Capital Market Portfolio Report: Investment Strategy and Evaluation

VerifiedAdded on 2020/06/06

|15

|4056

|119

Report

AI Summary

This report presents a comprehensive analysis of a capital market portfolio, focusing on investment strategies, risk management, and return optimization. The report begins with an introduction to capital markets and the rationale behind the selection of securities and bonds, emphasizing diversification and risk mitigation. It then delves into the evaluation and application of investment theory, including investment styles, asset allocation, and the efficient market hypothesis. The report provides detailed financial analysis of selected assets, including Diageo Plc, Astra Zeneca, Smith & Nephew Plc, and various bonds. The analysis includes beta values, EPS, and expected returns. Furthermore, the report applies the Capital Asset Pricing Model (CAPM) to determine the required rate of return for the portfolio, concluding with an evaluation of the portfolio's overall performance and recommendations for future investment strategies.

Capital Market

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

Rationale behind the choice of portfolio.....................................................................................3

Evaluation and application of investment theory........................................................................7

EVALUATION.............................................................................................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................3

Rationale behind the choice of portfolio.....................................................................................3

Evaluation and application of investment theory........................................................................7

EVALUATION.............................................................................................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................14

INTRODUCTION

Capital market implies for the financial area where equities and debts are bought and

sold. In the recent times, investors lay high level of emphasis on investing money in the

securities for generating high returns. Further, now investors also make focus on investing

money in the wide range of securities rather than in only one. In other words, investors manage

portfolio for reducing the risk level and making value addition in money. On the basis of cited

case situation, investor has £150000 for investing money in the securities, bonds, derivatives and

combination of the same. Hence, with the motive to earn return from portfolio combination of

securities and bonds have been selected. In this, 3 securities and 2 bonds are selected for

managing the risk level. In this, portfolio period will be from 27th February to 3rd April 2018.

Along with this, for spreading risk level investment is allocated to the securities of different

sector. Here, the main motive of investor is to minimize the risk level and earning suitable

returns from the investment made. In this, report will provide deeper insight about the aspects

considered while making selection of assets and overall portfolio. Further, report will also

develop understanding about the theoretical aspects associated with the investment aspects.

Rationale behind the choice of portfolio

In relation with selecting these industries and analysis their financial strengthen is to

acknowledge the market value of them. Therefore, it will be beneficial to have appropriate

information and knowledge regarding the business strength as investor's point of view. The P/E

ratio of Diageo, Astra Zeneca and Smith & Nephew is on favourable state such as these are more

than 10%. Therefore, it will be beneficial for firm in terms of retaining the that much or return

over their sold securities. In the upcoming time it will benefit the investors to have appropriate

returns on their investments. The PE ration of Diageo is 19.30%, Astra Zeneca as 30.25% and

Smiths and Nephew as 15.30%. On the other side, the beta rate and EPS of these industries are

up to the mark and which will be beneficial to it equity holders to have long-term advantages

from business. In accordance with bonds such as TR28 and V025 which has been selected is on

the basis of their maturity period and weights of these securities in the market. Therefore, V025

Capital market implies for the financial area where equities and debts are bought and

sold. In the recent times, investors lay high level of emphasis on investing money in the

securities for generating high returns. Further, now investors also make focus on investing

money in the wide range of securities rather than in only one. In other words, investors manage

portfolio for reducing the risk level and making value addition in money. On the basis of cited

case situation, investor has £150000 for investing money in the securities, bonds, derivatives and

combination of the same. Hence, with the motive to earn return from portfolio combination of

securities and bonds have been selected. In this, 3 securities and 2 bonds are selected for

managing the risk level. In this, portfolio period will be from 27th February to 3rd April 2018.

Along with this, for spreading risk level investment is allocated to the securities of different

sector. Here, the main motive of investor is to minimize the risk level and earning suitable

returns from the investment made. In this, report will provide deeper insight about the aspects

considered while making selection of assets and overall portfolio. Further, report will also

develop understanding about the theoretical aspects associated with the investment aspects.

Rationale behind the choice of portfolio

In relation with selecting these industries and analysis their financial strengthen is to

acknowledge the market value of them. Therefore, it will be beneficial to have appropriate

information and knowledge regarding the business strength as investor's point of view. The P/E

ratio of Diageo, Astra Zeneca and Smith & Nephew is on favourable state such as these are more

than 10%. Therefore, it will be beneficial for firm in terms of retaining the that much or return

over their sold securities. In the upcoming time it will benefit the investors to have appropriate

returns on their investments. The PE ration of Diageo is 19.30%, Astra Zeneca as 30.25% and

Smiths and Nephew as 15.30%. On the other side, the beta rate and EPS of these industries are

up to the mark and which will be beneficial to it equity holders to have long-term advantages

from business. In accordance with bonds such as TR28 and V025 which has been selected is on

the basis of their maturity period and weights of these securities in the market. Therefore, V025

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

has weight of 2% and TR28 as 1%. Thus, to make the investments in these organisations which

will be helpful and beneficial to investors in terms of taking the long terms advantages.

Assets

For avoiding high risk level investment fund has allocated by the investor in 5 assets

include both securities and bonds. Out of 3 securities, 2 has high beta approximately near to 1

which shows high level of volatility. On the other side, one security with low beta has considered

for balancing the risk level. In addition to this, bonds provide investors with fixed returns and are

not subject of high fluctuations. Hence, for avoiding loss at all cost combination of debt and

security has undertaken by the investors.

DGE.L- Diageo Plc:

This is a beverage group which usually serves alcoholic products such as wines, liquors

and beers. There are various brands of this firm such as Guinness, Johnnie Walker, Baileys and

Smirnoff. The performance of organisation is at favourable constant as it has made net sales of

14.5% more than previous year. Moreover, to demonstrate the profitability of the organisation in

context with meeting the requirements such as the beta value of firm is 0.61 which is near to 1.

Thus, it can be said that the changes in share prices of Diageo is not that much fluctuating. On

the other side the EPS is 93.3, it determines that business will have appropriate earning over each

sale of security.

Astra Zeneca:

This is an Anglo-Swedish MNC which deals in pharmaceutical and biopharmaceutical

business. In the year 2013 it moved to Cambridge and has operated research and development in

such pharmaceutical industries. The main aim of this organisation is to develop and manufacture

medicines which will be helpful to the citizens and members which will be helpful in treating the

disorders in gastrointestinal, vascular, psychiatric, respiratory, cardiac, infection, pathology,

oncology and inflammation. The growth of organisation is not that satisfactory as it determined

by the professionals and the external parties. However, it has been argued here that investors

make investments in many shares instead of one which reduces funds for the particular

will be helpful and beneficial to investors in terms of taking the long terms advantages.

Assets

For avoiding high risk level investment fund has allocated by the investor in 5 assets

include both securities and bonds. Out of 3 securities, 2 has high beta approximately near to 1

which shows high level of volatility. On the other side, one security with low beta has considered

for balancing the risk level. In addition to this, bonds provide investors with fixed returns and are

not subject of high fluctuations. Hence, for avoiding loss at all cost combination of debt and

security has undertaken by the investors.

