Financial Impact Analysis: Carart Ltd. Bonus Declaration Report

VerifiedAdded on 2020/01/23

|7

|1948

|67

Report

AI Summary

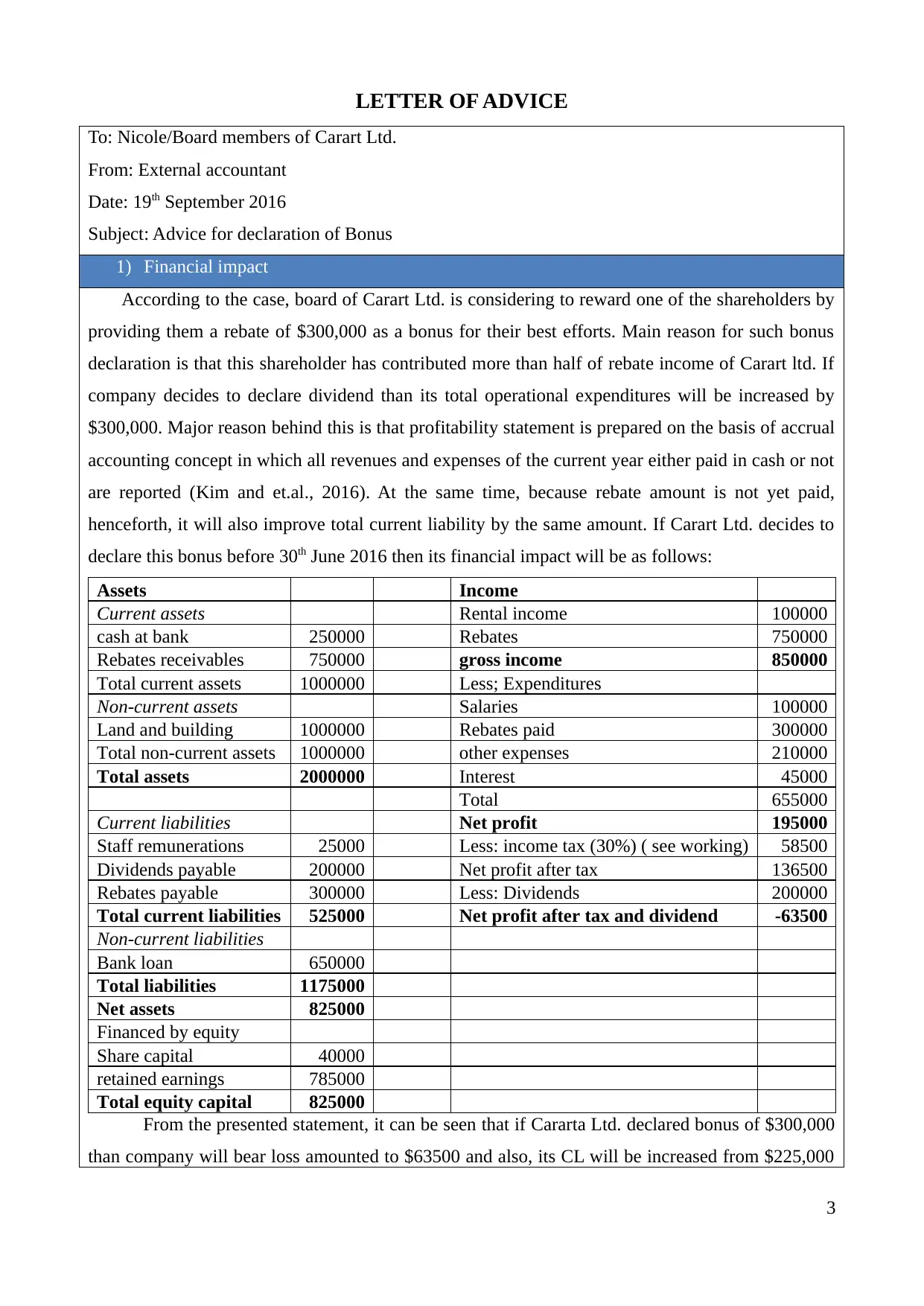

This report analyzes the financial implications of Carart Ltd.'s decision to declare a bonus of $300,000 to a shareholder. It examines the impact on the company's financial statements, including assets, liabilities, income, and equity. The analysis reveals that the bonus declaration would result in a net loss, decreased net assets, and an increase in current liabilities. The report also discusses earning management, highlighting how the bonus decision could negatively impact stakeholders, such as investors and lenders, and potentially violate debt covenants. The study further recommends against the bonus declaration before June 30, 2016, based on the AAA model, which considers profitability, legality, fairness, and sustainability. The report concludes that the bonus decision reflects poor earning management and suggests that it should be postponed to avoid adverse financial and reputational consequences. The analysis relies on financial data, calculations, and relevant accounting principles.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.