Chartered Banker MBA: Capital Markets and Treasury Management Report

VerifiedAdded on 2023/01/16

|27

|7237

|45

Report

AI Summary

This report provides a detailed analysis of capital markets and treasury management, drawing insights from both academic and practitioner research. It begins with an executive summary outlining the key areas covered, including the treasury departments of banks, credit rating agencies, money and foreign exchange markets, and risk management failures. The report then delves into the treasury department, examining its functions through front, middle, and back offices and the potential benefits of an integrated unit. It further evaluates the aims of regulatory reforms of credit rating agencies in Europe and the USA, considering the criticisms and impacts of these agencies. The analysis extends to the conditions of money and global foreign exchange markets between 2009 and 2019, comparing the periods to highlight changes and trends. Moreover, the report identifies the tools used by treasury management to mitigate foreign exchange risk and discusses the failures of risk management techniques in banks, particularly concerning the use of VaR and derivatives. The report concludes with a summary of the findings and a comprehensive reference list supporting the analysis.

Running head: CAPITAL MARKET AND TREASURY

Capital market and treasury

Name of the student

Name of the university

Student ID

Author note

Capital market and treasury

Name of the student

Name of the university

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CAPITAL MARKET AND TREASURY

Executive summary:

The current paper focuses on the analysis of the capital and treasury market that considers

different aspect which include treasury department of banks, credit rating agencies, money

and foreign exchange market and risks management failure in banks. All the discussions have

been supported from the insights that have been gained from practitioner and academic

research. For the purpose of analysis, several papers have been refereed that provided

relevant information on the concerned topic. There are total four topics that have been

addressed individually in the present report.

Executive summary:

The current paper focuses on the analysis of the capital and treasury market that considers

different aspect which include treasury department of banks, credit rating agencies, money

and foreign exchange market and risks management failure in banks. All the discussions have

been supported from the insights that have been gained from practitioner and academic

research. For the purpose of analysis, several papers have been refereed that provided

relevant information on the concerned topic. There are total four topics that have been

addressed individually in the present report.

2CAPITAL MARKET AND TREASURY

Table of Contents

Introduction:...............................................................................................................................4

Evaluation of treasury department of banks by analysing the example of failed banks:...........4

Evaluating the aims of regulatory reforms of credit rating agencies in Europe and USA:........6

Evaluating the conditions of money market and global foreign exchange during 2014-2019

and comparing the situation with that in 2009-2013:...............................................................10

Identification of tools by treasury management of banks to mitigate foreign exchange risk:. 15

Discussing the failures of risk management technique in banks in the financial contexts such

as use of VaR and derivatives:.................................................................................................17

Conclusion:..............................................................................................................................20

Reference list:...........................................................................................................................22

Table of Contents

Introduction:...............................................................................................................................4

Evaluation of treasury department of banks by analysing the example of failed banks:...........4

Evaluating the aims of regulatory reforms of credit rating agencies in Europe and USA:........6

Evaluating the conditions of money market and global foreign exchange during 2014-2019

and comparing the situation with that in 2009-2013:...............................................................10

Identification of tools by treasury management of banks to mitigate foreign exchange risk:. 15

Discussing the failures of risk management technique in banks in the financial contexts such

as use of VaR and derivatives:.................................................................................................17

Conclusion:..............................................................................................................................20

Reference list:...........................................................................................................................22

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CAPITAL MARKET AND TREASURY

Introduction:

The report is prepared for analysing the capital and treasury market by deriving the

insights from academic and practitioner research. Such report has been prepared by covering

the topics as mentioned in the mandatory section and additional two topics are chosen from

the additional section. The first section comprise of two topics that is treasury department of

banks and credit rating agencies. The analysis of treasury department of bank is done in terms

of the activities performed by the front, middle and back office and whether the introduction

of an integrated unit would be efficient. Treasury department of banks form an important part

as it deals with management and balancing of daily flow of cash along with other activities

such as investment of banks in foreign exchange, securities, cash and liability management

instruments (Labidi et al. 2018). In light of the reforms for monitoring credit rating agencies,

the aims of such reforms in USA and Europe have been analysed. All such analysis and the

findings from the research conducted are supported by the insights gained from practitioner

and academic research. The later part of report demonstrates the analysis of condition of

global money and foreign exchange market from the time period 2009 to 2018. In addition to

this, report also outlines the different tools employed by treasury management of bank for

managing credit risk and mitigating foreign exchange risk. Furthermore, the report focuses on

the risk management failure in banking and financial institutions due to the failure on part of

risk metrics to assess the risks.

