Management Accounting Report for Capital Joinery Ltd: Analysis

VerifiedAdded on 2023/01/03

|15

|3970

|134

Report

AI Summary

This report provides a comprehensive analysis of management accounting practices at Capital Joinery Ltd. It begins with an introduction to managerial accounting, highlighting its importance in financial decision-making, and then introduces Capital Joinery Ltd, a carpentry firm. The report examines different types of management accounting systems (MAS), including cost accounting, stock management, job costing, and price optimization systems. It then delves into various MAS reporting methods, such as accounts receivable, budget, inventory management, and performance reports. The report further explores costing methods, comparing absorption and marginal costing through income statements and reconciliation statements. Additionally, it examines budgetary control through sales, cash, and zero-based budgets. The report concludes by discussing how MAS can be used to resolve financial problems, offering valuable insights into the application of management accounting principles in a real-world business context.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

Task 1...............................................................................................................................................3

P1 Different types of MAS..........................................................................................................3

P2. Various MA reporting...........................................................................................................4

Task 2...............................................................................................................................................5

P3. Costing method to generate income statement......................................................................5

Task 3...............................................................................................................................................9

P4. Planning tool for budgetary control.......................................................................................9

Task 4.............................................................................................................................................11

P5. MAS used to resolve the financial problems.......................................................................11

Conclusion.....................................................................................................................................13

References......................................................................................................................................15

INTRODUCTION...........................................................................................................................3

Task 1...............................................................................................................................................3

P1 Different types of MAS..........................................................................................................3

P2. Various MA reporting...........................................................................................................4

Task 2...............................................................................................................................................5

P3. Costing method to generate income statement......................................................................5

Task 3...............................................................................................................................................9

P4. Planning tool for budgetary control.......................................................................................9

Task 4.............................................................................................................................................11

P5. MAS used to resolve the financial problems.......................................................................11

Conclusion.....................................................................................................................................13

References......................................................................................................................................15

INTRODUCTION

Managerial accounting is a philosophy that describes a framework for reporting economic

statistical analyses and reasoning routinely to promote vital financial decision also for individual

role (Cooper, Ezzamel and Qu, 2017). To clarify a need for more help, the importance of

financial reporting has been identified. Capital Joinery Ltd., the firm that is selected for the task,

produces a wide variety of carpentry, helps make doors, windows, etc. The research identified

the importance of the MAS and the introduction of interventions to predict or calculate benefits

prices including for this assessment the requirements for the estimating system for a given

perspective and the planning by budget management of testing process as well as other reporting

strategies for coping with the financial problem.

Task 1

P1 Different types of MAS

MA is really a synthesis of two principles that define managing also as mechanism for co-

ordinating, coordinating, controlling and supervising company operations. In another side,

accounting is viewed as a systemic means of handling data to obtain and report accounting

information. MA is a standardised term used to periodically display accounting documents for

international corporations' purposes (Malmi, 2016). This seeks to address the cost inflation issue,

non-specific reporting, the recognition of the correct solution, appraisal as well as the best use of

programs as well as the reporting field. Cost monitoring, frequently emphasised as an integral

aspect of reporting, is necessary only for financial relationships.

Costs accounting system: To assess the costs generated by the execution of corporate

operations, benefit is a multinational accounting management technology for selling products.

The manager uses various approaches to measure costs: marginal, accumulative, contingent and

normal costing. In the measurement of benefits and evaluation of the effects of per offers

profitable improvements, Capital Joinery Ltd employs minimal and perhaps even normal costing

approaches. Throughout the context of restricted capital loans, this accounting approach can

indeed be generalised and relevant for them. The essential requirement of this system is to

control the cost which is involved in different operations and manage in a way that it will never

impact the profit making of company. Manager can make use of absorption and marginal costing

methods to determine the net profit and control the cost in effective manner. It is such that with

Managerial accounting is a philosophy that describes a framework for reporting economic

statistical analyses and reasoning routinely to promote vital financial decision also for individual

role (Cooper, Ezzamel and Qu, 2017). To clarify a need for more help, the importance of

financial reporting has been identified. Capital Joinery Ltd., the firm that is selected for the task,

produces a wide variety of carpentry, helps make doors, windows, etc. The research identified

the importance of the MAS and the introduction of interventions to predict or calculate benefits

prices including for this assessment the requirements for the estimating system for a given

perspective and the planning by budget management of testing process as well as other reporting

strategies for coping with the financial problem.

Task 1

P1 Different types of MAS

MA is really a synthesis of two principles that define managing also as mechanism for co-

ordinating, coordinating, controlling and supervising company operations. In another side,

accounting is viewed as a systemic means of handling data to obtain and report accounting

information. MA is a standardised term used to periodically display accounting documents for

international corporations' purposes (Malmi, 2016). This seeks to address the cost inflation issue,

non-specific reporting, the recognition of the correct solution, appraisal as well as the best use of

programs as well as the reporting field. Cost monitoring, frequently emphasised as an integral

aspect of reporting, is necessary only for financial relationships.

