Management Accounting Report: Capital Joinery Performance Analysis

VerifiedAdded on 2023/01/03

|14

|3760

|30

Report

AI Summary

This report delves into management accounting, focusing on Capital Joinery Limited, a UK-based firm specializing in windows, doors, and stairs. It begins by defining management accounting and contrasting it with financial accounting, highlighting the importance of various accounting systems like cost-accounting, inventory management, and job-costing. The report then describes different management accounting reports such as performance, budget, inventory, and accounts receivable aging reports. Task 2 focuses on preparing income statements using marginal and absorption costing methods, along with a reconciliation statement and material variance analysis. Finally, the report evaluates budgetary control planning tools and compares management system adoption by businesses to address financial problems, providing a comprehensive analysis of accounting practices and financial strategies relevant to Capital Joinery and similar businesses.

Management

accounting

accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

P1. Defining management accounting and its comparison with different systems and financial

accounting....................................................................................................................................1

P2 Description of different methods of management accounting reports:..................................3

TASK 2............................................................................................................................................4

P3. Preparing income statement with the help of different aspects that possess a lot of value in

the current scenario......................................................................................................................4

TASK 3............................................................................................................................................7

P4: Evaluation of advantages as well as disadvantages of budgetary control planning tools:....7

TASK 4............................................................................................................................................8

P5 Comparison of management system adoption by businesses for responding financial

problems:.....................................................................................................................................8

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

P1. Defining management accounting and its comparison with different systems and financial

accounting....................................................................................................................................1

P2 Description of different methods of management accounting reports:..................................3

TASK 2............................................................................................................................................4

P3. Preparing income statement with the help of different aspects that possess a lot of value in

the current scenario......................................................................................................................4

TASK 3............................................................................................................................................7

P4: Evaluation of advantages as well as disadvantages of budgetary control planning tools:....7

TASK 4............................................................................................................................................8

P5 Comparison of management system adoption by businesses for responding financial

problems:.....................................................................................................................................8

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting means managing the most important aspect of a firm that is

accounting which is regarded as an integral part of every business (Bourmistrov, Grossi and

Haldma, 2019). It is a process in which an identification of different factors are done in order to

help the organisation to sustain in the market for a much longer period of time as compared to its

competitors that are prevailing in the similar market conditions. Capital Joinery Limited is a firm

that deals in windows, doors, and stairs is geographically located in the UK and is operational

since 2008 and is doing a pretty good job in the market too. In this report there is a brief

discussion of management accounting and other aspects that are closely relate with it which

possess a lot of important for the above mentioned firm. Apart from that the report also included

different tools of budgetary control, costing system, its advantages as well as disadvantages, etc.

Further in this report there is an evaluation of Capital Joinery Limited with its competitors in an

effective manner.

P1. Defining management accounting and its comparison with different systems and financial

accounting

Management accounting is referred to as a process of identification of different factors

that both directly or indirectly affects and impacts the working of the firm so that appropriate

rectification measures can be taken according to the needs, requirements, and demand of the

enterprise. These factors possess a lot of importance in the current market scenario as they

carriers the potential to substantially improve the condition so the firm in the long run if

identified in a correct manner. Capital Joinery Limited is a company that is established not a long

ago but with the help of many aspects that are directly related with the working of the business it

has captured a larger share in the market as compared to its rivals and that too within a short

period of time. There is another aspect that is financial accounting which is also carriers a lot of

importance and its comparison with management accounting has been done below with the

context of the above discussed firm-

Management accounting Financial accounting

It is a type of accounting that is not

compulsory in nature and a firm adopts

it by its own choice. Capital Joinery

It is an accounting method that is

compulsory in nature and has to be

maintained by specific firms. Capital

Management accounting means managing the most important aspect of a firm that is

accounting which is regarded as an integral part of every business (Bourmistrov, Grossi and

Haldma, 2019). It is a process in which an identification of different factors are done in order to

help the organisation to sustain in the market for a much longer period of time as compared to its

competitors that are prevailing in the similar market conditions. Capital Joinery Limited is a firm

that deals in windows, doors, and stairs is geographically located in the UK and is operational

since 2008 and is doing a pretty good job in the market too. In this report there is a brief

discussion of management accounting and other aspects that are closely relate with it which

possess a lot of important for the above mentioned firm. Apart from that the report also included

different tools of budgetary control, costing system, its advantages as well as disadvantages, etc.

Further in this report there is an evaluation of Capital Joinery Limited with its competitors in an

effective manner.

P1. Defining management accounting and its comparison with different systems and financial

accounting

Management accounting is referred to as a process of identification of different factors

that both directly or indirectly affects and impacts the working of the firm so that appropriate

rectification measures can be taken according to the needs, requirements, and demand of the

enterprise. These factors possess a lot of importance in the current market scenario as they

carriers the potential to substantially improve the condition so the firm in the long run if

identified in a correct manner. Capital Joinery Limited is a company that is established not a long

ago but with the help of many aspects that are directly related with the working of the business it

has captured a larger share in the market as compared to its rivals and that too within a short

period of time. There is another aspect that is financial accounting which is also carriers a lot of

importance and its comparison with management accounting has been done below with the

context of the above discussed firm-

Management accounting Financial accounting

It is a type of accounting that is not

compulsory in nature and a firm adopts

it by its own choice. Capital Joinery

It is an accounting method that is

compulsory in nature and has to be

maintained by specific firms. Capital

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Limited uses it as it has proved very

beneficial for the firm in increasing its

profit volume within a limited period of

time (Cockcroft and Russell, 2018).