Evaluation of treasury department of banks by analysing the example of failed banks:

The treasury department of a bank is a part of investment banking business which has

the responsibility of managing and balancing the liquidity of funds and daily flow of cash

within the banks. The primary objective of such department within the bank is to forecast the

amount of net interest income by preparing several financial models. The treasury department

Introduction:

The report is prepared for analysing the capital and treasury market by deriving the

insights from academic and practitioner research. Such report has been prepared by covering

the topics as mentioned in the mandatory section and additional two topics are chosen from

the additional section. The first section comprise of two topics that is treasury department of

banks and credit rating agencies. The analysis of treasury department of bank is done in terms

of the activities performed by the front, middle and back office and whether the introduction

of an integrated unit would be efficient. Treasury department of banks form an important part

as it deals with management and balancing of daily flow of cash along with other activities

such as investment of banks in foreign exchange, securities, cash and liability management

instruments (Labidi et al. 2018). In light of the reforms for monitoring credit rating agencies,

the aims of such reforms in USA and Europe have been analysed. All such analysis and the

findings from the research conducted are supported by the insights gained from practitioner

and academic research. The later part of report demonstrates the analysis of condition of

global money and foreign exchange market from the time period 2009 to 2018. In addition to

this, report also outlines the different tools employed by treasury management of bank for

managing credit risk and mitigating foreign exchange risk. Furthermore, the report focuses on

the risk management failure in banking and financial institutions due to the failure on part of

risk metrics to assess the risks.

Evaluation of treasury department of banks by analysing the example of failed banks:

The treasury department of a bank is a part of investment banking business which has

the responsibility of managing and balancing the liquidity of funds and daily flow of cash

within the banks. The primary objective of such department within the bank is to forecast the

amount of net interest income by preparing several financial models. The treasury department

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CAPITAL MARKET AND TREASURY

has multiple units having front, middle and back office as it is entrusted to perform all such

functions. The treasury department perform the role of front office as it assist banks in

generating revenue and profits and the key players lining up in such role include asset

managers, brokers, structuring professionals and brokers (Bashir 2016). The middle office of

treasury banks performs the role of mitigation of investment risk as much as possible and it

consists of research, risk management and compliance departments. In addition to this, there

are various normal back office activities which the treasury department of bank has to

perform. The total amount of loan that can be extended and the extent of deposits taken by

the bank are supposed to be enquired by the treasury department by regularly communicating

with the bank. In addition to this, the amount of risk that can be taken by the banks at certain

point of time is also monitored by the bank by liaising with the proprietary and Forex

department. In addition to this, they are to ensure that bank is not running out of cash and

adequate amount of cash is available in the banks (Kidwell et al. 2016). Therefore, there are

different roles that are required to be performed by treasury department which results in unit

having different offices.

The failure of banks to efficiently manage its treasury department would lead to

failure of banks because of deterioration associated with the liquidity position. The Latvian

bank was one the largest lender which failed because of deterioration in its liquidity position

as there were not sufficient funds to meet the stressed outflow. The bank experienced a bank

run that resulted in draining out of money by bank. The US treasury further triggered bank

run and they were promptly denied the funding from US treasury. All the payments out of

the bank were frozen by the banks for preventing the collapse. The business practice of bank

was to bank high shell companies in the absence of appropriate policies and procedures of

risk mitigation that facilitating transactions for the parties concerned (Berndsen et al. 2018).

Such failure of bank causing deterioration of its liquidity position is due to its failure of

has multiple units having front, middle and back office as it is entrusted to perform all such

functions. The treasury department perform the role of front office as it assist banks in

generating revenue and profits and the key players lining up in such role include asset

managers, brokers, structuring professionals and brokers (Bashir 2016). The middle office of

treasury banks performs the role of mitigation of investment risk as much as possible and it

consists of research, risk management and compliance departments. In addition to this, there

are various normal back office activities which the treasury department of bank has to

perform. The total amount of loan that can be extended and the extent of deposits taken by

the bank are supposed to be enquired by the treasury department by regularly communicating

with the bank. In addition to this, the amount of risk that can be taken by the banks at certain

point of time is also monitored by the bank by liaising with the proprietary and Forex

department. In addition to this, they are to ensure that bank is not running out of cash and

adequate amount of cash is available in the banks (Kidwell et al. 2016). Therefore, there are

different roles that are required to be performed by treasury department which results in unit

having different offices.

