Management Accounting Report: Capital Journey Ltd Financial Analysis

VerifiedAdded on 2023/01/03

|15

|4522

|52

Report

AI Summary

This report provides a comprehensive analysis of management accounting practices, focusing on the case study of Capital Journey Ltd. It explores various management accounting systems, including inventory management, cost-volume-profit analysis, budgetary control, and cash budgeting. The report delves into different methods such as marginal costing and absorption costing, comparing their applications and implications. It also examines the advantages and disadvantages of different planning tools used for budgetary control within the organization. Furthermore, the report addresses how Capital Journey Ltd adapts its management accounting system to respond to financial problems, providing insights into financial reporting and decision-making processes. The analysis includes the production of financial reports and concludes with a summary of the key findings and recommendations for effective financial management.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION......................................................................................................................3

SCENARIO 1.............................................................................................................................3

Types of management accounting system..............................................................................3

Different methods of management accounting.......................................................................6

Advantages and disadvantages of different type of planning tools for budgetary control\....8

Comparing how organization adapts the management accounting system in order to

respond to financial problems................................................................................................9

SCENARIO 2...........................................................................................................................10

Producing financial report....................................................................................................10

CONCLUSION........................................................................................................................14

REFERENCES.........................................................................................................................16

INTRODUCTION......................................................................................................................3

SCENARIO 1.............................................................................................................................3

Types of management accounting system..............................................................................3

Different methods of management accounting.......................................................................6

Advantages and disadvantages of different type of planning tools for budgetary control\....8

Comparing how organization adapts the management accounting system in order to

respond to financial problems................................................................................................9

SCENARIO 2...........................................................................................................................10

Producing financial report....................................................................................................10

CONCLUSION........................................................................................................................14

REFERENCES.........................................................................................................................16

INTRODUCTION

Management accounting is all about reporting the financial transactions associated

with the organisation (Schaltegger, 2018). This is about to report the financial position

associated with the organisation. This report is based on the case study of Capital Journey Ltd

in respect to the management of the financial transactions of organisation. This project would

assess various elements related to the accounting of organisation. Henceforth, report will

emphasis over various types of management accounting system associated with the

organisation. Various methods associated with the management accounting system can be

projected in this report. Income statement with the support of different methods of

management accounting will be projected briefly in this project. Advantages and

disadvantages associated with the different planning tools part of the organisation.

Furthermore, project will demonstrate the fact how management accounting would respond to

various financial problems associated with the organisation. All different areas associated

with the management accounting would demonstrate in this project.

SCENARIO 1

Types of management accounting system

Management accounting is comprises with various systems that involve different

methodologies and techniques to support the best form of representation of the company’s

books of accounts. Management accounting is a methodology that delivers the better

presentation of the financial reporting of the organisation. The reporting done in the

management accounting project about all key information in respect to the user of the

financial statements (NGUYEN and LE, 2020). Different methodologies and tools and

techniques that support in the management accounting provide the clinical information to

user of the financial statement. They get to know about all different information about the

financial position of organisation. All these various technique support the organisation to

represent all different critical areas to represent the financial position of organisation in the

best way possible. All different techniques and methods part of the management accounting

can be projected in the following points.

Inventory management system

This is also a major type of management accounting system used by Capital Joinery. Under

this management accounting system all the requirement and application of the inventory used

Management accounting is all about reporting the financial transactions associated

with the organisation (Schaltegger, 2018). This is about to report the financial position

associated with the organisation. This report is based on the case study of Capital Journey Ltd

in respect to the management of the financial transactions of organisation. This project would

assess various elements related to the accounting of organisation. Henceforth, report will

emphasis over various types of management accounting system associated with the

organisation. Various methods associated with the management accounting system can be

projected in this report. Income statement with the support of different methods of

management accounting will be projected briefly in this project. Advantages and

disadvantages associated with the different planning tools part of the organisation.

Furthermore, project will demonstrate the fact how management accounting would respond to

various financial problems associated with the organisation. All different areas associated

with the management accounting would demonstrate in this project.

SCENARIO 1

Types of management accounting system

Management accounting is comprises with various systems that involve different

methodologies and techniques to support the best form of representation of the company’s

books of accounts. Management accounting is a methodology that delivers the better

presentation of the financial reporting of the organisation. The reporting done in the

management accounting project about all key information in respect to the user of the

financial statements (NGUYEN and LE, 2020). Different methodologies and tools and

techniques that support in the management accounting provide the clinical information to

user of the financial statement. They get to know about all different information about the

financial position of organisation. All these various technique support the organisation to

represent all different critical areas to represent the financial position of organisation in the

best way possible. All different techniques and methods part of the management accounting

can be projected in the following points.

Inventory management system

This is also a major type of management accounting system used by Capital Joinery. Under

this management accounting system all the requirement and application of the inventory used

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

within the company. The major reason underlying this fact is that the inventory is the most

essential aspect of the business and for this its proper availability is very important. Thus, for

this Capital Joinery uses the inventory management system in order to have all the records of

the inventory coming to business and going out in form of finished goods. Further if the

inventory will not be managed in effective manner then this will have a great impact over the

overall working of the company. This system is used on the basis of the nature of

organisation, resources of the business entity, information quality and many such factors.

