Financial Management Analysis of Petronas and Adventa Bhd

VerifiedAdded on 2022/11/23

|16

|4272

|70

Report

AI Summary

This report provides a comprehensive financial analysis of two Malaysian companies: Petronas (Oil and Gas) and Adventa Bhd (Healthcare), focusing on their capital structures from 2013 to 2017. The analysis includes the calculation of capital structure ratios, specifically the debt-to-equity ratio, to evaluate the level of debt (gearing) in each company's capital structure. The report further delves into the calculation of the weighted average cost of capital (WACC) for both companies, incorporating the cost of equity (calculated using the CAPM model) and the cost of debt. The financial performance of the companies is evaluated through the analysis of their return on equity (ROE) over the five-year period. The report also explores the impact of capital structure on the companies' financial risk and profitability. The analysis includes an explanation of capital structure theories, such as the impact of debt and equity financing, and their implications for the companies' financial health. The findings highlight the differences in capital structure between Petronas, with a lower debt level, and Adventa Bhd, which has a higher proportion of debt. The report concludes with recommendations for optimizing the capital structure of both companies, taking into account industry standards and the specific financial characteristics of each business. The report is written in response to an assignment brief requiring analysis of financial management in the context of Malaysian companies.

Running head: FINANCIAL MANAGEMENT

Financial Management

Name of the Student:

Name of the University:

Author’s Note:

Financial Management

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCIAL MANAGEMENT

Table of Contents

Introduction......................................................................................................................................2

Discussion........................................................................................................................................3

Capital Structure Ratio................................................................................................................3

Explanation of Companies Capital Structure Ratio’s..................................................................6

Capital Structure Theories...........................................................................................................8

Financial Performance...............................................................................................................10

Recommendations..........................................................................................................................11

Conclusion.....................................................................................................................................12

References......................................................................................................................................13

Table of Contents

Introduction......................................................................................................................................2

Discussion........................................................................................................................................3

Capital Structure Ratio................................................................................................................3

Explanation of Companies Capital Structure Ratio’s..................................................................6

Capital Structure Theories...........................................................................................................8

Financial Performance...............................................................................................................10

Recommendations..........................................................................................................................11

Conclusion.....................................................................................................................................12

References......................................................................................................................................13

2FINANCIAL MANAGEMENT

Introduction

Petronas Company operating as an integrating Oil and Gas Company has been taken into

consideration for the purpose of financial analysis of the company. The company is operating as

one of the global operating company with its wide range of services in the oil and gas services.

The company explores produces and delivers energy sources for the purpose of meeting the

growing demand globally (Watanabe et al., 2018). The company is operating in the Oil and Gas

Industry where the key products that the company delivers is the Petroleum, Natural Gas and

Petrochemicals. The operations of the business is spread globally with its main business centre in

Malaysia. The company was founded in the year 1974 and the operations of the company has

been growing sustainably for around 44 years (Choudhuri et al., 2018). The Malaysian

Government that oversees the operations and the management decision about the company owns

the ownership position of the company. The company is also having a sound employee base

whereby around 51,000 employees are currently employed in the business operations of the

company. The second company which is considered for the analysis is a healthcare company

which is Adventa Bhd which operates in Malaysia. The company was founded in 2004 and it is a

holding company under which several subsidiary companies also operates. The company mainly

includes healthcare companies but also a logistic line of operations and also provides distribution

services to different parties. The company in 2014 has also started a renal dialysis service which

would be the flagship business for the company. The company is well recognised in Malaysia for

its operations and provides invaluable services in terms of healthcare for the protection and

welfare of the residents of the country.

The weighted average cost of capital for both the company was calculated with the help

of the cost of equity and cost of debt for the firm along with the respective weights of equity and

Introduction

Petronas Company operating as an integrating Oil and Gas Company has been taken into

consideration for the purpose of financial analysis of the company. The company is operating as

one of the global operating company with its wide range of services in the oil and gas services.

The company explores produces and delivers energy sources for the purpose of meeting the

growing demand globally (Watanabe et al., 2018). The company is operating in the Oil and Gas

Industry where the key products that the company delivers is the Petroleum, Natural Gas and

Petrochemicals. The operations of the business is spread globally with its main business centre in

Malaysia. The company was founded in the year 1974 and the operations of the company has

been growing sustainably for around 44 years (Choudhuri et al., 2018). The Malaysian

Government that oversees the operations and the management decision about the company owns

the ownership position of the company. The company is also having a sound employee base

whereby around 51,000 employees are currently employed in the business operations of the

company. The second company which is considered for the analysis is a healthcare company

which is Adventa Bhd which operates in Malaysia. The company was founded in 2004 and it is a

holding company under which several subsidiary companies also operates. The company mainly

includes healthcare companies but also a logistic line of operations and also provides distribution

services to different parties. The company in 2014 has also started a renal dialysis service which

would be the flagship business for the company. The company is well recognised in Malaysia for

its operations and provides invaluable services in terms of healthcare for the protection and

welfare of the residents of the country.

The weighted average cost of capital for both the company was calculated with the help

of the cost of equity and cost of debt for the firm along with the respective weights of equity and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCIAL MANAGEMENT

debt in the financials of the company. Gearing level or the level of debt in the company has been

primarily stable in the financials of the company (Zaid, Kasuma & Gregory, 2018). The

weighted average cost of capital for the company was calculated with the help of the cost of

equity that was calculated with the CAPM Model. On the other hand, the cost of debt was

calculated with the help of the interest expenses paid and the weightage of debt in the financials

of the company. Return generated by the company on the shareholder’s equity of the company

for the two reported years by the company were taken into detailed analysis evaluating the

financial performance of the company. It is important to compare the level of profitability of the

company along with the undertaken capital structure of the company were taken into

consideration (Vătavu, 2015).