It is done for internal analysis and

Capital Joinery Limited does it in an

impactful manner so that it can add to

the value of the firm in the industry in

which it operates.

Joinery Limited is a company that puts

a lot of focus on this aspect as it is

capable of improving the performing of

the firm in the long run.

It is done for external purpose and

Capital Joinery Limited does it so as to

maintain a consistent image in the

market which helps it in improving its

performance.

There are a number of management accounting systems that are given below briefly-

Cost-accounting system- It is a system that is related with cost and other similar aspects

as it carriers a lot of value for each and every firm that is operating in the industry. Capital

Joinery Limited does a detailed research, analysis and evaluation of these factors so that it can

reduce unnecessary expenses so as to improve the performance of the company.

Inventory management system- It is a system that deals in managing the inventories

that a firm possesses. Capital Joinery Limited has an improved supply chain that proves

beneficial for it in this regard as it helps in managing inventories in an accurate manner.

Job-costing system- This system deals in allocation of funds according to the job so that

it can result in full utilisation of the resources available. Capital Joinery Limited recruits special

team to do all the research work and allocate the resources according to the information that is

given by that team (Daferighe, 2019).

Price-optimising system- This system deals in striking a balance between catering the

needs of the customers and earning profits. Capital Joinery Limited is profitable since its

establishment because it has opted for a price that suits both buyer and the organisation.

Also there are various other aspects too that are explained below in detail-

Management style- There are different management styles prevailing in the industry and

Capital Joinery Limited must adopt a suitable one so that it can add to the value of the

firm in the long run.

Organisation structure- To maintain an intact structure of organisation is very

important as well as crucial and the above mentioned firm gives a lot of value to this

aspect.

beneficial for the firm in increasing its

profit volume within a limited period of

time (Cockcroft and Russell, 2018).

It is done for internal analysis and

Capital Joinery Limited does it in an

impactful manner so that it can add to

the value of the firm in the industry in

which it operates.

Joinery Limited is a company that puts

a lot of focus on this aspect as it is

capable of improving the performing of

the firm in the long run.

It is done for external purpose and

Capital Joinery Limited does it so as to

maintain a consistent image in the

market which helps it in improving its

performance.

There are a number of management accounting systems that are given below briefly-

Cost-accounting system- It is a system that is related with cost and other similar aspects

as it carriers a lot of value for each and every firm that is operating in the industry. Capital

Joinery Limited does a detailed research, analysis and evaluation of these factors so that it can

reduce unnecessary expenses so as to improve the performance of the company.

Inventory management system- It is a system that deals in managing the inventories

that a firm possesses. Capital Joinery Limited has an improved supply chain that proves

beneficial for it in this regard as it helps in managing inventories in an accurate manner.

Job-costing system- This system deals in allocation of funds according to the job so that

it can result in full utilisation of the resources available. Capital Joinery Limited recruits special

team to do all the research work and allocate the resources according to the information that is

given by that team (Daferighe, 2019).

Price-optimising system- This system deals in striking a balance between catering the

needs of the customers and earning profits. Capital Joinery Limited is profitable since its

establishment because it has opted for a price that suits both buyer and the organisation.

Also there are various other aspects too that are explained below in detail-

Management style- There are different management styles prevailing in the industry and

Capital Joinery Limited must adopt a suitable one so that it can add to the value of the

firm in the long run.

Organisation structure- To maintain an intact structure of organisation is very

important as well as crucial and the above mentioned firm gives a lot of value to this

aspect.

P2 Description of different methods of management accounting reports:

Management accounting reports can be explained as a technique of business management

tool which records financial transactions of an organization. It helps in providing information

related to finance in relation to daily operations of Capital Joinery with motive of improving

their short as well as long term financial decision making. Such information is vital for internal

stakeholders as it pertains improvement in sustainability of business. There are different types

reports of management accounting which are further described below:

Performance report: This report indicates evaluation of performance of business. It

provides overview or outline regarding performance of various departments in business. It states

performances of activities of Capital Joinery and therefore helps in enhancement of enterprise

management which helps in development of business. Tracking and recoding performance of an

organization is important for evaluation of productive as well as unproductive areas for

improvisation of business efficiency (Ejiogu and Ejiogu, 2018).

Budget report: This report of managerial accounting is vital for measurement of

company’s performance and it is also helpful for managers of business to evaluate costs

that are incurred in Capital Joinery along with revenues generated by it. This helps in

evaluation of prior expenditure of an enterprise which is helpful in enabling managers for

adequate estimation of expenditures as well as income for future period of time.

Inventory management report: Management of stock is essential for company for the

purpose of effective analysis of its expenses in relevance to management of inventory.