DGE.L- Diageo Plc:

This is a beverage group which usually serves alcoholic products such as wines, liquors

and beers. There are various brands of this firm such as Guinness, Johnnie Walker, Baileys and

Smirnoff. The performance of organisation is at favourable constant as it has made net sales of

14.5% more than previous year. Moreover, to demonstrate the profitability of the organisation in

context with meeting the requirements such as the beta value of firm is 0.61 which is near to 1.

Thus, it can be said that the changes in share prices of Diageo is not that much fluctuating. On

the other side the EPS is 93.3, it determines that business will have appropriate earning over each

sale of security.

Astra Zeneca:

This is an Anglo-Swedish MNC which deals in pharmaceutical and biopharmaceutical

business. In the year 2013 it moved to Cambridge and has operated research and development in

such pharmaceutical industries. The main aim of this organisation is to develop and manufacture

medicines which will be helpful to the citizens and members which will be helpful in treating the

disorders in gastrointestinal, vascular, psychiatric, respiratory, cardiac, infection, pathology,

oncology and inflammation. The growth of organisation is not that satisfactory as it determined

by the professionals and the external parties. However, it has been argued here that investors

make investments in many shares instead of one which reduces funds for the particular

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

companies as well as the distribution of funds among several organisations. To analyse Astra

Zeneca's financial condition there will be analysis based on variables.

In relation with the beta value of industry which is 0.57 as it is co-operatively lower than

1. Therefore, it can be said that share value of firm will not be flexible as it will remain constant

for the longer period. Moreover, it will be beneficial for the investors to make investments in

Astra Zeneca.

Smith and Nephew Plc:

This organisation is the producer of medical equipments throughout the world. The firm

is based in UK and manufactures various medical tools such as Wound management products,

trauma, clinic therapy products, orthopaedic and reconstruction products as well as arthroscopy

products. Moreover, in relation with the argument there has been analysis over several variables.

In relation with the market value of this Smith and Nephew plc it has been analysed here

such as the beta value is 0.21 which determines there the share price of this firm will not have

sudden changes as it not flexible. Therefore, the prices will remain same or approximately to the

same for the long period.

V025:

This is the most successful rand in London in terms of Mobile business. Thus, Vodafone

group operates in various nations and have the higher consumer retention. The firm has provided

the bonds as the marketable securities namely V025. Therefore, to analyse the profitability of

this business the market value of bonds were allocated as 29,886.95 than the expected maturity

period of investment is in 2025. Thus, the expected return is 5.63%.

TR28:

These are corporate bonds which were being used by the government in terms with no

guaranteed any return namely Gilts. Therefore, the expected return of this organisation is 6%

which ascertains that the dividends will be payable in every 6 months. Moreover, it was issued

by the UK government on 29th January 1998 which will going to be matured on 7th December

2028.

Zeneca's financial condition there will be analysis based on variables.

In relation with the beta value of industry which is 0.57 as it is co-operatively lower than

1. Therefore, it can be said that share value of firm will not be flexible as it will remain constant

for the longer period. Moreover, it will be beneficial for the investors to make investments in

Astra Zeneca.

Smith and Nephew Plc:

This organisation is the producer of medical equipments throughout the world. The firm

is based in UK and manufactures various medical tools such as Wound management products,

trauma, clinic therapy products, orthopaedic and reconstruction products as well as arthroscopy

products. Moreover, in relation with the argument there has been analysis over several variables.

In relation with the market value of this Smith and Nephew plc it has been analysed here

such as the beta value is 0.21 which determines there the share price of this firm will not have

sudden changes as it not flexible. Therefore, the prices will remain same or approximately to the

same for the long period.

V025:

This is the most successful rand in London in terms of Mobile business. Thus, Vodafone

group operates in various nations and have the higher consumer retention. The firm has provided

the bonds as the marketable securities namely V025. Therefore, to analyse the profitability of

this business the market value of bonds were allocated as 29,886.95 than the expected maturity

period of investment is in 2025. Thus, the expected return is 5.63%.

TR28:

These are corporate bonds which were being used by the government in terms with no

guaranteed any return namely Gilts. Therefore, the expected return of this organisation is 6%

which ascertains that the dividends will be payable in every 6 months. Moreover, it was issued

by the UK government on 29th January 1998 which will going to be matured on 7th December

2028.

