Case Study: Valuation of Telstra and Wesfarmers for FINA6000 Module

VerifiedAdded on 2023/05/29

|20

|3173

|322

Case Study

AI Summary

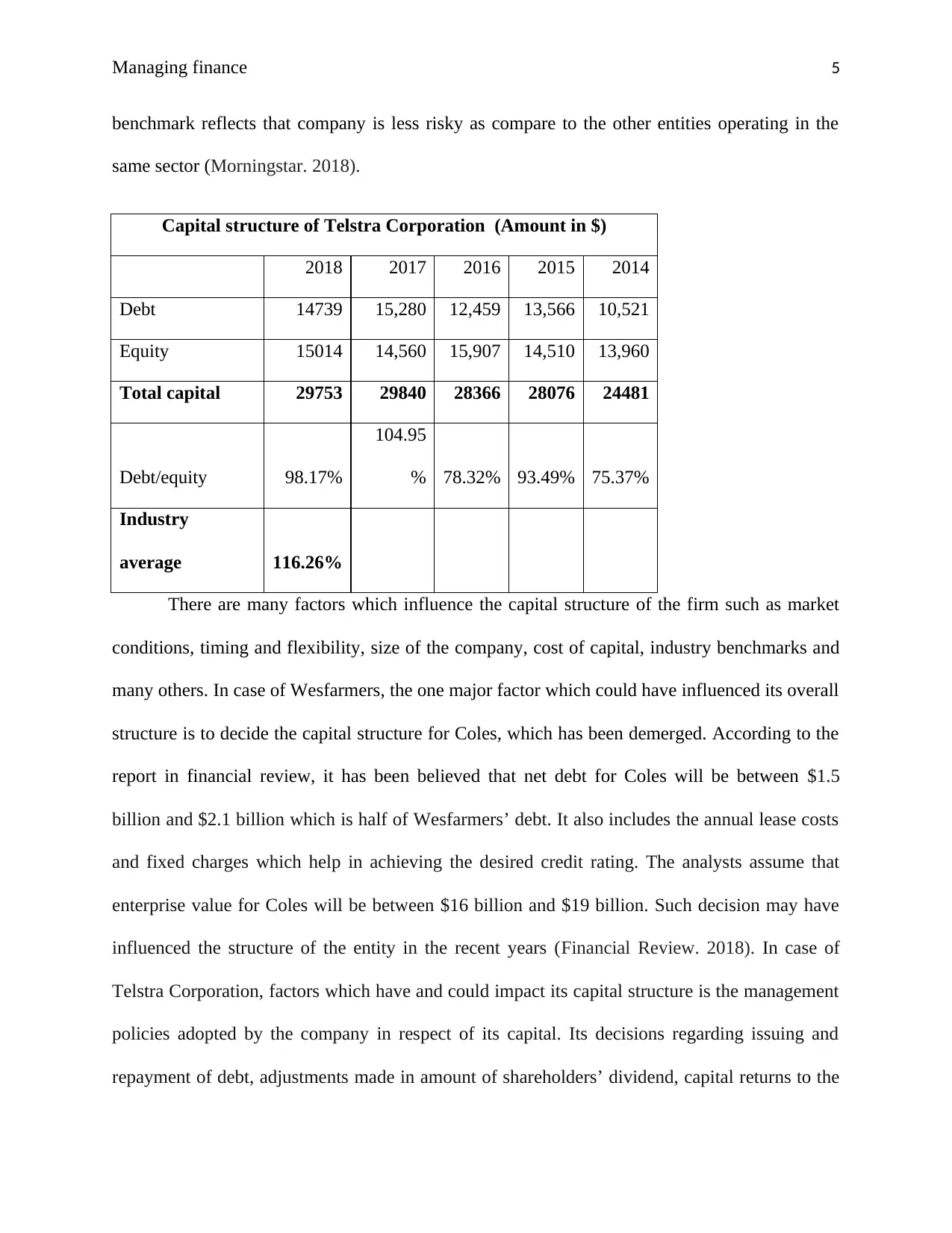

