Accounting and Finance Report: Capital Budgeting and Capital Structure

VerifiedAdded on 2021/06/17

|16

|2290

|239

Report

AI Summary

This report presents a detailed financial analysis in two parts. Part A evaluates capital budgeting decisions for Saturn Pet Care, comparing the Bathurst and Wodonga projects using NPV, payback period, and profitability index, also considering product cannibalization and sales budget estimations. Part B analyzes the capital structure of ARB Limited, calculating its WACC and assessing its financial performance through ratio analysis, comparing it to Modine Manufacturing, and evaluating efforts to maximize shareholder wealth. The report recommends strategies for determining an optimal capital structure and maximizing shareholder value, providing valuable insights into financial management and investment decisions. The report also includes an executive summary and a table of contents for easy navigation.

Running head: ACCOUNTING AND FINANCE

Accounting and Finance

Name of the Student

Name of the University

Author Note

Accounting and Finance

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING AND FINANCE

Executive summary:

This particular assignment is prepared in two sections with each section depicting two

different cases. There are two section that is part A and part B. Part A deals with the

evaluation of capital budgeting of two proposed projects that would be undertaken by Saturn

Pet care. Another case is about analysis of capital structure of ABR limited. The risk and

return of organization is evaluated by the implementation of CAPM.

Executive summary:

This particular assignment is prepared in two sections with each section depicting two

different cases. There are two section that is part A and part B. Part A deals with the

evaluation of capital budgeting of two proposed projects that would be undertaken by Saturn

Pet care. Another case is about analysis of capital structure of ABR limited. The risk and

return of organization is evaluated by the implementation of CAPM.

ACCOUNTING AND FINANCE

Table of Contents

Part A:........................................................................................................................................3

Capital budgeting analysis of Bathurst project:.........................................................................3

Capital budgeting analysis of Wodonga project:.......................................................................4

Importance of cannibalization of product in capital budgeting decision:..................................5

Estimation of sales budget and capital budgeting options:........................................................5

Analysis of original value of the vacant Wodonga factory:.......................................................6

Part B:.........................................................................................................................................6

Introduction:...............................................................................................................................6

Discussion:.................................................................................................................................7

Categorizing the capital structure of ARB limited:....................................................................7

Computation of after tax weighted average cost of capital:.......................................................8

Computation of appropriate level of return using CAPM:.........................................................9

Comparing the capital structure of ARB limited with that of Modine manufacturing company:

....................................................................................................................................................9

Analysis of financial performance of ARB limited using ratio:..............................................10

Changes in the capital structure of firm:..................................................................................12

Evaluating the firms’ efforts in maximizing the shareholder wealth:......................................13

Recommendation for determining alternative capital structure:..............................................13

Conclusion:..............................................................................................................................14

References list:.........................................................................................................................15

Table of Contents

Part A:........................................................................................................................................3

Capital budgeting analysis of Bathurst project:.........................................................................3

Capital budgeting analysis of Wodonga project:.......................................................................4

Importance of cannibalization of product in capital budgeting decision:..................................5

Estimation of sales budget and capital budgeting options:........................................................5

Analysis of original value of the vacant Wodonga factory:.......................................................6

Part B:.........................................................................................................................................6

Introduction:...............................................................................................................................6

Discussion:.................................................................................................................................7

Categorizing the capital structure of ARB limited:....................................................................7

Computation of after tax weighted average cost of capital:.......................................................8

Computation of appropriate level of return using CAPM:.........................................................9

Comparing the capital structure of ARB limited with that of Modine manufacturing company:

....................................................................................................................................................9

Analysis of financial performance of ARB limited using ratio:..............................................10

Changes in the capital structure of firm:..................................................................................12

Evaluating the firms’ efforts in maximizing the shareholder wealth:......................................13

Recommendation for determining alternative capital structure:..............................................13

Conclusion:..............................................................................................................................14

References list:.........................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING AND FINANCE

Part A:

