Capital Joinery Management Accounting Report: Financial Analysis

VerifiedAdded on 2023/01/05

|15

|3695

|62

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles, focusing on the case study of Capital Joinery. It begins with an introduction to management accounting, defining its role in financial resource management and its importance in achieving organizational objectives. The report identifies key fields within management accounting, such as profit maximization, efficiency boosting, and inventory management, and discusses their requirements within the context of Capital Joinery. It then delves into management accounting reporting, including budget reports, cost managerial accounting reports, and performance reports. The report further examines income statements, comparing marginal and absorption costing methods. It also explores various budgetary tools, such as capital budgeting, and evaluates their merits and demerits. Finally, the report addresses how organizations can respond to financial problems using management accounting systems. The report concludes by summarizing the key findings and providing references for further study.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION......................................................................................................................3

MAIN BODY.............................................................................................................................3

Identification of fields in management accounting and their requirements...........................3

P2 management accounting reporting and Method................................................................5

TASK2.......................................................................................................................................6

P3 Income statement using marginal and absorption costs....................................................6

TASK3.......................................................................................................................................8

P4 Merits and demerits of budgetary tools............................................................................8

TASK4.....................................................................................................................................10

P5 Financial problem and response of organization............................................................10

CONCLUSION........................................................................................................................12

REFERENCES.........................................................................................................................13

Books and journals...............................................................................................................13

INTRODUCTION......................................................................................................................3

MAIN BODY.............................................................................................................................3

Identification of fields in management accounting and their requirements...........................3

P2 management accounting reporting and Method................................................................5

TASK2.......................................................................................................................................6

P3 Income statement using marginal and absorption costs....................................................6

TASK3.......................................................................................................................................8

P4 Merits and demerits of budgetary tools............................................................................8

TASK4.....................................................................................................................................10

P5 Financial problem and response of organization............................................................10

CONCLUSION........................................................................................................................12

REFERENCES.........................................................................................................................13

Books and journals...............................................................................................................13

INTRODUCTION

Management accounting is referred to a process which is related to identification of various

cost and using appropriate information in order to manage the financial resources of

organisation (Drury, 2018). There are a number of purposes which will be included under the

management accounting system which are related to communication of info to different

parties in order to achieve the objectives of organisation. In relation to the current report, it is

based on study of Capital joinery. In relation to the current report it includes discussion about

the management accounting and its essential requirements. There is also a discussion about

various methods used in management reporting. Along with this, this report is also the

discussion about calculation about the cost of organisation. In last, there is discussion about

various planning tools which are used for budgetary control with advantages and

disadvantages and differentiating how the enterprises can adopt a management accounting

system in response to the financial problems.

MAIN BODY

P1 Identification of fields in management accounting and their requirements

Management accounting can be defined as a process which involves managing

various accounts of organization in order to meet the financial requirements and identification

of different cost so that organization can perform its function in an appropriate way and

achieves the objectives in timely manner. Management accounting is useful system to the

organization as it promotes standardization within the work as well as help in meeting the

requirements of stakeholders. Capital joineryis also using management accounting in order to

strengthen its decision making process as well as identify various requirements in the

meantime (Otley, 2016).

According to the institute of management accounting "management accounting can be

defined as a term which is used by professionals in relation to meeting the decision-making

abilities of organization and planning about the financial performance. Include evaluation of

different financial accounts and identification of cost which are related to the products and

services offered by organization in the current business time".

There are a number of management accounting systems and types which has to be

managed by organization in order to achieve better system. In context of Capital joineryit is

Management accounting is referred to a process which is related to identification of various

cost and using appropriate information in order to manage the financial resources of

organisation (Drury, 2018). There are a number of purposes which will be included under the

management accounting system which are related to communication of info to different

parties in order to achieve the objectives of organisation. In relation to the current report, it is

based on study of Capital joinery. In relation to the current report it includes discussion about

the management accounting and its essential requirements. There is also a discussion about

various methods used in management reporting. Along with this, this report is also the

discussion about calculation about the cost of organisation. In last, there is discussion about

various planning tools which are used for budgetary control with advantages and

disadvantages and differentiating how the enterprises can adopt a management accounting

system in response to the financial problems.