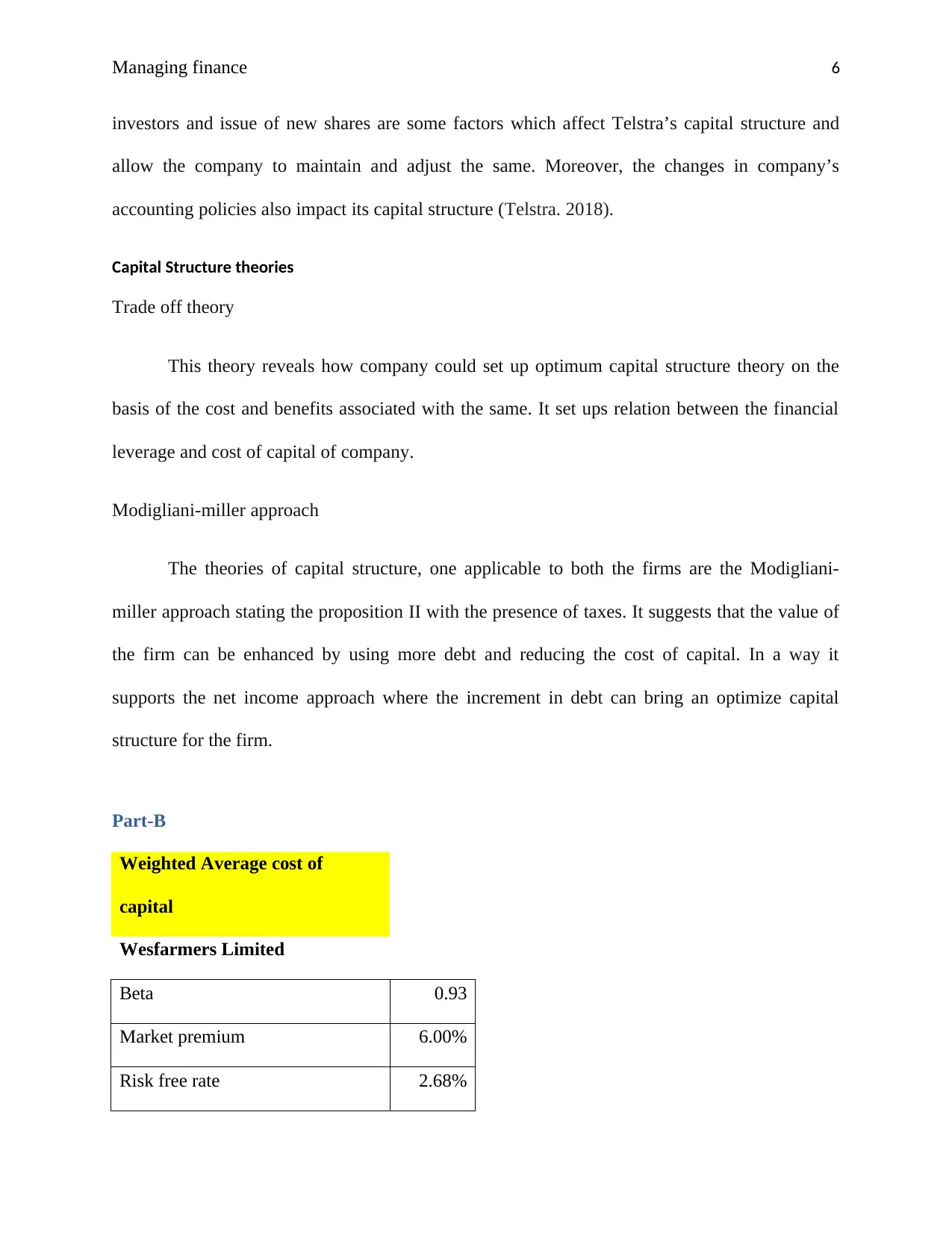

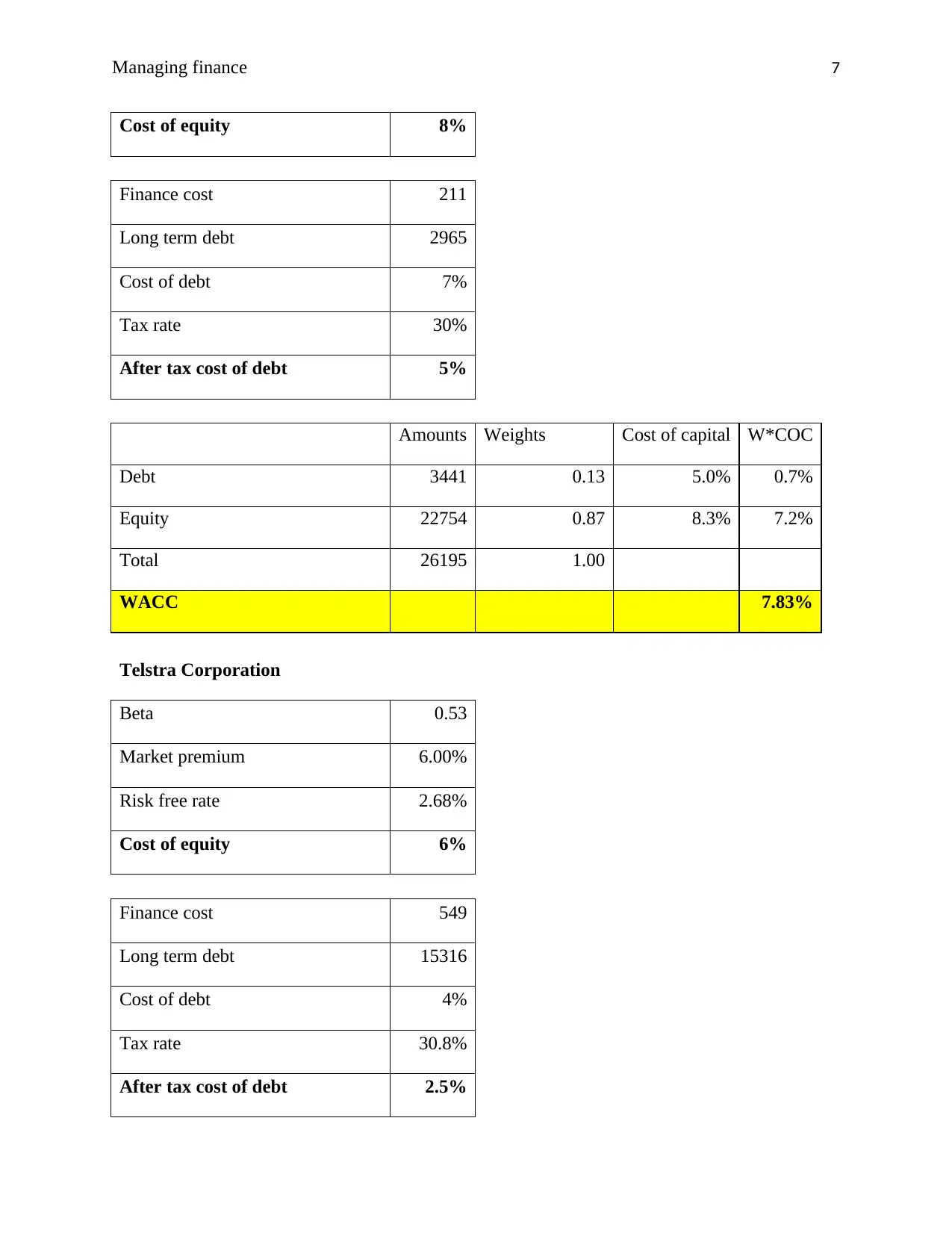

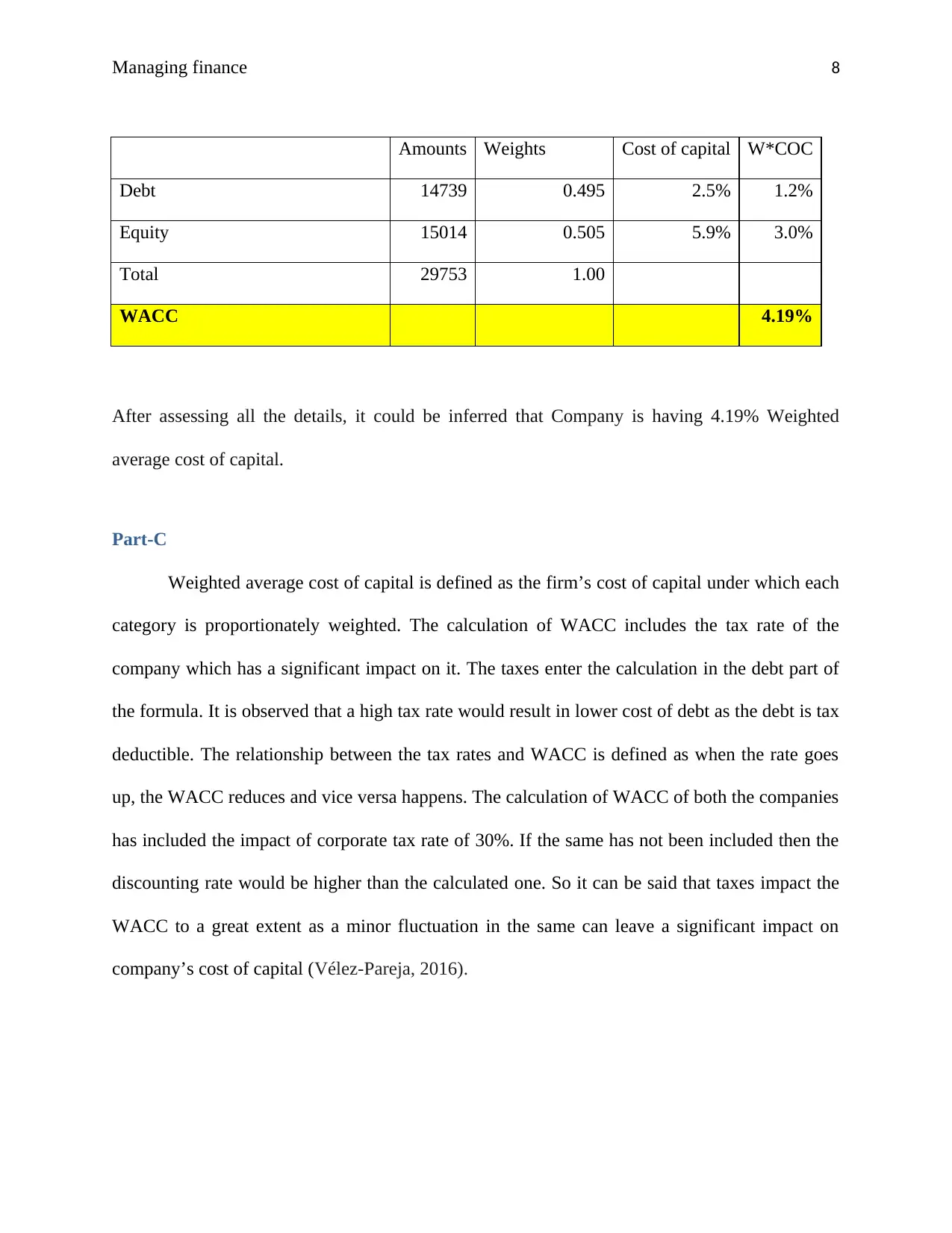

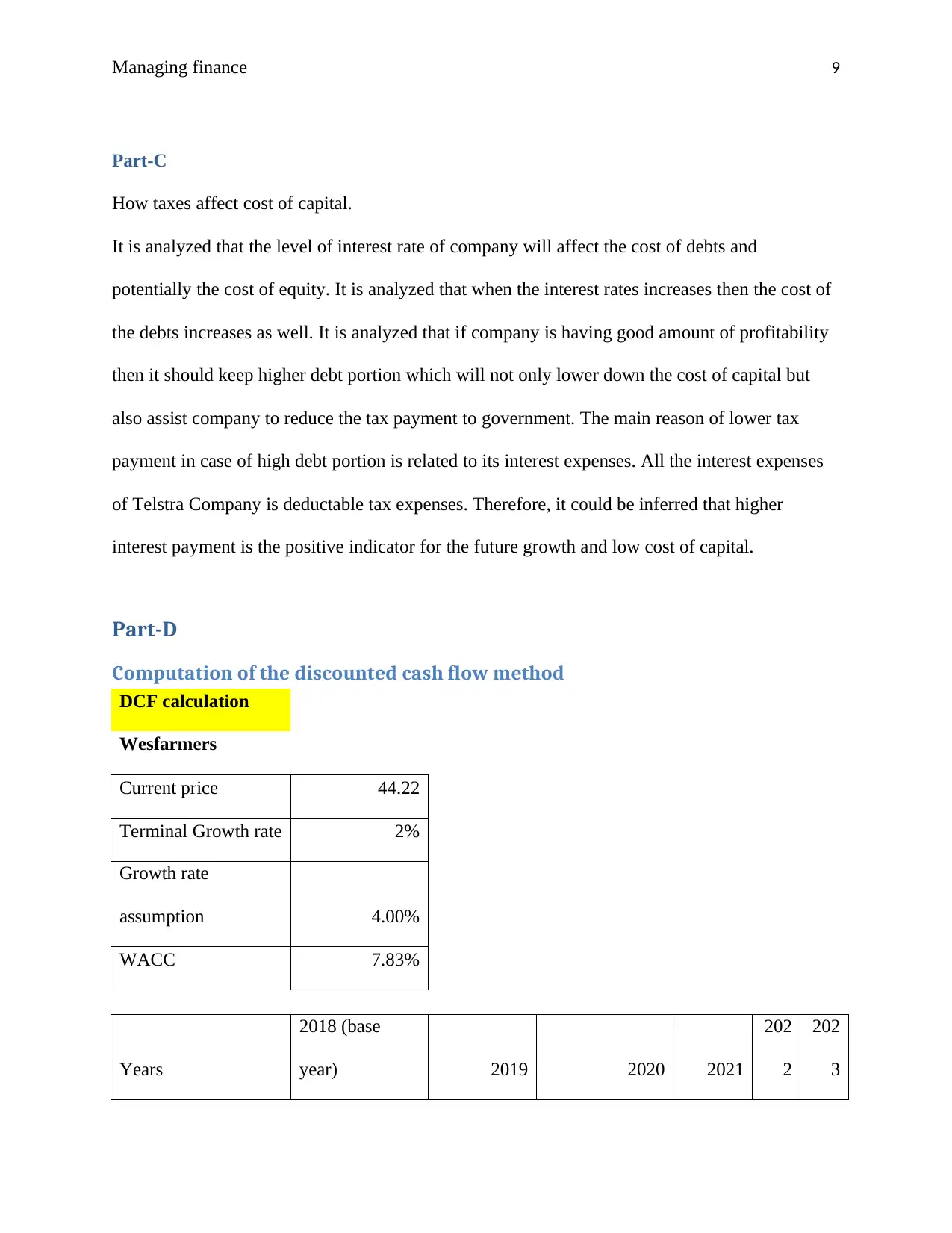

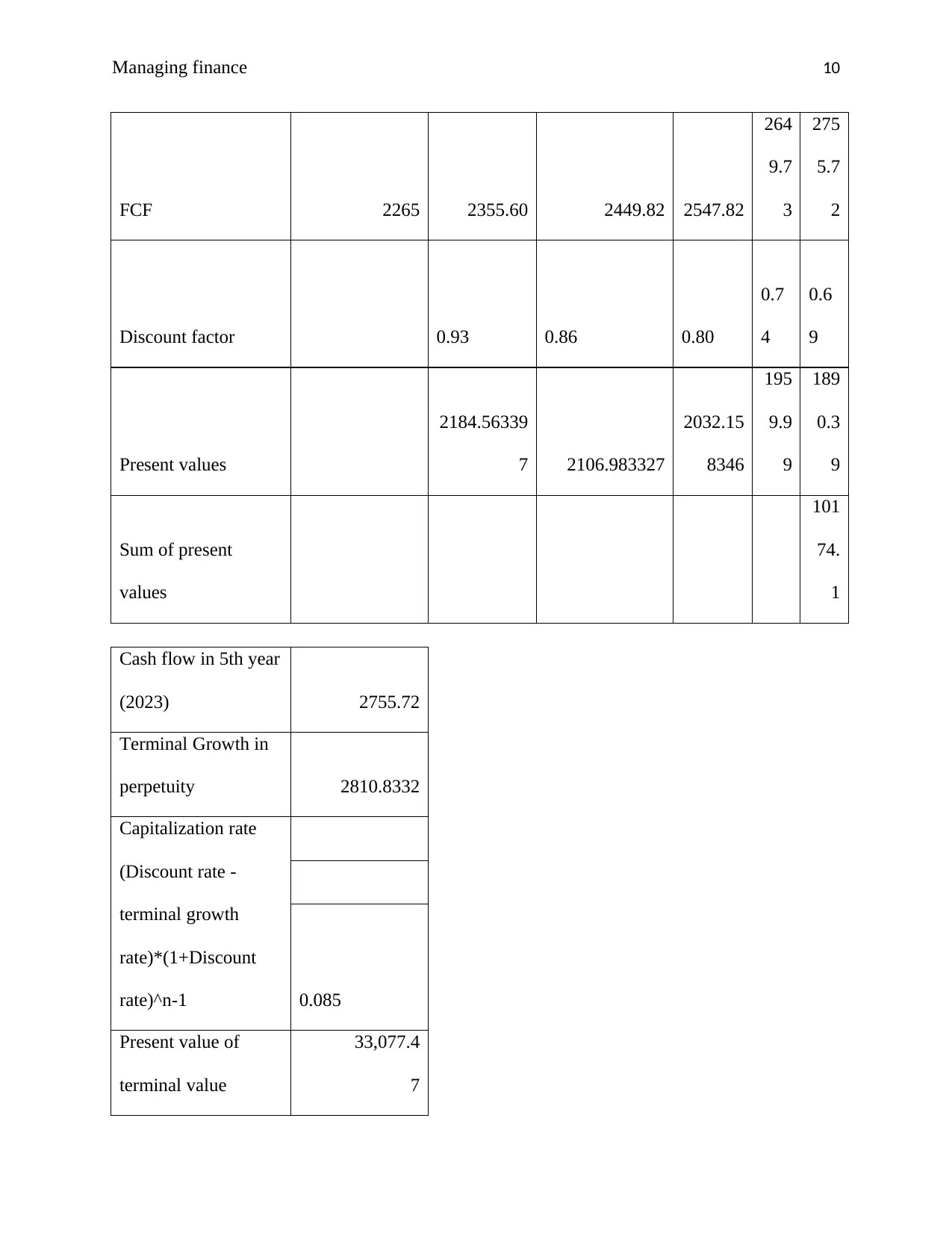