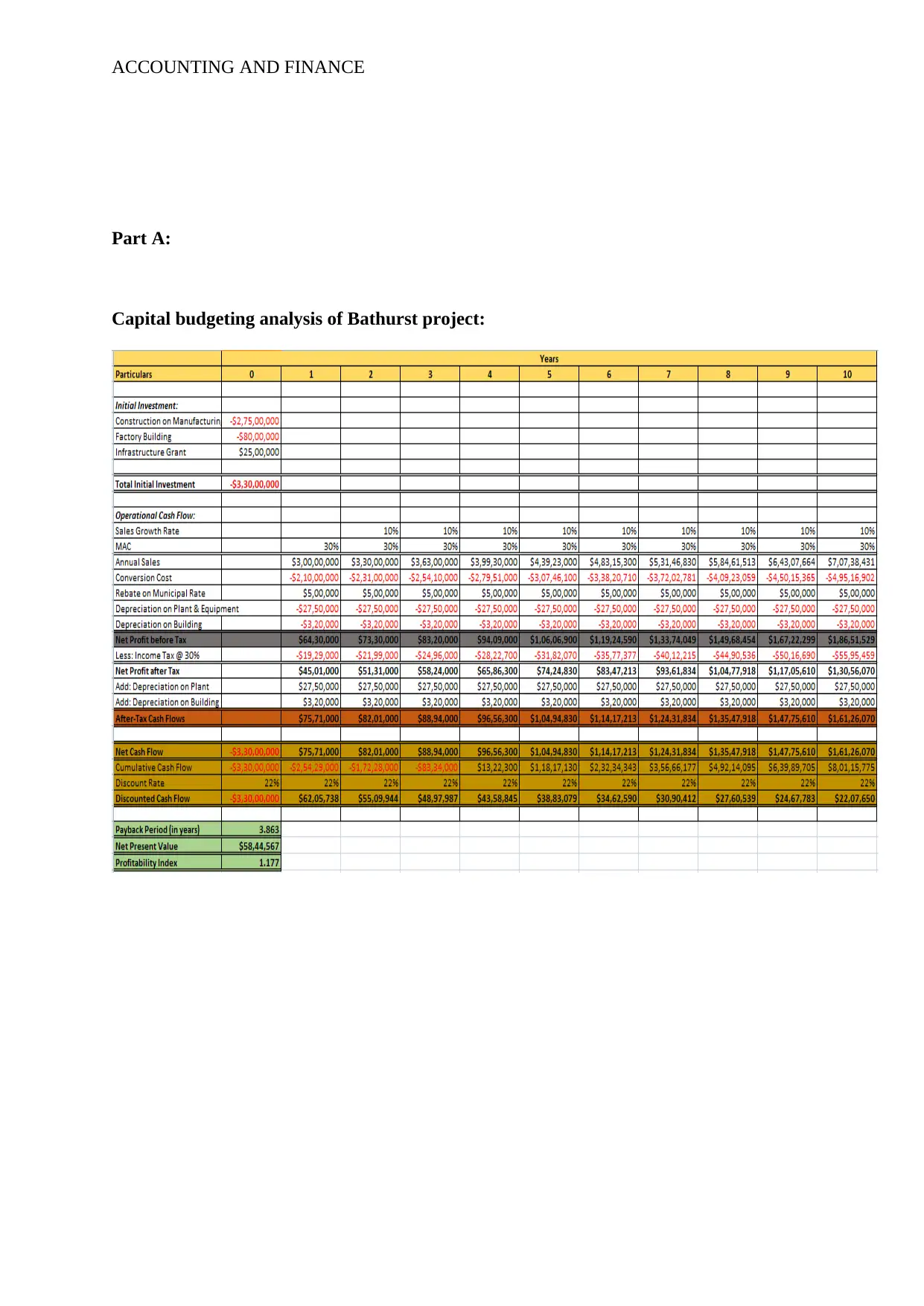

Capital budgeting analysis of Bathurst project:

Part A:

Capital budgeting analysis of Bathurst project:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING AND FINANCE