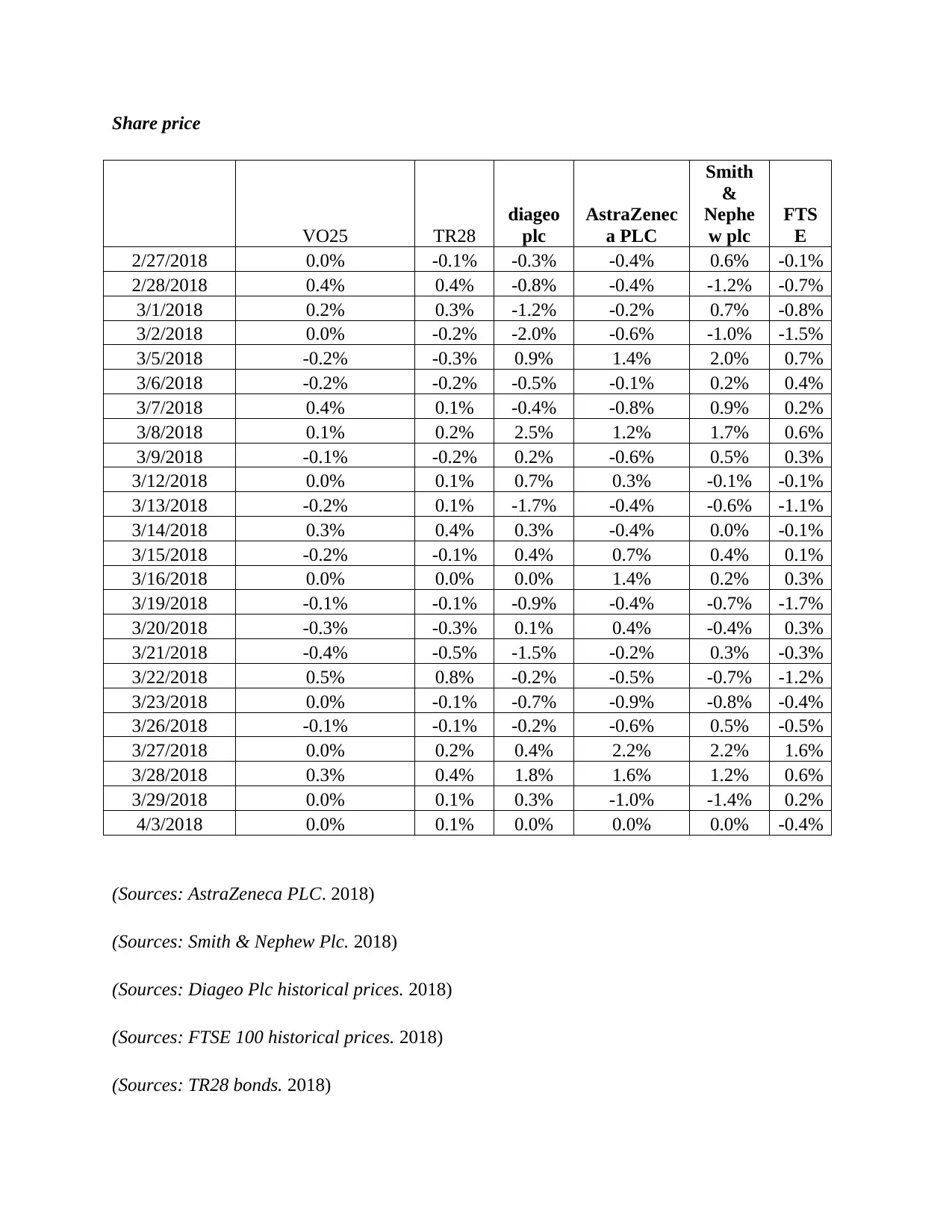

Share price

VO25 TR28

diageo

plc

AstraZenec

a PLC

Smith

&

Nephe

w plc

FTS

E

2/27/2018 0.0% -0.1% -0.3% -0.4% 0.6% -0.1%

2/28/2018 0.4% 0.4% -0.8% -0.4% -1.2% -0.7%

3/1/2018 0.2% 0.3% -1.2% -0.2% 0.7% -0.8%

3/2/2018 0.0% -0.2% -2.0% -0.6% -1.0% -1.5%

3/5/2018 -0.2% -0.3% 0.9% 1.4% 2.0% 0.7%

3/6/2018 -0.2% -0.2% -0.5% -0.1% 0.2% 0.4%

3/7/2018 0.4% 0.1% -0.4% -0.8% 0.9% 0.2%

3/8/2018 0.1% 0.2% 2.5% 1.2% 1.7% 0.6%

3/9/2018 -0.1% -0.2% 0.2% -0.6% 0.5% 0.3%

3/12/2018 0.0% 0.1% 0.7% 0.3% -0.1% -0.1%

3/13/2018 -0.2% 0.1% -1.7% -0.4% -0.6% -1.1%

3/14/2018 0.3% 0.4% 0.3% -0.4% 0.0% -0.1%

3/15/2018 -0.2% -0.1% 0.4% 0.7% 0.4% 0.1%

3/16/2018 0.0% 0.0% 0.0% 1.4% 0.2% 0.3%

3/19/2018 -0.1% -0.1% -0.9% -0.4% -0.7% -1.7%

3/20/2018 -0.3% -0.3% 0.1% 0.4% -0.4% 0.3%

3/21/2018 -0.4% -0.5% -1.5% -0.2% 0.3% -0.3%

3/22/2018 0.5% 0.8% -0.2% -0.5% -0.7% -1.2%

3/23/2018 0.0% -0.1% -0.7% -0.9% -0.8% -0.4%

3/26/2018 -0.1% -0.1% -0.2% -0.6% 0.5% -0.5%

3/27/2018 0.0% 0.2% 0.4% 2.2% 2.2% 1.6%

3/28/2018 0.3% 0.4% 1.8% 1.6% 1.2% 0.6%

3/29/2018 0.0% 0.1% 0.3% -1.0% -1.4% 0.2%

4/3/2018 0.0% 0.1% 0.0% 0.0% 0.0% -0.4%

(Sources: AstraZeneca PLC. 2018)

(Sources: Smith & Nephew Plc. 2018)

(Sources: Diageo Plc historical prices. 2018)

(Sources: FTSE 100 historical prices. 2018)

(Sources: TR28 bonds. 2018)

VO25 TR28

diageo

plc

AstraZenec

a PLC

Smith

&

Nephe

w plc

FTS

E

2/27/2018 0.0% -0.1% -0.3% -0.4% 0.6% -0.1%

2/28/2018 0.4% 0.4% -0.8% -0.4% -1.2% -0.7%

3/1/2018 0.2% 0.3% -1.2% -0.2% 0.7% -0.8%

3/2/2018 0.0% -0.2% -2.0% -0.6% -1.0% -1.5%

3/5/2018 -0.2% -0.3% 0.9% 1.4% 2.0% 0.7%

3/6/2018 -0.2% -0.2% -0.5% -0.1% 0.2% 0.4%

3/7/2018 0.4% 0.1% -0.4% -0.8% 0.9% 0.2%

3/8/2018 0.1% 0.2% 2.5% 1.2% 1.7% 0.6%

3/9/2018 -0.1% -0.2% 0.2% -0.6% 0.5% 0.3%

3/12/2018 0.0% 0.1% 0.7% 0.3% -0.1% -0.1%

3/13/2018 -0.2% 0.1% -1.7% -0.4% -0.6% -1.1%

3/14/2018 0.3% 0.4% 0.3% -0.4% 0.0% -0.1%

3/15/2018 -0.2% -0.1% 0.4% 0.7% 0.4% 0.1%

3/16/2018 0.0% 0.0% 0.0% 1.4% 0.2% 0.3%

3/19/2018 -0.1% -0.1% -0.9% -0.4% -0.7% -1.7%

3/20/2018 -0.3% -0.3% 0.1% 0.4% -0.4% 0.3%

3/21/2018 -0.4% -0.5% -1.5% -0.2% 0.3% -0.3%

3/22/2018 0.5% 0.8% -0.2% -0.5% -0.7% -1.2%

3/23/2018 0.0% -0.1% -0.7% -0.9% -0.8% -0.4%

3/26/2018 -0.1% -0.1% -0.2% -0.6% 0.5% -0.5%

3/27/2018 0.0% 0.2% 0.4% 2.2% 2.2% 1.6%

3/28/2018 0.3% 0.4% 1.8% 1.6% 1.2% 0.6%

3/29/2018 0.0% 0.1% 0.3% -1.0% -1.4% 0.2%

4/3/2018 0.0% 0.1% 0.0% 0.0% 0.0% -0.4%

(Sources: AstraZeneca PLC. 2018)

(Sources: Smith & Nephew Plc. 2018)

(Sources: Diageo Plc historical prices. 2018)

(Sources: FTSE 100 historical prices. 2018)

