Determinants of Leverage and Capital Structure: A Financial Project

VerifiedAdded on 2022/12/14

|5

|632

|72

Project

AI Summary

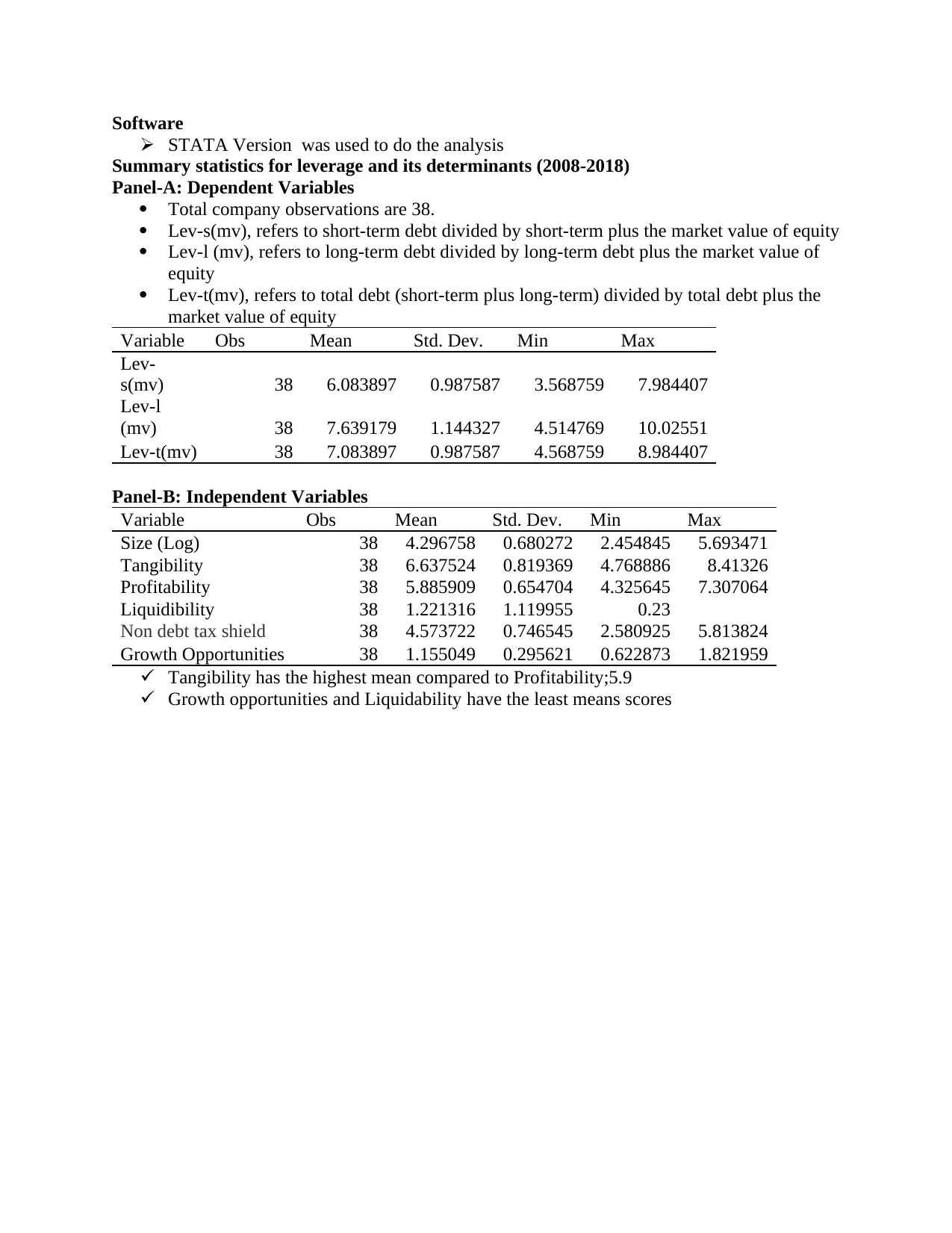

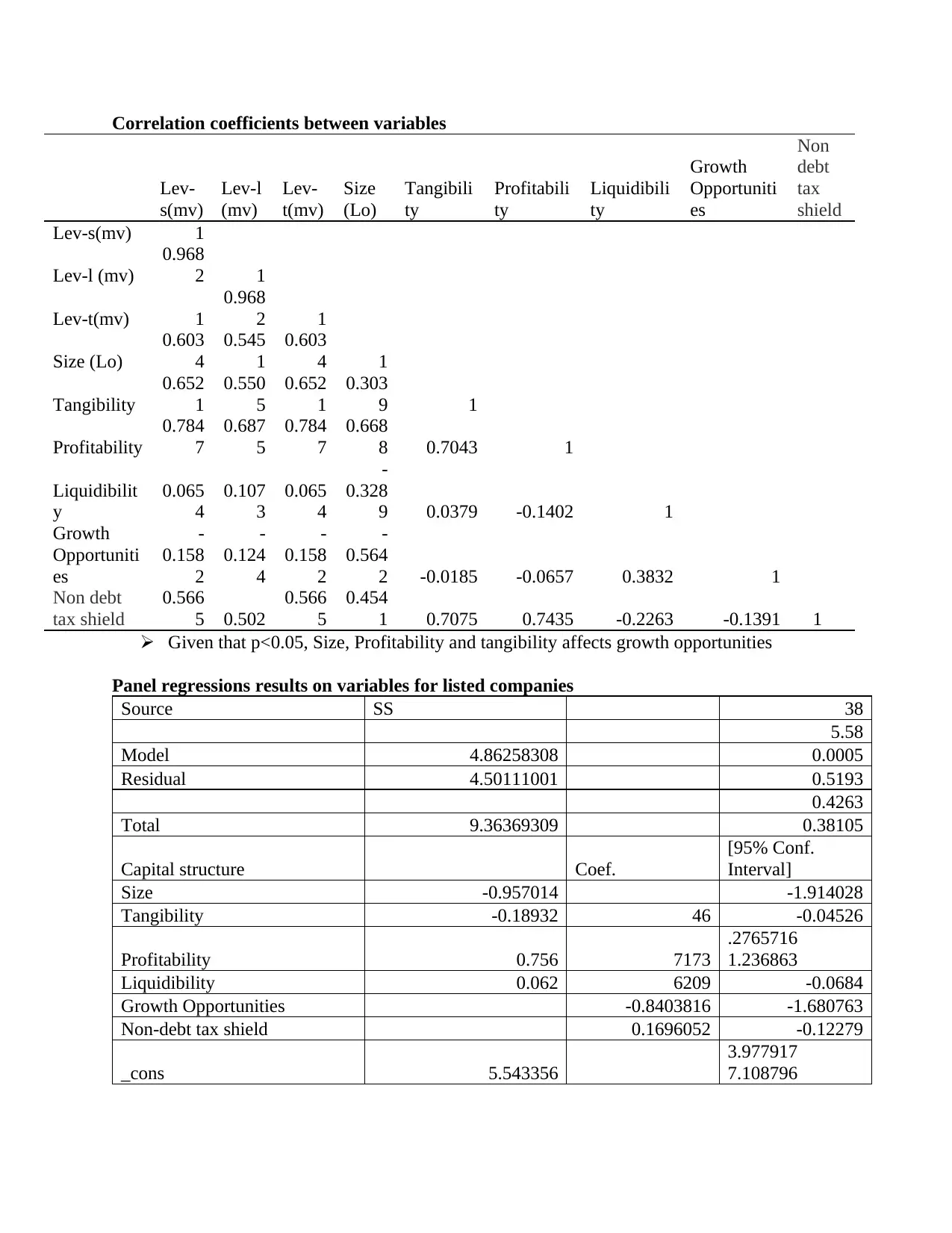

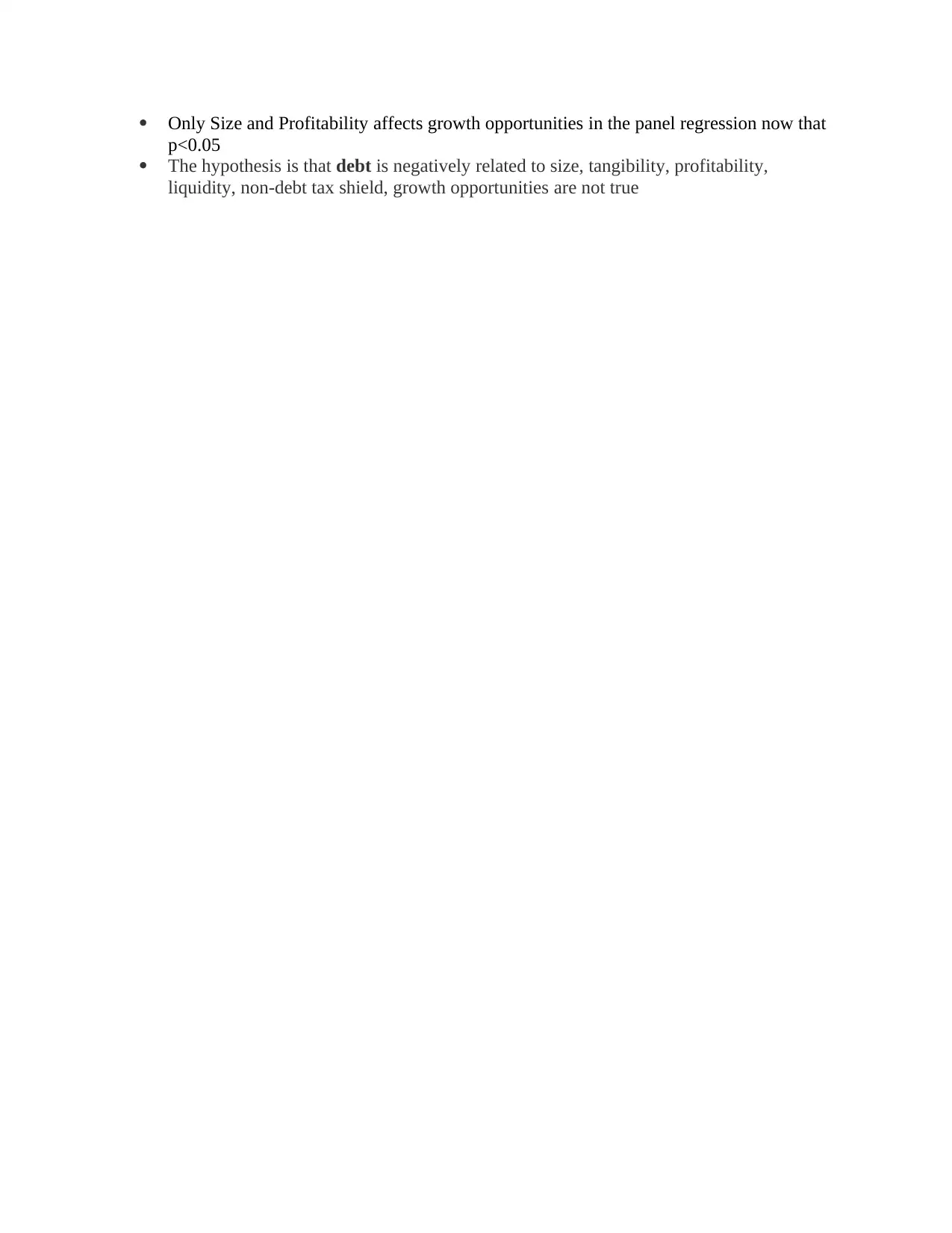

