Tesco & Sainsbury Capital Structure: A Comparative Analysis (2014-18)

VerifiedAdded on 2023/04/21

|12

|2254

|381

Report

AI Summary

This report provides a comprehensive analysis of the capital structure policies of Tesco and Sainsbury Plc. from 2014 to 2018. It critically evaluates their financing decisions in light of established capital structure theories, including the traditional approach, Modigliani-Miller propositions, trade-off theory, and pecking order theory. The analysis incorporates financial data from the companies' annual reports, examining their debt-to-equity ratios and overall capital structure compositions. The report concludes by assessing the extent to which these theories explain the observed financing decisions, highlighting the importance of balancing debt and equity based on business type and associated risks. Desklib provides access to similar past papers and solved assignments for students.

Running head: ADVANCED FINANCIAL DECISION

Advanced Financial Decision

Name of the Student:

Name of the University:

Author’s Note:

Advanced Financial Decision

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ADVANCED FINANCIAL DECISION

Table of Contents

Introduction......................................................................................................................................2

Overview of Capital Structure.........................................................................................................2

Theories of Capital Structure.......................................................................................................2

Empirical Evidence......................................................................................................................6

Analysis of Capital Structure...........................................................................................................7

Conclusion.......................................................................................................................................8

References........................................................................................................................................9

Appendix........................................................................................................................................11

Table of Contents

Introduction......................................................................................................................................2

Overview of Capital Structure.........................................................................................................2

Theories of Capital Structure.......................................................................................................2

Empirical Evidence......................................................................................................................6

Analysis of Capital Structure...........................................................................................................7

Conclusion.......................................................................................................................................8

References........................................................................................................................................9

Appendix........................................................................................................................................11

2ADVANCED FINANCIAL DECISION

Introduction

Capital Structure shows the financing structure of a company. It shows how firms on an

overall basis finances the operations and growth of firms from various available sources of funds

for the company. In the context of corporate finance, the capital structure of the companies

shows the various ways by combining different available capital sources like equity, debt and

hybrid securities for the company. Capital Structure is important for financing decision, as it is

important for the company to have an optimal debt and equity mix in the operations and

financing activities of the company. An optimal mix of debt and equity will be necessary for the

company for financing the assets and projects of the company. The report covers the various

aspect of the capital structure maintained by TESCO Company and Sainsbury’s Company.

Overview of Capital Structure

Theories of Capital Structure

The capital structure of the companies plays an important role in the overall financing

decisions of the company. The five important theory that significantly explains the long term

capital sources of financing are:

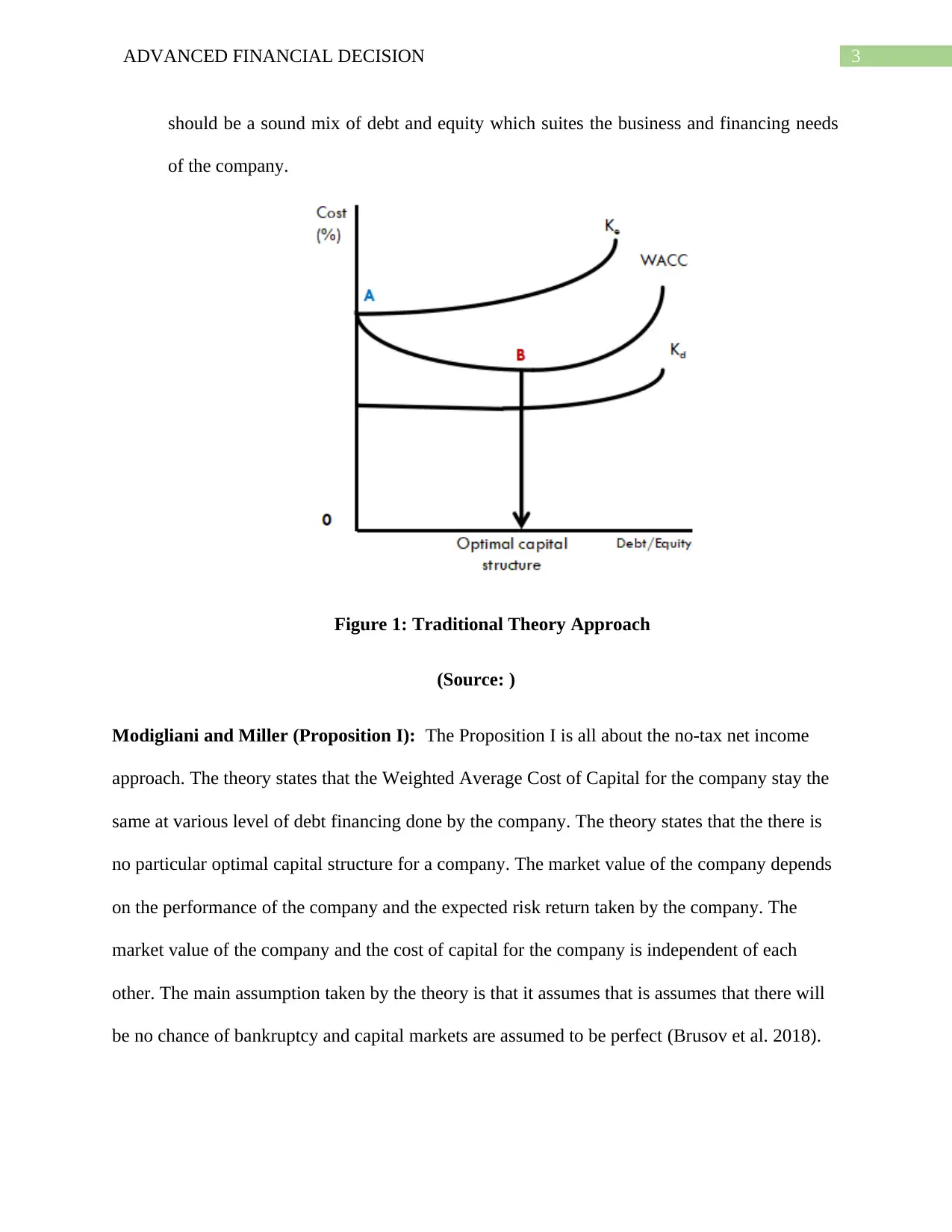

Traditional Approach: The traditional theory approach shows that there is an optimal

capital structure in the firm where the companies and firms have an optimal amount of

debt in contrast to the equity level of the company. The traditional theory approach

focuses on the minimum cost of capital approach to attain highest amount of market

value of the firm. The traditional approach assumes that no taxes exists at both the

personal and corporate level (Bhattacharyya and Morrill 2015). The key proposition

made by the traditional theory is that in order to have a minimum cost of capital there

Introduction

Capital Structure shows the financing structure of a company. It shows how firms on an

overall basis finances the operations and growth of firms from various available sources of funds

for the company. In the context of corporate finance, the capital structure of the companies

shows the various ways by combining different available capital sources like equity, debt and

hybrid securities for the company. Capital Structure is important for financing decision, as it is

important for the company to have an optimal debt and equity mix in the operations and

financing activities of the company. An optimal mix of debt and equity will be necessary for the

company for financing the assets and projects of the company. The report covers the various

aspect of the capital structure maintained by TESCO Company and Sainsbury’s Company.

Overview of Capital Structure

Theories of Capital Structure

The capital structure of the companies plays an important role in the overall financing

decisions of the company. The five important theory that significantly explains the long term

capital sources of financing are:

Traditional Approach: The traditional theory approach shows that there is an optimal

capital structure in the firm where the companies and firms have an optimal amount of

debt in contrast to the equity level of the company. The traditional theory approach

focuses on the minimum cost of capital approach to attain highest amount of market

value of the firm. The traditional approach assumes that no taxes exists at both the

personal and corporate level (Bhattacharyya and Morrill 2015). The key proposition

made by the traditional theory is that in order to have a minimum cost of capital there

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ADVANCED FINANCIAL DECISION

should be a sound mix of debt and equity which suites the business and financing needs

of the company.

Figure 1: Traditional Theory Approach

(Source: )