Costs accounting system: To assess the costs generated by the execution of corporate

operations, benefit is a multinational accounting management technology for selling products.

The manager uses various approaches to measure costs: marginal, accumulative, contingent and

normal costing. In the measurement of benefits and evaluation of the effects of per offers

profitable improvements, Capital Joinery Ltd employs minimal and perhaps even normal costing

approaches. Throughout the context of restricted capital loans, this accounting approach can

indeed be generalised and relevant for them. The essential requirement of this system is to

control the cost which is involved in different operations and manage in a way that it will never

impact the profit making of company. Manager can make use of absorption and marginal costing

methods to determine the net profit and control the cost in effective manner. It is such that with

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

this approach they can classify the expense of replacing doors, etc. The quality of raw, labour

costs and even else can be classified. Through that they could appreciate the effect of consuming

higher prices.

Stock management scheme: Indeed, stock identification is a critical product for the enterprise

market, it leads to anticipated abuse of gains and lowers the expense of managing these stocks.

By using MASs such as EOQ, JIT, businesses are able to control the stock ratio and to create the

optimal storage for processing (Otley, 2016). In Capital Joinery, LIFO uses FIFO's technique to

measure the sale stock level. They would be told of the categories of goods stored in factories as

well as the kinds of items to be produced to satisfy consumption needs. The essential

requirement of this system is to handle stock level of company and make sure that supply and

demand cycle be on track. The standard, median and secure inventory structure is also useful for

calculating. Its need for increased manufactured goods to create more furnishings can be

assessed in terms of this accounting rules the above company.

Job costs method: This MAS method is typically further used define the profit margin for

products processed with ore. This truly reflects the consumer's order specifications, the file, the

number of orders issued, costs, the schedule required to deliver the products. The main

requirement of this system is to make sure that each and every job of company is making a

profitable contribution in making company more successful. The relevant preferred corporation

uses this approach to measure demand for the market. This accountability is useful for service

capital firms above for tracking the operating expenses used during the production of windows

and certain other light fittings throughout a duration or system revenue.

Price Optimization System: This framework is implemented in the business; management will

be required to choose for their goods the right price plan. The value of a specific well quality is

often calculated by values skimming, penetrating and discounting. The marketing strategy, which

successfully assesses cost advantage as well as achieves a fair price advantage, covers the

business strategic nature with the company's operational policies. In order to manage its

customer base, Capital Joinery Ltd does it. Therefore, the value of every other good is calculated

according to the goal requirement. Customers are split into discreet, loyal, forward-looking,

positive customer imperial measurements. They main essential of propagation pricing techniques

only when they change into separate target driven by growing products as well as other products.

costs and even else can be classified. Through that they could appreciate the effect of consuming

higher prices.

Stock management scheme: Indeed, stock identification is a critical product for the enterprise

market, it leads to anticipated abuse of gains and lowers the expense of managing these stocks.

By using MASs such as EOQ, JIT, businesses are able to control the stock ratio and to create the

optimal storage for processing (Otley, 2016). In Capital Joinery, LIFO uses FIFO's technique to

measure the sale stock level. They would be told of the categories of goods stored in factories as

well as the kinds of items to be produced to satisfy consumption needs. The essential

requirement of this system is to handle stock level of company and make sure that supply and

demand cycle be on track. The standard, median and secure inventory structure is also useful for

calculating. Its need for increased manufactured goods to create more furnishings can be

assessed in terms of this accounting rules the above company.

Job costs method: This MAS method is typically further used define the profit margin for

products processed with ore. This truly reflects the consumer's order specifications, the file, the

number of orders issued, costs, the schedule required to deliver the products. The main

requirement of this system is to make sure that each and every job of company is making a

profitable contribution in making company more successful. The relevant preferred corporation

uses this approach to measure demand for the market. This accountability is useful for service

capital firms above for tracking the operating expenses used during the production of windows

and certain other light fittings throughout a duration or system revenue.

Price Optimization System: This framework is implemented in the business; management will

be required to choose for their goods the right price plan. The value of a specific well quality is

often calculated by values skimming, penetrating and discounting. The marketing strategy, which

successfully assesses cost advantage as well as achieves a fair price advantage, covers the

business strategic nature with the company's operational policies. In order to manage its

customer base, Capital Joinery Ltd does it. Therefore, the value of every other good is calculated

according to the goal requirement. Customers are split into discreet, loyal, forward-looking,

positive customer imperial measurements. They main essential of propagation pricing techniques

only when they change into separate target driven by growing products as well as other products.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

They set costs in order with demand and consumer requirement in the abovementioned context

for their different kinds of furnishings parts.

