Understanding Capital Market Line, Security Market Line, and CAPM

VerifiedAdded on 2021/09/27

|9

|2887

|134

Report

AI Summary

This report provides a detailed explanation of the Capital Market Line (CML), the Security Market Line (SML), and the Capital Asset Pricing Model (CAPM). It begins by outlining the assumptions of the CML, including homogeneous expectations and the market portfolio, and describes how investors combine the market portfolio with a risk-free asset to form efficient portfolios. The report then explains the relationship between risk and return on the CML, and the formula used to calculate expected returns. The report then transitions to the SML, which illustrates the relationship between expected return and beta for all securities and portfolios, whether efficient or inefficient. It differentiates between systematic and unsystematic risk, emphasizing the importance of beta as a measure of systematic risk. The report also provides formulas for calculating expected return based on beta and the market risk premium. Finally, the report contrasts the CML and SML, and explains how the CAPM can be used for security valuation, including identifying underpriced and overpriced securities based on their position relative to the SML.

THE CAPITAL MARKET LINE

All investors are assumed to have identical (homogeneous) expectations. Hence, all of

them will face the same efficient frontier depicted in Fig. Every investor will seek to

combine the same risky portfolio B with different levels of lending or borrowing according to

his desired level of risk. Because all investors hold the same risky portfolio, then it will

include all risky securities in the market. This portfolio of all risky securities is referred to as

the market portfolio M. Each security will be held in the proportion which the market value

of the security bears to the total market value of all risky securities in the market. All

investors will hold combinations of only two assets, the market portfolio and a riskless

security.

All these combinations will lie along the straight line representing the efficient

frontier. This line formed by the action of all investors mixing the market portfolio with the

risk free asset is known as the capital market line (CML). All efficient portfolios of all

investors will lie along this capital market line.

The relationship between the return and risk of any efficient portfolio on the capital

market line can be expressed in the form of the following equation.

Re = Rf + [ Re – Rf] σe

σm

Where the subscript e denotes an efficient portfolio.

The risk free return Rf represents the reward for waiting. It is, in other words, the

price of time. The term [(Rm – Rf/σ m] represents the price of risk or risk premium, i.e. the

excess return earned per unit of risk or standard deviation. It measures the additional return

for an additional unit of risk. When the risk of the efficient portfolio, σ e , is multiplied with

this term, we get the risk premium available for the particular efficient portfolio under

consideration.

Thus, the expected return on an efficient portfolio is :

(Expected return) = (Price of time) + (Price of risk) (Amount of risk)

The CML provides a risk return relationship and a measure of risk for efficient

portfolios. The appropriate measure of risk for an efficient portfolio is the standard deviation

of return of the portfolio. There is a linear relationship between the risk as measured by the

standard deviation and the expected return for these efficient portfolios.

All investors are assumed to have identical (homogeneous) expectations. Hence, all of

them will face the same efficient frontier depicted in Fig. Every investor will seek to

combine the same risky portfolio B with different levels of lending or borrowing according to

his desired level of risk. Because all investors hold the same risky portfolio, then it will

include all risky securities in the market. This portfolio of all risky securities is referred to as

the market portfolio M. Each security will be held in the proportion which the market value

of the security bears to the total market value of all risky securities in the market. All

investors will hold combinations of only two assets, the market portfolio and a riskless

security.

All these combinations will lie along the straight line representing the efficient

frontier. This line formed by the action of all investors mixing the market portfolio with the

risk free asset is known as the capital market line (CML). All efficient portfolios of all

investors will lie along this capital market line.

The relationship between the return and risk of any efficient portfolio on the capital

market line can be expressed in the form of the following equation.

Re = Rf + [ Re – Rf] σe

σm

Where the subscript e denotes an efficient portfolio.

The risk free return Rf represents the reward for waiting. It is, in other words, the

price of time. The term [(Rm – Rf/σ m] represents the price of risk or risk premium, i.e. the

excess return earned per unit of risk or standard deviation. It measures the additional return

for an additional unit of risk. When the risk of the efficient portfolio, σ e , is multiplied with

this term, we get the risk premium available for the particular efficient portfolio under

consideration.

Thus, the expected return on an efficient portfolio is :

(Expected return) = (Price of time) + (Price of risk) (Amount of risk)

The CML provides a risk return relationship and a measure of risk for efficient

portfolios. The appropriate measure of risk for an efficient portfolio is the standard deviation

of return of the portfolio. There is a linear relationship between the risk as measured by the

standard deviation and the expected return for these efficient portfolios.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

THE SECURITY MARKET LINE

The CML shows the risk – return relationship for all efficient portfolios. They would

all lie along the capital market line. All portfolios other than the efficient ones will lie below

the capital market line. The CML does not describe the risk – return relationship of inefficient

portfolios or of individual securities. The capital asset pricing model specifies the relationship

between expected return and risk for all securities and all portfolios, whether efficient or

inefficient.