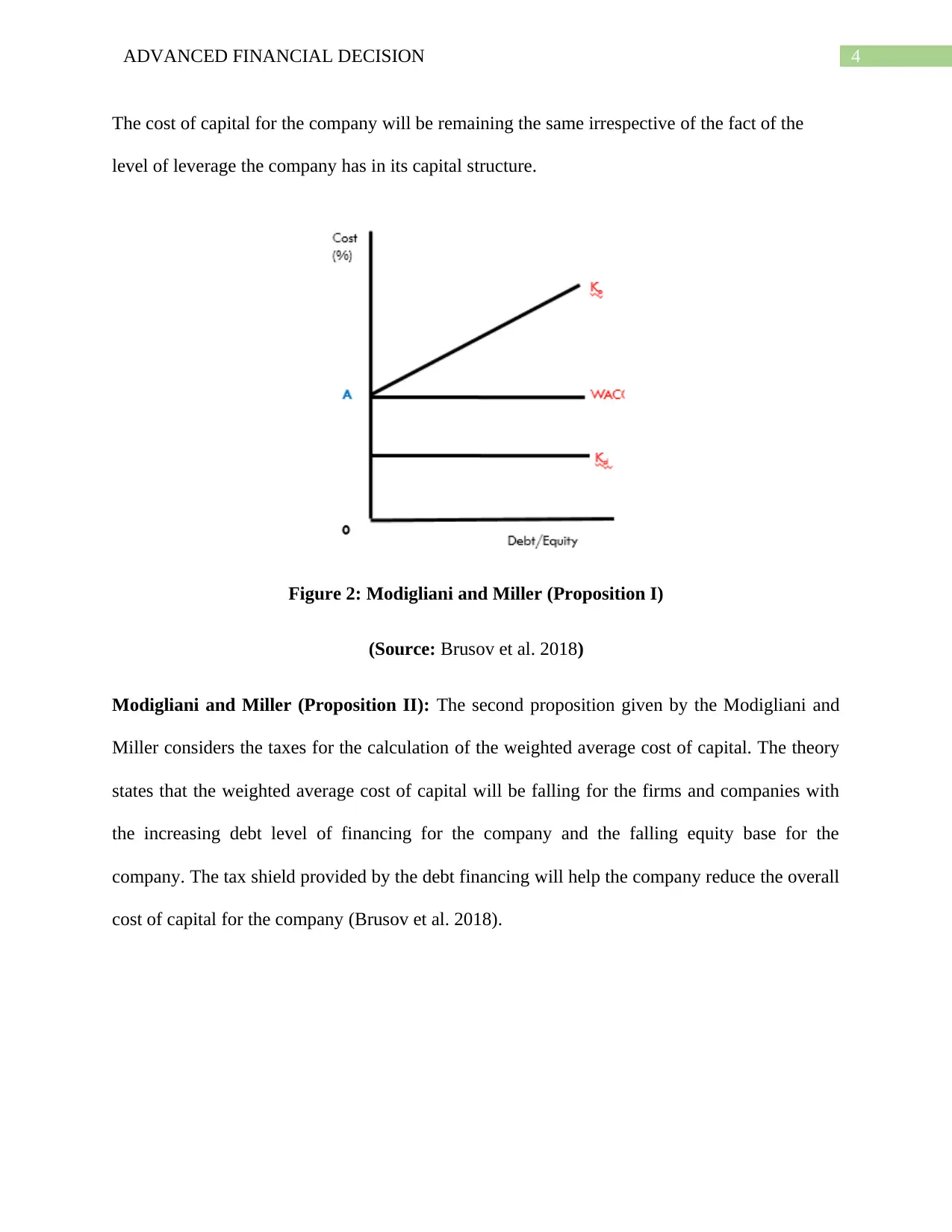

Modigliani and Miller (Proposition I): The Proposition I is all about the no-tax net income

approach. The theory states that the Weighted Average Cost of Capital for the company stay the

same at various level of debt financing done by the company. The theory states that the there is

no particular optimal capital structure for a company. The market value of the company depends

on the performance of the company and the expected risk return taken by the company. The

market value of the company and the cost of capital for the company is independent of each

other. The main assumption taken by the theory is that it assumes that is assumes that there will

be no chance of bankruptcy and capital markets are assumed to be perfect (Brusov et al. 2018).

should be a sound mix of debt and equity which suites the business and financing needs

of the company.

Figure 1: Traditional Theory Approach

(Source: )

Modigliani and Miller (Proposition I): The Proposition I is all about the no-tax net income

approach. The theory states that the Weighted Average Cost of Capital for the company stay the

same at various level of debt financing done by the company. The theory states that the there is

no particular optimal capital structure for a company. The market value of the company depends

on the performance of the company and the expected risk return taken by the company. The

market value of the company and the cost of capital for the company is independent of each

other. The main assumption taken by the theory is that it assumes that is assumes that there will

be no chance of bankruptcy and capital markets are assumed to be perfect (Brusov et al. 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ADVANCED FINANCIAL DECISION

The cost of capital for the company will be remaining the same irrespective of the fact of the

level of leverage the company has in its capital structure.

Figure 2: Modigliani and Miller (Proposition I)

(Source: Brusov et al. 2018)

