Commonwealth Bank and Carbon Reporting: A Financial Perspective

VerifiedAdded on 2022/10/19

|12

|2947

|414

Report

AI Summary

This report examines the crucial role of carbon credits and carbon liabilities within the framework of financial reporting, particularly in the context of Australian Accounting Standards Board (AASB) standards. It provides a comprehensive overview of the AASB 101 and AASB 137 standards, emphasizing their importance in disclosing environmental-related information and potential future liabilities. The report delves into the recognition and measurement of carbon credits and liabilities, offering insights into how organizations like the Commonwealth Bank of Australia address these issues in their annual reports. It analyzes a carbon-related issue reported by the Commonwealth Bank, providing comments on appropriate disclosure, and explores the investor's perspective in evaluating such disclosures. The report underscores the significance of the conceptual framework in disclosing material information to stakeholders, concluding with a discussion on the implications of these practices for financial performance and environmental sustainability.

Company and Financial reporting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive summary

The AASB is one of the most important accounting body that is set by the government of the

country so as to identify and develop the accounting standard for the purpose of better

development of the accounting disclosures. The accounting standard helps in giving the best

disclosure of the financial statements of the company to the users which includes the

stakeholders of the company. The AASB 101 helps in providing the disclosure of environment

related fundamentals and the steps taken by the company to reduce the same. also, the AASB

137 should be followed by the companies to identify the liability that may occur in future to the

companies which may be related to the environment protection and other factors. Also, the

conceptual framework must be followed by the company so that they are able to disclose the

material information related to the company to the stakeholders of the company.

The AASB is one of the most important accounting body that is set by the government of the

country so as to identify and develop the accounting standard for the purpose of better

development of the accounting disclosures. The accounting standard helps in giving the best

disclosure of the financial statements of the company to the users which includes the

stakeholders of the company. The AASB 101 helps in providing the disclosure of environment

related fundamentals and the steps taken by the company to reduce the same. also, the AASB

137 should be followed by the companies to identify the liability that may occur in future to the

companies which may be related to the environment protection and other factors. Also, the

conceptual framework must be followed by the company so that they are able to disclose the

material information related to the company to the stakeholders of the company.

Contents

Executive summary.........................................................................................................................2

Contents...........................................................................................................................................3

Introduction......................................................................................................................................4

Main body........................................................................................................................................5

Part A...............................................................................................................................................5

Discuss whether carbon credits and carbon liabilities should be presented in annual report of a

corporation...................................................................................................................................5

Recognition and measurement of carbon credits by an entity.....................................................6

Recognition and measurement of carbon liabilities by an entity.................................................7

PART B...........................................................................................................................................8

Example of a carbon-related issue that is reported in the annual report of Common wealth

bank of Australia along with comments related to appropriate disclosure..................................8

Perspective of the investor and evaluation of disclosure towards asset, liabilities and financial

performance of organization......................................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

Executive summary.........................................................................................................................2

Contents...........................................................................................................................................3

Introduction......................................................................................................................................4

Main body........................................................................................................................................5

Part A...............................................................................................................................................5

Discuss whether carbon credits and carbon liabilities should be presented in annual report of a

corporation...................................................................................................................................5

Recognition and measurement of carbon credits by an entity.....................................................6

Recognition and measurement of carbon liabilities by an entity.................................................7

PART B...........................................................................................................................................8

Example of a carbon-related issue that is reported in the annual report of Common wealth

bank of Australia along with comments related to appropriate disclosure..................................8

Perspective of the investor and evaluation of disclosure towards asset, liabilities and financial

performance of organization......................................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

Accounting standard refers to a set of principles, policies, and standards that define the basic

steps of financial accounting. Moreover, this is beneficial for a country for improving

transparency in financial transactions and reporting of them. AASB exists in Australia which

works as a board or committee. The main agenda of the Australian accounting standard is to

formulate and maintain financial reporting acts for Australia. They are applied in both public as

well as private sector of Australia. This report is written from the perspective of the

commonwealth bank of Australia which provides financial and investment services to its clients.

Further, the major focus of this report is on the issue of carbon credits and carbon liabilities.

Along with this there an example will also be considered for understanding the disclosures of

assets and liabilities of an organization.