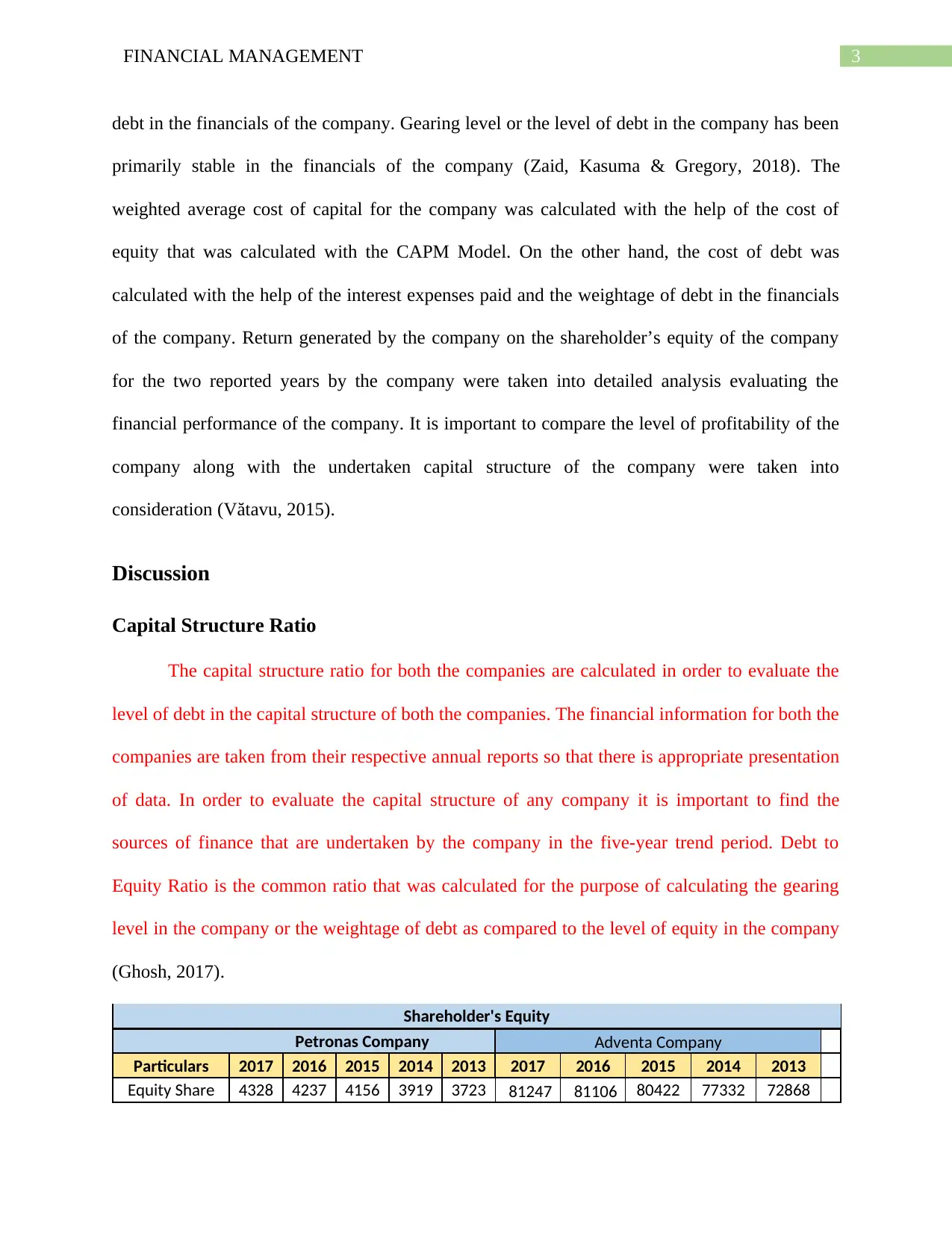

Discussion

Capital Structure Ratio

The capital structure ratio for both the companies are calculated in order to evaluate the

level of debt in the capital structure of both the companies. The financial information for both the

companies are taken from their respective annual reports so that there is appropriate presentation

of data. In order to evaluate the capital structure of any company it is important to find the

sources of finance that are undertaken by the company in the five-year trend period. Debt to

Equity Ratio is the common ratio that was calculated for the purpose of calculating the gearing

level in the company or the weightage of debt as compared to the level of equity in the company

(Ghosh, 2017).

