Capital Asset Pricing Model: Strengths, Weaknesses, and Alternatives

VerifiedAdded on 2023/01/10

|12

|2919

|36

Essay

AI Summary

This essay provides a comprehensive overview of the Capital Asset Pricing Model (CAPM), a crucial tool for businesses to determine the cost of capital. It delves into the model's core concepts, including the calculation of the cost of equity capital, the role of beta, and the relationship between risk and return. The essay critically examines the criticisms of CAPM, such as the assumption of a true market portfolio, the use of historical data for beta calculation, and the assumption of risk-free borrowing. It also explores alternative models and the continued importance of CAPM in practical financial decision-making, discussing its advantages and the insights it offers for portfolio management and investment analysis. The paper concludes by highlighting the CAPM's enduring relevance despite its limitations.

1

Strategic Finance

Strategic Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Table of Contents

Introduction to CAPM.....................................................................................................................3

Criticisms of Model.........................................................................................................................4

Assumption of true market portfolio...........................................................................................4

Assumption of Beta.....................................................................................................................4

Argument for future cash flows...................................................................................................5

Concern in relation to risk free borrowing assumption...............................................................5

Alternative model............................................................................................................................6

Importance of CAPM......................................................................................................................6

Advantages of CAPM......................................................................................................................7

Conclusion.......................................................................................................................................9

References......................................................................................................................................11

Table of Contents

Introduction to CAPM.....................................................................................................................3

Criticisms of Model.........................................................................................................................4

Assumption of true market portfolio...........................................................................................4

Assumption of Beta.....................................................................................................................4

Argument for future cash flows...................................................................................................5

Concern in relation to risk free borrowing assumption...............................................................5

Alternative model............................................................................................................................6

Importance of CAPM......................................................................................................................6

Advantages of CAPM......................................................................................................................7

Conclusion.......................................................................................................................................9

References......................................................................................................................................11

3

Introduction to CAPM

Capital asset pricing model is the technique which is used by the businesses for the

ascertainment of the cost of capital for their entity. This is very useful and so it is necessary that

all the information in this relationship shall be identified. The essay will be representing the

manner in which this is useful with the undertaken assumptions also. All of the aspects are

covered and in that the assumptions which are involved will also be undertaken. This is the

technique which will be of great use for the business as will also be helpful in the making of

various decisions which are relevant for the business (Chong, Jin and Phillips, 2014). This is the

model in which the risk and return both are taken into account and by that the relation among

them is identified. There will be consideration of all the elements which are involved in relation

to them. By that, the calculation of the rate of capital is made which is attained after involving all

the aspects and so is the accurate one. In this, the risk premium and beta both are taken into

account so that all the uncertainties involved are determined and involved in advance. There is

the involvement of the systematic risk in this and due to that, it is widely used (Fama and French,

2012). By the help of this, the impact of the diversification and other elements on the returns is

eliminated. There is the sensitivity which is involved in relation to the return which is obtained

on the stock in comparison to the market portfolio and for that the beta is taken into

consideration. It is taken into consideration in this model that the beta will be the main factor in

the determination of the cost of equity capital for investors. There is the formula which is used

for the calculation of the same in which the risk-free rate, risk premium, and beta are taken into

use. The beta will be multiplied with the risk premium and then the outcome will be added to the

risk-free rate. The result which will be attained is identified as the cost of equity capital.

Introduction to CAPM

Capital asset pricing model is the technique which is used by the businesses for the

ascertainment of the cost of capital for their entity. This is very useful and so it is necessary that

all the information in this relationship shall be identified. The essay will be representing the

manner in which this is useful with the undertaken assumptions also. All of the aspects are

covered and in that the assumptions which are involved will also be undertaken. This is the

technique which will be of great use for the business as will also be helpful in the making of

various decisions which are relevant for the business (Chong, Jin and Phillips, 2014). This is the

model in which the risk and return both are taken into account and by that the relation among

them is identified. There will be consideration of all the elements which are involved in relation

to them. By that, the calculation of the rate of capital is made which is attained after involving all

the aspects and so is the accurate one. In this, the risk premium and beta both are taken into

account so that all the uncertainties involved are determined and involved in advance. There is

the involvement of the systematic risk in this and due to that, it is widely used (Fama and French,