Accounting standard refers to a set of principles, policies, and standards that define the basic

steps of financial accounting. Moreover, this is beneficial for a country for improving

transparency in financial transactions and reporting of them. AASB exists in Australia which

works as a board or committee. The main agenda of the Australian accounting standard is to

formulate and maintain financial reporting acts for Australia. They are applied in both public as

well as private sector of Australia. This report is written from the perspective of the

commonwealth bank of Australia which provides financial and investment services to its clients.

Further, the major focus of this report is on the issue of carbon credits and carbon liabilities.

Along with this there an example will also be considered for understanding the disclosures of

assets and liabilities of an organization.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Main body

Part A

Discuss whether carbon credits and carbon liabilities should be presented in annual report of a

corporation.

Carbon credits in Australia work as a permit for an organisation that provides to emanate carbon

dioxide and other gases. In the present scenario, it is mandatory for all organisations to holds

such a certificate to perform their operations constantly in a country. The main agenda to

implement carbon credits in a country is to minimize the emission of harmful gases from the

environment. Commonwealth Bank of Australia is focused and executed all rules to gain or

collect the carbon credit certificate from the ruling Australian government (ASB and Business,

2018).

AASB101 impacts on various function of an organisation, therefore, this is important for them to

make an effective statement for a business entity. This statement undertakes all statements for

ensuring all capabilities of existing as well as previous financial reports of an organisation.

Commonwealth Bank of Australia develops effective statements for the organisation to prepare

financial reports by undertaking all essential guidelines and requirements that are needed by

organisation to develop effective content. Whereas, disclosure, measurement and recognition

acts are different from presentation of financial which will also be discussed in later part of these

report. An organisation must include carbon credits in organisation due to which it is easy for

stakeholders to taking further decision such as about the investment and performance of them

towards organisational aspect (ASB, et. al., 2018).

Carbon liability of an organisation relates with the approximate value which is needed to be pay

by organisation for economic extension and realization of harmful gases in the environment.

Moreover, in present scenario most of the corporation are performing their work at a global

level. It determines that all activities of an organisation impact on the environment of the overall

globe. To overcome this management of commonwealth bank focused on formulating effective

budgets. Like with expanding industrialization from the last two centuries impacts on the globe.

So, company males carbon budget this results it is easy for them to relate their function with its

impacts on natural activities. On the other side while the formulation of balance sheet of

Part A

Discuss whether carbon credits and carbon liabilities should be presented in annual report of a

corporation.

Carbon credits in Australia work as a permit for an organisation that provides to emanate carbon

dioxide and other gases. In the present scenario, it is mandatory for all organisations to holds

such a certificate to perform their operations constantly in a country. The main agenda to

implement carbon credits in a country is to minimize the emission of harmful gases from the

environment. Commonwealth Bank of Australia is focused and executed all rules to gain or

collect the carbon credit certificate from the ruling Australian government (ASB and Business,

2018).

AASB101 impacts on various function of an organisation, therefore, this is important for them to

make an effective statement for a business entity. This statement undertakes all statements for

ensuring all capabilities of existing as well as previous financial reports of an organisation.

Commonwealth Bank of Australia develops effective statements for the organisation to prepare

financial reports by undertaking all essential guidelines and requirements that are needed by

organisation to develop effective content. Whereas, disclosure, measurement and recognition

acts are different from presentation of financial which will also be discussed in later part of these

report. An organisation must include carbon credits in organisation due to which it is easy for

stakeholders to taking further decision such as about the investment and performance of them

towards organisational aspect (ASB, et. al., 2018).

Carbon liability of an organisation relates with the approximate value which is needed to be pay

by organisation for economic extension and realization of harmful gases in the environment.

Moreover, in present scenario most of the corporation are performing their work at a global

level. It determines that all activities of an organisation impact on the environment of the overall

globe. To overcome this management of commonwealth bank focused on formulating effective

budgets. Like with expanding industrialization from the last two centuries impacts on the globe.

So, company males carbon budget this results it is easy for them to relate their function with its

impacts on natural activities. On the other side while the formulation of balance sheet of

common wealth bank of Australia it is important for them to undertake carbon liability. This act

helps them to predict the estimated budget for performing CSR activities in the organisation.

Australia is an organisation that is expanding its day to day their operation to improve its global

economy. So, to maintain them effectively, some of standards are decided by the Australian

accounting standard committee which leads them to complete their work that are favourable for

organization, government and specifically for environment. In the context of carbon liabilities,

AASB 137 is needed to be executed or follow up on common wealth bank of Australia (Bar dill,

and Garrison, 2015). Further, the 137 acts of AASB states that an asset or liability of an

organisation that raises from past events and whose existence is need to confirmed with the

occurrence a non-occurrence of events. Further, they are not in control of a particular entity as it

managed by an industry and government of a country.

