MN7705: Capital Structure Theories' Impact on Corporate Strategy

VerifiedAdded on 2022/09/07

|14

|3455

|16

Report

AI Summary

This report provides a comprehensive analysis of capital structure theories, specifically focusing on the Trade-off and Pecking Order theories. It begins with an introduction to the significance of capital in corporate finance and the challenges in managing capital structure decisions. The report delves into the core concepts of each theory, examining their assumptions, strengths, and limitations. The Trade-off theory is discussed in detail, including the balancing of benefits (tax shields) against costs (financial distress and agency costs). The Pecking Order theory is then explored, emphasizing the role of information asymmetry and the hierarchy of financing decisions. The discussion includes relevant graphs illustrating the Trade-off theory and the importance of internal financing. The report also addresses the impact of taxes and bankruptcy costs on capital structure choices, offering a thorough understanding of how companies make financing decisions. The conclusion summarizes the key findings and implications of these theories for corporate policy and strategy.

Running Head: MANAGING FINANCE FOR CORPORATE POLICY AND STRATEGY

MANAGING FINANCE FOR CORPORATE POLICY AND STRATEGY

Name of the Student

Name of the University

Author Note

MANAGING FINANCE FOR CORPORATE POLICY AND STRATEGY

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGING FINANCE FOR CORPORATE POLICY AND STRATEGY

Table of Contents

Introduction................................................................................................................................2

Discussion..................................................................................................................................3

Capital Structure Theories’ Overview...................................................................................3

Trade-Off Theory...................................................................................................................3

Pecking Order Theory............................................................................................................6

Conclusion..................................................................................................................................9

Reference..................................................................................................................................11

Table of Contents

Introduction................................................................................................................................2

Discussion..................................................................................................................................3

Capital Structure Theories’ Overview...................................................................................3

Trade-Off Theory...................................................................................................................3

Pecking Order Theory............................................................................................................6

Conclusion..................................................................................................................................9

Reference..................................................................................................................................11

2MANAGING FINANCE FOR CORPORATE POLICY AND STRATEGY

Introduction

Capital plays significant role in activities of the company. The competitive

environment of today has made managers cautious as well as more aware regarding the way

their business activities could be financed and capital structure could be managed. Capital

structure signified as most debatable concepts in the corporate finance. Majority of the

entities shows their concerns relating to capital structure as well as its decisions on the capital

structure, which is challenging for entity’s management. The reason behind this is capital

structure decision plays key role in business organization’s survival and any wrong decision

may results in financial distress of entities that leads to bankruptcy. Hence, decision

regarding company’s capital structure is most important decision confronting an entity in the

corporate finance. Further, decision-making of the capital structure is tactic, which is the art

for tackle down the complex situations (Yapa Abeywardhana 2017).

The capital structure is regarding financing the operations of business at the optimum

cost, which maximizes firm’s overall value. It is relative proportion of the equity and debt

that is used for financing the long-term funds sources used by companies. This include

common equity, debt and the preferred stock. There are different strategies that can be

employed for raising required funds, however most vital and basic financial sources are

shares, debt and retained earnings. The two major sources of company’s financing include

external and the internal financing. The external financing is referred to issue of debt or

equity and the internal financing source include retained earnings (Yulianto, Suseno and

Widiyanto 2016). Hence, this report aims to discuss two main theories of the capital

structure, which are Pecking order theory and Trade-off theory.

Introduction

Capital plays significant role in activities of the company. The competitive

environment of today has made managers cautious as well as more aware regarding the way

their business activities could be financed and capital structure could be managed. Capital

structure signified as most debatable concepts in the corporate finance. Majority of the

entities shows their concerns relating to capital structure as well as its decisions on the capital

structure, which is challenging for entity’s management. The reason behind this is capital

structure decision plays key role in business organization’s survival and any wrong decision

may results in financial distress of entities that leads to bankruptcy. Hence, decision

regarding company’s capital structure is most important decision confronting an entity in the

corporate finance. Further, decision-making of the capital structure is tactic, which is the art

for tackle down the complex situations (Yapa Abeywardhana 2017).

