APC308 - Financial Management: Capital Structure, Cost & Appraisal

VerifiedAdded on 2023/06/18

|14

|3802

|393

Report

AI Summary

This report delves into financial management, focusing on the cost of capital and capital structure of Trust PLC. It includes a book value and market value analysis to evaluate the company's Weighted Average Cost of Capital (WACC). The report calculates and interprets WACC based on both market and book values, discussing its relationship with the Internal Rate of Return (IRR). Furthermore, the report explores investment appraisal techniques such as payback period, rate of return, Net Present Value (NPV), and IRR, applying these methods to STS Limited. The analysis covers the influence of investment appraisal approaches on organizations, highlighting the benefits and disadvantages of capital assessment methodologies in industries. The document concludes by summarizing the key findings and implications for financial decision-making.

APC308 Financial

Management

Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

Question 1- Cost of Capital and Capital Structure......................................................................1

a. Book Value and Market Value Analysis.................................................................................1

b. Evaluation of the Total WACC Cost of Capital......................................................................3

c. Interpretations..........................................................................................................................4

d. The relationship between the organization's IRR and WACC grade......................................5

Question 2- Investment Appraisal Techniques............................................................................5

a. Computation of the payback period, the rate of return, the net present value, and the IRR

value.............................................................................................................................................5

ROI Value Evaluation..................................................................................................................6

b. The Influence of Investment Appraisal Approaches in Organizations....................................7

c. Benefits and Disadvantages of Capital Assessment Methodology in Industries.....................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

Question 1- Cost of Capital and Capital Structure......................................................................1

a. Book Value and Market Value Analysis.................................................................................1

b. Evaluation of the Total WACC Cost of Capital......................................................................3

c. Interpretations..........................................................................................................................4

d. The relationship between the organization's IRR and WACC grade......................................5

Question 2- Investment Appraisal Techniques............................................................................5

a. Computation of the payback period, the rate of return, the net present value, and the IRR

value.............................................................................................................................................5

ROI Value Evaluation..................................................................................................................6

b. The Influence of Investment Appraisal Approaches in Organizations....................................7

c. Benefits and Disadvantages of Capital Assessment Methodology in Industries.....................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial accounting is a subset of accounting that handles with expenditures, earnings,

capital, and mortgages (Commerford, Hatfield and Houston, 2018). Financial regime is a

management function wherein organization is in charge of conceptualization, implementation,

coordination, regulation, and evaluation. In ability to execute a corporate efficiency of operation,

the management must have a thorough knowledge of operational budget. Financial regimes often

include incorporating management strategies to the financial tools of the organization while also

playing a significant role in financial control. As a consequence, it is also essential to suggest

that monetary and social regimes are inextricably linked.

MAIN BODY

Economic design relates to the money foundation of an organization, which comprises of a

precise combination of debt and equity used by any entity to finance expansion and progress.

The term "capital framework" relates to the company's ownership rights and also a financial hold

on future income inputs and returns. The obligations of the organization come in the form of

stocks or loans.

The cost of capital is the required proportion of income on any enterprise or deal which the

owner must obtain. Whenever a number of executives or an analyst states the amount of

borrowing, they were talking to the modified median expenditure of capital. Larger companies

produce funds from either a portfolio of investments; include stocks, loans, as well as other

channels, rather than from a specific provider (Fan and Chatterjee, 2019). The overall expense of

capital estimated by taking into account all costs from multiple origins is known as the Generic

Average Pricing of Investing (WACC).