2012). By the help of this, the impact of the diversification and other elements on the returns is

eliminated. There is the sensitivity which is involved in relation to the return which is obtained

on the stock in comparison to the market portfolio and for that the beta is taken into

consideration. It is taken into consideration in this model that the beta will be the main factor in

the determination of the cost of equity capital for investors. There is the formula which is used

for the calculation of the same in which the risk-free rate, risk premium, and beta are taken into

use. The beta will be multiplied with the risk premium and then the outcome will be added to the

risk-free rate. The result which will be attained is identified as the cost of equity capital.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

Criticisms of Model

The relationship which is present among all of them is identified and understood in an effective

manner by the help of this model. There are several criticisms which have been faced by the

CAPM model in relation to its validity (Zabarankin, Pavlikov, and Uryasev, 2014). The making

of the capital asset pricing model is dependent on certain assumptions which were used in its

formulation. This is one of the best models and provides accurate results and then also faces the

issues. It has been argued by many people that the model is not appropriate due to a large

number of assumptions which are made under this.

Assumption of true market portfolio

In this model, it is assumed that there is a true market portfolio and according to Richard roll,

this is not possible as there is no such portfolio (Roll, 1977). Due to this, the model is considered

to be inaccurate and inadequate by him. It has been provided by him that a portfolio will be

considered to be diversified only if there has been consideration of all the investments which

have been made in all the assets and that too covered in the whole world. In accordance with this,

the method of incorporating the inefficient market proxies is inefficient which is used in CAPM

as there is not the involvement of all the financial assets into this. Therefore the use of mean-

variance in this is not correct and by that, the perfect employee will be represented as less

efficient.

Assumption of Beta

Another argument which was posted against the capital asset pricing model is that the capital

structure which is there in the company changes from time to time but the beta value which is

Criticisms of Model

The relationship which is present among all of them is identified and understood in an effective

manner by the help of this model. There are several criticisms which have been faced by the

CAPM model in relation to its validity (Zabarankin, Pavlikov, and Uryasev, 2014). The making

of the capital asset pricing model is dependent on certain assumptions which were used in its

formulation. This is one of the best models and provides accurate results and then also faces the

issues. It has been argued by many people that the model is not appropriate due to a large

number of assumptions which are made under this.

Assumption of true market portfolio

In this model, it is assumed that there is a true market portfolio and according to Richard roll,

this is not possible as there is no such portfolio (Roll, 1977). Due to this, the model is considered

to be inaccurate and inadequate by him. It has been provided by him that a portfolio will be

considered to be diversified only if there has been consideration of all the investments which

have been made in all the assets and that too covered in the whole world. In accordance with this,

the method of incorporating the inefficient market proxies is inefficient which is used in CAPM

as there is not the involvement of all the financial assets into this. Therefore the use of mean-

variance in this is not correct and by that, the perfect employee will be represented as less

efficient.

Assumption of Beta

Another argument which was posted against the capital asset pricing model is that the capital

structure which is there in the company changes from time to time but the beta value which is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

taken into use is calculated with the help of the historical data. It does not cover all the changes

which have been made and also the expected market return is based on the estimate in which

there are high chances of having an error.

Argument for future cash flows

The argument has been made against the assumption which is present in respect of the future

cash flows. It is assumed under this method that the future cash flows which will be available

with the business can be estimated by the company (Dayala, 2012). It is criticized that if the

ascertainment of the cash flows can be made in an accurate manner then the need for the

calculation of the cost of capital does not arise. The main issue is with the identification of the

cash flows for the coming period and if that is done accurately then the need will eliminate to use

the capital asset, pricing model.

