Financial Analysis: Investment Appraisal, WACC - NCC Group Report

VerifiedAdded on 2023/06/10

|19

|4073

|281

Report

AI Summary

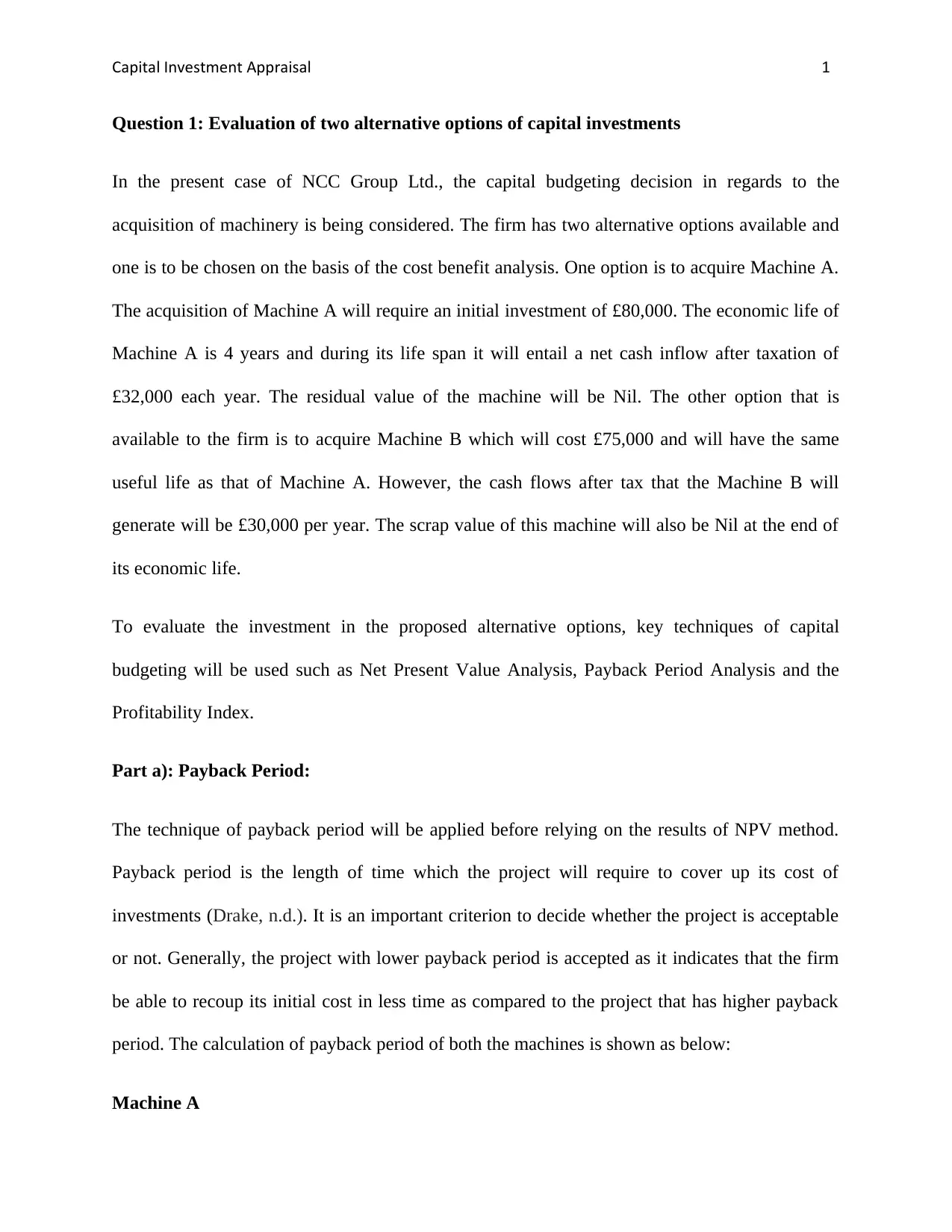

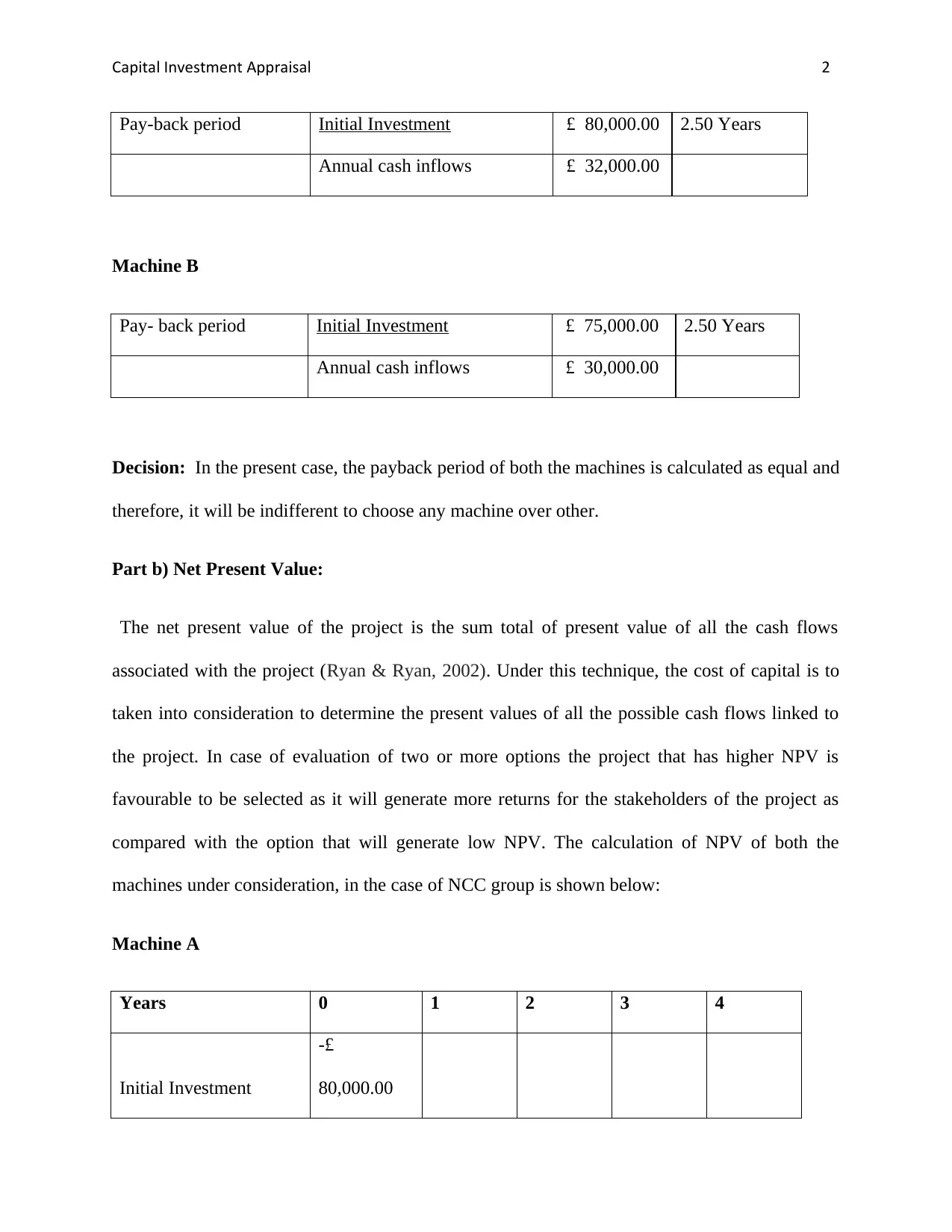

