BBMF2824 Financial Management Group Assignment: Silibin's Analysis

VerifiedAdded on 2021/08/23

|39

|6017

|18

Project

AI Summary

This project analyzes Silibin's financial management, focusing on its capital structure in response to changing market conditions, including declining competitiveness, interest expenses, and the impact of the Kinrara acquisition. The analysis evaluates the suitability of different debt ratios (40% vs. 25%), considering factors like hybrid securities, equity financing, diversification, and hedging strategies. The project recommends a 25% debt ratio to maintain financial flexibility, improve interest coverage, and potentially restore a higher bond rating, while also addressing the practicality of equity financing and the importance of optimal leverage to avoid financial constraints. The project's conclusion emphasizes the importance of financial flexibility and conservative financial planning for Silibin's long-term sustainability.

FACULTY OF ACCOUNTANCY, FINANCE AND BUSINESS

ACADEMIC YEAR 2020/2021

BACHELOR OF COMMERCE (HONOURS)

BBMF2824 FINANCIAL MANAGEMENT

GROUP ASSIGNMENT

Tutor name : MR. THEANG KOK FOO

Tutorial group no. : 5

Word count : Part 1: 1643 Part 2: 1600

Percentage of plagiarism : 1%

Name of students: Student ID No:

(1) HOONG JIA MING : 20WBR08075

(2) LOW CHEE SENG : 20WBR08127

(3) TEO KOK HAO : 20WBR08171

ACADEMIC YEAR 2020/2021

BACHELOR OF COMMERCE (HONOURS)

BBMF2824 FINANCIAL MANAGEMENT

GROUP ASSIGNMENT

Tutor name : MR. THEANG KOK FOO

Tutorial group no. : 5

Word count : Part 1: 1643 Part 2: 1600

Percentage of plagiarism : 1%

Name of students: Student ID No:

(1) HOONG JIA MING : 20WBR08075

(2) LOW CHEE SENG : 20WBR08127

(3) TEO KOK HAO : 20WBR08171

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

Part 1 (1643 words)

Introduction

Silibin faced rapid changing external environments since 2001 such as competitive pressure, oil

prices fluctuation and European debt crisis resulting in net income falls. It resulted in Silibin’s

cash shortage in meeting the capital expenditure needs. Silibin was forced to change capital

structure policy from fully equity to partial debt finance. Moreover, the acquisition of Kinrara at a

premium price increased the debt ratio dramatically to 36%, consequently resulted in a drop of

credit ratings from AAA to AA. As current financing structure has gone against conservative

financing policy, Silibin has to restructure its financing policy to meet its finance needs in view of

the change of environment and business.

The management has re-evaluated capital structure policy and compared it with similar industries

that use the same policy for their performance. Subsequently, they formulated two plans,

accounting as practising 40% debt ratio or reducing it to 25% for future. This analysis report aims

to consider the most appropriate capital structure policy that suits its current business conditions

and financial performance according to issues currently faced by Siliin. Selection of suitable

capital structure that suits the company could help the company fully utilize the financing to carry

out their business operations for the growth of the company without affecting the company and

shareholders’ wealth.

Issues

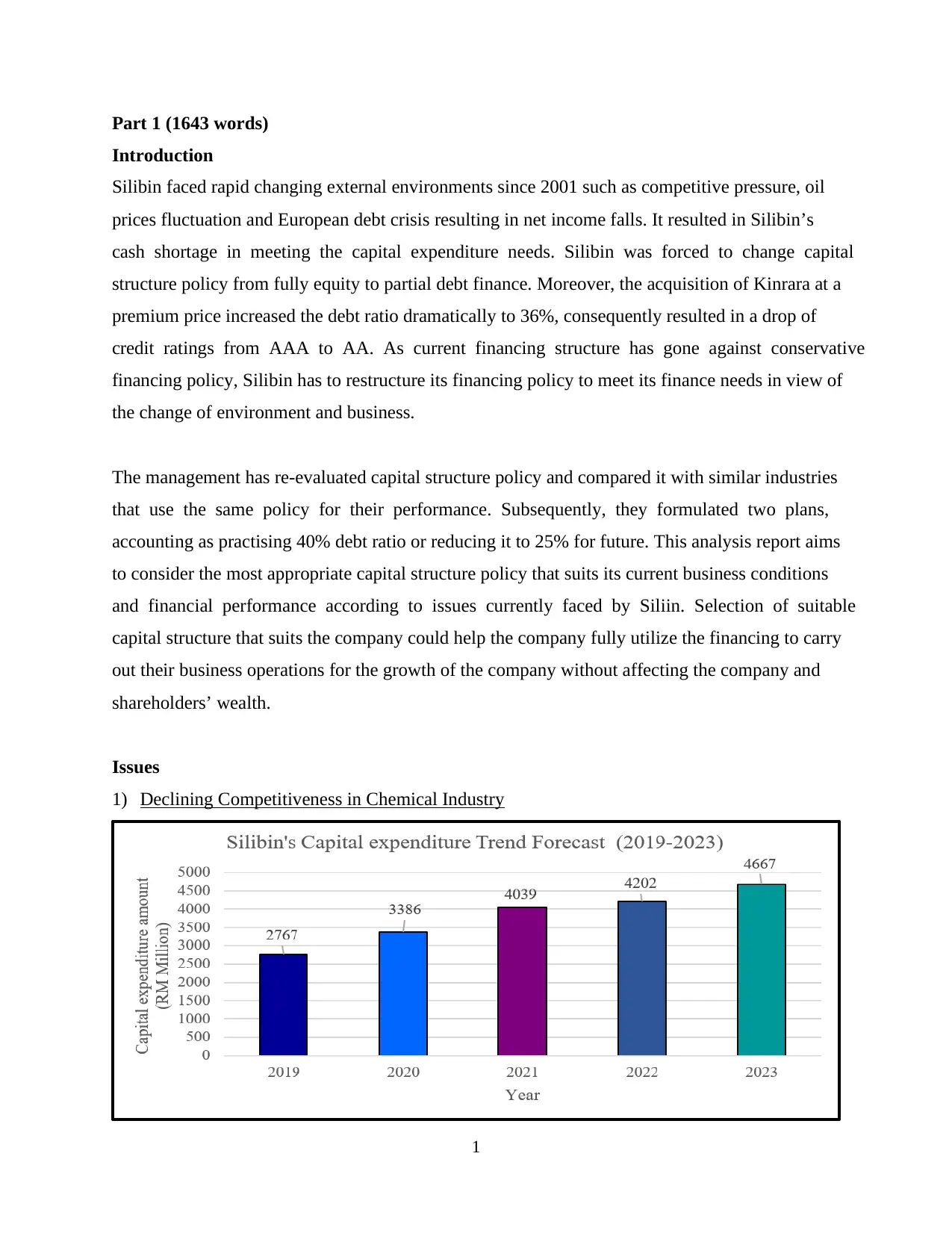

1) Declining Competitiveness in Chemical Industry

Part 1 (1643 words)