P2. Various MA reporting

Managerial accounting partnerships are vital aspects of financial management practises, wherein

administrators take deliberate action. In addition to these documents, corporations' monetary and

non-activity is produced by help (Hopper and Bui, 2016). Including Capital Joinery Ltd, they

compilation different types of paper described following table:

Account receivables report: The Accounts payable database is a major document but was

recognised to have been one of greatest subjective systems and data unless the creditors' reports

are anticipated to collect. In this study, consolidation bond holders were established who

transformed the weak credit resources of the group.

Budget report: It really is intended to create a framework for budgetary growth. Management

teams have collected this analysis by collection of data from all documentation produced. The

income accounts provide information on the success of the firm and its plans. In order to define

potential development prospects, the management team of Capital Journey Ltd was using the

Budget paper.

Inventory management report: This document is focused on inventory tracking data obtained.

The important segment for this learners make to evaluate the overall inventory output needed,

the operational costs as well as the assessment of potential inventory availability.

Performance report: This document discusses the most significant feature of the product

needed by each organisation. Information on the results of each business are also beneficial.

Managers also draw up incentive strategy to take decisions on corporate incentives mostly on

study will be based of this document in the light of success recognition and assessment. Capital

Journey Ltd is indeed a global company with over 500 workers. The Progress Report was based

for the managing director on one that monitors the degree of success across each segment of staff

and establishes policies.

Task 2

P3. Costing method to generate income statement

Absorption costing: It really is a tool for estimating the profit margin wherein operating costs as

well as varying costs are considered (van Helden and Uddin, 2016).

for their different kinds of furnishings parts.

P2. Various MA reporting

Managerial accounting partnerships are vital aspects of financial management practises, wherein

administrators take deliberate action. In addition to these documents, corporations' monetary and

non-activity is produced by help (Hopper and Bui, 2016). Including Capital Joinery Ltd, they

compilation different types of paper described following table:

Account receivables report: The Accounts payable database is a major document but was

recognised to have been one of greatest subjective systems and data unless the creditors' reports

are anticipated to collect. In this study, consolidation bond holders were established who

transformed the weak credit resources of the group.

Budget report: It really is intended to create a framework for budgetary growth. Management

teams have collected this analysis by collection of data from all documentation produced. The

income accounts provide information on the success of the firm and its plans. In order to define

potential development prospects, the management team of Capital Journey Ltd was using the

Budget paper.

Inventory management report: This document is focused on inventory tracking data obtained.

The important segment for this learners make to evaluate the overall inventory output needed,

the operational costs as well as the assessment of potential inventory availability.

Performance report: This document discusses the most significant feature of the product

needed by each organisation. Information on the results of each business are also beneficial.

Managers also draw up incentive strategy to take decisions on corporate incentives mostly on

study will be based of this document in the light of success recognition and assessment. Capital

Journey Ltd is indeed a global company with over 500 workers. The Progress Report was based

for the managing director on one that monitors the degree of success across each segment of staff

and establishes policies.

Task 2

P3. Costing method to generate income statement

Absorption costing: It really is a tool for estimating the profit margin wherein operating costs as

well as varying costs are considered (van Helden and Uddin, 2016).