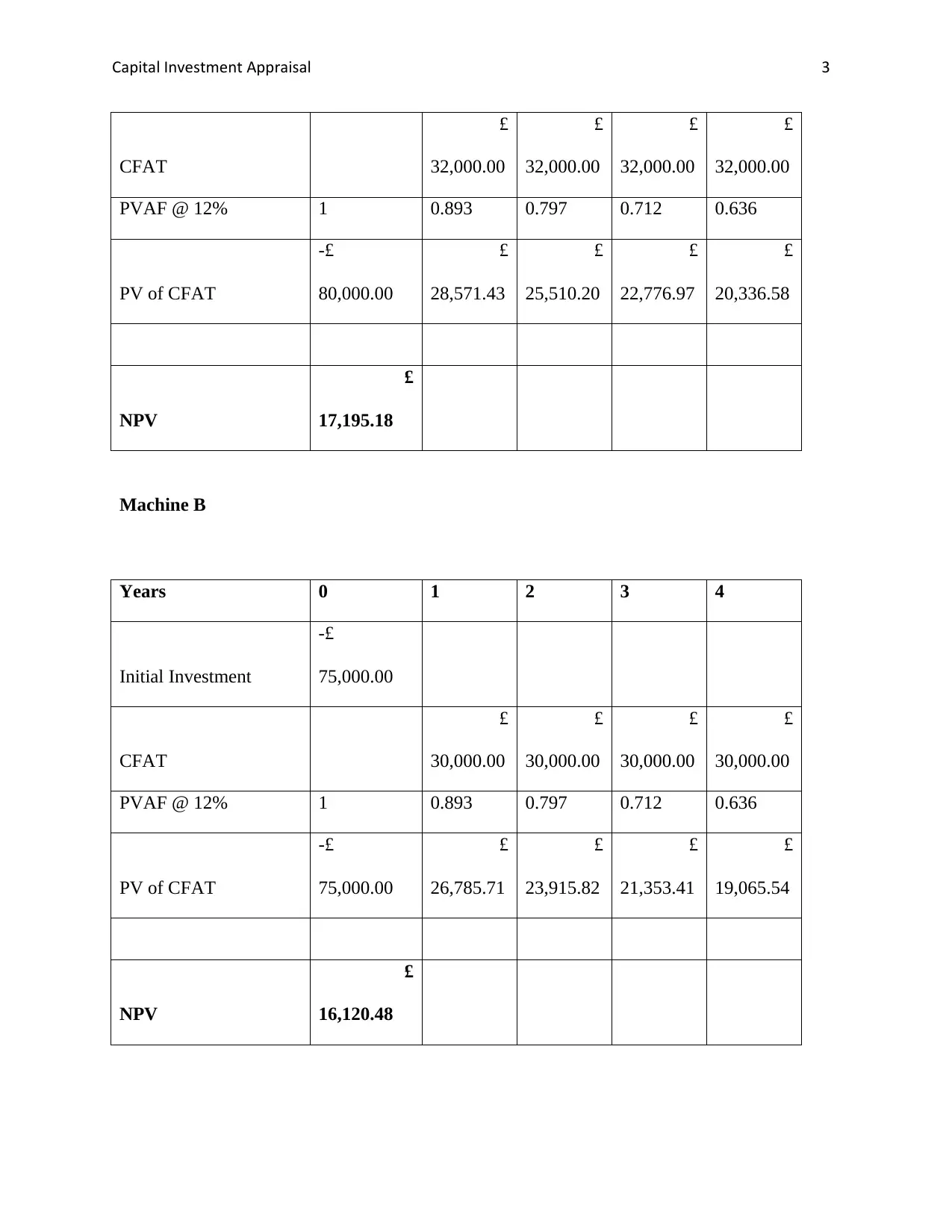

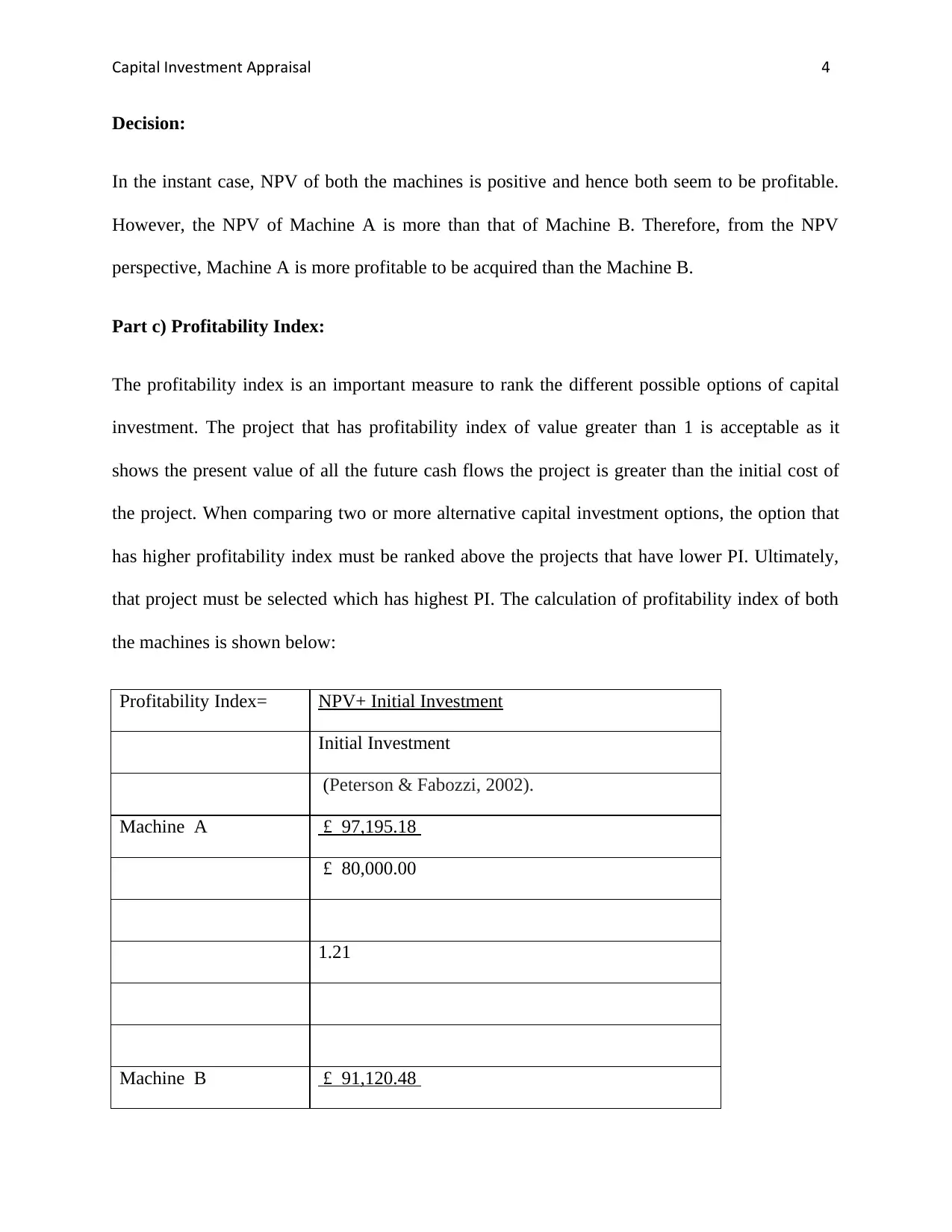

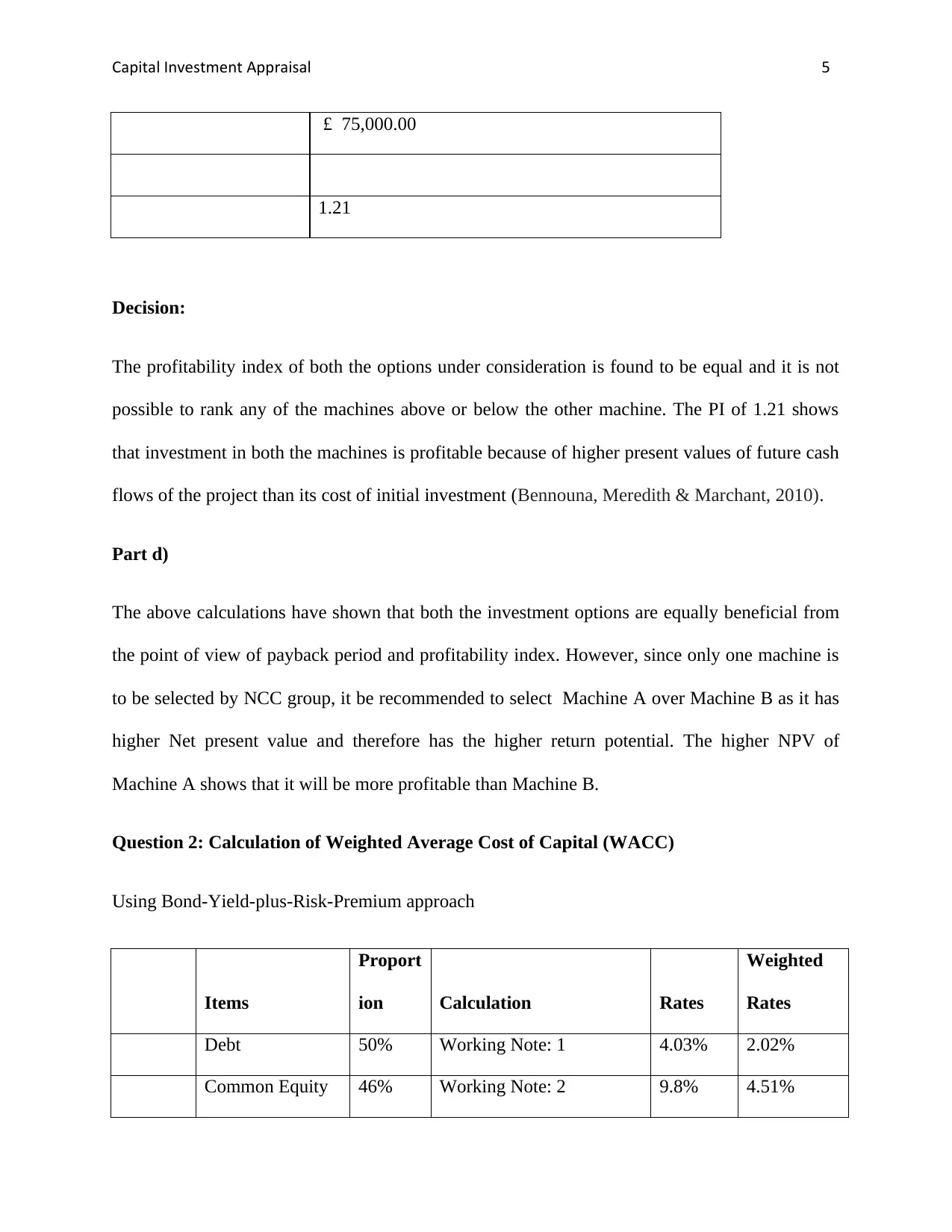

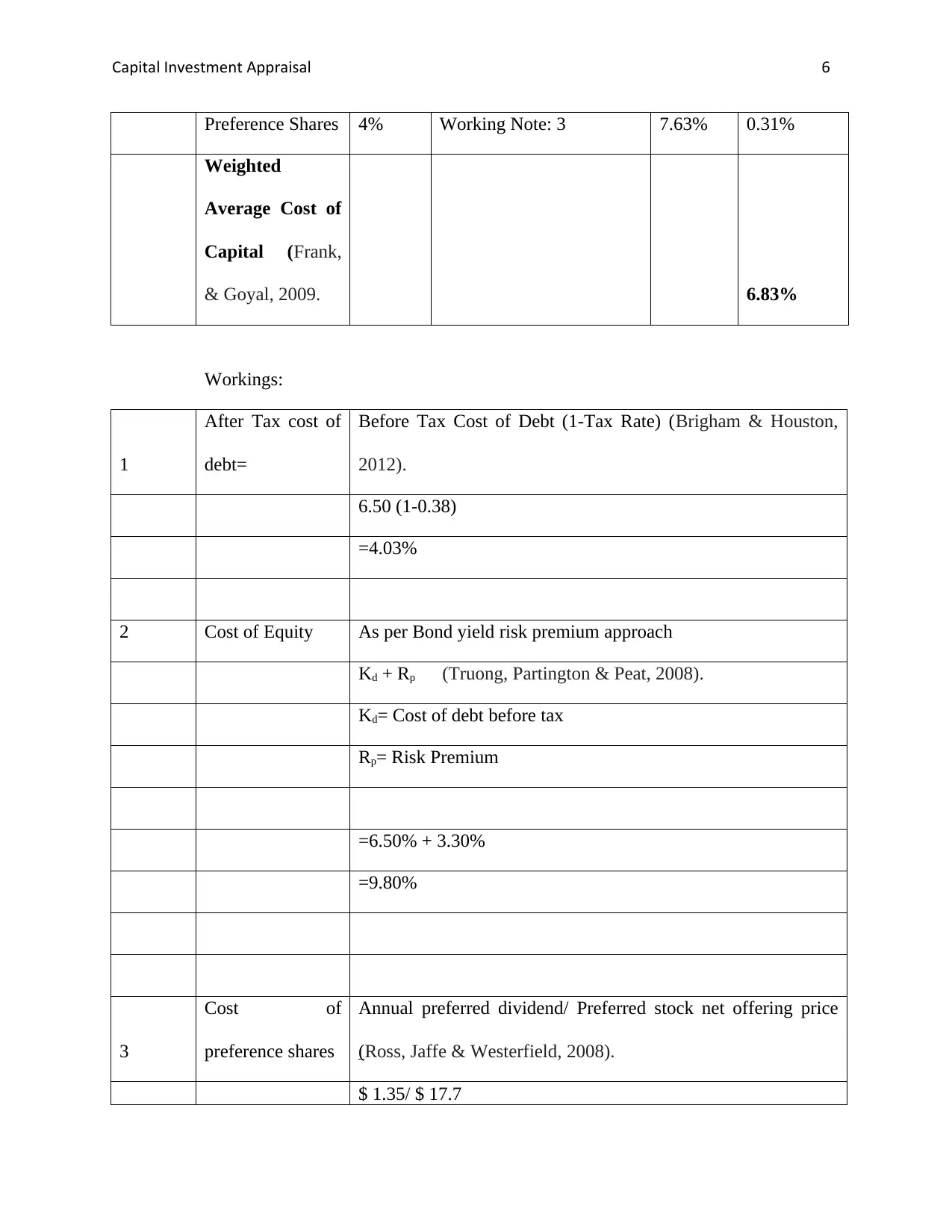

