Capital Structure and Valuation Project - Accommodate PLC Finance

VerifiedAdded on 2022/09/11

|11

|1607

|14

Project

AI Summary

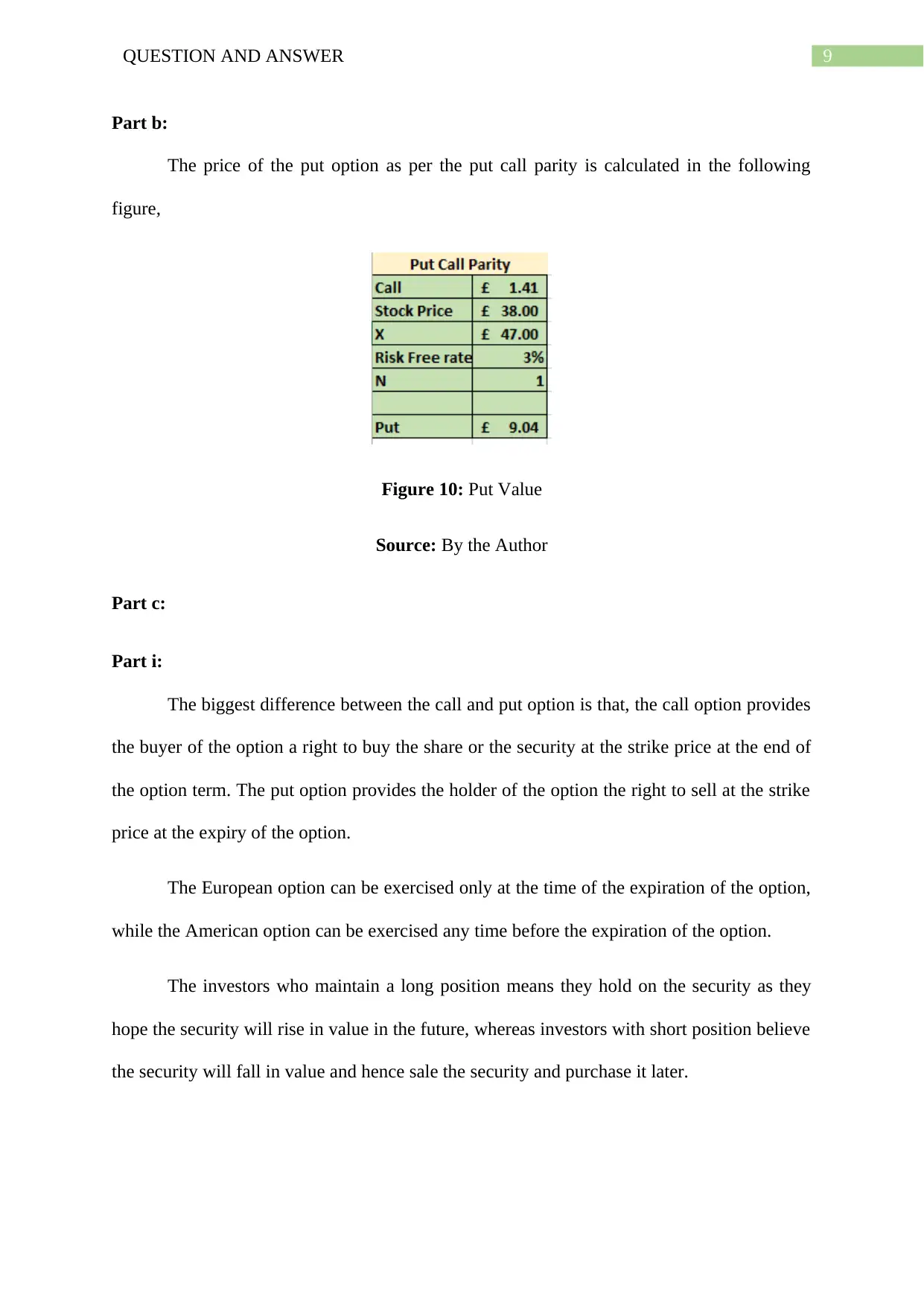

This project analyzes Accommodate PLC's financial decisions regarding a potential acquisition. It begins with a capital structure analysis, exploring the use of WACC and risk-adjusted WACC to evaluate the project's feasibility. The project calculates NPV to determine whether the investment should be accepted. It also delves into dividend policy, comparing residual dividend policy with constant growth, and discusses the benefits and limitations of each. The project further examines valuation methods, including net asset valuation, price-to-earnings ratio, and free cash flow valuation. Finally, it investigates option pricing using the Black-Scholes model and compares call and put options, along with the binomial option pricing model.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.