MAIN BODY

P1 Identification of fields in management accounting and their requirements

Management accounting can be defined as a process which involves managing

various accounts of organization in order to meet the financial requirements and identification

of different cost so that organization can perform its function in an appropriate way and

achieves the objectives in timely manner. Management accounting is useful system to the

organization as it promotes standardization within the work as well as help in meeting the

requirements of stakeholders. Capital joineryis also using management accounting in order to

strengthen its decision making process as well as identify various requirements in the

meantime (Otley, 2016).

According to the institute of management accounting "management accounting can be

defined as a term which is used by professionals in relation to meeting the decision-making

abilities of organization and planning about the financial performance. Include evaluation of

different financial accounts and identification of cost which are related to the products and

services offered by organization in the current business time".

There are a number of management accounting systems and types which has to be

managed by organization in order to achieve better system. In context of Capital joineryit is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

also utilizing appropriate system which is helpful for manager to utilize the function and

perform them in an effective manner. Some of these functions are discussed below:

Profit maximization: management accounting is useful for organization in

maximizing the profitability. This is because management accounting helps in evaluation of

various financial statements of organization which help in evaluating the current position of

firm and identifying the cost involved in different products and services. This enable

organization to use appropriate system and manage financial accounts according to the

requirements (Maas, Schaltegger and Crutzen, 2016).

Efficiency booster: management accounting is appropriate systems which help in

increasing the efficiency of employees and performing the function in an appropriate way. In

context of the current business environment, management accounting help in identifying the

actual function which are performed by organization and remedies which can be used to

improve those functions. These functions are associated with current profitability of

organisation and efficiency of employees in working. By utilizing the accounts in an

appropriate manner and performing the functions of management accounting lead in better

profitability and efficiency.

Management accounting system

Inventory management system: It is a part of management accounting which helps

business entity in managing inventory in accordance with its sales. In context of Capital

joinery, manager within management accounting identify the current stock of inventory is

within storage of organization As well as at physical stores. This is helpful to Organization in

analyzing its current functions and performing them in an appropriate manner. Real manager

divide inventory in raw material finished good and semi process good. This is helpful to the

manager in evaluating the inventory within Capital joineryand using an appropriate method to

identify the aging inventory and selling it prior to the new inventory.

Cost accounting: It is also act as a part of management accounting. This is helpful to

Organization in managing the functions of costing. It can be defined as a system which was

adopted by organization under the topic of management accounting where organization has to

identify different cost which are involved under the process of selling goods and services

from beginning to end. This provides specific guidelines to organization about the process of

cost involved in various function and help in achieving business objectives. Include

perform them in an effective manner. Some of these functions are discussed below:

Profit maximization: management accounting is useful for organization in

maximizing the profitability. This is because management accounting helps in evaluation of

various financial statements of organization which help in evaluating the current position of

firm and identifying the cost involved in different products and services. This enable

organization to use appropriate system and manage financial accounts according to the

requirements (Maas, Schaltegger and Crutzen, 2016).

Efficiency booster: management accounting is appropriate systems which help in

increasing the efficiency of employees and performing the function in an appropriate way. In

context of the current business environment, management accounting help in identifying the

actual function which are performed by organization and remedies which can be used to

improve those functions. These functions are associated with current profitability of

organisation and efficiency of employees in working. By utilizing the accounts in an

appropriate manner and performing the functions of management accounting lead in better

profitability and efficiency.

Management accounting system

Inventory management system: It is a part of management accounting which helps

business entity in managing inventory in accordance with its sales. In context of Capital

joinery, manager within management accounting identify the current stock of inventory is

within storage of organization As well as at physical stores. This is helpful to Organization in

analyzing its current functions and performing them in an appropriate manner. Real manager

divide inventory in raw material finished good and semi process good. This is helpful to the

manager in evaluating the inventory within Capital joineryand using an appropriate method to

identify the aging inventory and selling it prior to the new inventory.