The failure of banks to efficiently manage its treasury department would lead to

failure of banks because of deterioration associated with the liquidity position. The Latvian

bank was one the largest lender which failed because of deterioration in its liquidity position

as there were not sufficient funds to meet the stressed outflow. The bank experienced a bank

run that resulted in draining out of money by bank. The US treasury further triggered bank

run and they were promptly denied the funding from US treasury. All the payments out of

the bank were frozen by the banks for preventing the collapse. The business practice of bank

was to bank high shell companies in the absence of appropriate policies and procedures of

risk mitigation that facilitating transactions for the parties concerned (Berndsen et al. 2018).

Such failure of bank causing deterioration of its liquidity position is due to its failure of

5CAPITAL MARKET AND TREASURY

treasury department to properly manage its liquid funds. It can be inferred from the failure of

such banks that the treasury department of such banks is exposed to particular risks

concerning its operations and being susceptible because of involvement of large amount of

money implying potential complexities surrounding the activities. There is differences in

individual treasurers in terms of its scope, make up and allocation when considering

operational requirements (Isa 2016).

An integrated trading unit conducting trading, analysis, confirming, treasury and other

accounting activities can provide several advantages as the centralized treasury department

would have clear picture of long term liquidity position of bank. Such integrated unit would

be able to deploy the funds and take control and decision to then banks best advantage. It is

considered prudent to have integrated treasury unit because as it helps in closely monitoring

the activities from time to time that would help in minimizing the probability of making

default (Yeoh 2018). The unnecessary movement of funds around different centres would be

prevented due to centralized system. Furthermore, there would be a better managerial and

risk control along with the responsibility as a result of centralized treasury. Decentralisation

of treasury unit such as back office unit, middle and front office would not be necessarily

acquainted with the exposure taken by other units. It might be required by treasury to change

its position if the market is highly volatile and it is possible only if the treasury department in

well integrated (Georgiadis and Mehl 2016). Moreover, the decision of the management can

be promptly implemented in the light of centralized treasury unit. Therefore, the efficiency of

functions of bank can be improved with the help of integrated treasury department.

Evaluating the aims of regulatory reforms of credit rating agencies in Europe and USA:

For the current financial crisis, credit rating agencies (CRA) bears considerable

responsibility as they serve as the gatekeepers to the global credit market and consequently

treasury department to properly manage its liquid funds. It can be inferred from the failure of

such banks that the treasury department of such banks is exposed to particular risks

concerning its operations and being susceptible because of involvement of large amount of

money implying potential complexities surrounding the activities. There is differences in

individual treasurers in terms of its scope, make up and allocation when considering

operational requirements (Isa 2016).

An integrated trading unit conducting trading, analysis, confirming, treasury and other

accounting activities can provide several advantages as the centralized treasury department

would have clear picture of long term liquidity position of bank. Such integrated unit would

be able to deploy the funds and take control and decision to then banks best advantage. It is

considered prudent to have integrated treasury unit because as it helps in closely monitoring

the activities from time to time that would help in minimizing the probability of making

default (Yeoh 2018). The unnecessary movement of funds around different centres would be

prevented due to centralized system. Furthermore, there would be a better managerial and

risk control along with the responsibility as a result of centralized treasury. Decentralisation

of treasury unit such as back office unit, middle and front office would not be necessarily

acquainted with the exposure taken by other units. It might be required by treasury to change

its position if the market is highly volatile and it is possible only if the treasury department in

well integrated (Georgiadis and Mehl 2016). Moreover, the decision of the management can

be promptly implemented in the light of centralized treasury unit. Therefore, the efficiency of

functions of bank can be improved with the help of integrated treasury department.

Evaluating the aims of regulatory reforms of credit rating agencies in Europe and USA:

For the current financial crisis, credit rating agencies (CRA) bears considerable

responsibility as they serve as the gatekeepers to the global credit market and consequently

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CAPITAL MARKET AND TREASURY

occupies a unique place in the financial system. Between 2005 and 2007, there was issuance

of over $ 6.5 trillion into the global credit markets which was facilitated by the ratings on

structured finance securities provided by CRA. The catastrophic loss to investors was

because of their reliance on the rating by such agencies implying a significant role played by

rating agencies in such loss (Alsakka et al. 2017). Had the rating agencies performed

properly, the breakdown in the global credit market would have not occurred. Some of the

key criticisms associated with the rating agencies include widespread interest conflicts, lack

of transparency in the rating process and investors placing excessive reliance on rating. In

light of the criticism faced by credit rating agencies during crisis, the task intends to address

the critical evaluation of the key aims of the regulatory reforms of CRA.