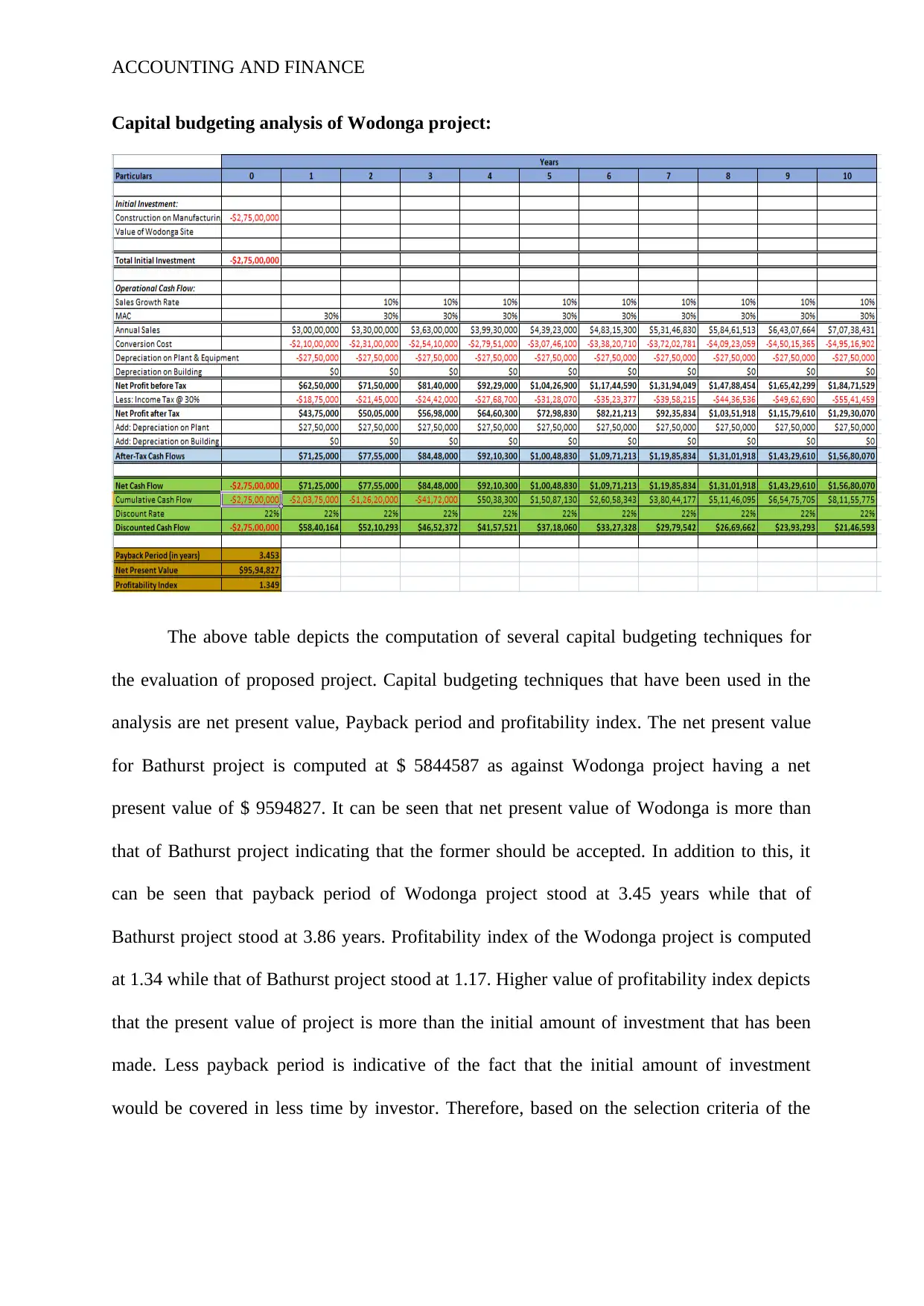

Capital budgeting analysis of Wodonga project:

The above table depicts the computation of several capital budgeting techniques for

the evaluation of proposed project. Capital budgeting techniques that have been used in the

analysis are net present value, Payback period and profitability index. The net present value

for Bathurst project is computed at $ 5844587 as against Wodonga project having a net

present value of $ 9594827. It can be seen that net present value of Wodonga is more than

that of Bathurst project indicating that the former should be accepted. In addition to this, it

can be seen that payback period of Wodonga project stood at 3.45 years while that of

Bathurst project stood at 3.86 years. Profitability index of the Wodonga project is computed

at 1.34 while that of Bathurst project stood at 1.17. Higher value of profitability index depicts

that the present value of project is more than the initial amount of investment that has been

made. Less payback period is indicative of the fact that the initial amount of investment

would be covered in less time by investor. Therefore, based on the selection criteria of the

Capital budgeting analysis of Wodonga project:

The above table depicts the computation of several capital budgeting techniques for

the evaluation of proposed project. Capital budgeting techniques that have been used in the

analysis are net present value, Payback period and profitability index. The net present value

for Bathurst project is computed at $ 5844587 as against Wodonga project having a net

present value of $ 9594827. It can be seen that net present value of Wodonga is more than

that of Bathurst project indicating that the former should be accepted. In addition to this, it

can be seen that payback period of Wodonga project stood at 3.45 years while that of

Bathurst project stood at 3.86 years. Profitability index of the Wodonga project is computed

at 1.34 while that of Bathurst project stood at 1.17. Higher value of profitability index depicts

that the present value of project is more than the initial amount of investment that has been

made. Less payback period is indicative of the fact that the initial amount of investment

would be covered in less time by investor. Therefore, based on the selection criteria of the

ACCOUNTING AND FINANCE

project, it is recommended to Saturn Pet Care to opt for making investment in Wodonga

project.

Importance of cannibalization of product in capital budgeting decision:

Product cannibalization is a phenomenon under which organization introduces new

product with an intention to reduce or lower the sales revenue, sales volume and market share

of existing product. This strategy is used by organization for promoting the new product that

has been launched by organization. Reducing the sales of new product by introducing new

product depicts negative incremental effects of new product and lower amount of profit

attributed from existing product should be treated as cost. This strategy is followed by Saturn

Pet Care with the objective of increasing the promotion of their new product. Such strategy is

adopted for increasing the sales revenue and has considerable impact on the capital budgeting

decision and selection of the project to be invested in (Andor et al., 2015).

Estimation of sales budget and capital budgeting options:

One of the concerns of marketing department is that the estimated sales budget might

be too high. The analysis of capital budgeting conducted by organization for the intended

projects is considerably impacted by the false or wrong budgeted sales estimation and thereby

would impact the process of planning and accordingly investment decision. Therefore, it is

required by management of Saturn to take appropriate measures for neutralizing the impact of

such errors relating to estimation of sales on the analysis of capital budgeting decision. Under

such circumstance of making wrong sales estimation, management can opt for the technique

such as net present value (Shimizun& Tamura, 2015). The reason attributable to the fact for

employing net present value is to offset the impact of wrong sales estimation and generating

an increased outflow of cash.

project, it is recommended to Saturn Pet Care to opt for making investment in Wodonga

project.