Cost accounting: It is also act as a part of management accounting. This is helpful to

Organization in managing the functions of costing. It can be defined as a system which was

adopted by organization under the topic of management accounting where organization has to

identify different cost which are involved under the process of selling goods and services

from beginning to end. This provides specific guidelines to organization about the process of

cost involved in various function and help in achieving business objectives. Include

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

appropriate process which has to be followed by manager of the organization so that they can

identify different cost and used the cost in accordance with organizational functioning

(Hopper and Bui, 2016)

Price optimization system: Price of optimization system is that part of organization

which is helpful in calculating the instruments cost which are implemented by the

organization in order to generate the revenue. This is important part of management

accounting which is responsible for identification of customer behavior and using the prices

according to the response of customers within market. This is helpful to the organization in

evaluating the current processes which has to be followed in order to meet the customer

requirement and using an appropriate pricing policy. In context of Capital joinery,

organizations performing its function at global level which means that it requires an

appropriate pricing policy to meet the requirements of global standards. Under this price

optimization system can be implemented which help the form in analyzing the pricing

policies according to the longer period and performing functions in an appropriate way for

identifying future growth.

Job costing system: Job costing systems include identification of different cost which

are involved in a particular job or a task which are performed under separate activity. job

costing system is useful for organization in management of various processes and using these

processes under a manufacturing industry. This involves identification of actual expenses and

using appropriate revenues in relation to the process performed by firm. there are a number of

cost which are involved in organizational process and help in identification of appropriate

profitability. Capital joineryalso involved job costing method in its management accounting

which helped the management in identification of actual cost which is implemented in a

particular process. This is also useful to the firm in utilizing its resources and managing

function according to the needs and requirements (Cooper, Ezzamel and Qu, 2017)

P2 management accounting reporting and Method

Management accounting report

Management accounting reporting is that part of management accounts which is

related to different reports which covered under the management accounting system in order

to manage different accounts. It includes different systematically procedures which are used

to formulate by the organisation in order to strengthen the decision-making process and

identify different cost and used the cost in accordance with organizational functioning

(Hopper and Bui, 2016)

Price optimization system: Price of optimization system is that part of organization

which is helpful in calculating the instruments cost which are implemented by the

organization in order to generate the revenue. This is important part of management

accounting which is responsible for identification of customer behavior and using the prices

according to the response of customers within market. This is helpful to the organization in

evaluating the current processes which has to be followed in order to meet the customer

requirement and using an appropriate pricing policy. In context of Capital joinery,

organizations performing its function at global level which means that it requires an

appropriate pricing policy to meet the requirements of global standards. Under this price

optimization system can be implemented which help the form in analyzing the pricing

policies according to the longer period and performing functions in an appropriate way for

identifying future growth.

Job costing system: Job costing systems include identification of different cost which

are involved in a particular job or a task which are performed under separate activity. job

costing system is useful for organization in management of various processes and using these

processes under a manufacturing industry. This involves identification of actual expenses and

using appropriate revenues in relation to the process performed by firm. there are a number of

cost which are involved in organizational process and help in identification of appropriate

profitability. Capital joineryalso involved job costing method in its management accounting

which helped the management in identification of actual cost which is implemented in a

particular process. This is also useful to the firm in utilizing its resources and managing

function according to the needs and requirements (Cooper, Ezzamel and Qu, 2017)

P2 management accounting reporting and Method

Management accounting report

Management accounting reporting is that part of management accounts which is

related to different reports which covered under the management accounting system in order

to manage different accounts. It includes different systematically procedures which are used

to formulate by the organisation in order to strengthen the decision-making process and

perform the function in an appropriate way. There are number of management accounting

reports which are used by Capital joinery, some of these are discussed below:

Budget report: Budget report is an essential part of management accounting system

which consist information about the budget allotted to different activities which are

performed in order to maintain the working condition. This is a important part of Capital

joinerybecause it consists action plans as well as budget to each and every activity in order to

manage the work of different activity. Manager it in Capital joineryalso use this function to

improve the functioning and achieve objectives (Jansen, 2018).

Cost managerial accounting report: This is that financial report which consist

information about different cost implemented by the managers in order to sell the products

and services and generate revenue. It is useful part in organisation which is prepared take

different actions against different cost which are implemented Organisation in manufacturing

a product selling it to the last consumer. In context of Capital joinery, manager in

organisation news report to identify the system and perform inventory management.

Performance report: Performance report is that report which includes description

about the performance of different individuals. What is the most essential report in

organisation as it helped us to identify the current requirement as soon as performance of

employees. This performance will be evaluated in appropriate places where different

decisions are taken accordingly (Makrygiannakis and Jack, 2016).

