Capital Structure and Firm Value: Analysis of UK Firms, 1970-2018

VerifiedAdded on 2022/10/06

|15

|2011

|55

Report

AI Summary

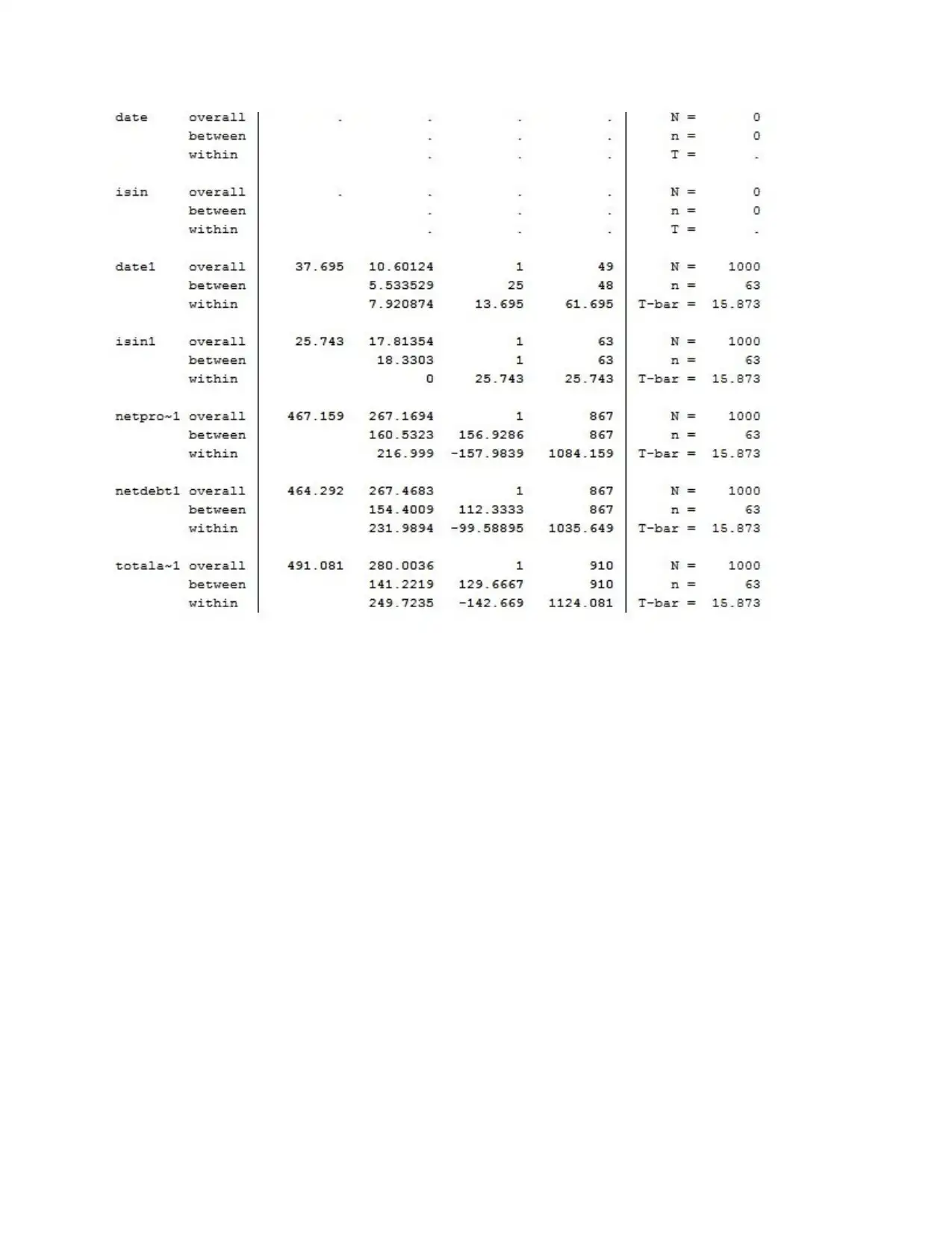

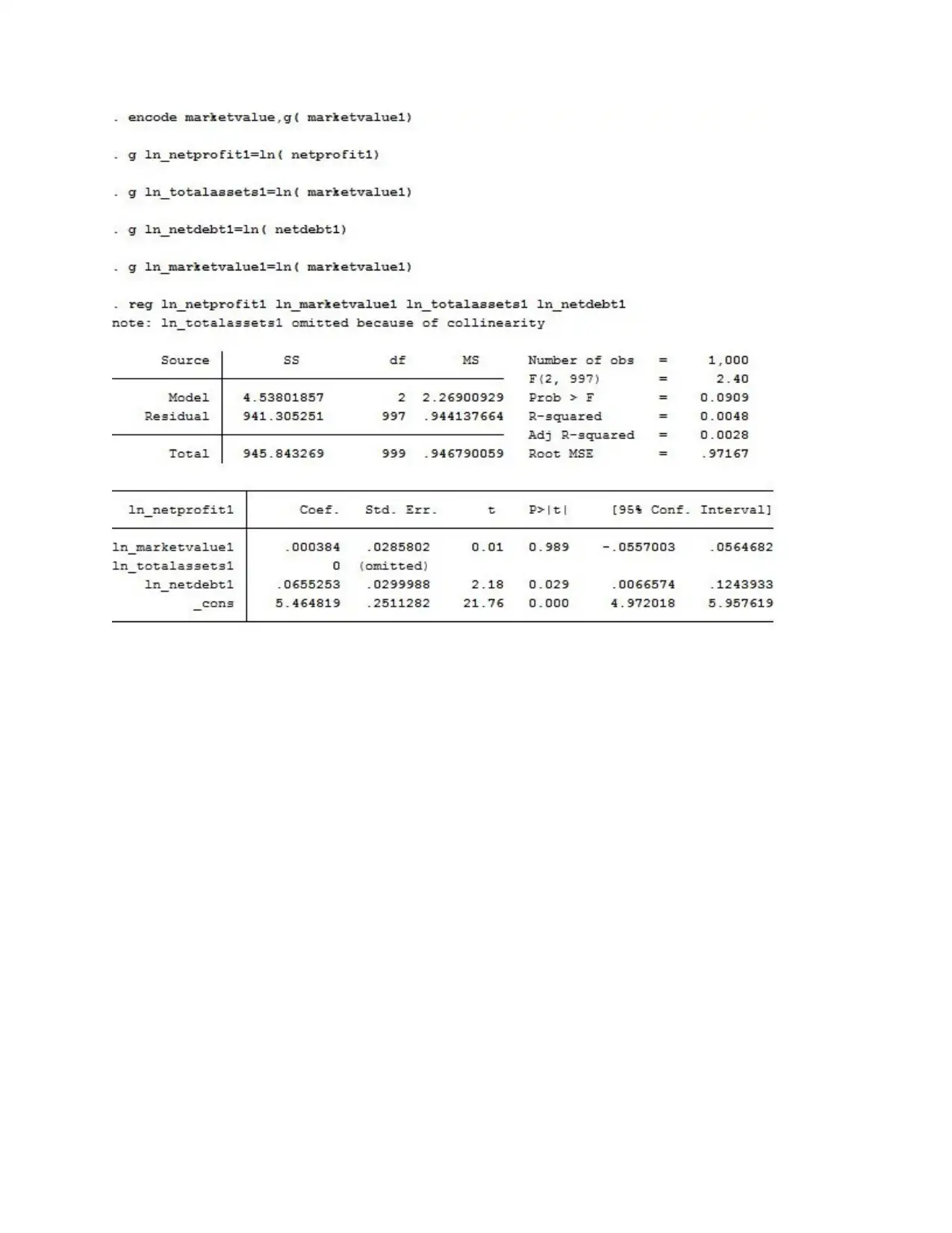

This report investigates the relationship between capital structure and firm value among UK listed firms from 1970 to 2018, utilizing panel data and STATA software for analysis. The study examines how changes in capital structure, including debt and equity, influence firm valuation, considering factors like exchange offers and recapitalizations. The analysis employs various econometric models, including pooled regression, error component models, and Hausman tests, to address potential biases and capture heterogeneity. The findings suggest a positive relationship between firm value and leverage, supporting the debt tax shield effect, although empirical support for the capital structure-firm value link is limited. The report also discusses limitations in the data, such as the availability of market forecasts and data dynamics and the implications of these limitations on the analysis. The study references relevant literature, including works by Masulis, Baltagi, and others, to support its theoretical framework and empirical findings.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.