have an advantage by issuing equity shares because in equity financing there is

no burden on company to repay its loan payment on monthly basis. The instalment

amount, thus can be used to expand business regionally or internationally.

Further, a newly established company like S plc does not enjoy much credit in the

market, therefore, it is difficult to get a bank loan. So, company can issue equity shares to

finance their operations.

By financing with equity shares, organization can also have an advantage of informal

partnership with many expert individuals which can potentially benefit company by

providing knowledgeable solutions to business issues.

In addition to this, if S plc is having fluctuating cash flows, than making regular

installment payment on a monthly basis can lead to a difficult and serious problem for

meeting payment dates.

Issuing equity shares does not involve any obligation to pay dividend on regular basis.

Company making profit can decide whether to share profits as dividends or retain it in

business for further expansion (Dowling and et.al., 2019).

On the other hand, equity financing leads to sharing of profits to each shareholder in the

form of dividend, making less profit available for company expand its business.

Therefore, bank loan does not involve any profit sharing and is a better option.

Shareholders are involved in decision making process which leads to share of control in

company, thus involving too many people in decision making. Taking a loan from bank

does not result in share of control.

Different people have different opinions and style of managing and running a business, S

plc has to consider all such opinions in case of equity financing which can lead to

conflicts and arguments. Financing business operations does not necessitate such things,

thus, S plc can opt for bank loan.

Bank loan is easier to get which requires minimum formalities whereas equity financing

involves too many requirements such as issue of prospectus and so on, and is time

consuming and complicated process.

Moreover, the interest paid on loan is a tax deductible item, on the other hand, dividend

payment is not. So, bank loan is more favorable than equity issue. In addition to this, the

interest and principal amount is already known in advance to S plc. So, it is easier for it to

examine working capital requirements (Allen, Qian and Xie, 2019).

Expanding business with the help of bank loan is much easier because it does not involve

participation of public in business related matters and decision making process. In equity

financing, shareholders are needed to be consulted before taking major decisions,

therefore, bank loan is much easy and simple to proceed with.

C)

