Capital Structure Theories and Analysis of Royal Dutch Shell PLC

VerifiedAdded on 2023/04/25

|11

|2485

|354

Report

AI Summary

This report evaluates the capital structure dilemma, examining various theories such as the Net Income Approach, Net Operating Income Approach, Conventional Approach, and Modigliani-Miller Approach. It analyzes conflicting arguments against these theories, particularly focusing on the balance between debt and equity financing and their impact on a company's cost of capital and financial risk. The report further analyzes the capital structures of Royal Dutch Shell PLC and British Petroleum (BP) PLC, revealing their strategies in managing debt and equity to optimize their capital mix, referencing their gearing ratios and interest coverage ratios, and concluding on the significant impact of capital structure on profitability and market value.

Executive Summary

The capital structure is known as debt amount and equity employed by the entity for

funding the processes and finances the assets. As per the technical point of view,

the capital structure is a cautious balance between equity and debt, which is used by

an organisation to finance the daily operations and its financial progress. The intent

of an evaluation of capital structure is to assess what mixture of equity and debt the

company is required to have. There are numerous conflicting capital structure

theories. These theories discuss the relations between financing through equity,

financing through debt and the market value of the company. In the following parts,

various theories of capital structure are discussed and critically examined.

The capital structure is known as debt amount and equity employed by the entity for

funding the processes and finances the assets. As per the technical point of view,

the capital structure is a cautious balance between equity and debt, which is used by

an organisation to finance the daily operations and its financial progress. The intent

of an evaluation of capital structure is to assess what mixture of equity and debt the

company is required to have. There are numerous conflicting capital structure

theories. These theories discuss the relations between financing through equity,

financing through debt and the market value of the company. In the following parts,

various theories of capital structure are discussed and critically examined.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CAPITAL STRUCTURE DILEMMA

Contents

Executive Summary......................................................................................................1

INTRODUCTION..........................................................................................................1

Aim and Objectives...................................................................................................1

SIGNIFICANT THEORIES of CAPITAL STRUCTURE AND UNDERLYING

RATIONALE.................................................................................................................1

The conflicting argument against different capital structure theories.......................2

ANALYSIS OF THE CAPITAL STRUCTURES OF ROYAL DUTCH SHELL PLC AND

BRITISH PETROLEUM PLC........................................................................................3

Royal Dutch Shell Plc...............................................................................................3

British Petroleum (BP) Plc........................................................................................4

CONCLUSION..............................................................................................................5

REFERENCE................................................................................................................6

Contents

Executive Summary......................................................................................................1

INTRODUCTION..........................................................................................................1

Aim and Objectives...................................................................................................1

SIGNIFICANT THEORIES of CAPITAL STRUCTURE AND UNDERLYING

RATIONALE.................................................................................................................1

The conflicting argument against different capital structure theories.......................2

ANALYSIS OF THE CAPITAL STRUCTURES OF ROYAL DUTCH SHELL PLC AND

BRITISH PETROLEUM PLC........................................................................................3

Royal Dutch Shell Plc...............................................................................................3

British Petroleum (BP) Plc........................................................................................4

CONCLUSION..............................................................................................................5

REFERENCE................................................................................................................6

INTRODUCTION

The success of an organisation is the highly associated capital structure of the

company. It determines an appropriate combination of funds such as debt and equity. A

capital structure of an organisation is having a direct impact on risk, cost and revenue of the

company (Gornall and Strebulaev, 2018). For this purpose, the evaluation of the capital

structure of Royal Dutch Shell PLC and British Petroleum (BP) PLC is carried out. Therefore,

this report is going to evaluate different capital structure theories. In the context of the

present study, the aim and objectives of the present study are mentioned below:

Aim and Objectives

Aim

The aim of the present study is “To evaluate capital structure dilemma and its

importance in business operations”.

Objectives

As per the aim, some objectives are mentioned below:

To examine different theories of capital structure

To analysis conflict argument against capital structure theories

To assess different aspects of assessing capital structure’s related changes.

SIGNIFICANT THEORIES of CAPITAL STRUCTURE AND UNDERLYING

RATIONALE

Capital structure theories play a critical role in determining an appropriate mix of

capital as per distinct business requirement. In this context, the four most important capital

structure theories are evaluated below:

Net income approach: This approach plays a critical role in determining an

appropriate capital mix. According to this approach, a firm is able to minimise the

WACC by enhancing company’s value or prices of equity shares in the marketplace

and with the help of debt, which is an important source of funds (Ridley-Duff and Bull,

2015). The theory has defined that a company is able to increase its value as well as

decrease the whole cost of funds with enhancing a amount of loan financing in firm’s

capital structure (Ardalan, 2017).

Net operating income approach: This approach has found very effective for

determining other great influence of leverage on firm’s value. This approach has

determined that alteration in the capital structure of a company is not having the

significant impact on company’s market value along with whole cost of capital (Mason

1

The success of an organisation is the highly associated capital structure of the

company. It determines an appropriate combination of funds such as debt and equity. A

capital structure of an organisation is having a direct impact on risk, cost and revenue of the

company (Gornall and Strebulaev, 2018). For this purpose, the evaluation of the capital

structure of Royal Dutch Shell PLC and British Petroleum (BP) PLC is carried out. Therefore,

this report is going to evaluate different capital structure theories. In the context of the

present study, the aim and objectives of the present study are mentioned below:

Aim and Objectives

Aim

The aim of the present study is “To evaluate capital structure dilemma and its

importance in business operations”.

Objectives

As per the aim, some objectives are mentioned below:

To examine different theories of capital structure

To analysis conflict argument against capital structure theories

To assess different aspects of assessing capital structure’s related changes.