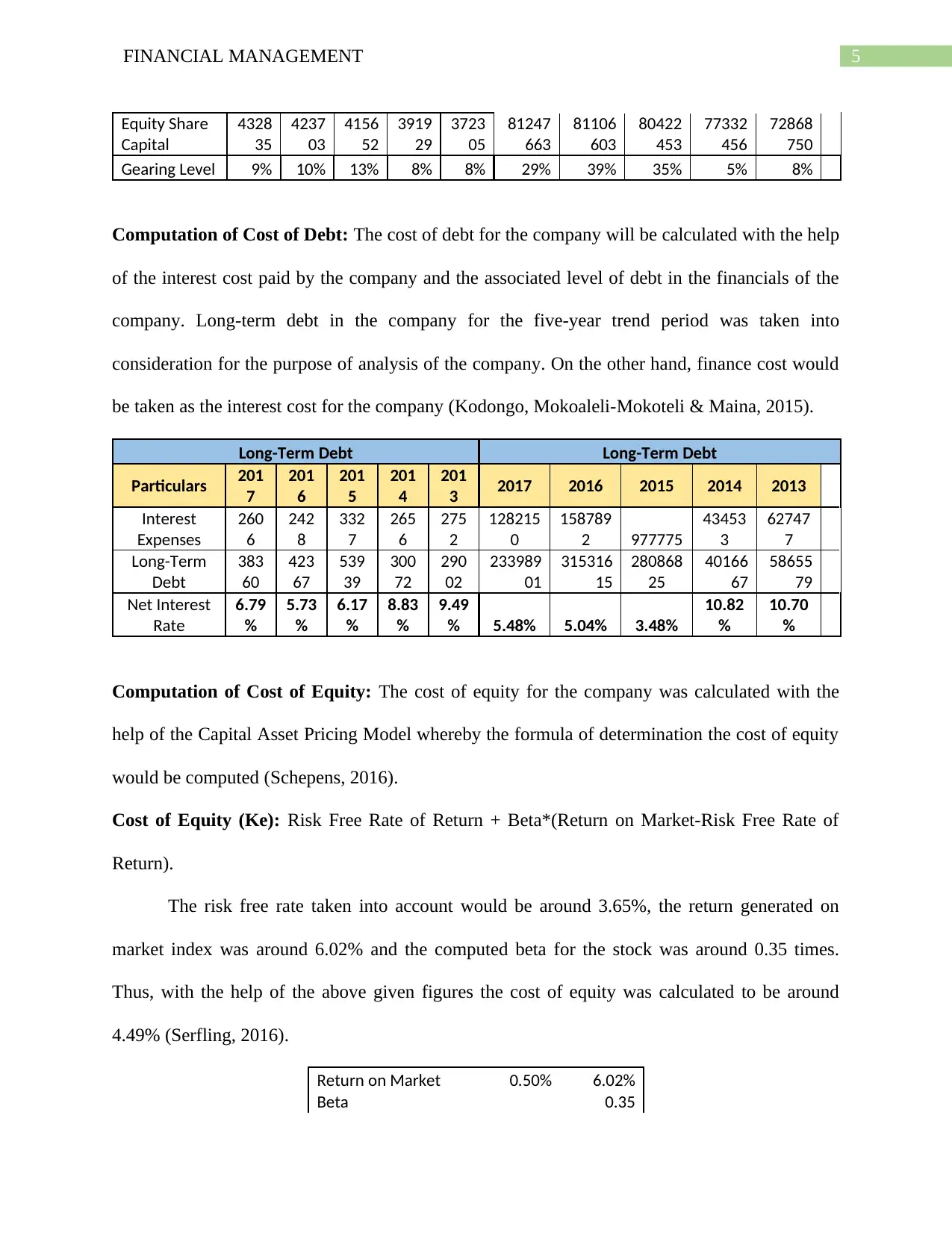

Shareholder's Equity

Petronas Company Adventa Company

Particulars 2017 2016 2015 2014 2013 2017 2016 2015 2014 2013

Equity Share 4328 4237 4156 3919 3723 81247 81106 80422 77332 72868

debt in the financials of the company. Gearing level or the level of debt in the company has been

primarily stable in the financials of the company (Zaid, Kasuma & Gregory, 2018). The

weighted average cost of capital for the company was calculated with the help of the cost of

equity that was calculated with the CAPM Model. On the other hand, the cost of debt was

calculated with the help of the interest expenses paid and the weightage of debt in the financials

of the company. Return generated by the company on the shareholder’s equity of the company

for the two reported years by the company were taken into detailed analysis evaluating the

financial performance of the company. It is important to compare the level of profitability of the

company along with the undertaken capital structure of the company were taken into

consideration (Vătavu, 2015).

Discussion

Capital Structure Ratio

The capital structure ratio for both the companies are calculated in order to evaluate the

level of debt in the capital structure of both the companies. The financial information for both the

companies are taken from their respective annual reports so that there is appropriate presentation

of data. In order to evaluate the capital structure of any company it is important to find the

sources of finance that are undertaken by the company in the five-year trend period. Debt to

Equity Ratio is the common ratio that was calculated for the purpose of calculating the gearing

level in the company or the weightage of debt as compared to the level of equity in the company

(Ghosh, 2017).