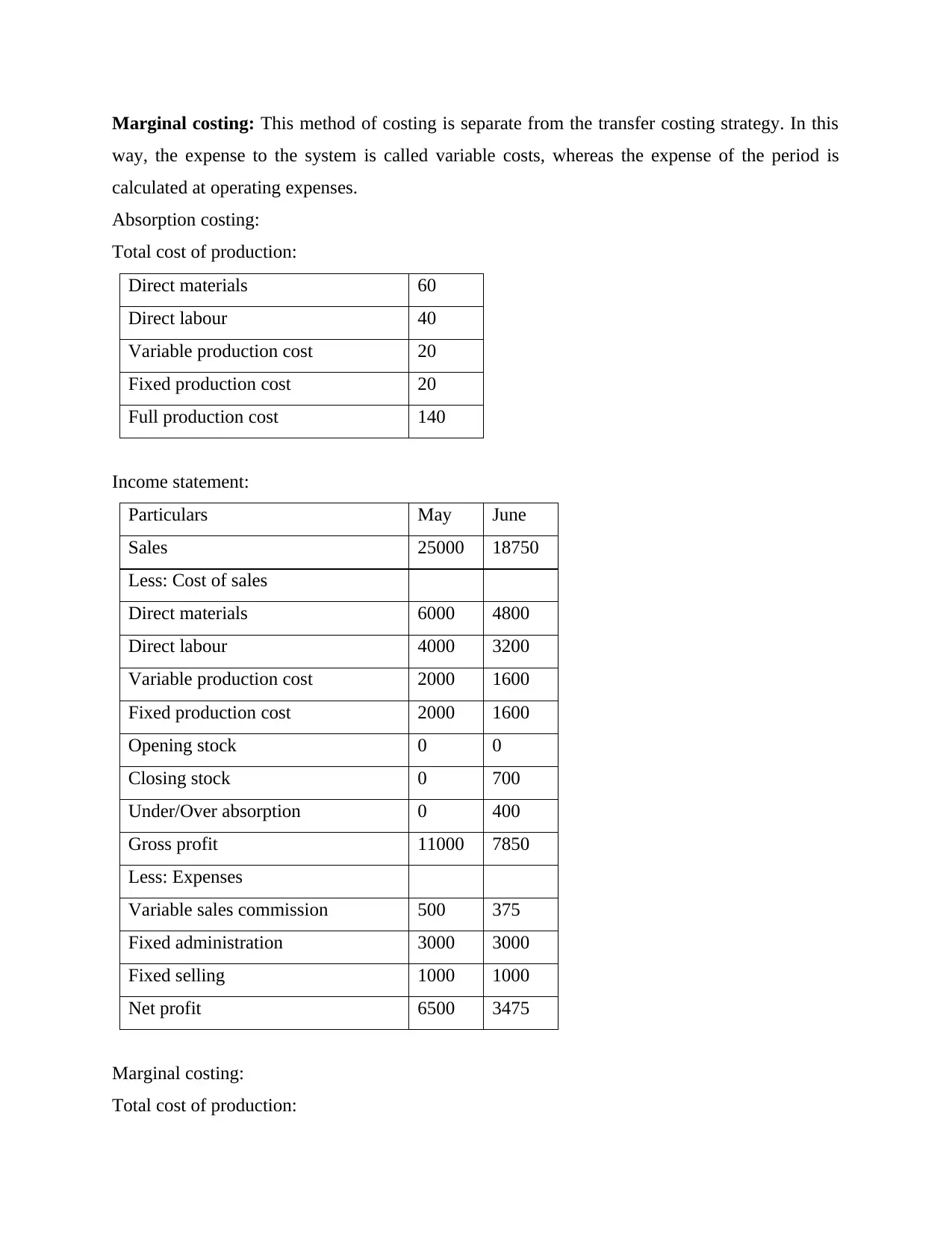

Marginal costing: This method of costing is separate from the transfer costing strategy. In this

way, the expense to the system is called variable costs, whereas the expense of the period is

calculated at operating expenses.

Absorption costing:

Total cost of production:

Direct materials 60

Direct labour 40

Variable production cost 20

Fixed production cost 20

Full production cost 140

Income statement:

Particulars May June

Sales 25000 18750

Less: Cost of sales

Direct materials 6000 4800

Direct labour 4000 3200

Variable production cost 2000 1600

Fixed production cost 2000 1600

Opening stock 0 0

Closing stock 0 700

Under/Over absorption 0 400

Gross profit 11000 7850

Less: Expenses

Variable sales commission 500 375

Fixed administration 3000 3000

Fixed selling 1000 1000

Net profit 6500 3475

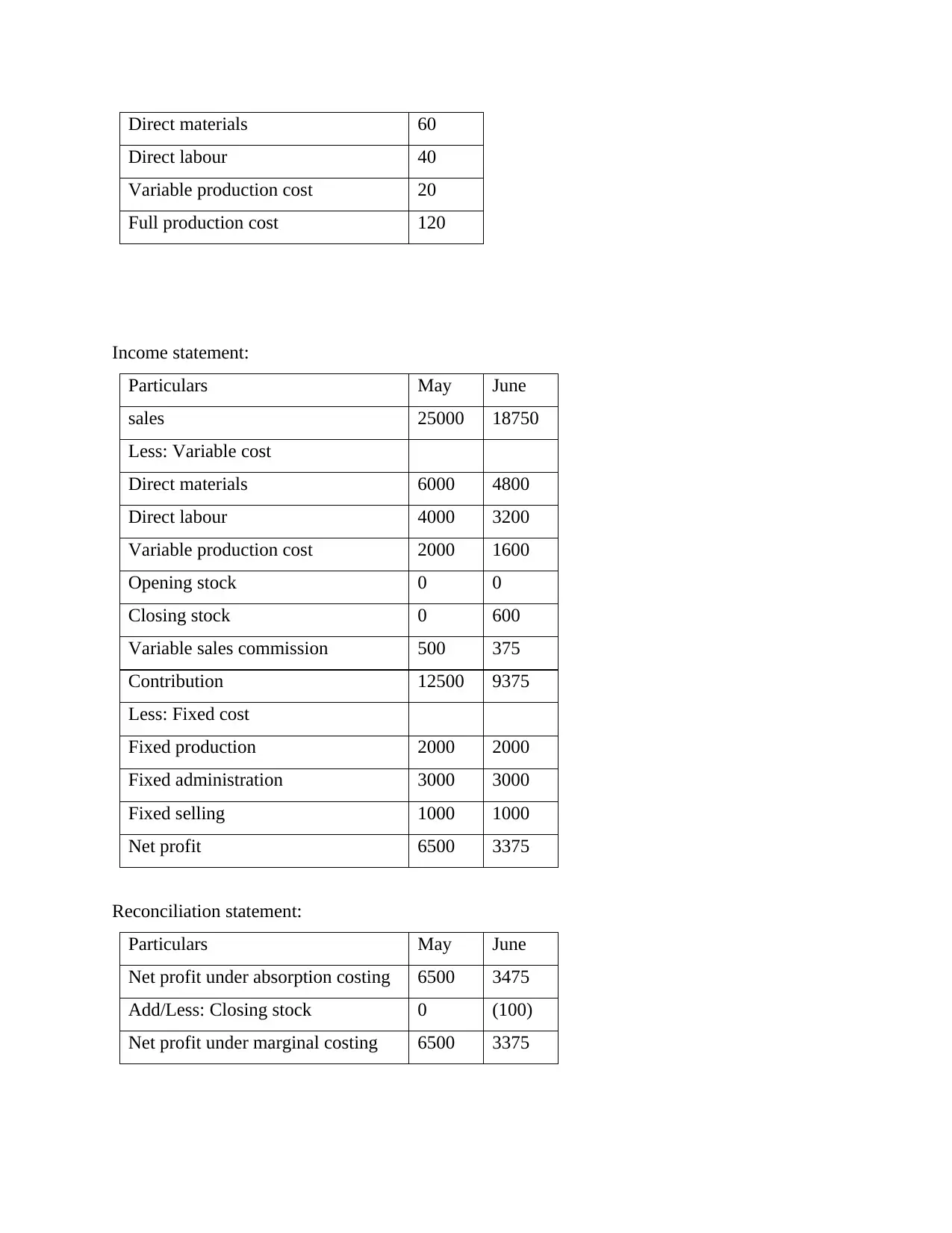

Marginal costing:

Total cost of production:

way, the expense to the system is called variable costs, whereas the expense of the period is

calculated at operating expenses.

Absorption costing:

Total cost of production:

Direct materials 60

Direct labour 40

Variable production cost 20

Fixed production cost 20

Full production cost 140

Income statement:

Particulars May June

Sales 25000 18750

Less: Cost of sales

Direct materials 6000 4800

Direct labour 4000 3200

Variable production cost 2000 1600

Fixed production cost 2000 1600

Opening stock 0 0

Closing stock 0 700

Under/Over absorption 0 400

Gross profit 11000 7850

Less: Expenses

Variable sales commission 500 375

Fixed administration 3000 3000

Fixed selling 1000 1000

Net profit 6500 3475

Marginal costing:

Total cost of production:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Direct materials 60

Direct labour 40

Variable production cost 20

Full production cost 120

Income statement:

Particulars May June

sales 25000 18750

Less: Variable cost

Direct materials 6000 4800

Direct labour 4000 3200

Variable production cost 2000 1600

Opening stock 0 0

Closing stock 0 600

Variable sales commission 500 375

Contribution 12500 9375

Less: Fixed cost

Fixed production 2000 2000

Fixed administration 3000 3000

Fixed selling 1000 1000

Net profit 6500 3375

Reconciliation statement:

Particulars May June

Net profit under absorption costing 6500 3475

Add/Less: Closing stock 0 (100)

Net profit under marginal costing 6500 3375

Direct labour 40

Variable production cost 20

Full production cost 120

Income statement:

Particulars May June

sales 25000 18750

Less: Variable cost

Direct materials 6000 4800

Direct labour 4000 3200

Variable production cost 2000 1600

Opening stock 0 0

Closing stock 0 600

Variable sales commission 500 375

Contribution 12500 9375

Less: Fixed cost

Fixed production 2000 2000

Fixed administration 3000 3000

Fixed selling 1000 1000

Net profit 6500 3375

Reconciliation statement:

Particulars May June

Net profit under absorption costing 6500 3475

Add/Less: Closing stock 0 (100)

