Capital Asset Pricing Model (CAPM) Theory Testing and Analysis Report

VerifiedAdded on 2020/01/15

|18

|3072

|254

Report

AI Summary

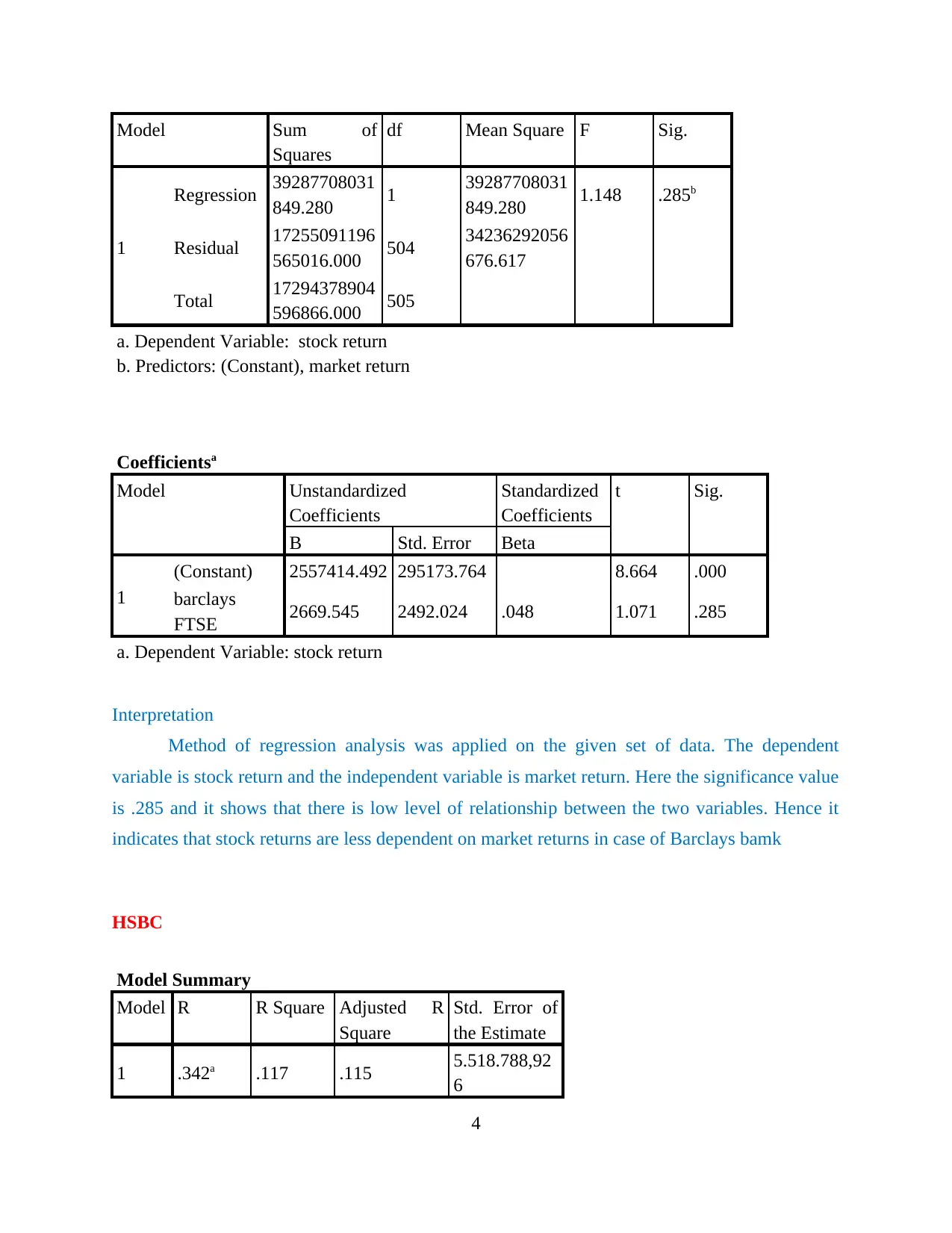