SIGNIFICANT THEORIES of CAPITAL STRUCTURE AND UNDERLYING

RATIONALE

Capital structure theories play a critical role in determining an appropriate mix of

capital as per distinct business requirement. In this context, the four most important capital

structure theories are evaluated below:

Net income approach: This approach plays a critical role in determining an

appropriate capital mix. According to this approach, a firm is able to minimise the

WACC by enhancing company’s value or prices of equity shares in the marketplace

and with the help of debt, which is an important source of funds (Ridley-Duff and Bull,

2015). The theory has defined that a company is able to increase its value as well as

decrease the whole cost of funds with enhancing a amount of loan financing in firm’s

capital structure (Ardalan, 2017).

Net operating income approach: This approach has found very effective for

determining other great influence of leverage on firm’s value. This approach has

determined that alteration in the capital structure of a company is not having the

significant impact on company’s market value along with whole cost of capital (Mason

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

and Harrison, 2017). This theory has determined that the cost of capital remains

constant whether an organisation has adopted the debt-equity mix.

Conventional approach: The conventional approach is refered as the middle

approach between the both above discussed approaches. It is stated by the

conventional approach that the company’s market value may be enhanced or the cost

of capital may be decreased with considering more debt financing because it offers

funds ata very low price as compared to equity (Barclay and Smith, 2005). Therefore,

an organisationis able to get the best capital structure by considering the sound debt-

equity mix. However, some extent determines that the cost of equity increases as a

result of improved debt enhances monetary risks of company’s equity stakeholders

(Zhang, 2018). An increased cost of equity offsets benefit of cheap debt at this stage

of company’s capital structure. Therefore, it is not possible to manage the improved

cost of equity by an evaluation of advantages from the debt having lower-cost. Modigliani and Miller Approach (Mm Approach): Modigliani and Miller Approach is

an important theory of capital structure. The Modigliani and Miller Approach is

developed by the Franco Modigliani and Merton Miller (Graham and Harvey, 2001).

MM theory proposed two propositions for determining an appropriate mix of capital

structure:

o Proposition I: In this context, this approach determines that the determination of

company’s value, the capital structure is not so relevant. The value of two

identical firms would remain the same, and it does not have an important

influence on choice of various financial resources (Lemmon and Zender, 2019).

Therefore, the value of a firm is highly associated with the expected future

earnings if management does not consider any taxes.

o Proposition II: According to this approach, financial leverage plays a critical role

in influencing the value of a firm along with the reduction in WACC. This

proposition is consideredwhen tax-related information is available (Myers, 2001).

The conflicting argument against different capital structure theories

According to Net income operating approach and Net income approach, it has found

that COC would be reduced by increasing the raising the funds through debt because cost

debt is comparatively low to equity (Zhang, 2018). On the contrary to assumptions of two

theories of capital structure, it has addressed that the increased use of debt will be

enhanced the financial risk of the equity shareholders that would result in an overall cost of

equity (Serfling, 2016). Therefore, it can be stated that capital structure theories are not

appropriate because these approaches have determined that the cost of debt remains

2

constant whether an organisation has adopted the debt-equity mix.

Conventional approach: The conventional approach is refered as the middle

approach between the both above discussed approaches. It is stated by the

conventional approach that the company’s market value may be enhanced or the cost

of capital may be decreased with considering more debt financing because it offers

funds ata very low price as compared to equity (Barclay and Smith, 2005). Therefore,

an organisationis able to get the best capital structure by considering the sound debt-

equity mix. However, some extent determines that the cost of equity increases as a

result of improved debt enhances monetary risks of company’s equity stakeholders

(Zhang, 2018). An increased cost of equity offsets benefit of cheap debt at this stage

of company’s capital structure. Therefore, it is not possible to manage the improved

cost of equity by an evaluation of advantages from the debt having lower-cost. Modigliani and Miller Approach (Mm Approach): Modigliani and Miller Approach is

an important theory of capital structure. The Modigliani and Miller Approach is

developed by the Franco Modigliani and Merton Miller (Graham and Harvey, 2001).

MM theory proposed two propositions for determining an appropriate mix of capital

structure:

o Proposition I: In this context, this approach determines that the determination of

company’s value, the capital structure is not so relevant. The value of two

identical firms would remain the same, and it does not have an important

influence on choice of various financial resources (Lemmon and Zender, 2019).

Therefore, the value of a firm is highly associated with the expected future

earnings if management does not consider any taxes.

o Proposition II: According to this approach, financial leverage plays a critical role

in influencing the value of a firm along with the reduction in WACC. This

proposition is consideredwhen tax-related information is available (Myers, 2001).

The conflicting argument against different capital structure theories

According to Net income operating approach and Net income approach, it has found

that COC would be reduced by increasing the raising the funds through debt because cost

debt is comparatively low to equity (Zhang, 2018). On the contrary to assumptions of two

theories of capital structure, it has addressed that the increased use of debt will be

enhanced the financial risk of the equity shareholders that would result in an overall cost of

equity (Serfling, 2016). Therefore, it can be stated that capital structure theories are not

appropriate because these approaches have determined that the cost of debt remains

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

constant even with the increament in a debt’s proportion as the economic risk and lenders

are not having a significant impact due to change in the financial risk factor (Denis, 2012).

In a similar way, the study of Gornall and Strebulaev (2018) has stated that

consideration of debt as a financial resource will be reduced COC in some extent but overall

this thing enhances the overall cost of capital as a reason of an increase in financial risk.

Therefore, an organisation needs to consider several factors such as market value, the

market price of equity share, the interest rate on debt and financial risk for selection of an

appropriate capital mix (Quan, 2002).