Therefore, Capital Joinery prepares stock management or inventory management report

with the motive of evaluation of stock’s position which enables business to manage or

monitor availability of inventory for the purpose of maintaining smooth or fluent

operations in an enterprise(van Helden, 2016).

Accounts receivable aging report: Focus of accounts receivable report is on receiving

payment from credit incorporated by an organization. Preparation of such report is for the

purpose of recording all receivables of Capital Joinery for receiving payment from

debtors of company. It is helpful for managers for elimination of high period incorporated

in receiving amount from debtors. Reason is that high receivable period leads to high risk

involvement in company which serves as a negative factor for business as their chances

of bad debt increases and issue of insufficient cash flow arises. Along with it,

Management accounting reports can be explained as a technique of business management

tool which records financial transactions of an organization. It helps in providing information

related to finance in relation to daily operations of Capital Joinery with motive of improving

their short as well as long term financial decision making. Such information is vital for internal

stakeholders as it pertains improvement in sustainability of business. There are different types

reports of management accounting which are further described below:

Performance report: This report indicates evaluation of performance of business. It

provides overview or outline regarding performance of various departments in business. It states

performances of activities of Capital Joinery and therefore helps in enhancement of enterprise

management which helps in development of business. Tracking and recoding performance of an

organization is important for evaluation of productive as well as unproductive areas for

improvisation of business efficiency (Ejiogu and Ejiogu, 2018).

Budget report: This report of managerial accounting is vital for measurement of

company’s performance and it is also helpful for managers of business to evaluate costs

that are incurred in Capital Joinery along with revenues generated by it. This helps in

evaluation of prior expenditure of an enterprise which is helpful in enabling managers for

adequate estimation of expenditures as well as income for future period of time.

Inventory management report: Management of stock is essential for company for the

purpose of effective analysis of its expenses in relevance to management of inventory.

Therefore, Capital Joinery prepares stock management or inventory management report

with the motive of evaluation of stock’s position which enables business to manage or

monitor availability of inventory for the purpose of maintaining smooth or fluent

operations in an enterprise(van Helden, 2016).

Accounts receivable aging report: Focus of accounts receivable report is on receiving

payment from credit incorporated by an organization. Preparation of such report is for the

purpose of recording all receivables of Capital Joinery for receiving payment from

debtors of company. It is helpful for managers for elimination of high period incorporated

in receiving amount from debtors. Reason is that high receivable period leads to high risk

involvement in company which serves as a negative factor for business as their chances

of bad debt increases and issue of insufficient cash flow arises. Along with it,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

involvement of high risk ultimately reduces credit worthiness of an organization which

can be eliminated by preparing report of accounts receivables (Ghanem and Sulaiman,

2016).

TASK 2

P3. Preparing income statement with the help of different aspects that possess a lot of value in

the current scenario

There are a number of different costs that are prevailing in the present time and the ones

that are most commonly by different firms are discussed below in detail-

Fixed cost- It is a cost that remains fixed whether there is increase or decrease in the

value of output and remains constant throughout. Capital joinery Limited operates at a low fixed

cost that enables it to earn more profits in the long run.

Variable cost- It is a cost that changes with the change in output of the firm. Capital

joinery Limited produces a large number of quantities which subsequently reduces it’s per unit

cost that makes the firm more profitable in the long run.

Semi-variable cost- These are costs that include some part of fixed and some part of

variable cost while the fixed part remains fixed and variable part changes with the change in

output. Capital joinery Limited has a lot semi-variable cost that enables it to sustain in the market

for a longer period of time as compared to its rivals.

Absorption costing- It includes all types of costs which are incurred while operating like

wages, rent, etc.

Marginal costing- It includes cost which are levied on the firm to produce an extra unit

of output in the market. It is the reason of change in total cost (Holzer and Schoenfeld, 2019).