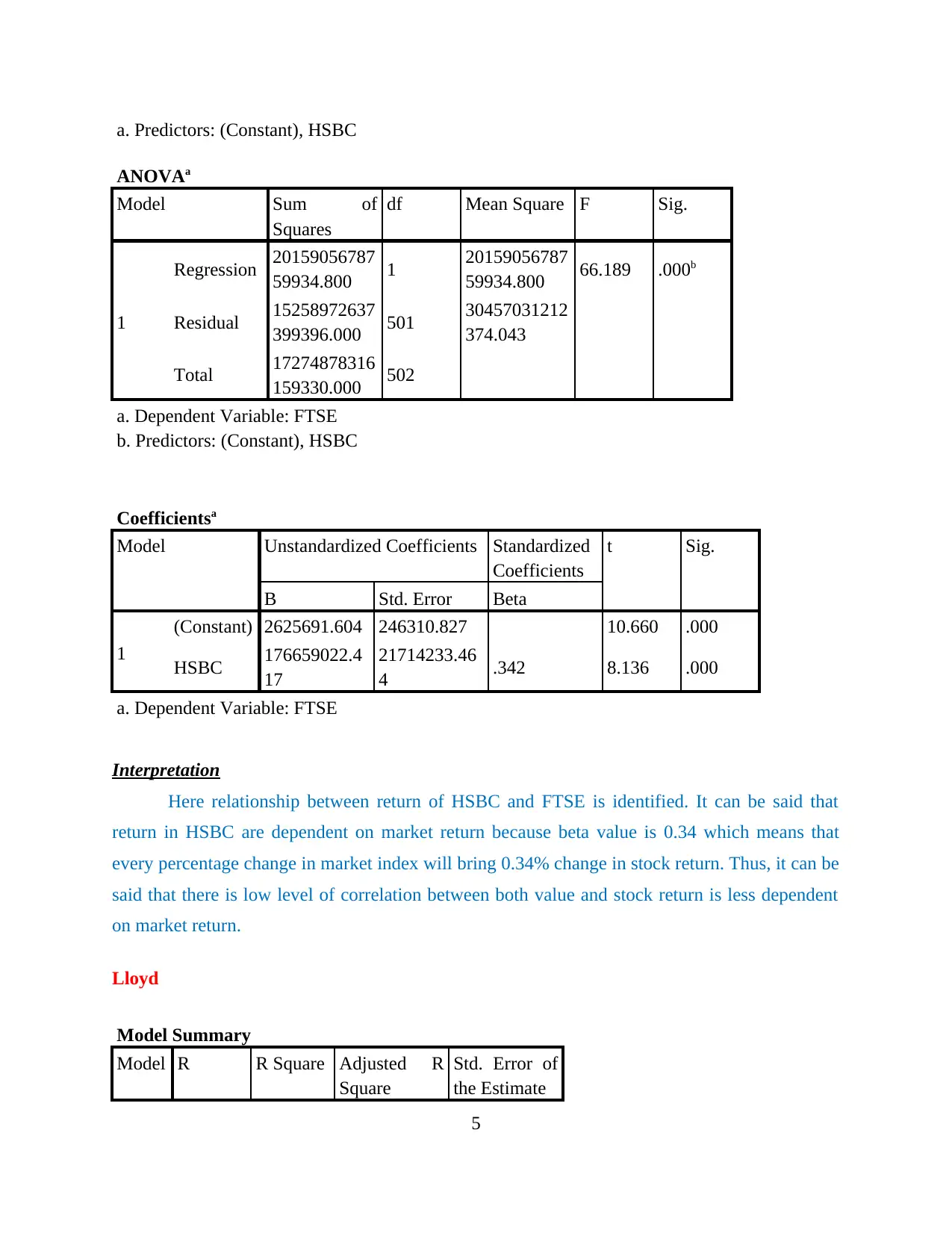

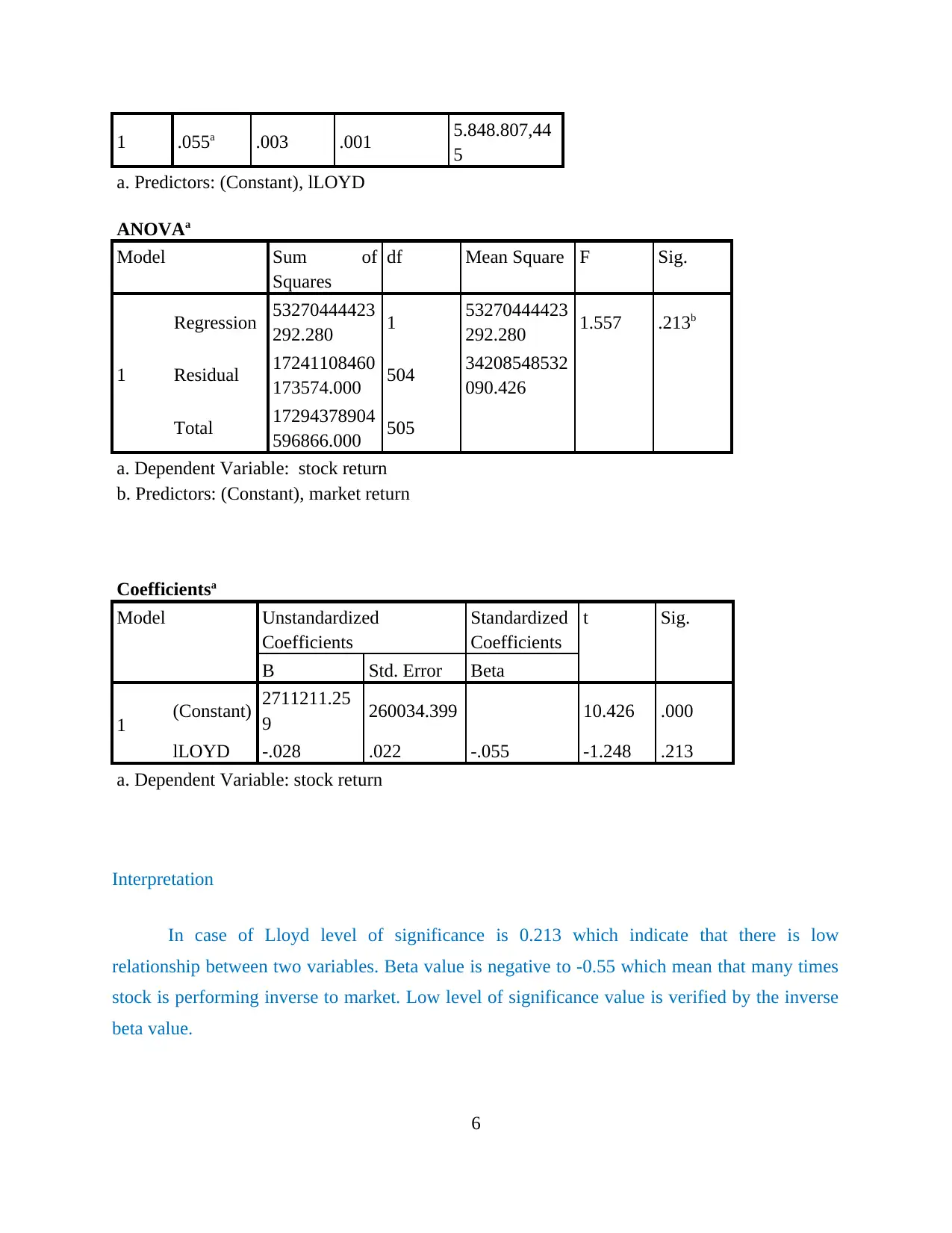

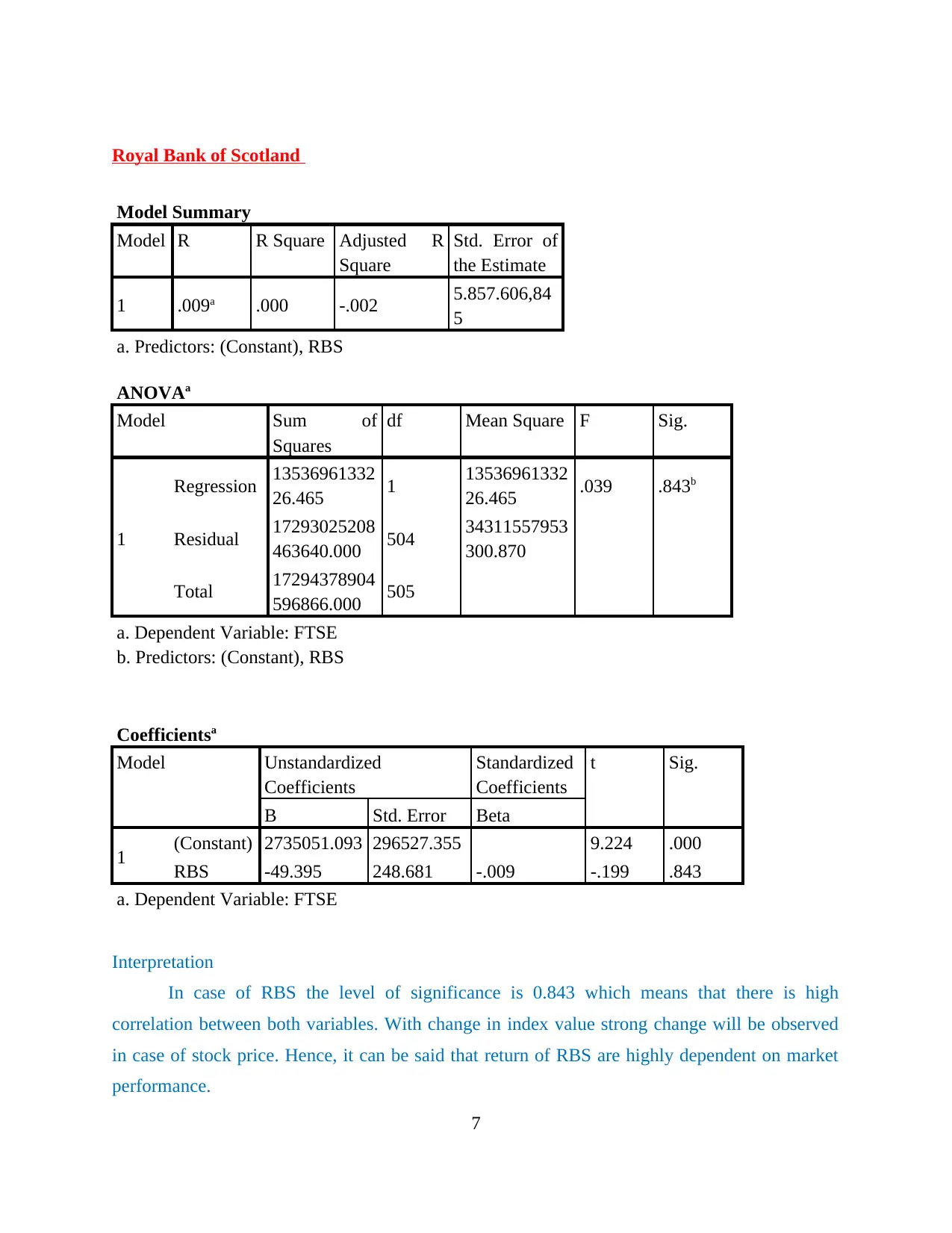

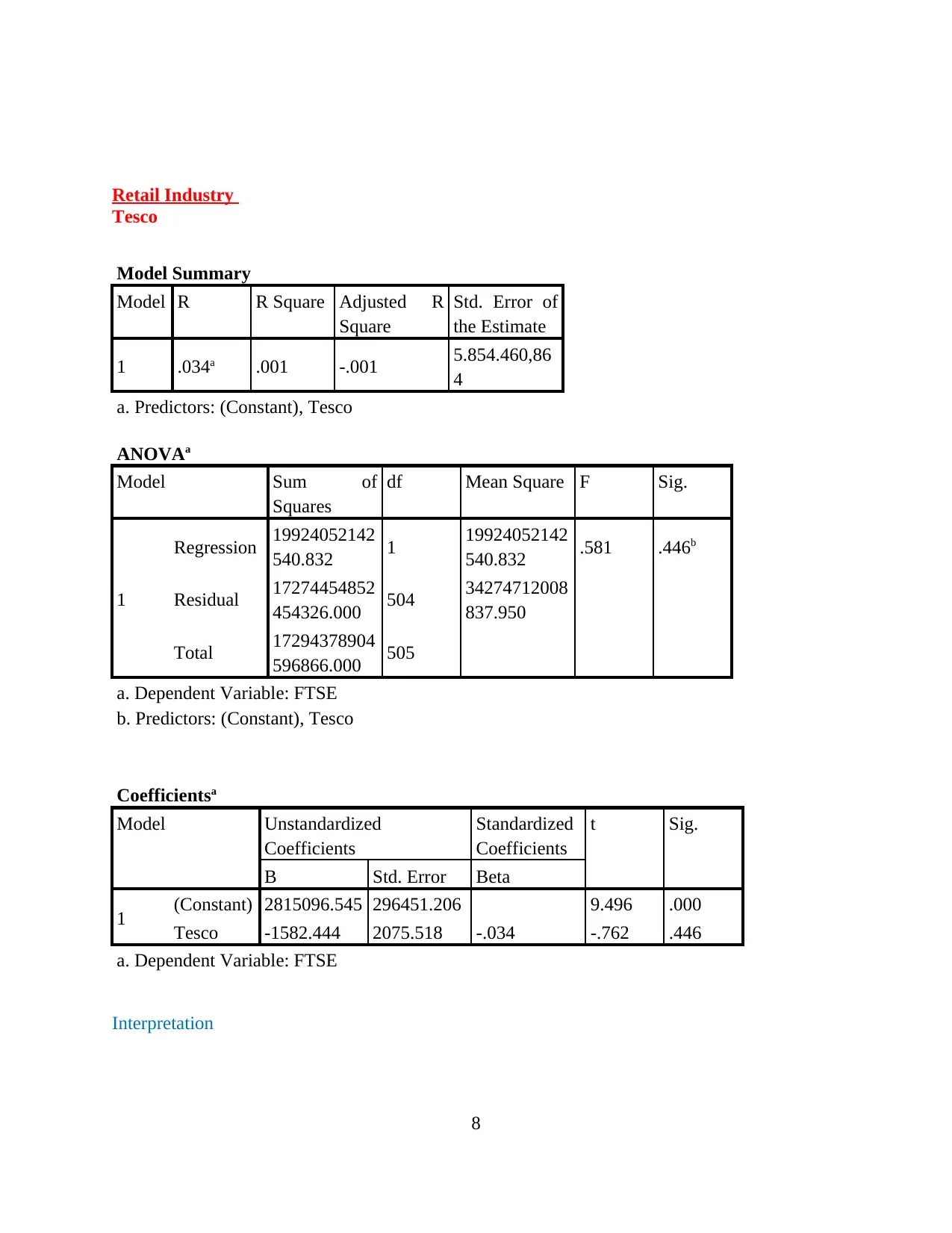