Net profit under marginal costing 6500 3375

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Calculation of material

variances

Budgeted Actual Variances

Materials cost per unit £24 £18.67 £5.33

Inventory ledger record LIFO Method

Dat

e Description Sale/Purchases Balance

Unit

s

Cos

t Total

Unit

s

Tot

al

Jun

-01

Opening

Inventory 10 £35 £350 10

£35

0

Jun

-09 Purchases 15 £38 £570 25

£92

0

Jun

-15 Issued -12 £38 -£456 13

£46

4

Jun

-20 Purchases 10 £32 £320 23

£78

4

Jun

-23 Issued -10 £32 -£320 13

£46

4

Jun

-27 Issued -3 £38 -£114 10

£35

0

Jun

-30 Issued -2 £35 -£70 8

£28

0

Average cost methods

Dat

e Purchases

Unit

s

Cos

t Total

Jun

-01

Opening

Inventory 10 £35 £350

variances

Budgeted Actual Variances

Materials cost per unit £24 £18.67 £5.33

Inventory ledger record LIFO Method

Dat

e Description Sale/Purchases Balance

Unit

s

Cos

t Total

Unit

s

Tot

al

Jun

-01

Opening

Inventory 10 £35 £350 10

£35

0

Jun

-09 Purchases 15 £38 £570 25

£92

0

Jun

-15 Issued -12 £38 -£456 13

£46

4

Jun

-20 Purchases 10 £32 £320 23

£78

4

Jun

-23 Issued -10 £32 -£320 13

£46

4

Jun

-27 Issued -3 £38 -£114 10

£35

0

Jun

-30 Issued -2 £35 -£70 8

£28

0

Average cost methods

Dat

e Purchases

Unit

s

Cos

t Total

Jun

-01

Opening

Inventory 10 £35 £350

Jun

-09 Purchases 15 £38 £570

Jun

-20 Purchases 10 £32 £320

Total 35

£1,24

0

Average cost of Inventory =

Total/Units

= 1240/35

= 35.42857143

Task 3

P4. Planning tool for budgetary control

The expenditure plan is a step explaining of the liquidity output over a defined period of time.

From this point on the expenditure proposal illustrates the dynamics of incentives and goals for a

certain amount of time (Maas, Schaltegger and Crutzen, 2016). Investment policies are expecting

promoters to achieve their goals, specifically when there's some type of payment, like success or

explanations behind accomplishment. The financial results analyse financial identification

method and any negative discontinuation.

Budget Committee: A strategy category is an institutional entity that oversees the distribution by

an organisation of resource tools and properly allocates money to parts of the operation. The

financial manager produces and reviews a business planning report. The aim is to research

different types of budgets used in small-scale businesses in addition to enhancing financial and

market control.

Sales budget: The sales financial plan to explain how money will be spent to reach the planned

sales. The major aspect of the revenue budget is to allow for optimal usage of capital and

economical approach. The specifics necessary for the preparing of a process plan are given in

various ways. This expenditure plan helps to monitor the net profits of a corporation for a certain

amount of time.

Advantage:

-09 Purchases 15 £38 £570

Jun

-20 Purchases 10 £32 £320

Total 35

£1,24

0

Average cost of Inventory =

Total/Units

= 1240/35

= 35.42857143

Task 3

P4. Planning tool for budgetary control

The expenditure plan is a step explaining of the liquidity output over a defined period of time.

From this point on the expenditure proposal illustrates the dynamics of incentives and goals for a

certain amount of time (Maas, Schaltegger and Crutzen, 2016). Investment policies are expecting

promoters to achieve their goals, specifically when there's some type of payment, like success or

explanations behind accomplishment. The financial results analyse financial identification

method and any negative discontinuation.

Budget Committee: A strategy category is an institutional entity that oversees the distribution by

an organisation of resource tools and properly allocates money to parts of the operation. The

financial manager produces and reviews a business planning report. The aim is to research

different types of budgets used in small-scale businesses in addition to enhancing financial and

market control.

Sales budget: The sales financial plan to explain how money will be spent to reach the planned

sales. The major aspect of the revenue budget is to allow for optimal usage of capital and

economical approach. The specifics necessary for the preparing of a process plan are given in

various ways. This expenditure plan helps to monitor the net profits of a corporation for a certain

amount of time.

Advantage:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It attempts to estimate sales revenue correctly over a number of years. This expenditure plan is it

accomplishes the target of overall capital management income.

Drawbacks

In cases where businesses carry a wide variety of products, this may not be beneficial. It would

not be helpful for smaller companies.

Cash budget: A budget plan is really a cash invoice or even a cash schedule planned over time.

Such profits and costs include taxes charged, expenses paid, income and compensation of loans

(McLaren, Appleyard and Mitchell, 2016). In other words, an estimation of money is really an

estimation of the performance of the company throughout the coming years. They intend to

enhance the accounting standards of this proposal throughout the context of the latter Capital

Ltd.

Advantage:

This analysis is suitable for corporations in forecasting accurate accounting records and

transactions. It eliminates liquidity costs for businesses in principle.