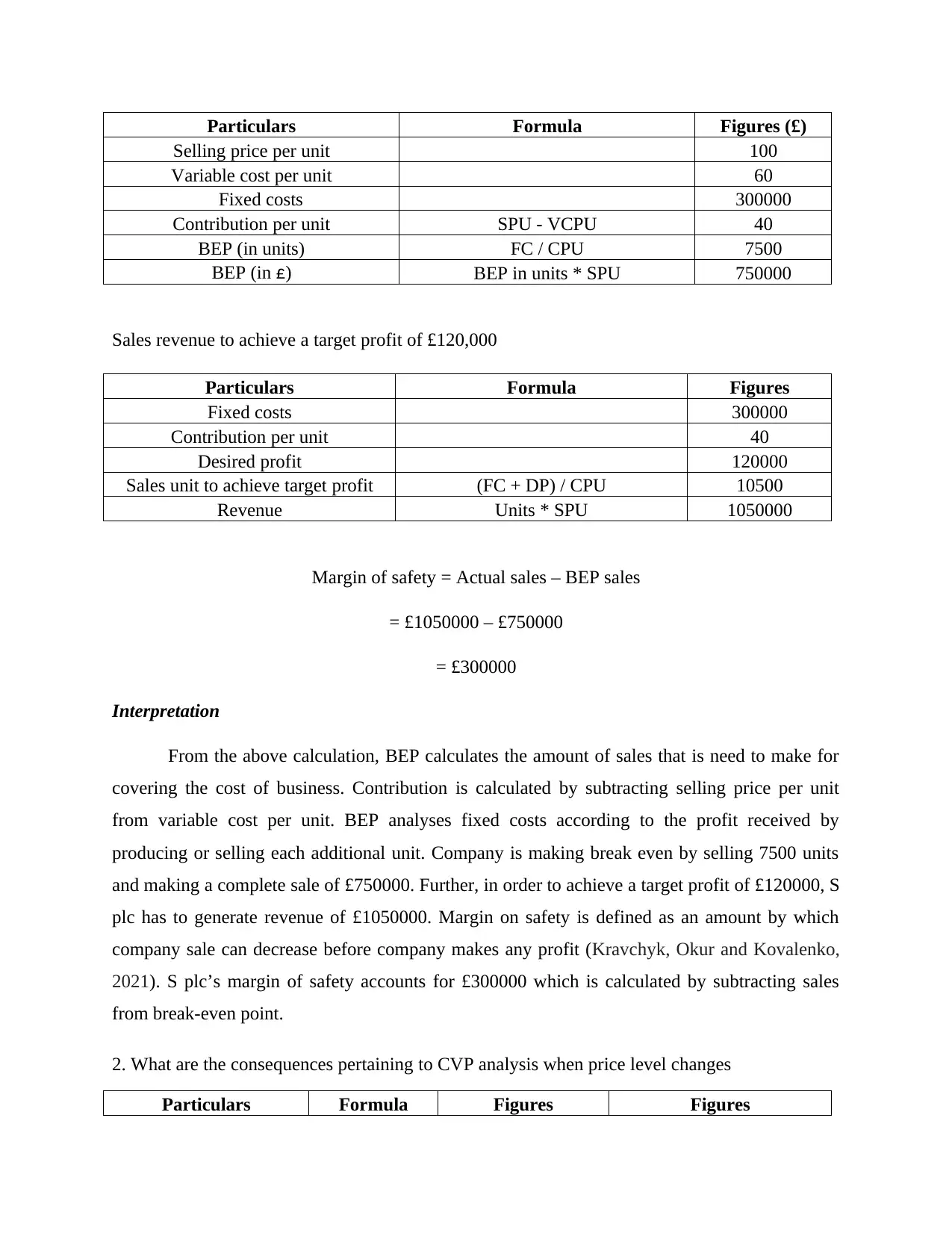

1. Presenting CVP analysis referring given scenario

BEP sales revenue

Company making profit can decide whether to share profits as dividends or retain it in

business for further expansion (Dowling and et.al., 2019).

On the other hand, equity financing leads to sharing of profits to each shareholder in the

form of dividend, making less profit available for company expand its business.

Therefore, bank loan does not involve any profit sharing and is a better option.

Shareholders are involved in decision making process which leads to share of control in

company, thus involving too many people in decision making. Taking a loan from bank

does not result in share of control.

Different people have different opinions and style of managing and running a business, S

plc has to consider all such opinions in case of equity financing which can lead to

conflicts and arguments. Financing business operations does not necessitate such things,

thus, S plc can opt for bank loan.

Bank loan is easier to get which requires minimum formalities whereas equity financing

involves too many requirements such as issue of prospectus and so on, and is time

consuming and complicated process.

Moreover, the interest paid on loan is a tax deductible item, on the other hand, dividend

payment is not. So, bank loan is more favorable than equity issue. In addition to this, the

interest and principal amount is already known in advance to S plc. So, it is easier for it to

examine working capital requirements (Allen, Qian and Xie, 2019).

Expanding business with the help of bank loan is much easier because it does not involve

participation of public in business related matters and decision making process. In equity

financing, shareholders are needed to be consulted before taking major decisions,

therefore, bank loan is much easy and simple to proceed with.