We have seen earlier that the total risk of a security as measured by standard deviation

is compared of two components: systematic risk and unsystematic risk or diversifiable risk.

As investment is diversified and more and more securities are added to a portfolio, the

unsystematic risk is reduced. For a very well diversified portfolio, unsystematic risk trends to

become zero and the only relevant risk is systematic risk measured by beta (β). Hence, it is

argued that the correct measure of a security‘s risk is beta.

It follows that the expected return of a security or of a portfolio should be related to

the risk of that security or portfolios as measured by β. Beta is a measure of the security‘s

sensitivity to change in market return. Beta value greater than one indicates higher sensitivity

to market changes, whereas beta value less than one indicates lower sensitivity to market

changes. A β value of one indicates that the security moves at the same rate and in the same

direction as the market. Thus, the β of the market may be taken as one.

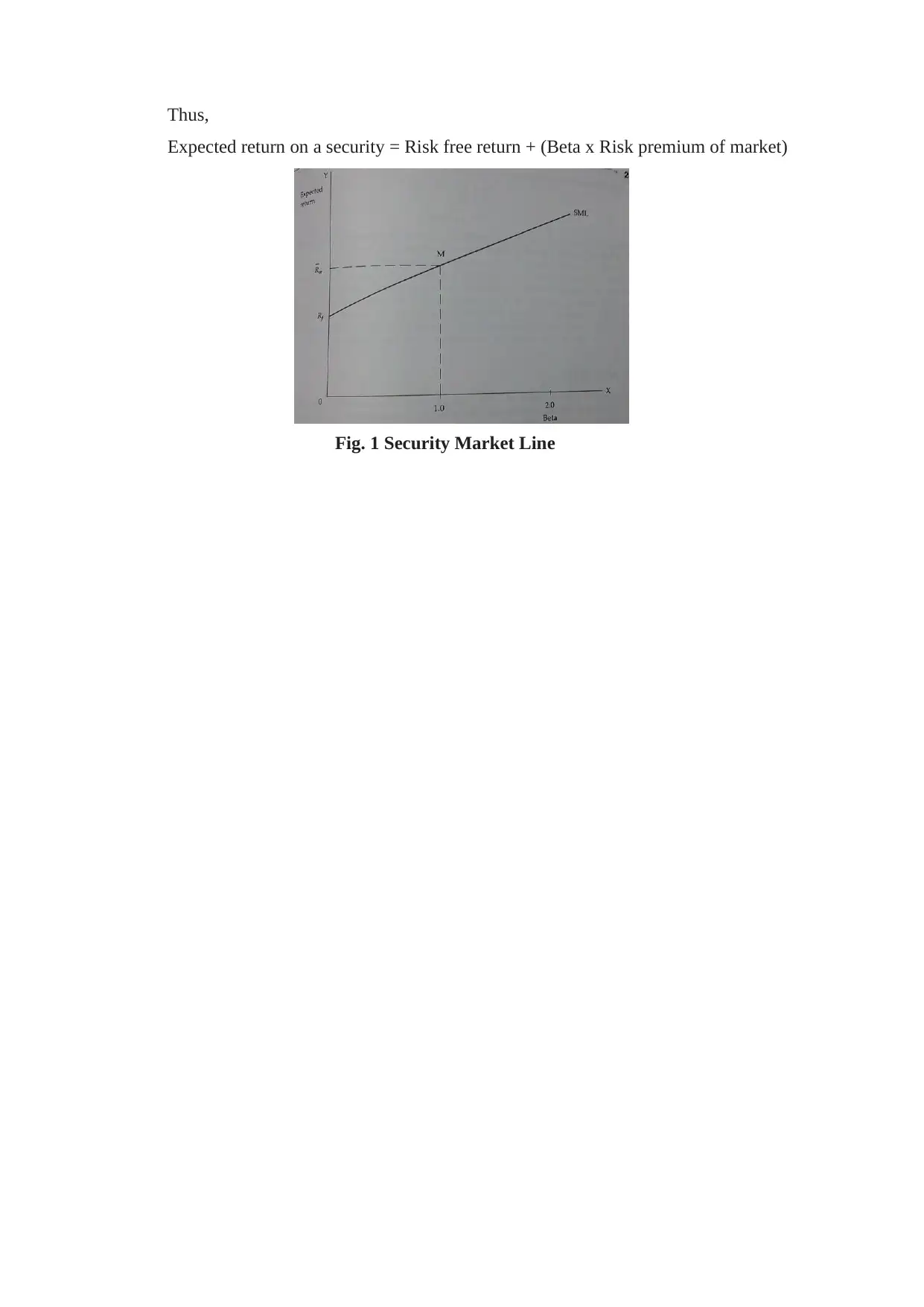

The relationship between expected return and β of a security can be determined

graphically. Let us consider and XY graph where expected returns are plotted on the Y axis