The subprime crisis in the European Union has led to rethink on the regulatory

intervention resulting to introduce binding and specific rules. It is argued that the regulatory

interventions are not able to suffice the problems that evolved due to the financial crisis. On

other hand, the regulatory reforms concerning CRA subsequent to the crisis appears to be

well balanced instruments as it create the introduction of essential checks upon the CRA by

avoiding the intervention of excess regulation. In a study on the comparison between the

evolution of framework of US regulations and law on the rating organization liability towards

investors as against the rules adopted by EU, it was concluded that in event of compensating

the investors the burden of rules plays a considerable obstacle. There has been adoption of the

manor reforms of CRA with some of the fundamental reforms being under the discussion of

the European Union. The development of CRA in the field of insurance industry is of great

importance because of direct impact on the business and general impact on the financial

markets (De Pascalis 2016).

The financial market of the world is majorly impacted by CRA as the actions of rating

agencies closely followed as it impacts the issuers, borrowers, investors and government. The

occupies a unique place in the financial system. Between 2005 and 2007, there was issuance

of over $ 6.5 trillion into the global credit markets which was facilitated by the ratings on

structured finance securities provided by CRA. The catastrophic loss to investors was

because of their reliance on the rating by such agencies implying a significant role played by

rating agencies in such loss (Alsakka et al. 2017). Had the rating agencies performed

properly, the breakdown in the global credit market would have not occurred. Some of the

key criticisms associated with the rating agencies include widespread interest conflicts, lack

of transparency in the rating process and investors placing excessive reliance on rating. In

light of the criticism faced by credit rating agencies during crisis, the task intends to address

the critical evaluation of the key aims of the regulatory reforms of CRA.

The subprime crisis in the European Union has led to rethink on the regulatory

intervention resulting to introduce binding and specific rules. It is argued that the regulatory

interventions are not able to suffice the problems that evolved due to the financial crisis. On

other hand, the regulatory reforms concerning CRA subsequent to the crisis appears to be

well balanced instruments as it create the introduction of essential checks upon the CRA by

avoiding the intervention of excess regulation. In a study on the comparison between the

evolution of framework of US regulations and law on the rating organization liability towards

investors as against the rules adopted by EU, it was concluded that in event of compensating

the investors the burden of rules plays a considerable obstacle. There has been adoption of the

manor reforms of CRA with some of the fundamental reforms being under the discussion of

the European Union. The development of CRA in the field of insurance industry is of great

importance because of direct impact on the business and general impact on the financial

markets (De Pascalis 2016).

The financial market of the world is majorly impacted by CRA as the actions of rating

agencies closely followed as it impacts the issuers, borrowers, investors and government. The

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CAPITAL MARKET AND TREASURY

existing rules concerning the credit rating agencies have been investigated with the serious

weakness in the context of euro debt crisis. During the financial crisis, the risk inherent in the

complicated financial instruments was not properly appreciated due to the failure on part of

such agencies. The reforms of rating agencies have been agreed with the aim such as

improving the quality of ratings of sovereign debts of member states of EU, reduction of over

reliance on credit ratings, reducing conflict of interest, publication of rating on the platform

of European rating and reducing conflict of interest.

The reform of credit rating agencies aims to reduce over reliance on the external

ratings by investors and requiring strengthen of the credit risk of financial institutions. In

addition to this the current directives on the undertaking of the collective instruments such as

alternative investment fund managers and investment in transferable securities is amended. It

is intended to reduce the reliance on agencies when assessing the credit worthiness of the

assets. Furthermore, reforms are also intended to make the rating agencies more accountable

for the actions of their ratings and in the event of intentional infringement by the agencies, it

is ensured by the new rules that the rating agency is held liable.

The dependencies on the credit rating agencies would be improved under the reforms

by ensuring the independence, diversity and opinions of credit ratings. For the rating of

structured financial instruments, it would be required by the issuers paying for the ratings, to

hire at least two credit rating agencies. In addition to this, a rule of mandatory rotation is

introduced by regulation under which issuers of structure finance products paying the

agencies for rating switch to different rating agency in every four years (Leippold and

Rueegg 2018). All such measures will help in improving the independence of credit rating

agencies.

existing rules concerning the credit rating agencies have been investigated with the serious

weakness in the context of euro debt crisis. During the financial crisis, the risk inherent in the

complicated financial instruments was not properly appreciated due to the failure on part of

such agencies. The reforms of rating agencies have been agreed with the aim such as

improving the quality of ratings of sovereign debts of member states of EU, reduction of over

reliance on credit ratings, reducing conflict of interest, publication of rating on the platform

of European rating and reducing conflict of interest.