C)

1. Presenting CVP analysis referring given scenario

BEP sales revenue

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Particulars Formula Figures (£)

Selling price per unit 100

Variable cost per unit 60

Fixed costs 300000

Contribution per unit SPU - VCPU 40

BEP (in units) FC / CPU 7500

BEP (in £) BEP in units * SPU 750000

Sales revenue to achieve a target profit of £120,000

Particulars Formula Figures

Fixed costs 300000

Contribution per unit 40

Desired profit 120000

Sales unit to achieve target profit (FC + DP) / CPU 10500

Revenue Units * SPU 1050000

Margin of safety = Actual sales – BEP sales

= £1050000 – £750000

= £300000

Interpretation

From the above calculation, BEP calculates the amount of sales that is need to make for

covering the cost of business. Contribution is calculated by subtracting selling price per unit

from variable cost per unit. BEP analyses fixed costs according to the profit received by

producing or selling each additional unit. Company is making break even by selling 7500 units

and making a complete sale of £750000. Further, in order to achieve a target profit of £120000, S

plc has to generate revenue of £1050000. Margin on safety is defined as an amount by which

company sale can decrease before company makes any profit (Kravchyk, Okur and Kovalenko,

2021). S plc’s margin of safety accounts for £300000 which is calculated by subtracting sales

from break-even point.