Inventory management system requires strong system of recording the inventory.

Management also must favour the infrastructure development so that proper recording and

monitoring can be conducted in the inventory records maintenance.

Cost volume profit analysis

Cost volume profit analysis formerly known as the breakeven point. This is the

position in the financial records of company that denote no profit no loss situation in context

to the organisation. It is essential for the organisation to achieve tis position in the

organisation as early as possible to denote the financial capability of the organisation. At the

Cost volume profit point in operations company get to recover all the expenditure the

organisation has entertained against the business operations by the organisation (Taylor and

Scapens, 2016). It is a critical technique that denote the exact position in organisation which

demonstrate about the point where the organisation has been capable enough to deliver the

outcomes in the business operations and functions to reach the point where company get to

recover all expenditure it required to incurred in the organisation to reach the point where the

company would contain no profit and no loss situation in operations. Break even point

company calculate in both the form total number of unit company needed to sail or in form of

total amount of turnover company need to address in the operations to achieve the maximum

level of outcomes against the business operations entertained by the company (Cuzdriorean,

2017). Cost volume analysis is a key point in the company as it denotes the reach ability of

the operations of organisation. Every time company deliver a product in target market at first

company try to reach the Cost volume profit point so that overall cost incurred to produce and

deliver the final service can be recovered by the organisation. Beyond this point company get

to make profitability against the business operations entertained by the organisation. It is the

priority of the business functions of organisation to reach at this point in against to deliver the

business functions at the organisation level. In order to calculate and identify about the

essential aspect of the business and for this its proper availability is very important. Thus, for

this Capital Joinery uses the inventory management system in order to have all the records of

the inventory coming to business and going out in form of finished goods. Further if the

inventory will not be managed in effective manner then this will have a great impact over the

overall working of the company. This system is used on the basis of the nature of

organisation, resources of the business entity, information quality and many such factors.

Inventory management system requires strong system of recording the inventory.

Management also must favour the infrastructure development so that proper recording and

monitoring can be conducted in the inventory records maintenance.

Cost volume profit analysis

Cost volume profit analysis formerly known as the breakeven point. This is the

position in the financial records of company that denote no profit no loss situation in context

to the organisation. It is essential for the organisation to achieve tis position in the

organisation as early as possible to denote the financial capability of the organisation. At the

Cost volume profit point in operations company get to recover all the expenditure the

organisation has entertained against the business operations by the organisation (Taylor and

Scapens, 2016). It is a critical technique that denote the exact position in organisation which

demonstrate about the point where the organisation has been capable enough to deliver the

outcomes in the business operations and functions to reach the point where company get to

recover all expenditure it required to incurred in the organisation to reach the point where the

company would contain no profit and no loss situation in operations. Break even point

company calculate in both the form total number of unit company needed to sail or in form of

total amount of turnover company need to address in the operations to achieve the maximum

level of outcomes against the business operations entertained by the company (Cuzdriorean,

2017). Cost volume analysis is a key point in the company as it denotes the reach ability of

the operations of organisation. Every time company deliver a product in target market at first

company try to reach the Cost volume profit point so that overall cost incurred to produce and

deliver the final service can be recovered by the organisation. Beyond this point company get

to make profitability against the business operations entertained by the organisation. It is the

priority of the business functions of organisation to reach at this point in against to deliver the

business functions at the organisation level. In order to calculate and identify about the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

breakeven point in units company need to compare fixed cost with the contribution per unit.

In case company require to identify the breakeven point in amount than it has to compare the

fixed cost entertained by the organisation in the respective time with the profit volume ratio

of the organisation. In both the cases result will remain the same. It is only a different ways to

represent the overall outcomes of operations. Once the organisation has been capable enough

to reach the Cost volume profit point than it can form further strategies and policies to

enhance and boost the overall profitability of the organisation. This system requires a

favourable nature of the management to apply this approach. Many times progressive

leadership seek this approach to implement in operations.

Budgetary control

Budgetary control is another key technique that is a part of the operations of the

company. Management accounting methodology comprises with different techniques and

methods to achieve the maximum possible outcomes of the business functions entertained by

the organisation. Budgetary control is a technique which involve preparing the budget,

coordinate about the budget in all different functional department of the organisation,

compare the actual performance of organisation with the estimation made in the budget of

company and to assess the performance of organization to form future budgets (Fleischman

and McLean, 2020). This is a clinical approach part of management accounting that denote

the different aspecs that can support the organisation to deliver the maximum level of

outcomes against the business operations entertained by the organisation. Budget are off

different types that are idealised as the fixed budget, flexible budget, cash budget and various

other types of budget. This is a key practice that can be indulged with any of the operation of

organisation. Management required to be positive enough to apply this approach. This also

favour the organisation to sustain an effective control over projection and also needed strong

system to identify the cost required in performing specific operations.