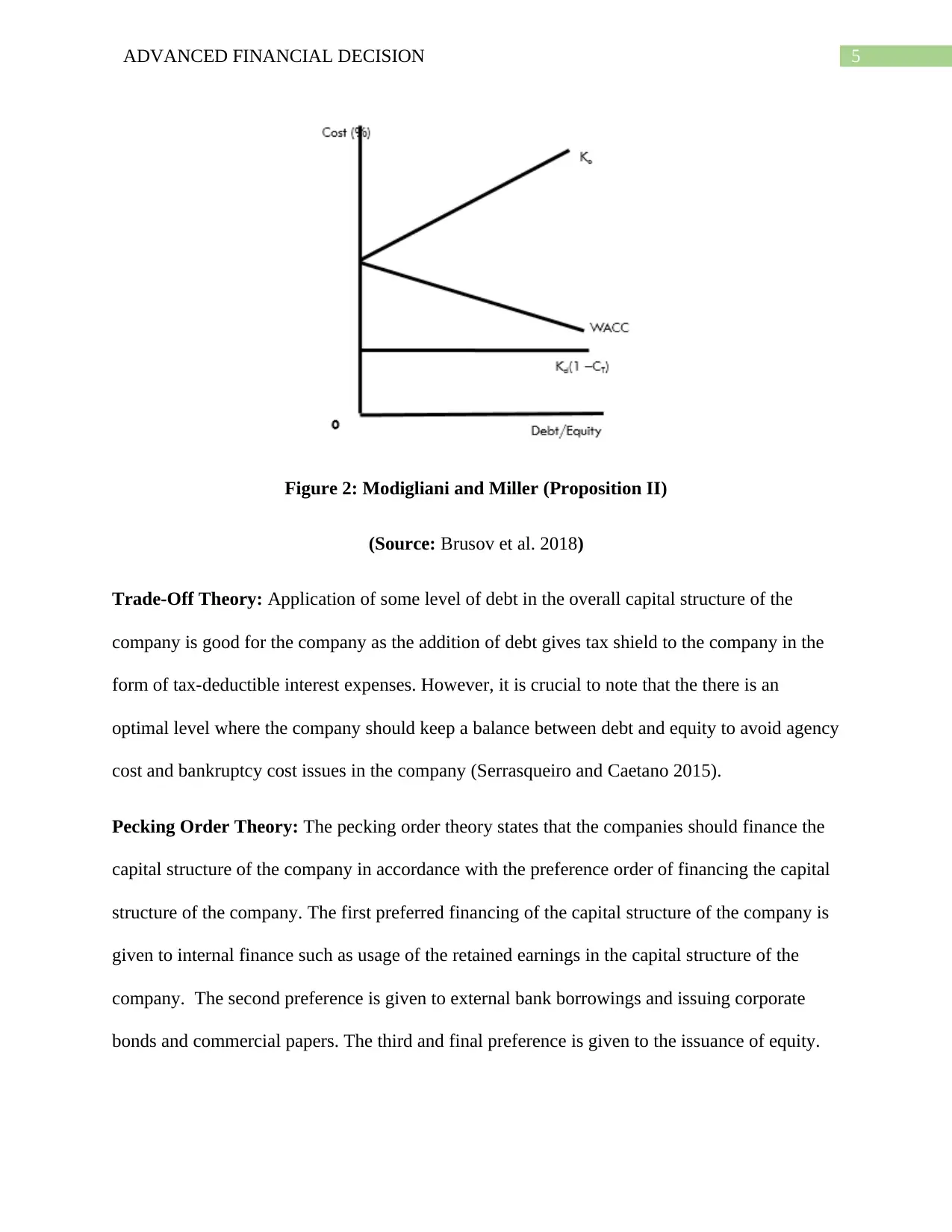

Modigliani and Miller (Proposition II): The second proposition given by the Modigliani and

Miller considers the taxes for the calculation of the weighted average cost of capital. The theory

states that the weighted average cost of capital will be falling for the firms and companies with

the increasing debt level of financing for the company and the falling equity base for the

company. The tax shield provided by the debt financing will help the company reduce the overall

cost of capital for the company (Brusov et al. 2018).

The cost of capital for the company will be remaining the same irrespective of the fact of the

level of leverage the company has in its capital structure.

Figure 2: Modigliani and Miller (Proposition I)

(Source: Brusov et al. 2018)

Modigliani and Miller (Proposition II): The second proposition given by the Modigliani and

Miller considers the taxes for the calculation of the weighted average cost of capital. The theory

states that the weighted average cost of capital will be falling for the firms and companies with

the increasing debt level of financing for the company and the falling equity base for the

company. The tax shield provided by the debt financing will help the company reduce the overall

cost of capital for the company (Brusov et al. 2018).

5ADVANCED FINANCIAL DECISION

Figure 2: Modigliani and Miller (Proposition II)

(Source: Brusov et al. 2018)

Trade-Off Theory: Application of some level of debt in the overall capital structure of the

company is good for the company as the addition of debt gives tax shield to the company in the

form of tax-deductible interest expenses. However, it is crucial to note that the there is an

optimal level where the company should keep a balance between debt and equity to avoid agency

cost and bankruptcy cost issues in the company (Serrasqueiro and Caetano 2015).

Pecking Order Theory: The pecking order theory states that the companies should finance the

capital structure of the company in accordance with the preference order of financing the capital

structure of the company. The first preferred financing of the capital structure of the company is

given to internal finance such as usage of the retained earnings in the capital structure of the

company. The second preference is given to external bank borrowings and issuing corporate

bonds and commercial papers. The third and final preference is given to the issuance of equity.

Figure 2: Modigliani and Miller (Proposition II)

(Source: Brusov et al. 2018)

Trade-Off Theory: Application of some level of debt in the overall capital structure of the

company is good for the company as the addition of debt gives tax shield to the company in the

form of tax-deductible interest expenses. However, it is crucial to note that the there is an

optimal level where the company should keep a balance between debt and equity to avoid agency

cost and bankruptcy cost issues in the company (Serrasqueiro and Caetano 2015).

Pecking Order Theory: The pecking order theory states that the companies should finance the

capital structure of the company in accordance with the preference order of financing the capital

structure of the company. The first preferred financing of the capital structure of the company is

given to internal finance such as usage of the retained earnings in the capital structure of the

company. The second preference is given to external bank borrowings and issuing corporate

bonds and commercial papers. The third and final preference is given to the issuance of equity.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ADVANCED FINANCIAL DECISION

Thus, on an overall basis the theory does not emphasizes on the reduction of cost of capital for

the company rather it shows the preferred financing structures available for the companies.

Empirical Evidence

The traditional approach discussed does not fit into the corporate world as the theory

ignores the tax shield, which is gained to the firm from the taxable interest expenses paid by the

firm. Empirically many authors have reflected in there articles that the theory does not represent

the true and fair view in association with the cost of capital for the company. The Modigliani

Miller Proposition I takes the net income approach where the theory is not used for determine the

optimum cost of capital for the company because of constant weighted average cost of capital for

the company with the changing level of debt and equity in the company (Ardalan 2015).

However, it is crucial to note that companies pay interest on the debt borrowed which, is tax

deductible allowing the companies to have a lower cost of capital for the company. The

Modigliani Miller Proposition II stands out perfect in the corporate world, which considers taxes.