Disadvantage

It is not really appropriate to companies with the maximum degree. To produce a plan it takes

much more time and expenses.

Zero-based budget: This is a guide that can clarify costs over a specific amount of time for

money management. This encourages the manager to continue again this year not use projections

of a single year with the beginning of the year. In the maintenance of a substantive degree of

operation and performance, through use of Capital Joinery Ltd. is highly useful.

Advantage:

This decreases their prices when they are used in industries. This describes and incentives the

administration of Capital Joinery Ltd.

Its use ensures that the right preparation is made within firms. This will also continue to assist

the administration of Capital Joinery Ltd. with a profit.

Drawbacks

The establishment of a zero-based budget consumes a lot of effort to work. A downside for

Capital Joinery Ltd could also be built in this way.

accomplishes the target of overall capital management income.

Drawbacks

In cases where businesses carry a wide variety of products, this may not be beneficial. It would

not be helpful for smaller companies.

Cash budget: A budget plan is really a cash invoice or even a cash schedule planned over time.

Such profits and costs include taxes charged, expenses paid, income and compensation of loans

(McLaren, Appleyard and Mitchell, 2016). In other words, an estimation of money is really an

estimation of the performance of the company throughout the coming years. They intend to

enhance the accounting standards of this proposal throughout the context of the latter Capital

Ltd.

Advantage:

This analysis is suitable for corporations in forecasting accurate accounting records and

transactions. It eliminates liquidity costs for businesses in principle.

Disadvantage

It is not really appropriate to companies with the maximum degree. To produce a plan it takes

much more time and expenses.

Zero-based budget: This is a guide that can clarify costs over a specific amount of time for

money management. This encourages the manager to continue again this year not use projections

of a single year with the beginning of the year. In the maintenance of a substantive degree of

operation and performance, through use of Capital Joinery Ltd. is highly useful.

Advantage:

This decreases their prices when they are used in industries. This describes and incentives the

administration of Capital Joinery Ltd.

Its use ensures that the right preparation is made within firms. This will also continue to assist

the administration of Capital Joinery Ltd. with a profit.

Drawbacks

The establishment of a zero-based budget consumes a lot of effort to work. A downside for

Capital Joinery Ltd could also be built in this way.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

A zero budget can produce numerous problems and difficulties of organisational plans and

coordination.

Production budget: A budget for production is really an expenditure plan that determines the

amount of goods produced over a great many years (Ax and Greve, 2017). In many other terms,

this study tests from moment to time the amount of units provided by a plant. Within the above

business, they scheduled such investment to manage their overall carpentry output effectively.

As described below, certain strengths and disadvantages

Advantages

The best power are being used for equipment and machinery. This aims to minimise production

costs as manufacturing products are implemented. The entire inventory of publications must be

retained.

Drawbacks

The budget preparation is a long process. It takes some time, therefore. If predictions go

incorrect, limited working days will be exhausted. This expenditure plan is completely focused

on the projected revenue prices. The resource handling is subjective and is likely to present a lot

of insecurity.

Labour budget: The significant research proposal is often used to measure the moment needed

for producing the financial sector components (Wagenhofer, 2016). The maximum additional

hours needed can indeed be defined by a more thorough direct work budget and furthermore

dissolved by work division. They schedule the staff costs in the capital juggernaut, which aims to

strengthen working ties. It contains the following advantages and disadvantages:

Advantages-

Some additional costs differ to some degree from the amount of staff hired as the sum of salaries

paid, relative to the percentage of workers, depends on the processing payment.

Based on the income study statement, the specific information presented to predict the

coefficient is clear and workers’ wages were never raised.

Drawbacks

The framework offers mediocre results as guaranteed wage salaries are paid for actual effort as

employers receive extra compensation. However, overhead rates will climb to almost the same

amount. For firms that operate at a minimal concentration or a smaller business model, that is not

enough.

coordination.

Production budget: A budget for production is really an expenditure plan that determines the

amount of goods produced over a great many years (Ax and Greve, 2017). In many other terms,

this study tests from moment to time the amount of units provided by a plant. Within the above

business, they scheduled such investment to manage their overall carpentry output effectively.

As described below, certain strengths and disadvantages

Advantages

The best power are being used for equipment and machinery. This aims to minimise production

costs as manufacturing products are implemented. The entire inventory of publications must be

retained.

Drawbacks

The budget preparation is a long process. It takes some time, therefore. If predictions go

incorrect, limited working days will be exhausted. This expenditure plan is completely focused

on the projected revenue prices. The resource handling is subjective and is likely to present a lot

of insecurity.