Introduction

Silibin faced rapid changing external environments since 2001 such as competitive pressure, oil

prices fluctuation and European debt crisis resulting in net income falls. It resulted in Silibin’s

cash shortage in meeting the capital expenditure needs. Silibin was forced to change capital

structure policy from fully equity to partial debt finance. Moreover, the acquisition of Kinrara at a

premium price increased the debt ratio dramatically to 36%, consequently resulted in a drop of

credit ratings from AAA to AA. As current financing structure has gone against conservative

financing policy, Silibin has to restructure its financing policy to meet its finance needs in view of

the change of environment and business.

The management has re-evaluated capital structure policy and compared it with similar industries

that use the same policy for their performance. Subsequently, they formulated two plans,

accounting as practising 40% debt ratio or reducing it to 25% for future. This analysis report aims

to consider the most appropriate capital structure policy that suits its current business conditions

and financial performance according to issues currently faced by Siliin. Selection of suitable

capital structure that suits the company could help the company fully utilize the financing to carry

out their business operations for the growth of the company without affecting the company and

shareholders’ wealth.

Issues

1) Declining Competitiveness in Chemical Industry

2

Silibin is relatively less competitive in comparison to its peers, DC Bhd and MST Bhd in the

aspects of ROE, EPS growth rate and net income, despite its high sales (Exhibit 3). In addition, in

view of Silibin’s financial inability for the execution of non-deferrable capital expenditures

(CAPEX) programmes which is critical to restore and sustain a better chemical product line

competitive cost position relative to its rivals, capital structure re-evaluation is vital. Silibin’s

existing capital structure may no longer be relevant, as it struggles to support its CAPEX which is

projected to rise by 46.07% (2019-2023) to improve its competitiveness (Exhibit 6).

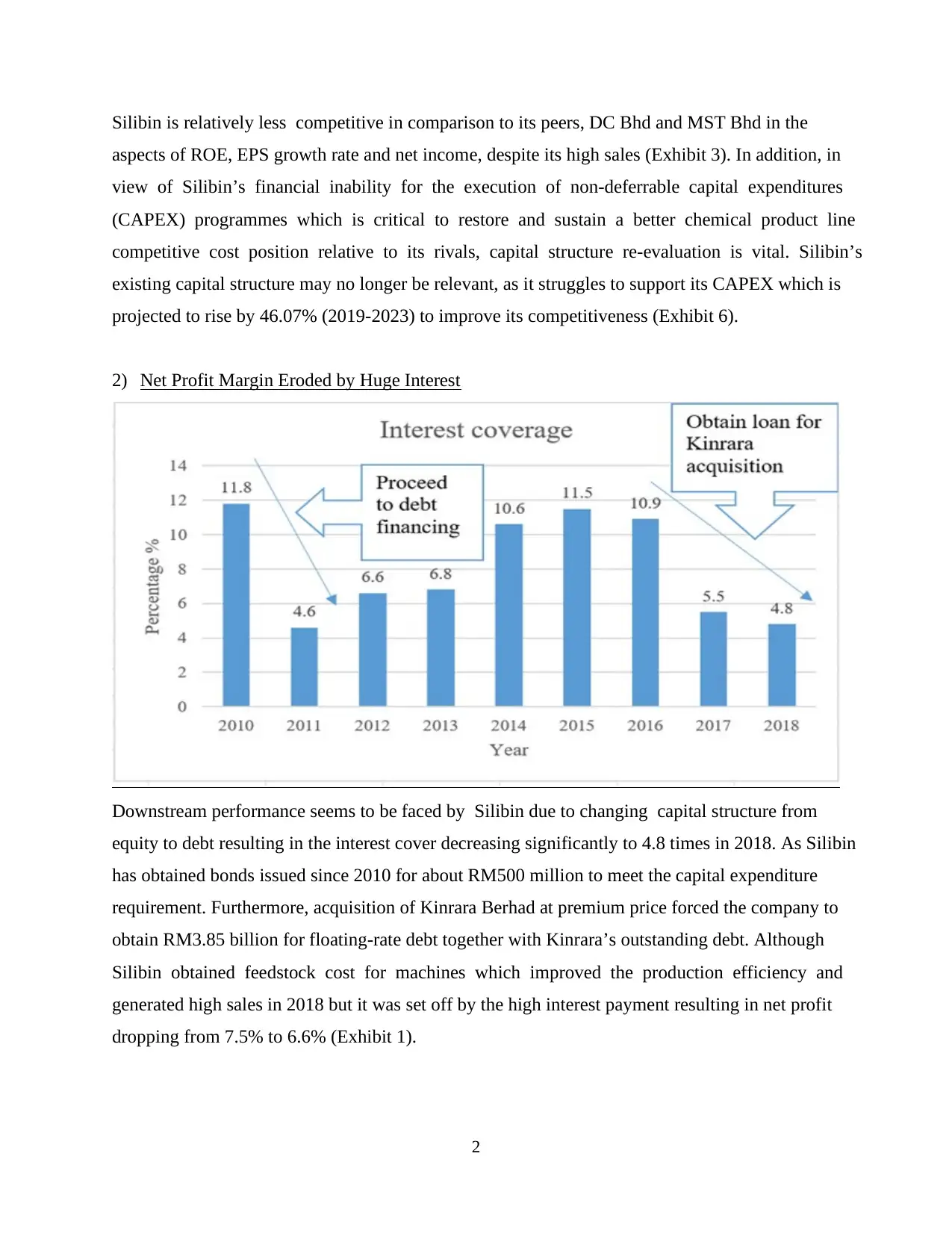

2) Net Profit Margin Eroded by Huge Interest

Downstream performance seems to be faced by Silibin due to changing capital structure from

equity to debt resulting in the interest cover decreasing significantly to 4.8 times in 2018. As Silibin

has obtained bonds issued since 2010 for about RM500 million to meet the capital expenditure

requirement. Furthermore, acquisition of Kinrara Berhad at premium price forced the company to

obtain RM3.85 billion for floating-rate debt together with Kinrara’s outstanding debt. Although

Silibin obtained feedstock cost for machines which improved the production efficiency and

generated high sales in 2018 but it was set off by the high interest payment resulting in net profit

dropping from 7.5% to 6.6% (Exhibit 1).