ANALYSIS OF THE CAPITAL STRUCTURES OF ROYAL DUTCH SHELL PLC

AND BRITISH PETROLEUM PLC

Royal Dutch Shell Plc and British Petroleum Plc are addressed as leading companies

in the field of petroleum and natural gas extraction. These companies have maintained huge

capital for different business objectives(Ridley-Duff and Bull, 2015). In the context,

consideration of a proper capital structure is a very crucial task used for both companies and

evaluation of the capital structure of both companies is carried out below:

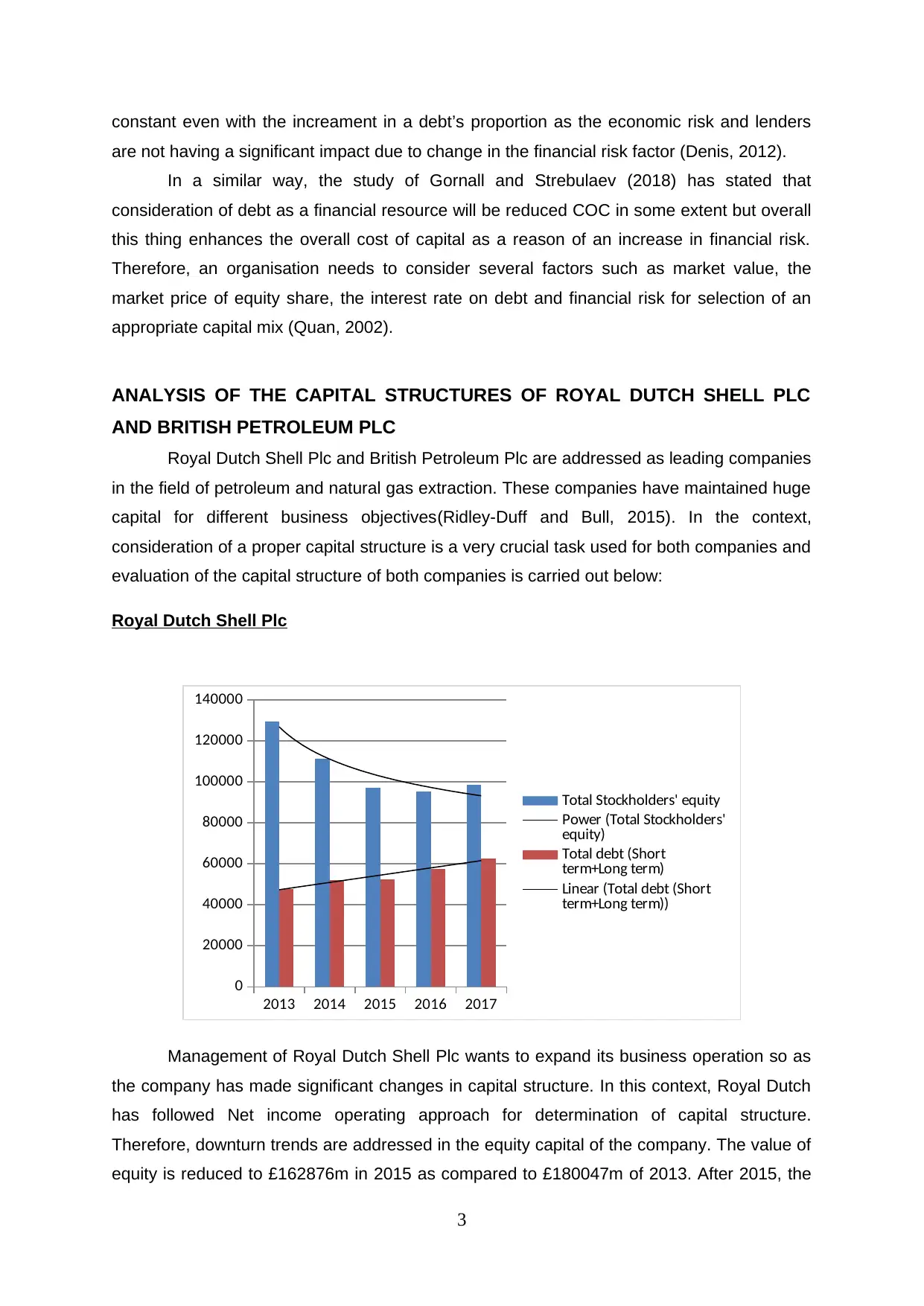

Royal Dutch Shell Plc

2013 2014 2015 2016 2017

0

20000

40000

60000

80000

100000

120000

140000

Total Stockholders' equity

Power (Total Stockholders'

equity)

Total debt (Short

term+Long term)

Linear (Total debt (Short

term+Long term))