Labour budget: The significant research proposal is often used to measure the moment needed

for producing the financial sector components (Wagenhofer, 2016). The maximum additional

hours needed can indeed be defined by a more thorough direct work budget and furthermore

dissolved by work division. They schedule the staff costs in the capital juggernaut, which aims to

strengthen working ties. It contains the following advantages and disadvantages:

Advantages-

Some additional costs differ to some degree from the amount of staff hired as the sum of salaries

paid, relative to the percentage of workers, depends on the processing payment.

Based on the income study statement, the specific information presented to predict the

coefficient is clear and workers’ wages were never raised.

Drawbacks

The framework offers mediocre results as guaranteed wage salaries are paid for actual effort as

employers receive extra compensation. However, overhead rates will climb to almost the same

amount. For firms that operate at a minimal concentration or a smaller business model, that is not

enough.

Task 4

P5. MAS used to resolve the financial problems.

The aim is to examine the usefulness of different measures of corporate systems to address many

financial difficulties. In addition to provide it, two businesses were compared with each other.

Comparison of financial challenges solved by Tesco and Sainsbury-

Financial crisis – The management could not have the money to control the activities and

activities of the company adequately, which are seen as a cost issue. The financial collapse Since

Capital Joinery Ltd. is a manufacturing company, it must also face budgetary restrictions. The

financial challenges facing the organisation are:

Challenge of inventory management - The stock will usually be supplied in warehouses unless

the supply chains necessitate something that. The job was to extract a substance from a farm. The

concern is dealt with or replaced by the components (Alsharari and Youssef, 2017). This

dilemma causes companies to face many other challenges, including larger storage prices, poor

inventory management costs and so on. There is a major problem with above Tesco plc division.

Financial management problem: The company risk can be viewed as the mechanism for

monitoring, analysing and streamlining net financial spending less cash costs. Due to higher

amounts of cash expenses, businesses may face challenges in money management. As seen in the

case of Sainsbury plc above, they deal with this issue of insufficient cash flow management.

The benchmark: it is the process by which the company chooses the goal of the provided

resources during the year. Three explanations may even be identified in support of benchmark

assessments; the costs plan for the agreement, the budgetary overview of prior years, as well as

investigators' integration; for example, Tesco ltd. also sets efficiency tests to obtain a payment of

25 percent of treaty obligations. Naturally, Starbucks also remain responsible mostly on grounds

of prices and operating costs. This is designed to minimise redundancy and to continually reduce

variable expenses by 10%.

KPI: commonly regarded as the key success indicator; the proportion tests are the critical KPIs

for each association. It thinks fair that the Judge is liable for 2 years of financial reporting and

the usual degree of the competitiveness of the position (Tucker and Schaltegger, 2016). Tesco

Ltd., for example, maintains an ideal scale of the new 2:1 scale; there is still a financial dilemma

within the relationship. Similarly, the organisation has set a profit margin of 25%. It's a financial

P5. MAS used to resolve the financial problems.

The aim is to examine the usefulness of different measures of corporate systems to address many

financial difficulties. In addition to provide it, two businesses were compared with each other.

Comparison of financial challenges solved by Tesco and Sainsbury-

Financial crisis – The management could not have the money to control the activities and

activities of the company adequately, which are seen as a cost issue. The financial collapse Since

Capital Joinery Ltd. is a manufacturing company, it must also face budgetary restrictions. The

financial challenges facing the organisation are:

Challenge of inventory management - The stock will usually be supplied in warehouses unless

the supply chains necessitate something that. The job was to extract a substance from a farm. The

concern is dealt with or replaced by the components (Alsharari and Youssef, 2017). This

dilemma causes companies to face many other challenges, including larger storage prices, poor

inventory management costs and so on. There is a major problem with above Tesco plc division.

Financial management problem: The company risk can be viewed as the mechanism for

monitoring, analysing and streamlining net financial spending less cash costs. Due to higher

amounts of cash expenses, businesses may face challenges in money management. As seen in the

case of Sainsbury plc above, they deal with this issue of insufficient cash flow management.

The benchmark: it is the process by which the company chooses the goal of the provided

resources during the year. Three explanations may even be identified in support of benchmark

assessments; the costs plan for the agreement, the budgetary overview of prior years, as well as

investigators' integration; for example, Tesco ltd. also sets efficiency tests to obtain a payment of

25 percent of treaty obligations. Naturally, Starbucks also remain responsible mostly on grounds

of prices and operating costs. This is designed to minimise redundancy and to continually reduce

variable expenses by 10%.

KPI: commonly regarded as the key success indicator; the proportion tests are the critical KPIs

for each association. It thinks fair that the Judge is liable for 2 years of financial reporting and

the usual degree of the competitiveness of the position (Tucker and Schaltegger, 2016). Tesco

Ltd., for example, maintains an ideal scale of the new 2:1 scale; there is still a financial dilemma

within the relationship. Similarly, the organisation has set a profit margin of 25%. It's a financial

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.