Silibin is relatively less competitive in comparison to its peers, DC Bhd and MST Bhd in the

aspects of ROE, EPS growth rate and net income, despite its high sales (Exhibit 3). In addition, in

view of Silibin’s financial inability for the execution of non-deferrable capital expenditures

(CAPEX) programmes which is critical to restore and sustain a better chemical product line

competitive cost position relative to its rivals, capital structure re-evaluation is vital. Silibin’s

existing capital structure may no longer be relevant, as it struggles to support its CAPEX which is

projected to rise by 46.07% (2019-2023) to improve its competitiveness (Exhibit 6).

2) Net Profit Margin Eroded by Huge Interest

Downstream performance seems to be faced by Silibin due to changing capital structure from

equity to debt resulting in the interest cover decreasing significantly to 4.8 times in 2018. As Silibin

has obtained bonds issued since 2010 for about RM500 million to meet the capital expenditure

requirement. Furthermore, acquisition of Kinrara Berhad at premium price forced the company to

obtain RM3.85 billion for floating-rate debt together with Kinrara’s outstanding debt. Although

Silibin obtained feedstock cost for machines which improved the production efficiency and

generated high sales in 2018 but it was set off by the high interest payment resulting in net profit

dropping from 7.5% to 6.6% (Exhibit 1).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

3) Post-Inherent Detrimental Effect of Kinrara Acquisition

Merger with potentially overvalued Kinrara at a 77% premium price may not be a wise decision

as it has adversely impacted Silibin’s financial performance. It pressured Silibin’s stock price,

indicating a negative stock market response as stakeholders in the market showed a pessimistic

view on the merger. As of the end of 2018, its stock price (RM37.19) has yet to recover from the

market's negative reaction (Exhibit 1). Additionally, the merger has significantly impacted its

profit margin, interest coverage and ROE negatively. Besides, Silibin’s bond rating was

downgraded to AA, which was attributed to the substantial debt financing for the merger.

4) Financing Needs Arises from Business Condition

The change within the chemical industry from 2001 to 2006, particularly supply growth

outstripped demand growth, results in internally generated funds no longer enough for finance

needs. It is further proved by cut off of dividend and working capital in 2010 and 2011 was

insufficient to meet financing requirements. The trend of decreasing net margin and ROCE

continue until 2018 demand for external finance.

Externally, oil price fluctuation has eroded Silibin net profit margin. At 2009-year end, the rapid

increase of oil price resulted in feedstock cost shot up, oil shortage and disruption of production.

3) Post-Inherent Detrimental Effect of Kinrara Acquisition

Merger with potentially overvalued Kinrara at a 77% premium price may not be a wise decision

as it has adversely impacted Silibin’s financial performance. It pressured Silibin’s stock price,

indicating a negative stock market response as stakeholders in the market showed a pessimistic

view on the merger. As of the end of 2018, its stock price (RM37.19) has yet to recover from the

market's negative reaction (Exhibit 1). Additionally, the merger has significantly impacted its

profit margin, interest coverage and ROE negatively. Besides, Silibin’s bond rating was

downgraded to AA, which was attributed to the substantial debt financing for the merger.

4) Financing Needs Arises from Business Condition

The change within the chemical industry from 2001 to 2006, particularly supply growth

outstripped demand growth, results in internally generated funds no longer enough for finance

needs. It is further proved by cut off of dividend and working capital in 2010 and 2011 was

insufficient to meet financing requirements. The trend of decreasing net margin and ROCE

continue until 2018 demand for external finance.

Externally, oil price fluctuation has eroded Silibin net profit margin. At 2009-year end, the rapid

increase of oil price resulted in feedstock cost shot up, oil shortage and disruption of production.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

Consequently Silibin net income fell by 31% in 2010. The decline in oil price at 2018-year end

again hampered Kinrara oil price.