The reform of credit rating agencies aims to reduce over reliance on the external

ratings by investors and requiring strengthen of the credit risk of financial institutions. In

addition to this the current directives on the undertaking of the collective instruments such as

alternative investment fund managers and investment in transferable securities is amended. It

is intended to reduce the reliance on agencies when assessing the credit worthiness of the

assets. Furthermore, reforms are also intended to make the rating agencies more accountable

for the actions of their ratings and in the event of intentional infringement by the agencies, it

is ensured by the new rules that the rating agency is held liable.

The dependencies on the credit rating agencies would be improved under the reforms

by ensuring the independence, diversity and opinions of credit ratings. For the rating of

structured financial instruments, it would be required by the issuers paying for the ratings, to

hire at least two credit rating agencies. In addition to this, a rule of mandatory rotation is

introduced by regulation under which issuers of structure finance products paying the

agencies for rating switch to different rating agency in every four years (Leippold and

Rueegg 2018). All such measures will help in improving the independence of credit rating

agencies.

8CAPITAL MARKET AND TREASURY

In US, CRA is required to make a series of disclosures and such disclosures include

information on the procedures and policies for determining ratings, conflict of interest and

preventing the use of non public material information. The oversight of credit rating agencies

is further strengthened by the proposed regulations by SEC (Securities and exchange

committee). Such reforms are required ratings are often considered by investors in selling and

purchasing any security. The regulatory reforms directing credit agencies call for more

accountability and transparency and restructuring the rating industry like the profession of

public accounting (Arcelli et al. 2017). There is a proposal of promulgating generally

accepted rating principles as they influence the capital market enormously. The impact of the

loss of reliability in the ratings of CRA in US resulted in the new regulation that is based on

rules of SEC and credit rating agencies reforms. It can be seen that the current regulation

concerning credit rating agencies appears to be exhaustive and detailed. The amendment

requires providing SEC with the additional reports relating to credit action such as

downgrade, upgrade and placement for each class of security within each financial year.

The Basel II accord represents the set of rules concerning the role which the credit

rating agencies play in the financial market. The risk faced by banks is measured in a reliable

and standardized manner which is the main task of the first pillar of accord. Methods that are

prescribed in the provision of accord should be used to assess the risks. The portfolio of

banks and financial institutions in US is evaluated by the regulatory force which forces the

bank to use the service of credit rating agencies in order to be in compliance with the rules

(Bis.org 2019).

It is recognized by the act of Dodd Frank that there is a systematic importance of

credit ratings in the financial system. As per the act, the role of national recognized statistical

rating agency (NRSRO) should be reduced by using credit ratings in regulation that restricts

the holding of assets and set capital requirement for financial institutions. In addition to this,

In US, CRA is required to make a series of disclosures and such disclosures include

information on the procedures and policies for determining ratings, conflict of interest and

preventing the use of non public material information. The oversight of credit rating agencies

is further strengthened by the proposed regulations by SEC (Securities and exchange

committee). Such reforms are required ratings are often considered by investors in selling and

purchasing any security. The regulatory reforms directing credit agencies call for more

accountability and transparency and restructuring the rating industry like the profession of

public accounting (Arcelli et al. 2017). There is a proposal of promulgating generally

accepted rating principles as they influence the capital market enormously. The impact of the

loss of reliability in the ratings of CRA in US resulted in the new regulation that is based on

rules of SEC and credit rating agencies reforms. It can be seen that the current regulation

concerning credit rating agencies appears to be exhaustive and detailed. The amendment

requires providing SEC with the additional reports relating to credit action such as

downgrade, upgrade and placement for each class of security within each financial year.

The Basel II accord represents the set of rules concerning the role which the credit

rating agencies play in the financial market. The risk faced by banks is measured in a reliable

and standardized manner which is the main task of the first pillar of accord. Methods that are

prescribed in the provision of accord should be used to assess the risks. The portfolio of

banks and financial institutions in US is evaluated by the regulatory force which forces the

bank to use the service of credit rating agencies in order to be in compliance with the rules

(Bis.org 2019).