Recognition and measurement of carbon credits by an entity

The term carbon credits define the terms which is used by an organization for completion of

several task or operations by minimising its impacts on environmental factors. Common wealth

bank of Australia performing its business effectively in organisation by following, several

activities which is needed to be accomplished by management. This results in increases the

profitability of organisation by increasing its goodwill among customers for completion of their

task effectively. In recent years the livelihoods carbon funds which is a newly launched

investment funds for carbon related to an organisation. A major benefit of carbon funds in

organisation is used to make a sustainable development by overcoming the impacts of emission

gases in organisation (Chand, et. al., 2015).

Livelihoods carbon funds are targeted to improve the economic condition of Africa, Asia, and

America. To implement the improve changes in major continents of the world; the administration

of funds is focused to gather an amount of $ 118 million to restore the economic conditions of all

over the world. Commonwealth is operating their business sector. So, carbon credits are raised

by them in the form of mutual funds. Along with this to recognition them effectively they follow

the principle of additionality, its present investment efforts to develop an organisation

sustainably (Newberry, 2015).

On the other, this is also essential for organisation to calculate or measure the cost of

organisation that is mandatory to pay for implementing carbon credit policy in common wealth

bank of Australia. The accounting standard act of AASB 13 helps an organisation for calculating

helps them to predict the estimated budget for performing CSR activities in the organisation.

Australia is an organisation that is expanding its day to day their operation to improve its global

economy. So, to maintain them effectively, some of standards are decided by the Australian

accounting standard committee which leads them to complete their work that are favourable for

organization, government and specifically for environment. In the context of carbon liabilities,

AASB 137 is needed to be executed or follow up on common wealth bank of Australia (Bar dill,

and Garrison, 2015). Further, the 137 acts of AASB states that an asset or liability of an

organisation that raises from past events and whose existence is need to confirmed with the

occurrence a non-occurrence of events. Further, they are not in control of a particular entity as it

managed by an industry and government of a country.

Recognition and measurement of carbon credits by an entity

The term carbon credits define the terms which is used by an organization for completion of

several task or operations by minimising its impacts on environmental factors. Common wealth

bank of Australia performing its business effectively in organisation by following, several

activities which is needed to be accomplished by management. This results in increases the

profitability of organisation by increasing its goodwill among customers for completion of their

task effectively. In recent years the livelihoods carbon funds which is a newly launched

investment funds for carbon related to an organisation. A major benefit of carbon funds in

organisation is used to make a sustainable development by overcoming the impacts of emission

gases in organisation (Chand, et. al., 2015).

Livelihoods carbon funds are targeted to improve the economic condition of Africa, Asia, and

America. To implement the improve changes in major continents of the world; the administration

of funds is focused to gather an amount of $ 118 million to restore the economic conditions of all

over the world. Commonwealth is operating their business sector. So, carbon credits are raised

by them in the form of mutual funds. Along with this to recognition them effectively they follow

the principle of additionality, its present investment efforts to develop an organisation

sustainably (Newberry, 2015).

On the other, this is also essential for organisation to calculate or measure the cost of

organisation that is mandatory to pay for implementing carbon credit policy in common wealth

bank of Australia. The accounting standard act of AASB 13 helps an organisation for calculating

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the fair value of its operation and function. This act states that fair value of the products or

services must be decided by management. The rational price of the products helps leads common

wealth bank of Australia to purchase and sell their asset in the market. Further, the another

benefit that management easily recognize accurate prices of existing organisational asset and

liabilities. To implement this effectively they measure and monitor dates on which transaction

takes place. These assist them to maintain proper records for completion of their work in a

systematic and sequential manner.

Recognition and measurement of carbon liabilities by an entity

Carbon liabilities are determined as the process to analysis or predict how much pollution is

generated by organization for completion of their work. In present scenario, regular goals are

impacted by a corporation due to its less environmental factors. Therefore, to protect the interest

of local organisation AASB 137 is developed by organisation due to which effective corporation

between organisational government and organisation is maintained. There are several risks are

existing in economic conditions of a country it governs that industry is facing regular changes to

ensure the safety of the environment (Haider, 2015).