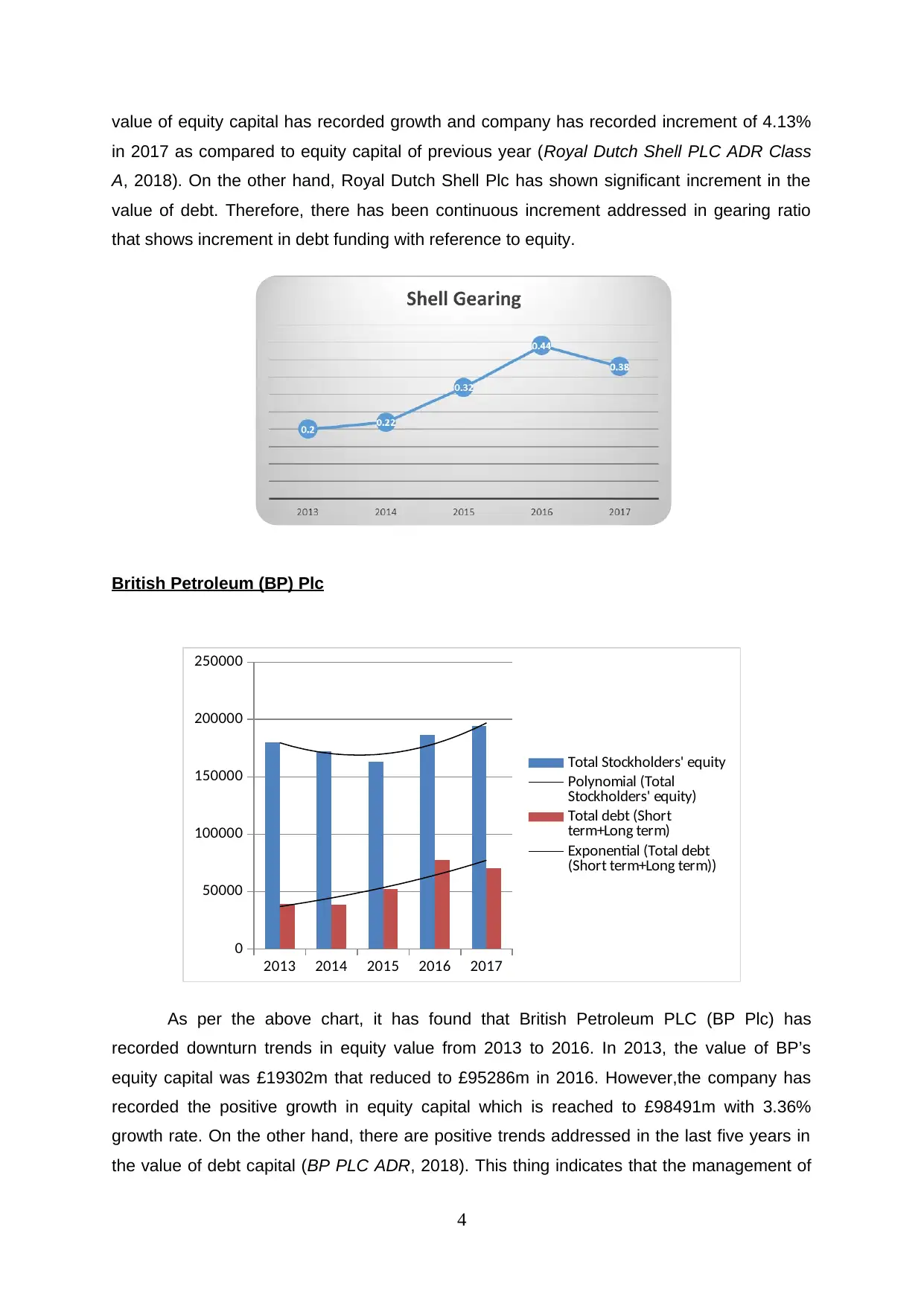

Management of Royal Dutch Shell Plc wants to expand its business operation so as

the company has made significant changes in capital structure. In this context, Royal Dutch

has followed Net income operating approach for determination of capital structure.

Therefore, downturn trends are addressed in the equity capital of the company. The value of

equity is reduced to £162876m in 2015 as compared to £180047m of 2013. After 2015, the

3

are not having a significant impact due to change in the financial risk factor (Denis, 2012).

In a similar way, the study of Gornall and Strebulaev (2018) has stated that

consideration of debt as a financial resource will be reduced COC in some extent but overall

this thing enhances the overall cost of capital as a reason of an increase in financial risk.

Therefore, an organisation needs to consider several factors such as market value, the

market price of equity share, the interest rate on debt and financial risk for selection of an

appropriate capital mix (Quan, 2002).

ANALYSIS OF THE CAPITAL STRUCTURES OF ROYAL DUTCH SHELL PLC

AND BRITISH PETROLEUM PLC

Royal Dutch Shell Plc and British Petroleum Plc are addressed as leading companies

in the field of petroleum and natural gas extraction. These companies have maintained huge

capital for different business objectives(Ridley-Duff and Bull, 2015). In the context,

consideration of a proper capital structure is a very crucial task used for both companies and

evaluation of the capital structure of both companies is carried out below:

Royal Dutch Shell Plc

2013 2014 2015 2016 2017

0

20000

40000

60000

80000

100000

120000

140000

Total Stockholders' equity

Power (Total Stockholders'

equity)

Total debt (Short

term+Long term)

Linear (Total debt (Short

term+Long term))

Management of Royal Dutch Shell Plc wants to expand its business operation so as

the company has made significant changes in capital structure. In this context, Royal Dutch

has followed Net income operating approach for determination of capital structure.

Therefore, downturn trends are addressed in the equity capital of the company. The value of

equity is reduced to £162876m in 2015 as compared to £180047m of 2013. After 2015, the

3

value of equity capital has recorded growth and company has recorded increment of 4.13%

in 2017 as compared to equity capital of previous year (Royal Dutch Shell PLC ADR Class

A, 2018). On the other hand, Royal Dutch Shell Plc has shown significant increment in the

value of debt. Therefore, there has been continuous increment addressed in gearing ratio

that shows increment in debt funding with reference to equity.