Shareholder's Equity

Petronas Company Adventa Company

Particulars 2017 2016 2015 2014 2013 2017 2016 2015 2014 2013

Equity Share 4328 4237 4156 3919 3723 81247 81106 80422 77332 72868

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCIAL MANAGEMENT

Capital 35 03 52 29 05 663 603 453 456 750

Long-Term Debt Long-Term Debt

Particulars 2017 2016 2015 2014 2013 2017 2016 2015 2014 2013

Interest

Expenses 2606 2428 3327 2656 2752

12821

50

15878

92

97777

5

43453

3

62747

7

Long-Term

Debt

3836

0

4236

7

5393

9

3007

2

2900

2

23398

901

31531

615

28086

825

40166

67

58655

79

Net Interest

Rate

6.79

%

5.73

%

6.17

%

8.83

%

9.49

% 5.48% 5.04% 3.48%

10.82

%

10.70

%

Past Performance Past Performance

Particulars 2017 2016 2015 2014 2013 2017 2016 2015 2014 2013

Net Profit

4551

8

2376

2

2086

2

4761

3

6558

6

14106

0

68415

0

30899

97

44637

06

82379

094

Shareholder's

Equity

4328

35

4237

03

4156

52

3919

29

3723

05

81247

663

81106

603

80422

453

77332

456

72868

750

Return on

Equity 11% 6% 5% 12% 18% 0% 1% 4% 6% 113%

Gearing Level Gearing Level

Particulars 2017 2016 2015 2014 2013 2017 2016 2015 2014 2013

Long-Term

Debt

3836

0

4236

7

5393

9

3007

2

2900

2

23398

901

31531

615

28086

825

40166

67

58655

79

Equity Share

Capital

4328

35

4237

03

4156

52

3919

29

3723

05

81247

663

81106

603

80422

453

77332

456

72868

750

Gearing Level 9% 10% 13% 8% 8% 29% 39% 35% 5% 8%

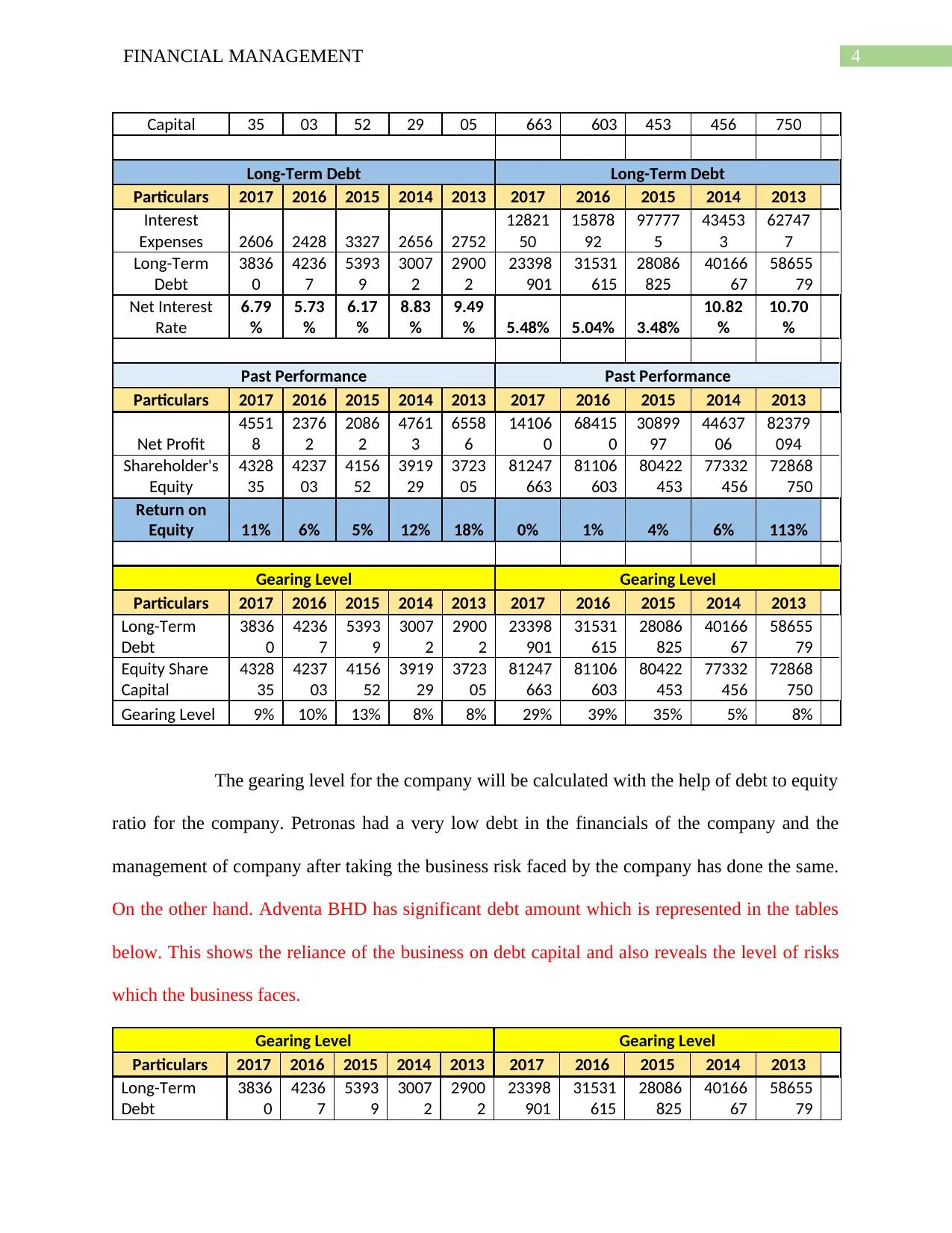

The gearing level for the company will be calculated with the help of debt to equity

ratio for the company. Petronas had a very low debt in the financials of the company and the

management of company after taking the business risk faced by the company has done the same.

On the other hand. Adventa BHD has significant debt amount which is represented in the tables

below. This shows the reliance of the business on debt capital and also reveals the level of risks

which the business faces.

Gearing Level Gearing Level

Particulars 2017 2016 2015 2014 2013 2017 2016 2015 2014 2013

Long-Term

Debt

3836

0

4236

7

5393

9

3007

2

2900

2

23398

901

31531

615

28086

825

40166

67

58655

79

Capital 35 03 52 29 05 663 603 453 456 750

Long-Term Debt Long-Term Debt

Particulars 2017 2016 2015 2014 2013 2017 2016 2015 2014 2013

Interest

Expenses 2606 2428 3327 2656 2752

12821

50

15878

92

97777

5

43453

3

62747

7

Long-Term

Debt

3836

0

4236

7

5393

9

3007

2

2900

2

23398

901

31531

615

28086

825

40166

67

58655

79

Net Interest

Rate

6.79

%

5.73

%

6.17

%

8.83

%

9.49

% 5.48% 5.04% 3.48%

10.82

%

10.70

%

Past Performance Past Performance

Particulars 2017 2016 2015 2014 2013 2017 2016 2015 2014 2013

Net Profit

4551

8

2376

2

2086

2

4761

3

6558

6

14106

0

68415

0

30899

97

44637

06

82379

094

Shareholder's

Equity

4328

35

4237

03

4156

52

3919

29

3723

05

81247

663

81106

603

80422

453

77332

456

72868

750

Return on

Equity 11% 6% 5% 12% 18% 0% 1% 4% 6% 113%

Gearing Level Gearing Level

Particulars 2017 2016 2015 2014 2013 2017 2016 2015 2014 2013

Long-Term

Debt

3836

0

4236

7

5393

9

3007

2

2900

2

23398

901

31531

615

28086

825

40166

67

58655

79

Equity Share

Capital

4328

35

4237

03

4156

52

3919

29

3723

05

81247

663

81106

603

80422

453

77332

456

72868

750

Gearing Level 9% 10% 13% 8% 8% 29% 39% 35% 5% 8%

The gearing level for the company will be calculated with the help of debt to equity

ratio for the company. Petronas had a very low debt in the financials of the company and the

management of company after taking the business risk faced by the company has done the same.

On the other hand. Adventa BHD has significant debt amount which is represented in the tables

below. This shows the reliance of the business on debt capital and also reveals the level of risks

which the business faces.

