Theoretical Analysis of CAPM Model - University Name, PC-AS0197

VerifiedAdded on 2023/06/05

|14

|2498

|284

Report

AI Summary

This report provides a comprehensive analysis of the Capital Asset Pricing Model (CAPM), examining its application in risk and return assessment for investment decisions. It evaluates systematic and unsystematic risks, discusses problems and critiques of the CAPM model, and explores its assumptions. The report also highlights the model's utility for investors compared to other financial analysis tools, referencing the CAPM equation and its components such as risk-free rate, beta, and market premium. It emphasizes the importance of balancing risk and return, utilizing capital market lines, and considering both realistic and unrealistic assumptions when evaluating investment projects. The conclusion underscores the CAPM model's usefulness in determining investment options and profitability, while referencing alternative models like Arbitrage Pricing Theory. Desklib provides access to this and other solved assignments for students.

CAPM

[Type the document title]

Theoretical model analysis

PC-AS0197

University Name-

[Type the document title]

Theoretical model analysis

PC-AS0197

University Name-

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction.................................................................................................................................................2

Risk and return analysis in CAPM Model...................................................................................................2

Evaluation of the systematic, undiversified risk, and unsystematic risk......................................................3

Problems in the CAPM model.....................................................................................................................4

Critique of CAPM.......................................................................................................................................5

What are the main assumption of CAPM and why it is mostly used by investors as compared to other

financial analysis tool..................................................................................................................................6

Conclusion...................................................................................................................................................7

References...................................................................................................................................................8

Introduction.................................................................................................................................................2

Risk and return analysis in CAPM Model...................................................................................................2

Evaluation of the systematic, undiversified risk, and unsystematic risk......................................................3

Problems in the CAPM model.....................................................................................................................4

Critique of CAPM.......................................................................................................................................5

What are the main assumption of CAPM and why it is mostly used by investors as compared to other

financial analysis tool..................................................................................................................................6

Conclusion...................................................................................................................................................7

References...................................................................................................................................................8

Introduction

With the ramified economic changes, the use of capital assets pricing model has gained

momentum throughout the time. Investors have been using the CAPM model the cost of equity

of the company. The CAPM model has been used to evaluate the required rate of return of the

assets which could be used by investors to choose the particular asset. It is used mainly when

there is well-diversified portfolio. This Capital asset pricing model was developed in 1952 with

a view to find out the rate of return on the assets and according to that the decision about adding

or developing the assets in the business is taken. It helps investors to not only increase the overall

return on capital employed but also assist him to accept the one particular project which assists in

determining the project option which will give best possible outcomes. This model was faced

with many numerous empirical tests, and presences of many more advance assets pricing and

selection of portfolio method in the market. But this model carries some of the important and

unique feature which makes it very popular that is its simplicity and utility in different situations

and circumstances. In 1972 there were different version of CAPM was developed called black

CAPM or zero based CAPM Model. This version was very must strong against the empirical

testing which leads the organization to use the CAPM worldwide.

Risk and return analysis in CAPM Model

The CAPM model is used by organization to give the ranking to the project investment

options on the basis required rate of return, the net present value, profitability and internal rate of

return. This option is very much beneficial to make the best investment decision. In capital asset

pricing model, the pricing of the assets is been done to identity their present values. For

instance, if the organization finds out the expected rate of return is less than its cost of capital

then the project should not be accepted. They can then analyses the rate of return to the expected

rate from return after that the organization can find out whether to invest in this appropriate

investment or not. But while going through this process the organization have to make an

independent estimate than can be expected from the security in which they are interested to

invest this can be done through technical analysis techniques. The technical analysis is made so

that investors could choose which option would give best possible return from the possible

required rate of return. It is further analyzed that risk and return associated with the investment

With the ramified economic changes, the use of capital assets pricing model has gained

momentum throughout the time. Investors have been using the CAPM model the cost of equity

of the company. The CAPM model has been used to evaluate the required rate of return of the

assets which could be used by investors to choose the particular asset. It is used mainly when

there is well-diversified portfolio. This Capital asset pricing model was developed in 1952 with

a view to find out the rate of return on the assets and according to that the decision about adding

or developing the assets in the business is taken. It helps investors to not only increase the overall

return on capital employed but also assist him to accept the one particular project which assists in

determining the project option which will give best possible outcomes. This model was faced

with many numerous empirical tests, and presences of many more advance assets pricing and

selection of portfolio method in the market. But this model carries some of the important and

unique feature which makes it very popular that is its simplicity and utility in different situations

and circumstances. In 1972 there were different version of CAPM was developed called black

CAPM or zero based CAPM Model. This version was very must strong against the empirical

testing which leads the organization to use the CAPM worldwide.