Importance of cannibalization of product in capital budgeting decision:

Product cannibalization is a phenomenon under which organization introduces new

product with an intention to reduce or lower the sales revenue, sales volume and market share

of existing product. This strategy is used by organization for promoting the new product that

has been launched by organization. Reducing the sales of new product by introducing new

product depicts negative incremental effects of new product and lower amount of profit

attributed from existing product should be treated as cost. This strategy is followed by Saturn

Pet Care with the objective of increasing the promotion of their new product. Such strategy is

adopted for increasing the sales revenue and has considerable impact on the capital budgeting

decision and selection of the project to be invested in (Andor et al., 2015).

Estimation of sales budget and capital budgeting options:

One of the concerns of marketing department is that the estimated sales budget might

be too high. The analysis of capital budgeting conducted by organization for the intended

projects is considerably impacted by the false or wrong budgeted sales estimation and thereby

would impact the process of planning and accordingly investment decision. Therefore, it is

required by management of Saturn to take appropriate measures for neutralizing the impact of

such errors relating to estimation of sales on the analysis of capital budgeting decision. Under

such circumstance of making wrong sales estimation, management can opt for the technique

such as net present value (Shimizun& Tamura, 2015). The reason attributable to the fact for

employing net present value is to offset the impact of wrong sales estimation and generating

an increased outflow of cash.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING AND FINANCE

Analysis of original value of the vacant Wodonga factory:

Another concern in the analysis of capital budgeting is the inclusion of original value

of vacant Wodonga factory. The opinion of Natha is considering the original cost of factory

that has been determined and it should be incorporated in the analysis of net present value.

However, the analysis of net present value would change if the cost of old factory is

incorporated. Such inclusion would make it difficult on part of investors as the results would

be negatively impacted and thereby the decision making process of organization would be

unfavorably impacted (Bartlett, 2014).

Part B:

Introduction:

The report is prepared for analyzing the capital structure of ARB Corporation Limited

that is a manufacturer, designer and distributor of light metal engineering works and vehicle

accessories. Analysis of the capability of organization in maximizing the wealth of

shareholders has also been analyzed. In addition to this, the capital structure of organization

is evaluated by comparing to other similar firms operating in the industry. Financial

performance of ARB limited is analyzed using the tool of financial ratios and any significant

changes in the capital structure of organization is analyzed for the past three years.

Analysis of original value of the vacant Wodonga factory:

Another concern in the analysis of capital budgeting is the inclusion of original value

of vacant Wodonga factory. The opinion of Natha is considering the original cost of factory

that has been determined and it should be incorporated in the analysis of net present value.

However, the analysis of net present value would change if the cost of old factory is

incorporated. Such inclusion would make it difficult on part of investors as the results would

be negatively impacted and thereby the decision making process of organization would be

unfavorably impacted (Bartlett, 2014).

Part B:

Introduction:

The report is prepared for analyzing the capital structure of ARB Corporation Limited

that is a manufacturer, designer and distributor of light metal engineering works and vehicle

accessories. Analysis of the capability of organization in maximizing the wealth of

shareholders has also been analyzed. In addition to this, the capital structure of organization

is evaluated by comparing to other similar firms operating in the industry. Financial

performance of ARB limited is analyzed using the tool of financial ratios and any significant

changes in the capital structure of organization is analyzed for the past three years.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING AND FINANCE

Discussion:

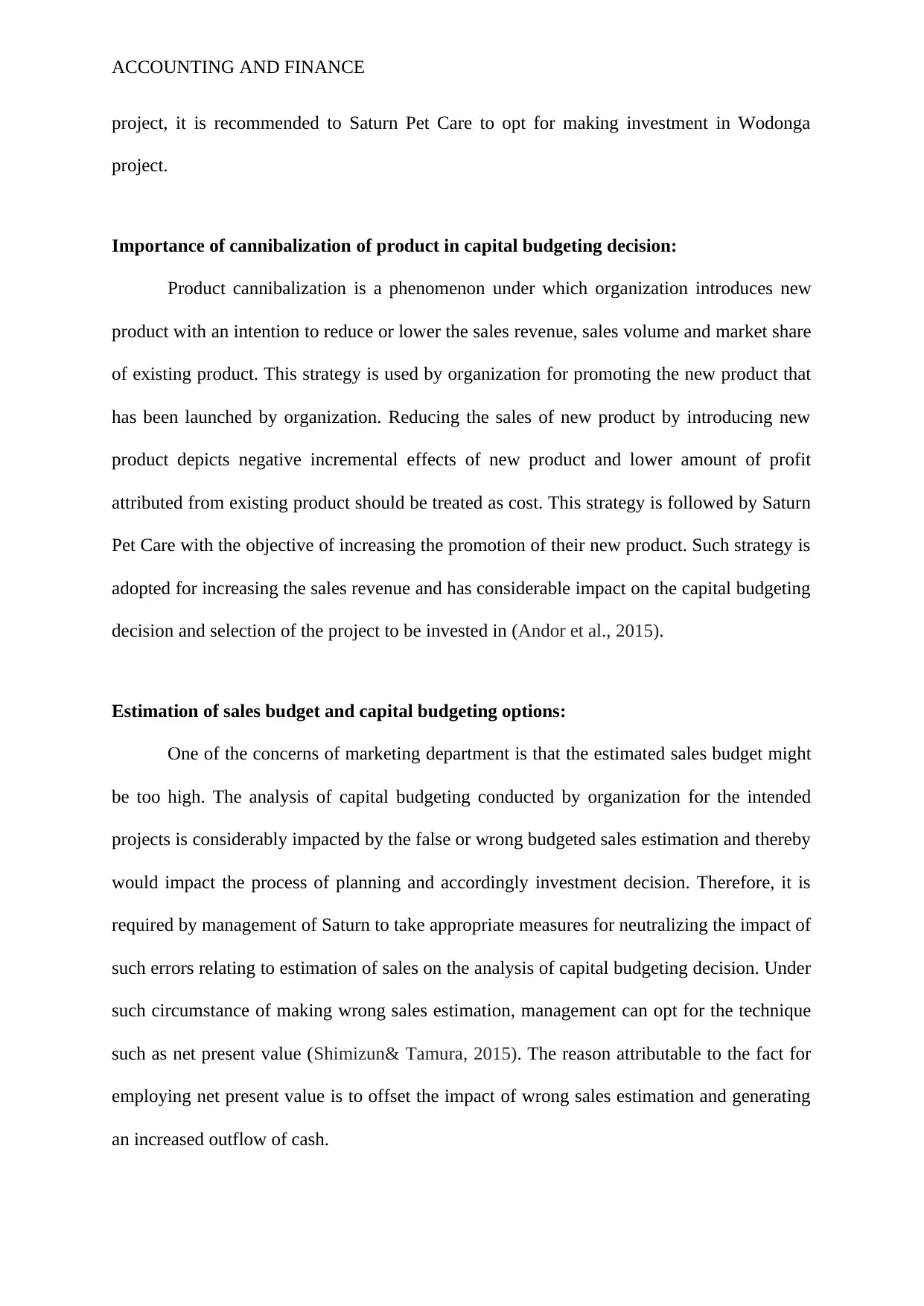

Categorizing the capital structure of ARB limited:

The above table presents the capital structure of ARB limited that involves only share

capital and no external borrowings. Organization makes use of its shareholder equity for

financing its capital and the total amount of capital stood at $ 272341. Therefore, it can be

said that company is not at all leveraged and finance all the operations using the equity of

shareholders.

Discussion:

Categorizing the capital structure of ARB limited:

The above table presents the capital structure of ARB limited that involves only share

capital and no external borrowings. Organization makes use of its shareholder equity for

financing its capital and the total amount of capital stood at $ 272341. Therefore, it can be

said that company is not at all leveraged and finance all the operations using the equity of

shareholders.