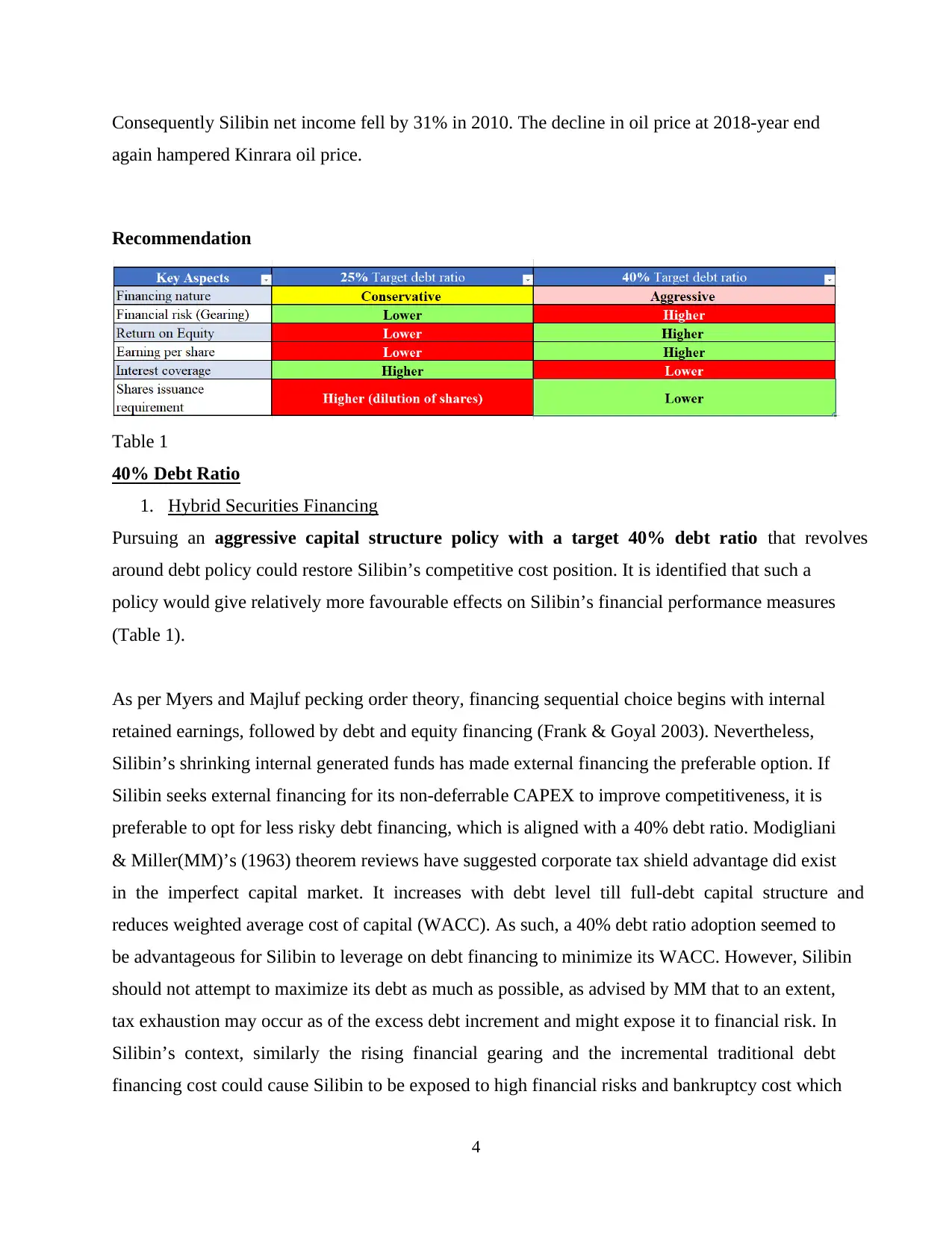

Recommendation

Table 1

40% Debt Ratio

1. Hybrid Securities Financing

Pursuing an aggressive capital structure policy with a target 40% debt ratio that revolves

around debt policy could restore Silibin’s competitive cost position. It is identified that such a

policy would give relatively more favourable effects on Silibin’s financial performance measures

(Table 1).

As per Myers and Majluf pecking order theory, financing sequential choice begins with internal

retained earnings, followed by debt and equity financing (Frank & Goyal 2003). Nevertheless,

Silibin’s shrinking internal generated funds has made external financing the preferable option. If

Silibin seeks external financing for its non-deferrable CAPEX to improve competitiveness, it is

preferable to opt for less risky debt financing, which is aligned with a 40% debt ratio. Modigliani

& Miller(MM)’s (1963) theorem reviews have suggested corporate tax shield advantage did exist

in the imperfect capital market. It increases with debt level till full-debt capital structure and

reduces weighted average cost of capital (WACC). As such, a 40% debt ratio adoption seemed to

be advantageous for Silibin to leverage on debt financing to minimize its WACC. However, Silibin

should not attempt to maximize its debt as much as possible, as advised by MM that to an extent,

tax exhaustion may occur as of the excess debt increment and might expose it to financial risk. In

Silibin’s context, similarly the rising financial gearing and the incremental traditional debt

financing cost could cause Silibin to be exposed to high financial risks and bankruptcy cost which

Consequently Silibin net income fell by 31% in 2010. The decline in oil price at 2018-year end

again hampered Kinrara oil price.

Recommendation

Table 1

40% Debt Ratio

1. Hybrid Securities Financing

Pursuing an aggressive capital structure policy with a target 40% debt ratio that revolves

around debt policy could restore Silibin’s competitive cost position. It is identified that such a

policy would give relatively more favourable effects on Silibin’s financial performance measures

(Table 1).

As per Myers and Majluf pecking order theory, financing sequential choice begins with internal

retained earnings, followed by debt and equity financing (Frank & Goyal 2003). Nevertheless,

Silibin’s shrinking internal generated funds has made external financing the preferable option. If

Silibin seeks external financing for its non-deferrable CAPEX to improve competitiveness, it is

preferable to opt for less risky debt financing, which is aligned with a 40% debt ratio. Modigliani

& Miller(MM)’s (1963) theorem reviews have suggested corporate tax shield advantage did exist

in the imperfect capital market. It increases with debt level till full-debt capital structure and

reduces weighted average cost of capital (WACC). As such, a 40% debt ratio adoption seemed to

be advantageous for Silibin to leverage on debt financing to minimize its WACC. However, Silibin

should not attempt to maximize its debt as much as possible, as advised by MM that to an extent,

tax exhaustion may occur as of the excess debt increment and might expose it to financial risk. In

Silibin’s context, similarly the rising financial gearing and the incremental traditional debt

financing cost could cause Silibin to be exposed to high financial risks and bankruptcy cost which

5

might offset the tax advantage.

In view of current gearing, convertible bonds may be an alternative option for Silibin if it pursues

a 40% debt ratio to finance CAPEX despite MM advocating on debt maximization. Mayer’s

financing theory suggested that convertible bonds could induce capital structure rebalancing

reactions where the leverage drops on conversion (Rastad 2016). It would free up Silibin’s debt

capacity upon conversion. Its hybrid attributes enable Silibin to leverage on lower financing cost

advantage and rebalance the debt-to-equity ratio upon potential conversion to avoid excessively

high gearing. Thus, Silibin could improve its competitive cost position to boost its performance

via efficient use of debt financing funds in expanding its chemical products.

25% Debt Ratio

2. Equity Finance Strategy

might offset the tax advantage.

In view of current gearing, convertible bonds may be an alternative option for Silibin if it pursues

a 40% debt ratio to finance CAPEX despite MM advocating on debt maximization. Mayer’s

financing theory suggested that convertible bonds could induce capital structure rebalancing

reactions where the leverage drops on conversion (Rastad 2016). It would free up Silibin’s debt

capacity upon conversion. Its hybrid attributes enable Silibin to leverage on lower financing cost

advantage and rebalance the debt-to-equity ratio upon potential conversion to avoid excessively

high gearing. Thus, Silibin could improve its competitive cost position to boost its performance

via efficient use of debt financing funds in expanding its chemical products.