Risk and return analysis in CAPM Model

The CAPM model is used by organization to give the ranking to the project investment

options on the basis required rate of return, the net present value, profitability and internal rate of

return. This option is very much beneficial to make the best investment decision. In capital asset

pricing model, the pricing of the assets is been done to identity their present values. For

instance, if the organization finds out the expected rate of return is less than its cost of capital

then the project should not be accepted. They can then analyses the rate of return to the expected

rate from return after that the organization can find out whether to invest in this appropriate

investment or not. But while going through this process the organization have to make an

independent estimate than can be expected from the security in which they are interested to

invest this can be done through technical analysis techniques. The technical analysis is made so

that investors could choose which option would give best possible return from the possible

required rate of return. It is further analyzed that risk and return associated with the investment

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

decision should also be analyzed by the investors while accepting the project. There should be

proper equilibrium between the risk and return and by using the CAPM method; investors would

accept those project which will give higher return on the basis of the low amount of return.

Evaluation of the systematic, undiversified risk, and unsystematic risk

The risk also come in two forms that are systematic risk also called undiversified risk, and

unsystematic risk also called diversified risk. The systematic risk are those risk that are common

for all the security that are there in the market, risk will be there equal on all the security.

Unsystematic risks are those that are there on the individuals assets. The unsystematic risk can be

diversified to the smaller level by the involvement of the great number of assets in the portfolio.

But diversification in the systematic risk, it cannot be possible within the one market as whole

market is cover with the risk. The CPAM model help to find out the risk that can be transferred

and the risk can cannot be transfer so that it becomes easy for the organization to think forward

for their business.

As we know with the advantage of many model they carry some of the disadvantage

with them the CAPM model as it is cover up with some of the assumptions that decrease its

value with a bit in the market, and with the assumption there are some of the problem also that

this model carry: The model says that there are no tax or transaction costs, but this cannot be

possible in the investment that it doesn’t carry tax or transaction cost so this was the problem for

this model although this assumption may be saved from the more complicated versions of this

model. CAPM assume that the entire active and the potential shareholders who take part in the

day to day activity of the business will consider all the assets but will optimize on portfolio only.

But this assumption was properly contradict by the individuals shareholders in the company as

human have the habit to move safely, so for these kind of situation also they make multiple

portfolio each portfolio for every goal (Fama, & Macbeth, 1973). CAPM model assume that the

economic agent will optimize in the short –term of time, according to the fact the long term

investor will choose the long –term outlooks instead of the short term of investment as long term

investment are more risk free assets for the agent (Graham, & Harvey, 2001), The traditional

CAPM use historical data for predicting the future expected return or the expected value, but just

on the basis of the historical value, it may become hard to predict the future flow of the business.

proper equilibrium between the risk and return and by using the CAPM method; investors would

accept those project which will give higher return on the basis of the low amount of return.

Evaluation of the systematic, undiversified risk, and unsystematic risk

The risk also come in two forms that are systematic risk also called undiversified risk, and

unsystematic risk also called diversified risk. The systematic risk are those risk that are common

for all the security that are there in the market, risk will be there equal on all the security.

Unsystematic risks are those that are there on the individuals assets. The unsystematic risk can be

diversified to the smaller level by the involvement of the great number of assets in the portfolio.

But diversification in the systematic risk, it cannot be possible within the one market as whole

market is cover with the risk. The CPAM model help to find out the risk that can be transferred

and the risk can cannot be transfer so that it becomes easy for the organization to think forward

for their business.