The rising level of debt in the company with the rising cost of equity for the company will be

enabling the company to have a lower cost of capital for the company (Denis 2012). The pecking

order of theory showed the preferable financing structure that showed by applied by the

companies for the financing of the company (APPLIED CORPORATE FINANCE 2005). The

same is very much applicable by the companies in the corporates where the companies usually

prefer the theory for the capital structure. The trade-off theory for the company shows the best

example of having a sound and an optimal capital structure, but also considers the implication on

the company with the inclusion of various capital sources like bankruptcy cost and agency cost,

which the company face in the long term.

Thus, on an overall basis the theory does not emphasizes on the reduction of cost of capital for

the company rather it shows the preferred financing structures available for the companies.

Empirical Evidence

The traditional approach discussed does not fit into the corporate world as the theory

ignores the tax shield, which is gained to the firm from the taxable interest expenses paid by the

firm. Empirically many authors have reflected in there articles that the theory does not represent

the true and fair view in association with the cost of capital for the company. The Modigliani

Miller Proposition I takes the net income approach where the theory is not used for determine the

optimum cost of capital for the company because of constant weighted average cost of capital for

the company with the changing level of debt and equity in the company (Ardalan 2015).

However, it is crucial to note that companies pay interest on the debt borrowed which, is tax

deductible allowing the companies to have a lower cost of capital for the company. The

Modigliani Miller Proposition II stands out perfect in the corporate world, which considers taxes.

The rising level of debt in the company with the rising cost of equity for the company will be

enabling the company to have a lower cost of capital for the company (Denis 2012). The pecking

order of theory showed the preferable financing structure that showed by applied by the

companies for the financing of the company (APPLIED CORPORATE FINANCE 2005). The

same is very much applicable by the companies in the corporates where the companies usually

prefer the theory for the capital structure. The trade-off theory for the company shows the best

example of having a sound and an optimal capital structure, but also considers the implication on

the company with the inclusion of various capital sources like bankruptcy cost and agency cost,

which the company face in the long term.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ADVANCED FINANCIAL DECISION