Question 1- Cost of Capital and Capital Structure

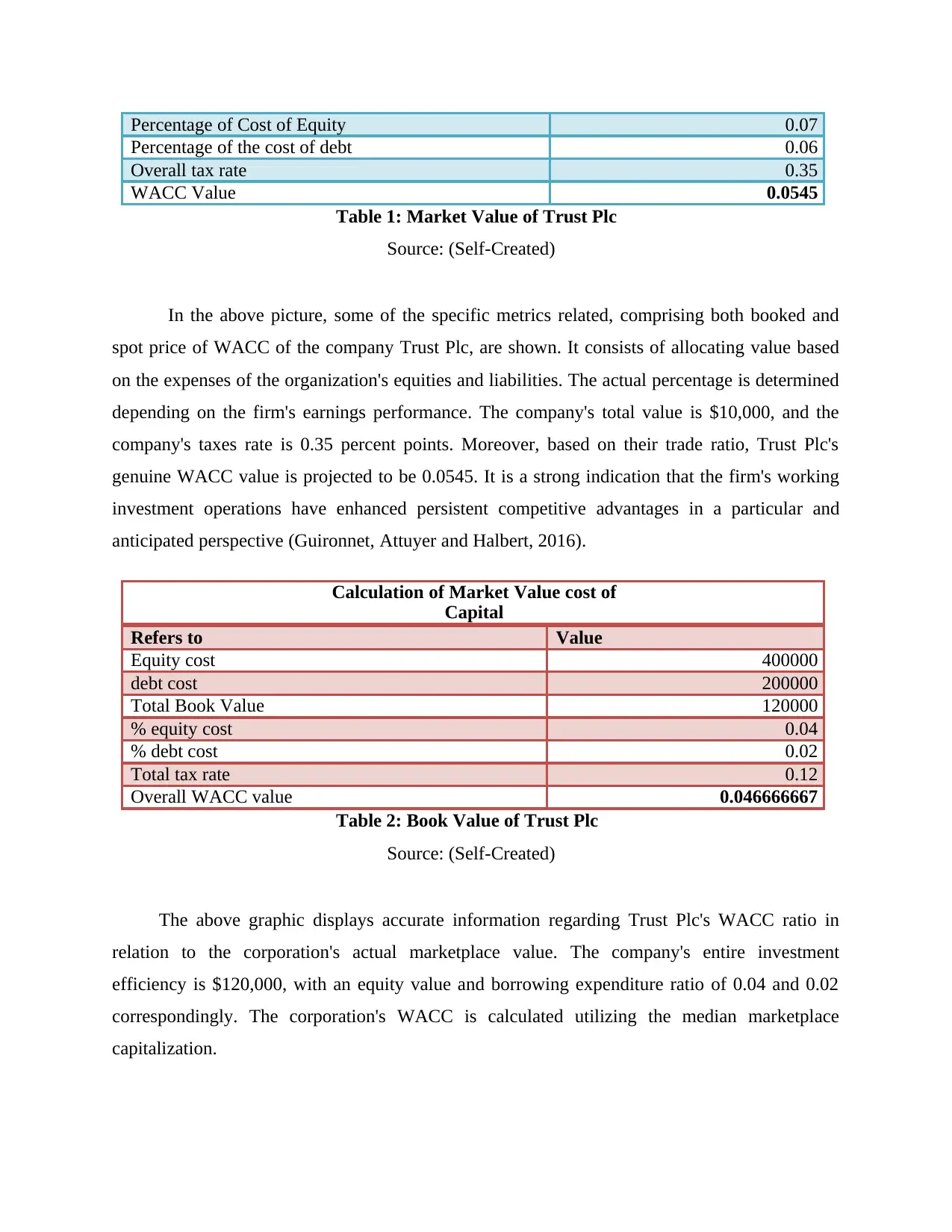

a. Book Value and Market Value Analysis

Calculation of Market value cost of

WACC

Refers to Value

Cost of equity 500000

cost of debt 500000

Overall Market Value 1000000

Financial accounting is a subset of accounting that handles with expenditures, earnings,

capital, and mortgages (Commerford, Hatfield and Houston, 2018). Financial regime is a

management function wherein organization is in charge of conceptualization, implementation,

coordination, regulation, and evaluation. In ability to execute a corporate efficiency of operation,

the management must have a thorough knowledge of operational budget. Financial regimes often

include incorporating management strategies to the financial tools of the organization while also

playing a significant role in financial control. As a consequence, it is also essential to suggest

that monetary and social regimes are inextricably linked.

MAIN BODY

Economic design relates to the money foundation of an organization, which comprises of a

precise combination of debt and equity used by any entity to finance expansion and progress.

The term "capital framework" relates to the company's ownership rights and also a financial hold

on future income inputs and returns. The obligations of the organization come in the form of

stocks or loans.

The cost of capital is the required proportion of income on any enterprise or deal which the

owner must obtain. Whenever a number of executives or an analyst states the amount of

borrowing, they were talking to the modified median expenditure of capital. Larger companies

produce funds from either a portfolio of investments; include stocks, loans, as well as other

channels, rather than from a specific provider (Fan and Chatterjee, 2019). The overall expense of

capital estimated by taking into account all costs from multiple origins is known as the Generic

Average Pricing of Investing (WACC).

Question 1- Cost of Capital and Capital Structure

a. Book Value and Market Value Analysis

Calculation of Market value cost of

WACC

Refers to Value

Cost of equity 500000

cost of debt 500000

Overall Market Value 1000000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Percentage of Cost of Equity 0.07

Percentage of the cost of debt 0.06

Overall tax rate 0.35

WACC Value 0.0545

Table 1: Market Value of Trust Plc

Source: (Self-Created)

In the above picture, some of the specific metrics related, comprising both booked and

spot price of WACC of the company Trust Plc, are shown. It consists of allocating value based

on the expenses of the organization's equities and liabilities. The actual percentage is determined

depending on the firm's earnings performance. The company's total value is $10,000, and the

company's taxes rate is 0.35 percent points. Moreover, based on their trade ratio, Trust Plc's

genuine WACC value is projected to be 0.0545. It is a strong indication that the firm's working

investment operations have enhanced persistent competitive advantages in a particular and

anticipated perspective (Guironnet, Attuyer and Halbert, 2016).

Calculation of Market Value cost of

Capital

Refers to Value

Equity cost 400000

debt cost 200000

Total Book Value 120000

% equity cost 0.04

% debt cost 0.02

Total tax rate 0.12

Overall WACC value 0.046666667

Table 2: Book Value of Trust Plc

Source: (Self-Created)

The above graphic displays accurate information regarding Trust Plc's WACC ratio in

relation to the corporation's actual marketplace value. The company's entire investment

efficiency is $120,000, with an equity value and borrowing expenditure ratio of 0.04 and 0.02

correspondingly. The corporation's WACC is calculated utilizing the median marketplace

capitalization.

Percentage of the cost of debt 0.06

Overall tax rate 0.35

WACC Value 0.0545

Table 1: Market Value of Trust Plc

Source: (Self-Created)

In the above picture, some of the specific metrics related, comprising both booked and

spot price of WACC of the company Trust Plc, are shown. It consists of allocating value based

on the expenses of the organization's equities and liabilities. The actual percentage is determined

depending on the firm's earnings performance. The company's total value is $10,000, and the

company's taxes rate is 0.35 percent points. Moreover, based on their trade ratio, Trust Plc's

genuine WACC value is projected to be 0.0545. It is a strong indication that the firm's working

investment operations have enhanced persistent competitive advantages in a particular and

anticipated perspective (Guironnet, Attuyer and Halbert, 2016).

Calculation of Market Value cost of

Capital

Refers to Value

Equity cost 400000

debt cost 200000

Total Book Value 120000

% equity cost 0.04

% debt cost 0.02

Total tax rate 0.12

Overall WACC value 0.046666667

Table 2: Book Value of Trust Plc

Source: (Self-Created)

The above graphic displays accurate information regarding Trust Plc's WACC ratio in

relation to the corporation's actual marketplace value. The company's entire investment

efficiency is $120,000, with an equity value and borrowing expenditure ratio of 0.04 and 0.02

correspondingly. The corporation's WACC is calculated utilizing the median marketplace

capitalization.

It can help provide a deeper knowledge of the corporation's inside and outside activities in

the industry in the nearest term. Organizations are having problems in their continuing activities

according to the company's calculated WACC score. It could benefit the firm's investment

operations and associated share value in addition to remain competitive and sustainable in the

near future (Kovalenko, 2019).