and beta coefficients are plotted on the X axis. A risk free asset has an expected return

equivalent to Rf and beta coefficient of zero. The market portfolio M has a beta coefficient of

one and expected return equivalent R m. A straight line joining these two points is known as

the security market line (SML). This is illustrated in Fig. 1

The security market line provides the relationship between the expected return and

beta of a security or portfolio. This relationship can be expressed in the form of the following

equation:

Rm – Rf + βi (Rm - Rf )

A part of the return on any security or portfolio is a reward for bearing risk and the

rest is the reward for waiting, representing the time value of money. The risk free rate, R f

(which is earned by a security which has no risk) is the reward for waiting. The reward for

bearing risk is the risk premium. The risk premium of a security is directly proportional to the

risk as measured by β. The risk premium of a security is calculated as the product of beta and

the risk premium of the market which is the excess of expected market return over the risk

free return, that is, [Rm - Rf ].

The CML shows the risk – return relationship for all efficient portfolios. They would

all lie along the capital market line. All portfolios other than the efficient ones will lie below

the capital market line. The CML does not describe the risk – return relationship of inefficient

portfolios or of individual securities. The capital asset pricing model specifies the relationship

between expected return and risk for all securities and all portfolios, whether efficient or

inefficient.

We have seen earlier that the total risk of a security as measured by standard deviation

is compared of two components: systematic risk and unsystematic risk or diversifiable risk.

As investment is diversified and more and more securities are added to a portfolio, the

unsystematic risk is reduced. For a very well diversified portfolio, unsystematic risk trends to

become zero and the only relevant risk is systematic risk measured by beta (β). Hence, it is

argued that the correct measure of a security‘s risk is beta.

It follows that the expected return of a security or of a portfolio should be related to

the risk of that security or portfolios as measured by β. Beta is a measure of the security‘s

sensitivity to change in market return. Beta value greater than one indicates higher sensitivity

to market changes, whereas beta value less than one indicates lower sensitivity to market

changes. A β value of one indicates that the security moves at the same rate and in the same

direction as the market. Thus, the β of the market may be taken as one.

The relationship between expected return and β of a security can be determined

graphically. Let us consider and XY graph where expected returns are plotted on the Y axis

and beta coefficients are plotted on the X axis. A risk free asset has an expected return

equivalent to Rf and beta coefficient of zero. The market portfolio M has a beta coefficient of

one and expected return equivalent R m. A straight line joining these two points is known as

the security market line (SML). This is illustrated in Fig. 1

The security market line provides the relationship between the expected return and

beta of a security or portfolio. This relationship can be expressed in the form of the following

equation:

Rm – Rf + βi (Rm - Rf )

A part of the return on any security or portfolio is a reward for bearing risk and the

rest is the reward for waiting, representing the time value of money. The risk free rate, R f

(which is earned by a security which has no risk) is the reward for waiting. The reward for

bearing risk is the risk premium. The risk premium of a security is directly proportional to the

risk as measured by β. The risk premium of a security is calculated as the product of beta and

the risk premium of the market which is the excess of expected market return over the risk

free return, that is, [Rm - Rf ].

Thus,

Expected return on a security = Risk free return + (Beta x Risk premium of market)

Fig. 1 Security Market Line

Expected return on a security = Risk free return + (Beta x Risk premium of market)

Fig. 1 Security Market Line

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CAPM

The relationship between risk and return established by the security market line in

known as the capital asset pricing model. It is basically a simple linear relationship. The

higher the value of beta, higher would be the risk of the security and therefore, larger would

be the return expected by the investors. In other words, all securities are expected to yield

returns commensurate with their riskiness as measured by β. This relationship is valid not

only for individual securities, but it also valid for all portfolios whether efficient or

inefficient.

The expected return on any security or portfolio can be determined from the CAPM

formula if we know the beta of that security or portfolio. To illustrate the application of the

CAPM, let us consider a simple example. There are two securities P and Q having values of

beta as 0.7 and 1.6 respectively. The risk free rate is assumed to be 6 per cent and the market

return is expected to be 15 per cent, thus providing a market risk premium of 9 per cent (i.e.