(Sources: TR28 bonds. 2018)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

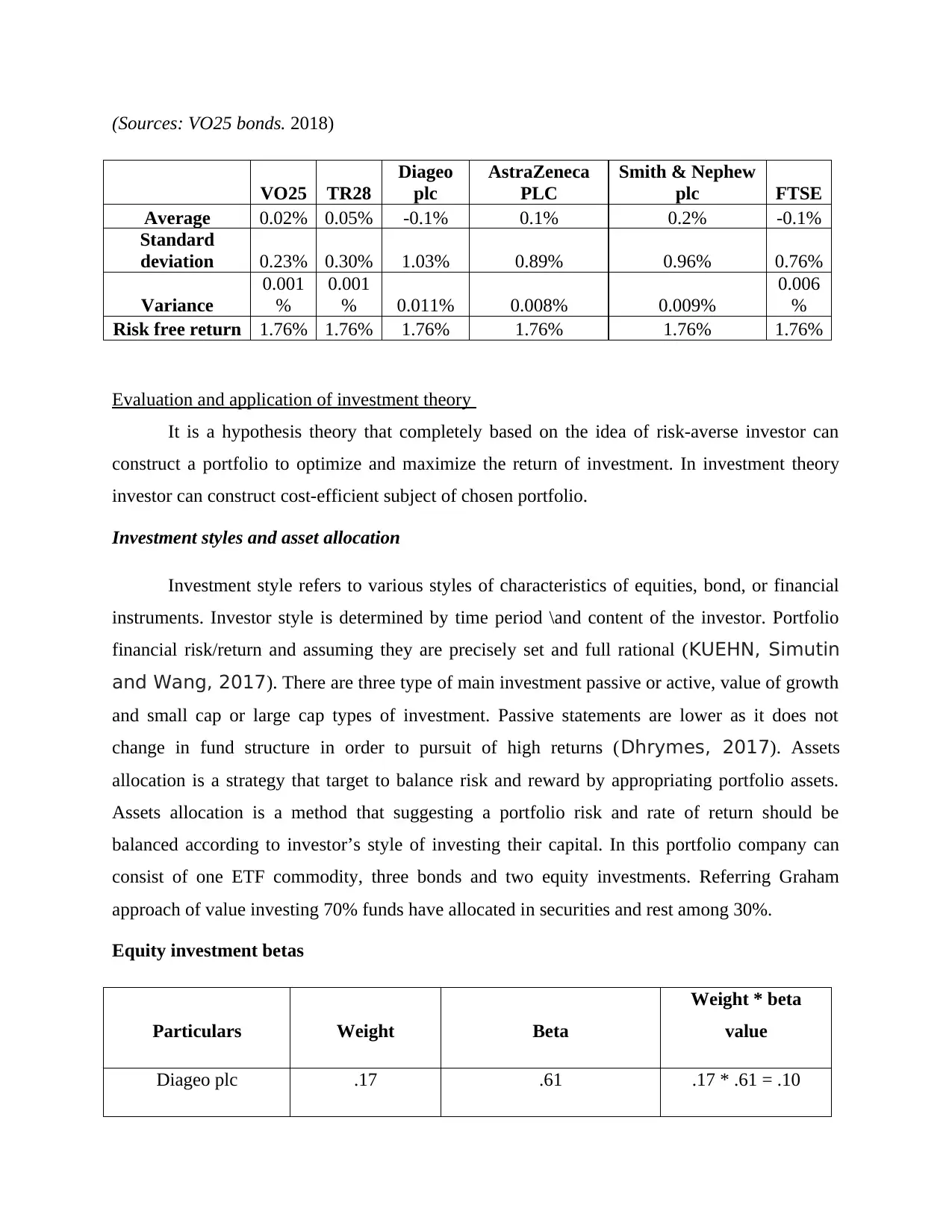

(Sources: VO25 bonds. 2018)

VO25 TR28

Diageo

plc

AstraZeneca

PLC

Smith & Nephew

plc FTSE

Average 0.02% 0.05% -0.1% 0.1% 0.2% -0.1%

Standard

deviation 0.23% 0.30% 1.03% 0.89% 0.96% 0.76%

Variance

0.001

%

0.001

% 0.011% 0.008% 0.009%

0.006

%

Risk free return 1.76% 1.76% 1.76% 1.76% 1.76% 1.76%

Evaluation and application of investment theory

It is a hypothesis theory that completely based on the idea of risk-averse investor can

construct a portfolio to optimize and maximize the return of investment. In investment theory

investor can construct cost-efficient subject of chosen portfolio.

Investment styles and asset allocation

Investment style refers to various styles of characteristics of equities, bond, or financial

instruments. Investor style is determined by time period \and content of the investor. Portfolio

financial risk/return and assuming they are precisely set and full rational (KUEHN, Simutin

and Wang, 2017). There are three type of main investment passive or active, value of growth

and small cap or large cap types of investment. Passive statements are lower as it does not

change in fund structure in order to pursuit of high returns (Dhrymes, 2017). Assets

allocation is a strategy that target to balance risk and reward by appropriating portfolio assets.

Assets allocation is a method that suggesting a portfolio risk and rate of return should be

balanced according to investor’s style of investing their capital. In this portfolio company can

consist of one ETF commodity, three bonds and two equity investments. Referring Graham

approach of value investing 70% funds have allocated in securities and rest among 30%.

Equity investment betas

Particulars Weight Beta

Weight * beta

value

Diageo plc .17 .61 .17 * .61 = .10

VO25 TR28

Diageo

plc

AstraZeneca

PLC

Smith & Nephew

plc FTSE

Average 0.02% 0.05% -0.1% 0.1% 0.2% -0.1%

Standard

deviation 0.23% 0.30% 1.03% 0.89% 0.96% 0.76%

Variance

0.001

%

0.001

% 0.011% 0.008% 0.009%

0.006

%

Risk free return 1.76% 1.76% 1.76% 1.76% 1.76% 1.76%

Evaluation and application of investment theory

It is a hypothesis theory that completely based on the idea of risk-averse investor can

construct a portfolio to optimize and maximize the return of investment. In investment theory

investor can construct cost-efficient subject of chosen portfolio.

Investment styles and asset allocation

Investment style refers to various styles of characteristics of equities, bond, or financial

instruments. Investor style is determined by time period \and content of the investor. Portfolio

financial risk/return and assuming they are precisely set and full rational (KUEHN, Simutin

and Wang, 2017). There are three type of main investment passive or active, value of growth

and small cap or large cap types of investment. Passive statements are lower as it does not

change in fund structure in order to pursuit of high returns (Dhrymes, 2017). Assets

allocation is a strategy that target to balance risk and reward by appropriating portfolio assets.

Assets allocation is a method that suggesting a portfolio risk and rate of return should be

balanced according to investor’s style of investing their capital. In this portfolio company can

consist of one ETF commodity, three bonds and two equity investments. Referring Graham

approach of value investing 70% funds have allocated in securities and rest among 30%.

Equity investment betas

Particulars Weight Beta

Weight * beta

value

Diageo plc .17 .61 .17 * .61 = .10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