25% Debt Ratio

2. Equity Finance Strategy

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

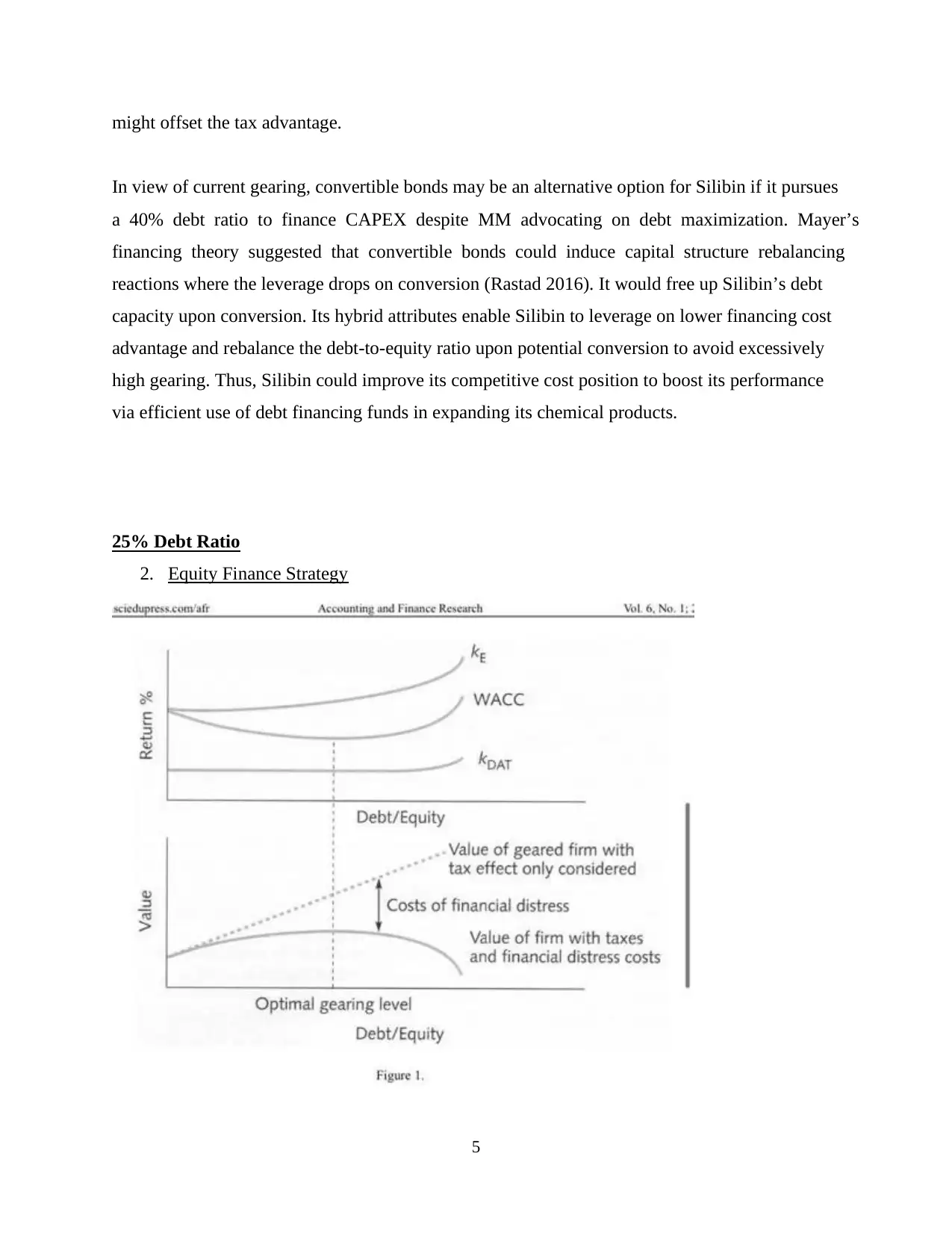

According to trade-off theory, the success of debt financing lies in balance between gain from tax

shield and loss from bankruptcy cost (Abeywardhana 2017), which would maximise firm values.

Silibin’s debt ratio had increased to 36%, led to a high gearing ratio and low interest

coverage(Exhibit 2). Such indication of increasingly high reliance on debt financing might lead to

failure to meet interest payment requirements. Consequently the loss from bankruptcy might

exceed the benefit from the tax shield.

As the industry’s cost of debts increased significantly starting 2014(Exhibit 7) due to bond issues,

with the decline of share prices for Silibin if they continued to obtain debt finance it caused the

cost of debts increased as they exceeded optimal gearing level that the company can accept. This

might lead shareholders to demand for high return to cover up the financial risk resulting in rising

cost of capital. This will cause the rise of interest payment and lower the net profit. A drop in net

profit will also result in share prices also dropping. This will affect shareholders’ wealth and they

might lose trust for the company as Silibin is yet to recover the share prices being dropped

continuously.

Therefore, Silibin should reduce the debt ratio to 25% by increasing equity finance. For instance,

the company can issue new shares to the public. Although current performance for Silibin is not

in good condition but the marketability for the share is still attractive as they are renowned as the

largest chemical manufacturer and they remained technological leader in the industry. Such action

will reduce the debt portion and directly reduce interest cost. Consequently, net profit will increase

resulting in share prices will recover back to their current situation in order to regain shareholders’

confidence. Not only that, a debt ratio decrease will increase interest coverage in future(Exhibit 8)

and the bond rating of the company will tend to recover to AAA.

Other

3. Diversification

In view of Silibin profitability is eroded by the industry's systematic risk, the diversification

strategy is recommended. Modern Portfolio Theory advocates investors to balance out investment

in several portfolios rather than depending on merely a single portfolio to reduce risk by spreading

it among portfolios. Applying the theory in the Silibin case, diversification may lead to spreading

the industry risk across several businesses to increase profitability (Oladimeji & Udosen 2019).

According to trade-off theory, the success of debt financing lies in balance between gain from tax

shield and loss from bankruptcy cost (Abeywardhana 2017), which would maximise firm values.

Silibin’s debt ratio had increased to 36%, led to a high gearing ratio and low interest

coverage(Exhibit 2). Such indication of increasingly high reliance on debt financing might lead to

failure to meet interest payment requirements. Consequently the loss from bankruptcy might

exceed the benefit from the tax shield.

As the industry’s cost of debts increased significantly starting 2014(Exhibit 7) due to bond issues,

with the decline of share prices for Silibin if they continued to obtain debt finance it caused the

cost of debts increased as they exceeded optimal gearing level that the company can accept. This

might lead shareholders to demand for high return to cover up the financial risk resulting in rising

cost of capital. This will cause the rise of interest payment and lower the net profit. A drop in net

profit will also result in share prices also dropping. This will affect shareholders’ wealth and they

might lose trust for the company as Silibin is yet to recover the share prices being dropped

continuously.

Therefore, Silibin should reduce the debt ratio to 25% by increasing equity finance. For instance,

the company can issue new shares to the public. Although current performance for Silibin is not

in good condition but the marketability for the share is still attractive as they are renowned as the

largest chemical manufacturer and they remained technological leader in the industry. Such action

will reduce the debt portion and directly reduce interest cost. Consequently, net profit will increase

resulting in share prices will recover back to their current situation in order to regain shareholders’

confidence. Not only that, a debt ratio decrease will increase interest coverage in future(Exhibit 8)

and the bond rating of the company will tend to recover to AAA.