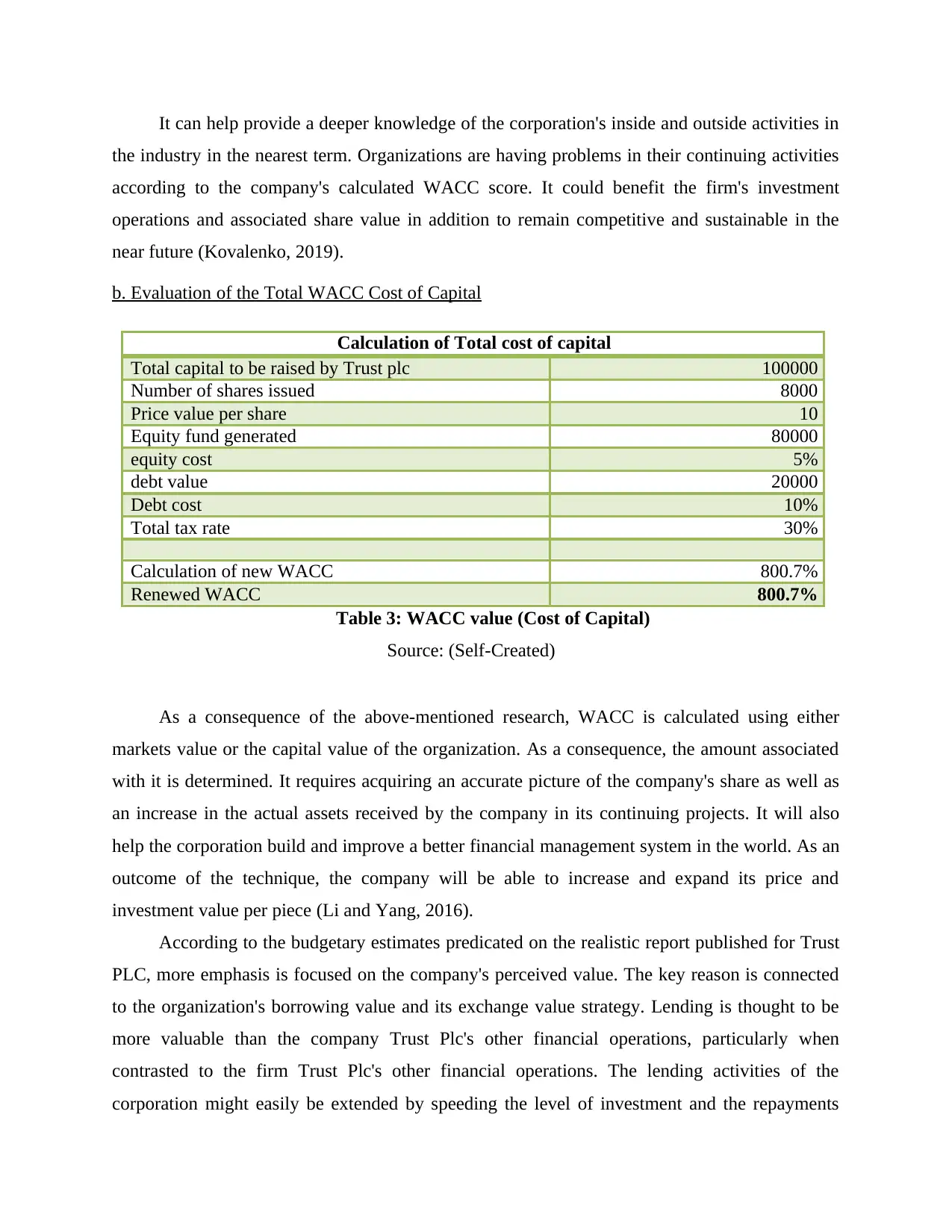

b. Evaluation of the Total WACC Cost of Capital

Calculation of Total cost of capital

Total capital to be raised by Trust plc 100000

Number of shares issued 8000

Price value per share 10

Equity fund generated 80000

equity cost 5%

debt value 20000

Debt cost 10%

Total tax rate 30%

Calculation of new WACC 800.7%

Renewed WACC 800.7%

Table 3: WACC value (Cost of Capital)

Source: (Self-Created)

As a consequence of the above-mentioned research, WACC is calculated using either

markets value or the capital value of the organization. As a consequence, the amount associated

with it is determined. It requires acquiring an accurate picture of the company's share as well as

an increase in the actual assets received by the company in its continuing projects. It will also

help the corporation build and improve a better financial management system in the world. As an

outcome of the technique, the company will be able to increase and expand its price and

investment value per piece (Li and Yang, 2016).

According to the budgetary estimates predicated on the realistic report published for Trust

PLC, more emphasis is focused on the company's perceived value. The key reason is connected

to the organization's borrowing value and its exchange value strategy. Lending is thought to be

more valuable than the company Trust Plc's other financial operations, particularly when

contrasted to the firm Trust Plc's other financial operations. The lending activities of the

corporation might easily be extended by speeding the level of investment and the repayments

the industry in the nearest term. Organizations are having problems in their continuing activities

according to the company's calculated WACC score. It could benefit the firm's investment

operations and associated share value in addition to remain competitive and sustainable in the

near future (Kovalenko, 2019).

b. Evaluation of the Total WACC Cost of Capital

Calculation of Total cost of capital

Total capital to be raised by Trust plc 100000

Number of shares issued 8000

Price value per share 10

Equity fund generated 80000

equity cost 5%

debt value 20000

Debt cost 10%

Total tax rate 30%

Calculation of new WACC 800.7%

Renewed WACC 800.7%

Table 3: WACC value (Cost of Capital)

Source: (Self-Created)

As a consequence of the above-mentioned research, WACC is calculated using either

markets value or the capital value of the organization. As a consequence, the amount associated

with it is determined. It requires acquiring an accurate picture of the company's share as well as

an increase in the actual assets received by the company in its continuing projects. It will also

help the corporation build and improve a better financial management system in the world. As an

outcome of the technique, the company will be able to increase and expand its price and

investment value per piece (Li and Yang, 2016).