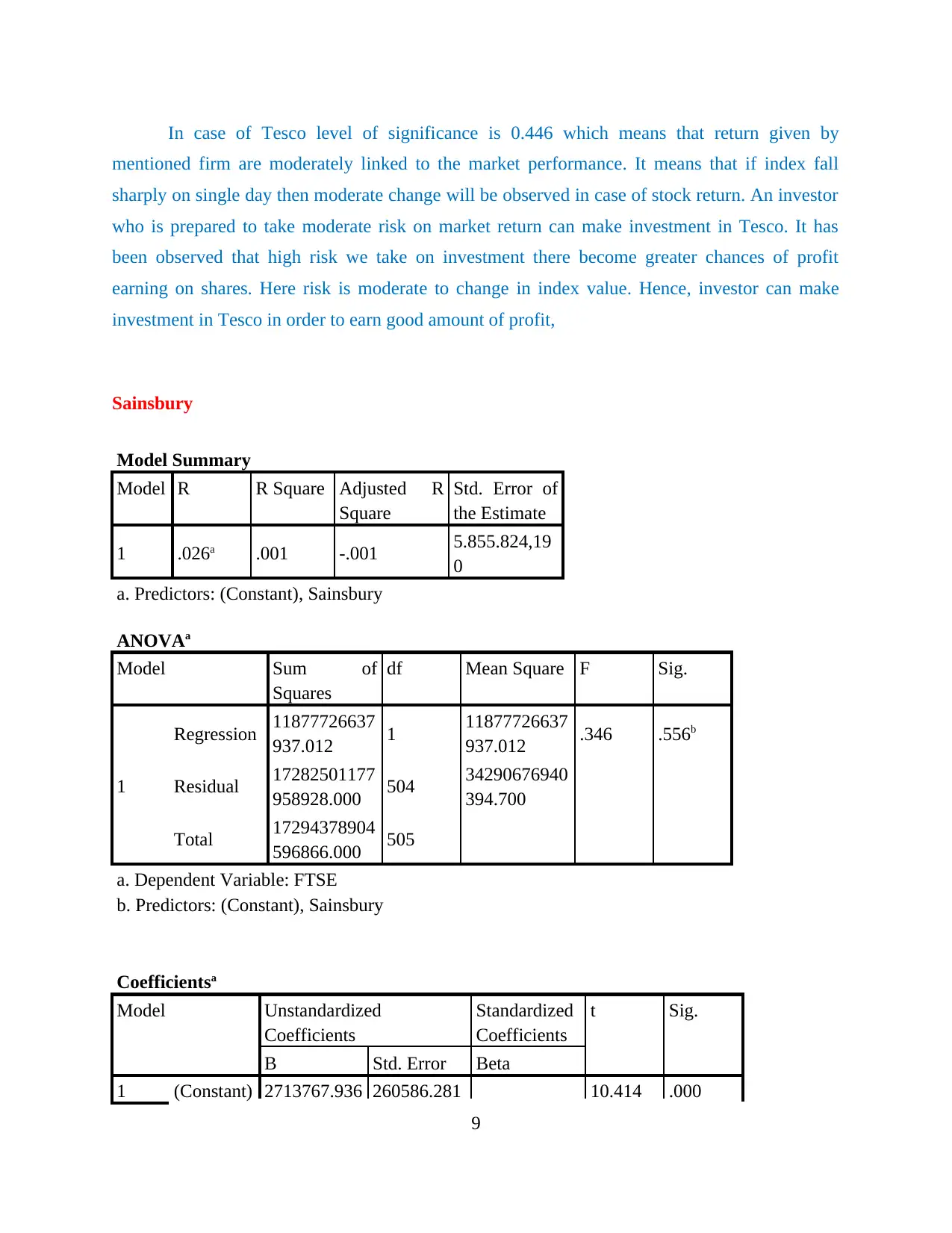

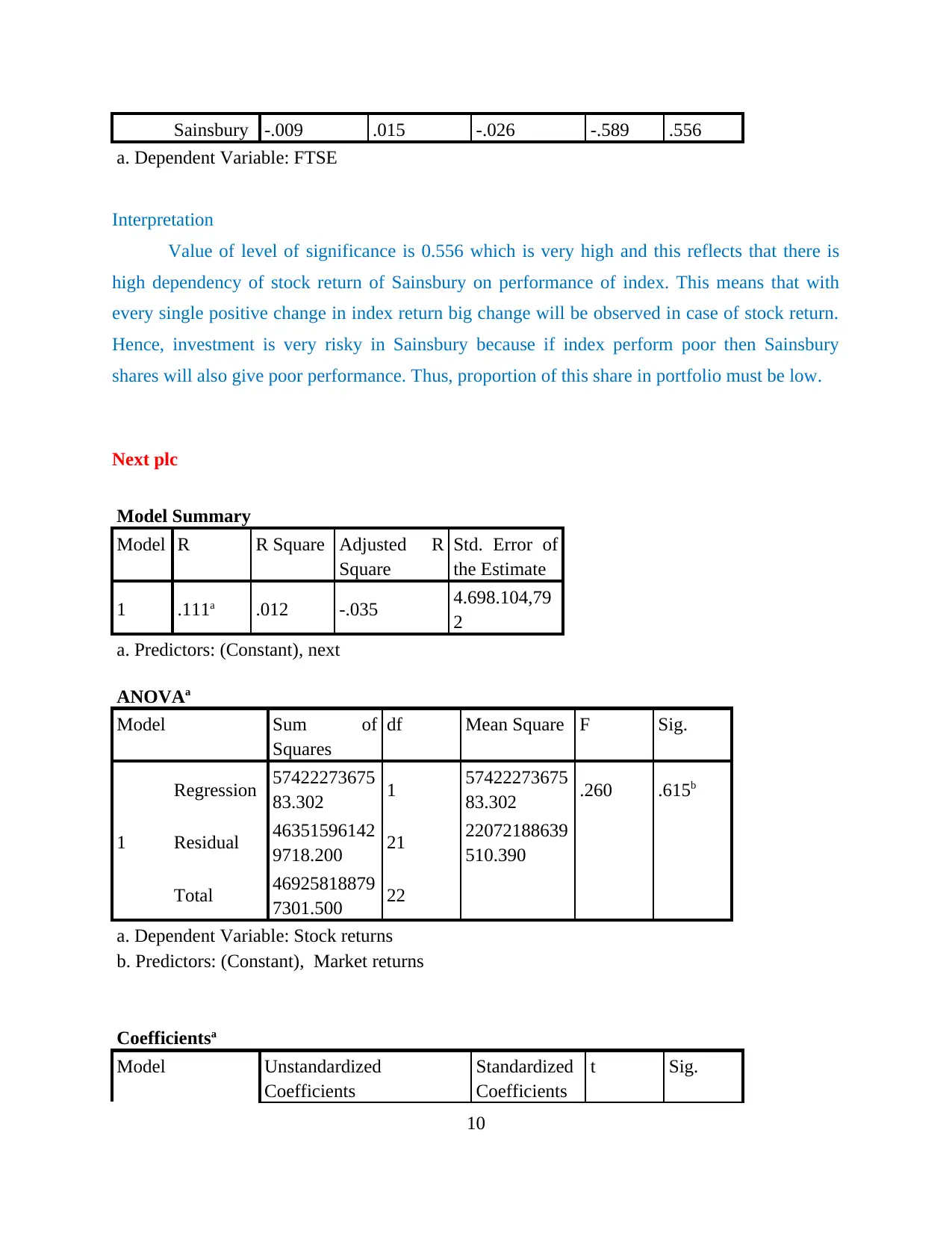

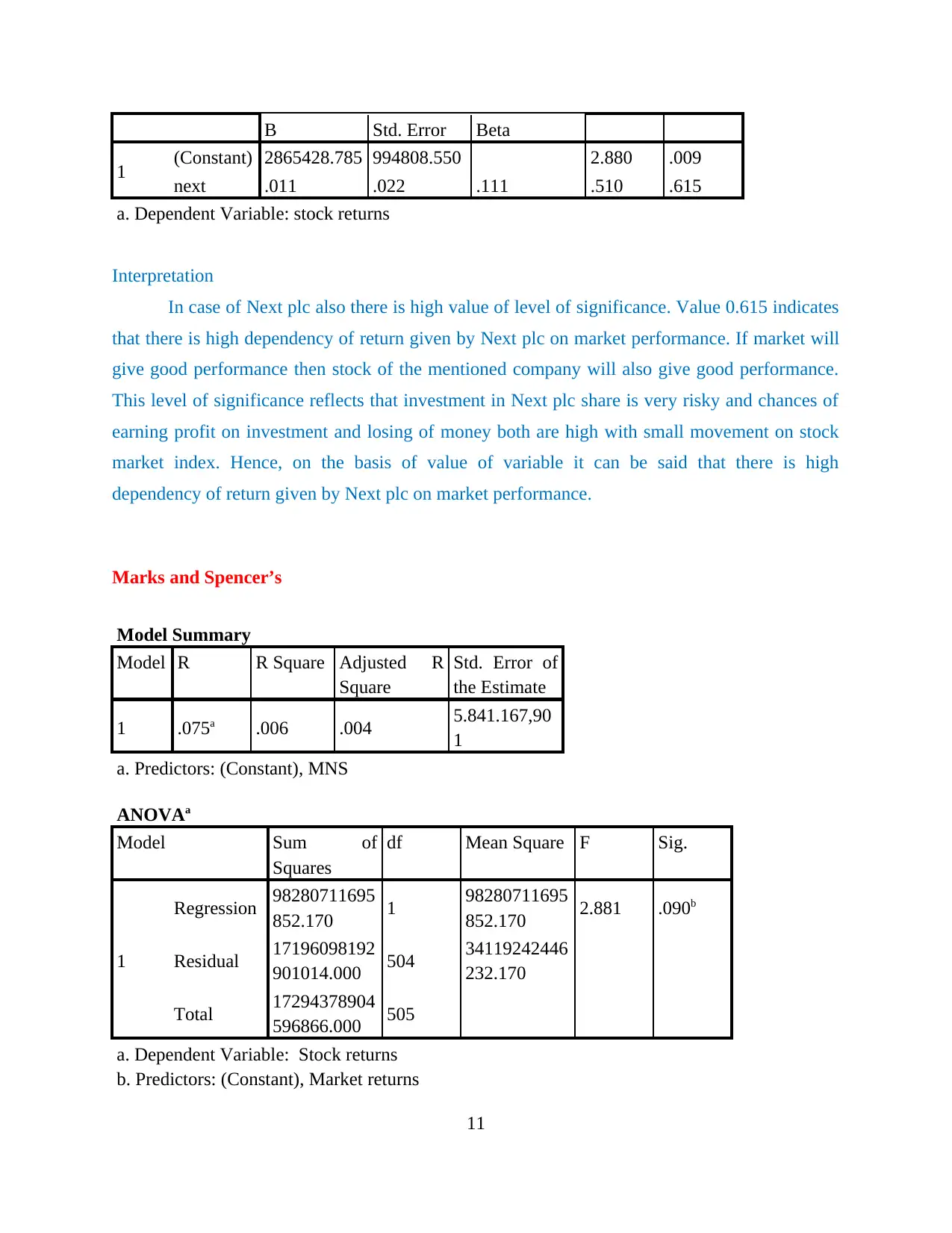

This report presents a comprehensive analysis of the Capital Asset Pricing Model (CAPM) theory. It utilizes financial data from 12 companies and a market index to test the validity of the model. The methodology involves time series regression analysis, with a focus on key statistical measures such as the t-statistic for alpha and the R-squared value for each company. The report provides detailed interpretations of the regression results for each company, including Barclays, HSBC, Lloyd, Royal Bank of Scotland, Tesco, Sainsbury, Next plc, Marks and Spencer’s, Thomas Cook, Virgin airlines, and Ryanair, examining the relationship between stock returns and market returns. Furthermore, the report discusses the merits and demerits of the CAPM analysis, offering a critical evaluation of the model's application and limitations in the context of the provided data.

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.