ACCOUNTING AND FINANCE

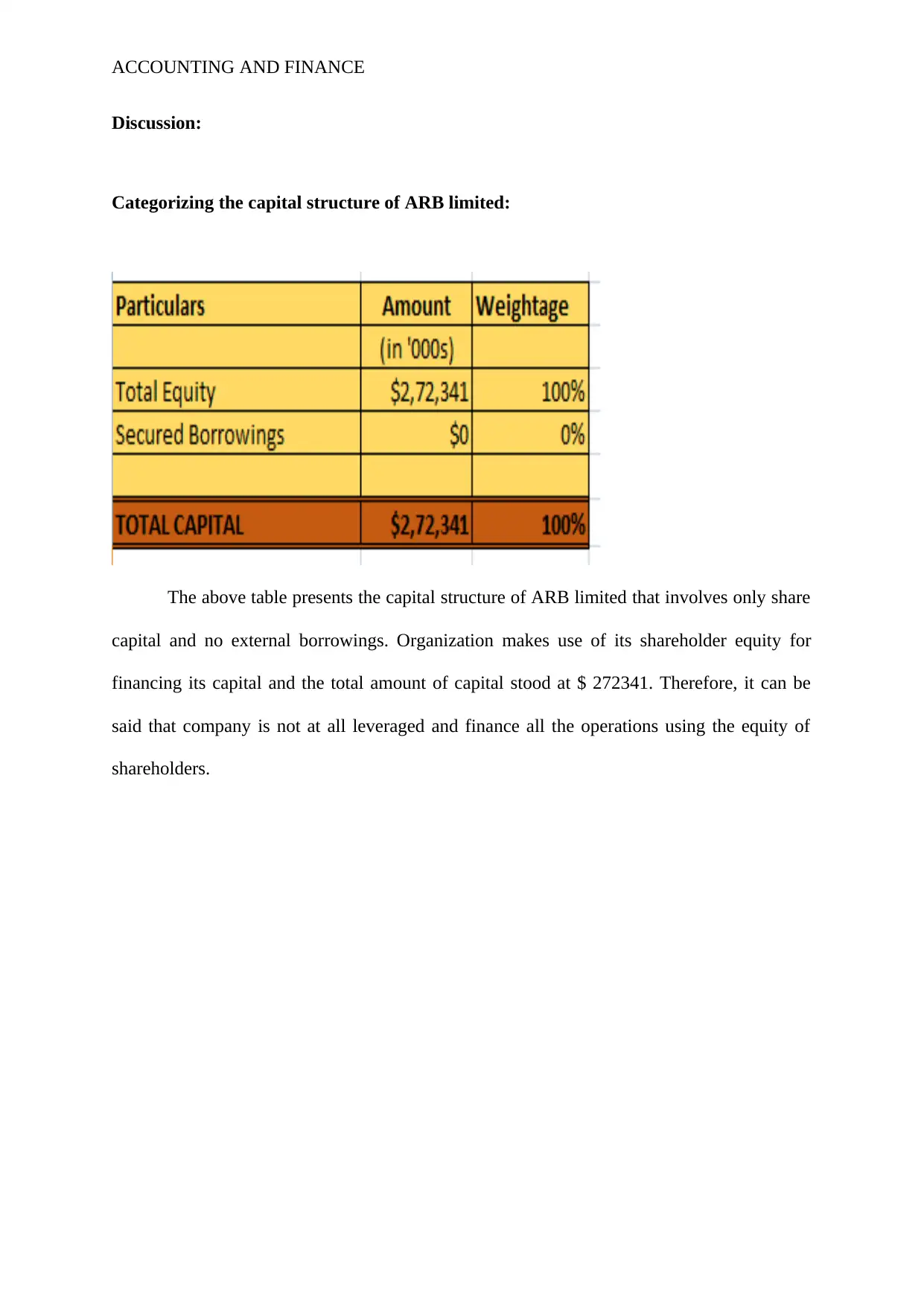

Computation of after tax weighted average cost of capital:

The weighted average cost of capital of ARB Limited is presented in the above table

and this is indicated that there has been decline in the value since year 2014. WACC has

decreased significantly from 21.52% in year 2014 to 18.05% in year 2017. This fall in

WACC is regarded as favorable from the viewpoint of organization as it signifies that lower

risk is associated with the operations of business. higher value of WACC is associated with

higher level of risks and requires investors to be provided with higher return for undertaking

higher risk.

Computation of after tax weighted average cost of capital:

The weighted average cost of capital of ARB Limited is presented in the above table

and this is indicated that there has been decline in the value since year 2014. WACC has

decreased significantly from 21.52% in year 2014 to 18.05% in year 2017. This fall in

WACC is regarded as favorable from the viewpoint of organization as it signifies that lower

risk is associated with the operations of business. higher value of WACC is associated with

higher level of risks and requires investors to be provided with higher return for undertaking