According to the budgetary estimates predicated on the realistic report published for Trust

PLC, more emphasis is focused on the company's perceived value. The key reason is connected

to the organization's borrowing value and its exchange value strategy. Lending is thought to be

more valuable than the company Trust Plc's other financial operations, particularly when

contrasted to the firm Trust Plc's other financial operations. The lending activities of the

corporation might easily be extended by speeding the level of investment and the repayments

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

associated with the existing debts. Nonetheless, it includes methods aimed at decreasing and

reducing the company's taxable revenue. The reduction in applicable tax liability is displayed as

cash flows. Moreover, income protection is widely regarded as among the most critical areas of

the industry for firms. This would have been a significant part of the organization's current flow

administration and also enhancing the firm's revenue monetary value.

c. Interpretations

According to calculations, the WACC value on the company's yield on money activities is

perhaps the most crucial component for expanding the organization's investment activities.

Additionally, the element of performing procedures in a structured manner needs the

organization's commitment to specific procedures in case of applying exact same thing. In this

respect, the organization's key effort is to lay a special focus on its operating expenses. However,

the company should double-check that it would be priced accurately. The value associated with

the organization's gearing proportion, on either hand, must not fluctuate on a regular basis. For

the near future, this would also present serious challenges whenever it refers to evaluating and

analyzing the business's monetization strategies (Ljungqvist, Richardson and Wolfenzon, 2020).

Additionally, if the entities oriented prospective clients, the corporation's fundamental

investment value will be significantly impacted. This will have a negative influence on the firm's

earnings structure. The management of the company Trust PLC ensures that the overall

functioning of the firm remains consistent. It will be a useful resource to the organisation in

respect of monetary fluctuation tracking and reduction. Perhaps the most relevant assumption

which might be implemented into the company's WACC pricing evaluation technique is the

conventional idea. The financial activities of Trust Plc, and its leverage proportion, must be

established. This will aid in obtaining stronger and more consistent control over the WACC rate.

On either hand, because when organization's gearing proportion rises the WACC valuation

of the business remains managed and preserved. When the leverage levels associated with the

corporation's investment expenditure increase, the WACC calculation grows significantly and

increasingly exact and dependable. A drop in the effective leverage rates, on either side, would

assist the organisation in respect of building a more equitable technique of forecasting for the

current and future.

reducing the company's taxable revenue. The reduction in applicable tax liability is displayed as

cash flows. Moreover, income protection is widely regarded as among the most critical areas of

the industry for firms. This would have been a significant part of the organization's current flow

administration and also enhancing the firm's revenue monetary value.

c. Interpretations

According to calculations, the WACC value on the company's yield on money activities is

perhaps the most crucial component for expanding the organization's investment activities.

Additionally, the element of performing procedures in a structured manner needs the

organization's commitment to specific procedures in case of applying exact same thing. In this

respect, the organization's key effort is to lay a special focus on its operating expenses. However,

the company should double-check that it would be priced accurately. The value associated with

the organization's gearing proportion, on either hand, must not fluctuate on a regular basis. For

the near future, this would also present serious challenges whenever it refers to evaluating and

analyzing the business's monetization strategies (Ljungqvist, Richardson and Wolfenzon, 2020).

Additionally, if the entities oriented prospective clients, the corporation's fundamental

investment value will be significantly impacted. This will have a negative influence on the firm's

earnings structure. The management of the company Trust PLC ensures that the overall

functioning of the firm remains consistent. It will be a useful resource to the organisation in

respect of monetary fluctuation tracking and reduction. Perhaps the most relevant assumption

which might be implemented into the company's WACC pricing evaluation technique is the

conventional idea. The financial activities of Trust Plc, and its leverage proportion, must be

established. This will aid in obtaining stronger and more consistent control over the WACC rate.

On either hand, because when organization's gearing proportion rises the WACC valuation

of the business remains managed and preserved. When the leverage levels associated with the

corporation's investment expenditure increase, the WACC calculation grows significantly and

increasingly exact and dependable. A drop in the effective leverage rates, on either side, would

assist the organisation in respect of building a more equitable technique of forecasting for the

current and future.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

d. The relationship between the organization's IRR and WACC grade

Both the WACC "Weighted Average Cost of Capital" and IRR "Internal Rate of Return"

methodologies are utilised simultaneously in the case of asset management or numerous financial

situations of the business, but for different goals. Additionally, regardless of the notion that they

are used interchangeably, the meanings of IRR and WACC differ. It is widely perceived as an

assessment matrix that shows the proportions used to calculate the overall present price of an

income input series. Likewise, the present firm Trust Plc, uses the approach to determine and

analyse capital projects. Better corporate goals can lead to greater economic accomplishment for

the organisation (Lohk and Siimann, 2016).

Additionally, WACC is a way of calculating the yearly taxes expenditure of a company's

capital assets as a percentage. It enables the company to calculate its payout in addition to

calculate its corporate equity shares. Whenever a company starts a venture, it must estimate

WACC to assess the industry's variability, whereas IRR is utilised to evaluate the spending. To

make a decision on corporate currency transactions, the company strongly promotes the

approach as well as the method of financial management. As an outcome, such techniques help

the company extend its repertory by selecting advantageous and dangerous locations. Businesses

used to connect the process of investment decision-making with average financing expenditures

from the standpoint of management. The link argues that maybe the present value of the business

is greater than the value of financial spending, enabling the NPV to be computed, and the sum is

NPV 0.

Question 2- Investment Appraisal Techniques

a. Computation of the payback period, the rate of return, the net present value, and the IRR value

Payback, NPV,

IRR

1st Year

performance

2nd-year

performance

3rd-year

Performance

Initial Investment

process

-£

2,23,700.00

Discounting Rate of

the organization

£

10.00

Both the WACC "Weighted Average Cost of Capital" and IRR "Internal Rate of Return"

methodologies are utilised simultaneously in the case of asset management or numerous financial

situations of the business, but for different goals. Additionally, regardless of the notion that they

are used interchangeably, the meanings of IRR and WACC differ. It is widely perceived as an

assessment matrix that shows the proportions used to calculate the overall present price of an

income input series. Likewise, the present firm Trust Plc, uses the approach to determine and

analyse capital projects. Better corporate goals can lead to greater economic accomplishment for

the organisation (Lohk and Siimann, 2016).