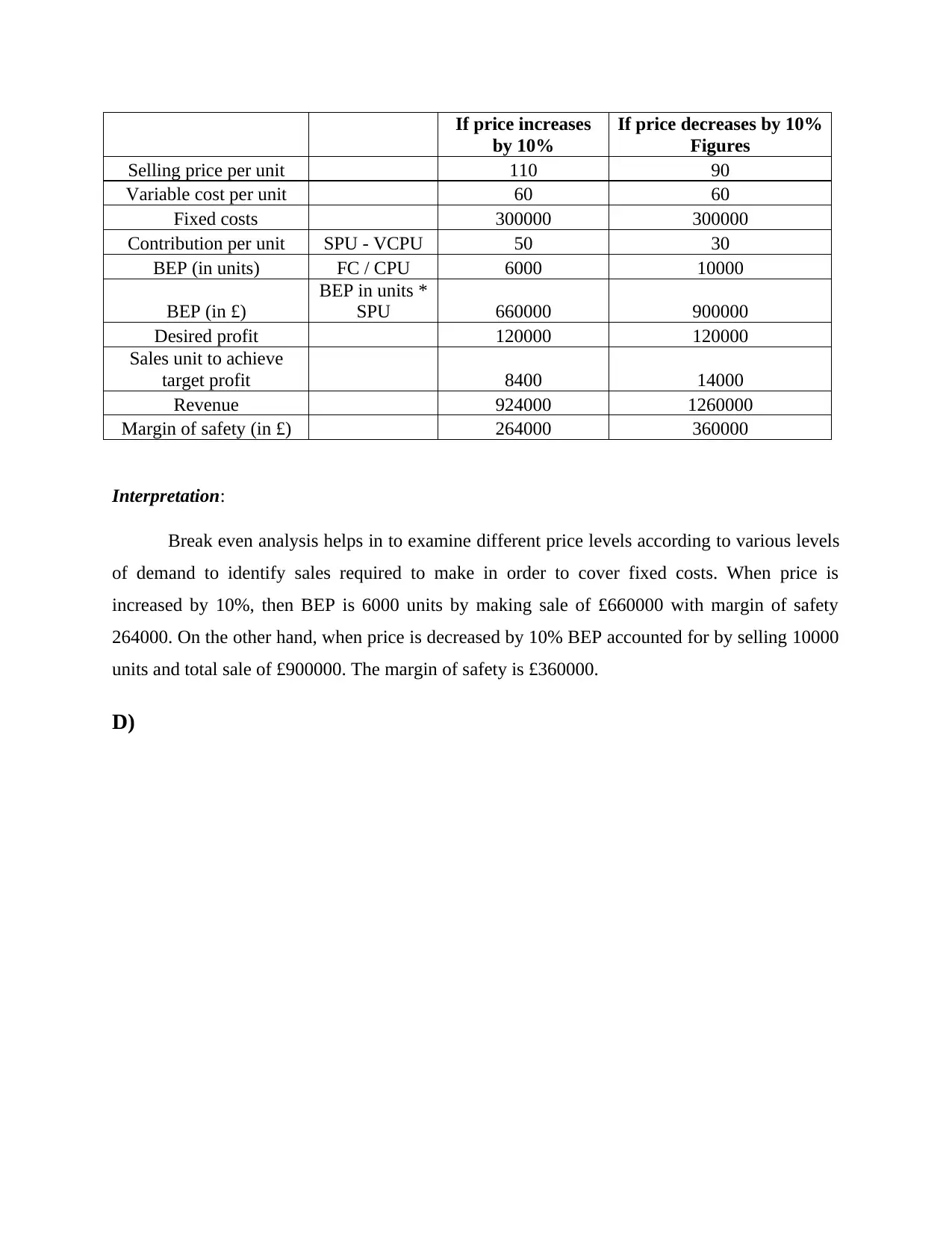

2. What are the consequences pertaining to CVP analysis when price level changes

Particulars Formula Figures Figures

Selling price per unit 100

Variable cost per unit 60

Fixed costs 300000

Contribution per unit SPU - VCPU 40

BEP (in units) FC / CPU 7500

BEP (in £) BEP in units * SPU 750000

Sales revenue to achieve a target profit of £120,000

Particulars Formula Figures

Fixed costs 300000

Contribution per unit 40

Desired profit 120000

Sales unit to achieve target profit (FC + DP) / CPU 10500

Revenue Units * SPU 1050000

Margin of safety = Actual sales – BEP sales

= £1050000 – £750000

= £300000

Interpretation

From the above calculation, BEP calculates the amount of sales that is need to make for

covering the cost of business. Contribution is calculated by subtracting selling price per unit

from variable cost per unit. BEP analyses fixed costs according to the profit received by

producing or selling each additional unit. Company is making break even by selling 7500 units

and making a complete sale of £750000. Further, in order to achieve a target profit of £120000, S

plc has to generate revenue of £1050000. Margin on safety is defined as an amount by which

company sale can decrease before company makes any profit (Kravchyk, Okur and Kovalenko,

2021). S plc’s margin of safety accounts for £300000 which is calculated by subtracting sales

from break-even point.

2. What are the consequences pertaining to CVP analysis when price level changes

Particulars Formula Figures Figures

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

If price increases

by 10%

If price decreases by 10%

Figures

Selling price per unit 110 90

Variable cost per unit 60 60

Fixed costs 300000 300000

Contribution per unit SPU - VCPU 50 30

BEP (in units) FC / CPU 6000 10000

BEP (in £)

BEP in units *

SPU 660000 900000

Desired profit 120000 120000

Sales unit to achieve

target profit 8400 14000

Revenue 924000 1260000

Margin of safety (in £) 264000 360000

Interpretation:

Break even analysis helps in to examine different price levels according to various levels

of demand to identify sales required to make in order to cover fixed costs. When price is

increased by 10%, then BEP is 6000 units by making sale of £660000 with margin of safety

264000. On the other hand, when price is decreased by 10% BEP accounted for by selling 10000

units and total sale of £900000. The margin of safety is £360000.

D)

by 10%

If price decreases by 10%

Figures

Selling price per unit 110 90

Variable cost per unit 60 60

Fixed costs 300000 300000

Contribution per unit SPU - VCPU 50 30

BEP (in units) FC / CPU 6000 10000

BEP (in £)

BEP in units *

SPU 660000 900000

Desired profit 120000 120000

Sales unit to achieve

target profit 8400 14000

Revenue 924000 1260000

Margin of safety (in £) 264000 360000

Interpretation:

Break even analysis helps in to examine different price levels according to various levels

of demand to identify sales required to make in order to cover fixed costs. When price is

increased by 10%, then BEP is 6000 units by making sale of £660000 with margin of safety

264000. On the other hand, when price is decreased by 10% BEP accounted for by selling 10000

units and total sale of £900000. The margin of safety is £360000.

D)

1) Distinguishing the categories of suppliers

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.