Cash budget

Cash budget is another approach that is involved in the management accounting

methods. This budget control the liquidity position of the organisation. On the basis of the

expected future cash requirements and needs of the Capital Journey Ltd this budget is

prepared. Assessment in respect to the cash resources company require to channelizes the

business operation in the respective financial year this budget is prepared by company

(Johnstone, 2020). Cash budget control the liquidity position of the organisation.

In case company require to identify the breakeven point in amount than it has to compare the

fixed cost entertained by the organisation in the respective time with the profit volume ratio

of the organisation. In both the cases result will remain the same. It is only a different ways to

represent the overall outcomes of operations. Once the organisation has been capable enough

to reach the Cost volume profit point than it can form further strategies and policies to

enhance and boost the overall profitability of the organisation. This system requires a

favourable nature of the management to apply this approach. Many times progressive

leadership seek this approach to implement in operations.

Budgetary control

Budgetary control is another key technique that is a part of the operations of the

company. Management accounting methodology comprises with different techniques and

methods to achieve the maximum possible outcomes of the business functions entertained by

the organisation. Budgetary control is a technique which involve preparing the budget,

coordinate about the budget in all different functional department of the organisation,

compare the actual performance of organisation with the estimation made in the budget of

company and to assess the performance of organization to form future budgets (Fleischman

and McLean, 2020). This is a clinical approach part of management accounting that denote

the different aspecs that can support the organisation to deliver the maximum level of

outcomes against the business operations entertained by the organisation. Budget are off

different types that are idealised as the fixed budget, flexible budget, cash budget and various

other types of budget. This is a key practice that can be indulged with any of the operation of

organisation. Management required to be positive enough to apply this approach. This also

favour the organisation to sustain an effective control over projection and also needed strong

system to identify the cost required in performing specific operations.

Cash budget

Cash budget is another approach that is involved in the management accounting

methods. This budget control the liquidity position of the organisation. On the basis of the

expected future cash requirements and needs of the Capital Journey Ltd this budget is

prepared. Assessment in respect to the cash resources company require to channelizes the

business operation in the respective financial year this budget is prepared by company

(Johnstone, 2020). Cash budget control the liquidity position of the organisation.

The above mentioned tools are a key techniques utilised in management accounting

practice. With the support of all these tools bets level of accounting management is

conducted at the organisation level. Financial stability is among the key requirement part of

the organisation and all these tools support the Capital Journey Ltd to address the financial

stability that is desired by the organisation in against to the business operations entertained by

the company.

Different methods of management accounting

Management accounting is comprises with different methods that can be projected in

marginal costing technique and absorption costing technique. All these techniques can be

projected in the following manner.

Budgetary report

This is also a management accounting report which involves the details relating to all the

budgets which are planned and made by the company in order to manage the performance of

the company. Thus for this Capital Joinery makes the use of all the budgets and reports them

in these budgetary reporting. This is done in order to make and have a record of all the

changes and these records are also being used in the future.

Inventory reports

This is a type of report in which the company records all the transaction relating to the

inventory. The inventory is the most important thing for the company as if this will not be

managed then the whole working will be impacted. Further Capital Joinery uses the inventory

report in order to record all the transaction relating to the inventory and this assist the

company to have proper knowledge of inventory coming to business and going out from the

business.

Marginal costing

Marginal costing is all about comparing cost with quantity produced by the company.

This is an effective way to report the financial transactions entertained by the company in

comparative manner where company get to match the complete balance in between the cost

and quantity produced by the organisation to deliver the maximum level of outcomes against

the business operations entertained by the company. This method charges the variable cost to

evaluate the financial outcomes of the organisation (Drury, 2018). This technique support the

practice. With the support of all these tools bets level of accounting management is

conducted at the organisation level. Financial stability is among the key requirement part of

the organisation and all these tools support the Capital Journey Ltd to address the financial

stability that is desired by the organisation in against to the business operations entertained by

the company.

Different methods of management accounting

Management accounting is comprises with different methods that can be projected in

marginal costing technique and absorption costing technique. All these techniques can be

projected in the following manner.

Budgetary report

This is also a management accounting report which involves the details relating to all the

budgets which are planned and made by the company in order to manage the performance of

the company. Thus for this Capital Joinery makes the use of all the budgets and reports them

in these budgetary reporting. This is done in order to make and have a record of all the

changes and these records are also being used in the future.

Inventory reports

This is a type of report in which the company records all the transaction relating to the

inventory. The inventory is the most important thing for the company as if this will not be

managed then the whole working will be impacted. Further Capital Joinery uses the inventory

report in order to record all the transaction relating to the inventory and this assist the

company to have proper knowledge of inventory coming to business and going out from the

business.

Marginal costing

Marginal costing is all about comparing cost with quantity produced by the company.