In present scenario due to the fast increase in industrialization activities, it is complex for the

environment to breath. This governs an increase in pollution, harmful gases and exploitation of

nature is impacting on environment in a negative way. All of the issues are raised due to the

increase in number of organisation and its activities which work to satisfy human needs.

Common wealth bank of Australia develops its infrastructure in those cities or districts which are

environment friendly (Laing and Perrin, 2014). Along with this some steps which is taken by the

bank are mention as follow:

Management is using only those platforms which are environment friendly and are

essential to manage their portfolio.

Most of the activities of the commonwealth bank of Australia are digitalized that also

release minimum harmful waves towards the environment.

To maintain regulatory change, the organisation is also influencing and increasing

awareness to perform CSR activities among its stakeholders in order to secure the

environment.

services must be decided by management. The rational price of the products helps leads common

wealth bank of Australia to purchase and sell their asset in the market. Further, the another

benefit that management easily recognize accurate prices of existing organisational asset and

liabilities. To implement this effectively they measure and monitor dates on which transaction

takes place. These assist them to maintain proper records for completion of their work in a

systematic and sequential manner.

Recognition and measurement of carbon liabilities by an entity

Carbon liabilities are determined as the process to analysis or predict how much pollution is

generated by organization for completion of their work. In present scenario, regular goals are

impacted by a corporation due to its less environmental factors. Therefore, to protect the interest

of local organisation AASB 137 is developed by organisation due to which effective corporation

between organisational government and organisation is maintained. There are several risks are

existing in economic conditions of a country it governs that industry is facing regular changes to

ensure the safety of the environment (Haider, 2015).

In present scenario due to the fast increase in industrialization activities, it is complex for the

environment to breath. This governs an increase in pollution, harmful gases and exploitation of

nature is impacting on environment in a negative way. All of the issues are raised due to the

increase in number of organisation and its activities which work to satisfy human needs.

Common wealth bank of Australia develops its infrastructure in those cities or districts which are

environment friendly (Laing and Perrin, 2014). Along with this some steps which is taken by the

bank are mention as follow:

Management is using only those platforms which are environment friendly and are

essential to manage their portfolio.

Most of the activities of the commonwealth bank of Australia are digitalized that also

release minimum harmful waves towards the environment.

To maintain regulatory change, the organisation is also influencing and increasing

awareness to perform CSR activities among its stakeholders in order to secure the

environment.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PART B

Example of a carbon-related issue that is reported in the annual report of Common wealth bank