The capital structure is regarding financing the operations of business at the optimum

cost, which maximizes firm’s overall value. It is relative proportion of the equity and debt

that is used for financing the long-term funds sources used by companies. This include

common equity, debt and the preferred stock. There are different strategies that can be

employed for raising required funds, however most vital and basic financial sources are

shares, debt and retained earnings. The two major sources of company’s financing include

external and the internal financing. The external financing is referred to issue of debt or

equity and the internal financing source include retained earnings (Yulianto, Suseno and

Widiyanto 2016). Hence, this report aims to discuss two main theories of the capital

structure, which are Pecking order theory and Trade-off theory.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANAGING FINANCE FOR CORPORATE POLICY AND STRATEGY

Discussion

Capital Structure Theories’ Overview

‘Modigliani and Miller’ in 1958, firstly began the revolutionary work on the capital

structure in corporate finance field. The theory by MM states that in the perfect capital

markets, the leverage impact cannot be seen on the value of firm. It is because of this reason,

the theories propounded by MM is also termed as “The Irrelevance Theory”. This theory

documented that value of firm is not affected by ratio of debt to equity. However, in the real

world, structure of capital structure is relevant, which means, organization’s value is affected

by capital structure employed (Yang, Chueh and Lee 2014). Moreover, Myers in 1984

contrasted to the previous studies by saying that various theories of the capital structure does

not seems to explain the actual financing behavior and it appears to be presumptions for

advising companies on the optimum structure of capital, when one is so far from the

explanations of actual decisions. Later, it has been proved in one study that at financial

structure yielding lowest WACC, overall organization’s value is also maximized. This is

identified in study that correlation in between increase in value of organization can be

enhanced with the increased debt level (Thippayana 2014).

Further, there are various theories of capital structure highlighted in literature.

Generally, capital structure is managed by two most important theories, which are “Trade-off

theory” and “Pecking order theory”. The intensive research indicates that both the theories

plays dominant role in financing decisions of companies. Both theories have its own merits

and demerits (Shahar et al. 2015).

Trade-Off Theory

The most prominent theory of capital structure was Trade Off Theory. Myers in 1984

stated that by including the imperfections of market, entities seems to get the optimal value-

maximizing ratio of debt-equity with the help of trading off benefits of debt against any

Discussion

Capital Structure Theories’ Overview

‘Modigliani and Miller’ in 1958, firstly began the revolutionary work on the capital

structure in corporate finance field. The theory by MM states that in the perfect capital

markets, the leverage impact cannot be seen on the value of firm. It is because of this reason,

the theories propounded by MM is also termed as “The Irrelevance Theory”. This theory

documented that value of firm is not affected by ratio of debt to equity. However, in the real

world, structure of capital structure is relevant, which means, organization’s value is affected

by capital structure employed (Yang, Chueh and Lee 2014). Moreover, Myers in 1984

contrasted to the previous studies by saying that various theories of the capital structure does

not seems to explain the actual financing behavior and it appears to be presumptions for

advising companies on the optimum structure of capital, when one is so far from the

explanations of actual decisions. Later, it has been proved in one study that at financial

structure yielding lowest WACC, overall organization’s value is also maximized. This is

identified in study that correlation in between increase in value of organization can be

enhanced with the increased debt level (Thippayana 2014).

Further, there are various theories of capital structure highlighted in literature.

Generally, capital structure is managed by two most important theories, which are “Trade-off

theory” and “Pecking order theory”. The intensive research indicates that both the theories

plays dominant role in financing decisions of companies. Both theories have its own merits

and demerits (Shahar et al. 2015).

Trade-Off Theory

The most prominent theory of capital structure was Trade Off Theory. Myers in 1984

stated that by including the imperfections of market, entities seems to get the optimal value-

maximizing ratio of debt-equity with the help of trading off benefits of debt against any

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGING FINANCE FOR CORPORATE POLICY AND STRATEGY

disadvantages. Hence, entities set the target ratio of debt and move gradually towards

achievement of goal. Trade off-theory is the oldest theory, which is associated with theory

from MM on the capital structure, which makes the emphasis on structure of optimum

capital. The main assumptions in MM theory is that there are no taxes. This theory suggested

that modified proposition of MM stress out advantage of the tax shield is counterbalance by

entity costs of agency cost and the financial distress. The achievement of optimum leverage

level is by the help of balancing benefits from payments of interest and cost of issuing debt

(Serrasqueiro and Caetano 2015).

Development of “trade-off theory” is of MM theorem takes into consideration effects

of costs of bankruptcy and taxes. The cost of bankruptcy is the cost incurred directly, after

there is perceived likelihood that company will default on the financing seems to be more

than zero. Further, example of the costs of bankruptcy is liquidation costs that helps in

representing value loss as outcome of the liquidating net assets of organization. The other

cost of bankruptcy is the distress cost, which is the cost incurred by organization, if it is

believed by shareholders that company will be discontinued. Moreover, financial distress and

theories of agency costs also assumes that the higher level of debts brings out financial

distress that ultimately bankrupt the entity or forced for going into restructuring or liquidation

of company. This explanation indicates that costs of the financial distress as well as

advantage from the tax shields gets balanced. Hence, entities having higher financial distress

cost would be having less debt in their structure of the capital (Mostafa and Boregowda

2014).