This is an effective way to report the financial transactions entertained by the company in

comparative manner where company get to match the complete balance in between the cost

and quantity produced by the organisation to deliver the maximum level of outcomes against

the business operations entertained by the company. This method charges the variable cost to

evaluate the financial outcomes of the organisation (Drury, 2018). This technique support the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

organization to evaluate the best level of outcomes against the business operations entertained

by the organisation with the support of variable nature cost entertained by the Capital Journey

Ltd where as the fixed cost is completely write off in this technique. This method of

management accounting work on the fundamentals that fixed cost is not directly associated

with the overall production of the products so it must not be considered while calculating the

overall profitability against the trading operation of company. This method completely

depends upon the variable nature of cost that directly involved in making the product ready to

sail to final customer in market.

Absorption costing

Absorption costing method of management accounting accumulates all types of cost

that has contributed in any manner in order to make the product ready to sail. This is a key

method of management accounting that support the organisation to deliver the profitability

projection on the fundamentals that accounting methodology must justify with the actual

profitability of the company. If the accounting do not project the actual level of outcomes

company is entertaining against the business operations entertained by the company than it is

not convenient and effective (Phornlaphatrachakorn and Khajit, 2020). This technique

involve all types of cost direct material, direct labour and all other types of cost that has

contributed in the overall production of the finished products that company can sail to its

potential level of customer in market.

The above methods are the two different methodologies part of the management

accounting. All different techniques and methods contain its own way to reflect the business

outcomes of the organisation. Management of Capital Journey Ltd make all decisions on the

basis of the outcomes represent by all different techniques so that bets level of decisions

against the business operations of organisation can entertain by the company.

Advantages and disadvantages of different type of planning tools for budgetary control\

There are different types of planning tools which assist the company in managing the

working and operation of the company to a great extent. This is particularly because of the

reason that these planning tools assist and guide the people in managing the business in

effective and efficient manner (Guo and Yang, 2018). For the company Capital Joinery there

are different types of tools used for planning the company. This is particularly because of the

reason that when the company will effectively make the use of these planning tools then this

will assist the company in managing their performance and the operations. The major reason

by the organisation with the support of variable nature cost entertained by the Capital Journey

Ltd where as the fixed cost is completely write off in this technique. This method of

management accounting work on the fundamentals that fixed cost is not directly associated

with the overall production of the products so it must not be considered while calculating the

overall profitability against the trading operation of company. This method completely

depends upon the variable nature of cost that directly involved in making the product ready to

sail to final customer in market.

Absorption costing

Absorption costing method of management accounting accumulates all types of cost

that has contributed in any manner in order to make the product ready to sail. This is a key

method of management accounting that support the organisation to deliver the profitability

projection on the fundamentals that accounting methodology must justify with the actual

profitability of the company. If the accounting do not project the actual level of outcomes

company is entertaining against the business operations entertained by the company than it is

not convenient and effective (Phornlaphatrachakorn and Khajit, 2020). This technique

involve all types of cost direct material, direct labour and all other types of cost that has

contributed in the overall production of the finished products that company can sail to its

potential level of customer in market.

The above methods are the two different methodologies part of the management

accounting. All different techniques and methods contain its own way to reflect the business

outcomes of the organisation. Management of Capital Journey Ltd make all decisions on the

basis of the outcomes represent by all different techniques so that bets level of decisions

against the business operations of organisation can entertain by the company.

Advantages and disadvantages of different type of planning tools for budgetary control\

There are different types of planning tools which assist the company in managing the

working and operation of the company to a great extent. This is particularly because of the

reason that these planning tools assist and guide the people in managing the business in

effective and efficient manner (Guo and Yang, 2018). For the company Capital Joinery there

are different types of tools used for planning the company. This is particularly because of the

reason that when the company will effectively make the use of these planning tools then this

will assist the company in managing their performance and the operations. The major reason

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

for this is that these planning tool for budgetary control are used in order to make the

performance of the company in better and effective manner. Thus, for this the company

makes the use of following different types of budgetary planning tools which are as follows-

Operational budget- this is a type of budget which assist the company in managing the

expenses and income which are being generated with the day to day business of the company.

This is particularly being used by the company in order to make the estimation of the daily

expense and the future income which the company Capital Joinery can have with assistance

of using this budget.

Advantages

The major advantage of using this budget by Capital Joinery is that this will give an

idea to the company that how their work will be done and what will be there expected income

and expense due to that particular operational activity. Further another major benefit of using

this operational budget is that these are very easy to prepare and also easy to understand. Any

person can easily understand by looking at the budget that what will be the operational

expenses and income which the company might face in order to doing the daily activities of

business (Soares and et.al., 2019).

Disadvantages

The major drawback of using this budget by Capital Joinery is that this is very time

consuming to prepare the budget and this takes up a lot of time of the budget maker. Thus,

because of this reason this is very time consuming and involve a lot of efforts of the maker of

budget as well. In addition to this another major drawback is that it is not possible that all the

expected things happen in the same manner as the future is unpredictable and it is not static.

Thus, this creates problems for the budget maker as there are many different types of

problems and changes taking place in the external environment (OYEBODE, 2018).