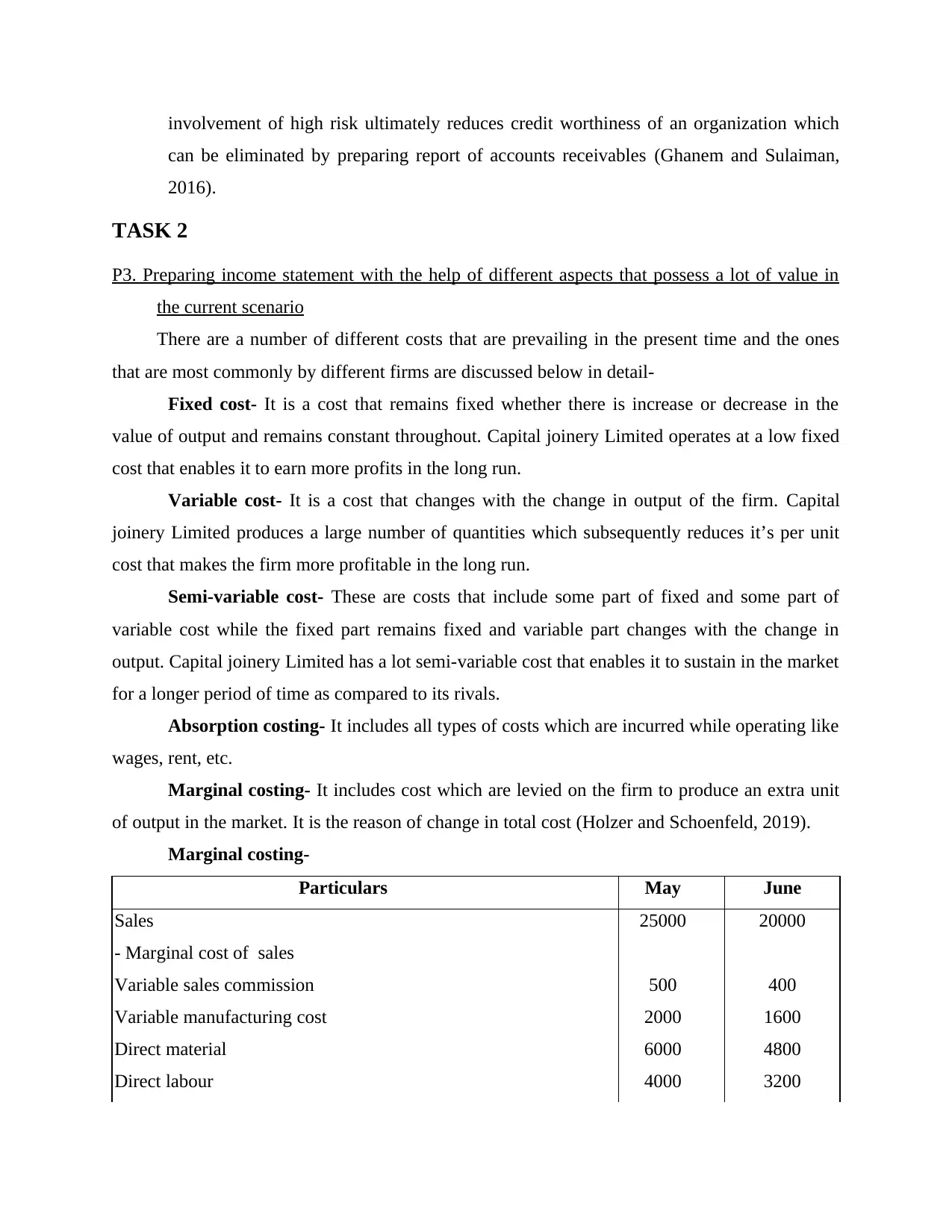

Marginal costing-

Particulars May June

Sales 25000 20000

- Marginal cost of sales

Variable sales commission 500 400

Variable manufacturing cost 2000 1600

Direct material 6000 4800

Direct labour 4000 3200

can be eliminated by preparing report of accounts receivables (Ghanem and Sulaiman,

2016).

TASK 2

P3. Preparing income statement with the help of different aspects that possess a lot of value in

the current scenario

There are a number of different costs that are prevailing in the present time and the ones

that are most commonly by different firms are discussed below in detail-

Fixed cost- It is a cost that remains fixed whether there is increase or decrease in the

value of output and remains constant throughout. Capital joinery Limited operates at a low fixed

cost that enables it to earn more profits in the long run.

Variable cost- It is a cost that changes with the change in output of the firm. Capital

joinery Limited produces a large number of quantities which subsequently reduces it’s per unit

cost that makes the firm more profitable in the long run.

Semi-variable cost- These are costs that include some part of fixed and some part of

variable cost while the fixed part remains fixed and variable part changes with the change in

output. Capital joinery Limited has a lot semi-variable cost that enables it to sustain in the market

for a longer period of time as compared to its rivals.

Absorption costing- It includes all types of costs which are incurred while operating like

wages, rent, etc.

Marginal costing- It includes cost which are levied on the firm to produce an extra unit

of output in the market. It is the reason of change in total cost (Holzer and Schoenfeld, 2019).

Marginal costing-

Particulars May June

Sales 25000 20000

- Marginal cost of sales

Variable sales commission 500 400

Variable manufacturing cost 2000 1600

Direct material 6000 4800

Direct labour 4000 3200

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Total marginal cost of sales 4500 3600