Concern in relation to risk free borrowing assumption

It is also considered in the calculation under CAPM that it is possible for the investors to make

the borrowing at the risk-free rate which is not possible in the practical world. This is also a

major concern and for that, the same is taken into account while considering the issue so that the

required decision can be made. There is no party in the market who will be providing the funds

at the risk-free rate as every person is sitting to earn the profits and so there will be some interest

which will have to be earned by them (Berk and Van Binsbergen, 2016). Due to that, there will

be some addition which will be made to the risk-free rate and the same will be charged from all

the borrowers. By this, the interest of all will be considered and no party will be at disadvantage.

There is the need to consider such aspects and the focus shall be made on that so that the

assumptions which are involved and are practically impossible can be focused. There will be an

action which will be taken to eliminate the impact of the same or to minimize the result of it.

taken into use is calculated with the help of the historical data. It does not cover all the changes

which have been made and also the expected market return is based on the estimate in which

there are high chances of having an error.

Argument for future cash flows

The argument has been made against the assumption which is present in respect of the future

cash flows. It is assumed under this method that the future cash flows which will be available

with the business can be estimated by the company (Dayala, 2012). It is criticized that if the

ascertainment of the cash flows can be made in an accurate manner then the need for the

calculation of the cost of capital does not arise. The main issue is with the identification of the

cash flows for the coming period and if that is done accurately then the need will eliminate to use

the capital asset, pricing model.

Concern in relation to risk free borrowing assumption

It is also considered in the calculation under CAPM that it is possible for the investors to make

the borrowing at the risk-free rate which is not possible in the practical world. This is also a

major concern and for that, the same is taken into account while considering the issue so that the

required decision can be made. There is no party in the market who will be providing the funds

at the risk-free rate as every person is sitting to earn the profits and so there will be some interest

which will have to be earned by them (Berk and Van Binsbergen, 2016). Due to that, there will

be some addition which will be made to the risk-free rate and the same will be charged from all

the borrowers. By this, the interest of all will be considered and no party will be at disadvantage.

There is the need to consider such aspects and the focus shall be made on that so that the

assumptions which are involved and are practically impossible can be focused. There will be an

action which will be taken to eliminate the impact of the same or to minimize the result of it.

6

Alternative model

The CAPM model was made with various expectations but they were not fulfilled due to various

inefficiencies involved in it (Johnstone, 2016). The model includes many such assumptions and

is based on the market portfolio theory and due to this, there are several challenges as there is

difficulty in testing the involved requirements. There are many such users who are in favor of the

model and they argue that in spite of various assumptions the model can be used in a successful

manner as it provides accurate results. There are many models which have been developed as the

alternative of the model and one of them is three-factor models. In CAPM there is only one

variable which is covered and to eliminate this limitation the three variable models has been

prepared in which there are three variables which are taken into consideration by which the stock

returns are explained (Sundaresan, 2013). According to this model the stock return itself is not

only the one factor and in addition to this book to market ratio and market capitalization there

was a relation which was identified by the help of this model and it stated that there is higher

return which is attained in the stocks which have small-cap stock or ones which have higher

book to market ratios. By the help of this, it was proved that in the calculation of the return there

is more importance of the two variables than that of the beta which is included in the capital asset

pricing model.

Importance of CAPM

In the practical world, the CAPM is still more important and used by the companies and is not

affected by the inefficiencies which are identified by many people in it. There is the paper which

is presented by Harvey and Graham and according to that, there are still 73.49% people who are

using the CAPM model and are satisfied with the results which are provided by it (Dempsey,

2013). In the market, there are different practitioners who are having various views and it is not

Alternative model

The CAPM model was made with various expectations but they were not fulfilled due to various

inefficiencies involved in it (Johnstone, 2016). The model includes many such assumptions and

is based on the market portfolio theory and due to this, there are several challenges as there is

difficulty in testing the involved requirements. There are many such users who are in favor of the

model and they argue that in spite of various assumptions the model can be used in a successful

manner as it provides accurate results. There are many models which have been developed as the

alternative of the model and one of them is three-factor models. In CAPM there is only one

variable which is covered and to eliminate this limitation the three variable models has been

prepared in which there are three variables which are taken into consideration by which the stock

returns are explained (Sundaresan, 2013). According to this model the stock return itself is not

only the one factor and in addition to this book to market ratio and market capitalization there

was a relation which was identified by the help of this model and it stated that there is higher

return which is attained in the stocks which have small-cap stock or ones which have higher

book to market ratios. By the help of this, it was proved that in the calculation of the return there

is more importance of the two variables than that of the beta which is included in the capital asset

pricing model.