Zero- based budgeting- this is a type of another planning tool for the budgetary control

which is assistive for the company in order to manage the working of the company. Under

this Capital Joinery uses this technique in order to make the budget from a scratch that is

from zero. This is a technique of budgeting within which all the expenses of the company are

identified from the starting that is from the beginning in every new financial year. This is

particularly because of the reason that under this method the Capital Joinery makes the

budget from the scratch. In simple terms the company does not involve the use of previous

budgets as the base for making the new budgets. Rather this involves making the whole of the

budget from the starting that is from initial stage.

Advantages

performance of the company in better and effective manner. Thus, for this the company

makes the use of following different types of budgetary planning tools which are as follows-

Operational budget- this is a type of budget which assist the company in managing the

expenses and income which are being generated with the day to day business of the company.

This is particularly being used by the company in order to make the estimation of the daily

expense and the future income which the company Capital Joinery can have with assistance

of using this budget.

Advantages

The major advantage of using this budget by Capital Joinery is that this will give an

idea to the company that how their work will be done and what will be there expected income

and expense due to that particular operational activity. Further another major benefit of using

this operational budget is that these are very easy to prepare and also easy to understand. Any

person can easily understand by looking at the budget that what will be the operational

expenses and income which the company might face in order to doing the daily activities of

business (Soares and et.al., 2019).

Disadvantages

The major drawback of using this budget by Capital Joinery is that this is very time

consuming to prepare the budget and this takes up a lot of time of the budget maker. Thus,

because of this reason this is very time consuming and involve a lot of efforts of the maker of

budget as well. In addition to this another major drawback is that it is not possible that all the

expected things happen in the same manner as the future is unpredictable and it is not static.

Thus, this creates problems for the budget maker as there are many different types of

problems and changes taking place in the external environment (OYEBODE, 2018).

Zero- based budgeting- this is a type of another planning tool for the budgetary control

which is assistive for the company in order to manage the working of the company. Under

this Capital Joinery uses this technique in order to make the budget from a scratch that is

from zero. This is a technique of budgeting within which all the expenses of the company are

identified from the starting that is from the beginning in every new financial year. This is

particularly because of the reason that under this method the Capital Joinery makes the

budget from the scratch. In simple terms the company does not involve the use of previous

budgets as the base for making the new budgets. Rather this involves making the whole of the

budget from the starting that is from initial stage.

Advantages

The major advantage of ZBB to Capital Joinery is that this method is accurate method

for the making of the budget as in this the company does not take any assumption or the data

based in the last or previous budget. Another major benefit of using this method of planning

tool is that this involves the reduction in the redundant activities. This means that this

includes the identification of the opportunities of doing the work in more cost effective

methods.

Disadvantages

The major drawback of this method is that this type of planning tools involve a lot of

expertise and for this the company need to hire some experts in order to make these budgets

(Zero Based Budgeting Meaning and Definition, 2020). Furthermore, another major

drawback of this planning tool is that when this also involves a lot of time for making this

budget as there is not any base for the company to use it as base. Thus, this involves a lot of

time to make the budgets.

Comparing how organization adapts the management accounting system in order to respond

to financial problems

Within the business there are many different types of financial problems which are

being encountered by the companies. The financial problem is the ones which drives the

company in some problem or issues which involves the money within the company. there are

many different types of the financial problem like not proper allocation of money, issues in

management of the finance, sudden increase in market value of products, less knowledge of

the use of finance within the business and many other financial problems. The business

operates in the external environment which involves many different types of problem which

are financial and non- financial problem and the company has to deal with these problems in

much effective manner. Thus, for this it is very important for the company to make the

effective use of the management accounting system which are discussed as follows-

Benchmarking- this is a model or tool which involve the use of setting up the

standards from the industry within which the company is operating (Kharlamova and et.al.,

2020). Further the company compares the performance of the company with the best

competitor within the industry. Thus, this assists the company in managing the performance

of its own by comparing the performance with that of the other competitor within the

company.

KPI- this is referred to as the Key Performance Indicator and this is a tool which

assists the company in managing the performance of the company. Under this method Capital

for the making of the budget as in this the company does not take any assumption or the data

based in the last or previous budget. Another major benefit of using this method of planning

tool is that this involves the reduction in the redundant activities. This means that this

includes the identification of the opportunities of doing the work in more cost effective

methods.

Disadvantages

The major drawback of this method is that this type of planning tools involve a lot of

expertise and for this the company need to hire some experts in order to make these budgets

(Zero Based Budgeting Meaning and Definition, 2020). Furthermore, another major

drawback of this planning tool is that when this also involves a lot of time for making this

budget as there is not any base for the company to use it as base. Thus, this involves a lot of

time to make the budgets.