“V= V+PV-PV where V is firm, PV is interest tax shields and financial distress cost”

disadvantages. Hence, entities set the target ratio of debt and move gradually towards

achievement of goal. Trade off-theory is the oldest theory, which is associated with theory

from MM on the capital structure, which makes the emphasis on structure of optimum

capital. The main assumptions in MM theory is that there are no taxes. This theory suggested

that modified proposition of MM stress out advantage of the tax shield is counterbalance by

entity costs of agency cost and the financial distress. The achievement of optimum leverage

level is by the help of balancing benefits from payments of interest and cost of issuing debt

(Serrasqueiro and Caetano 2015).

Development of “trade-off theory” is of MM theorem takes into consideration effects

of costs of bankruptcy and taxes. The cost of bankruptcy is the cost incurred directly, after

there is perceived likelihood that company will default on the financing seems to be more

than zero. Further, example of the costs of bankruptcy is liquidation costs that helps in

representing value loss as outcome of the liquidating net assets of organization. The other

cost of bankruptcy is the distress cost, which is the cost incurred by organization, if it is

believed by shareholders that company will be discontinued. Moreover, financial distress and

theories of agency costs also assumes that the higher level of debts brings out financial

distress that ultimately bankrupt the entity or forced for going into restructuring or liquidation

of company. This explanation indicates that costs of the financial distress as well as

advantage from the tax shields gets balanced. Hence, entities having higher financial distress

cost would be having less debt in their structure of the capital (Mostafa and Boregowda

2014).

“V= V+PV-PV where V is firm, PV is interest tax shields and financial distress cost”