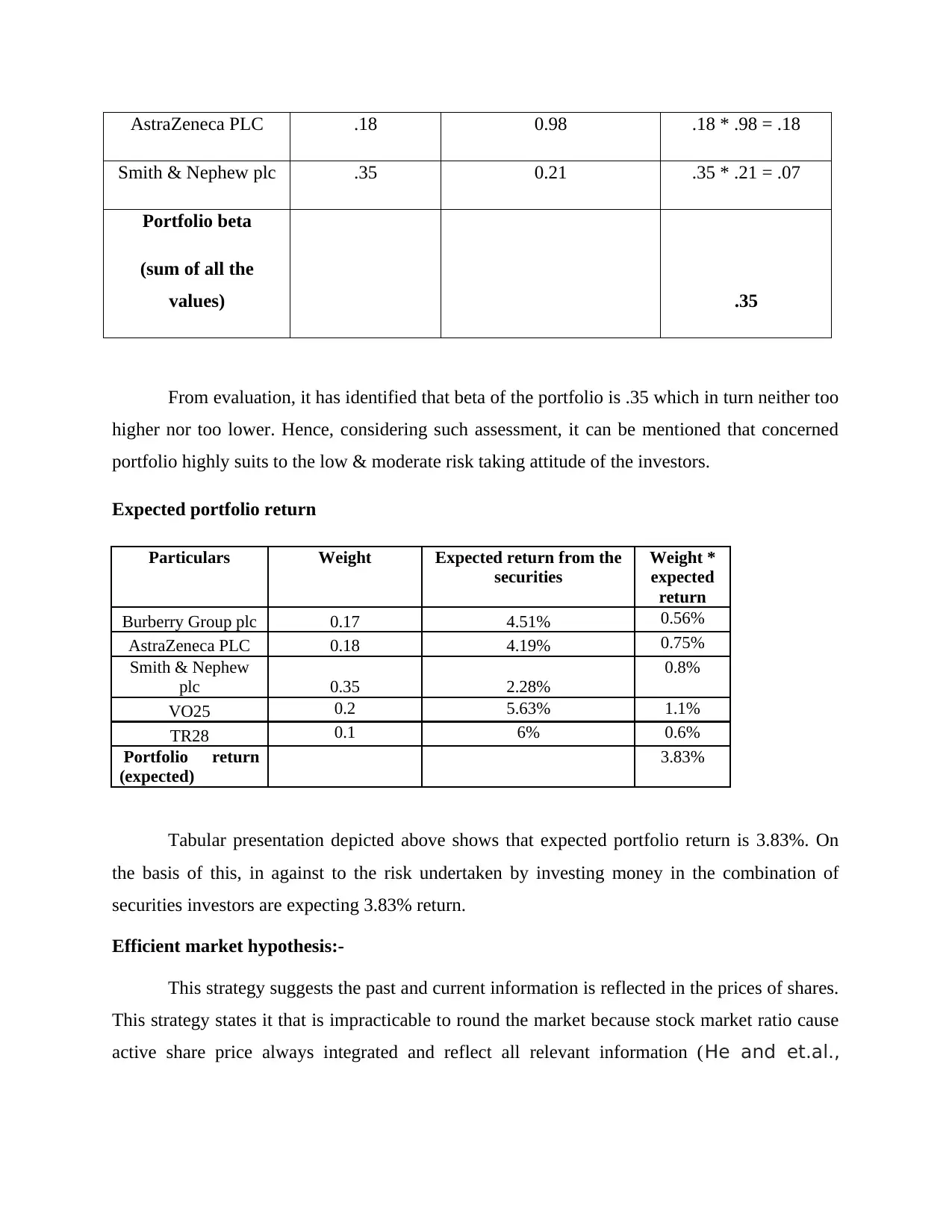

AstraZeneca PLC .18 0.98 .18 * .98 = .18

Smith & Nephew plc .35 0.21 .35 * .21 = .07

Portfolio beta

(sum of all the

values) .35

From evaluation, it has identified that beta of the portfolio is .35 which in turn neither too

higher nor too lower. Hence, considering such assessment, it can be mentioned that concerned

portfolio highly suits to the low & moderate risk taking attitude of the investors.

Expected portfolio return

Particulars Weight Expected return from the

securities

Weight *

expected

return

Burberry Group plc 0.17 4.51% 0.56%

AstraZeneca PLC 0.18 4.19% 0.75%

Smith & Nephew

plc 0.35 2.28%

0.8%

VO25 0.2 5.63% 1.1%

TR28 0.1 6% 0.6%

Portfolio return

(expected)

3.83%

Tabular presentation depicted above shows that expected portfolio return is 3.83%. On

the basis of this, in against to the risk undertaken by investing money in the combination of

securities investors are expecting 3.83% return.

Efficient market hypothesis:-

This strategy suggests the past and current information is reflected in the prices of shares.

This strategy states it that is impracticable to round the market because stock market ratio cause

active share price always integrated and reflect all relevant information (He and et.al.,

Smith & Nephew plc .35 0.21 .35 * .21 = .07

Portfolio beta

(sum of all the

values) .35

From evaluation, it has identified that beta of the portfolio is .35 which in turn neither too

higher nor too lower. Hence, considering such assessment, it can be mentioned that concerned

portfolio highly suits to the low & moderate risk taking attitude of the investors.

Expected portfolio return

Particulars Weight Expected return from the

securities

Weight *

expected

return

Burberry Group plc 0.17 4.51% 0.56%

AstraZeneca PLC 0.18 4.19% 0.75%

Smith & Nephew

plc 0.35 2.28%

0.8%

VO25 0.2 5.63% 1.1%

TR28 0.1 6% 0.6%

Portfolio return

(expected)

3.83%

Tabular presentation depicted above shows that expected portfolio return is 3.83%. On

the basis of this, in against to the risk undertaken by investing money in the combination of

securities investors are expecting 3.83% return.

Efficient market hypothesis:-

This strategy suggests the past and current information is reflected in the prices of shares.

This strategy states it that is impracticable to round the market because stock market ratio cause

active share price always integrated and reflect all relevant information (He and et.al.,

2016). According to this theory stocks are always exchange at their fair value on stock

exchange.

Efficient market hypothesis presents that it is impossible for the investors to beat the

market. The rationale behind this, stock market efficiency has direct influence on existing share

price level. In accordance with efficiency market hypothesis framework, stocks are usually trade

at fair values on stock market (Wang and et.al., 2018). Hence, due to this, it is highly impossible

for the investors to either invest money in undervalued stock or sell the same at inflated price

level. By considering this, it can be presented that it is not possible to outperform the overall

stock market through expert or effectual stock selection or market timing (Kristoufek and

Vosvrda, 2018). Thus, it entails that for gaining higher returns or margin investors need to invest

money in the riskier securities. However, on the critical note, it has assessed that theory

pertaining to efficiency market hypothesis is not appropriate because it emphasizes on

undertaking only riskier investments with the motive to generate high margin.

Capital asset pricing model

CAPM may be served as a modern investment which provides high level of assistance in

ascertaining the required rate of return associated with the particular kind of securities. Usually,

in against to the risk undertaken investors expect some return from the investment made under

securities. Now, CAPM model is widely used by the investors while developing and managing

portfolios (Suntraruk, 2018). Moreover, such model clearly presents expected returns associated

with the securities. Hence, by taking into account such tool investors can assess which asset or

security is offering high return over other. Thus, using CAPM model investors can make idea

about low performing securities. This model is highly effectual which in turn considers time

value of money concept by considering risk free rate of return. CAPM believes that positive

relationship takes place between risk and return (Bao, Diks and Li, 2018). On the basis of this,

return will increase with the rise in risk level. In addition to this, such model considers beta value

that clearly shows the volatility level associated with the securities. In this, stocks with beta

value less than 1 has selected by taking into account moderate risk acceptance attitude level of

the investors. In this, beta value of Diageo plc and Smith & Nephew plc accounts for .61 & .21

respectively.

exchange.

Efficient market hypothesis presents that it is impossible for the investors to beat the

market. The rationale behind this, stock market efficiency has direct influence on existing share

price level. In accordance with efficiency market hypothesis framework, stocks are usually trade

at fair values on stock market (Wang and et.al., 2018). Hence, due to this, it is highly impossible

for the investors to either invest money in undervalued stock or sell the same at inflated price

level. By considering this, it can be presented that it is not possible to outperform the overall

stock market through expert or effectual stock selection or market timing (Kristoufek and

Vosvrda, 2018). Thus, it entails that for gaining higher returns or margin investors need to invest

money in the riskier securities. However, on the critical note, it has assessed that theory

pertaining to efficiency market hypothesis is not appropriate because it emphasizes on

undertaking only riskier investments with the motive to generate high margin.