British Petroleum (BP) Plc

2013 2014 2015 2016 2017

0

50000

100000

150000

200000

250000

Total Stockholders' equity

Polynomial (Total

Stockholders' equity)

Total debt (Short

term+Long term)

Exponential (Total debt

(Short term+Long term))

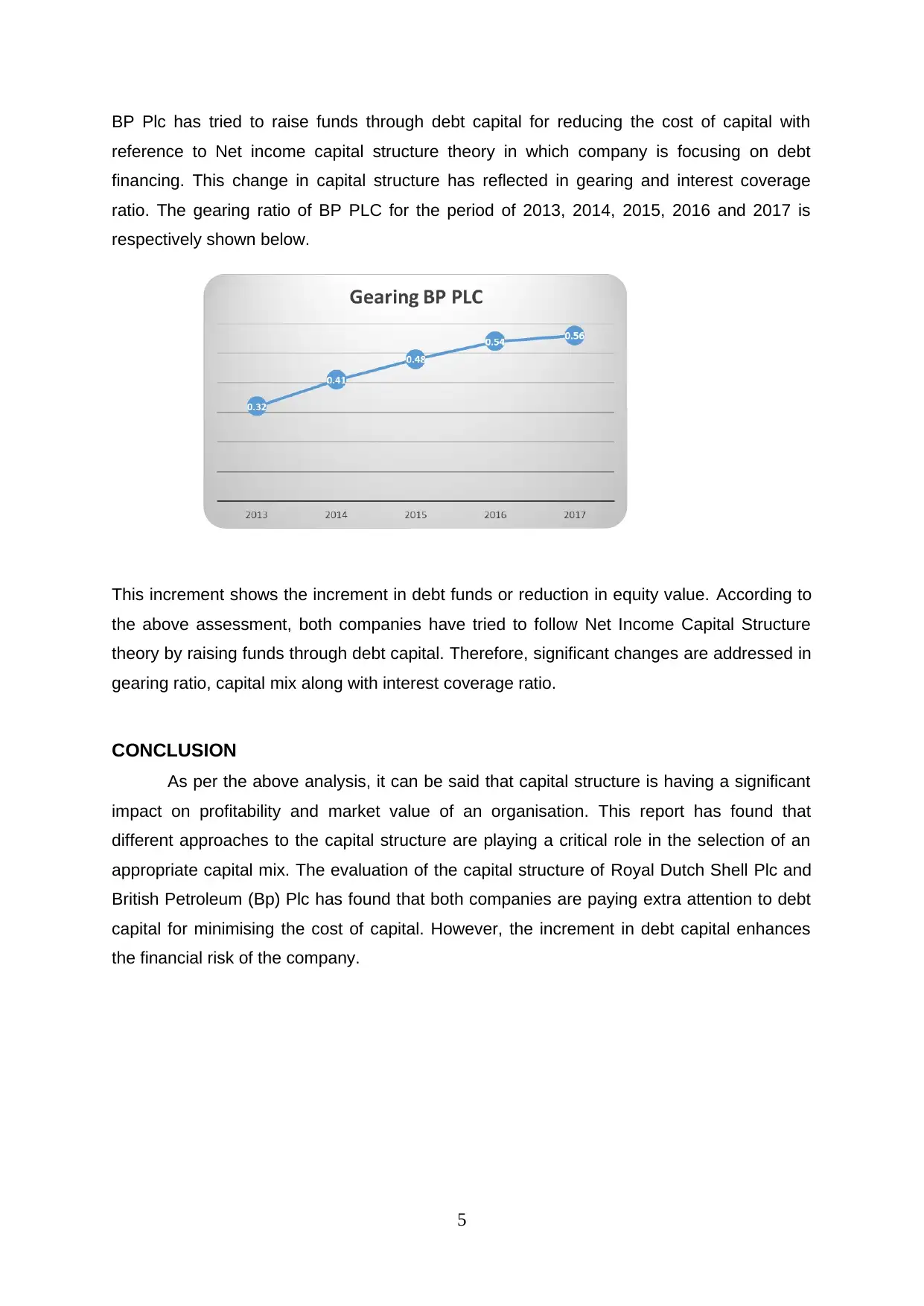

As per the above chart, it has found that British Petroleum PLC (BP Plc) has

recorded downturn trends in equity value from 2013 to 2016. In 2013, the value of BP’s

equity capital was £19302m that reduced to £95286m in 2016. However,the company has

recorded the positive growth in equity capital which is reached to £98491m with 3.36%

growth rate. On the other hand, there are positive trends addressed in the last five years in

the value of debt capital (BP PLC ADR, 2018). This thing indicates that the management of

4

in 2017 as compared to equity capital of previous year (Royal Dutch Shell PLC ADR Class

A, 2018). On the other hand, Royal Dutch Shell Plc has shown significant increment in the

value of debt. Therefore, there has been continuous increment addressed in gearing ratio

that shows increment in debt funding with reference to equity.

British Petroleum (BP) Plc

2013 2014 2015 2016 2017

0

50000

100000

150000

200000

250000

Total Stockholders' equity

Polynomial (Total

Stockholders' equity)

Total debt (Short

term+Long term)

Exponential (Total debt

(Short term+Long term))

As per the above chart, it has found that British Petroleum PLC (BP Plc) has

recorded downturn trends in equity value from 2013 to 2016. In 2013, the value of BP’s

equity capital was £19302m that reduced to £95286m in 2016. However,the company has

recorded the positive growth in equity capital which is reached to £98491m with 3.36%

growth rate. On the other hand, there are positive trends addressed in the last five years in

the value of debt capital (BP PLC ADR, 2018). This thing indicates that the management of