As we know with the advantage of many model they carry some of the disadvantage

with them the CAPM model as it is cover up with some of the assumptions that decrease its

value with a bit in the market, and with the assumption there are some of the problem also that

this model carry: The model says that there are no tax or transaction costs, but this cannot be

possible in the investment that it doesn’t carry tax or transaction cost so this was the problem for

this model although this assumption may be saved from the more complicated versions of this

model. CAPM assume that the entire active and the potential shareholders who take part in the

day to day activity of the business will consider all the assets but will optimize on portfolio only.

But this assumption was properly contradict by the individuals shareholders in the company as

human have the habit to move safely, so for these kind of situation also they make multiple

portfolio each portfolio for every goal (Fama, & Macbeth, 1973). CAPM model assume that the

economic agent will optimize in the short –term of time, according to the fact the long term

investor will choose the long –term outlooks instead of the short term of investment as long term

investment are more risk free assets for the agent (Graham, & Harvey, 2001), The traditional

CAPM use historical data for predicting the future expected return or the expected value, but just

on the basis of the historical value, it may become hard to predict the future flow of the business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The future inflow and outflow of cash would be used to determine the required amount of

investment. It will be used to strengthen the overall outcomes and by using the discounting

factors, investors could determine the present value of the cash inflow and outflow (Lewellen,

and Nagel., 2006).

Problems in the CAPM model

This model content so many problems as this model is based on lots of assumption but

still the investor use this model worldwide to calculate the risk that are expected from the

investment, the risk that can be diversified and the risk that cannot be diversified to the other

person and we can even calculate the coming return from the future investment in short terms

and more part of the business depends on the CAPM model (Roll, 1977). If these small problem

are removed from this model by revising some of the assumption than no other model can be

better than the CAPM model for the investment matter. This model plays a fundamental rule for

understanding the price of the determinants goods. Despite from its empirical performance, the

investor can think in the different manner about the expected return and the risk from the

investor. By understanding this model, investor can think in the different manner to allocate

proper return and analyse the facts related to risk and return at all from investment. After

analyse of various factors, it could be inferred that capital assets is very imperative tool while

making the investment choice or selecting one investment option but it is based on the several

assumptions such as risk and return as liner relation if one increase then another will also be

increased, it is hard to determine which capital market investment is perfect due to the volatility