Importance of CAPM

In the practical world, the CAPM is still more important and used by the companies and is not

affected by the inefficiencies which are identified by many people in it. There is the paper which

is presented by Harvey and Graham and according to that, there are still 73.49% people who are

using the CAPM model and are satisfied with the results which are provided by it (Dempsey,

2013). In the market, there are different practitioners who are having various views and it is not

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

possible to satisfy the requirement of all. If one aspect will be included and it will be improved

then the other will raise another issue (Kan, Robotti and Shanken, 2013). In the financial market,

there are several variables and the changes also take place on a continuous basis. It will be

required that there shall be the adoption of the one technique as the changes which happen on a

regular basis are not possible to be taken into account. There will be one or the aspect which will

be changing and so the assumptions which are made under the capital asset pricing model are not

irrelevant and will be required to be taken into account. The equation which is used in this

includes the risk free rate and risk premium together with the beta. By them the rate will be

calculated which is used for the decision making. The calculation can be made by that such as a

company has beta of 0.6 and risk free rate is 10%. The risk premium is identified to be 15%. The

calculation for the same will be as follows:

Ke = Rf + b (Rm – Rf)

= 10 + 0.6 * 15

= 19%

This will be the rate which will be treated as the rate of equity and the same will be used by the

business for the further calculation.

Advantages of CAPM

There is an easy process which is involved in the calculation of CAPM and also the comparison

is made possible among all the investment proposals which are available. Due to this, it is used

in a wider manner among all the companies (Elbannan, 2015). Another assumption which is

made in the capital asset pricing model is in relation to the risk-free rate. It is assumed that over

possible to satisfy the requirement of all. If one aspect will be included and it will be improved

then the other will raise another issue (Kan, Robotti and Shanken, 2013). In the financial market,

there are several variables and the changes also take place on a continuous basis. It will be

required that there shall be the adoption of the one technique as the changes which happen on a

regular basis are not possible to be taken into account. There will be one or the aspect which will

be changing and so the assumptions which are made under the capital asset pricing model are not

irrelevant and will be required to be taken into account. The equation which is used in this

includes the risk free rate and risk premium together with the beta. By them the rate will be

calculated which is used for the decision making. The calculation can be made by that such as a

company has beta of 0.6 and risk free rate is 10%. The risk premium is identified to be 15%. The

calculation for the same will be as follows:

Ke = Rf + b (Rm – Rf)

= 10 + 0.6 * 15

= 19%

This will be the rate which will be treated as the rate of equity and the same will be used by the

business for the further calculation.

Advantages of CAPM

There is an easy process which is involved in the calculation of CAPM and also the comparison

is made possible among all the investment proposals which are available. Due to this, it is used

in a wider manner among all the companies (Elbannan, 2015). Another assumption which is

made in the capital asset pricing model is in relation to the risk-free rate. It is assumed that over

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

the complete discounting period the rate will be remaining constant which is practically not

possible. There are various changes which are involved in the rate and they are needed to be

included as by that the cost of capital which is calculated is affected.

All of these issues have been raised but then also the capital asset pricing model is used by the

majority of the businesses as they have faith in the result which is provided by it. By the help of

CAPM, it will be possible for the investors to reduce the risk which is involved in the portfolio

management (Eisfeldt and Papanikolaou, 2013). They will be able to make the portfolio in such a

manner that the risk can be avoided and by this, it will be on the efficient frontier. There is still

the value of the model as this will be helpful in various processes which are undertaken and will

be providing the business with the positive results. The evaluation of the portfolio will be made

possible by the help of this model and also the comparison of the performance of any single

stock can also be made with the complete market.