Rm - Rf ).

The expected return on security P may be worked out as shown below:

Rm = Rf + βi [Rm - Rf )

= 6 + 0.7 (15 – 6)

= 6 + 6.3 = 12.3 per cent

The expected return on security Q is

Rm = 6 + 1.6 (15 – 6)

= 6 + 14.4

= 20.4 per cent

Security P with a β of 0.7 has an expected return of 12.3 per cent whereas security Q

with a higher beta of 1.6 has a higher expected return of 20.4 per cent.

CAPM represents one of the most important discoveries in the field of fiancé. It

describes the expected return for all assets and portfolios of assets in the economy. The

difference in the expected returns of any two assets can be related to the difference in their

betas. The model postulates that systematic risk is the only important ingredient in

determining expected return. As investors can eliminate all unsystematic risk through

diversification, they can be expected to be rewarded only for bearing systematic risk. Thus,

the relevant risk of an asset is its systematic risk and not the total risk.

The relationship between risk and return established by the security market line in

known as the capital asset pricing model. It is basically a simple linear relationship. The

higher the value of beta, higher would be the risk of the security and therefore, larger would

be the return expected by the investors. In other words, all securities are expected to yield

returns commensurate with their riskiness as measured by β. This relationship is valid not

only for individual securities, but it also valid for all portfolios whether efficient or

inefficient.

The expected return on any security or portfolio can be determined from the CAPM

formula if we know the beta of that security or portfolio. To illustrate the application of the

CAPM, let us consider a simple example. There are two securities P and Q having values of

beta as 0.7 and 1.6 respectively. The risk free rate is assumed to be 6 per cent and the market

return is expected to be 15 per cent, thus providing a market risk premium of 9 per cent (i.e.

Rm - Rf ).

The expected return on security P may be worked out as shown below:

Rm = Rf + βi [Rm - Rf )

= 6 + 0.7 (15 – 6)

= 6 + 6.3 = 12.3 per cent

The expected return on security Q is

Rm = 6 + 1.6 (15 – 6)

= 6 + 14.4

= 20.4 per cent

Security P with a β of 0.7 has an expected return of 12.3 per cent whereas security Q

with a higher beta of 1.6 has a higher expected return of 20.4 per cent.

CAPM represents one of the most important discoveries in the field of fiancé. It

describes the expected return for all assets and portfolios of assets in the economy. The

difference in the expected returns of any two assets can be related to the difference in their

betas. The model postulates that systematic risk is the only important ingredient in

determining expected return. As investors can eliminate all unsystematic risk through

diversification, they can be expected to be rewarded only for bearing systematic risk. Thus,

the relevant risk of an asset is its systematic risk and not the total risk.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

SML AND CML

It is necessary to contrast SML with CML. Both postulate a linear (straight line)

relationship between risk and return. In CML the risk is defined as total risk and is measured

by standard deviation, while in SML the risk is defined as systematic risk and is measured by

β. Capital market line is valid only for efficient portfolios while security market line is valid

for all portfolios and all individual securities as well. CML is the basis of the capital market

theory while SML is the basis of the capital asset pricing model.

PRICING OF SECURITIES WITH CAPM

The capital asset pricing model can also be used for evaluating the pricing of

securities. The CAPM provides a framework for assessing whether a security is underpriced,

overpriced or correctly priced. According to CAPM, each security is expected to provide a

return commensurate with its level of risk. A security may be offering more returns than the

expected return, making it more attractive. On the contrary, another security may be offering

less return than the expected return, making it less attractive.

The expected return on a security can be calculating using the CAPM formula. Let us

designate it as the theoretical return. The real rate of return estimated to be realsied from

investing in a security can be calculated by the following formula.

Ri = (P1 – P0) + D1

P0

It is necessary to contrast SML with CML. Both postulate a linear (straight line)

relationship between risk and return. In CML the risk is defined as total risk and is measured

by standard deviation, while in SML the risk is defined as systematic risk and is measured by

β. Capital market line is valid only for efficient portfolios while security market line is valid

for all portfolios and all individual securities as well. CML is the basis of the capital market

theory while SML is the basis of the capital asset pricing model.

PRICING OF SECURITIES WITH CAPM

The capital asset pricing model can also be used for evaluating the pricing of

securities. The CAPM provides a framework for assessing whether a security is underpriced,

overpriced or correctly priced. According to CAPM, each security is expected to provide a

return commensurate with its level of risk. A security may be offering more returns than the

expected return, making it more attractive. On the contrary, another security may be offering

less return than the expected return, making it less attractive.

