Heriot-Watt University: Capital Structure & Firm Performance Analysis

VerifiedAdded on 2022/10/15

|7

|1148

|117

Project

AI Summary

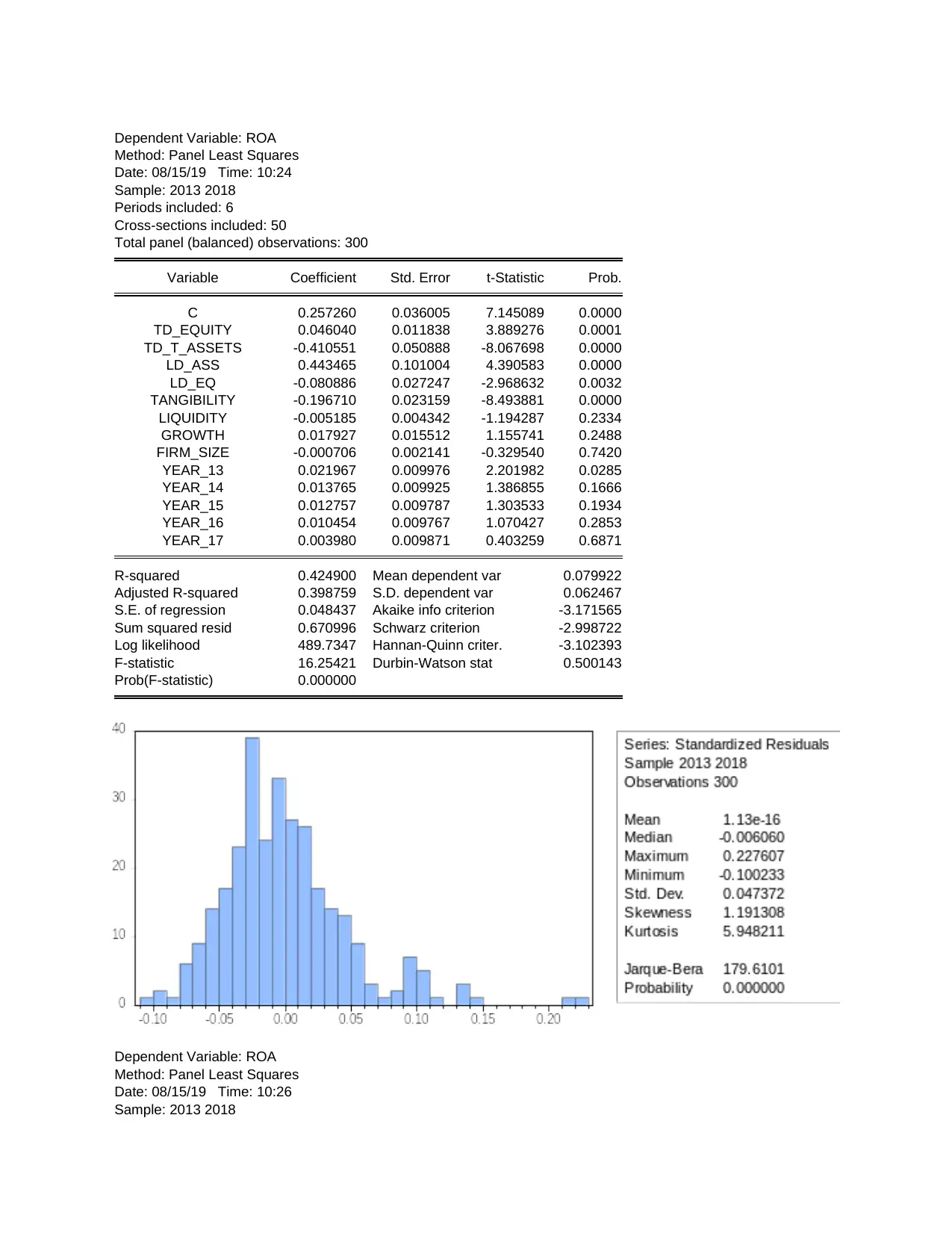

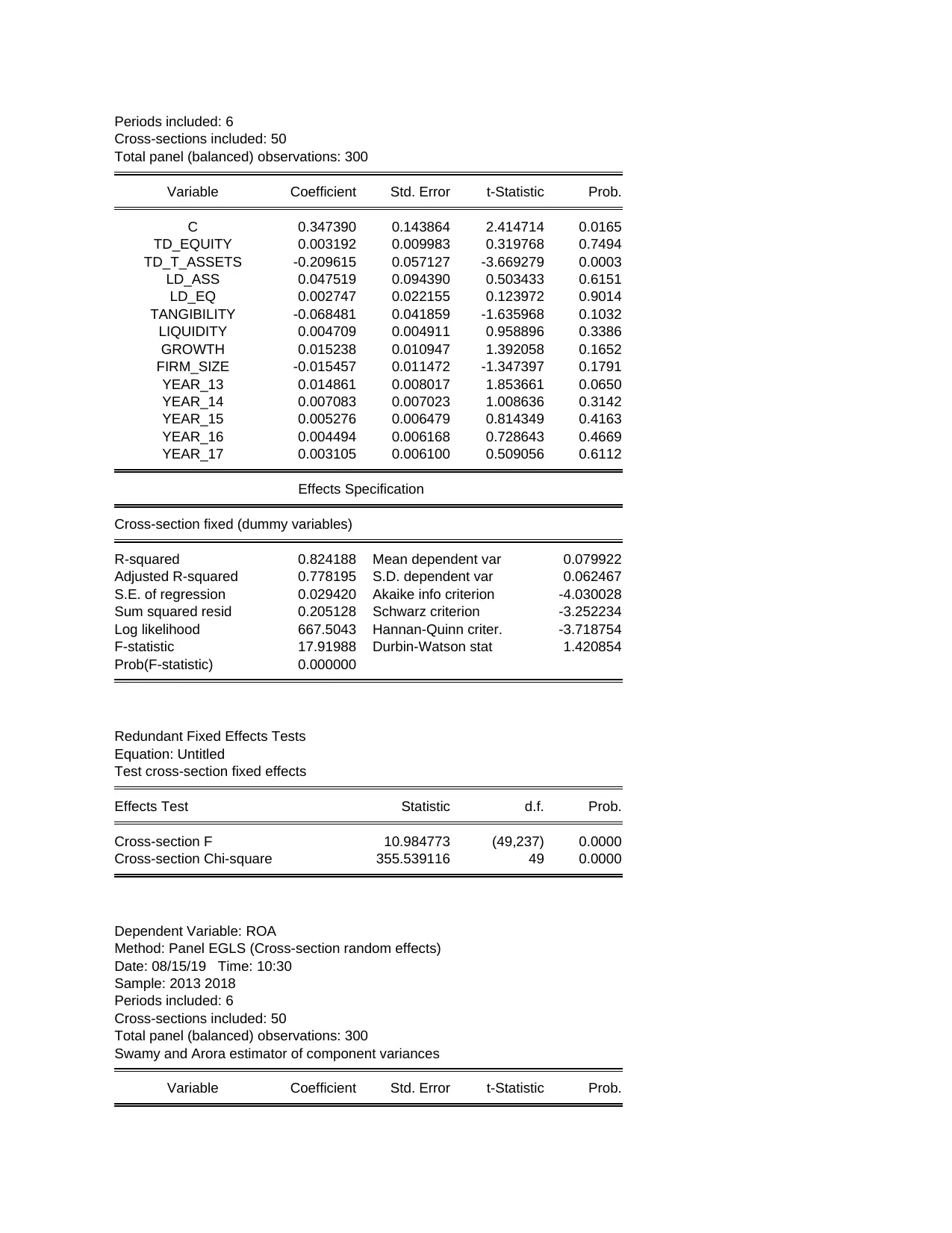