Comparing how organization adapts the management accounting system in order to respond

to financial problems

Within the business there are many different types of financial problems which are

being encountered by the companies. The financial problem is the ones which drives the

company in some problem or issues which involves the money within the company. there are

many different types of the financial problem like not proper allocation of money, issues in

management of the finance, sudden increase in market value of products, less knowledge of

the use of finance within the business and many other financial problems. The business

operates in the external environment which involves many different types of problem which

are financial and non- financial problem and the company has to deal with these problems in

much effective manner. Thus, for this it is very important for the company to make the

effective use of the management accounting system which are discussed as follows-

Benchmarking- this is a model or tool which involve the use of setting up the

standards from the industry within which the company is operating (Kharlamova and et.al.,

2020). Further the company compares the performance of the company with the best

competitor within the industry. Thus, this assists the company in managing the performance

of its own by comparing the performance with that of the other competitor within the

company.

KPI- this is referred to as the Key Performance Indicator and this is a tool which

assists the company in managing the performance of the company. Under this method Capital

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

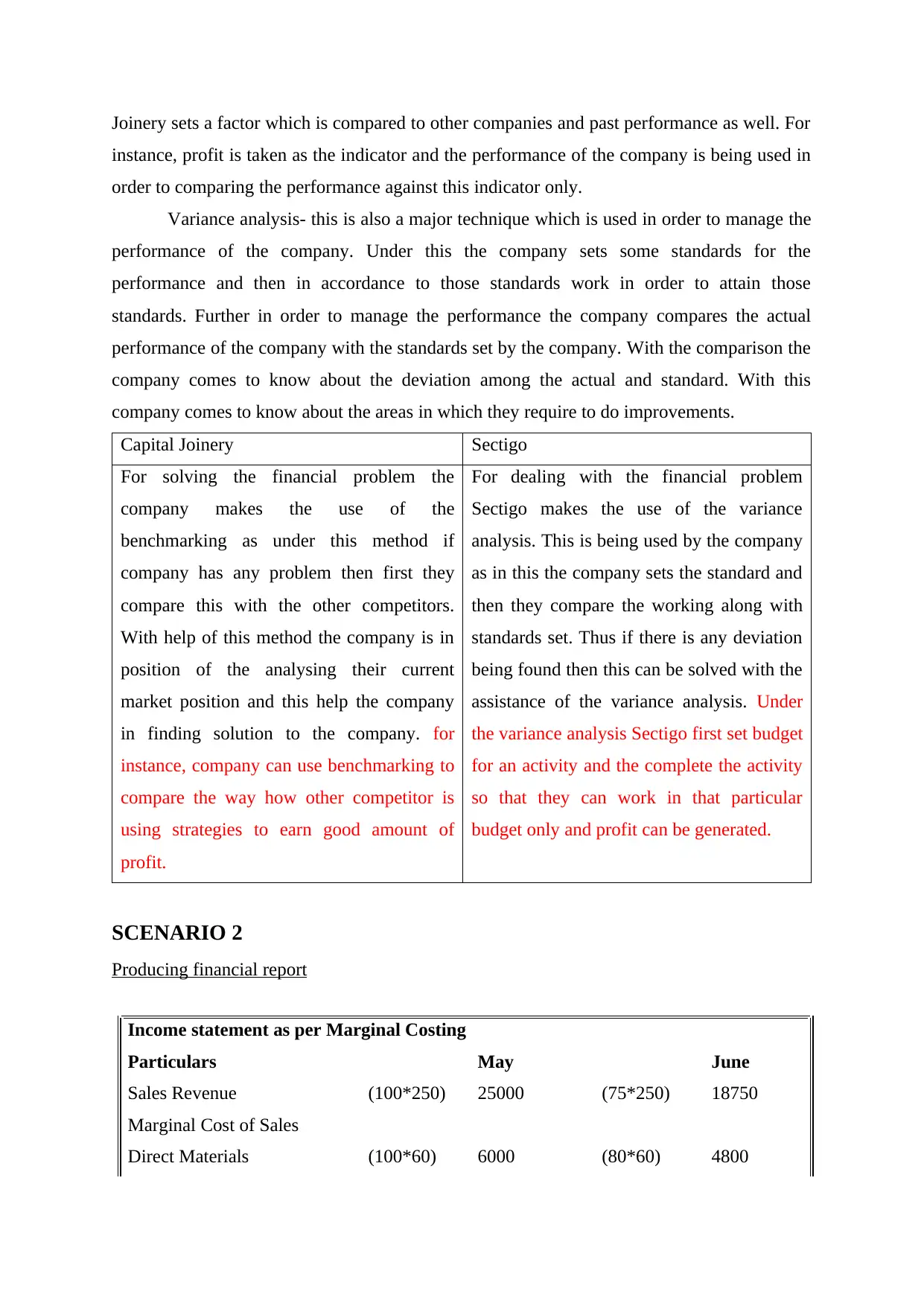

Joinery sets a factor which is compared to other companies and past performance as well. For

instance, profit is taken as the indicator and the performance of the company is being used in

order to comparing the performance against this indicator only.

Variance analysis- this is also a major technique which is used in order to manage the

performance of the company. Under this the company sets some standards for the

performance and then in accordance to those standards work in order to attain those

standards. Further in order to manage the performance the company compares the actual

performance of the company with the standards set by the company. With the comparison the

company comes to know about the deviation among the actual and standard. With this

company comes to know about the areas in which they require to do improvements.