The expected return on a security can be calculating using the CAPM formula. Let us

designate it as the theoretical return. The real rate of return estimated to be realsied from

investing in a security can be calculated by the following formula.

Ri = (P1 – P0) + D1

P0

Where

P0 = Current market price.

P1 = Estimated market price after one year

D1 = Anticipated dividend for the year.

This may be designated as the estimated return.

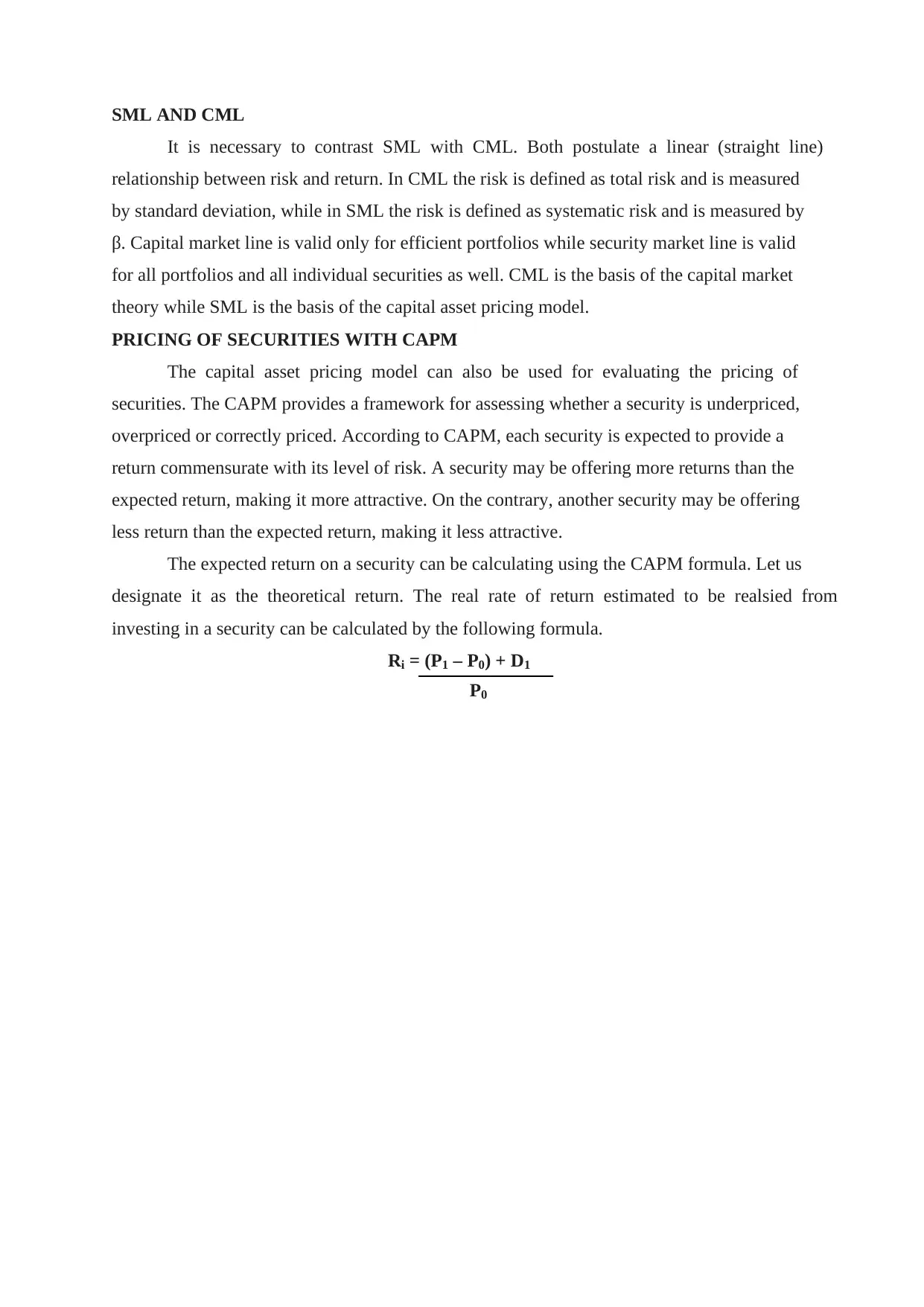

The CAPM framework for evaluation of pricing of securities can be illustrated with

Fig. 2.

Fig. 2. CAPM and Security Valuation

Fig. 2. shows the security market line. Beta values are plotted on the X axis, while

estimated returns are plotted on the Y axis. Nine securities are plotted on the graph according

to their beta values and estimated return values.