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

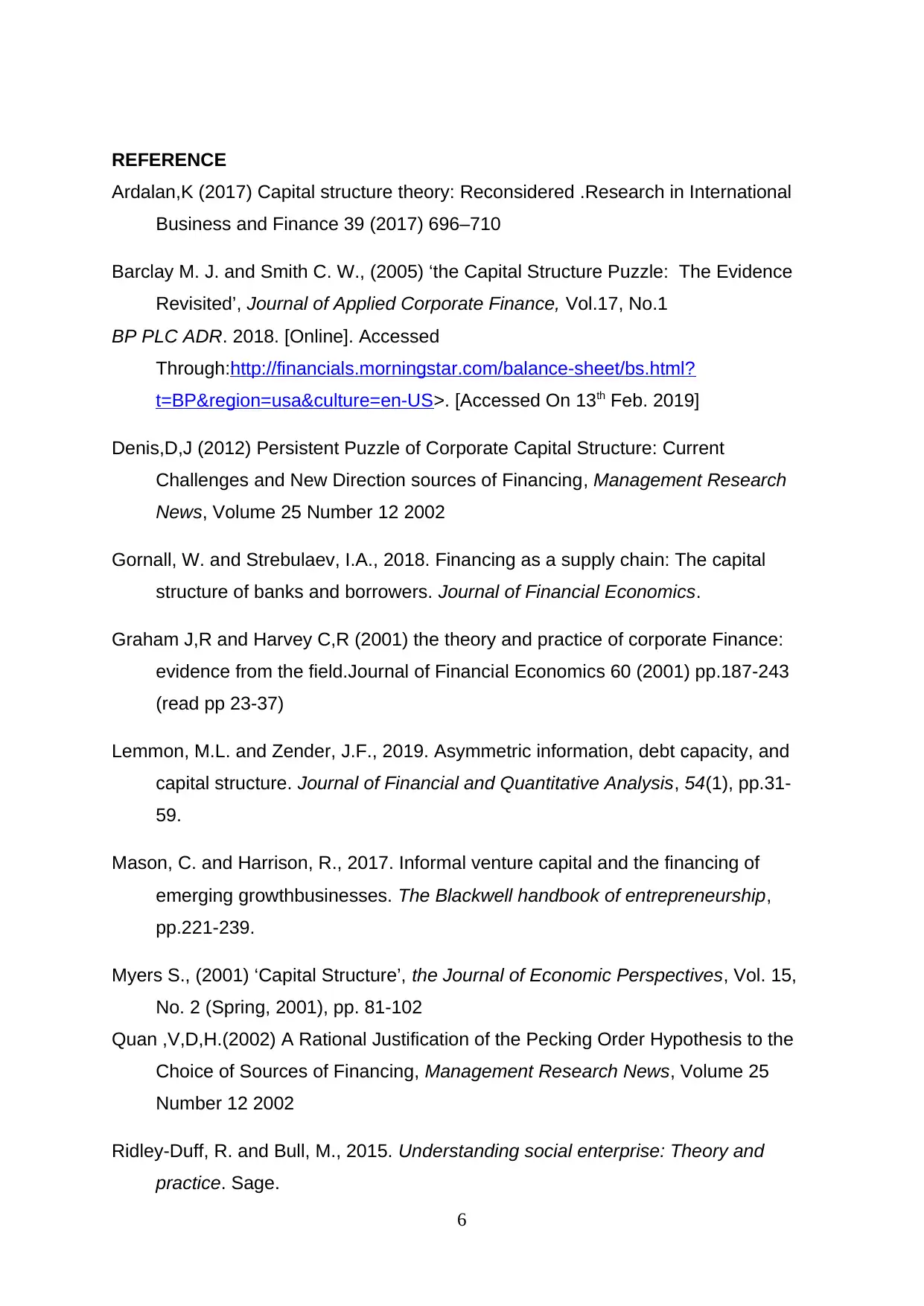

BP Plc has tried to raise funds through debt capital for reducing the cost of capital with

reference to Net income capital structure theory in which company is focusing on debt

financing. This change in capital structure has reflected in gearing and interest coverage

ratio. The gearing ratio of BP PLC for the period of 2013, 2014, 2015, 2016 and 2017 is

respectively shown below.

This increment shows the increment in debt funds or reduction in equity value. According to

the above assessment, both companies have tried to follow Net Income Capital Structure

theory by raising funds through debt capital. Therefore, significant changes are addressed in

gearing ratio, capital mix along with interest coverage ratio.

CONCLUSION

As per the above analysis, it can be said that capital structure is having a significant

impact on profitability and market value of an organisation. This report has found that

different approaches to the capital structure are playing a critical role in the selection of an

appropriate capital mix. The evaluation of the capital structure of Royal Dutch Shell Plc and

British Petroleum (Bp) Plc has found that both companies are paying extra attention to debt

capital for minimising the cost of capital. However, the increment in debt capital enhances

the financial risk of the company.

5

reference to Net income capital structure theory in which company is focusing on debt

financing. This change in capital structure has reflected in gearing and interest coverage

ratio. The gearing ratio of BP PLC for the period of 2013, 2014, 2015, 2016 and 2017 is

respectively shown below.

This increment shows the increment in debt funds or reduction in equity value. According to

the above assessment, both companies have tried to follow Net Income Capital Structure

theory by raising funds through debt capital. Therefore, significant changes are addressed in

gearing ratio, capital mix along with interest coverage ratio.