Additionally, WACC is a way of calculating the yearly taxes expenditure of a company's

capital assets as a percentage. It enables the company to calculate its payout in addition to

calculate its corporate equity shares. Whenever a company starts a venture, it must estimate

WACC to assess the industry's variability, whereas IRR is utilised to evaluate the spending. To

make a decision on corporate currency transactions, the company strongly promotes the

approach as well as the method of financial management. As an outcome, such techniques help

the company extend its repertory by selecting advantageous and dangerous locations. Businesses

used to connect the process of investment decision-making with average financing expenditures

from the standpoint of management. The link argues that maybe the present value of the business

is greater than the value of financial spending, enabling the NPV to be computed, and the sum is

NPV 0.

Question 2- Investment Appraisal Techniques

a. Computation of the payback period, the rate of return, the net present value, and the IRR value

Payback, NPV,

IRR

1st Year

performance

2nd-year

performance

3rd-year

Performance

Initial Investment

process

-£

2,23,700.00

Discounting Rate of

the organization

£

10.00

Annual Income rate £

7,88,300.00

£

2,00,000.00

£

50,000.00

Variable Cost value -£

4,72,980.00

-£

1,20,000.00

-£

30,000.00

Overheads cost -£

30,000.00

-£

30,000.00

-£

10,000.00

Resale value £

1,23,600.00

Net Cash flow rate -£

2,23,700.00

£

2,85,320.00

£

50,000.00

£

1,33,600.00

Discounted Cash

flow rate

-£

2,23,700.00

£

2,56,788.00

£

40,500.00

£

97,394.40

Cumulative cash

value

-£

2,23,700.00

£

33,088.00

£

73,588.00

£

1,70,982.40

NPV value -£

17,931.66

The overall cost of Value NPV, Payback Period

and

RO

I

IRR value £

0.47

Payback value £

4.51

Table 4: NPV, IRR and Payback Analysis of STS Limited

Source: (Self-Created)

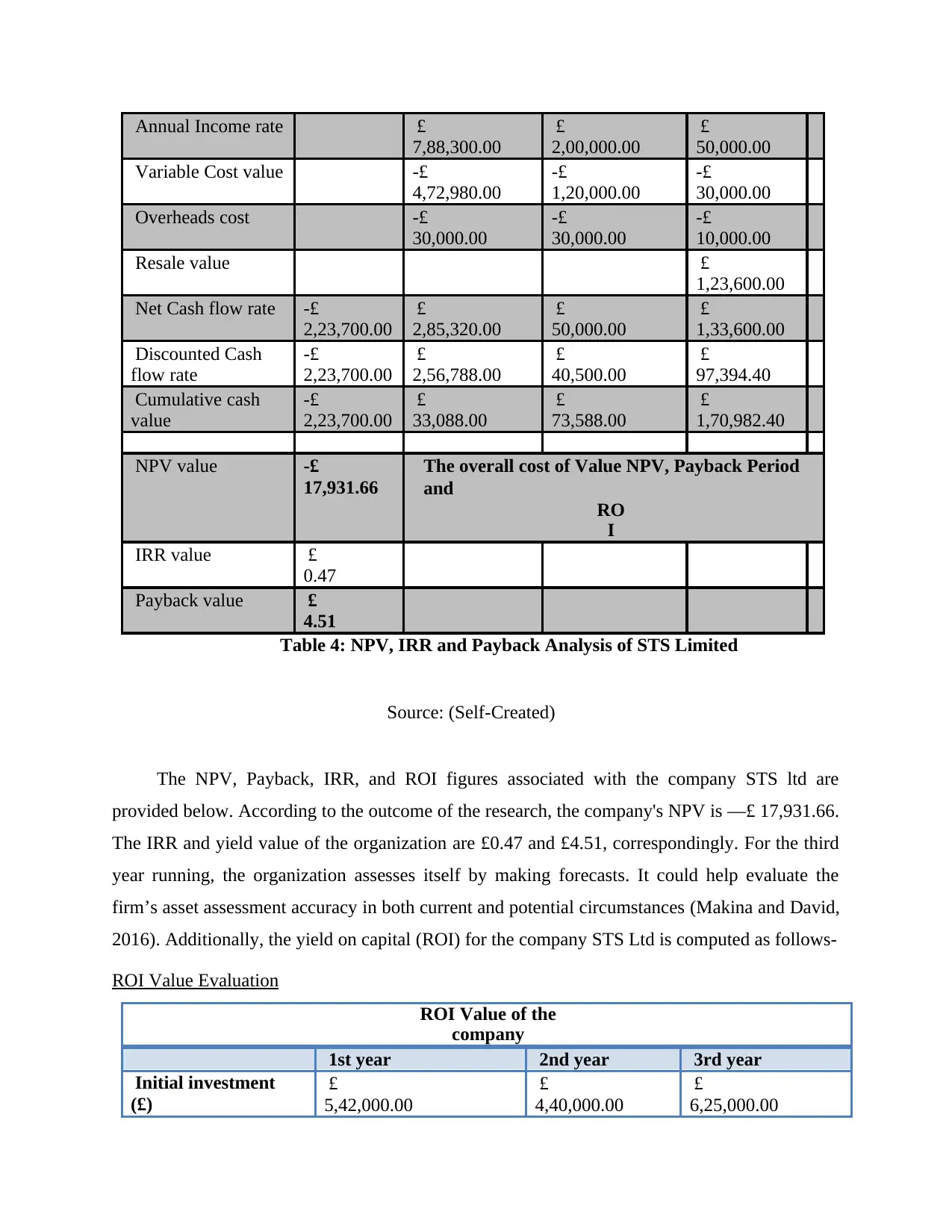

The NPV, Payback, IRR, and ROI figures associated with the company STS ltd are

provided below. According to the outcome of the research, the company's NPV is —£ 17,931.66.