of Australia along with comments related to appropriate disclosure

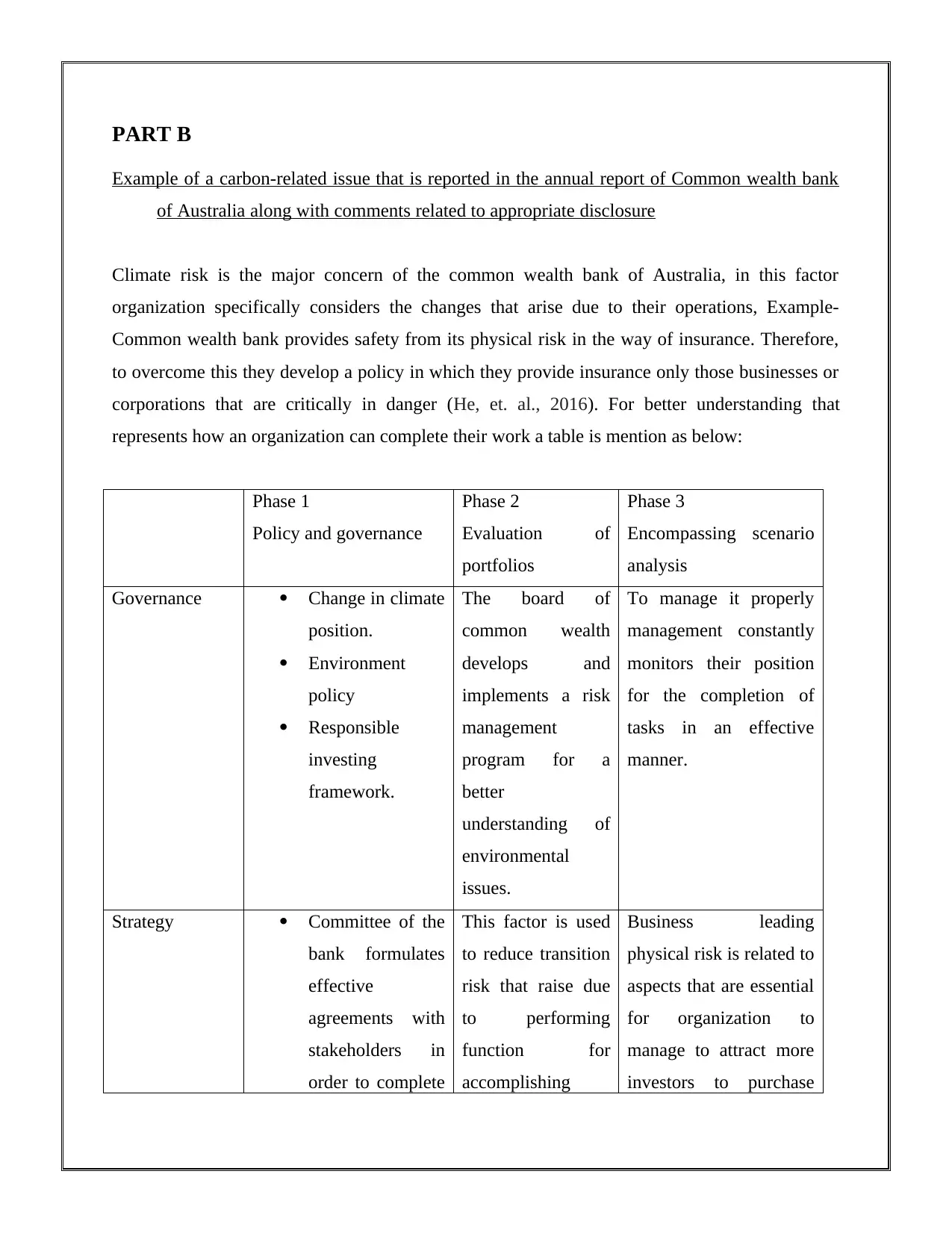

Climate risk is the major concern of the common wealth bank of Australia, in this factor

organization specifically considers the changes that arise due to their operations, Example-

Common wealth bank provides safety from its physical risk in the way of insurance. Therefore,

to overcome this they develop a policy in which they provide insurance only those businesses or

corporations that are critically in danger (He, et. al., 2016). For better understanding that

represents how an organization can complete their work a table is mention as below:

Phase 1

Policy and governance

Phase 2

Evaluation of

portfolios

Phase 3

Encompassing scenario

analysis

Governance Change in climate

position.

Environment

policy

Responsible

investing

framework.

The board of

common wealth

develops and

implements a risk

management

program for a

better

understanding of

environmental

issues.

To manage it properly

management constantly

monitors their position

for the completion of

tasks in an effective

manner.

Strategy Committee of the

bank formulates

effective

agreements with

stakeholders in

order to complete

This factor is used

to reduce transition

risk that raise due

to performing

function for

accomplishing

Business leading

physical risk is related to

aspects that are essential

for organization to

manage to attract more

investors to purchase

Example of a carbon-related issue that is reported in the annual report of Common wealth bank

of Australia along with comments related to appropriate disclosure

Climate risk is the major concern of the common wealth bank of Australia, in this factor

organization specifically considers the changes that arise due to their operations, Example-

Common wealth bank provides safety from its physical risk in the way of insurance. Therefore,

to overcome this they develop a policy in which they provide insurance only those businesses or

corporations that are critically in danger (He, et. al., 2016). For better understanding that

represents how an organization can complete their work a table is mention as below:

Phase 1

Policy and governance

Phase 2

Evaluation of

portfolios

Phase 3

Encompassing scenario

analysis

Governance Change in climate

position.

Environment

policy

Responsible

investing

framework.

The board of

common wealth

develops and

implements a risk

management

program for a

better

understanding of

environmental

issues.

To manage it properly

management constantly

monitors their position

for the completion of

tasks in an effective

manner.

Strategy Committee of the

bank formulates

effective

agreements with

stakeholders in

order to complete

This factor is used

to reduce transition

risk that raise due

to performing

function for

accomplishing

Business leading

physical risk is related to

aspects that are essential

for organization to

manage to attract more

investors to purchase

improve

environmental

conditions.

organisational

goals. Australian

share funds are the

best example of

totally free from

transition risk.

their services. It is more

favourable because it

engages clients for the

completion of their

work.