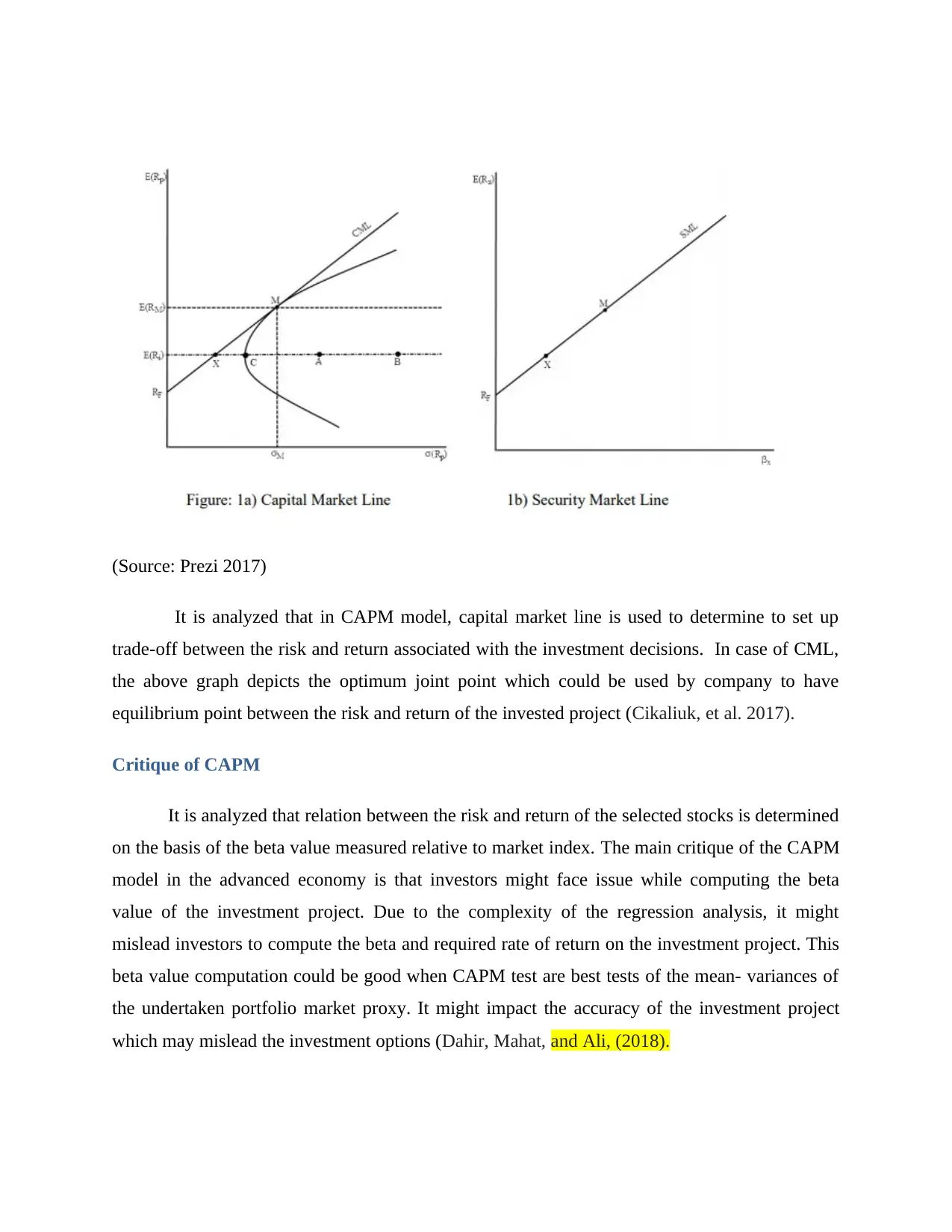

of the market. The SML and CML both are the two main aspects of the capital assets pricing

model which is widely used by investors to gauge the financial performance of the selected

securities. The below graph reflects the comparison between the capital (Capital Assets pricing

model, 2017).

investment. It will be used to strengthen the overall outcomes and by using the discounting

factors, investors could determine the present value of the cash inflow and outflow (Lewellen,

and Nagel., 2006).

Problems in the CAPM model

This model content so many problems as this model is based on lots of assumption but

still the investor use this model worldwide to calculate the risk that are expected from the

investment, the risk that can be diversified and the risk that cannot be diversified to the other

person and we can even calculate the coming return from the future investment in short terms

and more part of the business depends on the CAPM model (Roll, 1977). If these small problem

are removed from this model by revising some of the assumption than no other model can be

better than the CAPM model for the investment matter. This model plays a fundamental rule for

understanding the price of the determinants goods. Despite from its empirical performance, the

investor can think in the different manner about the expected return and the risk from the

investor. By understanding this model, investor can think in the different manner to allocate

proper return and analyse the facts related to risk and return at all from investment. After

analyse of various factors, it could be inferred that capital assets is very imperative tool while

making the investment choice or selecting one investment option but it is based on the several

assumptions such as risk and return as liner relation if one increase then another will also be

increased, it is hard to determine which capital market investment is perfect due to the volatility

of the market. The SML and CML both are the two main aspects of the capital assets pricing

model which is widely used by investors to gauge the financial performance of the selected

securities. The below graph reflects the comparison between the capital (Capital Assets pricing

model, 2017).

(Source: Prezi 2017)

It is analyzed that in CAPM model, capital market line is used to determine to set up

trade-off between the risk and return associated with the investment decisions. In case of CML,

the above graph depicts the optimum joint point which could be used by company to have

equilibrium point between the risk and return of the invested project (Cikaliuk, et al. 2017).

Critique of CAPM

It is analyzed that relation between the risk and return of the selected stocks is determined

on the basis of the beta value measured relative to market index. The main critique of the CAPM

model in the advanced economy is that investors might face issue while computing the beta

value of the investment project. Due to the complexity of the regression analysis, it might

mislead investors to compute the beta and required rate of return on the investment project. This

beta value computation could be good when CAPM test are best tests of the mean- variances of

the undertaken portfolio market proxy. It might impact the accuracy of the investment project

which may mislead the investment options (Dahir, Mahat, and Ali, (2018).

It is analyzed that in CAPM model, capital market line is used to determine to set up

trade-off between the risk and return associated with the investment decisions. In case of CML,

the above graph depicts the optimum joint point which could be used by company to have

equilibrium point between the risk and return of the invested project (Cikaliuk, et al. 2017).