higher risk.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING AND FINANCE

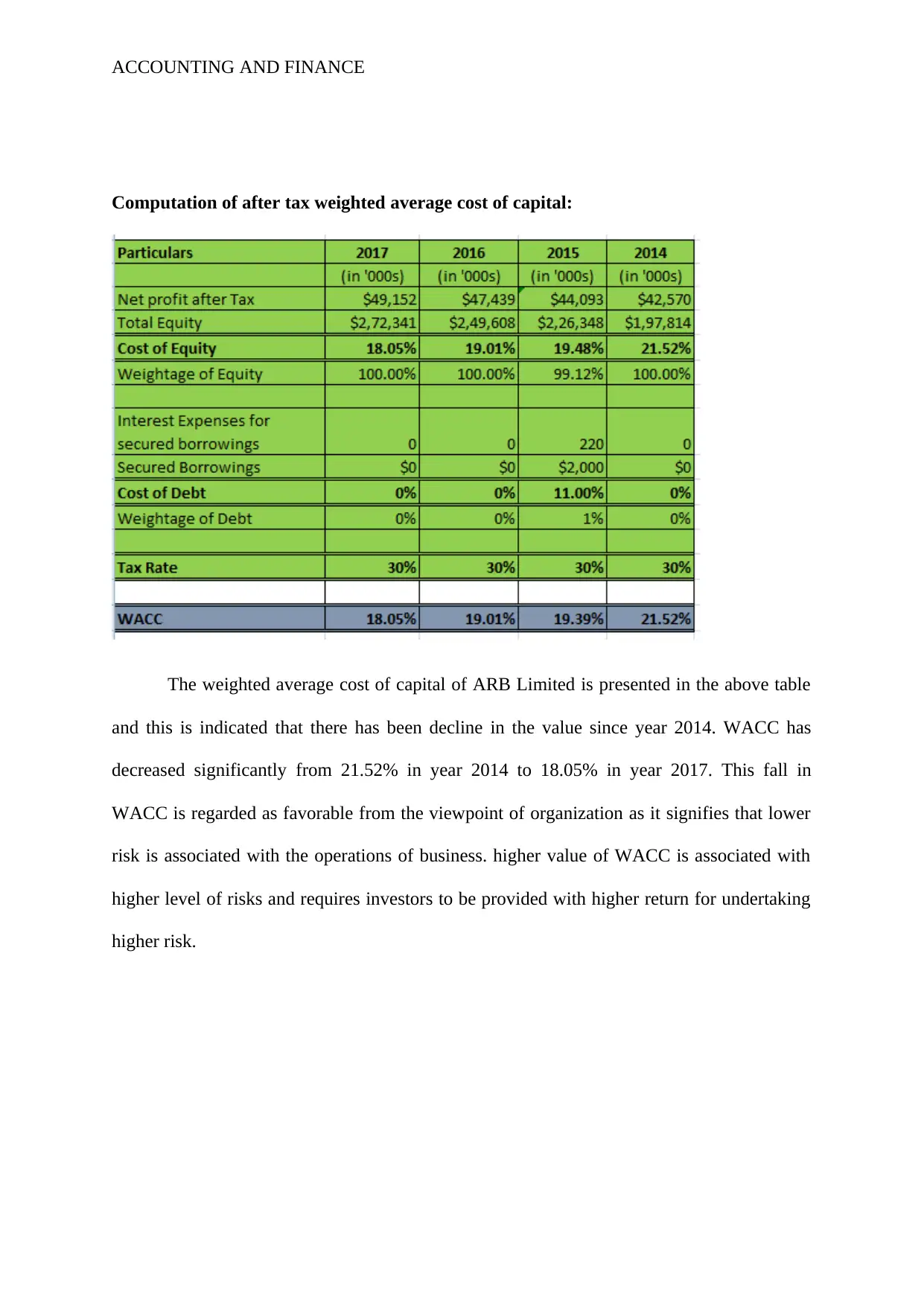

Computation of appropriate level of return using CAPM:

There is difference in value of cost of equity computed under general method as

against CAPM approach. Cost of equity of ABR limited under general method comes to

18.05% and the value computed under CAPM approach comes to 7.906%. Since the rate of

return provided by market comes to 8.54% and the cost of equity stood at 7.906% indicating

that this value is favorable as the return generated is more than the cost incurred for financing

the operations of business.