Contribution 20500 16400

- Fixed cost

Fixed selling 1000 1000

Fixed production overhead 2000 2000

Fixed administration 3000 3000

Net profit 14500 10400

Absorption costing-

Particulars May June

Sales 25000 20000

-Marginal cost of sales

Variable sales commission 500 400

Variable manufacturing cost 2000 1600

Fixed selling 1000 1000

Fixed administration 3000 3000

Direct material 6000 4800

Direct labour 4000 3200

Total marginal cost of sales 16500 14000

Gross profit 8500 6000

-Fixed production overhead 2000 2000

Net profit 6500 4000

Reconciliation statement-

Particulars May June

Profit/ loss under absorption costing 6500 4000

Add/less closing stock 8000 6400

Profit/loss under marginal costing 14500 10400

Profit/loss under marginal costing 14500 10400

Working note-

Particulars Amount

Material cost variance

Standard cost 24000

Contribution 20500 16400

- Fixed cost

Fixed selling 1000 1000

Fixed production overhead 2000 2000

Fixed administration 3000 3000

Net profit 14500 10400

Absorption costing-

Particulars May June

Sales 25000 20000

-Marginal cost of sales

Variable sales commission 500 400

Variable manufacturing cost 2000 1600

Fixed selling 1000 1000

Fixed administration 3000 3000

Direct material 6000 4800

Direct labour 4000 3200

Total marginal cost of sales 16500 14000

Gross profit 8500 6000

-Fixed production overhead 2000 2000

Net profit 6500 4000

Reconciliation statement-

Particulars May June

Profit/ loss under absorption costing 6500 4000

Add/less closing stock 8000 6400

Profit/loss under marginal costing 14500 10400

Profit/loss under marginal costing 14500 10400

Working note-

Particulars Amount

Material cost variance

Standard cost 24000

Actual cost 22400

Result 1600

Material price variance

Standard price 12

Actual price 9.3

Actual quantity 1000

Result 2700

Material usage variance

Standard quantity 2000

Actual quantity 2400

Standard price 12

Result -4800

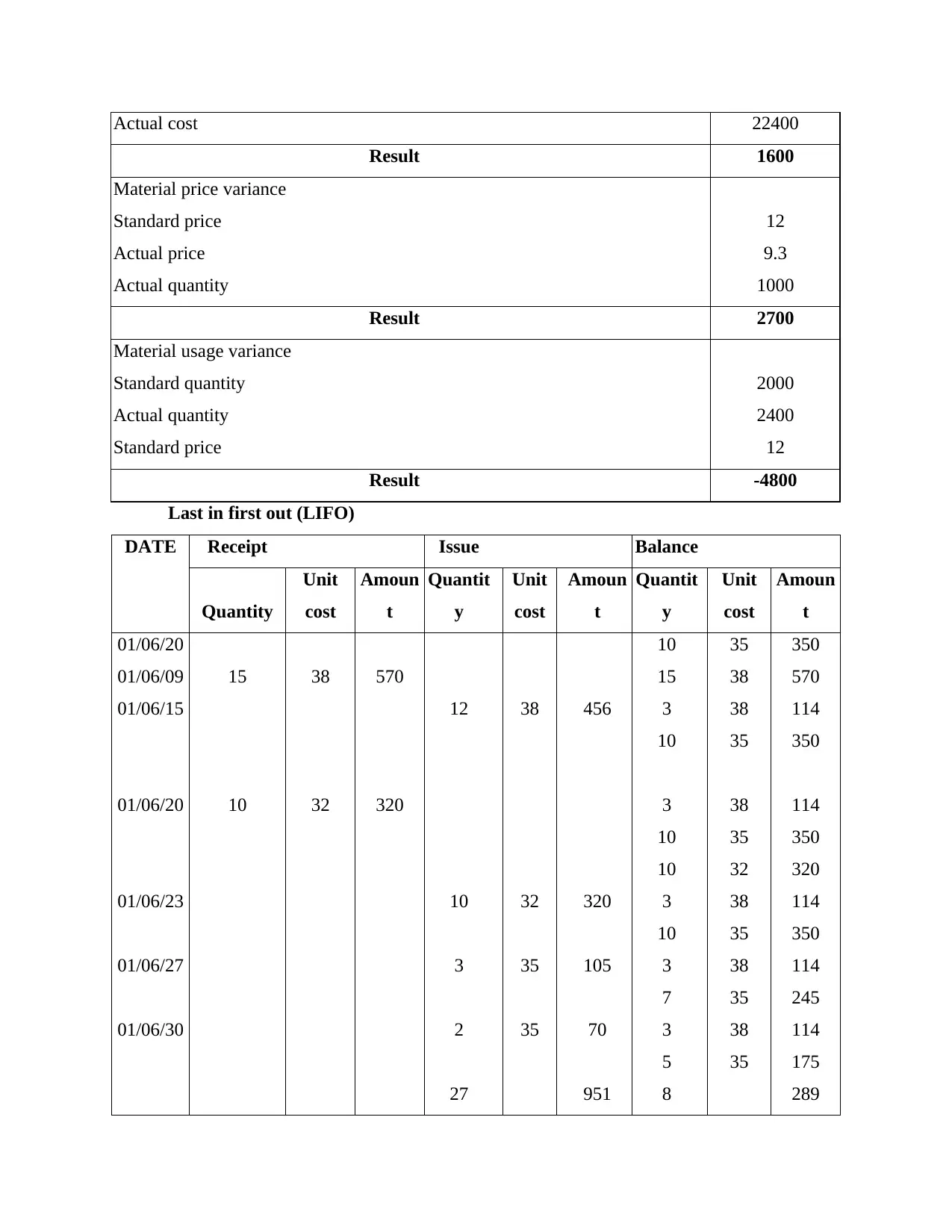

Last in first out (LIFO)