Critique of CAPM

It is analyzed that relation between the risk and return of the selected stocks is determined

on the basis of the beta value measured relative to market index. The main critique of the CAPM

model in the advanced economy is that investors might face issue while computing the beta

value of the investment project. Due to the complexity of the regression analysis, it might

mislead investors to compute the beta and required rate of return on the investment project. This

beta value computation could be good when CAPM test are best tests of the mean- variances of

the undertaken portfolio market proxy. It might impact the accuracy of the investment project

which may mislead the investment options (Dahir, Mahat, and Ali, (2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

What are the main assumption of CAPM and why it is mostly used by investors as

compared to other financial analysis tool

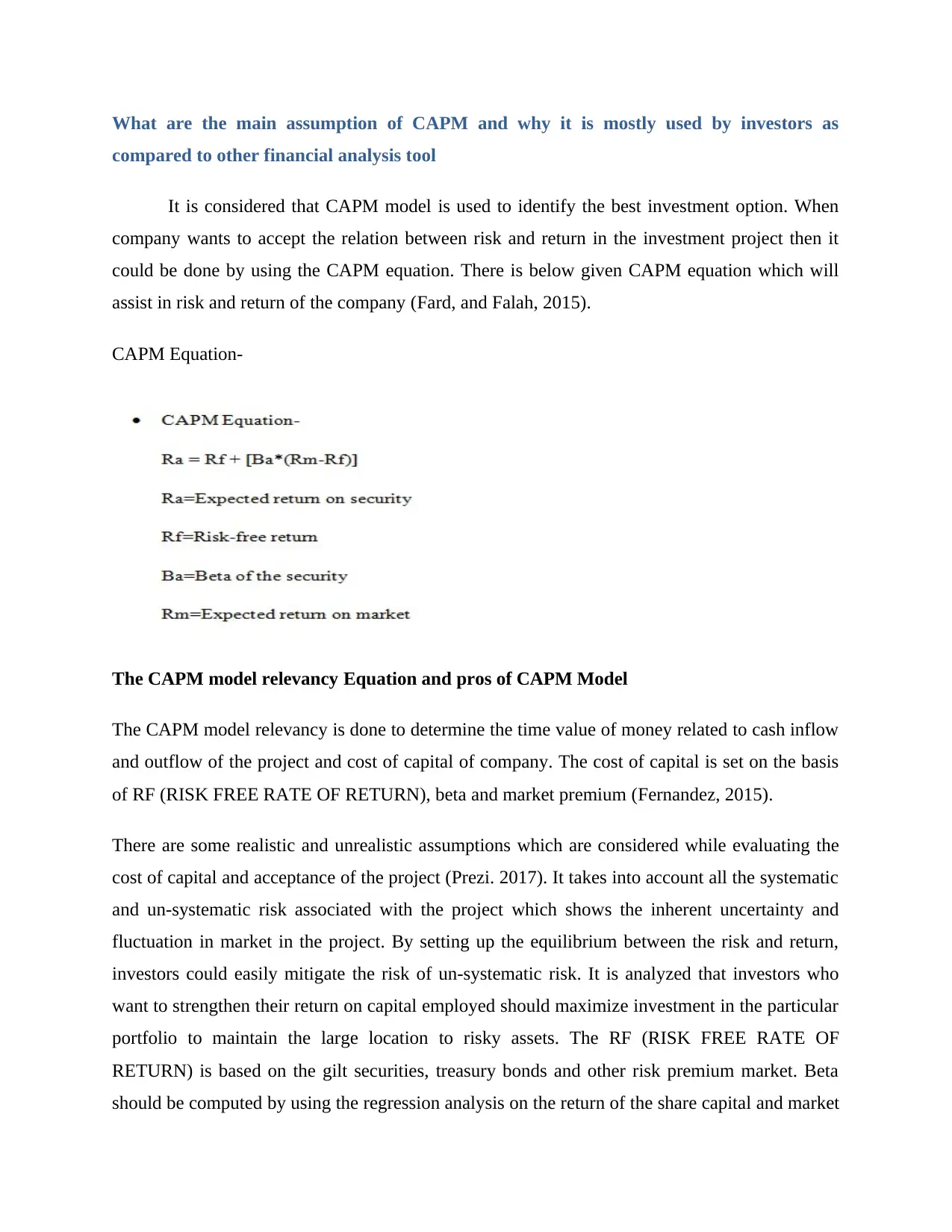

It is considered that CAPM model is used to identify the best investment option. When

company wants to accept the relation between risk and return in the investment project then it

could be done by using the CAPM equation. There is below given CAPM equation which will

assist in risk and return of the company (Fard, and Falah, 2015).