Securities A, L and P are in the same risk class having an identical beta value of 0.7.

The security market line shows the expected return for each level of risk. Security L plots on

the SML indicating that the estimated return and expected return on security L is identical.

Security A plots above the SML indicating that its estimated return is higher than its

theoretical return. It is offering higher return than what is commensurate with its risk. Hence,

it is attractive and is presumed to be underpriced. Stock P which plots below the SML has an

estimated return which is lower than its theoretical or expected return. This makes it

undesirable. The security may be considered to be overpriced.

Securities B, M and Q constitute a set of securities in the same risk class. Security B

may be assumed to be underpriced because it offers more return than expected, while security

Q may be assumed to be overpriced as it offers lower return than that expected on the basis of

its risk. Security M can be considered to be correctly priced as it provides a return

commensurate with its risk.

P0 = Current market price.

P1 = Estimated market price after one year

D1 = Anticipated dividend for the year.

This may be designated as the estimated return.

The CAPM framework for evaluation of pricing of securities can be illustrated with

Fig. 2.

Fig. 2. CAPM and Security Valuation

Fig. 2. shows the security market line. Beta values are plotted on the X axis, while

estimated returns are plotted on the Y axis. Nine securities are plotted on the graph according

to their beta values and estimated return values.

Securities A, L and P are in the same risk class having an identical beta value of 0.7.

The security market line shows the expected return for each level of risk. Security L plots on

the SML indicating that the estimated return and expected return on security L is identical.

Security A plots above the SML indicating that its estimated return is higher than its

theoretical return. It is offering higher return than what is commensurate with its risk. Hence,

it is attractive and is presumed to be underpriced. Stock P which plots below the SML has an

estimated return which is lower than its theoretical or expected return. This makes it

undesirable. The security may be considered to be overpriced.

Securities B, M and Q constitute a set of securities in the same risk class. Security B

may be assumed to be underpriced because it offers more return than expected, while security

Q may be assumed to be overpriced as it offers lower return than that expected on the basis of

its risk. Security M can be considered to be correctly priced as it provides a return

commensurate with its risk.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Securities C,N and R constitute another set of securities belonging to the same risk

class, each having a beta value of 1.3. It can be seen that security C is underpriced, security R

is overpriced and security N is correctly priced.

Thus, in the context of the security market line, securities that plot above the line

presumably are underpriced because they offer a higher return than that expected from

securities with same risk. On the other hand, a security is presumably overpriced if it plots

below the SML because it is estimated to provide a lower return than that expected from

securities in the same risk class. Securities which plot on SML are assumed to be

appropriately priced in the context of CAPM. These securities are offering returns in line

with their riskiness.

Securities plotting off the security market line would be evidence of mispricing in the

market place. CAPM can be used to identify and overpriced securities. If the expected return

on a security calculated according to CAPM is lower than the actual or estimated return

offered by that security, the security will be considered to be underpriced. On the contrary, a

security will be considered to be overpriced when the expected return on the security

according to CAPM formulation is higher than the actual return offered by the security.

Let us consider an example. The estimated rates of return and beta coefficients of

some securities are as given below:

Security Estimated returns (per cent) Beta

A 30 1.6

B 24 1.4

C 18 1.2

D 15 0.9

E 15 1.1

F 12 0.7

The risk free rate of return is 10 per cent; while the market return is expected to be 18

per cent.

We can use CAPM to determine which of these securities are correctly priced. For

this we have to calculate the expected return on each security using the CAPM equation.

Ri = Rf + βi [Rm - Rf )

Given that Rf = 10 and Rm = 18

The equation becomes

Ri = 10 + βi (18 – 10)

The expected return on security A can be calculated by substituting the beta value of

security A in the equation. Thus,

class, each having a beta value of 1.3. It can be seen that security C is underpriced, security R

is overpriced and security N is correctly priced.

Thus, in the context of the security market line, securities that plot above the line

presumably are underpriced because they offer a higher return than that expected from

securities with same risk. On the other hand, a security is presumably overpriced if it plots

below the SML because it is estimated to provide a lower return than that expected from

securities in the same risk class. Securities which plot on SML are assumed to be

appropriately priced in the context of CAPM. These securities are offering returns in line

with their riskiness.

Securities plotting off the security market line would be evidence of mispricing in the

market place. CAPM can be used to identify and overpriced securities. If the expected return

on a security calculated according to CAPM is lower than the actual or estimated return

offered by that security, the security will be considered to be underpriced. On the contrary, a

security will be considered to be overpriced when the expected return on the security

according to CAPM formulation is higher than the actual return offered by the security.