It can be evaluated from the above mentioned information that there are various

function which has to be analysed and will be used by organisation. This make it difficult for

the firm to choose appropriate system and finalize the accounts in an appropriate way. It

became responsibility for manager to use various reports in order to identify and perform

functions appropriately.

TASK2

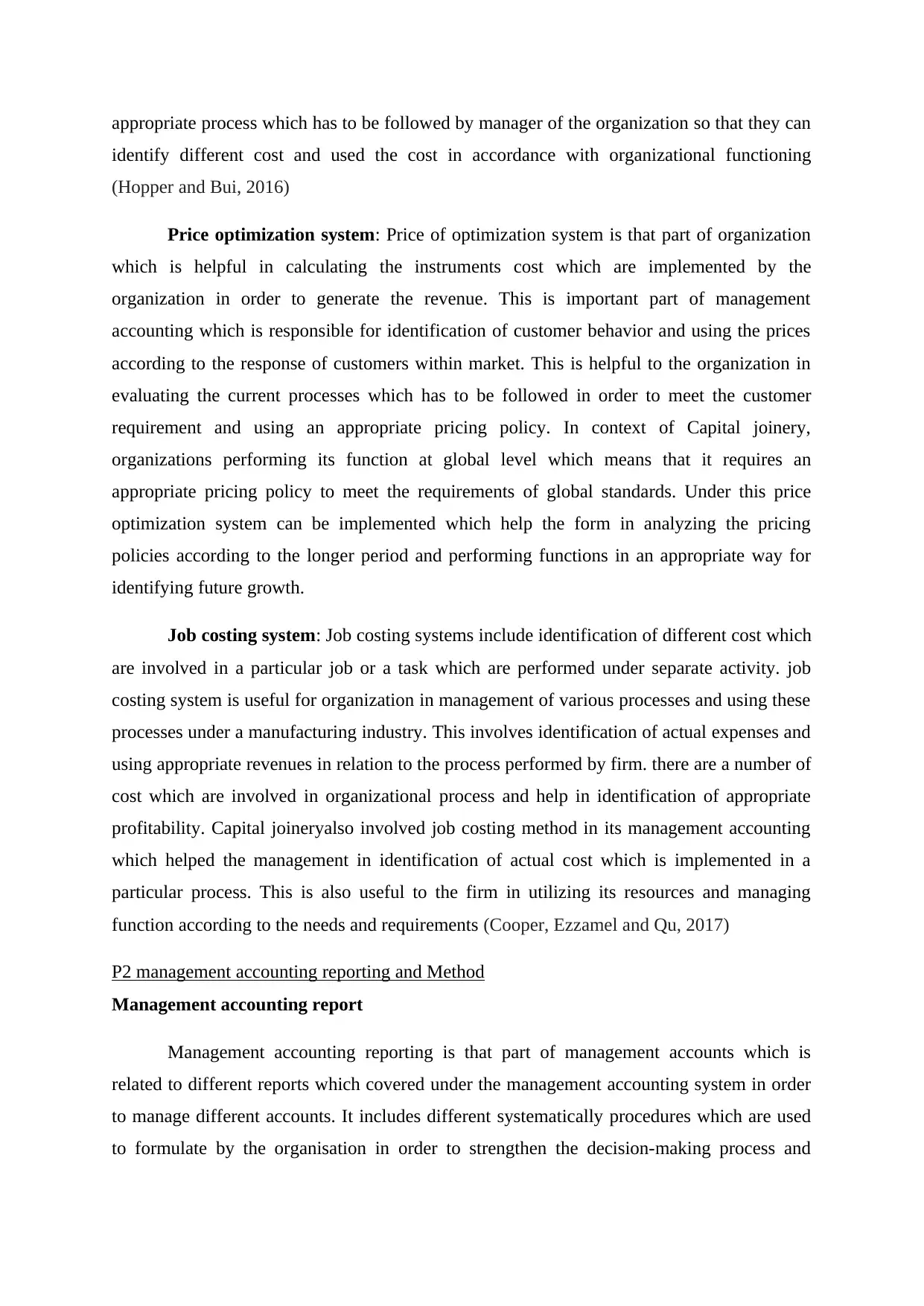

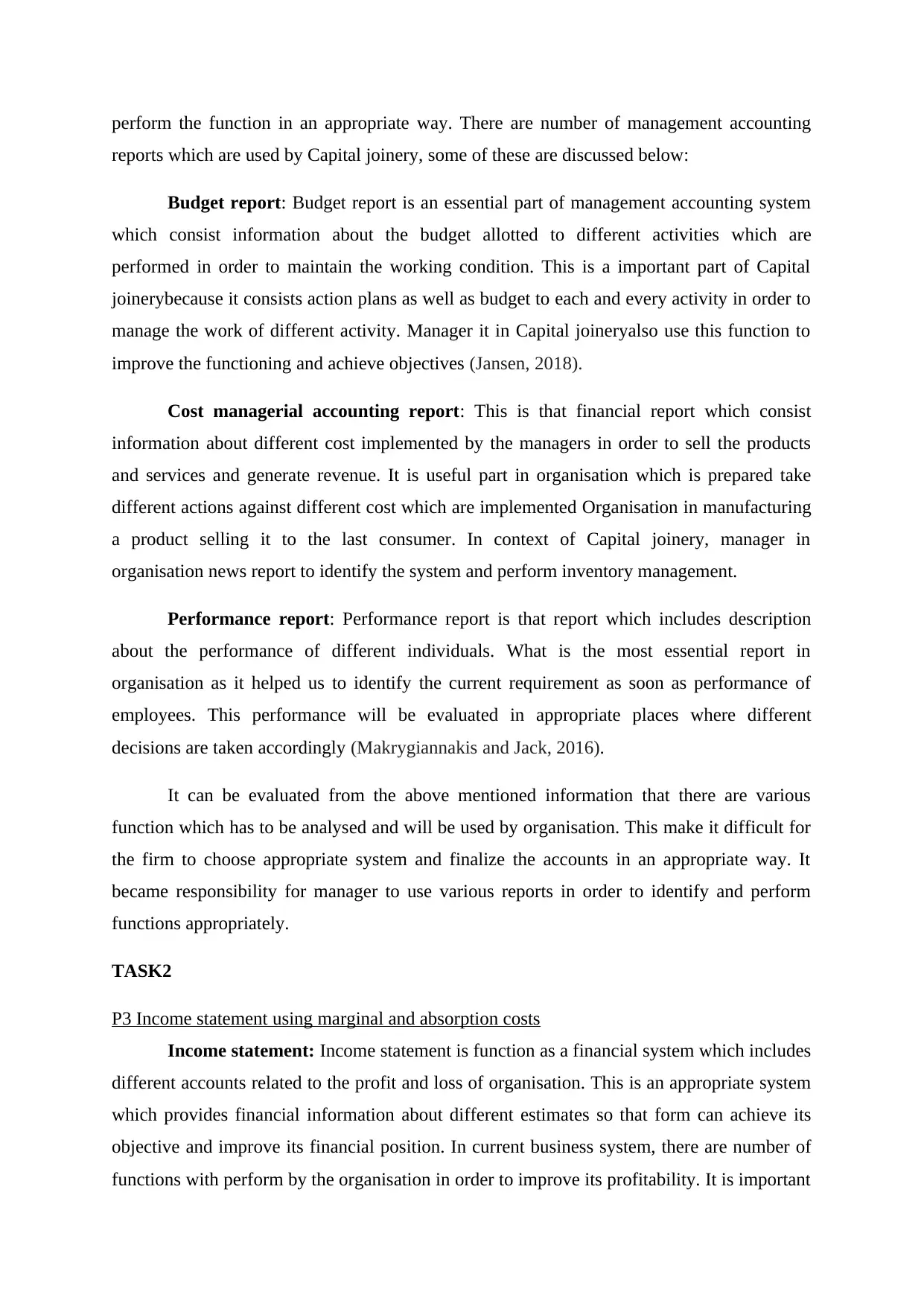

P3 Income statement using marginal and absorption costs

Income statement: Income statement is function as a financial system which includes

different accounts related to the profit and loss of organisation. This is an appropriate system

which provides financial information about different estimates so that form can achieve its

objective and improve its financial position. In current business system, there are number of

functions with perform by the organisation in order to improve its profitability. It is important

reports which are used by Capital joinery, some of these are discussed below:

Budget report: Budget report is an essential part of management accounting system

which consist information about the budget allotted to different activities which are

performed in order to maintain the working condition. This is a important part of Capital

joinerybecause it consists action plans as well as budget to each and every activity in order to

manage the work of different activity. Manager it in Capital joineryalso use this function to

improve the functioning and achieve objectives (Jansen, 2018).