It is recognized by the act of Dodd Frank that there is a systematic importance of

credit ratings in the financial system. As per the act, the role of national recognized statistical

rating agency (NRSRO) should be reduced by using credit ratings in regulation that restricts

the holding of assets and set capital requirement for financial institutions. In addition to this,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CAPITAL MARKET AND TREASURY

the legal liabilities of credit rating agencies have been increased in accordance with Dodd

Frank Act which created a rule for making CRA legally liable (Sec.gov 2019).

The reforms for credit rating agencies adopted by SEC intend to protect against

conflict of interest, enhance governance and increase transparency for increasing the

accountability of agency and improving the credit rating quality. The overall quality of

ratings of credit agency would be strengthened by the package of reforms. Some of the

aspects of credit rating agencies that would be addressed by the new requirements of NRSRO

include conflict of interest, procedures to protect the rating methodologies transparency and

integrity, training standards, competence and experience of credit analyst, promoting credit

rating transparency by way of disclosure. The credit rating should have additional

certifications to accompany the credit ratings with the attestation that the business activities

do not influence rating (Nottingham.ac.uk 2019).

Evaluating the conditions of money market and global foreign exchange during 2014-

2019 and comparing the situation with that in 2009-2013:

In the first half of 2015, the reserves of global foreign currency declined in dollar

terms because of valuation effects associated with the depreciation of non dollar exchange

rate. In addition to this, there was a fall in the exchange reserves over $ 200 billion and

allocation of reserves appear to have increased when the impact of adjustment in the

exchange rate are accounted for. The first half of 2015 has marked China as the seller of

reserves, although the reserves of country were at a high level in relation to the rest of world.

Similarly, it is suggested by the estimates of Korean foreign exchange data about large

foreign exchange purchases. The foreign reserves of India reached at an all time high in year

2015 and it was in lieu of moderating the appreciation of pressure from inflow of foreign

investment because of purchasing of foreign currency by central bank (Occ.treas.gov 2019).

the legal liabilities of credit rating agencies have been increased in accordance with Dodd

Frank Act which created a rule for making CRA legally liable (Sec.gov 2019).

The reforms for credit rating agencies adopted by SEC intend to protect against

conflict of interest, enhance governance and increase transparency for increasing the

accountability of agency and improving the credit rating quality. The overall quality of

ratings of credit agency would be strengthened by the package of reforms. Some of the

aspects of credit rating agencies that would be addressed by the new requirements of NRSRO

include conflict of interest, procedures to protect the rating methodologies transparency and

integrity, training standards, competence and experience of credit analyst, promoting credit

rating transparency by way of disclosure. The credit rating should have additional

certifications to accompany the credit ratings with the attestation that the business activities

do not influence rating (Nottingham.ac.uk 2019).

Evaluating the conditions of money market and global foreign exchange during 2014-

2019 and comparing the situation with that in 2009-2013:

In the first half of 2015, the reserves of global foreign currency declined in dollar

terms because of valuation effects associated with the depreciation of non dollar exchange

rate. In addition to this, there was a fall in the exchange reserves over $ 200 billion and

allocation of reserves appear to have increased when the impact of adjustment in the

exchange rate are accounted for. The first half of 2015 has marked China as the seller of

reserves, although the reserves of country were at a high level in relation to the rest of world.

Similarly, it is suggested by the estimates of Korean foreign exchange data about large

foreign exchange purchases. The foreign reserves of India reached at an all time high in year

2015 and it was in lieu of moderating the appreciation of pressure from inflow of foreign

investment because of purchasing of foreign currency by central bank (Occ.treas.gov 2019).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CAPITAL MARKET AND TREASURY