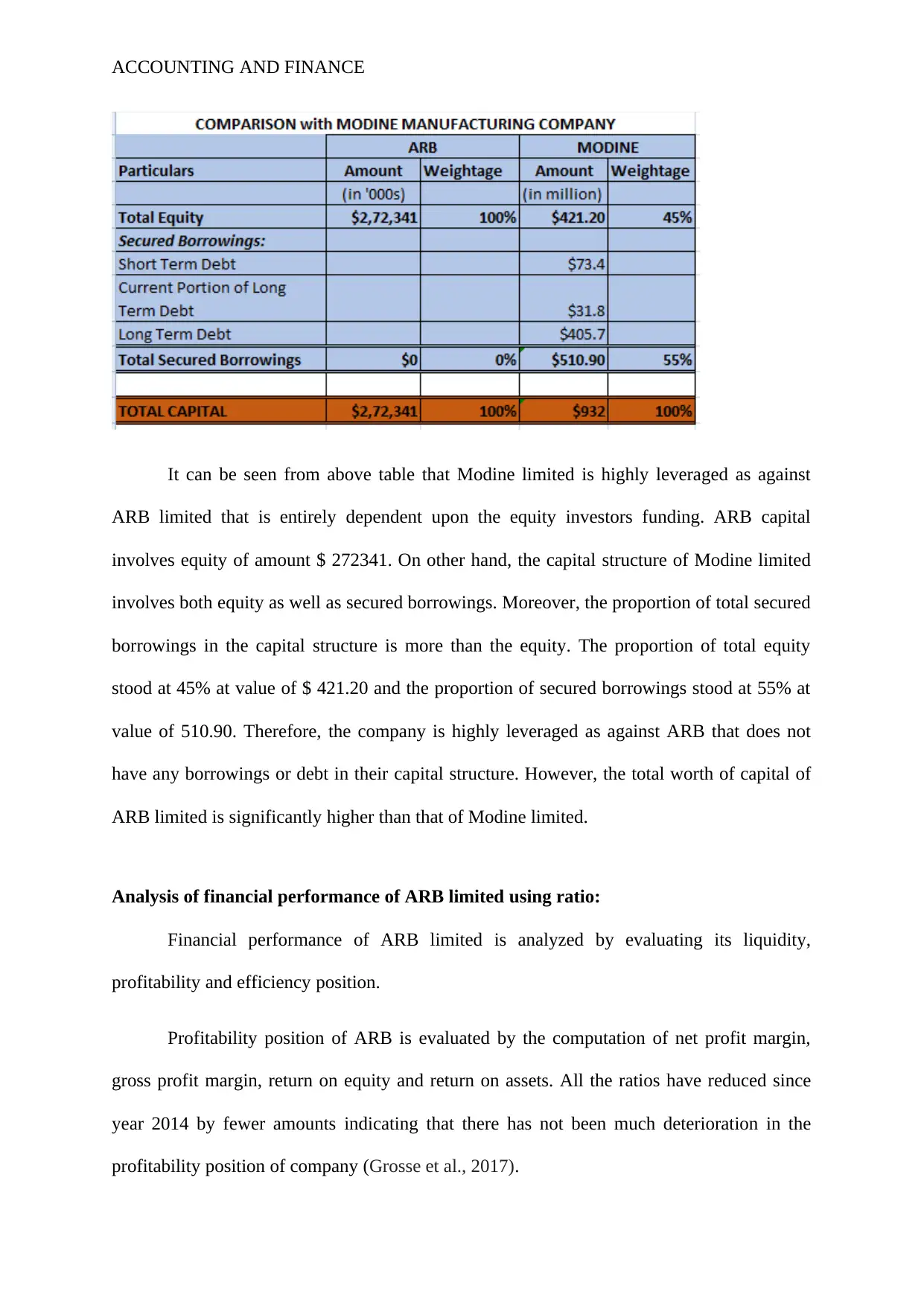

Comparing the capital structure of ARB limited with that of Modine manufacturing

company:

In this section, the capital structure of ARB Corporation is compared with one of the

firms operating in same industry that is Modine limited.

Computation of appropriate level of return using CAPM:

There is difference in value of cost of equity computed under general method as

against CAPM approach. Cost of equity of ABR limited under general method comes to

18.05% and the value computed under CAPM approach comes to 7.906%. Since the rate of

return provided by market comes to 8.54% and the cost of equity stood at 7.906% indicating

that this value is favorable as the return generated is more than the cost incurred for financing

the operations of business.

Comparing the capital structure of ARB limited with that of Modine manufacturing

company:

In this section, the capital structure of ARB Corporation is compared with one of the

firms operating in same industry that is Modine limited.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING AND FINANCE

It can be seen from above table that Modine limited is highly leveraged as against

ARB limited that is entirely dependent upon the equity investors funding. ARB capital

involves equity of amount $ 272341. On other hand, the capital structure of Modine limited

involves both equity as well as secured borrowings. Moreover, the proportion of total secured

borrowings in the capital structure is more than the equity. The proportion of total equity

stood at 45% at value of $ 421.20 and the proportion of secured borrowings stood at 55% at

value of 510.90. Therefore, the company is highly leveraged as against ARB that does not

have any borrowings or debt in their capital structure. However, the total worth of capital of

ARB limited is significantly higher than that of Modine limited.

Analysis of financial performance of ARB limited using ratio:

Financial performance of ARB limited is analyzed by evaluating its liquidity,

profitability and efficiency position.

Profitability position of ARB is evaluated by the computation of net profit margin,

gross profit margin, return on equity and return on assets. All the ratios have reduced since

year 2014 by fewer amounts indicating that there has not been much deterioration in the

profitability position of company (Grosse et al., 2017).

It can be seen from above table that Modine limited is highly leveraged as against

ARB limited that is entirely dependent upon the equity investors funding. ARB capital

involves equity of amount $ 272341. On other hand, the capital structure of Modine limited

involves both equity as well as secured borrowings. Moreover, the proportion of total secured

borrowings in the capital structure is more than the equity. The proportion of total equity

stood at 45% at value of $ 421.20 and the proportion of secured borrowings stood at 55% at

value of 510.90. Therefore, the company is highly leveraged as against ARB that does not

have any borrowings or debt in their capital structure. However, the total worth of capital of

ARB limited is significantly higher than that of Modine limited.

Analysis of financial performance of ARB limited using ratio:

Financial performance of ARB limited is analyzed by evaluating its liquidity,

profitability and efficiency position.

Profitability position of ARB is evaluated by the computation of net profit margin,

gross profit margin, return on equity and return on assets. All the ratios have reduced since

year 2014 by fewer amounts indicating that there has not been much deterioration in the

profitability position of company (Grosse et al., 2017).

ACCOUNTING AND FINANCE

The solvency position of company is evaluated by computation of debt to equity ratio,

time interest earned ratio, debt ratio and equity ratio. Table below depicts that there has been

fall in different solvency ratio by considerable amount indicating that the overall solvency

position of company have improved.

Evaluation of efficiency position of ARB limited is done by computation of inventory

turnover ratio, payable turnover and receivable turnover ratio. As indicated by figures, it can

The solvency position of company is evaluated by computation of debt to equity ratio,

time interest earned ratio, debt ratio and equity ratio. Table below depicts that there has been

fall in different solvency ratio by considerable amount indicating that the overall solvency

position of company have improved.

Evaluation of efficiency position of ARB limited is done by computation of inventory

turnover ratio, payable turnover and receivable turnover ratio. As indicated by figures, it can

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.