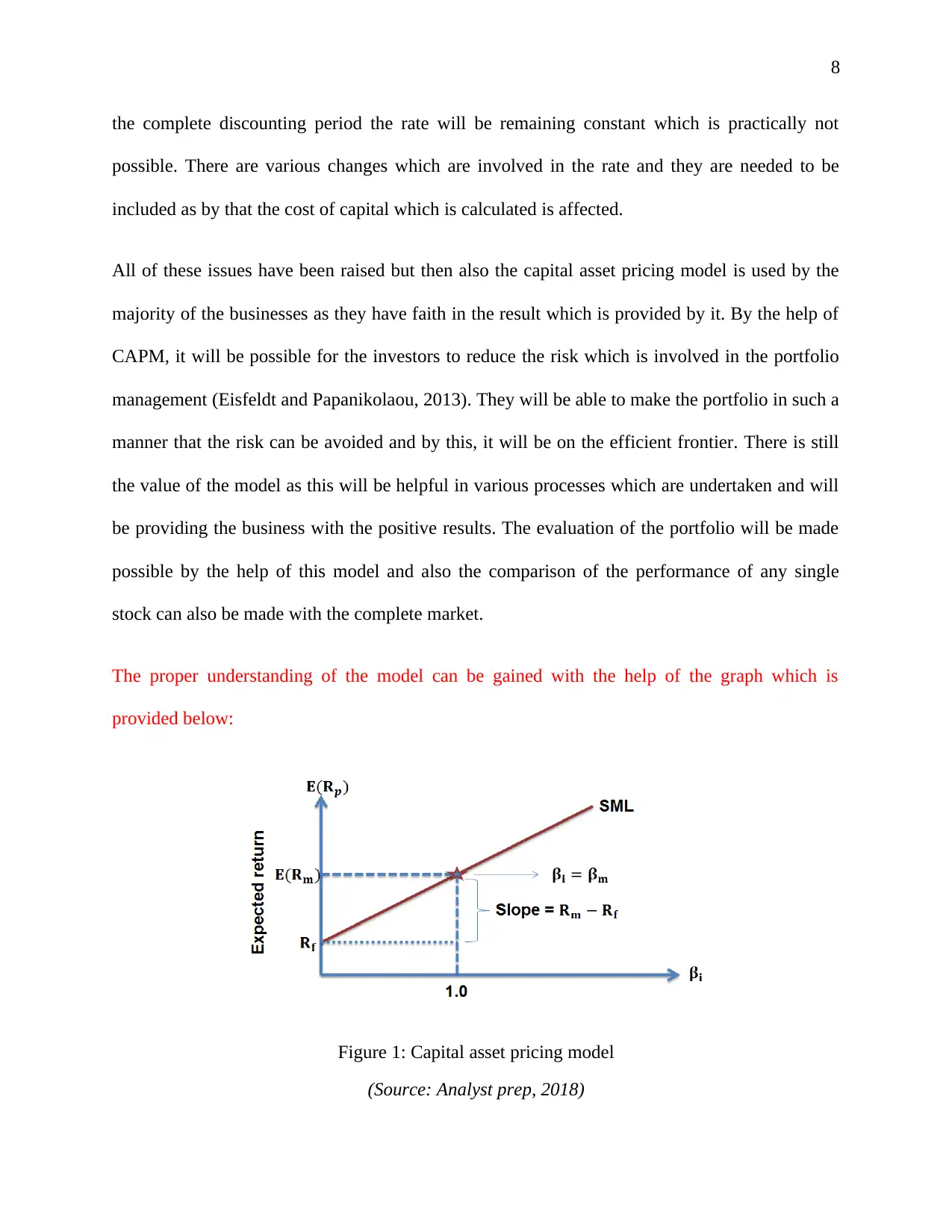

The proper understanding of the model can be gained with the help of the graph which is

provided below:

Figure 1: Capital asset pricing model

(Source: Analyst prep, 2018)

the complete discounting period the rate will be remaining constant which is practically not

possible. There are various changes which are involved in the rate and they are needed to be

included as by that the cost of capital which is calculated is affected.