Gearing Level Gearing Level

Particulars 2017 2016 2015 2014 2013 2017 2016 2015 2014 2013

Long-Term

Debt

3836

0

4236

7

5393

9

3007

2

2900

2

23398

901

31531

615

28086

825

40166

67

58655

79

5FINANCIAL MANAGEMENT

Equity Share

Capital

4328

35

4237

03

4156

52

3919

29

3723

05

81247

663

81106

603

80422

453

77332

456

72868

750

Gearing Level 9% 10% 13% 8% 8% 29% 39% 35% 5% 8%

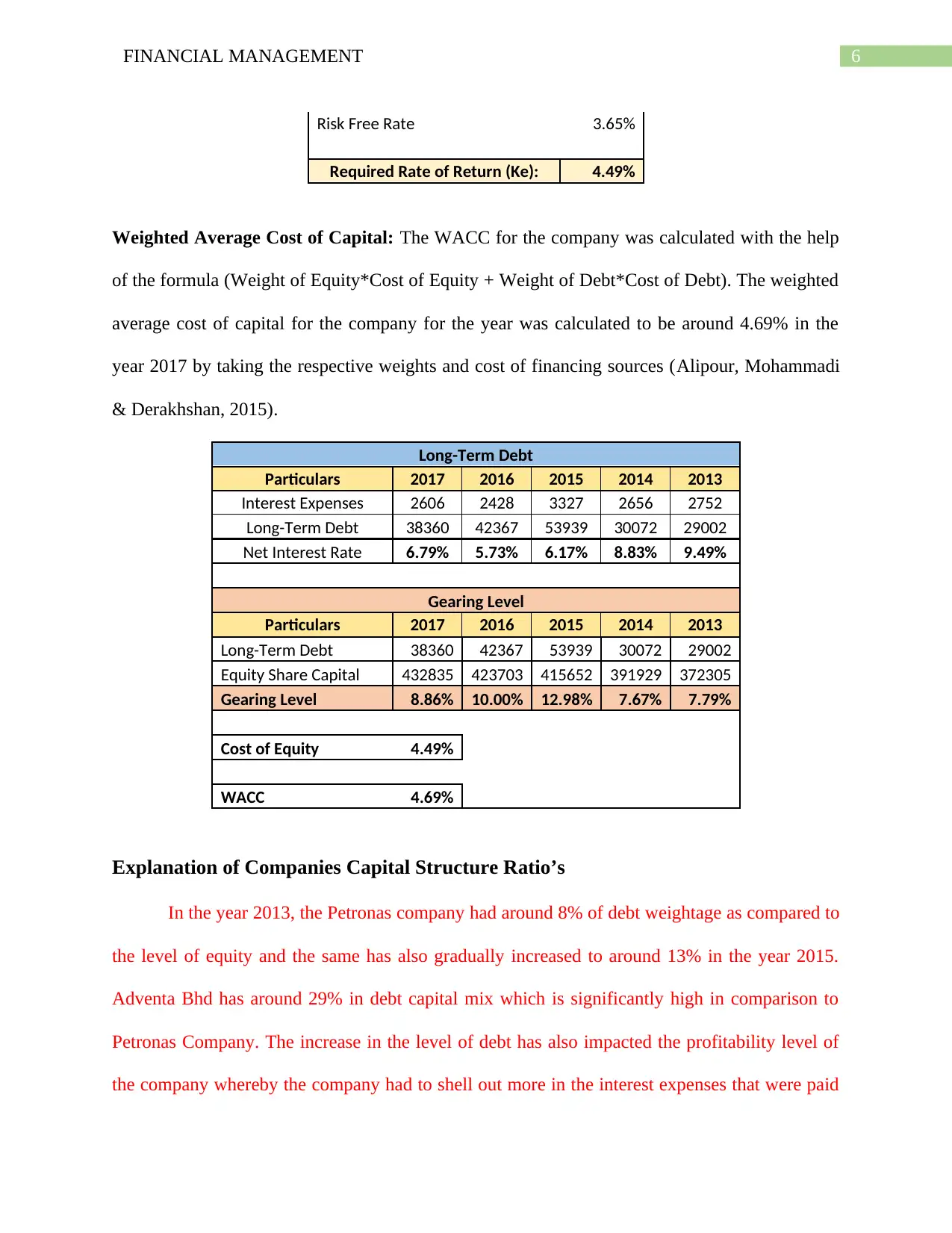

Computation of Cost of Debt: The cost of debt for the company will be calculated with the help

of the interest cost paid by the company and the associated level of debt in the financials of the

company. Long-term debt in the company for the five-year trend period was taken into

consideration for the purpose of analysis of the company. On the other hand, finance cost would

be taken as the interest cost for the company (Kodongo, Mokoaleli-Mokoteli & Maina, 2015).

Long-Term Debt Long-Term Debt

Particulars 201

7

201

6

201

5

201

4

201

3 2017 2016 2015 2014 2013

Interest

Expenses

260

6

242

8

332

7

265

6

275

2

128215

0

158789

2 977775

43453

3

62747

7

Long-Term

Debt

383

60

423

67

539

39

300

72

290

02

233989

01

315316

15

280868

25

40166

67

58655

79

Net Interest

Rate

6.79

%

5.73

%

6.17

%

8.83

%

9.49

% 5.48% 5.04% 3.48%

10.82

%

10.70

%

Computation of Cost of Equity: The cost of equity for the company was calculated with the

help of the Capital Asset Pricing Model whereby the formula of determination the cost of equity

would be computed (Schepens, 2016).

Cost of Equity (Ke): Risk Free Rate of Return + Beta*(Return on Market-Risk Free Rate of

Return).

The risk free rate taken into account would be around 3.65%, the return generated on

market index was around 6.02% and the computed beta for the stock was around 0.35 times.

Thus, with the help of the above given figures the cost of equity was calculated to be around

4.49% (Serfling, 2016).

Return on Market 0.50% 6.02%

Beta 0.35

Equity Share

Capital

4328

35

4237

03

4156

52

3919

29

3723

05

81247

663

81106

603

80422

453

77332

456

72868

750

Gearing Level 9% 10% 13% 8% 8% 29% 39% 35% 5% 8%

Computation of Cost of Debt: The cost of debt for the company will be calculated with the help

of the interest cost paid by the company and the associated level of debt in the financials of the

company. Long-term debt in the company for the five-year trend period was taken into

consideration for the purpose of analysis of the company. On the other hand, finance cost would

be taken as the interest cost for the company (Kodongo, Mokoaleli-Mokoteli & Maina, 2015).