Prioritization to

risk

management

Elevated and polluted

climate is a major risk

factor for organisation

due to which its financial

and non-financial is

impacted to complete

their work effectively.

ESG risk

assessment process

is executed by

organization for

completing their

work with more

efficiency. To

manage it

effectively

organisation uses

updated

information to

complete their

work.

Physical risk is a major

concern that is related to

the business lending

process. Update

utilization of tools leads

them to complete their

work in minimum time

factor by which

organisation make

changes to deal with

sensitive factors of

climate.

The above-stated table represent that organisation needs to disclose their operations or function

that are related to its carbon credit or liabilities. Commonwealth Bank of Australia follows the

AASB act 116, due to this it is easy for them to disclose all of its assets as well as liabilities

(Iqbal and Iqbal, 2015).

Commonwealth is listed on ASX; therefore, it is essential for them to list all of its asset and

liabilities that are related to economic exposure. Due to this act, it is easy for them to register

maintain environmental and social sustainability for overcoming carbon related factors. The

AASB act of 116 also considers some principle that is listed for completion of work effectively.

It is needed that at least members are considering a decision from majority must be

provided to independent directors.

environmental

conditions.

organisational

goals. Australian

share funds are the

best example of

totally free from

transition risk.

their services. It is more

favourable because it

engages clients for the

completion of their

work.

Prioritization to

risk

management

Elevated and polluted

climate is a major risk

factor for organisation

due to which its financial

and non-financial is

impacted to complete

their work effectively.

ESG risk

assessment process

is executed by

organization for

completing their

work with more

efficiency. To

manage it

effectively

organisation uses

updated

information to

complete their

work.

Physical risk is a major

concern that is related to

the business lending

process. Update

utilization of tools leads

them to complete their

work in minimum time

factor by which

organisation make

changes to deal with

sensitive factors of

climate.

The above-stated table represent that organisation needs to disclose their operations or function

that are related to its carbon credit or liabilities. Commonwealth Bank of Australia follows the

AASB act 116, due to this it is easy for them to disclose all of its assets as well as liabilities

(Iqbal and Iqbal, 2015).

Commonwealth is listed on ASX; therefore, it is essential for them to list all of its asset and

liabilities that are related to economic exposure. Due to this act, it is easy for them to register

maintain environmental and social sustainability for overcoming carbon related factors. The

AASB act of 116 also considers some principle that is listed for completion of work effectively.

It is needed that at least members are considering a decision from majority must be

provided to independent directors.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The top authority such as the independent director is responsible to disclose carbon-

related issues.

Members, as well as the charter of the committee, evaluates and monitor the changes that

raised due to regular issue regulatory modification of carbon-related issue.

Perspective of the investor and evaluation of disclosure towards asset, liabilities and financial

performance of organization

According to the present market, investors are major assets for an organisation that helps them to

achieve huge success in the industry (Joubert, et. al., 2017). Majority of the investor is more

favourable towards the perspective of dealing with organizational carbon-related issue. Some of

the major issue which is needed by organisation for completion of their work in an effective

manner are evaluated on several points that are explained as below:

Climate governance- The first factor which must improve by organisation is related to climate

and its governance need to be approved by the government. It generates trust among investors to

input their money in the market.

Doing business sustainability- To sustain business for a longer period effective services are

provided by banks. Such as commonwealth bank minimize its cost to increase the growth of their

profits.

related issues.

Members, as well as the charter of the committee, evaluates and monitor the changes that

raised due to regular issue regulatory modification of carbon-related issue.

Perspective of the investor and evaluation of disclosure towards asset, liabilities and financial

performance of organization

According to the present market, investors are major assets for an organisation that helps them to

achieve huge success in the industry (Joubert, et. al., 2017). Majority of the investor is more

favourable towards the perspective of dealing with organizational carbon-related issue. Some of

the major issue which is needed by organisation for completion of their work in an effective

manner are evaluated on several points that are explained as below:

Climate governance- The first factor which must improve by organisation is related to climate

and its governance need to be approved by the government. It generates trust among investors to

input their money in the market.

Doing business sustainability- To sustain business for a longer period effective services are

provided by banks. Such as commonwealth bank minimize its cost to increase the growth of their

profits.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONCLUSION

In the end, by monitoring all the above points it is concluded that banks are a crucial part of a

country which helps them to improve their economy. This factor relates to various aspects like

accounting standard of disclosure, accounting standard for fair value measurement and many

more. This all are favourable for a corporation as it helps them to deal with various issue of

carbon and to ensure the environmental safety by reducing negative impacts from climate.