Let us consider an example. The estimated rates of return and beta coefficients of

some securities are as given below:

Security Estimated returns (per cent) Beta

A 30 1.6

B 24 1.4

C 18 1.2

D 15 0.9

E 15 1.1

F 12 0.7

The risk free rate of return is 10 per cent; while the market return is expected to be 18

per cent.

We can use CAPM to determine which of these securities are correctly priced. For

this we have to calculate the expected return on each security using the CAPM equation.

Ri = Rf + βi [Rm - Rf )

Given that Rf = 10 and Rm = 18

The equation becomes

Ri = 10 + βi (18 – 10)

The expected return on security A can be calculated by substituting the beta value of

security A in the equation. Thus,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Ri = 10 + βi (18 – 10)

= 10 + 12.8

= 22.8

Similarly, the expected return on each security can be calculated by substituting the

beta value of each security in the equation.

The expected return according to CAPM formula and the estimated return of each

security are tabulated below:

Security Estimated return (CAPM) Estimated return

A 22.8 30

B 21.2 24

C 19.6 18

D 17.2 15

E 18.8 15

F 15.6 12

Securities A and B provide more return than the expected return and hence may be

assumed to be underpriced. Securities C,D,E and F may be assumed to be overpriced as each

of them provides lower return compared to the expected return.

In this chapter we have seen two equations representing risk return relationships. The

first of these was the capital market line which describes the risk return relationship for

efficient portfolios. The second was the security market line describing the risk return

relationship for all portfolios as well as individual securities. This formula is also known as

the capital asset pricing model or CAPM. It postulates that every security is expected to earn

a return commensurate with its risk as measured by beta. CAPM establishes a linear

relationship between the expected return and systematic risk of all assets. This relation can be

used to evaluate the pricing of assets.

Difference between CML & SML

CML SML

The CML is a line that is used to show the

rates of return, which depends on risk-free

rates of return and levels of risk for a specific

portfolio

SML, which is also called a Characteristic

Line, is a graphical representation of the

market's risk and return at a given time.

Standard deviation is the measure of risk for

CML.

Beta coefficient determines the risk factors of

the SML.

The CML measures the risk through standard

deviation, or through a total risk factor.

The SML measures the risk through beta,

which helps to find the security’s risk

contribution for the portfolio.

= 10 + 12.8

= 22.8

Similarly, the expected return on each security can be calculated by substituting the

beta value of each security in the equation.

The expected return according to CAPM formula and the estimated return of each

security are tabulated below:

Security Estimated return (CAPM) Estimated return

A 22.8 30

B 21.2 24

C 19.6 18

D 17.2 15

E 18.8 15

F 15.6 12

Securities A and B provide more return than the expected return and hence may be

assumed to be underpriced. Securities C,D,E and F may be assumed to be overpriced as each

of them provides lower return compared to the expected return.

In this chapter we have seen two equations representing risk return relationships. The

first of these was the capital market line which describes the risk return relationship for

efficient portfolios. The second was the security market line describing the risk return

relationship for all portfolios as well as individual securities. This formula is also known as

the capital asset pricing model or CAPM. It postulates that every security is expected to earn

a return commensurate with its risk as measured by beta. CAPM establishes a linear

relationship between the expected return and systematic risk of all assets. This relation can be

used to evaluate the pricing of assets.

Difference between CML & SML

CML SML

The CML is a line that is used to show the

rates of return, which depends on risk-free

rates of return and levels of risk for a specific

portfolio

SML, which is also called a Characteristic

Line, is a graphical representation of the

market's risk and return at a given time.

Standard deviation is the measure of risk for

CML.

Beta coefficient determines the risk factors of

the SML.

The CML measures the risk through standard

deviation, or through a total risk factor.

The SML measures the risk through beta,

which helps to find the security’s risk

contribution for the portfolio.