Cost managerial accounting report: This is that financial report which consist

information about different cost implemented by the managers in order to sell the products

and services and generate revenue. It is useful part in organisation which is prepared take

different actions against different cost which are implemented Organisation in manufacturing

a product selling it to the last consumer. In context of Capital joinery, manager in

organisation news report to identify the system and perform inventory management.

Performance report: Performance report is that report which includes description

about the performance of different individuals. What is the most essential report in

organisation as it helped us to identify the current requirement as soon as performance of

employees. This performance will be evaluated in appropriate places where different

decisions are taken accordingly (Makrygiannakis and Jack, 2016).

It can be evaluated from the above mentioned information that there are various

function which has to be analysed and will be used by organisation. This make it difficult for

the firm to choose appropriate system and finalize the accounts in an appropriate way. It

became responsibility for manager to use various reports in order to identify and perform

functions appropriately.

TASK2

P3 Income statement using marginal and absorption costs

Income statement: Income statement is function as a financial system which includes

different accounts related to the profit and loss of organisation. This is an appropriate system

which provides financial information about different estimates so that form can achieve its

objective and improve its financial position. In current business system, there are number of

functions with perform by the organisation in order to improve its profitability. It is important

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

for organisation to identify the performance and functioning so that it can operate in an

appropriate way and identify the current requirements of profitability. Income statement of

organisation is based on the period so that organisation can prepare appropriate balance sheet

and represent a position to its stakeholders (Abernethy and Wallis, 2019).

Absorption cost: Absorption cost can be defined as that kind of managerial cost

which is related to the fixed and variable cost implemented by the organisation on the product

and has to be identified in order to analyse the price of the product. Absorption costing is

important parts or organisation as it helps in identifying and all those caused which are

absorbed by the product and has to be maintained. Absorption cost is also defined as a cost of

manufacturing per unit so that organisation can analyse the appropriate costing system

appropriate way and identify the current requirements of profitability. Income statement of

organisation is based on the period so that organisation can prepare appropriate balance sheet

and represent a position to its stakeholders (Abernethy and Wallis, 2019).

Absorption cost: Absorption cost can be defined as that kind of managerial cost

which is related to the fixed and variable cost implemented by the organisation on the product

and has to be identified in order to analyse the price of the product. Absorption costing is

important parts or organisation as it helps in identifying and all those caused which are

absorbed by the product and has to be maintained. Absorption cost is also defined as a cost of

manufacturing per unit so that organisation can analyse the appropriate costing system

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK3

P4 Merits and demerits of budgetary tools

There are a number of planning to switch can be used by an organisation in order to

achieve its objectives as well as perform the function of budgetary control. These planning

tools are helpful in making effective system which can be executed by the firm in order to

P4 Merits and demerits of budgetary tools

There are a number of planning to switch can be used by an organisation in order to

achieve its objectives as well as perform the function of budgetary control. These planning

tools are helpful in making effective system which can be executed by the firm in order to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

achieve better profitability and perform the function in group oriented behaviour. There are a

number of to switch can be used by Capital joinery. Some of these are discussed below:

Capital budgeting: Capital budgeting can be defined as that to which is used by the

organisation and order to investment appraisal. It is a planning process which is useful to the

organisation in determining whether the organisations long term investment in relation to

machineries replacement of machinery building a new plant new product and other research

program can be utilised or will be worthy to the organisation according to its capitalisation

structure (Taylor and Scapens, 2016). In context of Capital joinery, the system can be used by

organisation in order to educating its major capital and investment and expenditures by

identifying its management accounts and forming the function in an appropriate manner. This

is useful for organisation in identifying the capital budgeting investment and increasing the

value of forms in front of its stakeholders.