In the end, by monitoring all the above points it is concluded that banks are a crucial part of a

country which helps them to improve their economy. This factor relates to various aspects like

accounting standard of disclosure, accounting standard for fair value measurement and many

more. This all are favourable for a corporation as it helps them to deal with various issue of

carbon and to ensure the environmental safety by reducing negative impacts from climate.

REFERENCES

ASB, A.A.S.B. and Business, B.G., 2018. Achievement and self-direction values, 23À24 Agency

theory, 52, 54 Agenda-setting theory, 165, 166 American economy, 29. small, 16, p.19.

ASB, A.A.S.B., Zone, A.S.E. and Network, B.G.B., 2018. Redefining Corporate Social

Responsibility. Agenda, 52, p.54.

Bar dill, J. and Garrison, N.A., 2015. Naming indigenous concerns, framing considerations for

stored biospecimens. The American Journal of Bioethics, 15(9), pp.73-75.

Chand, P., Patel, A. and White, M., 2015. Adopting international financial reporting standards

for small and medium‐sized enterprises. Australian Accounting Review, 25(2), pp.139-154.

Haider, S., 2015. Exploring the Relationship between Changes in Accounting Policies and

Valuation of Australian Banking Firms (Doctoral dissertation, Victoria University).

He, L., Evans, E. and He, R., 2016. The impact of AASB 8 operating segments on analysts’

earnings forecasts: Australian evidence. Australian Accounting Review, 26(4), pp.330-340.

Iqbal, S. and Iqbal, N., 2015. Financial reporting regime & financial statements antecedents

banking sector case of Pakistan. International Letters of Social and Humanistic Sciences, 59,

pp.126-130.

Joubert, M., Gravies, L. and Parle, G., 2017. Implications of the New Accounting Standard for

Leases AASB 16 (IFRS 16) with the Inclusion of Operating Leases in the Balance Sheet. The

Journal of New Business Ideas & Trends, 15(2), pp.1-11.

Laing, G. and Perrin, R.W., 2014. Deconstructing an accounting paradigm shift: AASB 116 non-

current asset measurement models. International Journal of Critical Accounting, 6(5/6), pp.509-

519.

Newberry, S., 2015. Public sector accounting: shifting concepts of accountability. Public Money

& Management, 35(5), pp.371-376.

ASB, A.A.S.B. and Business, B.G., 2018. Achievement and self-direction values, 23À24 Agency

theory, 52, 54 Agenda-setting theory, 165, 166 American economy, 29. small, 16, p.19.

ASB, A.A.S.B., Zone, A.S.E. and Network, B.G.B., 2018. Redefining Corporate Social

Responsibility. Agenda, 52, p.54.

Bar dill, J. and Garrison, N.A., 2015. Naming indigenous concerns, framing considerations for

stored biospecimens. The American Journal of Bioethics, 15(9), pp.73-75.

Chand, P., Patel, A. and White, M., 2015. Adopting international financial reporting standards

for small and medium‐sized enterprises. Australian Accounting Review, 25(2), pp.139-154.

Haider, S., 2015. Exploring the Relationship between Changes in Accounting Policies and

Valuation of Australian Banking Firms (Doctoral dissertation, Victoria University).

He, L., Evans, E. and He, R., 2016. The impact of AASB 8 operating segments on analysts’

earnings forecasts: Australian evidence. Australian Accounting Review, 26(4), pp.330-340.

Iqbal, S. and Iqbal, N., 2015. Financial reporting regime & financial statements antecedents

banking sector case of Pakistan. International Letters of Social and Humanistic Sciences, 59,

pp.126-130.

Joubert, M., Gravies, L. and Parle, G., 2017. Implications of the New Accounting Standard for

Leases AASB 16 (IFRS 16) with the Inclusion of Operating Leases in the Balance Sheet. The

Journal of New Business Ideas & Trends, 15(2), pp.1-11.

Laing, G. and Perrin, R.W., 2014. Deconstructing an accounting paradigm shift: AASB 116 non-

current asset measurement models. International Journal of Critical Accounting, 6(5/6), pp.509-

519.

Newberry, S., 2015. Public sector accounting: shifting concepts of accountability. Public Money

& Management, 35(5), pp.371-376.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.