Other

3. Diversification

In view of Silibin profitability is eroded by the industry's systematic risk, the diversification

strategy is recommended. Modern Portfolio Theory advocates investors to balance out investment

in several portfolios rather than depending on merely a single portfolio to reduce risk by spreading

it among portfolios. Applying the theory in the Silibin case, diversification may lead to spreading

the industry risk across several businesses to increase profitability (Oladimeji & Udosen 2019).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

The related diversification strategy of acquiring Kinrara may provide an opportunity for creating

synergy benefits (Khawaja Khalid Mehmood & Haim Hilman 2015). Nonetheless, the

management must strive to create synergy among Silibin and Kinrara in order to reap the benefits

of diversification instead of realizing the assets of Kinrara.

4. Hedging

According to Zhao, Meng, Zhang and Li (2019), hedging can be used as a means in the energy

futures market to reduce the loss brought by energy price volatility. Future contracts allow Silibin

to procure the commodity (oil) at a predetermined price within a specific timeframe. Consequently,

it allows Silibin to lock in profits and cost and reduce the impact brought by volatile oil price (Zhao

et al. 2019). The hedge can be extended to Kinrara which is involved in the oil industry, so that its

sales can be guaranteed and forecasted reliably.

Conclusion

We recommend that Silibin go for 25% debt ratio, on the basis that it remains financial flexibility

while solving numerous current issues. Although it has a lower rate of return compared to 40%

debt ratio, it has better interest coverage which we deem to be more conservative in its volatile

industry. Silibin also might be heading back towards AAA bond rating with the debt policy.

The related diversification strategy of acquiring Kinrara may provide an opportunity for creating

synergy benefits (Khawaja Khalid Mehmood & Haim Hilman 2015). Nonetheless, the

management must strive to create synergy among Silibin and Kinrara in order to reap the benefits

of diversification instead of realizing the assets of Kinrara.

4. Hedging

According to Zhao, Meng, Zhang and Li (2019), hedging can be used as a means in the energy

futures market to reduce the loss brought by energy price volatility. Future contracts allow Silibin

to procure the commodity (oil) at a predetermined price within a specific timeframe. Consequently,

it allows Silibin to lock in profits and cost and reduce the impact brought by volatile oil price (Zhao

et al. 2019). The hedge can be extended to Kinrara which is involved in the oil industry, so that its

sales can be guaranteed and forecasted reliably.

Conclusion

We recommend that Silibin go for 25% debt ratio, on the basis that it remains financial flexibility

while solving numerous current issues. Although it has a lower rate of return compared to 40%

debt ratio, it has better interest coverage which we deem to be more conservative in its volatile

industry. Silibin also might be heading back towards AAA bond rating with the debt policy.

8

Part 2

Hoong Jia Ming (550 words)

I agree with 25% debt ratio capital structure policy recommendation. Low-debt policy is more

preferable in view of the followings:

Equity Financing Practicality

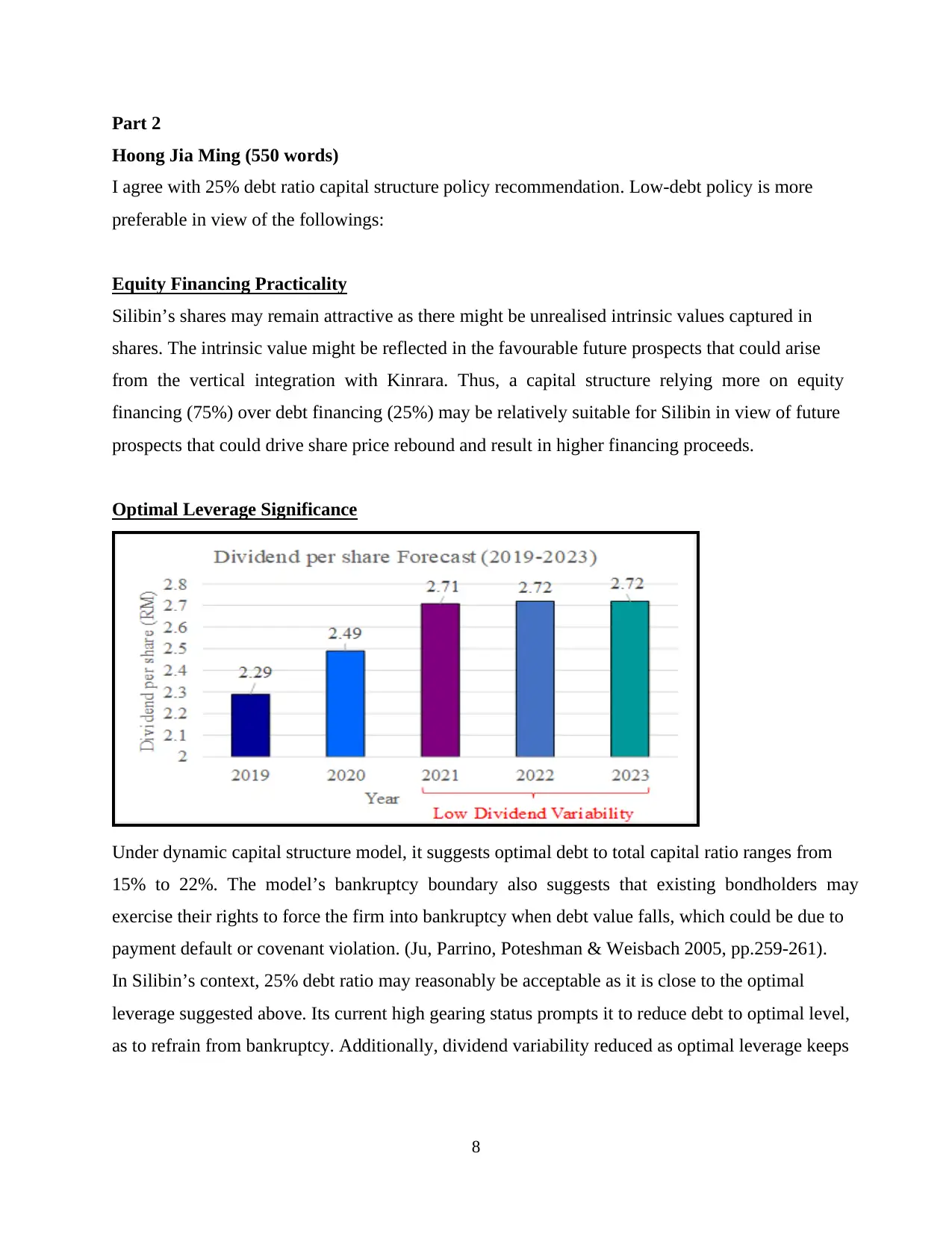

Silibin’s shares may remain attractive as there might be unrealised intrinsic values captured in

shares. The intrinsic value might be reflected in the favourable future prospects that could arise

from the vertical integration with Kinrara. Thus, a capital structure relying more on equity

financing (75%) over debt financing (25%) may be relatively suitable for Silibin in view of future

prospects that could drive share price rebound and result in higher financing proceeds.