All of these issues have been raised but then also the capital asset pricing model is used by the

majority of the businesses as they have faith in the result which is provided by it. By the help of

CAPM, it will be possible for the investors to reduce the risk which is involved in the portfolio

management (Eisfeldt and Papanikolaou, 2013). They will be able to make the portfolio in such a

manner that the risk can be avoided and by this, it will be on the efficient frontier. There is still

the value of the model as this will be helpful in various processes which are undertaken and will

be providing the business with the positive results. The evaluation of the portfolio will be made

possible by the help of this model and also the comparison of the performance of any single

stock can also be made with the complete market.

The proper understanding of the model can be gained with the help of the graph which is

provided below:

Figure 1: Capital asset pricing model

(Source: Analyst prep, 2018)

9

It can be seen that there is the risk free rate and also the risk premium is available. The point

where the beta is 1 is the place where the beta of investment and market will be equal. They

determine the systematic risk which is present and thus the decisions can be made accordingly.

The risk free rate will be added to this so that the return on the equity is determined.

The securities which will not be providing the investors with the benefit will be determined with

the help of this and that will be in the interest of the investors as they will be able to take the

decision accordingly. All the non-beneficial stocks will be eliminated from the portfolio so that

overall returns of the investors are maintained and no adverse impact is faced by them. There

will be steps which will be taken so that the risk which is involved will be affecting the returns

can be determined and the corrective actions can be made in respect of them.

Conclusion

After the complete evaluation, it can be concluded that the problems which are involved in

Capital asset pricing model are involved in almost all the financial models which are available in

the market. The other models such as the dividend growth model and various others also include

some of the issues and the cost of equity which is calculated with the help of CAPM is better and

there is no harm in using this model. This can be used by the businesses and the result which will

be attained from the use of it is reliable and companies can rely on the same. They can take the

decision on the basis of the cost of capital which is calculated under this approach and that will

be the most adequate and accurate one. No issue will be arising by the use of it and there will be

no adverse impact which will have to be faced. Due to all of these arguments, it can be said that

although there are a various assumption and many people criticize the same then also the

It can be seen that there is the risk free rate and also the risk premium is available. The point

where the beta is 1 is the place where the beta of investment and market will be equal. They

determine the systematic risk which is present and thus the decisions can be made accordingly.

The risk free rate will be added to this so that the return on the equity is determined.

The securities which will not be providing the investors with the benefit will be determined with

the help of this and that will be in the interest of the investors as they will be able to take the

decision accordingly. All the non-beneficial stocks will be eliminated from the portfolio so that

overall returns of the investors are maintained and no adverse impact is faced by them. There

will be steps which will be taken so that the risk which is involved will be affecting the returns

can be determined and the corrective actions can be made in respect of them.

Conclusion

After the complete evaluation, it can be concluded that the problems which are involved in

Capital asset pricing model are involved in almost all the financial models which are available in

the market. The other models such as the dividend growth model and various others also include

some of the issues and the cost of equity which is calculated with the help of CAPM is better and

there is no harm in using this model. This can be used by the businesses and the result which will

be attained from the use of it is reliable and companies can rely on the same. They can take the

decision on the basis of the cost of capital which is calculated under this approach and that will

be the most adequate and accurate one. No issue will be arising by the use of it and there will be

no adverse impact which will have to be faced. Due to all of these arguments, it can be said that

although there are a various assumption and many people criticize the same then also the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

companies can use the capital asset pricing method and this will be considered to be one of the

best models in the financial market.

companies can use the capital asset pricing method and this will be considered to be one of the

best models in the financial market.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

References

Analyst prep. (2018) The Capital Asset Pricing Model. [Online] Available at:

https://analystprep.com/study-notes/frm/part-1/the-capital-asset-pricing-model/ [Accessed 18

June 2019]

Berk, J.B. and Van Binsbergen, J.H. (2016) Assessing asset pricing models using revealed

preference. Journal of Financial Economics, 119(1), pp.1-23.