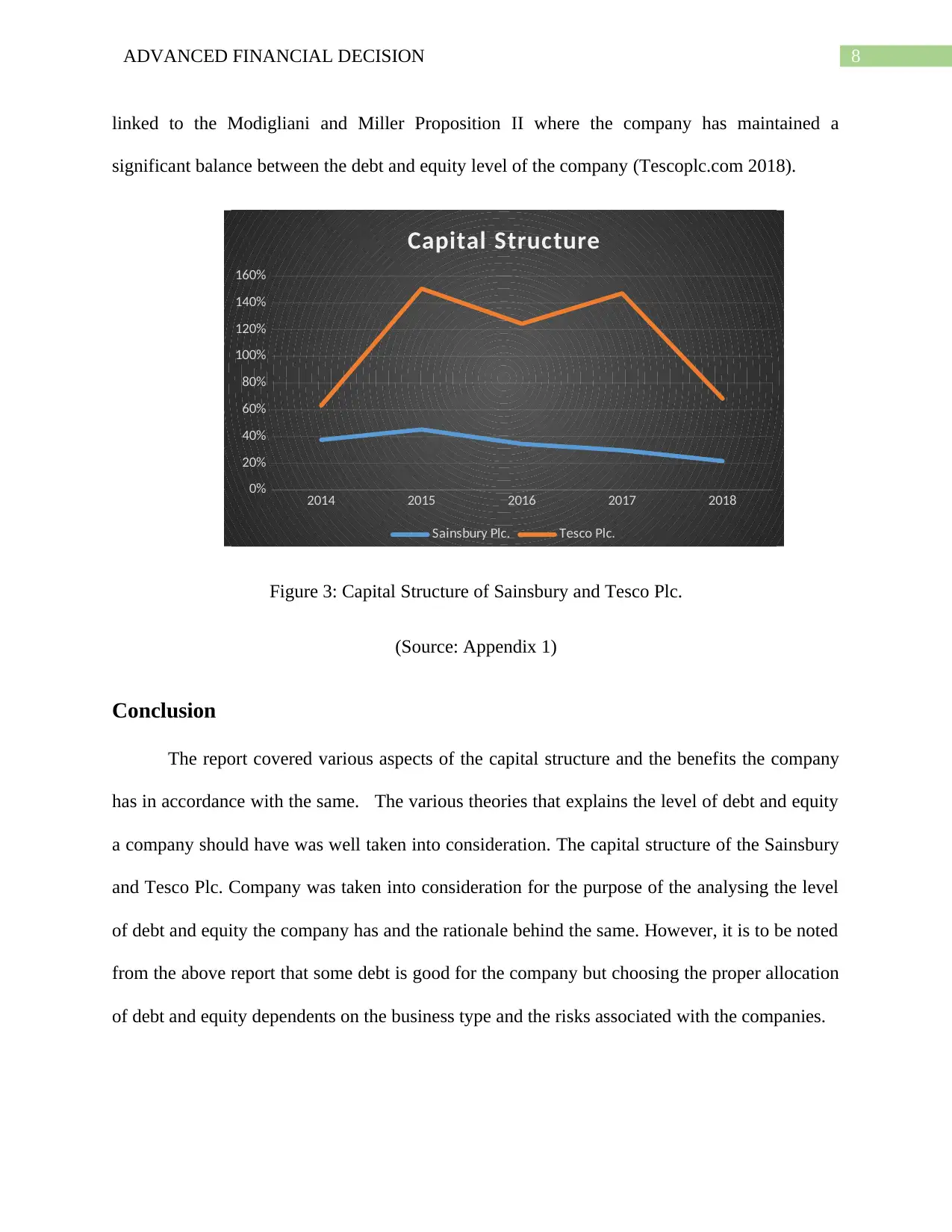

Analysis of Capital Structure

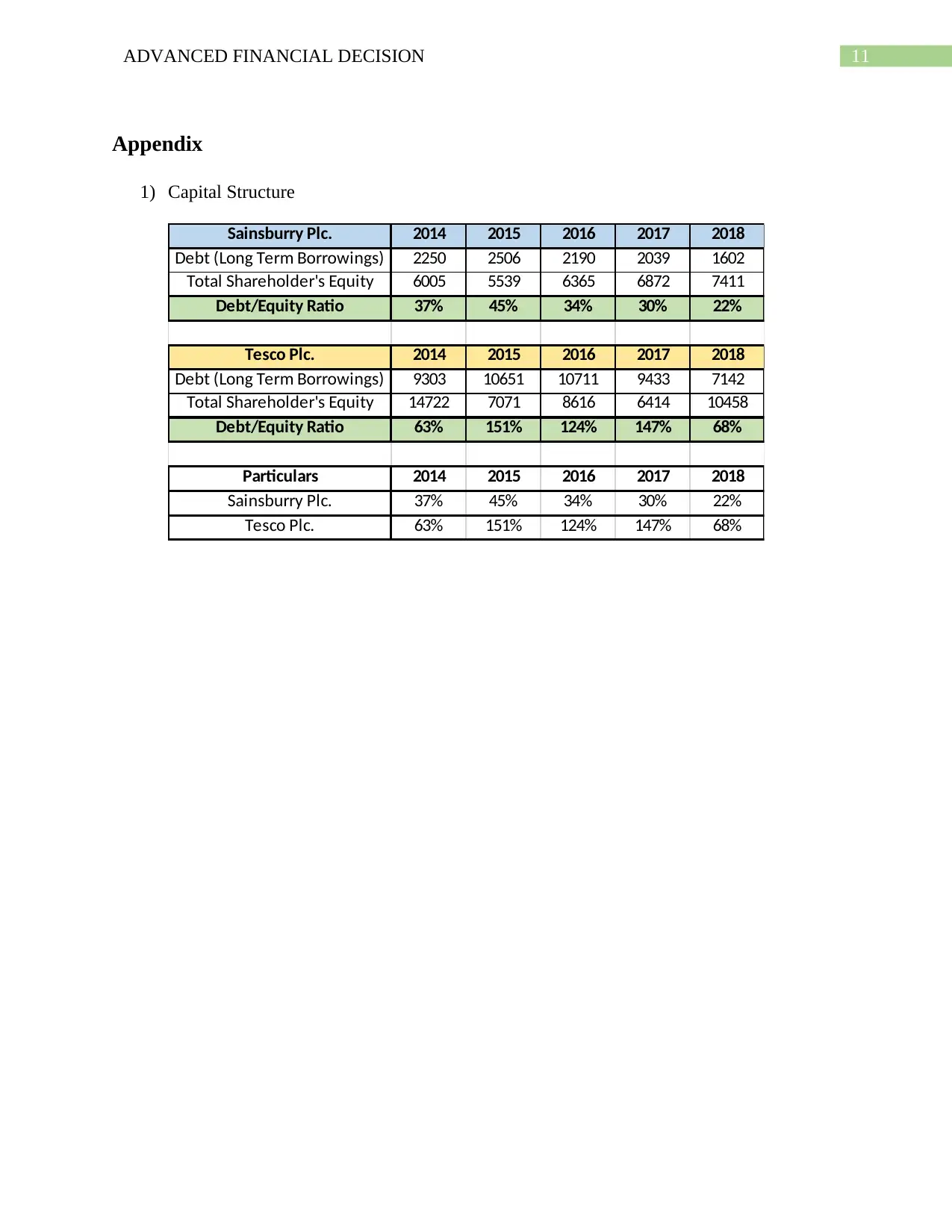

The capital structure of the Tesco Plc. and Sainsbury Company from the year 2014-18.

The debt to equity structure for the Sainsbury Company has been stable for the company with the

company choosing an optimal level of debt for financing the company. The effect of debt for the

company in the books of accounts has been falling constant the same has been done after

considering the level of debt in the books of accounts for the company. The Sainsbury Company

chooses both debt and equity financing for financing the long-term operations of the company

(About.sainsburys.co.uk 2016). The company has not specified any specific capital structure

policies followed by the management of the company for financing the operations of the

company. However, the company is more inclined with the trade-off theory policy where the

company is considering various factors and the business risk associated with the company and

selecting an optimal capital structure of the company (About.sainsburys.co.uk. 2018).