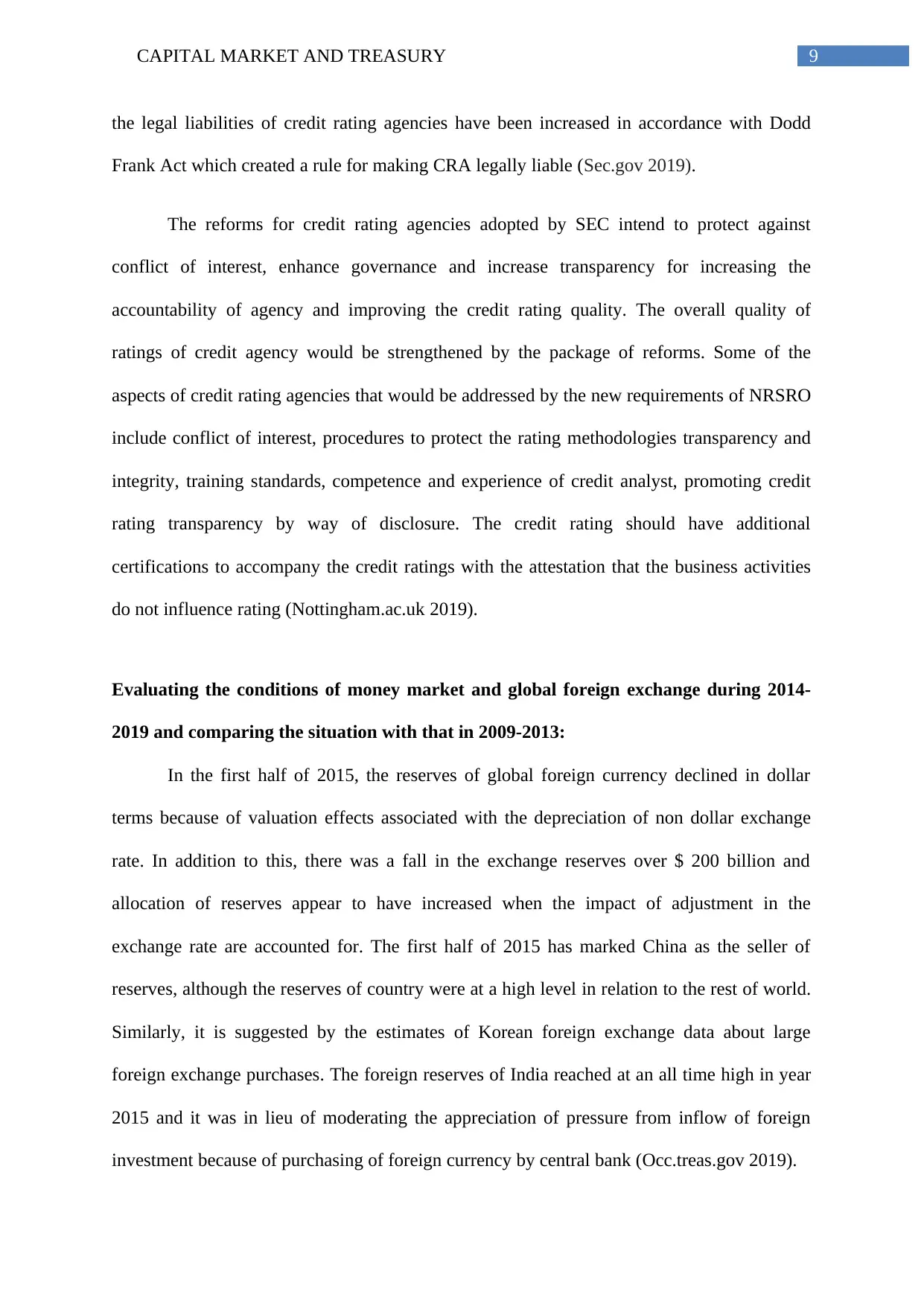

Toward the end of last year, the condition in the US dollar money markets was

tightened. For the regulatory purposes, the US dollar lending was reduced by the financial

market intermediaries over the year end period for minimizing the size of the balance sheet.

In early 2018, the conditions in the US dollar funding market eased particularly in repo and

foreign exchange swap (rba.gov.au 2019).

US dollar money market:

(Source: imf.org 2019)