Advantages

The major advantages of using capital budgeting as a tool of budgetary planning is

that it help the organisation in providing assistance about understanding different risk

with are involved in investment made by firm as well as return on investment for

successful business operations.

One more benefit of this system to the organisation is related to identification of

estimate related to different investment and identifying best possible returns.

Disadvantage

Capital budgeting is useful for organisation in identifying various decisions and

managing the decisions in an appropriate way so that it can plan for long term but

there is no relevance technique to identify the business challenges and changes in

environment for long period which act as a disadvantage.

Capital budgeting is also an appropriate and various situations because it includes

number of assumptions where there is no shortage of fulfilment of these assumptions.

Cash budget: Cash budget is important school in budgetary control which is helpful

to the organisation in managing techniques as well as using appropriate flow of cash so that

firm can achieve its objective. In context of Capital joinery, it is using appropriate flow of

cash which is helpful to the organisation in managing the activities and achieving the

performance at battery level. This will also allow organisation to identify the current flow of

number of to switch can be used by Capital joinery. Some of these are discussed below:

Capital budgeting: Capital budgeting can be defined as that to which is used by the

organisation and order to investment appraisal. It is a planning process which is useful to the

organisation in determining whether the organisations long term investment in relation to

machineries replacement of machinery building a new plant new product and other research

program can be utilised or will be worthy to the organisation according to its capitalisation

structure (Taylor and Scapens, 2016). In context of Capital joinery, the system can be used by

organisation in order to educating its major capital and investment and expenditures by

identifying its management accounts and forming the function in an appropriate manner. This

is useful for organisation in identifying the capital budgeting investment and increasing the

value of forms in front of its stakeholders.

Advantages

The major advantages of using capital budgeting as a tool of budgetary planning is

that it help the organisation in providing assistance about understanding different risk

with are involved in investment made by firm as well as return on investment for

successful business operations.

One more benefit of this system to the organisation is related to identification of

estimate related to different investment and identifying best possible returns.

Disadvantage

Capital budgeting is useful for organisation in identifying various decisions and

managing the decisions in an appropriate way so that it can plan for long term but

there is no relevance technique to identify the business challenges and changes in

environment for long period which act as a disadvantage.

Capital budgeting is also an appropriate and various situations because it includes

number of assumptions where there is no shortage of fulfilment of these assumptions.

Cash budget: Cash budget is important school in budgetary control which is helpful

to the organisation in managing techniques as well as using appropriate flow of cash so that

firm can achieve its objective. In context of Capital joinery, it is using appropriate flow of

cash which is helpful to the organisation in managing the activities and achieving the

performance at battery level. This will also allow organisation to identify the current flow of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

cash within the firm so that it can manage the functions and identify the requirement of funds

in order to maintain liquidity (Phornlaphatrachakorn and Khajit, 2020).

Advantages

This system is useful for Organisation in order to identifying the current needs and

requirements of liquidity and when is the function according to the flow of cash.

One more advantage of using cash budget as a budgetary tool and Capital joineryis

that It helped the form in being resourceful by initiating regular flow of cash and

ensuring availability of liquidity in each and every department.

Disadvantage

Addition of using cash budget within an organisation is that there are a number of

records which has to be maintained by the organisation for using the cache which can

also lead to left of cash as well as misleading the transaction.

It is analysed from the mention information that there are various functions which are

related to budgetary control to an organisation and helpful in implementing a particular

situation the most effective tool which can be used by Capital joineryis capital budgeting.

This is Helpful to the organisation in identifying the future requirements as well as return on

investment so that form can achieve its objectives in a timely manner.

TASK4

P5 Financial problem and response of organization

Listen to the current corporate environment it is important for every organisation to

perform its functions and identify the needs and requirement to utilise the businessman dual

strategies and processes according to the social challenges and value of stakeholders. This

make it important for organisation to utilise its resources and function in an appropriate way

by managing its financial account to solve different financial problems (Pelz,, 2019). Under

this system, there are different financial problems which are faced by the organisations

working in this scenario. In context of Capital joinery, it is also facing number of financial

problems which impact on management of organisation. Some of these are Unplanned

expenses, Poor management of money, Late payments from clients and Reduces profits due

to lower productivity. The main issue which is faced by Capital joinery is related to using the

budgetary targets key performance indicators and various business activities. Financial

in order to maintain liquidity (Phornlaphatrachakorn and Khajit, 2020).