Capital asset pricing model

CAPM may be served as a modern investment which provides high level of assistance in

ascertaining the required rate of return associated with the particular kind of securities. Usually,

in against to the risk undertaken investors expect some return from the investment made under

securities. Now, CAPM model is widely used by the investors while developing and managing

portfolios (Suntraruk, 2018). Moreover, such model clearly presents expected returns associated

with the securities. Hence, by taking into account such tool investors can assess which asset or

security is offering high return over other. Thus, using CAPM model investors can make idea

about low performing securities. This model is highly effectual which in turn considers time

value of money concept by considering risk free rate of return. CAPM believes that positive

relationship takes place between risk and return (Bao, Diks and Li, 2018). On the basis of this,

return will increase with the rise in risk level. In addition to this, such model considers beta value

that clearly shows the volatility level associated with the securities. In this, stocks with beta

value less than 1 has selected by taking into account moderate risk acceptance attitude level of

the investors. In this, beta value of Diageo plc and Smith & Nephew plc accounts for .61 & .21

respectively.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

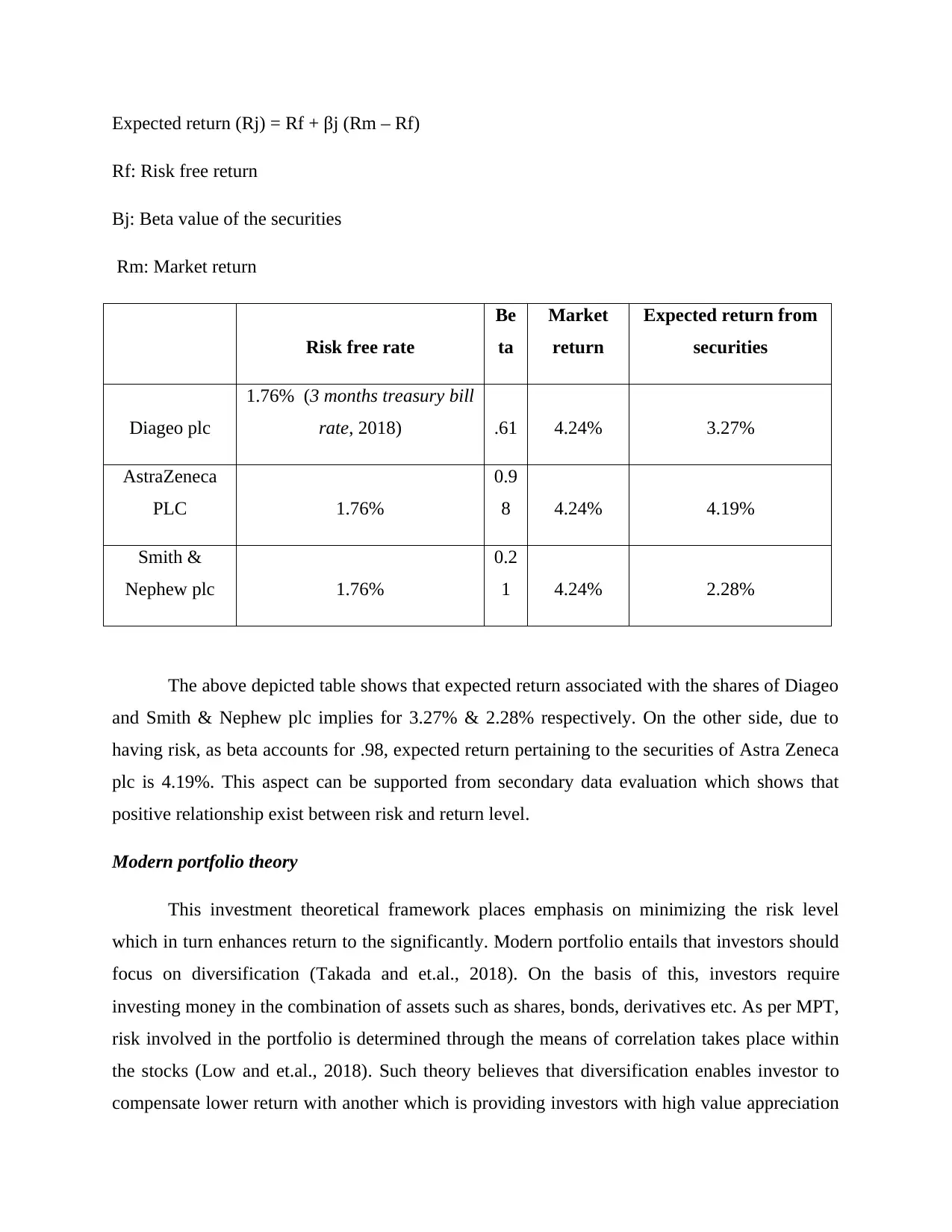

Expected return (Rj) = Rf + βj (Rm – Rf)

Rf: Risk free return

Βj: Beta value of the securities

Rm: Market return

Risk free rate

Be

ta

Market

return

Expected return from

securities

Diageo plc

1.76% (3 months treasury bill

rate, 2018) .61 4.24% 3.27%

AstraZeneca

PLC 1.76%

0.9

8 4.24% 4.19%

Smith &

Nephew plc 1.76%

0.2

1 4.24% 2.28%

The above depicted table shows that expected return associated with the shares of Diageo

and Smith & Nephew plc implies for 3.27% & 2.28% respectively. On the other side, due to

having risk, as beta accounts for .98, expected return pertaining to the securities of Astra Zeneca

plc is 4.19%. This aspect can be supported from secondary data evaluation which shows that

positive relationship exist between risk and return level.

Modern portfolio theory

This investment theoretical framework places emphasis on minimizing the risk level

which in turn enhances return to the significantly. Modern portfolio entails that investors should

focus on diversification (Takada and et.al., 2018). On the basis of this, investors require

investing money in the combination of assets such as shares, bonds, derivatives etc. As per MPT,

risk involved in the portfolio is determined through the means of correlation takes place within

the stocks (Low and et.al., 2018). Such theory believes that diversification enables investor to

compensate lower return with another which is providing investors with high value appreciation

Rf: Risk free return

Βj: Beta value of the securities

Rm: Market return

Risk free rate

Be

ta

Market

return

Expected return from

securities

Diageo plc

1.76% (3 months treasury bill

rate, 2018) .61 4.24% 3.27%

AstraZeneca

PLC 1.76%

0.9

8 4.24% 4.19%

Smith &

Nephew plc 1.76%

0.2

1 4.24% 2.28%

The above depicted table shows that expected return associated with the shares of Diageo

and Smith & Nephew plc implies for 3.27% & 2.28% respectively. On the other side, due to

having risk, as beta accounts for .98, expected return pertaining to the securities of Astra Zeneca

plc is 4.19%. This aspect can be supported from secondary data evaluation which shows that

positive relationship exist between risk and return level.