The IRR and yield value of the organization are £0.47 and £4.51, correspondingly. For the third

year running, the organization assesses itself by making forecasts. It could help evaluate the

firm’s asset assessment accuracy in both current and potential circumstances (Makina and David,

2016). Additionally, the yield on capital (ROI) for the company STS Ltd is computed as follows-

ROI Value Evaluation

ROI Value of the

company

1st year 2nd year 3rd year

Initial investment

(£)

£

5,42,000.00

£

4,40,000.00

£

6,25,000.00

7,88,300.00

£

2,00,000.00

£

50,000.00

Variable Cost value -£

4,72,980.00

-£

1,20,000.00

-£

30,000.00

Overheads cost -£

30,000.00

-£

30,000.00

-£

10,000.00

Resale value £

1,23,600.00

Net Cash flow rate -£

2,23,700.00

£

2,85,320.00

£

50,000.00

£

1,33,600.00

Discounted Cash

flow rate

-£

2,23,700.00

£

2,56,788.00

£

40,500.00

£

97,394.40

Cumulative cash

value

-£

2,23,700.00

£

33,088.00

£

73,588.00

£

1,70,982.40

NPV value -£

17,931.66

The overall cost of Value NPV, Payback Period

and

RO

I

IRR value £

0.47

Payback value £

4.51

Table 4: NPV, IRR and Payback Analysis of STS Limited

Source: (Self-Created)

The NPV, Payback, IRR, and ROI figures associated with the company STS ltd are

provided below. According to the outcome of the research, the company's NPV is —£ 17,931.66.

The IRR and yield value of the organization are £0.47 and £4.51, correspondingly. For the third

year running, the organization assesses itself by making forecasts. It could help evaluate the

firm’s asset assessment accuracy in both current and potential circumstances (Makina and David,

2016). Additionally, the yield on capital (ROI) for the company STS Ltd is computed as follows-

ROI Value Evaluation

ROI Value of the

company

1st year 2nd year 3rd year

Initial investment

(£)

£

5,42,000.00

£

4,40,000.00

£

6,25,000.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

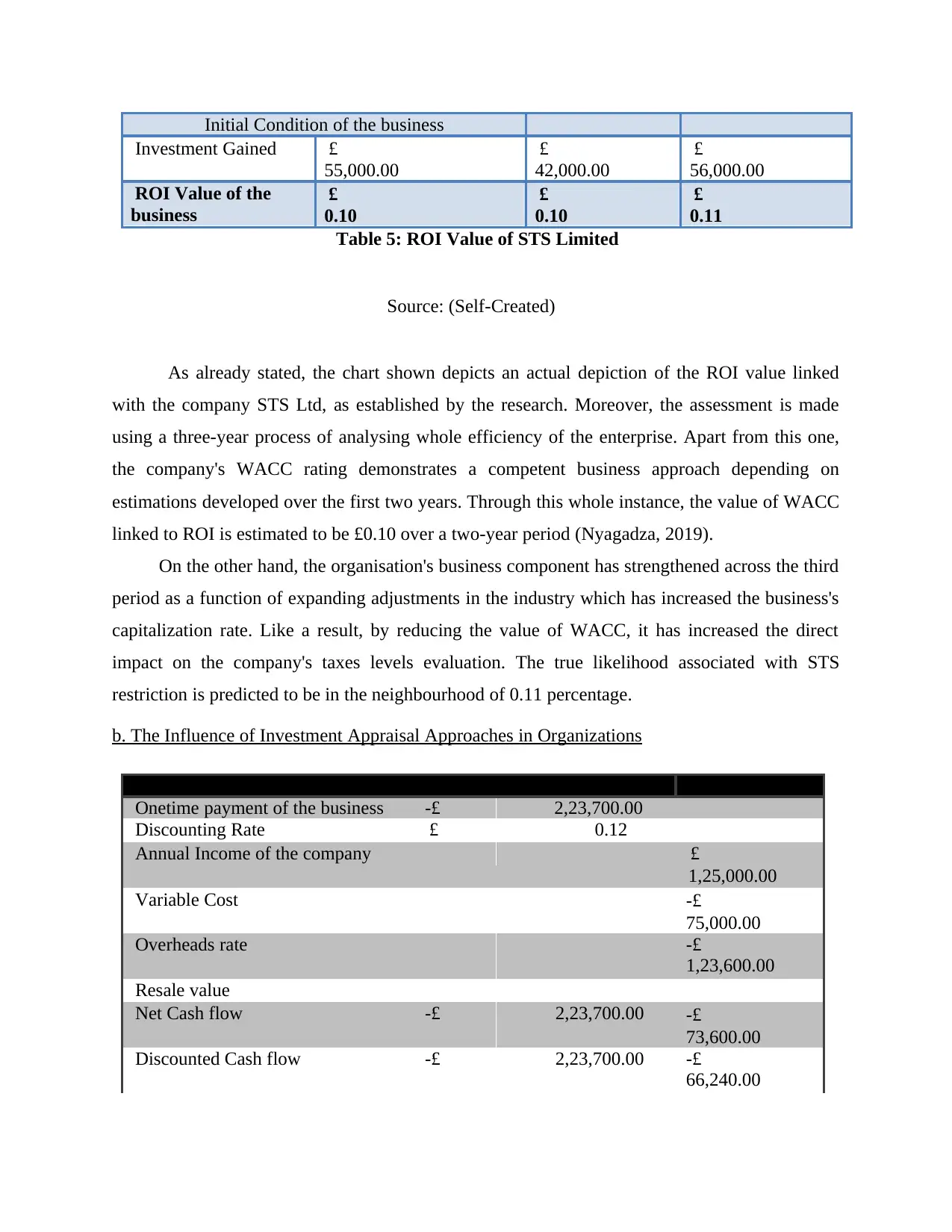

Initial Condition of the business

Investment Gained £

55,000.00

£

42,000.00

£

56,000.00

ROI Value of the

business

£

0.10

£

0.10

£

0.11

Table 5: ROI Value of STS Limited

Source: (Self-Created)

As already stated, the chart shown depicts an actual depiction of the ROI value linked

with the company STS Ltd, as established by the research. Moreover, the assessment is made

using a three-year process of analysing whole efficiency of the enterprise. Apart from this one,

the company's WACC rating demonstrates a competent business approach depending on

estimations developed over the first two years. Through this whole instance, the value of WACC

linked to ROI is estimated to be £0.10 over a two-year period (Nyagadza, 2019).