Capital Joinery Sectigo

For solving the financial problem the

company makes the use of the

benchmarking as under this method if

company has any problem then first they

compare this with the other competitors.

With help of this method the company is in

position of the analysing their current

market position and this help the company

in finding solution to the company. for

instance, company can use benchmarking to

compare the way how other competitor is

using strategies to earn good amount of

profit.

For dealing with the financial problem

Sectigo makes the use of the variance

analysis. This is being used by the company

as in this the company sets the standard and

then they compare the working along with

standards set. Thus if there is any deviation

being found then this can be solved with the

assistance of the variance analysis. Under

the variance analysis Sectigo first set budget

for an activity and the complete the activity

so that they can work in that particular

budget only and profit can be generated.

SCENARIO 2

Producing financial report

Income statement as per Marginal Costing

Particulars May June

Sales Revenue (100*250) 25000 (75*250) 18750

Marginal Cost of Sales

Direct Materials (100*60) 6000 (80*60) 4800

instance, profit is taken as the indicator and the performance of the company is being used in

order to comparing the performance against this indicator only.

Variance analysis- this is also a major technique which is used in order to manage the

performance of the company. Under this the company sets some standards for the

performance and then in accordance to those standards work in order to attain those

standards. Further in order to manage the performance the company compares the actual

performance of the company with the standards set by the company. With the comparison the

company comes to know about the deviation among the actual and standard. With this

company comes to know about the areas in which they require to do improvements.

Capital Joinery Sectigo

For solving the financial problem the

company makes the use of the

benchmarking as under this method if

company has any problem then first they

compare this with the other competitors.

With help of this method the company is in

position of the analysing their current

market position and this help the company

in finding solution to the company. for

instance, company can use benchmarking to

compare the way how other competitor is

using strategies to earn good amount of

profit.

For dealing with the financial problem

Sectigo makes the use of the variance

analysis. This is being used by the company

as in this the company sets the standard and

then they compare the working along with

standards set. Thus if there is any deviation

being found then this can be solved with the

assistance of the variance analysis. Under

the variance analysis Sectigo first set budget

for an activity and the complete the activity

so that they can work in that particular

budget only and profit can be generated.

SCENARIO 2

Producing financial report

Income statement as per Marginal Costing

Particulars May June

Sales Revenue (100*250) 25000 (75*250) 18750

Marginal Cost of Sales

Direct Materials (100*60) 6000 (80*60) 4800

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Direct Labour (100*40) 4000 (80*40) 3200

Variable sales commission

(25000*2%

) 500

(18750*2%

) 375

Variable Production

Overheads (100*20) 2000 (80*20) 1600

12500 9975

Add:

Opening Stock 0 0

Less:

Closing Stock 0 (5*120) 600

12500 9375

Contribution 12500 9375

Fixed production overheads 2000 2400

Fixed selling cost 1000 1000

Fixed administration cost 3000 3000

Net Income 6500 3175

Income statement as per Absorption Costing

Particulars May June

Sales Revenue (100*250) 25000 (75*250) 18750

Cost of Sales

Direct Materials (100*60) 6000 (80*60) 4800

Direct Labour (100*40) 4000 (80*40) 3200

Variable Production

Overheads (100*20) 2000 (80*20) 1600

Fixed production overheads (100*20) 2000 (100*20) 2000

14000 10800

Add:

Opening Stock 0 0

Less:

Variable sales commission

(25000*2%

) 500

(18750*2%

) 375

Variable Production

Overheads (100*20) 2000 (80*20) 1600

12500 9975

Add:

Opening Stock 0 0

Less:

Closing Stock 0 (5*120) 600

12500 9375

Contribution 12500 9375

Fixed production overheads 2000 2400

Fixed selling cost 1000 1000

Fixed administration cost 3000 3000

Net Income 6500 3175

Income statement as per Absorption Costing

Particulars May June

Sales Revenue (100*250) 25000 (75*250) 18750

Cost of Sales

Direct Materials (100*60) 6000 (80*60) 4800

Direct Labour (100*40) 4000 (80*40) 3200

Variable Production

Overheads (100*20) 2000 (80*20) 1600

Fixed production overheads (100*20) 2000 (100*20) 2000

14000 10800

Add:

Opening Stock 0 0

Less:

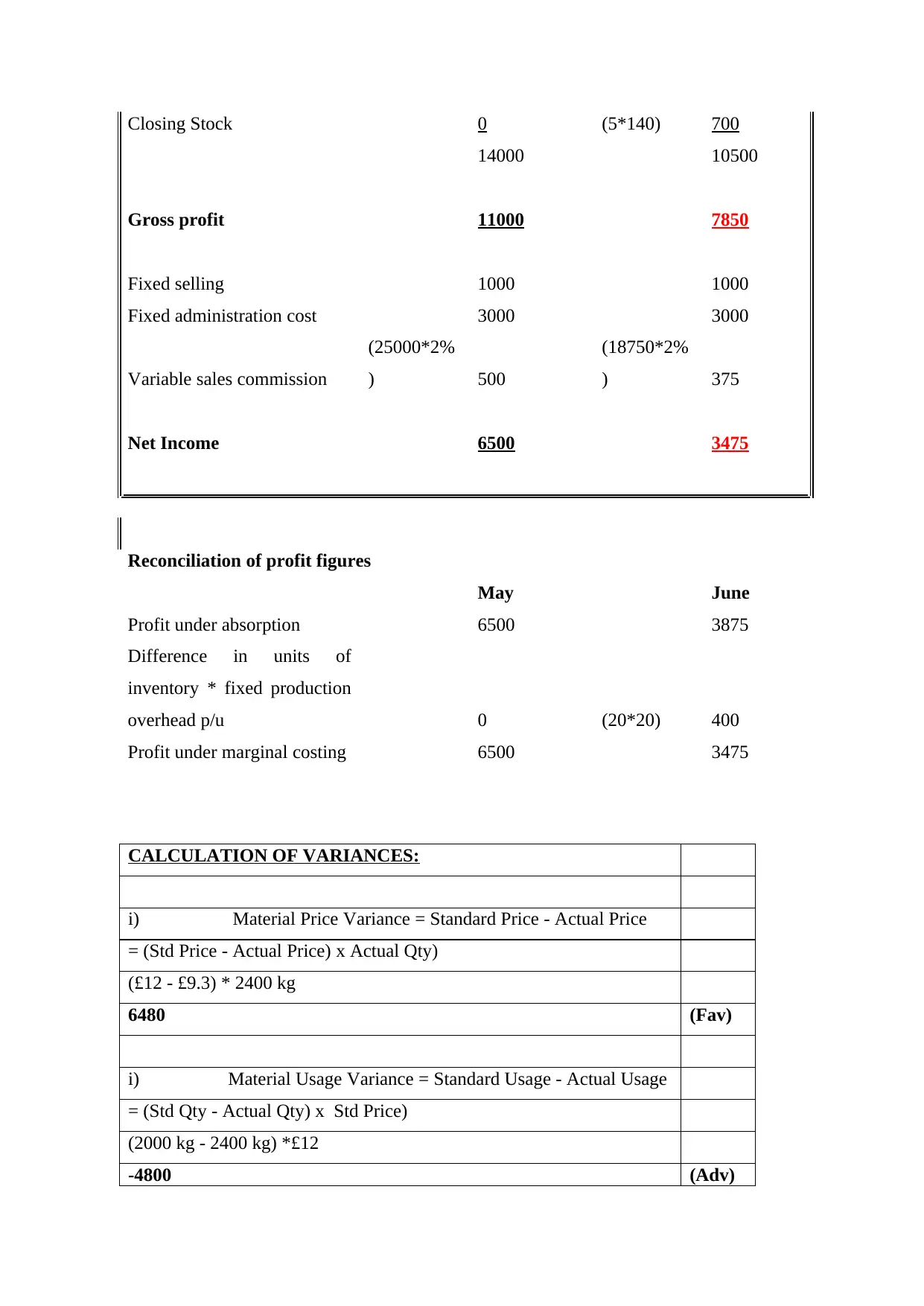

Closing Stock 0 (5*140) 700

14000 10500

Gross profit 11000 7850

Fixed selling 1000 1000

Fixed administration cost 3000 3000

Variable sales commission

(25000*2%

) 500

(18750*2%

) 375

Net Income 6500 3475

Reconciliation of profit figures

May June

Profit under absorption 6500 3875

Difference in units of

inventory * fixed production

overhead p/u 0 (20*20) 400

Profit under marginal costing 6500 3475

CALCULATION OF VARIANCES:

i) Material Price Variance = Standard Price - Actual Price

= (Std Price - Actual Price) x Actual Qty)

(£12 - £9.3) * 2400 kg

6480 (Fav)

i) Material Usage Variance = Standard Usage - Actual Usage

= (Std Qty - Actual Qty) x Std Price)

(2000 kg - 2400 kg) *£12

-4800 (Adv)

14000 10500

Gross profit 11000 7850

Fixed selling 1000 1000

Fixed administration cost 3000 3000

Variable sales commission

(25000*2%

) 500

(18750*2%

) 375

Net Income 6500 3475

Reconciliation of profit figures

May June

Profit under absorption 6500 3875

Difference in units of

inventory * fixed production

overhead p/u 0 (20*20) 400

Profit under marginal costing 6500 3475

CALCULATION OF VARIANCES:

i) Material Price Variance = Standard Price - Actual Price

= (Std Price - Actual Price) x Actual Qty)

(£12 - £9.3) * 2400 kg

6480 (Fav)

i) Material Usage Variance = Standard Usage - Actual Usage

= (Std Qty - Actual Qty) x Std Price)

(2000 kg - 2400 kg) *£12

-4800 (Adv)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.