Chong, J., Jin, Y. and Phillips, G. (2014) The Entrepreneur's Cost of Capital: Incorporating

Downside Risk. Business Valuation Review, 33(3), pp.81-91.

Dayala, R. (2012) The capital asset pricing model: A fundamental critique. Business Valuation

Review, 31(1), pp.23-34.

Dempsey, M. (2013) The capital asset pricing model (CAPM): the history of a failed

revolutionary idea in finance?. Abacus, 49, pp.7-23.

Eisfeldt, A.L., and Papanikolaou, D. (2013) Organization capital and the cross‐section of

expected returns. The Journal of Finance, 68(4), pp.1365-1406.

Elbannan, M.A. (2015) The capital asset pricing model: an overview of the theory. International

Journal of Economics and Finance, 7(1), pp.216-228.

Fama, E.F. and French, K.R. (2012) Size, value, and momentum in international stock

returns. Journal of financial economics, 105(3), pp.457-472.

References

Analyst prep. (2018) The Capital Asset Pricing Model. [Online] Available at:

https://analystprep.com/study-notes/frm/part-1/the-capital-asset-pricing-model/ [Accessed 18

June 2019]

Berk, J.B. and Van Binsbergen, J.H. (2016) Assessing asset pricing models using revealed

preference. Journal of Financial Economics, 119(1), pp.1-23.

Chong, J., Jin, Y. and Phillips, G. (2014) The Entrepreneur's Cost of Capital: Incorporating

Downside Risk. Business Valuation Review, 33(3), pp.81-91.

Dayala, R. (2012) The capital asset pricing model: A fundamental critique. Business Valuation

Review, 31(1), pp.23-34.

Dempsey, M. (2013) The capital asset pricing model (CAPM): the history of a failed

revolutionary idea in finance?. Abacus, 49, pp.7-23.

Eisfeldt, A.L., and Papanikolaou, D. (2013) Organization capital and the cross‐section of

expected returns. The Journal of Finance, 68(4), pp.1365-1406.

Elbannan, M.A. (2015) The capital asset pricing model: an overview of the theory. International

Journal of Economics and Finance, 7(1), pp.216-228.

Fama, E.F. and French, K.R. (2012) Size, value, and momentum in international stock

returns. Journal of financial economics, 105(3), pp.457-472.

12

Johnstone, D. (2016) The effect of information on uncertainty and the cost of

capital. Contemporary Accounting Research, 33(2), pp.752-774.

Kan, R., Robotti, C., and Shanken, J. (2013) Pricing model performance and the two‐pass cross‐

sectional regression methodology. The Journal of Finance, 68(6), pp.2617-2649.

Roll, R. (1977) A critique of the asset pricing theory's tests Part I: On past and potential

testability of the theory. Journal of financial economics, 4(2), pp.129-176.

Sundaresan, S. (2013) A review of Merton’s model of the firm’s capital structure with its wide

applications. Annu. Rev. Financ. Econ., 5(1), pp.21-41.

Zabarankin, M., Pavlikov, K. and Uryasev, S. (2014) Capital asset pricing model (CAPM) with

drawdown measure. European Journal of Operational Research, 234(2), pp.508-517.

Johnstone, D. (2016) The effect of information on uncertainty and the cost of

capital. Contemporary Accounting Research, 33(2), pp.752-774.

Kan, R., Robotti, C., and Shanken, J. (2013) Pricing model performance and the two‐pass cross‐

sectional regression methodology. The Journal of Finance, 68(6), pp.2617-2649.

Roll, R. (1977) A critique of the asset pricing theory's tests Part I: On past and potential

testability of the theory. Journal of financial economics, 4(2), pp.129-176.

Sundaresan, S. (2013) A review of Merton’s model of the firm’s capital structure with its wide

applications. Annu. Rev. Financ. Econ., 5(1), pp.21-41.

Zabarankin, M., Pavlikov, K. and Uryasev, S. (2014) Capital asset pricing model (CAPM) with

drawdown measure. European Journal of Operational Research, 234(2), pp.508-517.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.