Modern portfolio theory

This investment theoretical framework places emphasis on minimizing the risk level

which in turn enhances return to the significantly. Modern portfolio entails that investors should

focus on diversification (Takada and et.al., 2018). On the basis of this, investors require

investing money in the combination of assets such as shares, bonds, derivatives etc. As per MPT,

risk involved in the portfolio is determined through the means of correlation takes place within

the stocks (Low and et.al., 2018). Such theory believes that diversification enables investor to

compensate lower return with another which is providing investors with high value appreciation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

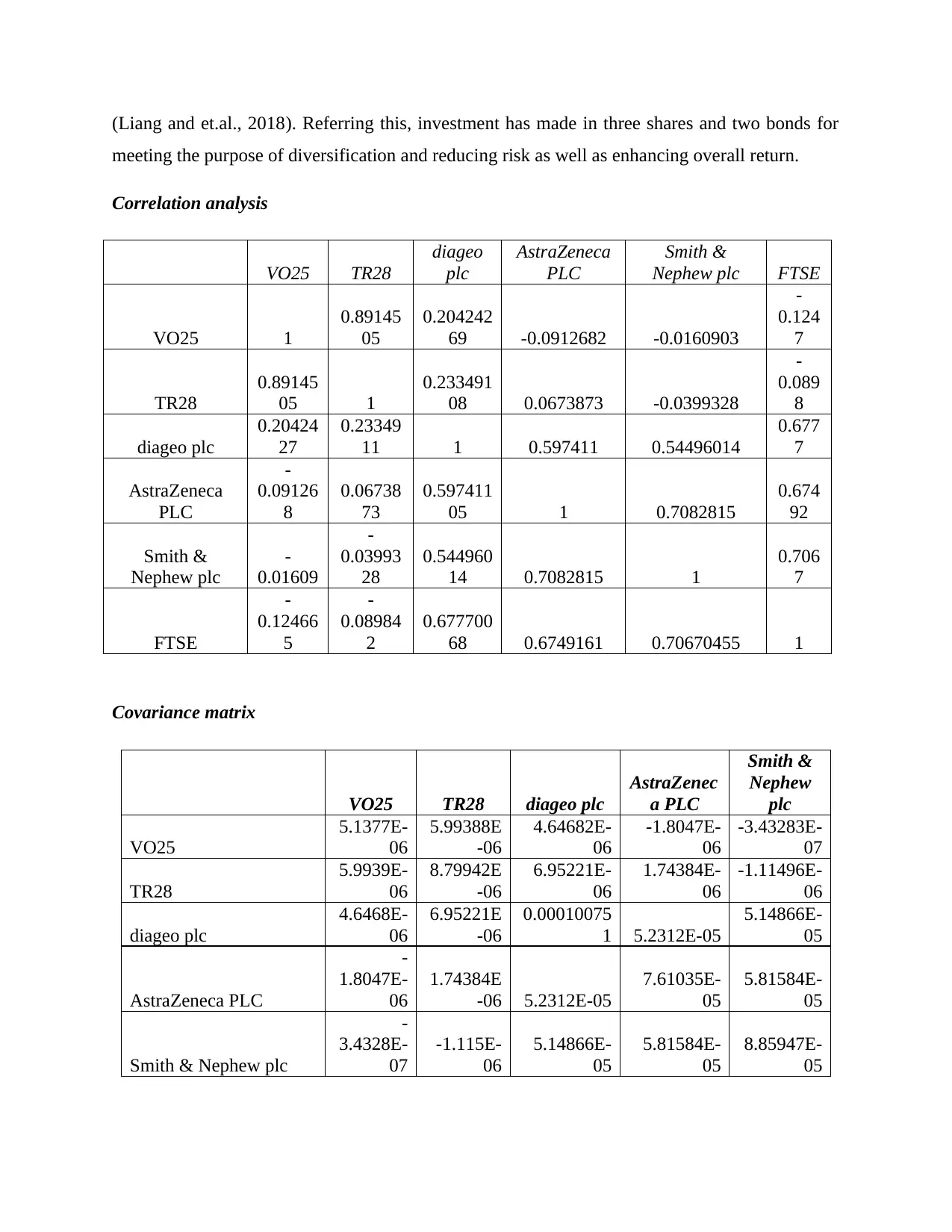

(Liang and et.al., 2018). Referring this, investment has made in three shares and two bonds for

meeting the purpose of diversification and reducing risk as well as enhancing overall return.

Correlation analysis

VO25 TR28

diageo

plc

AstraZeneca

PLC

Smith &

Nephew plc FTSE

VO25 1

0.89145

05

0.204242

69 -0.0912682 -0.0160903

-

0.124

7

TR28

0.89145

05 1

0.233491

08 0.0673873 -0.0399328

-

0.089

8

diageo plc

0.20424

27

0.23349

11 1 0.597411 0.54496014

0.677

7

AstraZeneca

PLC

-

0.09126

8

0.06738

73

0.597411

05 1 0.7082815

0.674

92

Smith &

Nephew plc

-

0.01609

-

0.03993

28

0.544960

14 0.7082815 1

0.706

7

FTSE

-

0.12466

5

-

0.08984

2

0.677700

68 0.6749161 0.70670455 1

Covariance matrix

VO25 TR28 diageo plc

AstraZenec

a PLC

Smith &

Nephew

plc

VO25

5.1377E-

06

5.99388E

-06

4.64682E-

06

-1.8047E-

06

-3.43283E-

07

TR28

5.9939E-

06

8.79942E

-06

6.95221E-

06

1.74384E-

06

-1.11496E-

06

diageo plc

4.6468E-

06

6.95221E

-06

0.00010075

1 5.2312E-05

5.14866E-

05

AstraZeneca PLC

-

1.8047E-

06

1.74384E

-06 5.2312E-05

7.61035E-

05

5.81584E-

05

Smith & Nephew plc

-

3.4328E-

07

-1.115E-

06

5.14866E-

05

5.81584E-

05

8.85947E-

05

meeting the purpose of diversification and reducing risk as well as enhancing overall return.