5MANAGING FINANCE FOR CORPORATE POLICY AND STRATEGY

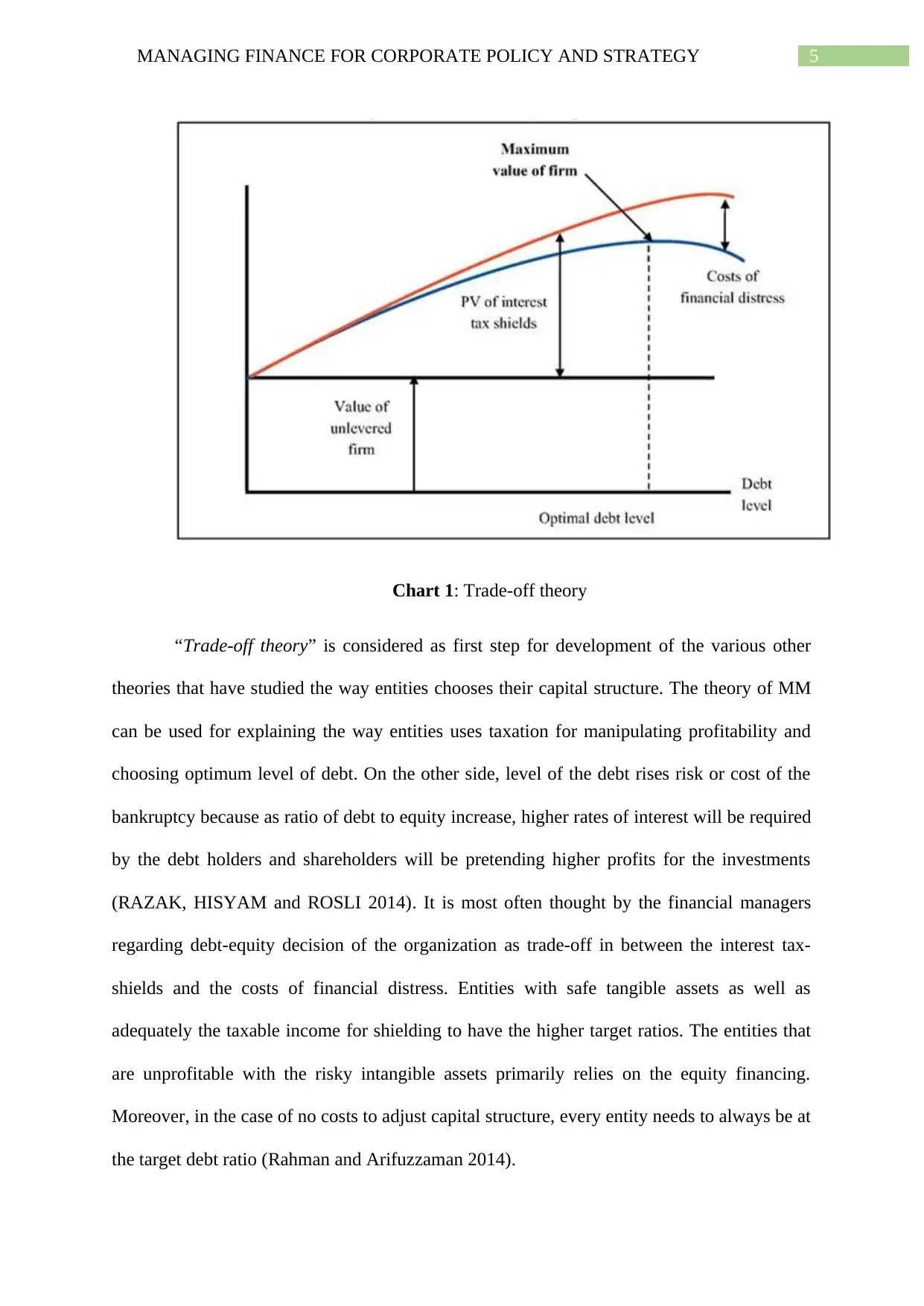

Chart 1: Trade-off theory

“Trade-off theory” is considered as first step for development of the various other

theories that have studied the way entities chooses their capital structure. The theory of MM

can be used for explaining the way entities uses taxation for manipulating profitability and

choosing optimum level of debt. On the other side, level of the debt rises risk or cost of the

bankruptcy because as ratio of debt to equity increase, higher rates of interest will be required

by the debt holders and shareholders will be pretending higher profits for the investments

(RAZAK, HISYAM and ROSLI 2014). It is most often thought by the financial managers

regarding debt-equity decision of the organization as trade-off in between the interest tax-

shields and the costs of financial distress. Entities with safe tangible assets as well as

adequately the taxable income for shielding to have the higher target ratios. The entities that

are unprofitable with the risky intangible assets primarily relies on the equity financing.

Moreover, in the case of no costs to adjust capital structure, every entity needs to always be at

the target debt ratio (Rahman and Arifuzzaman 2014).

Chart 1: Trade-off theory

“Trade-off theory” is considered as first step for development of the various other

theories that have studied the way entities chooses their capital structure. The theory of MM

can be used for explaining the way entities uses taxation for manipulating profitability and

choosing optimum level of debt. On the other side, level of the debt rises risk or cost of the

bankruptcy because as ratio of debt to equity increase, higher rates of interest will be required

by the debt holders and shareholders will be pretending higher profits for the investments

(RAZAK, HISYAM and ROSLI 2014). It is most often thought by the financial managers

regarding debt-equity decision of the organization as trade-off in between the interest tax-

shields and the costs of financial distress. Entities with safe tangible assets as well as

adequately the taxable income for shielding to have the higher target ratios. The entities that

are unprofitable with the risky intangible assets primarily relies on the equity financing.

Moreover, in the case of no costs to adjust capital structure, every entity needs to always be at

the target debt ratio (Rahman and Arifuzzaman 2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MANAGING FINANCE FOR CORPORATE POLICY AND STRATEGY

There include various fundamentals for considering debt in the capital structure of

firm. Apart from the interest tax shield’s advantage, debt is having multiple benefits to

companies. The first benefit is that the debt is valuable device used by entity for signaling.

Research suggested that the leverage will increase value of entity because enhanced leverage

coincides with market’s value realization (Pontoh 2017). The second benefit is that debt will

reduce costs of agency related to the equity. These agency costs include problem of free cash

flow that is also known as problem of over investment. The third benefit is that debt reduces

management’s agency cost so that it helps in discipling the managers. However, details of the

debt limitations besides costs of bankruptcy as well as the financial distress includes that

managers acting in the shareholders’ interest may shifts the investment to the riskier assets

and incurring of costs are by holders of debt (Qureshi, Sheikh and Khan 2015). The second

limitation is that the managers might borrow still more as well as pays out to shareholders, as

the result of which debt holders suffers. The third limitation is that the excessive debts leads

to problem of the underinvestment or the problem of “debt overhang”. It means various good

projects could be passed on due to the fact that more level of debt cannot be issued at right

time because of existing level of debt (Martinez, Scherger and Guercio 2019).

“Trade-off theory” has been supported as well as criticized based on fact that this

particular theory is based on assumptions of the perfect knowledge in the perfect market. This

theory predicts that the highly profitable entities will be having higher levels of debt for

maximizing benefits of taxation and increase capital liability. Moreover, various studies have

conducted for proving that whether in reality entities follows trade of theory (Köksal and

Orman 2015).