DATE Receipt Issue Balance

Quantity

Unit

cost

Amoun

t

Quantit

y

Unit

cost

Amoun

t

Quantit

y

Unit

cost

Amoun

t

01/06/20 10 35 350

01/06/09 15 38 570 15 38 570

01/06/15 12 38 456 3 38 114

10 35 350

01/06/20 10 32 320 3 38 114

10 35 350

10 32 320

01/06/23 10 32 320 3 38 114

10 35 350

01/06/27 3 35 105 3 38 114

7 35 245

01/06/30 2 35 70 3 38 114

5 35 175

27 951 8 289

Result 1600

Material price variance

Standard price 12

Actual price 9.3

Actual quantity 1000

Result 2700

Material usage variance

Standard quantity 2000

Actual quantity 2400

Standard price 12

Result -4800

Last in first out (LIFO)

DATE Receipt Issue Balance

Quantity

Unit

cost

Amoun

t

Quantit

y

Unit

cost

Amoun

t

Quantit

y

Unit

cost

Amoun

t

01/06/20 10 35 350

01/06/09 15 38 570 15 38 570

01/06/15 12 38 456 3 38 114

10 35 350

01/06/20 10 32 320 3 38 114

10 35 350

10 32 320

01/06/23 10 32 320 3 38 114

10 35 350

01/06/27 3 35 105 3 38 114

7 35 245

01/06/30 2 35 70 3 38 114

5 35 175

27 951 8 289

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

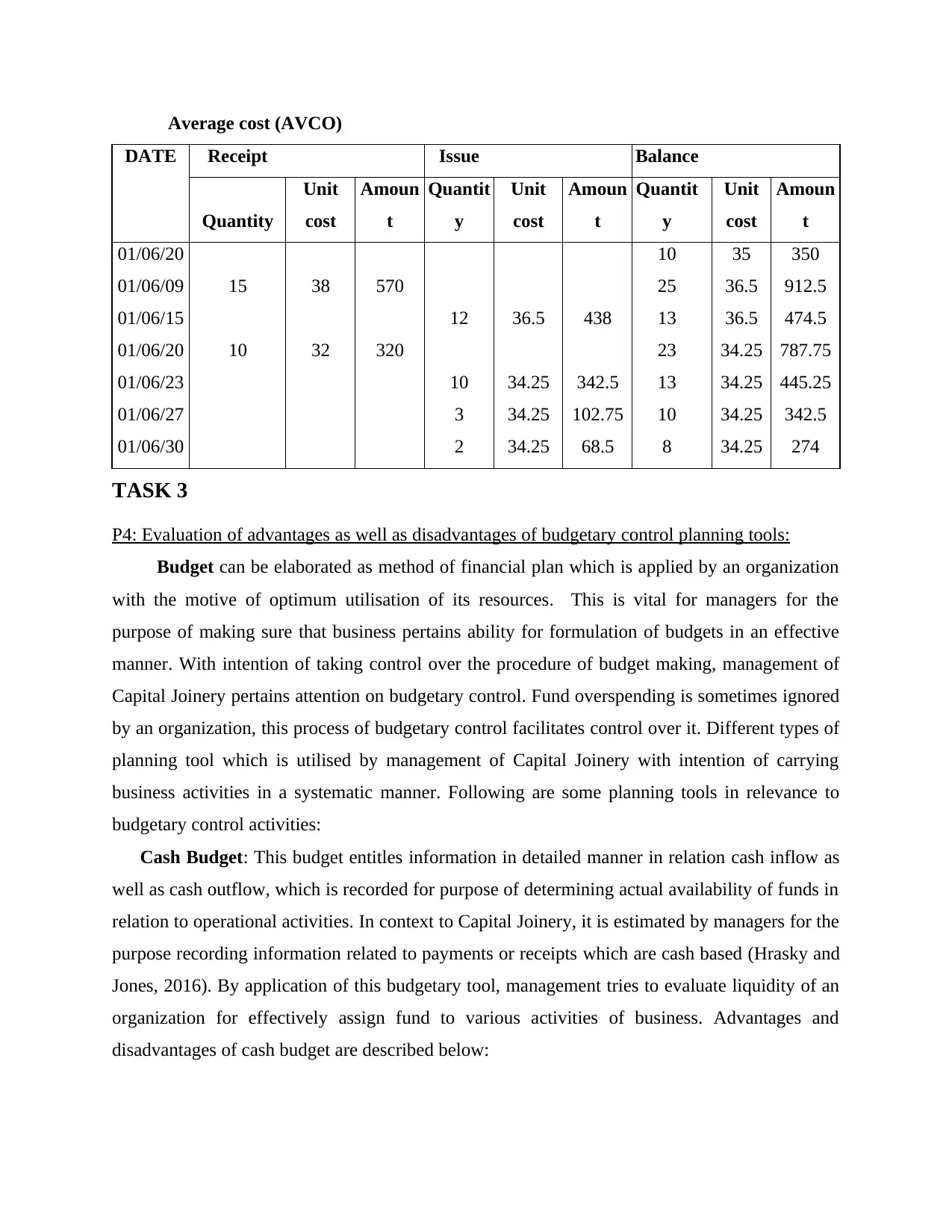

Average cost (AVCO)