Long-Term Debt Long-Term Debt

Particulars 201

7

201

6

201

5

201

4

201

3 2017 2016 2015 2014 2013

Interest

Expenses

260

6

242

8

332

7

265

6

275

2

128215

0

158789

2 977775

43453

3

62747

7

Long-Term

Debt

383

60

423

67

539

39

300

72

290

02

233989

01

315316

15

280868

25

40166

67

58655

79

Net Interest

Rate

6.79

%

5.73

%

6.17

%

8.83

%

9.49

% 5.48% 5.04% 3.48%

10.82

%

10.70

%

Computation of Cost of Equity: The cost of equity for the company was calculated with the

help of the Capital Asset Pricing Model whereby the formula of determination the cost of equity

would be computed (Schepens, 2016).

Cost of Equity (Ke): Risk Free Rate of Return + Beta*(Return on Market-Risk Free Rate of

Return).

The risk free rate taken into account would be around 3.65%, the return generated on

market index was around 6.02% and the computed beta for the stock was around 0.35 times.

Thus, with the help of the above given figures the cost of equity was calculated to be around

4.49% (Serfling, 2016).

Return on Market 0.50% 6.02%

Beta 0.35

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCIAL MANAGEMENT

Risk Free Rate 3.65%

Required Rate of Return (Ke): 4.49%

Weighted Average Cost of Capital: The WACC for the company was calculated with the help

of the formula (Weight of Equity*Cost of Equity + Weight of Debt*Cost of Debt). The weighted

average cost of capital for the company for the year was calculated to be around 4.69% in the

year 2017 by taking the respective weights and cost of financing sources (Alipour, Mohammadi

& Derakhshan, 2015).

Long-Term Debt

Particulars 2017 2016 2015 2014 2013

Interest Expenses 2606 2428 3327 2656 2752

Long-Term Debt 38360 42367 53939 30072 29002

Net Interest Rate 6.79% 5.73% 6.17% 8.83% 9.49%

Gearing Level

Particulars 2017 2016 2015 2014 2013

Long-Term Debt 38360 42367 53939 30072 29002

Equity Share Capital 432835 423703 415652 391929 372305

Gearing Level 8.86% 10.00% 12.98% 7.67% 7.79%

Cost of Equity 4.49%

WACC 4.69%

Explanation of Companies Capital Structure Ratio’s

In the year 2013, the Petronas company had around 8% of debt weightage as compared to

the level of equity and the same has also gradually increased to around 13% in the year 2015.

Adventa Bhd has around 29% in debt capital mix which is significantly high in comparison to

Petronas Company. The increase in the level of debt has also impacted the profitability level of

the company whereby the company had to shell out more in the interest expenses that were paid

Risk Free Rate 3.65%

Required Rate of Return (Ke): 4.49%

Weighted Average Cost of Capital: The WACC for the company was calculated with the help

of the formula (Weight of Equity*Cost of Equity + Weight of Debt*Cost of Debt). The weighted

average cost of capital for the company for the year was calculated to be around 4.69% in the

year 2017 by taking the respective weights and cost of financing sources (Alipour, Mohammadi

& Derakhshan, 2015).

Long-Term Debt

Particulars 2017 2016 2015 2014 2013

Interest Expenses 2606 2428 3327 2656 2752

Long-Term Debt 38360 42367 53939 30072 29002

Net Interest Rate 6.79% 5.73% 6.17% 8.83% 9.49%

Gearing Level

Particulars 2017 2016 2015 2014 2013

Long-Term Debt 38360 42367 53939 30072 29002

Equity Share Capital 432835 423703 415652 391929 372305

Gearing Level 8.86% 10.00% 12.98% 7.67% 7.79%

Cost of Equity 4.49%

WACC 4.69%

Explanation of Companies Capital Structure Ratio’s

In the year 2013, the Petronas company had around 8% of debt weightage as compared to

the level of equity and the same has also gradually increased to around 13% in the year 2015.

Adventa Bhd has around 29% in debt capital mix which is significantly high in comparison to

Petronas Company. The increase in the level of debt has also impacted the profitability level of

the company whereby the company had to shell out more in the interest expenses that were paid

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL MANAGEMENT

by the company. Financial risk of the company also had increased in the year 2015 that would be

limiting the ability of the company in taking business risk associated with the operations of the

company (Liang et al., 2016). However, keeping the same intact and into account the

management of the company has undertaken actions to reduce the level of debt in the financials

of the company in the financial year 2016-2017. Equity financing is comparatively better than

debt financing but it comes along with the high cost associated of equity financing. On the other

hand, the company can also get advantage of debt financing when it comes to calculation of the

effective tax rate evaluation. Both advantages and as well as disadvantages of debt financing is

associated with the company but it is important that the companies have an optimal capital

structure in the financials of the company. The capital structure of the company should also be in

the view of industry standards i.e., the level of debt in the financials of the company (Demirguc-

Kunt, Martinez-Peria & Tressel, 2015). The level of equity financing is the other important thing

that the company should consider while evaluating the capital structure of the company as the

same is not only safe financing option but also gives the liberty to the management of the

company to undertake various operational and business risk for the operations of the company.

Capital structure of the company should be reviewed on a periodic basis and the same should be

well compatible with the various level of operations of the company (Elsas & Florysiak, 2015).

The capital structure of the Petronas Company has been comparatively stable where the

associated level of debt has been comparatively lower but at the same time it is important that the

company should consider their effective tax rate when analysing the benefit and costs associated

with the same. On the other hand, the capital structure of Adventa Bhd is not stable as there is a

quite high proportion of debt capital which is used by the business which suggest that the

business faces tremendous amount of risks and also faces capital or liquidity shortages.

by the company. Financial risk of the company also had increased in the year 2015 that would be

limiting the ability of the company in taking business risk associated with the operations of the

company (Liang et al., 2016). However, keeping the same intact and into account the

management of the company has undertaken actions to reduce the level of debt in the financials

of the company in the financial year 2016-2017. Equity financing is comparatively better than

debt financing but it comes along with the high cost associated of equity financing. On the other

hand, the company can also get advantage of debt financing when it comes to calculation of the

effective tax rate evaluation. Both advantages and as well as disadvantages of debt financing is

associated with the company but it is important that the companies have an optimal capital

structure in the financials of the company. The capital structure of the company should also be in

the view of industry standards i.e., the level of debt in the financials of the company (Demirguc-

Kunt, Martinez-Peria & Tressel, 2015). The level of equity financing is the other important thing

that the company should consider while evaluating the capital structure of the company as the

same is not only safe financing option but also gives the liberty to the management of the

company to undertake various operational and business risk for the operations of the company.