Pecking Order Theory

Picking order theory has able to achieve noticeable importance in the descriptive

literature. Further, this major theory was developed by Myers in field of the corporate finance

There include various fundamentals for considering debt in the capital structure of

firm. Apart from the interest tax shield’s advantage, debt is having multiple benefits to

companies. The first benefit is that the debt is valuable device used by entity for signaling.

Research suggested that the leverage will increase value of entity because enhanced leverage

coincides with market’s value realization (Pontoh 2017). The second benefit is that debt will

reduce costs of agency related to the equity. These agency costs include problem of free cash

flow that is also known as problem of over investment. The third benefit is that debt reduces

management’s agency cost so that it helps in discipling the managers. However, details of the

debt limitations besides costs of bankruptcy as well as the financial distress includes that

managers acting in the shareholders’ interest may shifts the investment to the riskier assets

and incurring of costs are by holders of debt (Qureshi, Sheikh and Khan 2015). The second

limitation is that the managers might borrow still more as well as pays out to shareholders, as

the result of which debt holders suffers. The third limitation is that the excessive debts leads

to problem of the underinvestment or the problem of “debt overhang”. It means various good

projects could be passed on due to the fact that more level of debt cannot be issued at right

time because of existing level of debt (Martinez, Scherger and Guercio 2019).

“Trade-off theory” has been supported as well as criticized based on fact that this

particular theory is based on assumptions of the perfect knowledge in the perfect market. This

theory predicts that the highly profitable entities will be having higher levels of debt for

maximizing benefits of taxation and increase capital liability. Moreover, various studies have

conducted for proving that whether in reality entities follows trade of theory (Köksal and

Orman 2015).

Pecking Order Theory

Picking order theory has able to achieve noticeable importance in the descriptive

literature. Further, this major theory was developed by Myers in field of the corporate finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGING FINANCE FOR CORPORATE POLICY AND STRATEGY