On the other hand, the organisation's business component has strengthened across the third

period as a function of expanding adjustments in the industry which has increased the business's

capitalization rate. Like a result, by reducing the value of WACC, it has increased the direct

impact on the company's taxes levels evaluation. The true likelihood associated with STS

restriction is predicted to be in the neighbourhood of 0.11 percentage.

b. The Influence of Investment Appraisal Approaches in Organizations

Onetime payment of the business -£ 2,23,700.00

Discounting Rate £ 0.12

Annual Income of the company £

1,25,000.00

Variable Cost -£

75,000.00

Overheads rate -£

1,23,600.00

Resale value

Net Cash flow -£ 2,23,700.00 -£

73,600.00

Discounted Cash flow -£ 2,23,700.00 -£

66,240.00

Investment Gained £

55,000.00

£

42,000.00

£

56,000.00

ROI Value of the

business

£

0.10

£

0.10

£

0.11

Table 5: ROI Value of STS Limited

Source: (Self-Created)

As already stated, the chart shown depicts an actual depiction of the ROI value linked

with the company STS Ltd, as established by the research. Moreover, the assessment is made

using a three-year process of analysing whole efficiency of the enterprise. Apart from this one,

the company's WACC rating demonstrates a competent business approach depending on

estimations developed over the first two years. Through this whole instance, the value of WACC

linked to ROI is estimated to be £0.10 over a two-year period (Nyagadza, 2019).

On the other hand, the organisation's business component has strengthened across the third

period as a function of expanding adjustments in the industry which has increased the business's

capitalization rate. Like a result, by reducing the value of WACC, it has increased the direct

impact on the company's taxes levels evaluation. The true likelihood associated with STS

restriction is predicted to be in the neighbourhood of 0.11 percentage.

b. The Influence of Investment Appraisal Approaches in Organizations

Onetime payment of the business -£ 2,23,700.00

Discounting Rate £ 0.12

Annual Income of the company £

1,25,000.00

Variable Cost -£

75,000.00

Overheads rate -£

1,23,600.00

Resale value

Net Cash flow -£ 2,23,700.00 -£

73,600.00

Discounted Cash flow -£ 2,23,700.00 -£

66,240.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

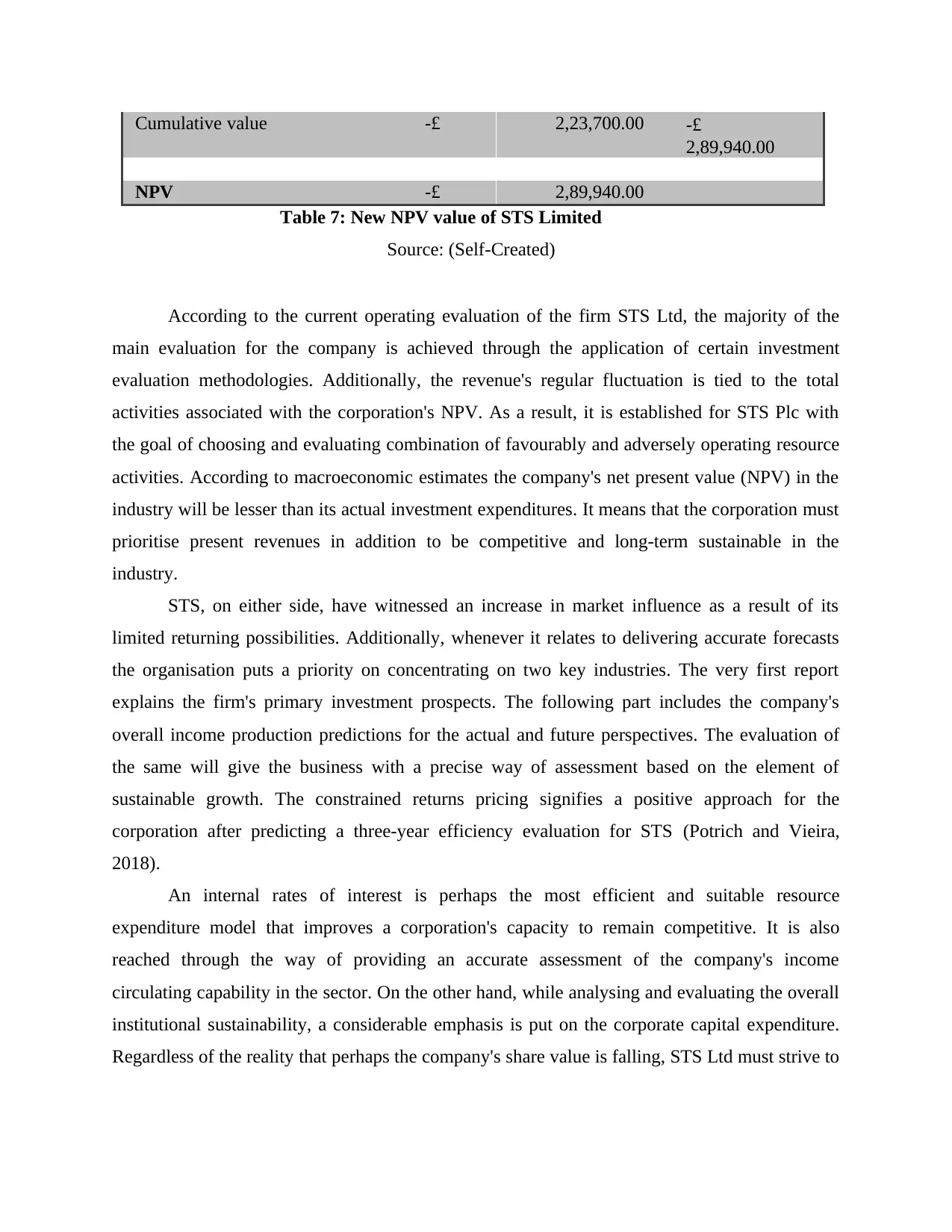

Cumulative value -£ 2,23,700.00 -£

2,89,940.00

NPV -£ 2,89,940.00

Table 7: New NPV value of STS Limited

Source: (Self-Created)

According to the current operating evaluation of the firm STS Ltd, the majority of the

main evaluation for the company is achieved through the application of certain investment

evaluation methodologies. Additionally, the revenue's regular fluctuation is tied to the total

activities associated with the corporation's NPV. As a result, it is established for STS Plc with

the goal of choosing and evaluating combination of favourably and adversely operating resource

activities. According to macroeconomic estimates the company's net present value (NPV) in the

industry will be lesser than its actual investment expenditures. It means that the corporation must

prioritise present revenues in addition to be competitive and long-term sustainable in the

industry.