CAPM Equation-

The CAPM model relevancy Equation and pros of CAPM Model

The CAPM model relevancy is done to determine the time value of money related to cash inflow

and outflow of the project and cost of capital of company. The cost of capital is set on the basis

of RF (RISK FREE RATE OF RETURN), beta and market premium (Fernandez, 2015).

There are some realistic and unrealistic assumptions which are considered while evaluating the

cost of capital and acceptance of the project (Prezi. 2017). It takes into account all the systematic

and un-systematic risk associated with the project which shows the inherent uncertainty and

fluctuation in market in the project. By setting up the equilibrium between the risk and return,

investors could easily mitigate the risk of un-systematic risk. It is analyzed that investors who

want to strengthen their return on capital employed should maximize investment in the particular

portfolio to maintain the large location to risky assets. The RF (RISK FREE RATE OF

RETURN) is based on the gilt securities, treasury bonds and other risk premium market. Beta

should be computed by using the regression analysis on the return of the share capital and market

compared to other financial analysis tool

It is considered that CAPM model is used to identify the best investment option. When

company wants to accept the relation between risk and return in the investment project then it

could be done by using the CAPM equation. There is below given CAPM equation which will

assist in risk and return of the company (Fard, and Falah, 2015).

CAPM Equation-

The CAPM model relevancy Equation and pros of CAPM Model

The CAPM model relevancy is done to determine the time value of money related to cash inflow

and outflow of the project and cost of capital of company. The cost of capital is set on the basis

of RF (RISK FREE RATE OF RETURN), beta and market premium (Fernandez, 2015).

There are some realistic and unrealistic assumptions which are considered while evaluating the

cost of capital and acceptance of the project (Prezi. 2017). It takes into account all the systematic

and un-systematic risk associated with the project which shows the inherent uncertainty and

fluctuation in market in the project. By setting up the equilibrium between the risk and return,

investors could easily mitigate the risk of un-systematic risk. It is analyzed that investors who

want to strengthen their return on capital employed should maximize investment in the particular

portfolio to maintain the large location to risky assets. The RF (RISK FREE RATE OF

RETURN) is based on the gilt securities, treasury bonds and other risk premium market. Beta

should be computed by using the regression analysis on the return of the share capital and market

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

index of the industry. CAPM tests are considered as best tests of the mean-variances efficiency

of the portfolio. There are other several models which could also be used by investors to

determine the cost of capital and risk associated with the project such as Arbitrage Pricing theory

model, Security market line model, dividend discount model and growth model (Yahoo finance,

2018).

Conclusion

CAPM model is useful when it is easy to collect the required data such as beta, risk

associated with the investment and return associated with the project. Now, in the end, it could

be inferred that CAPM model is used to determine investment option which could be used by

investors to determine which option would give him more return if he will invest his capital. The

CAPM model covers all the aspects of the investment choices such as return available on

investment, risk associated with the proposal and profitability of the project. Investors need to

use the particular investment model if he wants to accept the project. The risk and return

associated with the project could be analyzed by using the CAPM model and Arbitrage Pricing

theory model.

of the portfolio. There are other several models which could also be used by investors to

determine the cost of capital and risk associated with the project such as Arbitrage Pricing theory

model, Security market line model, dividend discount model and growth model (Yahoo finance,

2018).

Conclusion

CAPM model is useful when it is easy to collect the required data such as beta, risk

associated with the investment and return associated with the project. Now, in the end, it could

be inferred that CAPM model is used to determine investment option which could be used by

investors to determine which option would give him more return if he will invest his capital. The

CAPM model covers all the aspects of the investment choices such as return available on

investment, risk associated with the proposal and profitability of the project. Investors need to

use the particular investment model if he wants to accept the project. The risk and return

associated with the project could be analyzed by using the CAPM model and Arbitrage Pricing

theory model.