Advantages

This system is useful for Organisation in order to identifying the current needs and

requirements of liquidity and when is the function according to the flow of cash.

One more advantage of using cash budget as a budgetary tool and Capital joineryis

that It helped the form in being resourceful by initiating regular flow of cash and

ensuring availability of liquidity in each and every department.

Disadvantage

Addition of using cash budget within an organisation is that there are a number of

records which has to be maintained by the organisation for using the cache which can

also lead to left of cash as well as misleading the transaction.

It is analysed from the mention information that there are various functions which are

related to budgetary control to an organisation and helpful in implementing a particular

situation the most effective tool which can be used by Capital joineryis capital budgeting.

This is Helpful to the organisation in identifying the future requirements as well as return on

investment so that form can achieve its objectives in a timely manner.

TASK4

P5 Financial problem and response of organization

Listen to the current corporate environment it is important for every organisation to

perform its functions and identify the needs and requirement to utilise the businessman dual

strategies and processes according to the social challenges and value of stakeholders. This

make it important for organisation to utilise its resources and function in an appropriate way

by managing its financial account to solve different financial problems (Pelz,, 2019). Under

this system, there are different financial problems which are faced by the organisations

working in this scenario. In context of Capital joinery, it is also facing number of financial

problems which impact on management of organisation. Some of these are Unplanned

expenses, Poor management of money, Late payments from clients and Reduces profits due

to lower productivity. The main issue which is faced by Capital joinery is related to using the

budgetary targets key performance indicators and various business activities. Financial

governance is also faced by the organisation and impact on the functioning of organisation.

One more organisation which is facing these issues is HOUSEDEC. It also facing number of

financial problems in the current business environment where it can use different system in

order to meet the financial obligations.

Comparison of the company with other company is as follows in which both of them are

using management accounting to respond financial problems:

Management

accounting

technique

Capital joinery HOUSEDEC

Benchmarking In order to compare credit policies with

competitors and meet needs related to

management of credit period capital

joinery will use benchmarking.

In order to anticipate possibility of

lower profits, management in

Houcedec use benchmarking. This

helps in maintain position in business

firm.

Key

performance

indicators

This will help management in

identifying the reason behind the

function performed to reduces

possibility of sudden expenditures could

be reduced.

In order to identify the errors in

supply chain management,

management in firm use KPI.

Balance score

card

In order to deal with the problem

related lower profits. This is also used

in order to meet needs related to low

productivity. Here it helps in determine

the performance of all staff members

and provide them compensation

accordingly

This helps in managing performance

of employee in order to meet needs

and perform task in effective.

Activity based

costing

In order to create lack of funds for the

company as it can help to assign cost to

all the activities according to their

requirements is the technique which is

required to perform.

There are various activities that

possibility of overspending of budget

could be reduced by using this tool.

This helps in managing function and

costing in effective way.

One more organisation which is facing these issues is HOUSEDEC. It also facing number of

financial problems in the current business environment where it can use different system in

order to meet the financial obligations.

Comparison of the company with other company is as follows in which both of them are

using management accounting to respond financial problems:

Management

accounting

technique

Capital joinery HOUSEDEC

Benchmarking In order to compare credit policies with

competitors and meet needs related to

management of credit period capital

joinery will use benchmarking.

In order to anticipate possibility of

lower profits, management in

Houcedec use benchmarking. This

helps in maintain position in business

firm.

Key

performance

indicators

This will help management in

identifying the reason behind the

function performed to reduces

possibility of sudden expenditures could

be reduced.

In order to identify the errors in

supply chain management,

management in firm use KPI.

Balance score

card

In order to deal with the problem

related lower profits. This is also used

in order to meet needs related to low

productivity. Here it helps in determine

the performance of all staff members

and provide them compensation

accordingly

This helps in managing performance

of employee in order to meet needs

and perform task in effective.

Activity based

costing

In order to create lack of funds for the

company as it can help to assign cost to

all the activities according to their

requirements is the technique which is

required to perform.

There are various activities that

possibility of overspending of budget

could be reduced by using this tool.

This helps in managing function and

costing in effective way.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.