STS, on either side, have witnessed an increase in market influence as a result of its

limited returning possibilities. Additionally, whenever it relates to delivering accurate forecasts

the organisation puts a priority on concentrating on two key industries. The very first report

explains the firm's primary investment prospects. The following part includes the company's

overall income production predictions for the actual and future perspectives. The evaluation of

the same will give the business with a precise way of assessment based on the element of

sustainable growth. The constrained returns pricing signifies a positive approach for the

corporation after predicting a three-year efficiency evaluation for STS (Potrich and Vieira,

2018).

An internal rates of interest is perhaps the most efficient and suitable resource

expenditure model that improves a corporation's capacity to remain competitive. It is also

reached through the way of providing an accurate assessment of the company's income

circulating capability in the sector. On the other hand, while analysing and evaluating the overall

institutional sustainability, a considerable emphasis is put on the corporate capital expenditure.

Regardless of the reality that perhaps the company's share value is falling, STS Ltd must strive to

2,89,940.00

NPV -£ 2,89,940.00

Table 7: New NPV value of STS Limited

Source: (Self-Created)

According to the current operating evaluation of the firm STS Ltd, the majority of the

main evaluation for the company is achieved through the application of certain investment

evaluation methodologies. Additionally, the revenue's regular fluctuation is tied to the total

activities associated with the corporation's NPV. As a result, it is established for STS Plc with

the goal of choosing and evaluating combination of favourably and adversely operating resource

activities. According to macroeconomic estimates the company's net present value (NPV) in the

industry will be lesser than its actual investment expenditures. It means that the corporation must

prioritise present revenues in addition to be competitive and long-term sustainable in the

industry.

STS, on either side, have witnessed an increase in market influence as a result of its

limited returning possibilities. Additionally, whenever it relates to delivering accurate forecasts

the organisation puts a priority on concentrating on two key industries. The very first report

explains the firm's primary investment prospects. The following part includes the company's

overall income production predictions for the actual and future perspectives. The evaluation of

the same will give the business with a precise way of assessment based on the element of

sustainable growth. The constrained returns pricing signifies a positive approach for the

corporation after predicting a three-year efficiency evaluation for STS (Potrich and Vieira,

2018).

An internal rates of interest is perhaps the most efficient and suitable resource

expenditure model that improves a corporation's capacity to remain competitive. It is also

reached through the way of providing an accurate assessment of the company's income

circulating capability in the sector. On the other hand, while analysing and evaluating the overall

institutional sustainability, a considerable emphasis is put on the corporate capital expenditure.

Regardless of the reality that perhaps the company's share value is falling, STS Ltd must strive to

improve its level of interest and discounted rates in attempt to remain competitive in the near

future.

The return on investment (ROI), or the company's true returns on investor is not estimated

or calculated in money units. Additionally, the actual strategy for the same is performed out just

by reviewing the company's current and past annual investment activities. STS, on either side,

limited the evaluation for the company and assigned suitable grades. As per the data, the ROI of

the organization had a constant influence on the industry over the first two years. On either end

of the spectrum, the cost grew throughout the next year, which produced a considerable impact

on STS Limited's WACC activities. As a consequence of the suggestions made for the same, it is

possible to infer that STS Ltd must prioritise adopting a better technique of management over its

WACC levels in it to preserve current and prospective economic viability.

c. Benefits and Disadvantages of Capital Assessment Methodology in Industries

Capital assessment gives corporate strategically management procedures and functions as a

defender in physical investment decision-making. Altogether, the platform is extremely effective

and well-liked for its numerous capabilities and facilities. As a consequence, the present business

Trust Plc, has adopted and implemented the aforementioned in addition to strengthen its financial

activities and relationships. In terms of improving management and execution, the firm might

have to consider the advantages and disadvantages of a specific approach. The materials

spending technique and approach should be split into three areas before starting: payback, return

on investment, and cash flow operations (Saksonova and Savina, 2016). The preceding are the

benefits and drawbacks of investment assessment methodologies-

Benefits-

By forecasting reasonable steps, the technique assists in the identification of favourable

effects.

This may give the impression that the calculation technique is straightforward to

understand and compute.

The business can connect and analyse its potential budgetary development by computing

gross profit.

Multinational firms and many others have implemented initiatives to increase the

openness and clarity of their financial management.

future.

The return on investment (ROI), or the company's true returns on investor is not estimated

or calculated in money units. Additionally, the actual strategy for the same is performed out just

by reviewing the company's current and past annual investment activities. STS, on either side,

limited the evaluation for the company and assigned suitable grades. As per the data, the ROI of

the organization had a constant influence on the industry over the first two years. On either end

of the spectrum, the cost grew throughout the next year, which produced a considerable impact

on STS Limited's WACC activities. As a consequence of the suggestions made for the same, it is

possible to infer that STS Ltd must prioritise adopting a better technique of management over its

WACC levels in it to preserve current and prospective economic viability.

c. Benefits and Disadvantages of Capital Assessment Methodology in Industries

Capital assessment gives corporate strategically management procedures and functions as a

defender in physical investment decision-making. Altogether, the platform is extremely effective

and well-liked for its numerous capabilities and facilities. As a consequence, the present business

Trust Plc, has adopted and implemented the aforementioned in addition to strengthen its financial

activities and relationships. In terms of improving management and execution, the firm might

have to consider the advantages and disadvantages of a specific approach. The materials

spending technique and approach should be split into three areas before starting: payback, return

on investment, and cash flow operations (Saksonova and Savina, 2016). The preceding are the

benefits and drawbacks of investment assessment methodologies-

Benefits-

By forecasting reasonable steps, the technique assists in the identification of favourable

effects.

This may give the impression that the calculation technique is straightforward to

understand and compute.

The business can connect and analyse its potential budgetary development by computing

gross profit.

Multinational firms and many others have implemented initiatives to increase the

openness and clarity of their financial management.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.