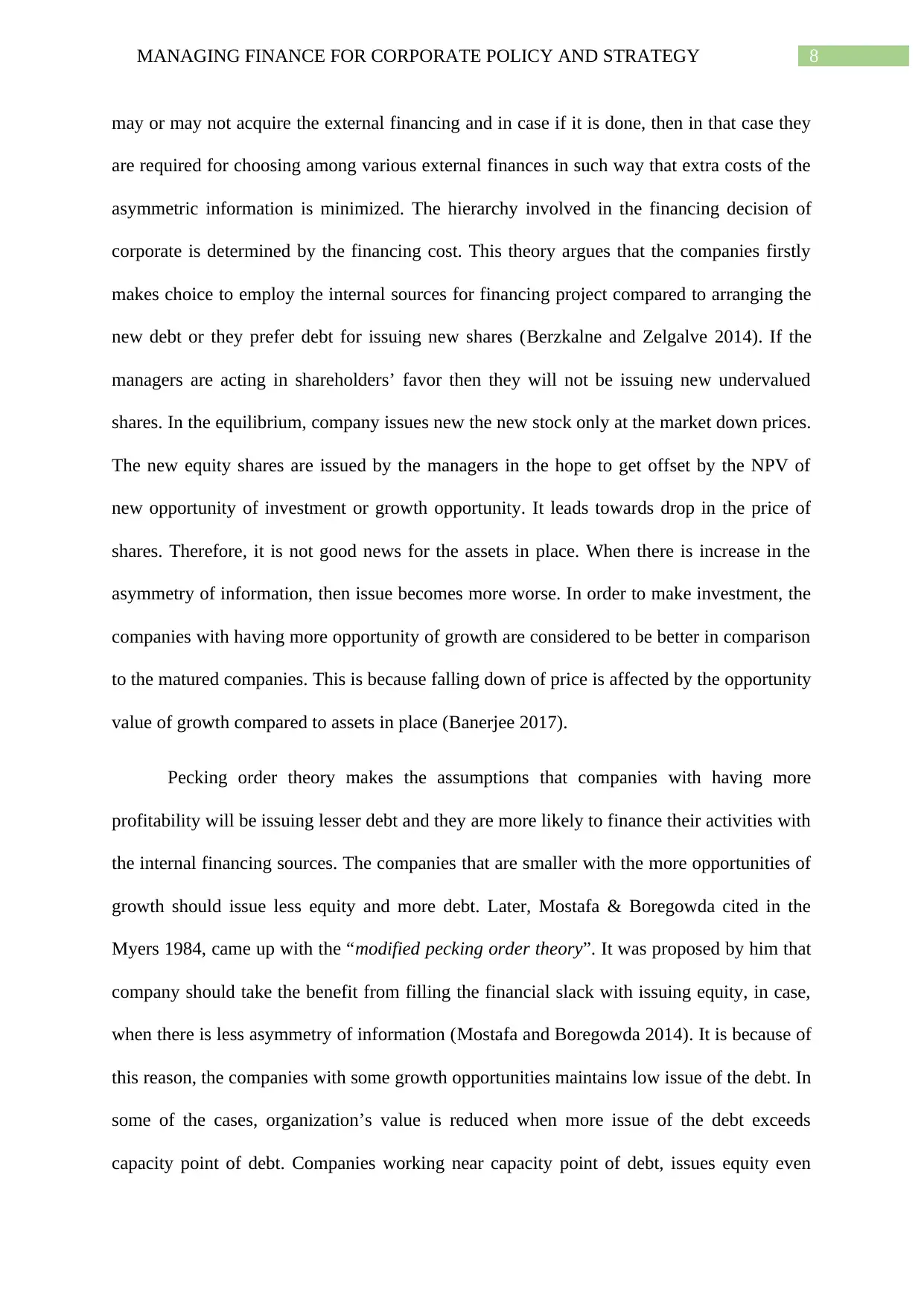

in relation to the capital structure. This is the alternative theory to the “trade-off theory”, in

which company is having perfect hierarchy of the financing decision. Main pillar of “Pecking

order theory” is information asymmetry. The theory of Trade-off does not consider

information asymmetry. However, this theory does not consider optimum structure of capital

or no target structure of capital. Further, apart from considering information asymmetry, it

also considers signaling effect. “Pecking order theory” was proposed by the “Myers and

Majluf” in year 1984. Further, they assume perfect market like MM (Güner 2016).

Figure 2: Pecking order theory hierarchy

Major factor that determines debt ratios levels includes demand and the supply

factors. However, decisions relating financing sources depends on preference order, which

includes internal finance, for instance retained earnings and reserves, equity and debts and

firms maximizes its values with the help of making choice for financing the new investment

with cheapest sources available (Chadha and Sharma 2015). The example of this is when

there are not sufficient internal funds for financing opportunities of investment then entities

in relation to the capital structure. This is the alternative theory to the “trade-off theory”, in

which company is having perfect hierarchy of the financing decision. Main pillar of “Pecking

order theory” is information asymmetry. The theory of Trade-off does not consider

information asymmetry. However, this theory does not consider optimum structure of capital

or no target structure of capital. Further, apart from considering information asymmetry, it

also considers signaling effect. “Pecking order theory” was proposed by the “Myers and

Majluf” in year 1984. Further, they assume perfect market like MM (Güner 2016).

Figure 2: Pecking order theory hierarchy

Major factor that determines debt ratios levels includes demand and the supply

factors. However, decisions relating financing sources depends on preference order, which

includes internal finance, for instance retained earnings and reserves, equity and debts and

firms maximizes its values with the help of making choice for financing the new investment

with cheapest sources available (Chadha and Sharma 2015). The example of this is when

there are not sufficient internal funds for financing opportunities of investment then entities

8MANAGING FINANCE FOR CORPORATE POLICY AND STRATEGY

may or may not acquire the external financing and in case if it is done, then in that case they

are required for choosing among various external finances in such way that extra costs of the

asymmetric information is minimized. The hierarchy involved in the financing decision of

corporate is determined by the financing cost. This theory argues that the companies firstly

makes choice to employ the internal sources for financing project compared to arranging the

new debt or they prefer debt for issuing new shares (Berzkalne and Zelgalve 2014). If the

managers are acting in shareholders’ favor then they will not be issuing new undervalued

shares. In the equilibrium, company issues new the new stock only at the market down prices.

The new equity shares are issued by the managers in the hope to get offset by the NPV of

new opportunity of investment or growth opportunity. It leads towards drop in the price of

shares. Therefore, it is not good news for the assets in place. When there is increase in the

asymmetry of information, then issue becomes more worse. In order to make investment, the

companies with having more opportunity of growth are considered to be better in comparison

to the matured companies. This is because falling down of price is affected by the opportunity

value of growth compared to assets in place (Banerjee 2017).

Pecking order theory makes the assumptions that companies with having more

profitability will be issuing lesser debt and they are more likely to finance their activities with

the internal financing sources. The companies that are smaller with the more opportunities of

growth should issue less equity and more debt. Later, Mostafa & Boregowda cited in the

Myers 1984, came up with the “modified pecking order theory”. It was proposed by him that

company should take the benefit from filling the financial slack with issuing equity, in case,

when there is less asymmetry of information (Mostafa and Boregowda 2014). It is because of

this reason, the companies with some growth opportunities maintains low issue of the debt. In

some of the cases, organization’s value is reduced when more issue of the debt exceeds

capacity point of debt. Companies working near capacity point of debt, issues equity even

may or may not acquire the external financing and in case if it is done, then in that case they

are required for choosing among various external finances in such way that extra costs of the

asymmetric information is minimized. The hierarchy involved in the financing decision of

corporate is determined by the financing cost. This theory argues that the companies firstly

makes choice to employ the internal sources for financing project compared to arranging the

new debt or they prefer debt for issuing new shares (Berzkalne and Zelgalve 2014). If the

managers are acting in shareholders’ favor then they will not be issuing new undervalued

shares. In the equilibrium, company issues new the new stock only at the market down prices.