Optimal Leverage Significance

Under dynamic capital structure model, it suggests optimal debt to total capital ratio ranges from

15% to 22%. The model’s bankruptcy boundary also suggests that existing bondholders may

exercise their rights to force the firm into bankruptcy when debt value falls, which could be due to

payment default or covenant violation. (Ju, Parrino, Poteshman & Weisbach 2005, pp.259-261).

In Silibin’s context, 25% debt ratio may reasonably be acceptable as it is close to the optimal

leverage suggested above. Its current high gearing status prompts it to reduce debt to optimal level,

as to refrain from bankruptcy. Additionally, dividend variability reduced as optimal leverage keeps

Part 2

Hoong Jia Ming (550 words)

I agree with 25% debt ratio capital structure policy recommendation. Low-debt policy is more

preferable in view of the followings:

Equity Financing Practicality

Silibin’s shares may remain attractive as there might be unrealised intrinsic values captured in

shares. The intrinsic value might be reflected in the favourable future prospects that could arise

from the vertical integration with Kinrara. Thus, a capital structure relying more on equity

financing (75%) over debt financing (25%) may be relatively suitable for Silibin in view of future

prospects that could drive share price rebound and result in higher financing proceeds.

Optimal Leverage Significance

Under dynamic capital structure model, it suggests optimal debt to total capital ratio ranges from

15% to 22%. The model’s bankruptcy boundary also suggests that existing bondholders may

exercise their rights to force the firm into bankruptcy when debt value falls, which could be due to

payment default or covenant violation. (Ju, Parrino, Poteshman & Weisbach 2005, pp.259-261).

In Silibin’s context, 25% debt ratio may reasonably be acceptable as it is close to the optimal

leverage suggested above. Its current high gearing status prompts it to reduce debt to optimal level,

as to refrain from bankruptcy. Additionally, dividend variability reduced as optimal leverage keeps

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

Silibin at lower financial risk that it would less likely fall into financial constraint that it cut

dividend payable to shareholders as to prioritize interest payment (exhibit 8).

Bond-Rating Restoration

As 25% debt ratio could restore bond rating to AAA, balancing 25% debt ratio would allow Silibin

to reap lower debt financing cost benefit while mitigating financial and bankruptcy risk. Low risk

status might stimulate positive market responses with strengthening confidence on its stock and

bond. It would also enhance marketability of Silibin's future debt financing as its high

creditworthiness could be an attraction to potential investors. Its high bond rating may be a

reflection of its creditworthiness or as a reference for other creditors to provide credit facilities or

borrowing with minimum or no restrictive covenants.

Financial Flexibility

Silibin would be at a better liquidity position as dividend is discretionary which differed from

committed interest payment. Financial flexibility enables it to be more adaptable to future

unprecedented financial crises which require cash flow and reserves to survive. Silibin could plan

its cash flow forecast to suit its needs, which it may defer interim dividend to as final dividend.

Nevertheless, Silibin should consider shareholding dilutive effects when pursuing the 25% debt

ratio policy that dominated in equity as overdependence on equity financing could lead to negative

responses from existing shareholders, which could be a hindrance for fundraising.

Diversification and Hedging

Diversification and hedging strategies are viable in reducing earning volatility and foreign

exchange risk arose from fluctuating crude oil, which aligned with the 25% debt ratio policy to

minimise Silibin’s overall business and financial risk.

Conclusion

Overall, analysis report outlined issues of declined competitiveness, eroded profit margin, Kinrara

acquisition detrimental effects and uncertain business environment, along with corresponding

solutions associated with Silibin's capital structure policy restructuring. The proposed

Silibin at lower financial risk that it would less likely fall into financial constraint that it cut

dividend payable to shareholders as to prioritize interest payment (exhibit 8).

Bond-Rating Restoration

As 25% debt ratio could restore bond rating to AAA, balancing 25% debt ratio would allow Silibin

to reap lower debt financing cost benefit while mitigating financial and bankruptcy risk. Low risk

status might stimulate positive market responses with strengthening confidence on its stock and

bond. It would also enhance marketability of Silibin's future debt financing as its high

creditworthiness could be an attraction to potential investors. Its high bond rating may be a

reflection of its creditworthiness or as a reference for other creditors to provide credit facilities or

borrowing with minimum or no restrictive covenants.

Financial Flexibility

Silibin would be at a better liquidity position as dividend is discretionary which differed from

committed interest payment. Financial flexibility enables it to be more adaptable to future

unprecedented financial crises which require cash flow and reserves to survive. Silibin could plan

its cash flow forecast to suit its needs, which it may defer interim dividend to as final dividend.

Nevertheless, Silibin should consider shareholding dilutive effects when pursuing the 25% debt

ratio policy that dominated in equity as overdependence on equity financing could lead to negative

responses from existing shareholders, which could be a hindrance for fundraising.

Diversification and Hedging

Diversification and hedging strategies are viable in reducing earning volatility and foreign

exchange risk arose from fluctuating crude oil, which aligned with the 25% debt ratio policy to

minimise Silibin’s overall business and financial risk.

Conclusion

Overall, analysis report outlined issues of declined competitiveness, eroded profit margin, Kinrara

acquisition detrimental effects and uncertain business environment, along with corresponding

solutions associated with Silibin's capital structure policy restructuring. The proposed

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

recommendations revolving around 25% debt ratio are justifiable to solve issues identified by

considering its high practicality, financial benefits and optimal leverage. No matter how, low-debt

policy also associates with its downsides of lower earnings as low risk comes with low return

under risk-return tradeoff theory (Campbell & Viceira 2005).

Low Chee Seng (494 words)

Modigliani and Miller (MM) Proposition 2

The above proposition highlights the higher the debt ratio, the higher the benefits arise from the

interest tax shield. Ideally, a company can maximise its value through increase of interest tax

shield, by holding the assumptions that cash inflow and weighted average cost of capital constant.

The assumption is portrayed in exhibit 8, the return on total capital remains the same regardless

which option to go after.