References

Capital Assets pricing model, (2017) Capital Asset Pricing Model (CAPM)? [Online] Available

from https://accountingexplained.com/capital/equity-valuation/capital-asset-pricing-model

[Accessed on 28th September 2018]

Cikaliuk, M., Erakovic, L., Jackson, B., Noonan, C. and Watson, S., (2017). Board Leadership

for Strategic Transformation: Aligning Diversity Initiatives at the Bank of New Zealand. 3(1),

pp.21-32.

Dahir, A.M., Mahat, F.B. and Ali, N.A.B., (2018). Funding liquidity risk and bank risk-taking in

BRICS countries: An application of system GMM approach. International Journal of Emerging

Markets, 13(1), pp.231-248.

Fama, E & Macbeth, J (1973) ‘Risk Return and Equilibrium: Some Empirical Tests’, Journal of

Political Economy, 8, 607-636

Fard, H.V. and Falah, A.B., (2015) A New Modified CAPM Model: The Two Beta

CAPM. Jurnal UMP Social Sciences and Technology Management 3(1). pp.23-28.

Fernandez, P., (2015) CAPM: an absurd model. Business Valuation Review, 34(1), pp.4-23.

Graham, J &Harvey, C (2001) ‘The Theory and Practice of Corporate Finance: Evidence From

The Field’, Journal Of Financial Economics 60, 187-243

Lewellen, J and Nagel (2006) “The conditional CAPM Does not Explain Asset Pricing

Anomalies”, The Journal of Financial Economics, 82, (2), 289 – 314.

Prezi. D, (2017) CAPM: Assumptions and Limitations | Securities | Financial Economics

[Online] Available from

http://www.economicsdiscussion.net/portfolio-management/capm/capm-assumptions-and-

limitations-securities-financial-economics/29904 [Accessed on 28th September 2018]

Roll, R (1977) ‘A Critique of the Asset Pricing Theory’s Test’, Journal of Financial Economics,

4 (1), 129-176

Capital Assets pricing model, (2017) Capital Asset Pricing Model (CAPM)? [Online] Available

from https://accountingexplained.com/capital/equity-valuation/capital-asset-pricing-model

[Accessed on 28th September 2018]

Cikaliuk, M., Erakovic, L., Jackson, B., Noonan, C. and Watson, S., (2017). Board Leadership

for Strategic Transformation: Aligning Diversity Initiatives at the Bank of New Zealand. 3(1),

pp.21-32.

Dahir, A.M., Mahat, F.B. and Ali, N.A.B., (2018). Funding liquidity risk and bank risk-taking in

BRICS countries: An application of system GMM approach. International Journal of Emerging

Markets, 13(1), pp.231-248.

Fama, E & Macbeth, J (1973) ‘Risk Return and Equilibrium: Some Empirical Tests’, Journal of

Political Economy, 8, 607-636

Fard, H.V. and Falah, A.B., (2015) A New Modified CAPM Model: The Two Beta

CAPM. Jurnal UMP Social Sciences and Technology Management 3(1). pp.23-28.

Fernandez, P., (2015) CAPM: an absurd model. Business Valuation Review, 34(1), pp.4-23.

Graham, J &Harvey, C (2001) ‘The Theory and Practice of Corporate Finance: Evidence From

The Field’, Journal Of Financial Economics 60, 187-243

Lewellen, J and Nagel (2006) “The conditional CAPM Does not Explain Asset Pricing

Anomalies”, The Journal of Financial Economics, 82, (2), 289 – 314.

Prezi. D, (2017) CAPM: Assumptions and Limitations | Securities | Financial Economics

[Online] Available from

http://www.economicsdiscussion.net/portfolio-management/capm/capm-assumptions-and-

limitations-securities-financial-economics/29904 [Accessed on 28th September 2018]

Roll, R (1977) ‘A Critique of the Asset Pricing Theory’s Test’, Journal of Financial Economics,

4 (1), 129-176

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Yahoo finance, (2018), Online] Available from https://in.finance.yahoo.com/[Accessed on 28th

September 2018]

September 2018]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.