The new equity shares are issued by the managers in the hope to get offset by the NPV of

new opportunity of investment or growth opportunity. It leads towards drop in the price of

shares. Therefore, it is not good news for the assets in place. When there is increase in the

asymmetry of information, then issue becomes more worse. In order to make investment, the

companies with having more opportunity of growth are considered to be better in comparison

to the matured companies. This is because falling down of price is affected by the opportunity

value of growth compared to assets in place (Banerjee 2017).

Pecking order theory makes the assumptions that companies with having more

profitability will be issuing lesser debt and they are more likely to finance their activities with

the internal financing sources. The companies that are smaller with the more opportunities of

growth should issue less equity and more debt. Later, Mostafa & Boregowda cited in the

Myers 1984, came up with the “modified pecking order theory”. It was proposed by him that

company should take the benefit from filling the financial slack with issuing equity, in case,

when there is less asymmetry of information (Mostafa and Boregowda 2014). It is because of

this reason, the companies with some growth opportunities maintains low issue of the debt. In

some of the cases, organization’s value is reduced when more issue of the debt exceeds

capacity point of debt. Companies working near capacity point of debt, issues equity even

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MANAGING FINANCE FOR CORPORATE POLICY AND STRATEGY

when debt is preferable. It is because issuing debt, which exceeds capacity point of debt

reduces company’s value. Hence, based on this concept, it can be said that capacity point of

debt looks like target debt ratio that is mentioned in traditional approach of trade-off theory

of the capital structure (Adair and Adaskou 2015). The most significant way for identifying

the company that are following traditional approach of “trade-off theory” or the “pecking

order theory” is during time of IPO, in this it needs to check that whether entity has used all

its internal financing sources or not. In case, if all the internal sources are used for the

investment in new project by company, then it means that entity is following the pecking

order theory (Abbasi and Delghandi 2016).

Conclusion

Therefore, this report concludes that financial decision is vital for any entity. Both

pioneering theories, pecking order and the trade-off theories are not considered to be

mutually exclusive and few explanatory variables helps in obtaining optimal leverage ratio.

Further, trade-off theory states that for reducing taxable income, the profitable entities lean

towards issuing of more debt. Moreover, pecking other theory states that the profitable

entities try for reducing their level of debt according to rule that firstly internal funds should

be chosen and when there are not satisfactory retained earnings, then policies need to be

converted to the external financing.

Trade-off theory extensively explains capital structure and it does not possess much

limitations except the fact that there is negative correlation of profitability to debt. In

relations to this phenomenon, the theory of pecking order provides straight explanations that

limitations that there are mixed-proof in considering Pecking order theory itself. Hence, there

is requirement of more development for incorporating trade-off ideas as well as asymmetric

information in the future models that will be furnishing assumed as well as theoretical

outcomes for understanding complexities of the theories in better manner. Further, there are

when debt is preferable. It is because issuing debt, which exceeds capacity point of debt

reduces company’s value. Hence, based on this concept, it can be said that capacity point of

debt looks like target debt ratio that is mentioned in traditional approach of trade-off theory

of the capital structure (Adair and Adaskou 2015). The most significant way for identifying

the company that are following traditional approach of “trade-off theory” or the “pecking

order theory” is during time of IPO, in this it needs to check that whether entity has used all

its internal financing sources or not. In case, if all the internal sources are used for the

investment in new project by company, then it means that entity is following the pecking

order theory (Abbasi and Delghandi 2016).

Conclusion

Therefore, this report concludes that financial decision is vital for any entity. Both

pioneering theories, pecking order and the trade-off theories are not considered to be

mutually exclusive and few explanatory variables helps in obtaining optimal leverage ratio.

Further, trade-off theory states that for reducing taxable income, the profitable entities lean

towards issuing of more debt. Moreover, pecking other theory states that the profitable

entities try for reducing their level of debt according to rule that firstly internal funds should

be chosen and when there are not satisfactory retained earnings, then policies need to be

converted to the external financing.