CONCLUSION

As per the above analysis, it can be said that capital structure is having a significant

impact on profitability and market value of an organisation. This report has found that

different approaches to the capital structure are playing a critical role in the selection of an

appropriate capital mix. The evaluation of the capital structure of Royal Dutch Shell Plc and

British Petroleum (Bp) Plc has found that both companies are paying extra attention to debt

capital for minimising the cost of capital. However, the increment in debt capital enhances

the financial risk of the company.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCE

Ardalan,K (2017) Capital structure theory: Reconsidered .Research in International

Business and Finance 39 (2017) 696–710

Barclay M. J. and Smith C. W., (2005) ‘the Capital Structure Puzzle: The Evidence

Revisited’, Journal of Applied Corporate Finance, Vol.17, No.1

BP PLC ADR. 2018. [Online]. Accessed

Through:http://financials.morningstar.com/balance-sheet/bs.html?

t=BP®ion=usa&culture=en-US>. [Accessed On 13th Feb. 2019]

Denis,D,J (2012) Persistent Puzzle of Corporate Capital Structure: Current

Challenges and New Direction sources of Financing, Management Research

News, Volume 25 Number 12 2002

Gornall, W. and Strebulaev, I.A., 2018. Financing as a supply chain: The capital

structure of banks and borrowers. Journal of Financial Economics.

Graham J,R and Harvey C,R (2001) the theory and practice of corporate Finance:

evidence from the field.Journal of Financial Economics 60 (2001) pp.187-243

(read pp 23-37)

Lemmon, M.L. and Zender, J.F., 2019. Asymmetric information, debt capacity, and

capital structure. Journal of Financial and Quantitative Analysis, 54(1), pp.31-

59.

Mason, C. and Harrison, R., 2017. Informal venture capital and the financing of

emerging growthbusinesses. The Blackwell handbook of entrepreneurship,

pp.221-239.

Myers S., (2001) ‘Capital Structure’, the Journal of Economic Perspectives, Vol. 15,

No. 2 (Spring, 2001), pp. 81-102

Quan ,V,D,H.(2002) A Rational Justification of the Pecking Order Hypothesis to the

Choice of Sources of Financing, Management Research News, Volume 25

Number 12 2002

Ridley-Duff, R. and Bull, M., 2015. Understanding social enterprise: Theory and

practice. Sage.

6

Ardalan,K (2017) Capital structure theory: Reconsidered .Research in International

Business and Finance 39 (2017) 696–710

Barclay M. J. and Smith C. W., (2005) ‘the Capital Structure Puzzle: The Evidence

Revisited’, Journal of Applied Corporate Finance, Vol.17, No.1

BP PLC ADR. 2018. [Online]. Accessed

Through:http://financials.morningstar.com/balance-sheet/bs.html?

t=BP®ion=usa&culture=en-US>. [Accessed On 13th Feb. 2019]

Denis,D,J (2012) Persistent Puzzle of Corporate Capital Structure: Current

Challenges and New Direction sources of Financing, Management Research

News, Volume 25 Number 12 2002

Gornall, W. and Strebulaev, I.A., 2018. Financing as a supply chain: The capital

structure of banks and borrowers. Journal of Financial Economics.

Graham J,R and Harvey C,R (2001) the theory and practice of corporate Finance:

evidence from the field.Journal of Financial Economics 60 (2001) pp.187-243

(read pp 23-37)

Lemmon, M.L. and Zender, J.F., 2019. Asymmetric information, debt capacity, and

capital structure. Journal of Financial and Quantitative Analysis, 54(1), pp.31-

59.

Mason, C. and Harrison, R., 2017. Informal venture capital and the financing of

emerging growthbusinesses. The Blackwell handbook of entrepreneurship,

pp.221-239.

Myers S., (2001) ‘Capital Structure’, the Journal of Economic Perspectives, Vol. 15,

No. 2 (Spring, 2001), pp. 81-102

Quan ,V,D,H.(2002) A Rational Justification of the Pecking Order Hypothesis to the

Choice of Sources of Financing, Management Research News, Volume 25

Number 12 2002

Ridley-Duff, R. and Bull, M., 2015. Understanding social enterprise: Theory and

practice. Sage.

6

Royal Dutch Shell PLC ADR Class A. 2018. [Online]. Accessed

Through :<http://financials.morningstar.com/income-statement/is.html?

t=RDS.A®ion=usa&culture=en-US>. [Accessed On 13th Feb. 2019]

Serfling, M., 2016. Firing costs and capital structure decisions. The Journal of

Finance, 71(5), pp.2239-2286.

Zhang, W.B., 2018. Economic Growth Theory: Capital, Knowledge, and Economic

Stuctures. Routledge.

7

Through :<http://financials.morningstar.com/income-statement/is.html?

t=RDS.A®ion=usa&culture=en-US>. [Accessed On 13th Feb. 2019]

Serfling, M., 2016. Firing costs and capital structure decisions. The Journal of

Finance, 71(5), pp.2239-2286.