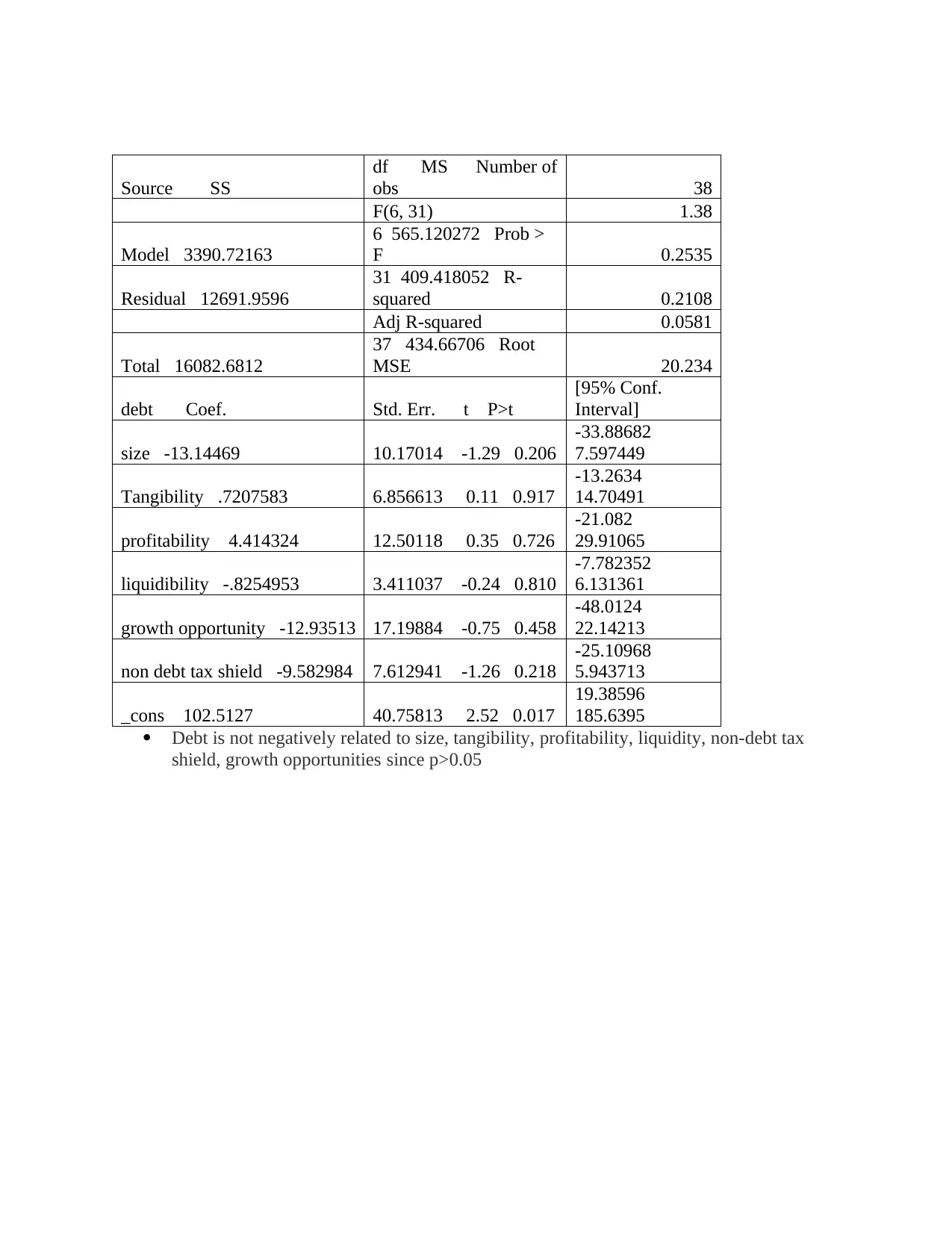

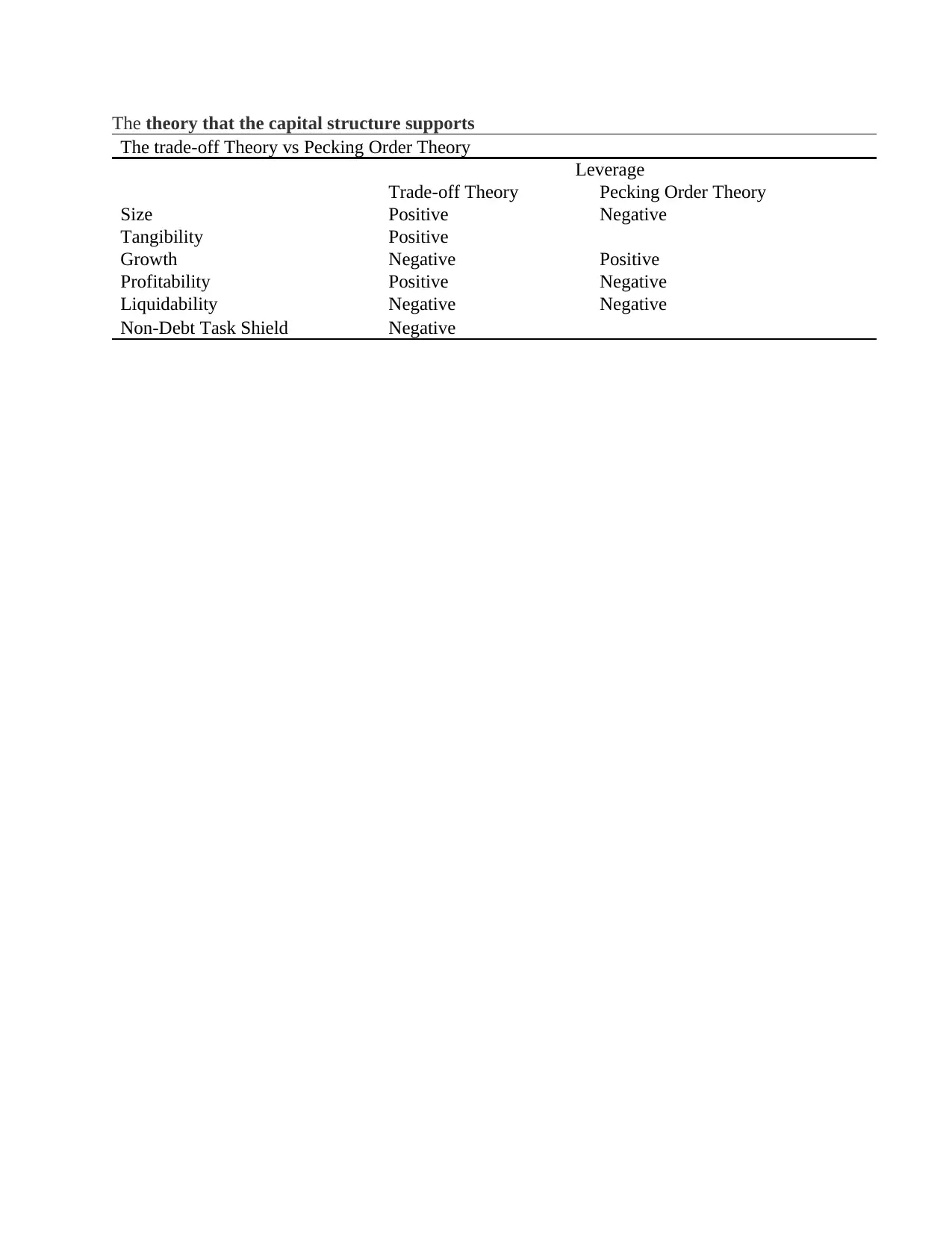

This project analyzes the determinants of leverage and capital structure using STATA. The analysis includes summary statistics for leverage and its determinants, examining short-term, long-term, and total debt relative to market value of equity. Independent variables such as size, tangibility, profitability, liquidity, non-debt tax shield, and growth opportunities are considered. Correlation coefficients and panel regression results are presented to determine the relationships between these variables and leverage. The findings suggest that size and profitability influence growth opportunities. The study tests hypotheses related to the impact of various factors on debt levels, comparing the results with the trade-off theory and pecking order theory. The project utilizes data from 38 companies over a period from 2008-2018, providing insights into the factors that influence capital structure decisions.

1 out of 5

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.