Capital structure of the company should be reviewed on a periodic basis and the same should be

well compatible with the various level of operations of the company (Elsas & Florysiak, 2015).

The capital structure of the Petronas Company has been comparatively stable where the

associated level of debt has been comparatively lower but at the same time it is important that the

company should consider their effective tax rate when analysing the benefit and costs associated

with the same. On the other hand, the capital structure of Adventa Bhd is not stable as there is a

quite high proportion of debt capital which is used by the business which suggest that the

business faces tremendous amount of risks and also faces capital or liquidity shortages.

8FINANCIAL MANAGEMENT

The key factor that influences the capital structure of the company is the applicability of

the equity or debt financing that is available to the company. Petronas as a Government

Company has also On the other hand the cost of each source of financing is the other key factor

that influences significantly while calculating the optimal capital structure of the company. The

level of debt financing in the company is also a crucial part while calculating the associated

capital structure of the company. The cost of debt for the company can be calculated with the

help of the interest and debt levels in the financial statements of the company (Brusov et al.,

2018).

Capital Structure Theories

Capital Structure applies all relevant combination and various sources of finance that the

company can apply in the capital structure of the company. Capital Structure Theories include

Equity financing, Reserves, Preference Share Capital, Loan and Debentures. It is dependent on

the company to apply various sources of finance and the same should be compatible with the

operations and financials of the company (Onatca Engin, Unver Erbas & Sokmen, 2019). The

theories that can explain the capital structure prevailing are as follows:

Net Income Approach: The net income approach is approached by Duxoisrand and is

much favour of the financial decision of taking leverage. Any change in the leverage can

lead to the difference in the cost of capital for the company. The theory states that

addition in debt in the financial position of the company would ultimately be decreasing

the weighted average cost of capital for the company, which further would increase the

value of the firm (Serrasqueiro & Caetano, 2015).

Net Operating Income Approach: The theory was introduced by Durand and is

completely different from the Net Income Approach when the applicable taxation rate

The key factor that influences the capital structure of the company is the applicability of

the equity or debt financing that is available to the company. Petronas as a Government

Company has also On the other hand the cost of each source of financing is the other key factor

that influences significantly while calculating the optimal capital structure of the company. The

level of debt financing in the company is also a crucial part while calculating the associated

capital structure of the company. The cost of debt for the company can be calculated with the

help of the interest and debt levels in the financial statements of the company (Brusov et al.,

2018).

Capital Structure Theories

Capital Structure applies all relevant combination and various sources of finance that the

company can apply in the capital structure of the company. Capital Structure Theories include

Equity financing, Reserves, Preference Share Capital, Loan and Debentures. It is dependent on

the company to apply various sources of finance and the same should be compatible with the

operations and financials of the company (Onatca Engin, Unver Erbas & Sokmen, 2019). The

theories that can explain the capital structure prevailing are as follows:

Net Income Approach: The net income approach is approached by Duxoisrand and is

much favour of the financial decision of taking leverage. Any change in the leverage can

lead to the difference in the cost of capital for the company. The theory states that

addition in debt in the financial position of the company would ultimately be decreasing

the weighted average cost of capital for the company, which further would increase the

value of the firm (Serrasqueiro & Caetano, 2015).

Net Operating Income Approach: The theory was introduced by Durand and is

completely different from the Net Income Approach when the applicable taxation rate

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCIAL MANAGEMENT

does not exist. The theory states that the weighted average cost of capital for the company

remains constant for the company (Muritala, 2018). The theory believes states that the

valuation of the firm is not affected by the debt to equity ratio, instead there are specific

and other aspects that the investors analyses and review while valuation of the firm based

on a specific discount rate that will be applicable for the company. But the crucial point is

that the theory states that if there are information regarding the applicable tax rate given

for the analysis then the firm should intake more amount of debt thereby reducing the

weighted average cost of capital for the company and increasing the value of the firm.

Traditional Approach: The theory states that the cost of capital for the company is a

function of the capital structure that is adopted by the company in the financials of the

company. The key and crucial thing to note in this regard is that the optimal capital

structure is the key point that the theory focuses on. In terms of optimal capital structure

the theory states that the value of the firm will be at a optimal rate when the capital

structure of the firm is in accordance with the business and financial operational

operations of the company thereby suiting the overall financing scenario for the company

(Lin, 2017).

Modigliani and Miller Approach: The capital structure theory was named after the

Franco Modigliani and Merton Miller. The MM theory proposed two of the key

propositions as:

Proposition 1: The first proposition for the firm says that whatever the capital

structure exist for the company, the same stays irrelevant for the company. The

value of two identical firms would be remaining the same and the value of the

does not exist. The theory states that the weighted average cost of capital for the company

remains constant for the company (Muritala, 2018). The theory believes states that the

valuation of the firm is not affected by the debt to equity ratio, instead there are specific

and other aspects that the investors analyses and review while valuation of the firm based

on a specific discount rate that will be applicable for the company. But the crucial point is

that the theory states that if there are information regarding the applicable tax rate given

for the analysis then the firm should intake more amount of debt thereby reducing the

weighted average cost of capital for the company and increasing the value of the firm.

Traditional Approach: The theory states that the cost of capital for the company is a

function of the capital structure that is adopted by the company in the financials of the

company. The key and crucial thing to note in this regard is that the optimal capital

structure is the key point that the theory focuses on. In terms of optimal capital structure

the theory states that the value of the firm will be at a optimal rate when the capital

structure of the firm is in accordance with the business and financial operational

operations of the company thereby suiting the overall financing scenario for the company

(Lin, 2017).