Zhang, W.B., 2018. Economic Growth Theory: Capital, Knowledge, and Economic

Stuctures. Routledge.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

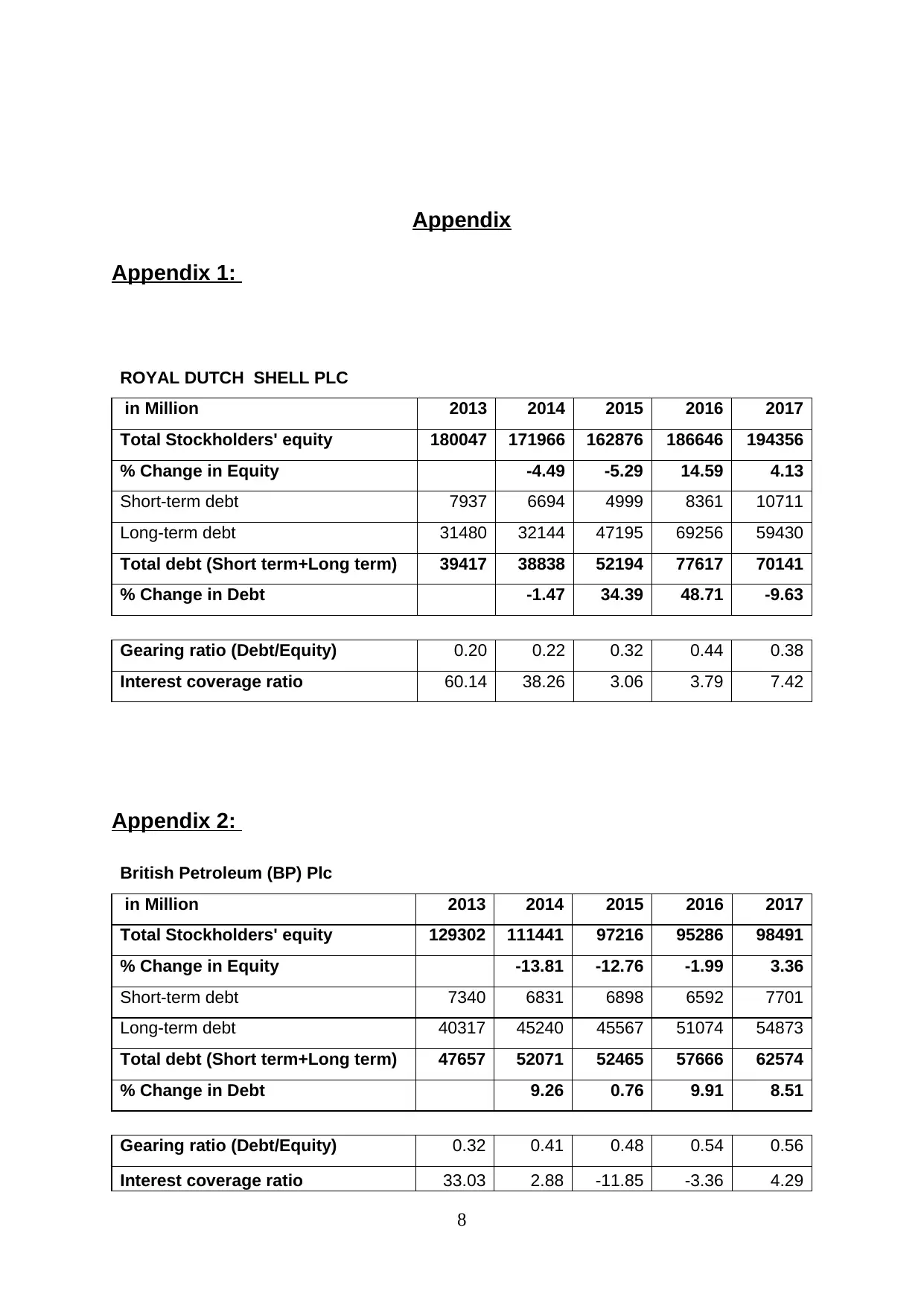

Appendix

Appendix 1:

ROYAL DUTCH SHELL PLC

in Million 2013 2014 2015 2016 2017

Total Stockholders' equity 180047 171966 162876 186646 194356

% Change in Equity -4.49 -5.29 14.59 4.13

Short-term debt 7937 6694 4999 8361 10711

Long-term debt 31480 32144 47195 69256 59430

Total debt (Short term+Long term) 39417 38838 52194 77617 70141

% Change in Debt -1.47 34.39 48.71 -9.63

Gearing ratio (Debt/Equity) 0.20 0.22 0.32 0.44 0.38

Interest coverage ratio 60.14 38.26 3.06 3.79 7.42

Appendix 2:

British Petroleum (BP) Plc

in Million 2013 2014 2015 2016 2017

Total Stockholders' equity 129302 111441 97216 95286 98491

% Change in Equity -13.81 -12.76 -1.99 3.36

Short-term debt 7340 6831 6898 6592 7701

Long-term debt 40317 45240 45567 51074 54873

Total debt (Short term+Long term) 47657 52071 52465 57666 62574

% Change in Debt 9.26 0.76 9.91 8.51

Gearing ratio (Debt/Equity) 0.32 0.41 0.48 0.54 0.56

Interest coverage ratio 33.03 2.88 -11.85 -3.36 4.29

8

Appendix 1:

ROYAL DUTCH SHELL PLC

in Million 2013 2014 2015 2016 2017

Total Stockholders' equity 180047 171966 162876 186646 194356

% Change in Equity -4.49 -5.29 14.59 4.13

Short-term debt 7937 6694 4999 8361 10711

Long-term debt 31480 32144 47195 69256 59430

Total debt (Short term+Long term) 39417 38838 52194 77617 70141

% Change in Debt -1.47 34.39 48.71 -9.63

Gearing ratio (Debt/Equity) 0.20 0.22 0.32 0.44 0.38

Interest coverage ratio 60.14 38.26 3.06 3.79 7.42

Appendix 2:

British Petroleum (BP) Plc

in Million 2013 2014 2015 2016 2017

Total Stockholders' equity 129302 111441 97216 95286 98491

% Change in Equity -13.81 -12.76 -1.99 3.36

Short-term debt 7340 6831 6898 6592 7701

Long-term debt 40317 45240 45567 51074 54873

Total debt (Short term+Long term) 47657 52071 52465 57666 62574

% Change in Debt 9.26 0.76 9.91 8.51

Gearing ratio (Debt/Equity) 0.32 0.41 0.48 0.54 0.56

Interest coverage ratio 33.03 2.88 -11.85 -3.36 4.29

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

9

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.