Thus, Silibin is suggested, with reference to MM theory, to pursue the 40% debt ratio or even

higher in order to reap the benefits of tax shield. According to exhibit 8, the 40% debt indeed yields

higher return of equity compared to 25% debt, for a maximum of 1.2%. In terms of earning per

shares and dividend per share, the projection of 40% yields higher figure compared to 25% debt

too, as a result of enjoying the benefits of interest tax shield.

Risk and return from the proposition

However, according to general assumption of financial leverage, the higher the risk, the higher the

return and vice versa (Daniel, Anne & Le 2020). In other words, the exceed of earning per shares

brought by 40% debt over 25% debt is accompanied along with higher risk compared to 25% debt.

This can be observed through the comparison of interest coverage. 40% results in a range of 3.86-

3.95 times while 25% results in increase from 3.91 to 6.17 times. The higher return from 40% debt

is being compensated by its ability to repay the interest using generated earnings. Moreover, with

conservative projection of lower PBIT of 20% in 2023 years, 25% still remain about 5 times

interest coverage while 40% reduce to around 3 times. It shows Silibin’s ability to meet interest

obligation would be in doubt when company not performing well. While the return from 40% debt

ratio seems appearing, we shall not neglect the risk accompanied.

recommendations revolving around 25% debt ratio are justifiable to solve issues identified by

considering its high practicality, financial benefits and optimal leverage. No matter how, low-debt

policy also associates with its downsides of lower earnings as low risk comes with low return

under risk-return tradeoff theory (Campbell & Viceira 2005).

Low Chee Seng (494 words)

Modigliani and Miller (MM) Proposition 2

The above proposition highlights the higher the debt ratio, the higher the benefits arise from the

interest tax shield. Ideally, a company can maximise its value through increase of interest tax

shield, by holding the assumptions that cash inflow and weighted average cost of capital constant.

The assumption is portrayed in exhibit 8, the return on total capital remains the same regardless

which option to go after.

Thus, Silibin is suggested, with reference to MM theory, to pursue the 40% debt ratio or even

higher in order to reap the benefits of tax shield. According to exhibit 8, the 40% debt indeed yields

higher return of equity compared to 25% debt, for a maximum of 1.2%. In terms of earning per

shares and dividend per share, the projection of 40% yields higher figure compared to 25% debt

too, as a result of enjoying the benefits of interest tax shield.

Risk and return from the proposition

However, according to general assumption of financial leverage, the higher the risk, the higher the

return and vice versa (Daniel, Anne & Le 2020). In other words, the exceed of earning per shares

brought by 40% debt over 25% debt is accompanied along with higher risk compared to 25% debt.

This can be observed through the comparison of interest coverage. 40% results in a range of 3.86-

3.95 times while 25% results in increase from 3.91 to 6.17 times. The higher return from 40% debt

is being compensated by its ability to repay the interest using generated earnings. Moreover, with

conservative projection of lower PBIT of 20% in 2023 years, 25% still remain about 5 times

interest coverage while 40% reduce to around 3 times. It shows Silibin’s ability to meet interest

obligation would be in doubt when company not performing well. While the return from 40% debt

ratio seems appearing, we shall not neglect the risk accompanied.

11

Consideration from EBIT point of view

The current EBIT is having an assumption that annual sales growth rate amounts to 10% based on

exhibit 6. Nonetheless, exhibit 3 shows 10 years compound annual EPS growth rate is merely

2.9%. The volatile industry condition, especially oil price fluctuation cast further doubt on the

annual growth rate assumptions.

In addition, from macroeconomic point of view, Brou E. Aka (2006) pointed out that banking

crises are likely to surface every 10 years or so, owing to “financial stability fatigue” or “time

wearing effect”. The cycle holds on even if the economic system has been stable until the year

before the crises. It worth the management attention that it has been about 10 years ever since

2007-2008 financial crisis.

Personal Conclusion

MM have suggested that firms maintain ‘reserve borrowing capacity’ (Abo Hamza 1977). In my

opinion, indeed the cash flow projection has projected a better return applying 40% debt ratio,

however conservative debt policy of 25% might be more appropriate to Silibin in view of current

industry and economic conditions.

Teo Kok Hao (539 words)

In my opinion, I agree with the 25% capital structure policy. Below explained the reason for

preferable low debt ratio:

Business Risk

Silibin seems to have incurred high business risk and financial risk. For business risk, it is due to

the nature of its volatile business performance(Exhibit 5). For instance, downturn of the chemical

industry and oil prices fluctuation caused a drop in net profit margin significantly. Hence, financial

difficulties faced by Silibin lead to change in the capital structure to debt financing. However, such

a method did not improve the company’s performance and even become worse especially after the

acquisition of Kinrara in 2017. They do utilize the benefit from obtaining loans as it will provide

cash for acquisition without using internally generated funds and not affect the daily operational

cost. Although after acquisition it increases the sales of the company but it was set off by the high-

Consideration from EBIT point of view

The current EBIT is having an assumption that annual sales growth rate amounts to 10% based on

exhibit 6. Nonetheless, exhibit 3 shows 10 years compound annual EPS growth rate is merely

2.9%. The volatile industry condition, especially oil price fluctuation cast further doubt on the

annual growth rate assumptions.

In addition, from macroeconomic point of view, Brou E. Aka (2006) pointed out that banking

crises are likely to surface every 10 years or so, owing to “financial stability fatigue” or “time

wearing effect”. The cycle holds on even if the economic system has been stable until the year

before the crises. It worth the management attention that it has been about 10 years ever since

2007-2008 financial crisis.

Personal Conclusion

MM have suggested that firms maintain ‘reserve borrowing capacity’ (Abo Hamza 1977). In my

opinion, indeed the cash flow projection has projected a better return applying 40% debt ratio,

however conservative debt policy of 25% might be more appropriate to Silibin in view of current

industry and economic conditions.

Teo Kok Hao (539 words)

In my opinion, I agree with the 25% capital structure policy. Below explained the reason for

preferable low debt ratio:

Business Risk

Silibin seems to have incurred high business risk and financial risk. For business risk, it is due to

the nature of its volatile business performance(Exhibit 5). For instance, downturn of the chemical

industry and oil prices fluctuation caused a drop in net profit margin significantly. Hence, financial

difficulties faced by Silibin lead to change in the capital structure to debt financing. However, such

a method did not improve the company’s performance and even become worse especially after the

acquisition of Kinrara in 2017. They do utilize the benefit from obtaining loans as it will provide

cash for acquisition without using internally generated funds and not affect the daily operational

cost. Although after acquisition it increases the sales of the company but it was set off by the high-

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 39

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.