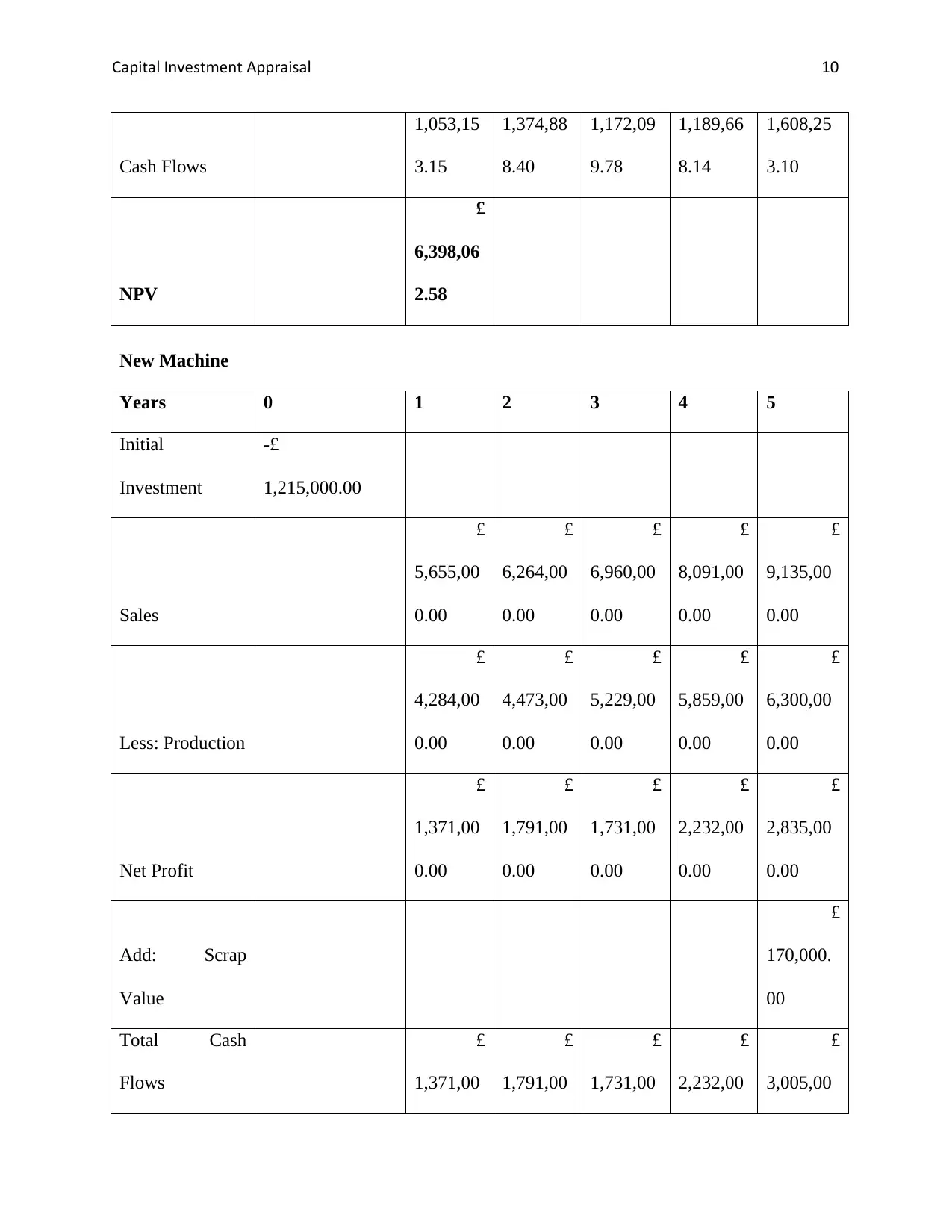

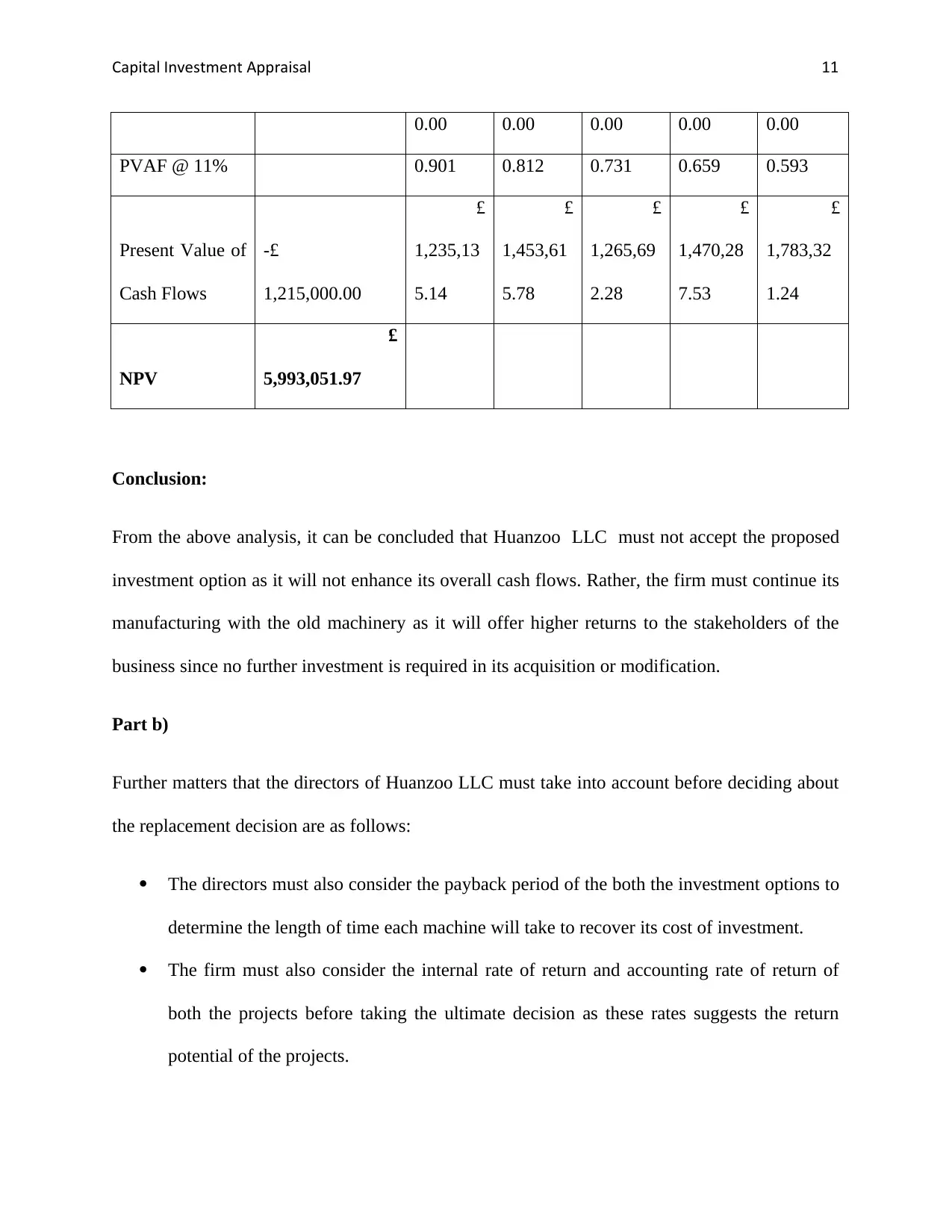

This assignment provides a comprehensive analysis of capital investment appraisal techniques, focusing on machine selection and weighted average cost of capital (WACC) calculations. It begins with an evaluation of two alternative machine options for NCC Group Ltd., utilizing payback period, net present value (NPV), and profitability index (PI) methods to determine the most profitable investment. Despite conflicting results from different methods, the report recommends Machine A based on its higher NPV. The assignment then calculates the WACC for Jemz Corporation using the bond-yield-plus-risk-premium approach, considering debt, common equity, and preferred shares. Finally, it assesses a replacement decision for Huanzoo LLC plc, comparing the NPV of existing and new machinery, ultimately advising against the replacement due to the existing machine's higher NPV. The report also highlights additional factors for Huanzoo LLC's directors to consider before making a final decision. Desklib offers a wealth of similar solved assignments and resources for students.

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.