MGT723 Research Project: Stakeholder Theory & Carbon Disclosure

VerifiedAdded on 2023/06/14

|10

|1592

|251

Report

AI Summary

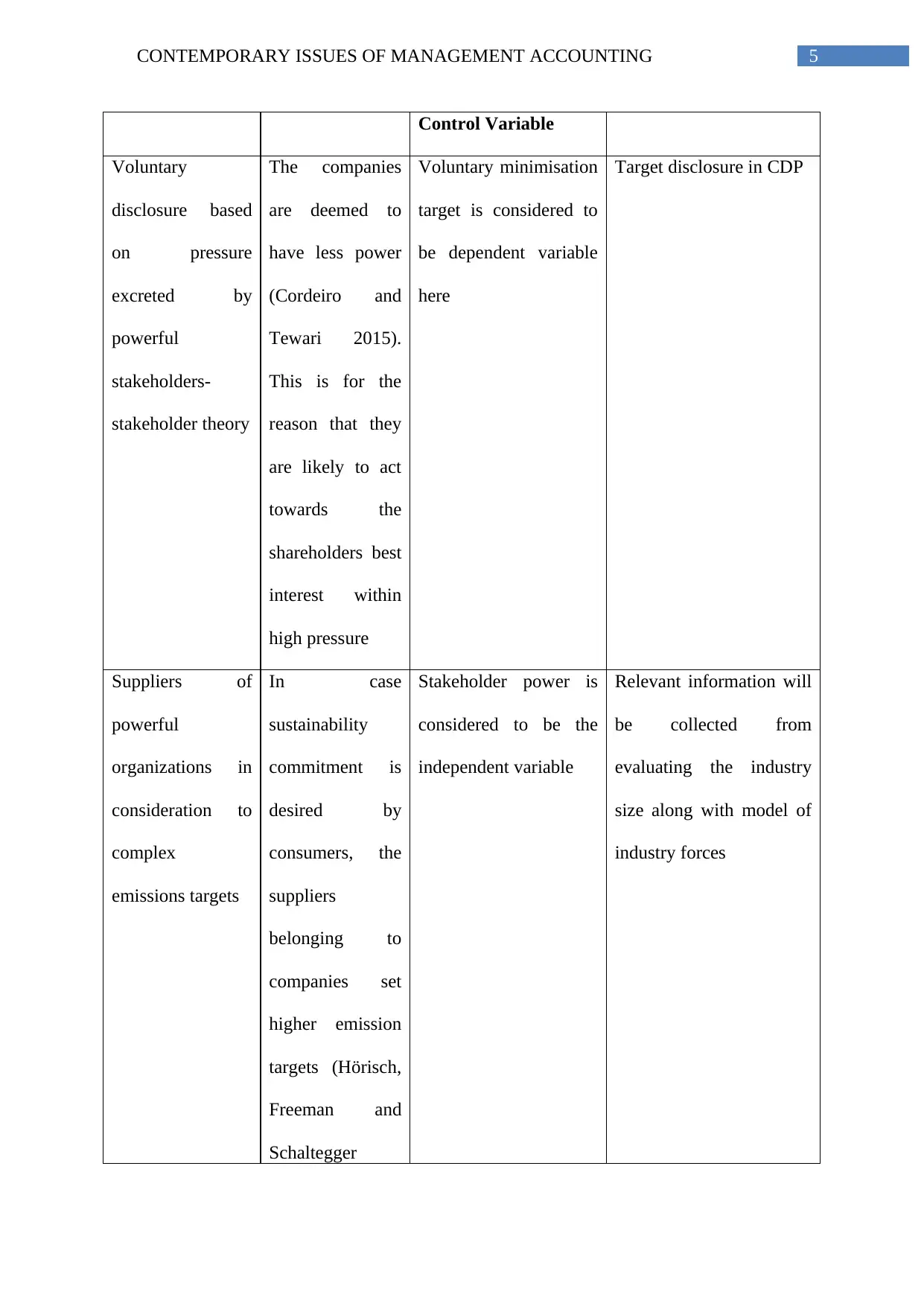

This research proposal investigates the effect of stakeholder theory on carbon disclosure reporting within companies. It begins with a literature review, outlining practical and theoretical motivations for the study, defining stakeholder theory, and identifying key theoretical constructs, dependent (voluntary reduction targets), and independent variables (stakeholder power). A conceptual model is presented, illustrating the relationships between these variables, leading to the formulation of testable hypotheses regarding the association between stakeholder power and voluntary reduction targets, responses of low-powered organizations to powerful stakeholders, and the role of suppliers in complex emission targets. Proxy measures for the theoretical constructs are defined. The research method section details the use of a quantitative approach, employing both primary and secondary data, simple random sampling of 34 managers from UK companies, and data analysis using MS Excel to assess the impact of climate change on stakeholders. The proposal includes an open-ended questionnaire for gathering relevant data from managers regarding their companies' stakeholder theory practices and environmental sustainability initiatives. The goal is to find reliable findings associated with companies' stakeholder theory practice and addressing accounting issues related to environmental sustainability.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.