Trade-off theory extensively explains capital structure and it does not possess much

limitations except the fact that there is negative correlation of profitability to debt. In

relations to this phenomenon, the theory of pecking order provides straight explanations that

limitations that there are mixed-proof in considering Pecking order theory itself. Hence, there

is requirement of more development for incorporating trade-off ideas as well as asymmetric

information in the future models that will be furnishing assumed as well as theoretical

outcomes for understanding complexities of the theories in better manner. Further, there are

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MANAGING FINANCE FOR CORPORATE POLICY AND STRATEGY

various empirical studies that have studied these theories, but researcher still not able to

identify the theory, which explains choice of capital structure in the best way. Many asserted

that theory of Pecking order better describes behavior of firm compared to traditional

approach of trade-off theory. Other researchers were having different opinions. Hence, there

are no universal theory of the choice of debt as well as equity and there should be no purpose

for expecting one. Yet, there are various valuable conditional theories that enables in

understanding financial structure, which is chosen by firm.

various empirical studies that have studied these theories, but researcher still not able to

identify the theory, which explains choice of capital structure in the best way. Many asserted

that theory of Pecking order better describes behavior of firm compared to traditional

approach of trade-off theory. Other researchers were having different opinions. Hence, there

are no universal theory of the choice of debt as well as equity and there should be no purpose

for expecting one. Yet, there are various valuable conditional theories that enables in

understanding financial structure, which is chosen by firm.

11MANAGING FINANCE FOR CORPORATE POLICY AND STRATEGY

Reference

Abbasi, E. and Delghandi, M., 2016. Impact of Firm Specific Factors on Capital Structure

based on Trade off Theory and Pecking Order Theory-An Empirical Study of the Tehran’s

Stock Market Companies. Arabian Journal of Business and Management Review, 6(2), pp.1-

4.

Adair, P. and Adaskou, M., 2015. Trade-off-theory vs. pecking order theory and the

determinants of corporate leverage: Evidence from a panel data analysis upon French SMEs

(2002–2010). Cogent Economics & Finance, 3(1), p.1006477.

Banerjee, A., 2017. Capital Structure and its determinants during the pre and post period of

recession: Pecking order vs. Trade off theory. Indian Journal of Finance (Scopus

Indexed), 11(1), p.44.

Berzkalne, I. and Zelgalve, E., 2014. Trade-off theory vs. Pecking order theory–empirical

evidence from the baltic countries. Journal of economic and social developmen, 1(1), pp.22-

32.

Chadha, S. and Sharma, A.K., 2015. Determinants of capital structure: An empirical

evaluation from India. Journal of Advances in Management Research.

Güner, A., 2016. The determinants of capital structure decisions: New evidence from Turkish

companies. Procedia economics and finance, 38, pp.84-89.

Köksal, B. and Orman, C., 2015. Determinants of capital structure: evidence from a major

developing economy. Small Business Economics, 44(2), pp.255-282.

Martinez, L.B., Scherger, V. and Guercio, M.B., 2019. SMEs capital structure: trade-off or

pecking order theory: a systematic review. Journal of Small Business and Enterprise

Development.

Reference

Abbasi, E. and Delghandi, M., 2016. Impact of Firm Specific Factors on Capital Structure

based on Trade off Theory and Pecking Order Theory-An Empirical Study of the Tehran’s

Stock Market Companies. Arabian Journal of Business and Management Review, 6(2), pp.1-

4.

Adair, P. and Adaskou, M., 2015. Trade-off-theory vs. pecking order theory and the

determinants of corporate leverage: Evidence from a panel data analysis upon French SMEs

(2002–2010). Cogent Economics & Finance, 3(1), p.1006477.

Banerjee, A., 2017. Capital Structure and its determinants during the pre and post period of

recession: Pecking order vs. Trade off theory. Indian Journal of Finance (Scopus

Indexed), 11(1), p.44.

Berzkalne, I. and Zelgalve, E., 2014. Trade-off theory vs. Pecking order theory–empirical

evidence from the baltic countries. Journal of economic and social developmen, 1(1), pp.22-

32.

Chadha, S. and Sharma, A.K., 2015. Determinants of capital structure: An empirical

evaluation from India. Journal of Advances in Management Research.

Güner, A., 2016. The determinants of capital structure decisions: New evidence from Turkish

companies. Procedia economics and finance, 38, pp.84-89.

Köksal, B. and Orman, C., 2015. Determinants of capital structure: evidence from a major

developing economy. Small Business Economics, 44(2), pp.255-282.

Martinez, L.B., Scherger, V. and Guercio, M.B., 2019. SMEs capital structure: trade-off or

pecking order theory: a systematic review. Journal of Small Business and Enterprise

Development.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.