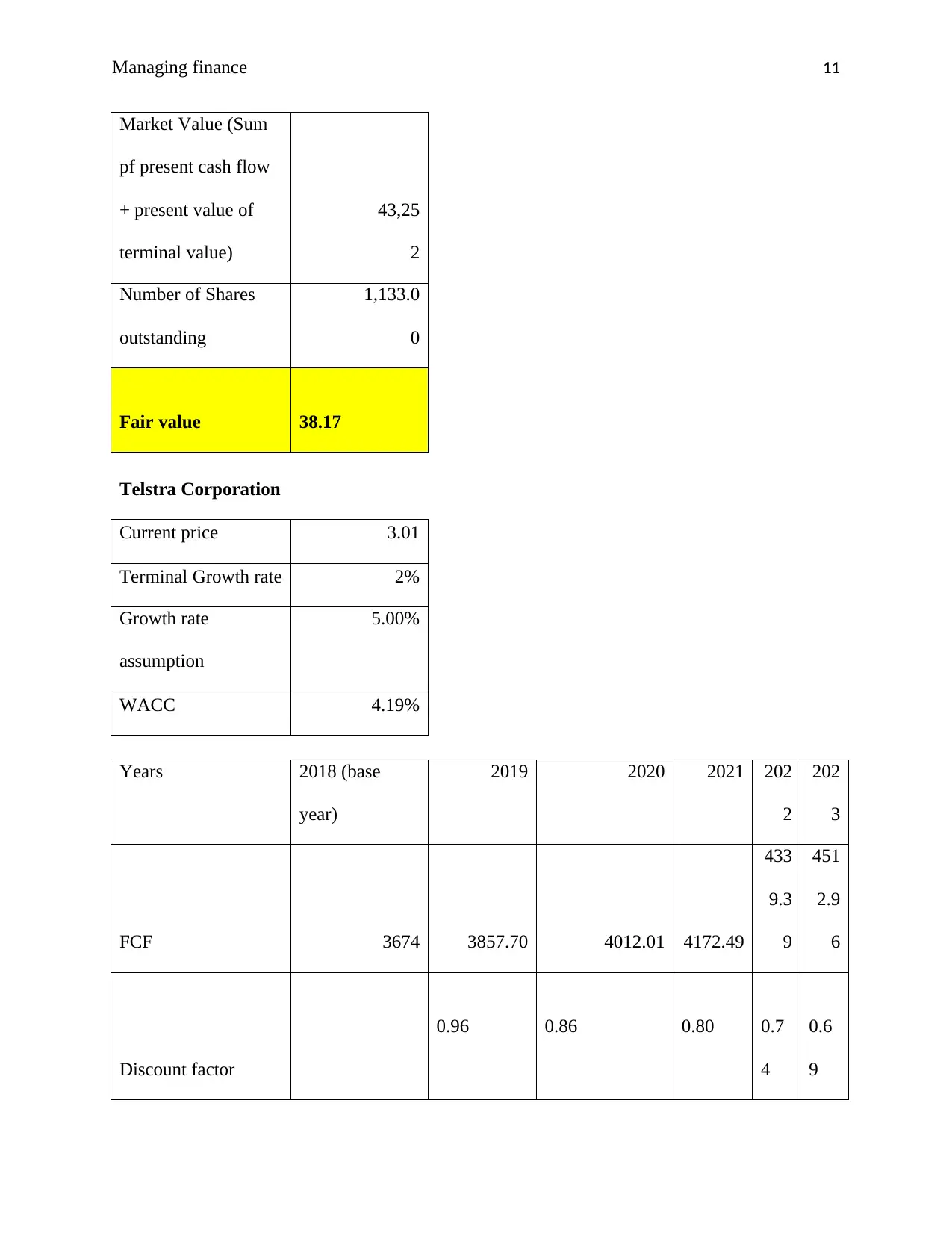

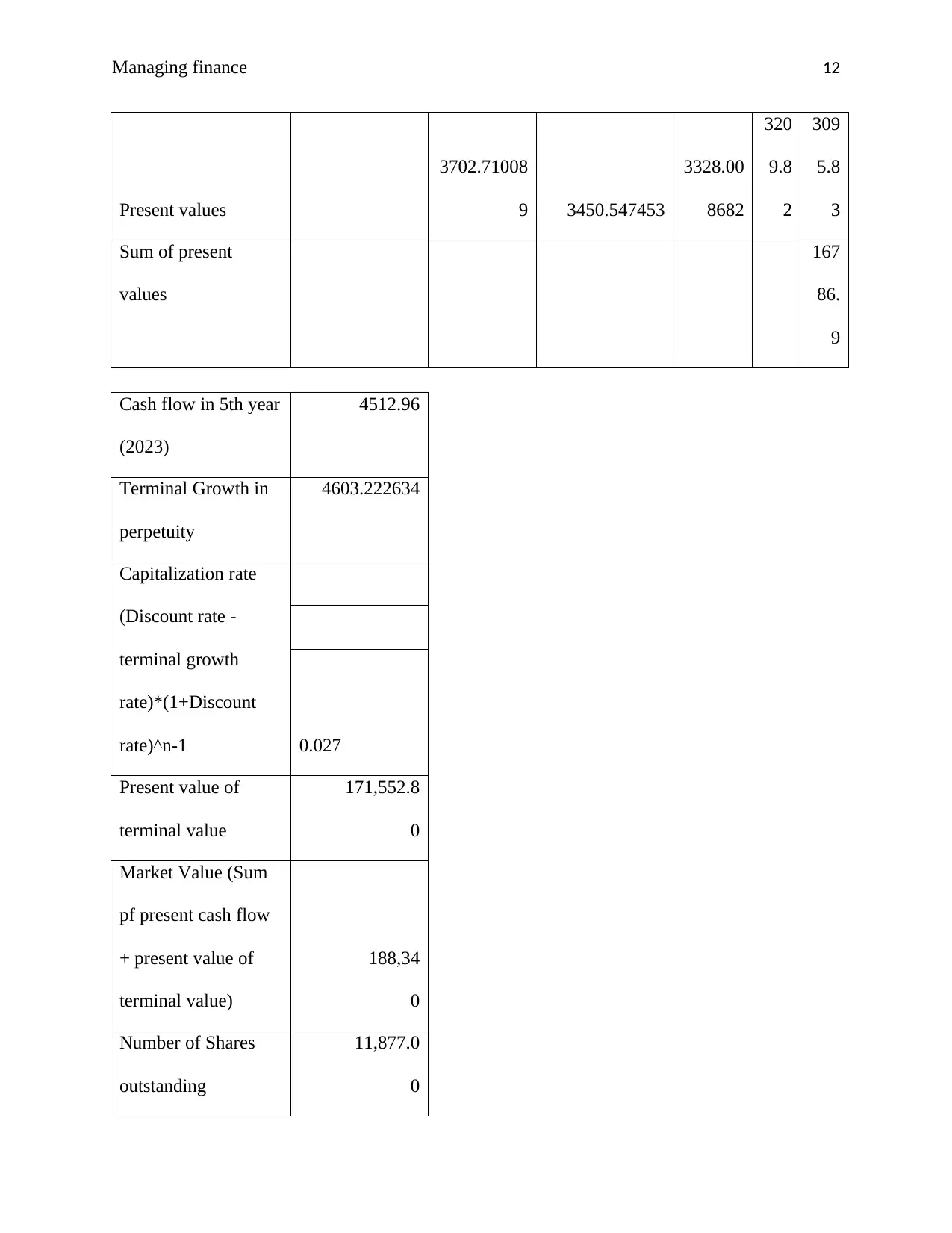

This case study undertakes a comprehensive financial analysis of two Australian companies, Telstra and Wesfarmers, focusing on their capital structures, valuation methods, and financial performance. The analysis includes an examination of each company's capital structure over a five-year period, considering factors like debt-to-equity ratios and industry benchmarks. The study then delves into the weighted average cost of capital (WACC) for both companies, highlighting the impact of tax rates on the cost of debt. Furthermore, the discounted cash flow (DCF) method is applied to estimate the fair value of each company's stock, considering growth rates and terminal values. The report also employs a relative valuation method using price-earnings, price-to-book, and price-to-sales ratios to assess the companies' valuations relative to their industry averages. The findings offer insights into the companies' financial health, investment potential, and the influence of various financial metrics on their market values.

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.