Capital Structure Analysis of Panasonic Manufacturing Berhad, Malaysia

VerifiedAdded on 2023/06/04

|6

|843

|66

Report

AI Summary

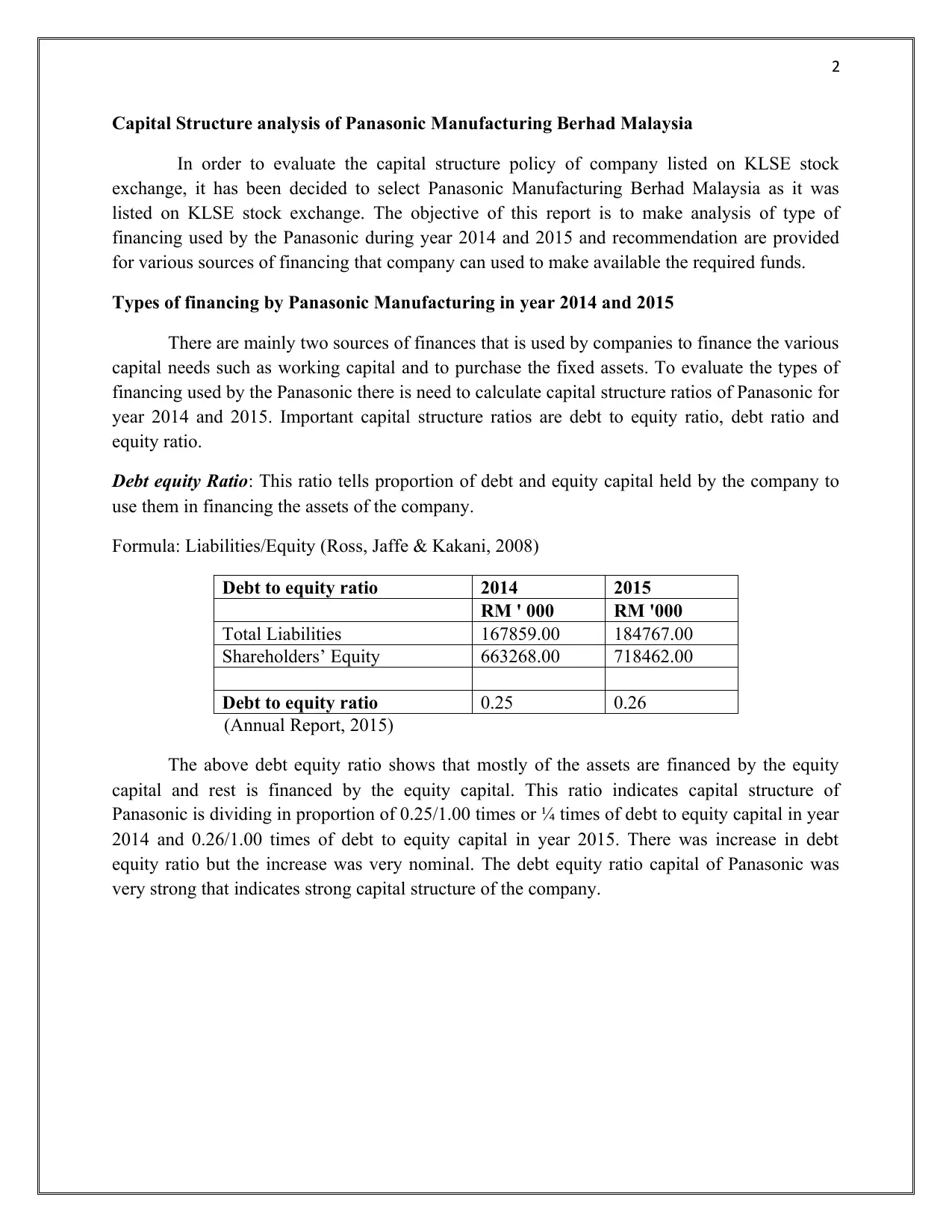

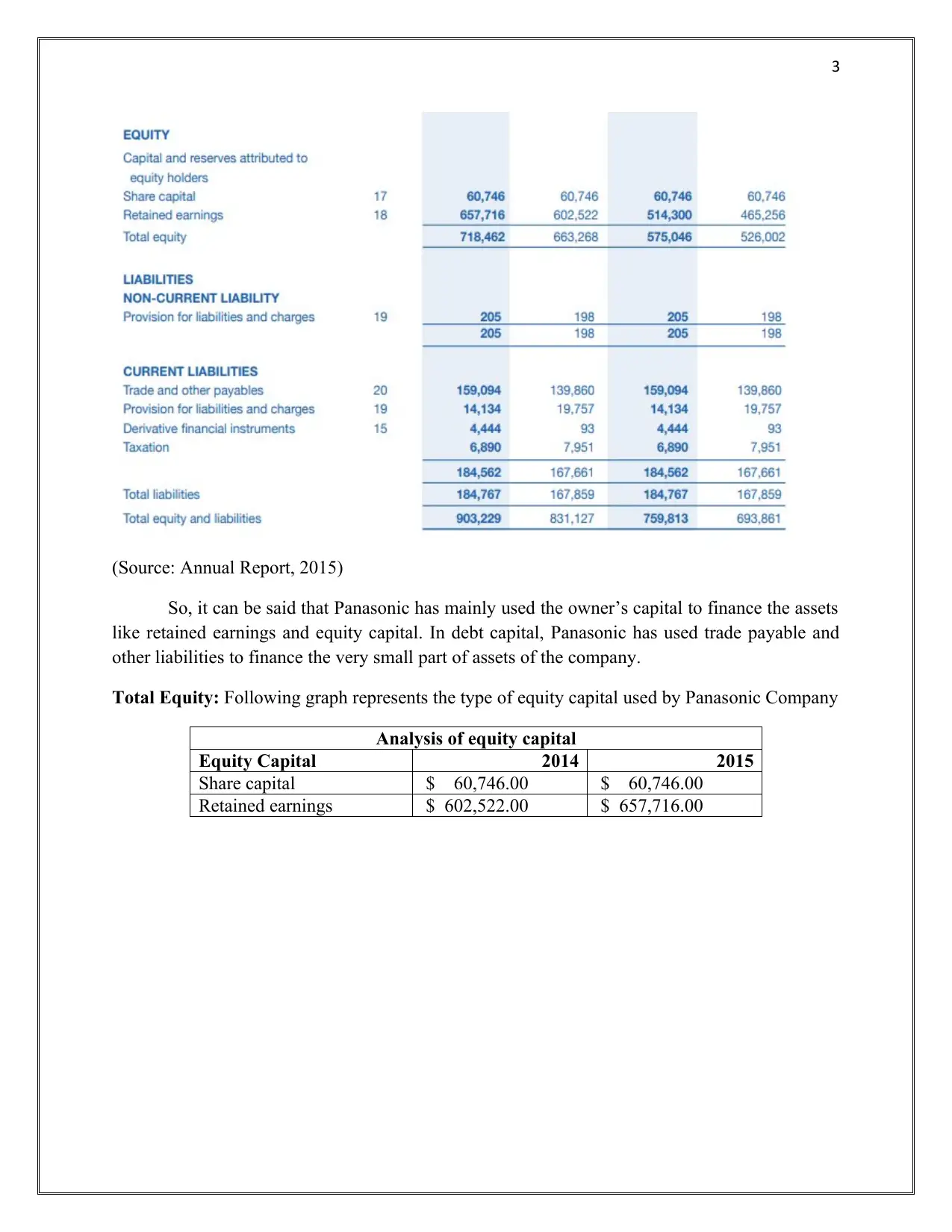

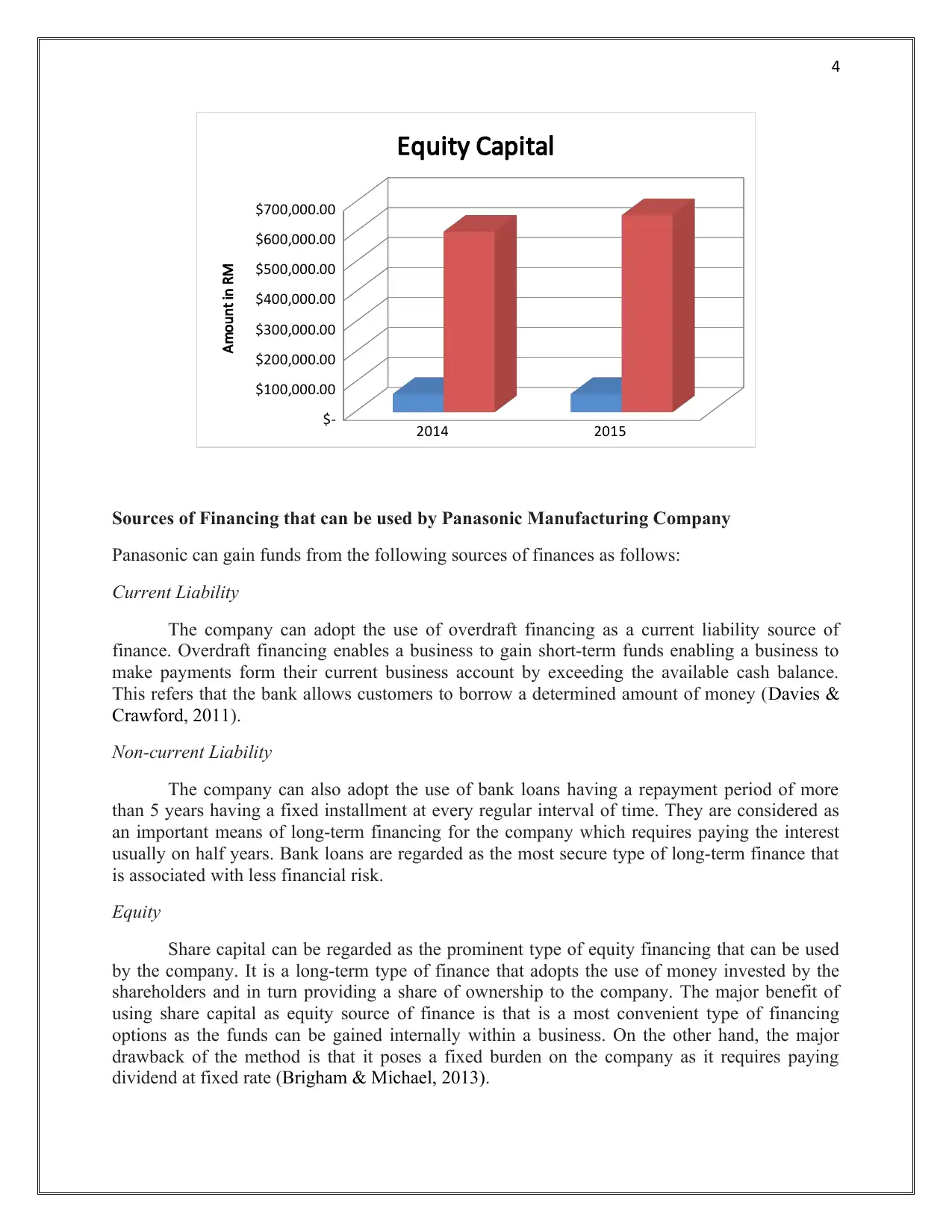

This report presents an analysis of the capital structure of Panasonic Manufacturing Berhad, a company listed on the KLSE stock exchange, focusing on the years 2014 and 2015. The objective is to evaluate the types of financing utilized by Panasonic and provide recommendations for future funding strategies. The analysis involves calculating key capital structure ratios, including the debt-to-equity ratio, debt ratio, and equity ratio, to assess the proportion of debt and equity financing. The report highlights the company's reliance on equity capital, particularly retained earnings, while also examining the use of current and non-current liabilities. Furthermore, the report explores potential sources of financing that Panasonic could leverage, such as overdraft financing, bank loans, and equity share capital. The findings indicate a strong capital structure for Panasonic and offer insights into optimizing its financial strategies.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.