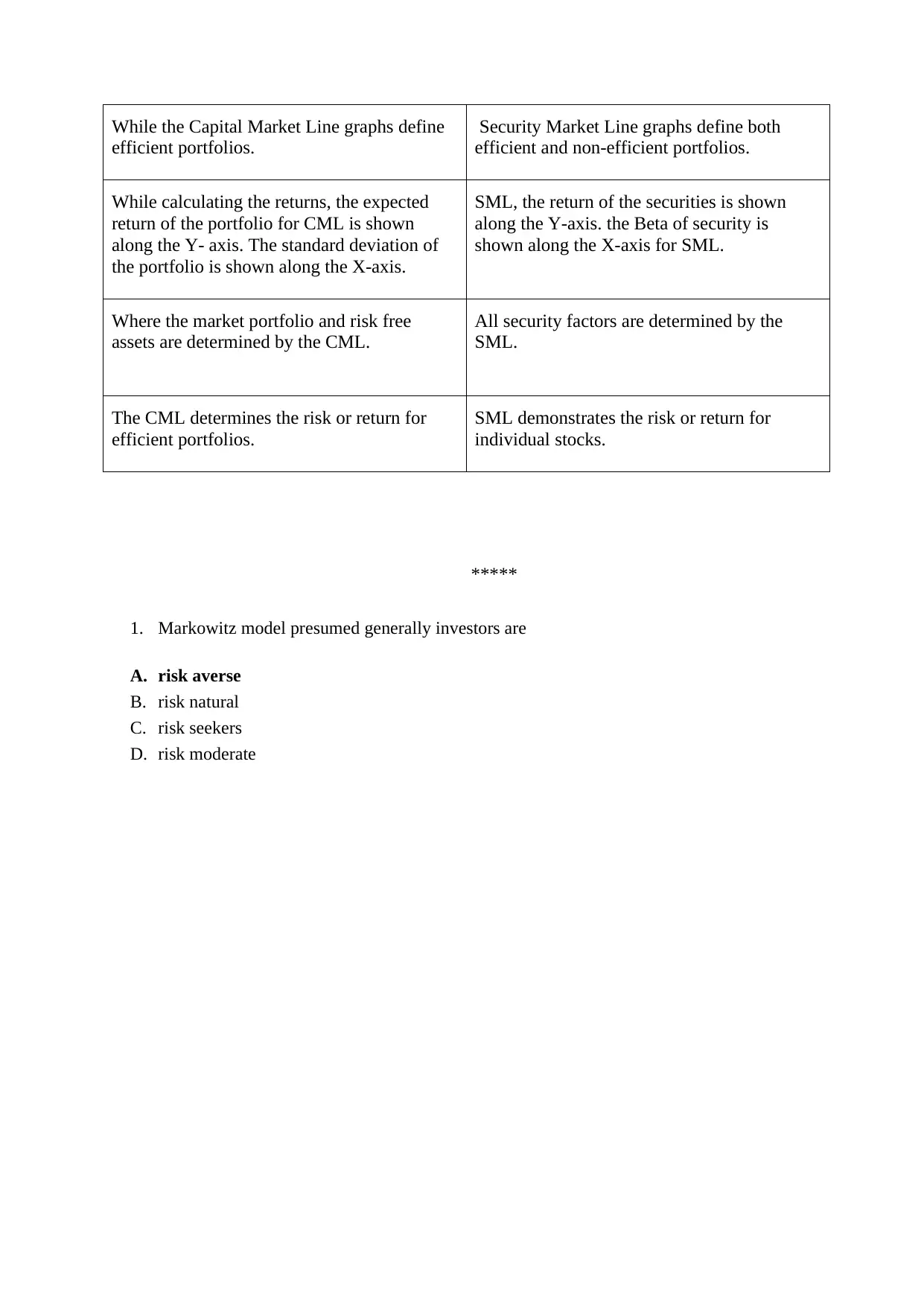

While the Capital Market Line graphs define

efficient portfolios.

Security Market Line graphs define both

efficient and non-efficient portfolios.

While calculating the returns, the expected

return of the portfolio for CML is shown

along the Y- axis. The standard deviation of

the portfolio is shown along the X-axis.

SML, the return of the securities is shown

along the Y-axis. the Beta of security is

shown along the X-axis for SML.

Where the market portfolio and risk free

assets are determined by the CML.

All security factors are determined by the

SML.

The CML determines the risk or return for

efficient portfolios.

SML demonstrates the risk or return for

individual stocks.

*****

1. Markowitz model presumed generally investors are

A. risk averse

B. risk natural

C. risk seekers

D. risk moderate

efficient portfolios.

Security Market Line graphs define both

efficient and non-efficient portfolios.

While calculating the returns, the expected

return of the portfolio for CML is shown

along the Y- axis. The standard deviation of

the portfolio is shown along the X-axis.

SML, the return of the securities is shown

along the Y-axis. the Beta of security is

shown along the X-axis for SML.

Where the market portfolio and risk free

assets are determined by the CML.

All security factors are determined by the

SML.

The CML determines the risk or return for

efficient portfolios.

SML demonstrates the risk or return for

individual stocks.

*****

1. Markowitz model presumed generally investors are

A. risk averse

B. risk natural

C. risk seekers

D. risk moderate

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.