Financial Management: Corporate Tax, CAPM and Investment Decisions

VerifiedAdded on 2023/06/15

|8

|1594

|474

Homework Assignment

AI Summary

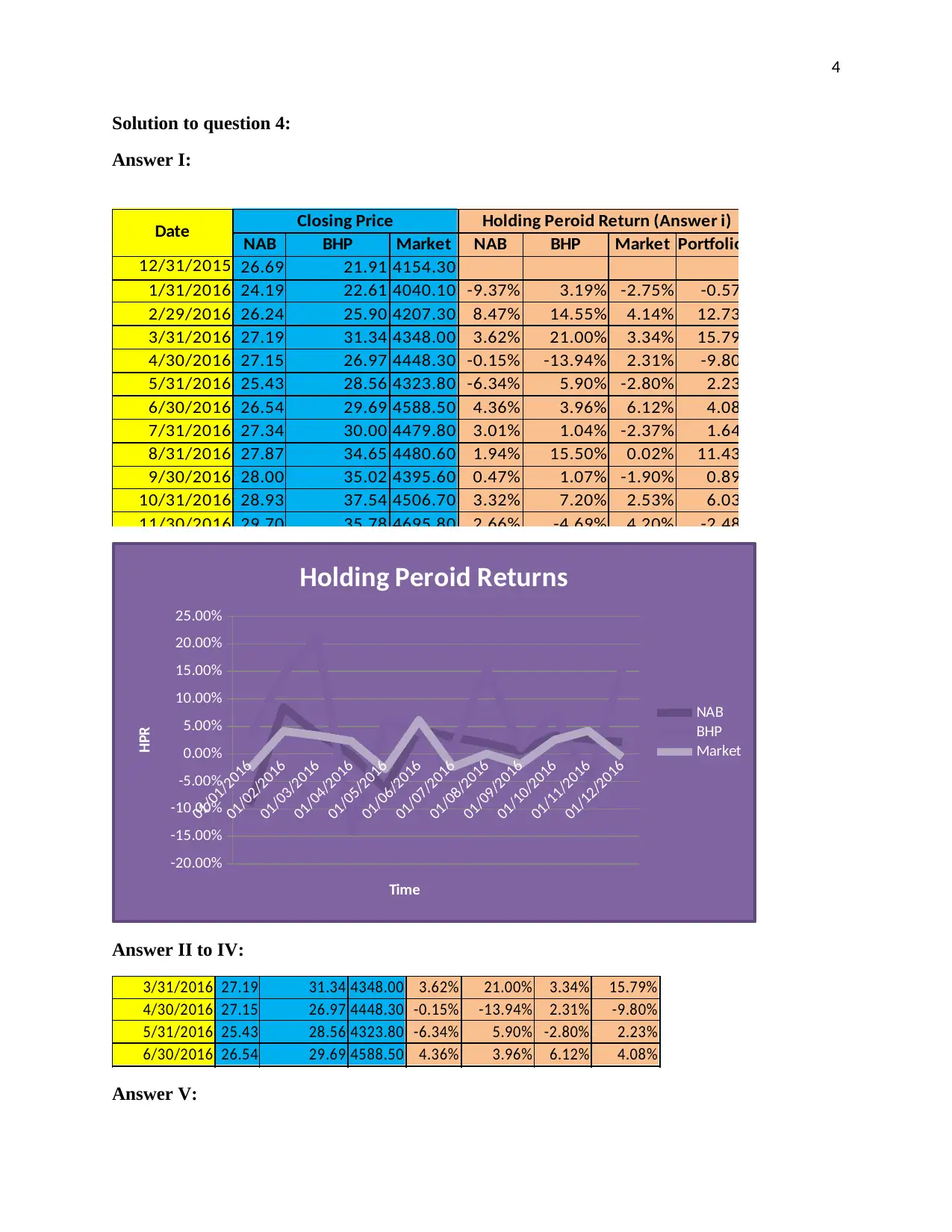

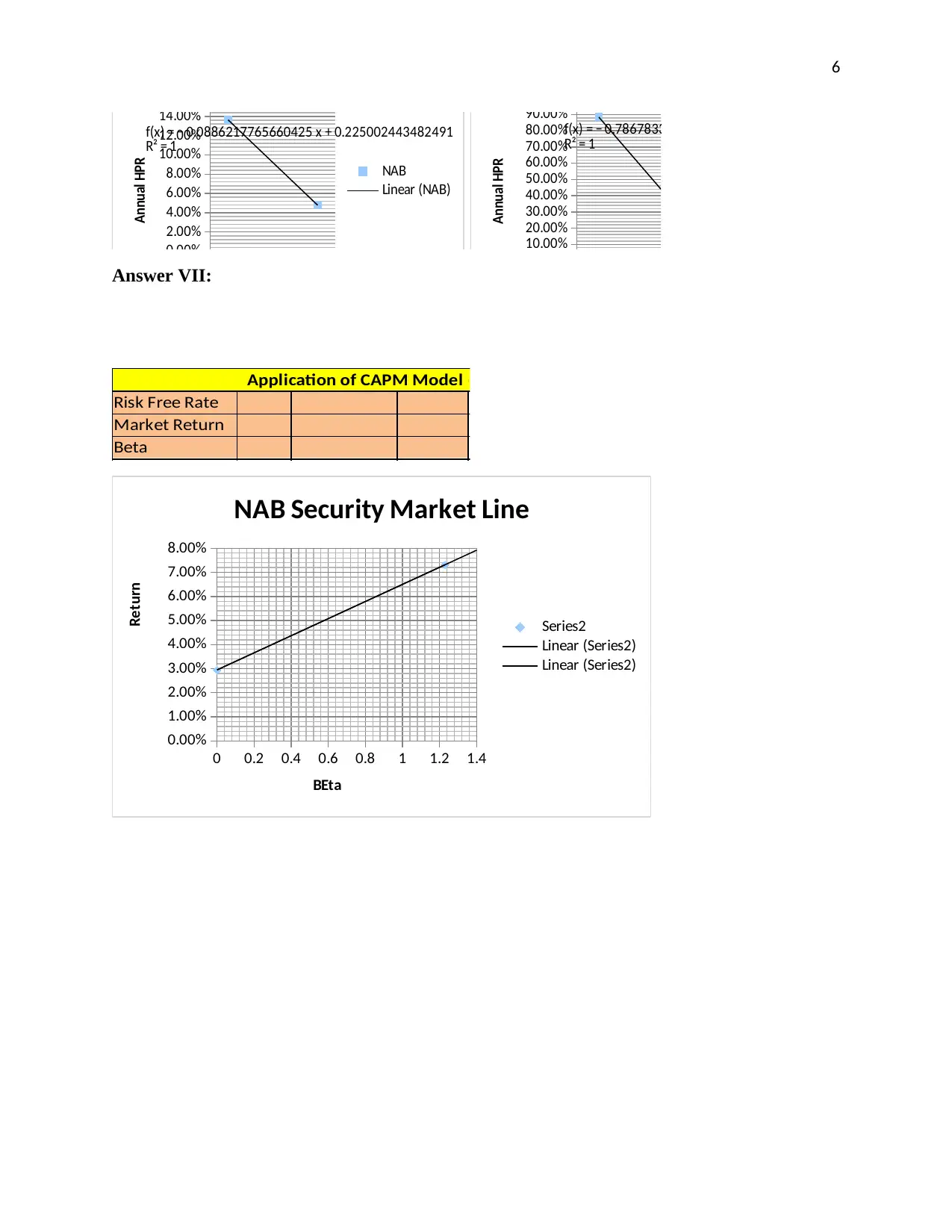

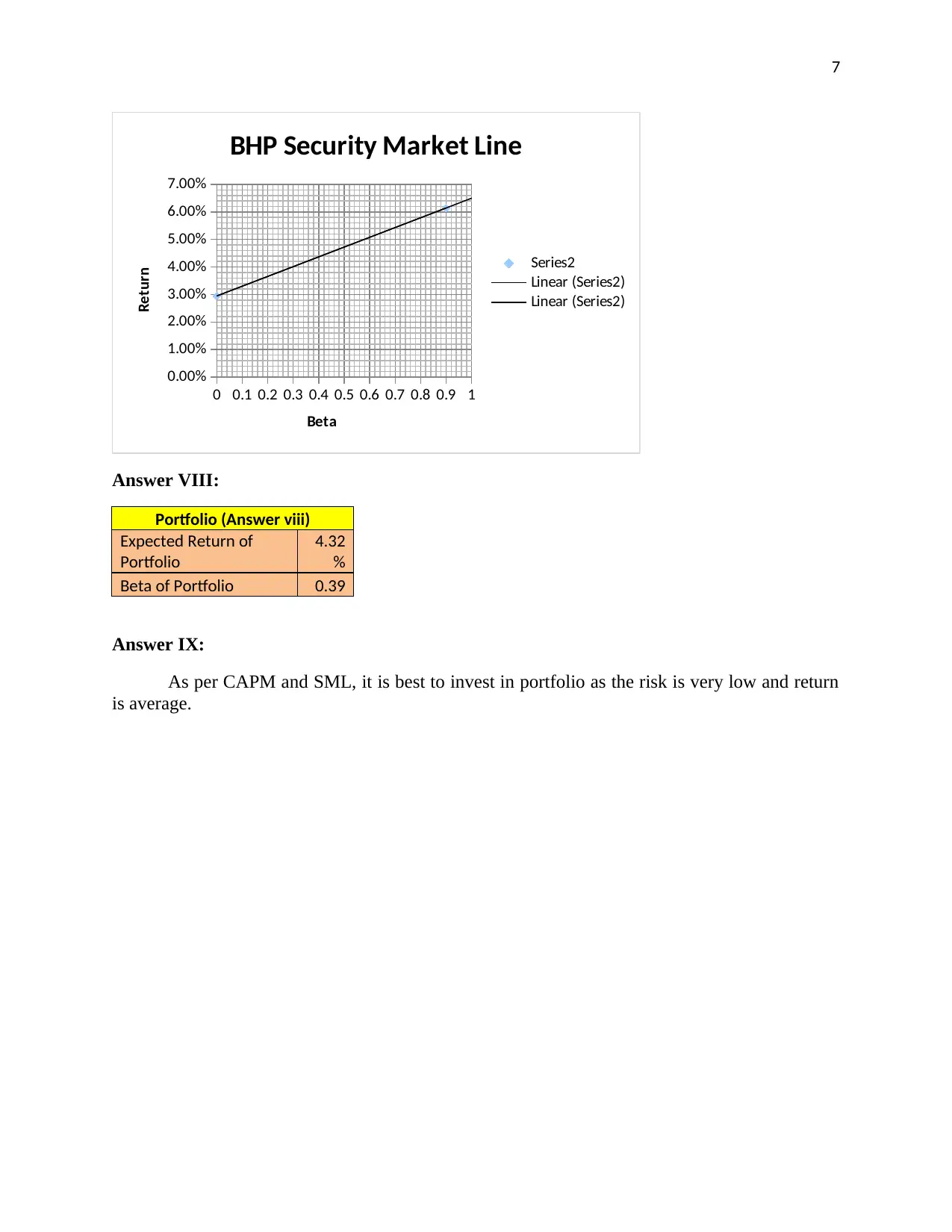

This assignment provides a detailed analysis of the Australian government's decision to reduce the corporate tax rate to 25%, examining both the positive and negative implications of this policy. It discusses how the tax cut aims to stimulate economic growth by attracting foreign investment and fostering job creation. However, it also considers the potential drawbacks, particularly the impact of Australia's dividend imputation system, which may limit the benefits for domestic shareholders. The analysis includes calculations and explanations related to investment returns, risk assessment using the Capital Asset Pricing Model (CAPM), and portfolio analysis. Furthermore, it evaluates the effectiveness of the tax cut in enhancing Australia's global competitiveness compared to other countries like the US, concluding with recommendations for alternative measures to promote economic growth. The assignment also contains numerical problems related to financial mathematics, including present value calculations and loan amortization.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.