DATE Receipt Issue Balance

Quantity

Unit

cost

Amoun

t

Quantit

y

Unit

cost

Amoun

t

Quantit

y

Unit

cost

Amoun

t

01/06/20 10 35 350

01/06/09 15 38 570 25 36.5 912.5

01/06/15 12 36.5 438 13 36.5 474.5

01/06/20 10 32 320 23 34.25 787.75

01/06/23 10 34.25 342.5 13 34.25 445.25

01/06/27 3 34.25 102.75 10 34.25 342.5

01/06/30 2 34.25 68.5 8 34.25 274

TASK 3

P4: Evaluation of advantages as well as disadvantages of budgetary control planning tools:

Budget can be elaborated as method of financial plan which is applied by an organization

with the motive of optimum utilisation of its resources. This is vital for managers for the

purpose of making sure that business pertains ability for formulation of budgets in an effective

manner. With intention of taking control over the procedure of budget making, management of

Capital Joinery pertains attention on budgetary control. Fund overspending is sometimes ignored

by an organization, this process of budgetary control facilitates control over it. Different types of

planning tool which is utilised by management of Capital Joinery with intention of carrying

business activities in a systematic manner. Following are some planning tools in relevance to

budgetary control activities:

Cash Budget: This budget entitles information in detailed manner in relation cash inflow as

well as cash outflow, which is recorded for purpose of determining actual availability of funds in

relation to operational activities. In context to Capital Joinery, it is estimated by managers for the

purpose recording information related to payments or receipts which are cash based (Hrasky and

Jones, 2016). By application of this budgetary tool, management tries to evaluate liquidity of an

organization for effectively assign fund to various activities of business. Advantages and

disadvantages of cash budget are described below:

DATE Receipt Issue Balance

Quantity

Unit

cost

Amoun

t

Quantit

y

Unit

cost

Amoun

t

Quantit

y

Unit

cost

Amoun

t

01/06/20 10 35 350

01/06/09 15 38 570 25 36.5 912.5

01/06/15 12 36.5 438 13 36.5 474.5

01/06/20 10 32 320 23 34.25 787.75

01/06/23 10 34.25 342.5 13 34.25 445.25

01/06/27 3 34.25 102.75 10 34.25 342.5

01/06/30 2 34.25 68.5 8 34.25 274

TASK 3

P4: Evaluation of advantages as well as disadvantages of budgetary control planning tools:

Budget can be elaborated as method of financial plan which is applied by an organization

with the motive of optimum utilisation of its resources. This is vital for managers for the

purpose of making sure that business pertains ability for formulation of budgets in an effective

manner. With intention of taking control over the procedure of budget making, management of

Capital Joinery pertains attention on budgetary control. Fund overspending is sometimes ignored

by an organization, this process of budgetary control facilitates control over it. Different types of

planning tool which is utilised by management of Capital Joinery with intention of carrying

business activities in a systematic manner. Following are some planning tools in relevance to

budgetary control activities:

Cash Budget: This budget entitles information in detailed manner in relation cash inflow as

well as cash outflow, which is recorded for purpose of determining actual availability of funds in

relation to operational activities. In context to Capital Joinery, it is estimated by managers for the

purpose recording information related to payments or receipts which are cash based (Hrasky and

Jones, 2016). By application of this budgetary tool, management tries to evaluate liquidity of an

organization for effectively assign fund to various activities of business. Advantages and

disadvantages of cash budget are described below:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Advantages: By application of this technique, business can evaluate availability of cash

in an organization. This budget type helps in analysing all incomes as well as expenses

ofCapital Joinery which are in cash form.

Disadvantages: Recorded information of cash budget is historic and it pertains effect on

accuracy of results. Originality of such budget type lacks and reason is that most

businesses are utilising transactions on the basis of credit instead of cash basis.

Zero based budget: This can be explained as that budget which is applied by an

organization for the purpose of determining exact or actual information in relation to

transactions for current period of time because it is started with zero base and information is

kept for a year only. Managing team of Capital Joinery formulates this budget type with

intention of evaluating accurate business position. Managers need to justify every expense as

well as income which is recorded in this budget as it accurately formulates budget. Some

major advantages as well as disadvantages of zero-based budget are explained below:

Advantages: With application of this budget, managers can determine information

regarding all operations of Capital Joinery which is essential for management team to

evaluate accurate financial position of business during particular period of time. It

increases level of involvement of staff members in an organization, reason is that zero

based budget provides information regarding employees of an enterprise in detailed

manner (Isaac Roque and Cañizares Roig, 2019).

Disadvantages: The procedure of estimating this budget is a critical task and high

experienced manager is required for the purpose of formulating it. High cost is incurred

in Capital Joinery for formulation of this kind of budget.

TASK 4

P5 Comparison of management system adoption by businesses for responding financial

problems:

Financial problems: It can be described as problem that can be faced by business because

of incapability of an organization in monitoring business activities in relation to finance. These

problems serve as a hindrance in improvement of profitability of Capital Joinery. Therefore, it is

required by an organization to eliminate by management for enhancing efficiency of business. In

context to business, problems in regard to finance are described below:

in an organization. This budget type helps in analysing all incomes as well as expenses

ofCapital Joinery which are in cash form.