TESCO Plc. Company is also having a mixture of debt financing and equity financing in

the overall capital structure of the company. The debt to equity ratio for the company has been

volatile in the trend period analysed for the company where the company in the year 2018 has

significantly reduced the level of debt to avoid financial risk. The increasing level of leverage in

the company will increase the agency cost and the bankruptcy cost (Tescoplc.com 2016). The

business risk and the financial risk are some of the common risk that should be taken into

consideration while analysing the capital structure of the company. The level of debt for the

company in the initial year has been increasing but after taking into account with the rising level

of risk in the company has reduced debt and considered equity financing as a considerable source

of financing for the company. The capital structure policy followed by the company can be well

Analysis of Capital Structure

The capital structure of the Tesco Plc. and Sainsbury Company from the year 2014-18.

The debt to equity structure for the Sainsbury Company has been stable for the company with the

company choosing an optimal level of debt for financing the company. The effect of debt for the

company in the books of accounts has been falling constant the same has been done after

considering the level of debt in the books of accounts for the company. The Sainsbury Company

chooses both debt and equity financing for financing the long-term operations of the company

(About.sainsburys.co.uk 2016). The company has not specified any specific capital structure

policies followed by the management of the company for financing the operations of the

company. However, the company is more inclined with the trade-off theory policy where the

company is considering various factors and the business risk associated with the company and

selecting an optimal capital structure of the company (About.sainsburys.co.uk. 2018).

TESCO Plc. Company is also having a mixture of debt financing and equity financing in

the overall capital structure of the company. The debt to equity ratio for the company has been

volatile in the trend period analysed for the company where the company in the year 2018 has

significantly reduced the level of debt to avoid financial risk. The increasing level of leverage in

the company will increase the agency cost and the bankruptcy cost (Tescoplc.com 2016). The

business risk and the financial risk are some of the common risk that should be taken into

consideration while analysing the capital structure of the company. The level of debt for the

company in the initial year has been increasing but after taking into account with the rising level

of risk in the company has reduced debt and considered equity financing as a considerable source

of financing for the company. The capital structure policy followed by the company can be well

8ADVANCED FINANCIAL DECISION

linked to the Modigliani and Miller Proposition II where the company has maintained a

significant balance between the debt and equity level of the company (Tescoplc.com 2018).

2014 2015 2016 2017 2018

0%

20%

40%

60%

80%

100%

120%

140%

160%

Capital Structure

Sainsbury Plc. Tesco Plc.

Figure 3: Capital Structure of Sainsbury and Tesco Plc.

(Source: Appendix 1)

Conclusion

The report covered various aspects of the capital structure and the benefits the company

has in accordance with the same. The various theories that explains the level of debt and equity

a company should have was well taken into consideration. The capital structure of the Sainsbury

and Tesco Plc. Company was taken into consideration for the purpose of the analysing the level

of debt and equity the company has and the rationale behind the same. However, it is to be noted

from the above report that some debt is good for the company but choosing the proper allocation

of debt and equity dependents on the business type and the risks associated with the companies.

linked to the Modigliani and Miller Proposition II where the company has maintained a

significant balance between the debt and equity level of the company (Tescoplc.com 2018).

2014 2015 2016 2017 2018

0%

20%

40%

60%

80%

100%

120%

140%

160%

Capital Structure

Sainsbury Plc. Tesco Plc.

Figure 3: Capital Structure of Sainsbury and Tesco Plc.

(Source: Appendix 1)

Conclusion

The report covered various aspects of the capital structure and the benefits the company

has in accordance with the same. The various theories that explains the level of debt and equity

a company should have was well taken into consideration. The capital structure of the Sainsbury

and Tesco Plc. Company was taken into consideration for the purpose of the analysing the level

of debt and equity the company has and the rationale behind the same. However, it is to be noted

from the above report that some debt is good for the company but choosing the proper allocation

of debt and equity dependents on the business type and the risks associated with the companies.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ADVANCED FINANCIAL DECISION

References

About.sainsburys.co.uk. 2016. Sainsbury Annual report 2016. [online] Available at:

https://www.about.sainsburys.co.uk/~/media/Files/S/Sainsburys/documents/reports-and-

presentations/annual-reports/annual-report-2016.pdf [Accessed 24 Feb. 2019].

About.sainsburys.co.uk. 2018. Sainsburys Annual Report 2018. [online] Available at:

https://www.about.sainsburys.co.uk/~/media/Files/S/Sainsburys/documents/reports-and-

presentations/annual-reports/sainsburys-ar-2018-full-report-v2.pdf [Accessed 24 Feb. 2019].

APPLIED CORPORATE FINANCE. 2005. 1st ed. Morgan Stanley, pp.3-6.

Ardalan, K. 2015. Capital structure theory: Reconsidered. [ebook] New York 12601-1387,

USA: Elsevier, pp.2-10. Available at: http://www.elsevier.com/locate/ribaf [Accessed 24 Feb.

2019].

Bhattacharyya, N. and Morrill, C.K., 2015. Capital Structure: Theory and Evidence. Available at

SSRN 2611371.

Brusov, P., Filatova, T., Orekhova, N. and Eskindarov, M., 2018. New meaningful effects in

modern capital structure theory. In Modern Corporate Finance, Investments, Taxation and

Ratings (pp. 537-568). Springer, Cham.