Modigliani and Miller Approach: The capital structure theory was named after the

Franco Modigliani and Merton Miller. The MM theory proposed two of the key

propositions as:

Proposition 1: The first proposition for the firm says that whatever the capital

structure exist for the company, the same stays irrelevant for the company. The

value of two identical firms would be remaining the same and the value of the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCIAL MANAGEMENT

firm would not be affected by the choice of financing sources that would be

adopted by the company for the purpose of financing.

Proposition 2: The second proposition for the firm says that the financial

leverage would be boosting the value of the firm and further would be reducing

the WACC. The theory is applicable when information regarding taxation is

given.

Financial Performance

The financial performance of Petronas Company from the year 2013-2017 trend period

has been volatile from 18% return on equity in the year 2013 to around 5% in the year 2015 were

some of the key evolution that were noted in the financials of Petronas Company. The past

performance of the company can be well compared with the help of the variability in the

profitability of the company with the changes in the level of debt in the company. It is for sure if

the associated level of debt increases for the company then the associated cost of debt would be

rising for the company. The financials of Adventa Bhd shows that the return for 2017 is lower

than 1% which shows that the company is not earning profits in the current times. The profits

and returns which is generated by the business is falling as the table which is shown below

suggests

The net cost of interest that is paid by the company is also dependent on the actual

interest expenses, which is determined after taking on various factors like the associated business

risk and the overall risk associated with the company (PETRONAS GLOBAL, 2019).

Past Performance Past Performance

Particulars 2017 2016 2015 2014 2013 2017 2016 2015 2014 2013

Net Profit

4551

8

2376

2

2086

2

4761

3

6558

6

14106

0

68415

0

30899

97

44637

06

82379

094

Shareholder's

Equity

4328

35

4237

03

4156

52

3919

29

3723

05

81247

663

81106

603

80422

453

77332

456

72868

750

firm would not be affected by the choice of financing sources that would be

adopted by the company for the purpose of financing.

Proposition 2: The second proposition for the firm says that the financial

leverage would be boosting the value of the firm and further would be reducing

the WACC. The theory is applicable when information regarding taxation is

given.

Financial Performance

The financial performance of Petronas Company from the year 2013-2017 trend period

has been volatile from 18% return on equity in the year 2013 to around 5% in the year 2015 were

some of the key evolution that were noted in the financials of Petronas Company. The past

performance of the company can be well compared with the help of the variability in the

profitability of the company with the changes in the level of debt in the company. It is for sure if

the associated level of debt increases for the company then the associated cost of debt would be

rising for the company. The financials of Adventa Bhd shows that the return for 2017 is lower

than 1% which shows that the company is not earning profits in the current times. The profits

and returns which is generated by the business is falling as the table which is shown below

suggests

The net cost of interest that is paid by the company is also dependent on the actual

interest expenses, which is determined after taking on various factors like the associated business

risk and the overall risk associated with the company (PETRONAS GLOBAL, 2019).

Past Performance Past Performance

Particulars 2017 2016 2015 2014 2013 2017 2016 2015 2014 2013

Net Profit

4551

8

2376

2

2086

2

4761

3

6558

6

14106

0

68415

0

30899

97

44637

06

82379

094

Shareholder's

Equity

4328

35

4237

03

4156

52

3919

29

3723

05

81247

663

81106

603

80422

453

77332

456

72868

750

11FINANCIAL MANAGEMENT

Return on

Equity 11% 6% 5% 12% 18% 0% 1% 4% 6% 113%

In terms of valuation of the firm, it is well said that the capital structure of the company

plays a crucial and an important role in the overall valuation of the firm. Different theories have

their own belief regarding the optimal capital structure of a firm and how the same is linked to

the financial performance of the company. However, it is key that the capital structure of the firm

should be on an optimal basis after looking the various aspects of the firm after talking in the

business and the financial aspects of the company. The capital structure of the firm should be

such that it allows the management of the company to take the amount of optimal risk in the

operations of the company so that the value of the firm can be maximized by the actions and

strategies that will be built by the company (PETRONAS GLOBAL, 2019). The capital structure

of the firm should be such that the weighted average cost of capital reduces for the firm and the

same could be done with the help of increasing weightage of low cost financing in the capital

structure of the company. However, the same can be compared with the help of the debt

financing for the company where the increase in the debt financing would have slowed down the

net profitability of the company but on the other hand, the same may increase the residual

income of the company (PETRONAS GLOBAL, 2019).

Recommendations

The analysis of the financials of the company stated that the Petronas Company had a

very low amount of debt in the financial statement of the company. It is recommended that the

management of the company should reduce the WACC of the company with the help of the

increase in the debt in the financing sources. The introduction of the debt should be done at an

optimal point keeping the debt to equity ratio compatible with the financial performance of the

Return on

Equity 11% 6% 5% 12% 18% 0% 1% 4% 6% 113%

In terms of valuation of the firm, it is well said that the capital structure of the company

plays a crucial and an important role in the overall valuation of the firm. Different theories have

their own belief regarding the optimal capital structure of a firm and how the same is linked to

the financial performance of the company. However, it is key that the capital structure of the firm

should be on an optimal basis after looking the various aspects of the firm after talking in the

business and the financial aspects of the company. The capital structure of the firm should be

such that it allows the management of the company to take the amount of optimal risk in the

operations of the company so that the value of the firm can be maximized by the actions and

strategies that will be built by the company (PETRONAS GLOBAL, 2019). The capital structure

of the firm should be such that the weighted average cost of capital reduces for the firm and the

same could be done with the help of increasing weightage of low cost financing in the capital

structure of the company. However, the same can be compared with the help of the debt

financing for the company where the increase in the debt financing would have slowed down the

net profitability of the company but on the other hand, the same may increase the residual

income of the company (PETRONAS GLOBAL, 2019).

Recommendations

The analysis of the financials of the company stated that the Petronas Company had a

very low amount of debt in the financial statement of the company. It is recommended that the

management of the company should reduce the WACC of the company with the help of the

increase in the debt in the financing sources. The introduction of the debt should be done at an

optimal point keeping the debt to equity ratio compatible with the financial performance of the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.