Disadvantages: Recorded information of cash budget is historic and it pertains effect on

accuracy of results. Originality of such budget type lacks and reason is that most

businesses are utilising transactions on the basis of credit instead of cash basis.

Zero based budget: This can be explained as that budget which is applied by an

organization for the purpose of determining exact or actual information in relation to

transactions for current period of time because it is started with zero base and information is

kept for a year only. Managing team of Capital Joinery formulates this budget type with

intention of evaluating accurate business position. Managers need to justify every expense as

well as income which is recorded in this budget as it accurately formulates budget. Some

major advantages as well as disadvantages of zero-based budget are explained below:

Advantages: With application of this budget, managers can determine information

regarding all operations of Capital Joinery which is essential for management team to

evaluate accurate financial position of business during particular period of time. It

increases level of involvement of staff members in an organization, reason is that zero

based budget provides information regarding employees of an enterprise in detailed

manner (Isaac Roque and Cañizares Roig, 2019).

Disadvantages: The procedure of estimating this budget is a critical task and high

experienced manager is required for the purpose of formulating it. High cost is incurred

in Capital Joinery for formulation of this kind of budget.

TASK 4

P5 Comparison of management system adoption by businesses for responding financial

problems:

Financial problems: It can be described as problem that can be faced by business because

of incapability of an organization in monitoring business activities in relation to finance. These

problems serve as a hindrance in improvement of profitability of Capital Joinery. Therefore, it is

required by an organization to eliminate by management for enhancing efficiency of business. In

context to business, problems in regard to finance are described below:

Insufficient cash flow: Problems in relevance to cash flow states incapability of an

organization in maintenance of liquidity for daily operations of an enterprise. In addition

to it, payment related problems lead to hindrance in payment of short-term loans.

High storage costs: High expense of storing refers to that expense which company bears

in storage of inventory of an organization. It ultimately leads to improvement of overall

expenses of an organization; therefore, profitability and productivity of an enterprise

reduces (Lutilsky, Liović and Marković, 2018).

Various techniques of monitoring can be used by management of an organization for the

purpose of identification and evaluation of issues in relevance to finance. Some of such

techniques are described below in addition to its application in identification of problems:

Key performance indicator: KPI or key performance indicator can be determined as

that process which company utilises for the purpose of analysing its progress towards

achievement of results. This indicator of performance is basically of two types, which

are, non-financial as well as financial key performance indicator. Financial key

performance indicator is a helpful too for evaluation of company’s financial performance

(Reizinger-Ducsai, 2018).

Benchmarking: It can be explained as process of comparison between policies of

businesses and procedure of its activity for the purpose of evaluating results of business

and comparison of it by standards which are set by management. Application of this tool

of monitoring, business can evaluate problems regarding management of cash flow.

Financial governance: It can be defined as a procedure of monitoring and collecting

information of financial transaction of company. It indicates process of tracking of

financial related performance of an organization which ensures management implication

for controlling problematic areas of financial and gaining profitability as well as expertise

in relevance to business operations (Rogošić and Perica, 2016).

TESCO MORRISONS

Financial problem faced by Tesco is that

company fails in management of cash flow.

For the purpose of solving this issue job

costing system is best suited as it helps

business in tracking expense of business in

Over expenditure is a problem related to

finance which is face by Morrisons. For

solving this problem management can

apply cost accounting system. It records al

cash expenses of business. Hence,

organization in maintenance of liquidity for daily operations of an enterprise. In addition

to it, payment related problems lead to hindrance in payment of short-term loans.

High storage costs: High expense of storing refers to that expense which company bears

in storage of inventory of an organization. It ultimately leads to improvement of overall

expenses of an organization; therefore, profitability and productivity of an enterprise

reduces (Lutilsky, Liović and Marković, 2018).

Various techniques of monitoring can be used by management of an organization for the

purpose of identification and evaluation of issues in relevance to finance. Some of such

techniques are described below in addition to its application in identification of problems:

Key performance indicator: KPI or key performance indicator can be determined as

that process which company utilises for the purpose of analysing its progress towards

achievement of results. This indicator of performance is basically of two types, which

are, non-financial as well as financial key performance indicator. Financial key

performance indicator is a helpful too for evaluation of company’s financial performance

(Reizinger-Ducsai, 2018).

Benchmarking: It can be explained as process of comparison between policies of

businesses and procedure of its activity for the purpose of evaluating results of business

and comparison of it by standards which are set by management. Application of this tool

of monitoring, business can evaluate problems regarding management of cash flow.

Financial governance: It can be defined as a procedure of monitoring and collecting

information of financial transaction of company. It indicates process of tracking of

financial related performance of an organization which ensures management implication

for controlling problematic areas of financial and gaining profitability as well as expertise

in relevance to business operations (Rogošić and Perica, 2016).

TESCO MORRISONS

Financial problem faced by Tesco is that

company fails in management of cash flow.

For the purpose of solving this issue job

costing system is best suited as it helps

business in tracking expense of business in

Over expenditure is a problem related to

finance which is face by Morrisons. For

solving this problem management can

apply cost accounting system. It records al

cash expenses of business. Hence,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.