Brusov, P., Filatova, T., Orekhova, N. and Eskindarov, M., 2018. Capital Structure: Modigliani–

Miller Theory. In Modern Corporate Finance, Investments, Taxation and Ratings (pp. 9-27).

Springer, Cham.

Denis, D. 2012. The Persistent Puzzle of Corporate Capital Structure: Current Challenges and

New Directions. The Financial Review 47, pp.1-6.

References

About.sainsburys.co.uk. 2016. Sainsbury Annual report 2016. [online] Available at:

https://www.about.sainsburys.co.uk/~/media/Files/S/Sainsburys/documents/reports-and-

presentations/annual-reports/annual-report-2016.pdf [Accessed 24 Feb. 2019].

About.sainsburys.co.uk. 2018. Sainsburys Annual Report 2018. [online] Available at:

https://www.about.sainsburys.co.uk/~/media/Files/S/Sainsburys/documents/reports-and-

presentations/annual-reports/sainsburys-ar-2018-full-report-v2.pdf [Accessed 24 Feb. 2019].

APPLIED CORPORATE FINANCE. 2005. 1st ed. Morgan Stanley, pp.3-6.

Ardalan, K. 2015. Capital structure theory: Reconsidered. [ebook] New York 12601-1387,

USA: Elsevier, pp.2-10. Available at: http://www.elsevier.com/locate/ribaf [Accessed 24 Feb.

2019].

Bhattacharyya, N. and Morrill, C.K., 2015. Capital Structure: Theory and Evidence. Available at

SSRN 2611371.

Brusov, P., Filatova, T., Orekhova, N. and Eskindarov, M., 2018. New meaningful effects in

modern capital structure theory. In Modern Corporate Finance, Investments, Taxation and

Ratings (pp. 537-568). Springer, Cham.

Brusov, P., Filatova, T., Orekhova, N. and Eskindarov, M., 2018. Capital Structure: Modigliani–

Miller Theory. In Modern Corporate Finance, Investments, Taxation and Ratings (pp. 9-27).

Springer, Cham.

Denis, D. 2012. The Persistent Puzzle of Corporate Capital Structure: Current Challenges and

New Directions. The Financial Review 47, pp.1-6.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ADVANCED FINANCIAL DECISION

Serrasqueiro, Z. and Caetano, A., 2015. Trade-Off Theory versus Pecking Order Theory: capital

structure decisions in a peripheral region of Portugal. Journal of Business Economics and

Management, 16(2), pp.445-466.

Tescoplc.com. 2016. Tesco Annual Report 2016. [online] Available at:

https://www.tescoplc.com/media/264194/annual-report-2016.pdf [Accessed 24 Feb. 2019].

Tescoplc.com. 2018. Tesco Annual Report 2018. [online] Available at:

https://www.tescoplc.com/media/474793/tesco_ar_2018.pdf [Accessed 24 Feb. 2019].

Serrasqueiro, Z. and Caetano, A., 2015. Trade-Off Theory versus Pecking Order Theory: capital

structure decisions in a peripheral region of Portugal. Journal of Business Economics and

Management, 16(2), pp.445-466.

Tescoplc.com. 2016. Tesco Annual Report 2016. [online] Available at:

https://www.tescoplc.com/media/264194/annual-report-2016.pdf [Accessed 24 Feb. 2019].

Tescoplc.com. 2018. Tesco Annual Report 2018. [online] Available at:

https://www.tescoplc.com/media/474793/tesco_ar_2018.pdf [Accessed 24 Feb. 2019].

11ADVANCED FINANCIAL DECISION

Appendix

1) Capital Structure

Sainsburry Plc. 2014 2015 2016 2017 2018

Debt (Long Term Borrowings) 2250 2506 2190 2039 1602

Total Shareholder's Equity 6005 5539 6365 6872 7411

Debt/Equity Ratio 37% 45% 34% 30% 22%

Tesco Plc. 2014 2015 2016 2017 2018

Debt (Long Term Borrowings) 9303 10651 10711 9433 7142

Total Shareholder's Equity 14722 7071 8616 6414 10458

Debt/Equity Ratio 63% 151% 124% 147% 68%

Particulars 2014 2015 2016 2017 2018

Sainsburry Plc. 37% 45% 34% 30% 22%

Tesco Plc. 63% 151% 124% 147% 68%

Appendix

1) Capital Structure

Sainsburry Plc. 2014 2015 2016 2017 2018

Debt (Long Term Borrowings) 2250 2506 2190 2039 1602

Total Shareholder's Equity 6005 5539 6365 6872 7411

Debt/Equity Ratio 37% 45% 34% 30% 22%

Tesco Plc. 2014 2015 2016 2017 2018

Debt (Long Term Borrowings) 9303 10651 10711 9433 7142

Total Shareholder's Equity 14722 7071 8616 6414 10458

Debt/Equity Ratio 63% 151% 124% 147% 68%

Particulars 2014 2015 2016 2017 2018

Sainsburry Plc. 37% 45% 34% 30% 22%

Tesco Plc. 63% 151% 124% 147% 68%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.