Correlation analysis

VO25 TR28

diageo

plc

AstraZeneca

PLC

Smith &

Nephew plc FTSE

VO25 1

0.89145

05

0.204242

69 -0.0912682 -0.0160903

-

0.124

7

TR28

0.89145

05 1

0.233491

08 0.0673873 -0.0399328

-

0.089

8

diageo plc

0.20424

27

0.23349

11 1 0.597411 0.54496014

0.677

7

AstraZeneca

PLC

-

0.09126

8

0.06738

73

0.597411

05 1 0.7082815

0.674

92

Smith &

Nephew plc

-

0.01609

-

0.03993

28

0.544960

14 0.7082815 1

0.706

7

FTSE

-

0.12466

5

-

0.08984

2

0.677700

68 0.6749161 0.70670455 1

Covariance matrix

VO25 TR28 diageo plc

AstraZenec

a PLC

Smith &

Nephew

plc

VO25

5.1377E-

06

5.99388E

-06

4.64682E-

06

-1.8047E-

06

-3.43283E-

07

TR28

5.9939E-

06

8.79942E

-06

6.95221E-

06

1.74384E-

06

-1.11496E-

06

diageo plc

4.6468E-

06

6.95221E

-06

0.00010075

1 5.2312E-05

5.14866E-

05

AstraZeneca PLC

-

1.8047E-

06

1.74384E

-06 5.2312E-05

7.61035E-

05

5.81584E-

05

Smith & Nephew plc

-

3.4328E-

07

-1.115E-

06

5.14866E-

05

5.81584E-

05

8.85947E-

05

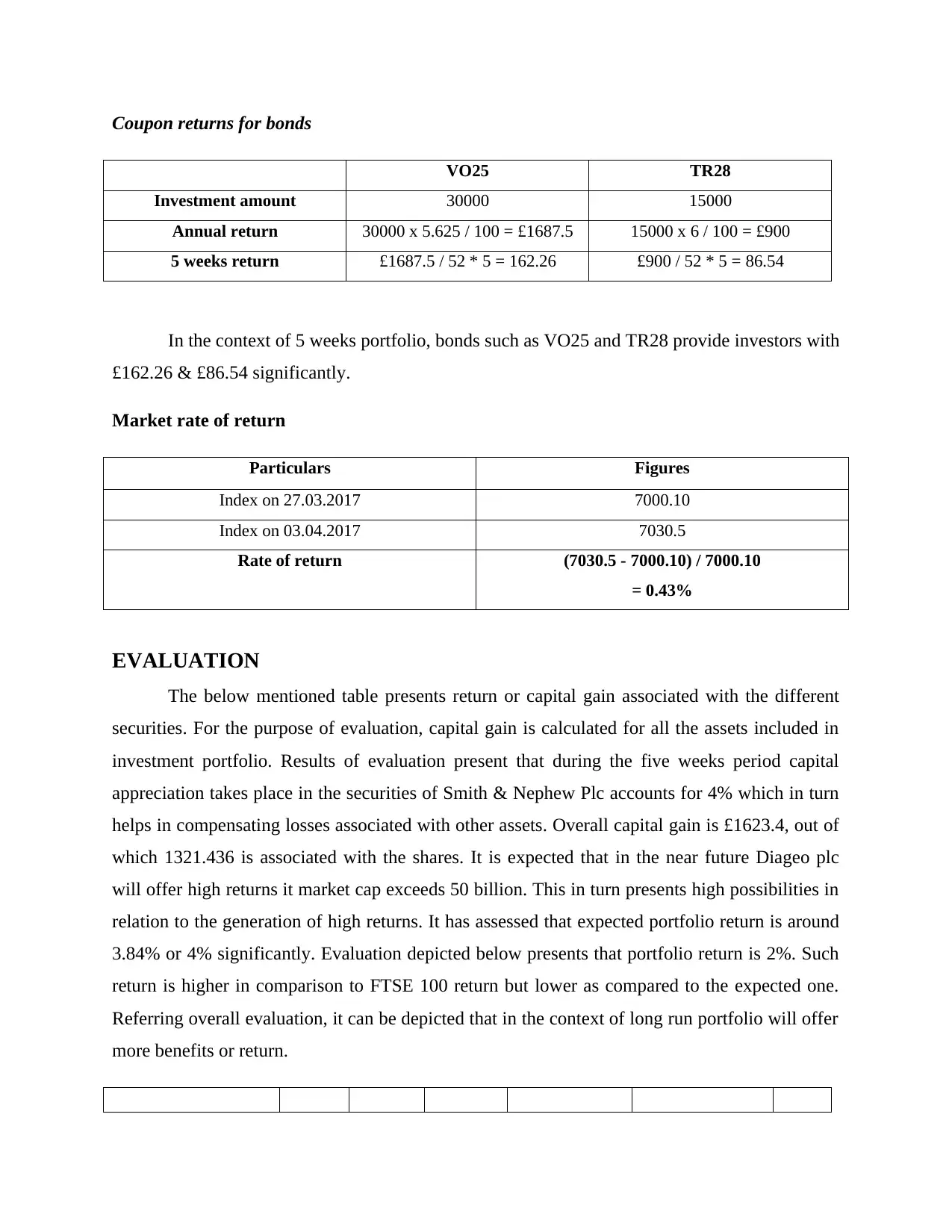

Coupon returns for bonds

VO25 TR28

Investment amount 30000 15000

Annual return 30000 x 5.625 / 100 = £1687.5 15000 x 6 / 100 = £900

5 weeks return £1687.5 / 52 * 5 = 162.26 £900 / 52 * 5 = 86.54

In the context of 5 weeks portfolio, bonds such as VO25 and TR28 provide investors with

£162.26 & £86.54 significantly.

Market rate of return

Particulars Figures

Index on 27.03.2017 7000.10

Index on 03.04.2017 7030.5

Rate of return (7030.5 - 7000.10) / 7000.10

= 0.43%

EVALUATION

The below mentioned table presents return or capital gain associated with the different

securities. For the purpose of evaluation, capital gain is calculated for all the assets included in

investment portfolio. Results of evaluation present that during the five weeks period capital

appreciation takes place in the securities of Smith & Nephew Plc accounts for 4% which in turn

helps in compensating losses associated with other assets. Overall capital gain is £1623.4, out of

which 1321.436 is associated with the shares. It is expected that in the near future Diageo plc

will offer high returns it market cap exceeds 50 billion. This in turn presents high possibilities in

relation to the generation of high returns. It has assessed that expected portfolio return is around

3.84% or 4% significantly. Evaluation depicted below presents that portfolio return is 2%. Such

return is higher in comparison to FTSE 100 return but lower as compared to the expected one.

Referring overall evaluation, it can be depicted that in the context of long run portfolio will offer

more benefits or return.

VO25 TR28

Investment amount 30000 15000

Annual return 30000 x 5.625 / 100 = £1687.5 15000 x 6 / 100 = £900

5 weeks return £1687.5 / 52 * 5 = 162.26 £900 / 52 * 5 = 86.54

In the context of 5 weeks portfolio, bonds such as VO25 and TR28 provide investors with

£162.26 & £86.54 significantly.

Market rate of return

Particulars Figures

Index on 27.03.2017 7000.10

Index on 03.04.2017 7030.5

Rate of return (7030.5 - 7000.10) / 7000.10

= 0.43%

EVALUATION

The below mentioned table presents return or capital gain associated with the different

securities. For the purpose of evaluation, capital gain is calculated for all the assets included in

investment portfolio. Results of evaluation present that during the five weeks period capital

appreciation takes place in the securities of Smith & Nephew Plc accounts for 4% which in turn

helps in compensating losses associated with other assets. Overall capital gain is £1623.4, out of

which 1321.436 is associated with the shares. It is expected that in the near future Diageo plc

will offer high returns it market cap exceeds 50 billion. This in turn presents high possibilities in

relation to the generation of high returns. It has assessed that expected portfolio return is around

3.84% or 4% significantly. Evaluation depicted below presents that portfolio return is 2%. Such

return is higher in comparison to FTSE 100 return but lower as compared to the expected one.

Referring overall evaluation, it can be depicted that in the context of long run portfolio will offer

more benefits or return.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.