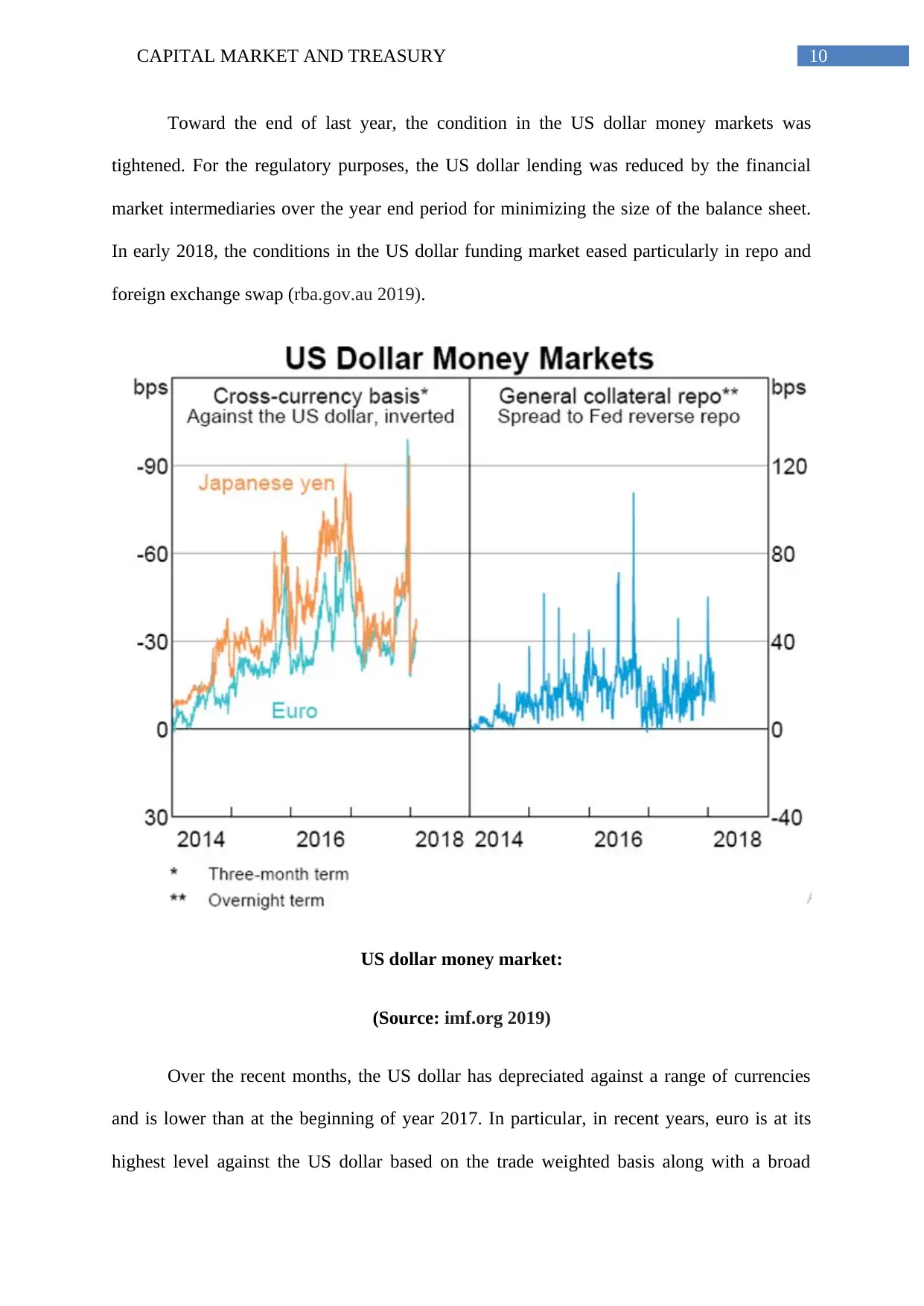

Over the recent months, the US dollar has depreciated against a range of currencies

and is lower than at the beginning of year 2017. In particular, in recent years, euro is at its

highest level against the US dollar based on the trade weighted basis along with a broad

Toward the end of last year, the condition in the US dollar money markets was

tightened. For the regulatory purposes, the US dollar lending was reduced by the financial

market intermediaries over the year end period for minimizing the size of the balance sheet.

In early 2018, the conditions in the US dollar funding market eased particularly in repo and

foreign exchange swap (rba.gov.au 2019).

US dollar money market:

(Source: imf.org 2019)

Over the recent months, the US dollar has depreciated against a range of currencies

and is lower than at the beginning of year 2017. In particular, in recent years, euro is at its

highest level against the US dollar based on the trade weighted basis along with a broad

11CAPITAL MARKET AND TREASURY

based improvement in economic conditions across region. A number of currencies

appreciated against the US dollar because of evolvement of expectation of market for

accommodating the withdrawal of monetary policy in other advanced economy and an

improvement in the global economic outlook. There has been increase in the price of

commodity that has provided an additional impetus for the currency appreciation in some

commodity exporting economies which included Australia (rba.gov.au 2019).

Exchange rate of Canadian, Japanese and US dollar:

(Source: imf.org 2019)

based improvement in economic conditions across region. A number of currencies

appreciated against the US dollar because of evolvement of expectation of market for

accommodating the withdrawal of monetary policy in other advanced economy and an

improvement in the global economic outlook. There has been increase in the price of

commodity that has provided an additional impetus for the currency appreciation in some

commodity exporting economies which included Australia (rba.gov.au 2019).

Exchange rate of Canadian, Japanese and US dollar:

(Source: imf.org 2019)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 27

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.