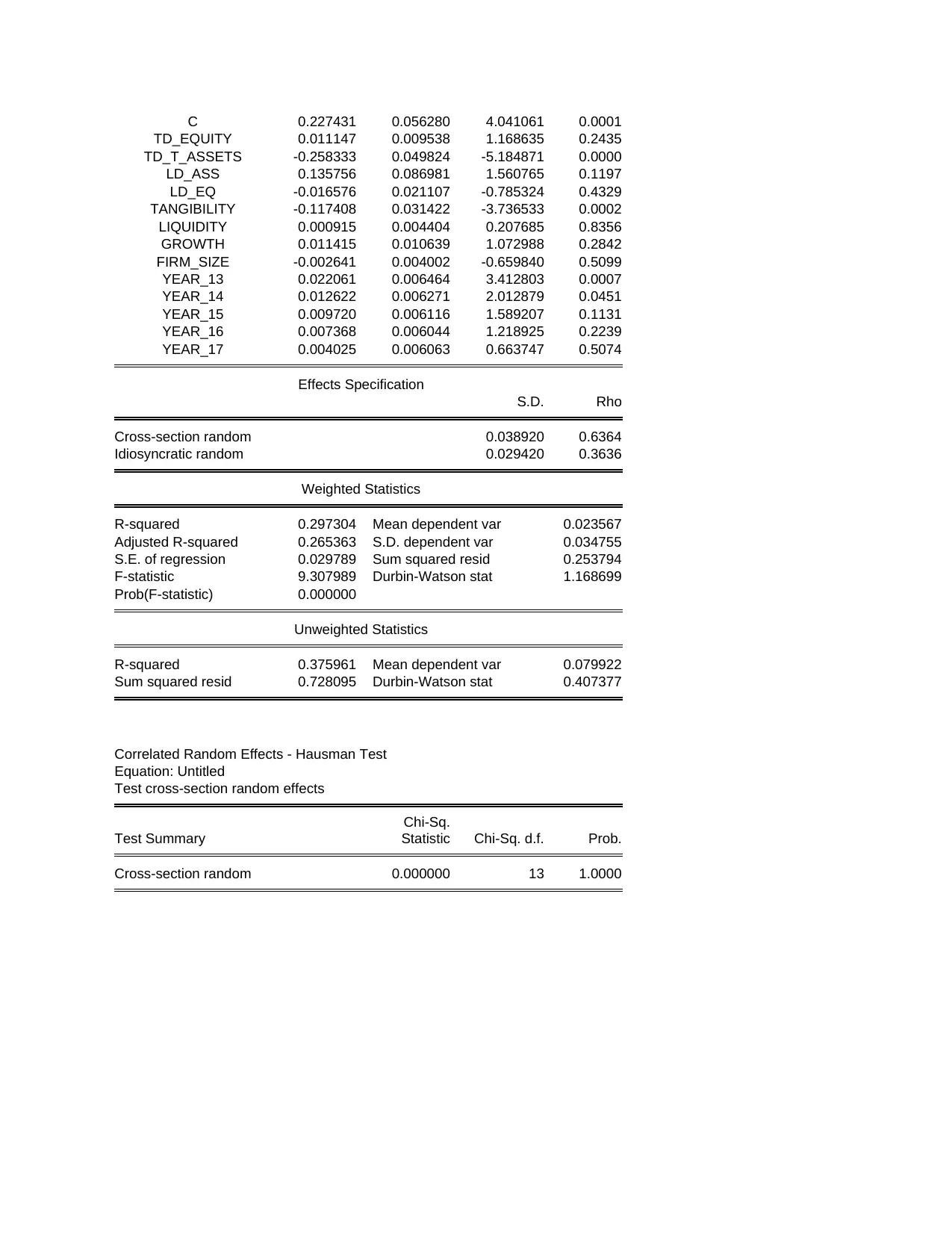

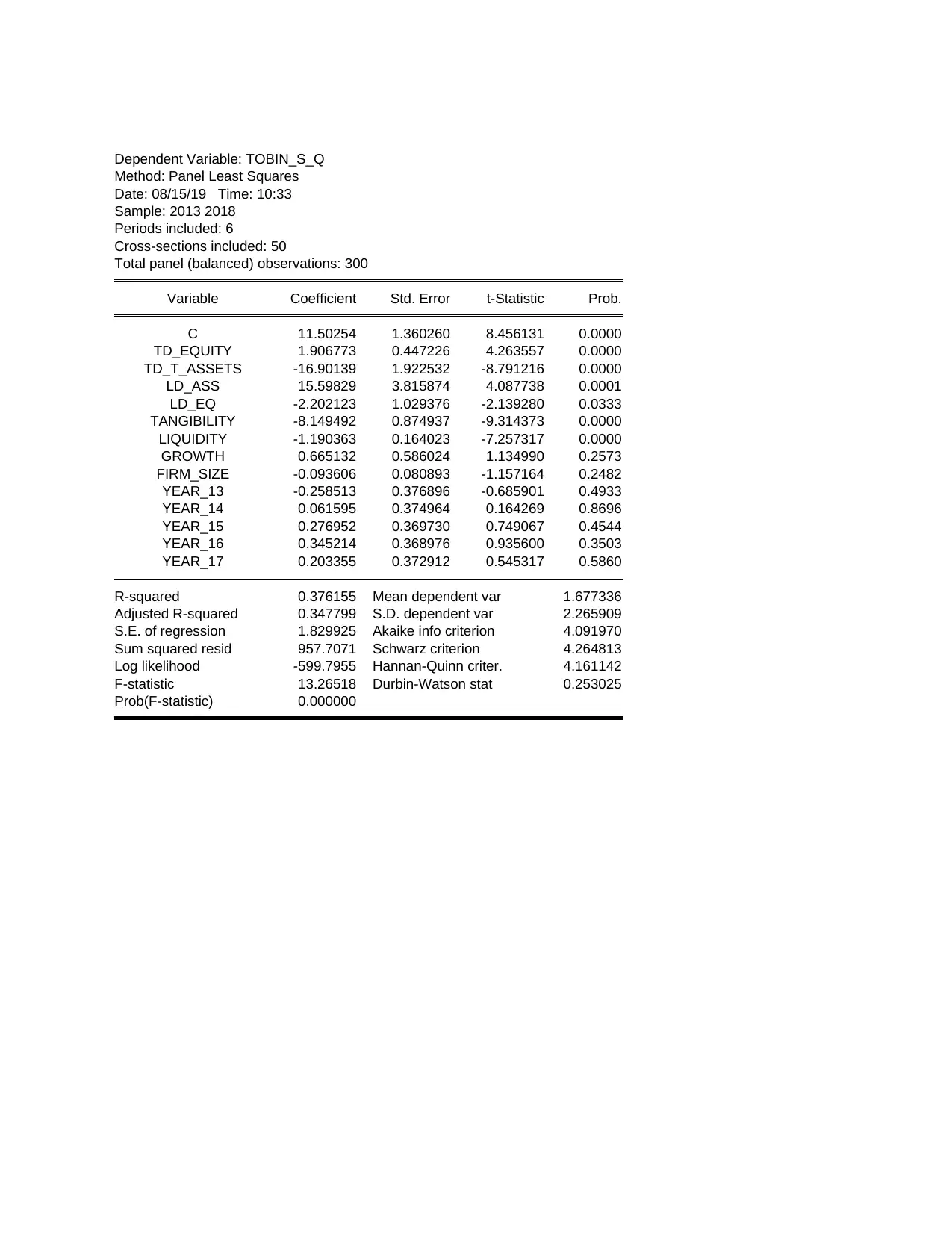

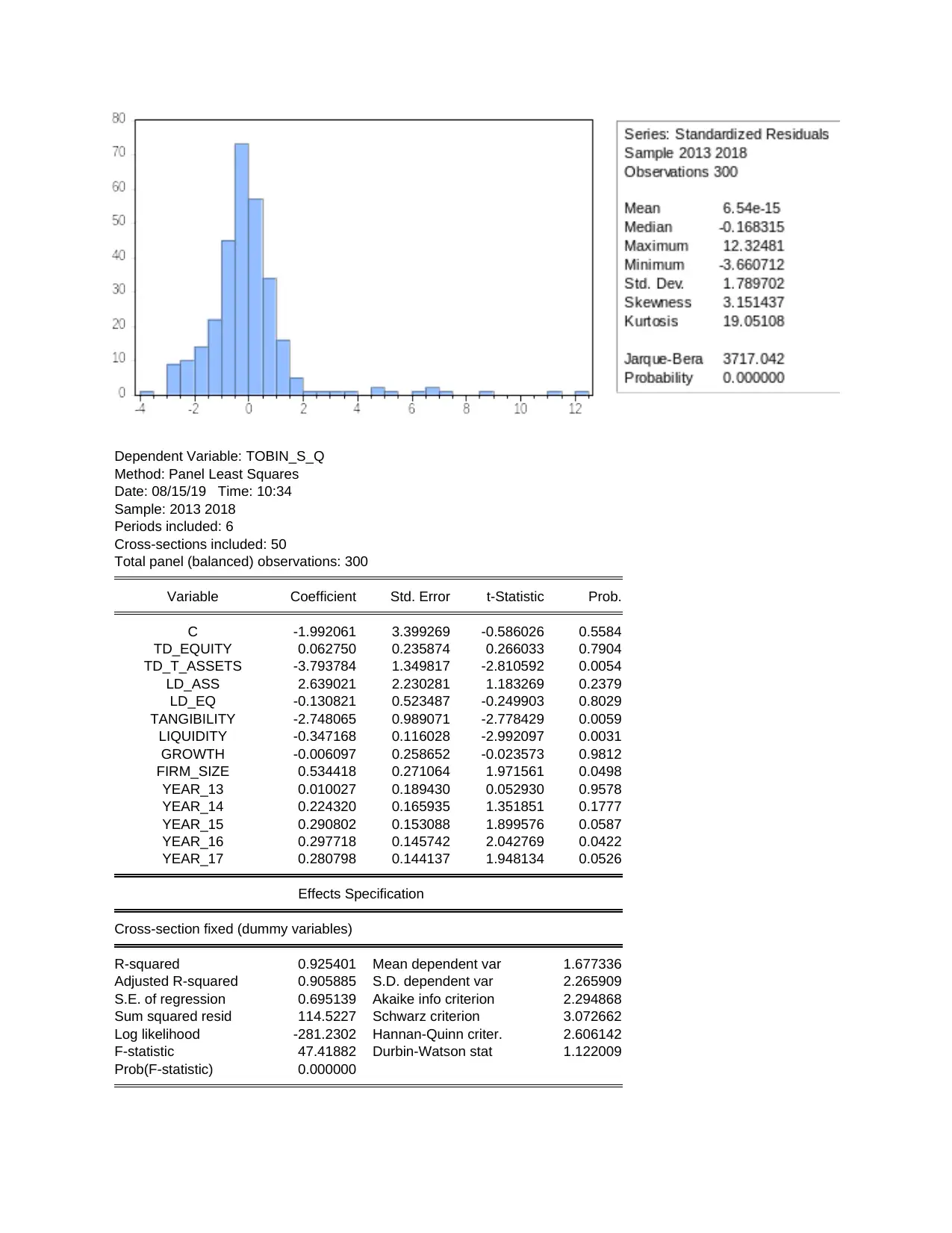

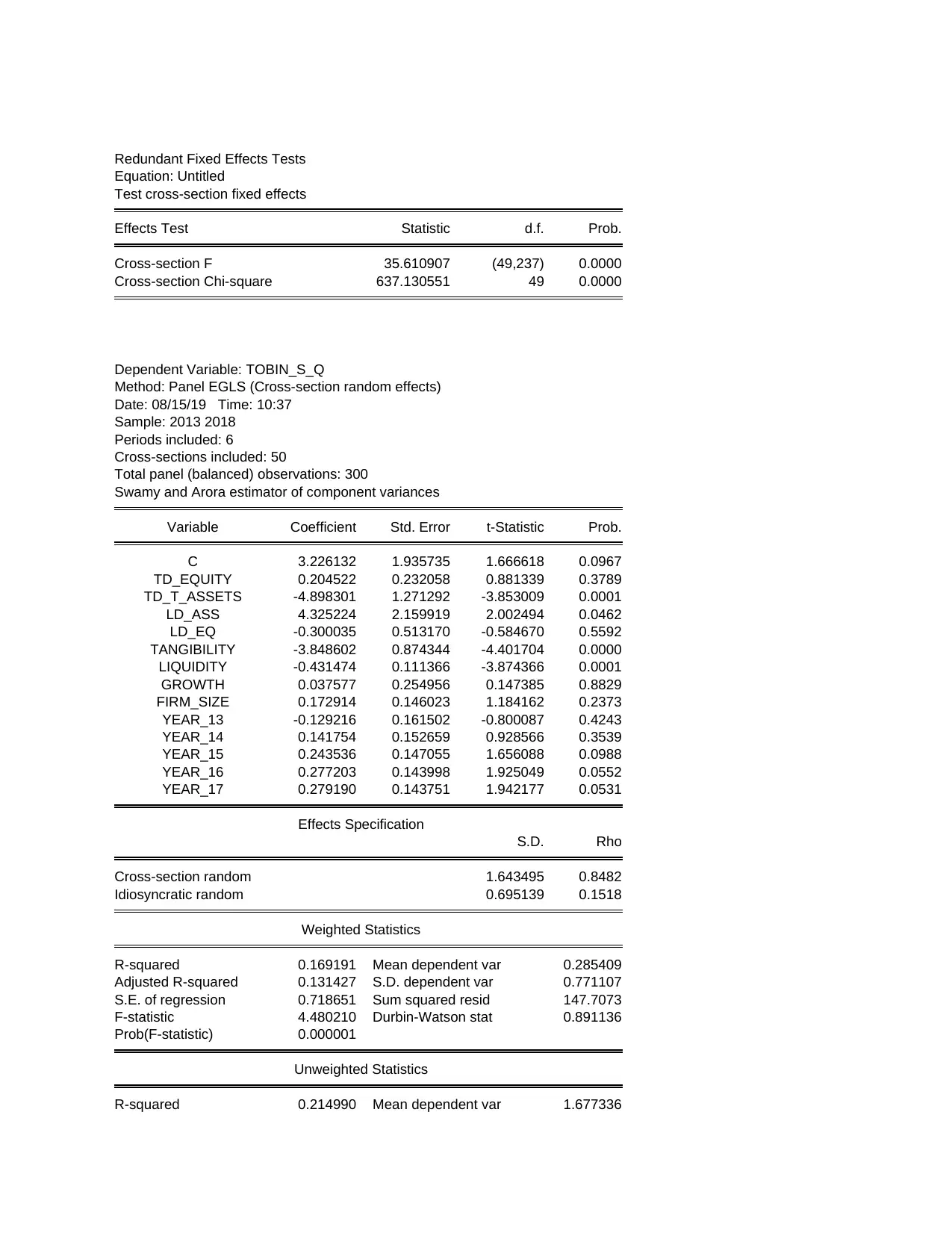

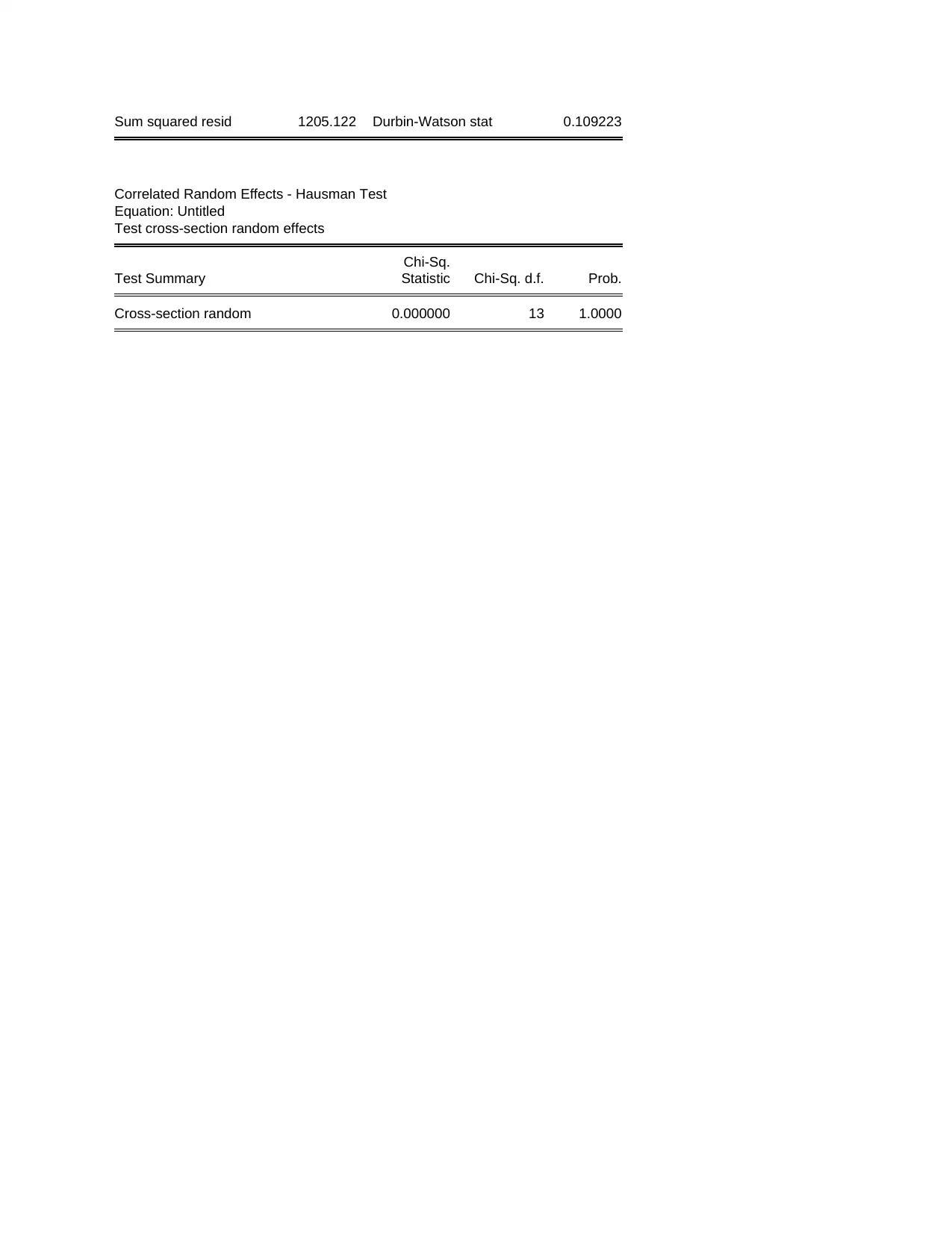

This project presents an analysis of the determinants of capital structure and its impact on firm performance. The study uses panel data from a sample of firms, employing regression analysis to examine the relationships between various financial variables. The analysis explores the influence of factors such as debt-to-equity ratio, tangibility, profitability, liquidity, and firm size on firm performance, measured by metrics such as Return on Assets (ROA) and Tobin's Q. The project includes econometric models using panel least squares, fixed effects, and random effects, along with relevant statistical tests. The results provide insights into the significant determinants of capital structure and their effects on firm valuation and profitability, offering valuable information for financial decision-making. The study synthesizes the broad literature on capital structure theories, including the Modigliani and Miller model, trade-off theory, and pecking order theory, to provide a comprehensive understanding of the topic.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.