Carbon Emission Analysis: Agency Theory and Business Impact

VerifiedAdded on 2020/05/28

|20

|3430

|121

Report

AI Summary

This report delves into the intricacies of carbon emissions and their relationship with agency theory, exploring the impact of global warming on the environment and economy. It examines practical and theoretical motivations, focusing on carbon risk management and climate change disclosures. The report reviews existing literature, including agency theory and carbon footprint measurement, to formulate hypotheses regarding the relationship between carbon risk management, the quality of carbon disclosure, and the association between CSR and accounting performance. It also discusses the socio-political and economic-based disclosure theories, providing a comprehensive analysis of the factors influencing environmental performance and corporate responses to climate change challenges. The report concludes by summarizing the key findings and emphasizing the significance of carbon emission management and its implications for businesses and stakeholders.

Running head: CARBON EMISSION AS PER AGENCY THEORY

Carbon Emission as Per Agency Theory

Name of the Student

Name of the University

Authors Note

Course ID

Carbon Emission as Per Agency Theory

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CARBON EMISSION AS PER AGENCY THEORY

Table of Contents

Introduction................................................................................................................................2

Practical Motivation...................................................................................................................2

Theoretical Motivation...............................................................................................................3

Literature Review.......................................................................................................................4

Hypotheses.................................................................................................................................5

Conclusion..................................................................................................................................6

Reference List............................................................................................................................8

Appendix..................................................................................................................................10

Table of Contents

Introduction................................................................................................................................2

Practical Motivation...................................................................................................................2

Theoretical Motivation...............................................................................................................3

Literature Review.......................................................................................................................4

Hypotheses.................................................................................................................................5

Conclusion..................................................................................................................................6

Reference List............................................................................................................................8

Appendix..................................................................................................................................10

2CARBON EMISSION AS PER AGENCY THEORY

Introduction

It is discerned that in general there are several issues which relates to global warming

and its consequence on environment and economy. This particular consideration is seen with

the uniformity of “United Nation Framework Convention on Climate Change (UNFCCC) and

the Kyoto Protocol”. The important agreements to address the global warming are taken into

account with reducing the disclosures pertaining to the GHG emission. The study will

consider the practical motivation and the importance of this practice. The important aspects

of the study will state the theoretical motivation which will address the gaps in the existing

research study. Some of the other aspects of the study is able to depict the relationship

between the identified practical and theoretical motivational factors. The part of the study is

able to evaluate the hypothesis which as related to the selected areas of learning (Golosov et

al. 2014).

Practical Motivation

The important form of the effect of the carbon emission is based on its impact on

general public.

There are many organisations which offers the footprint calculators for public and

corporate use for depiction of carbon footprints of products. This particular consideration is

seen to be important for both accountant’s public in general. As per the number of previous

articles which are seen to be published by “US Environmental Protection Agency” these are

addressed with several issues pertaining to paper, plastic (candy wrappers), glass, cans,

computers, carpet and tires (Liao, Luo and Tang 2015). In Australia the regulators and the

managers pertaining to this consideration has been able to contribute to the number of issues

related to the matters of lumber and other building materials. Several companies and non-

profit making academics have been able to address number of issues pertaining to mailing

Introduction

It is discerned that in general there are several issues which relates to global warming

and its consequence on environment and economy. This particular consideration is seen with

the uniformity of “United Nation Framework Convention on Climate Change (UNFCCC) and

the Kyoto Protocol”. The important agreements to address the global warming are taken into

account with reducing the disclosures pertaining to the GHG emission. The study will

consider the practical motivation and the importance of this practice. The important aspects

of the study will state the theoretical motivation which will address the gaps in the existing

research study. Some of the other aspects of the study is able to depict the relationship

between the identified practical and theoretical motivational factors. The part of the study is

able to evaluate the hypothesis which as related to the selected areas of learning (Golosov et

al. 2014).

Practical Motivation

The important form of the effect of the carbon emission is based on its impact on

general public.

There are many organisations which offers the footprint calculators for public and

corporate use for depiction of carbon footprints of products. This particular consideration is

seen to be important for both accountant’s public in general. As per the number of previous

articles which are seen to be published by “US Environmental Protection Agency” these are

addressed with several issues pertaining to paper, plastic (candy wrappers), glass, cans,

computers, carpet and tires (Liao, Luo and Tang 2015). In Australia the regulators and the

managers pertaining to this consideration has been able to contribute to the number of issues

related to the matters of lumber and other building materials. Several companies and non-

profit making academics have been able to address number of issues pertaining to mailing

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CARBON EMISSION AS PER AGENCY THEORY

letters and packages. In several types of the other cases the main form of the initiatives is

related to introducing CO2 label on the products. This particular initiative was takin in March

2007 by the UK manufacturers on foods, shirts and detergents. The evaluation of the

packages in the several types of the other incidences are seen to be addressed as per the

actively participating with the “Carbon Trust state” (Rodrik 2014).

The evaluation of the significant nature of the other packages are taken into account

with the number of the factors which are related to carbon footprint. These considerations has

highlighted number of the factors which are seen to be taken into account with using aseptic

carton and aluminium to prevent the impacts of carbon footprints in the environment (Hale

and Roger 2014).

Theoretical Motivation

In general, there are different types the of other theories which are seen to be related

to address the theories associated to carbon footprint. Some of the different types of the

specific theories for the carbon footprint are taken into account with investigating impact of

the carbon risk management and disclosure of the same with non-investor stakeholders. The

quality of the carbon climate change disclosers is seen to be related to the specific aspects of

implementing quality of the climate change disclosures. This particular factor is seen to be

related to the disaggregated carbon risk management and the different types of the disclosure

which are made from the scores of the other sources. There have been significantly less

associated factors for the carbon risk management and ex-ante cost of equity capital and

market value. It has been also discerned that carbon emissions do not provide any additional

information on the non-investor stakeholders over and above carbon risk management. As per

the findings of the previous study the carbon risk management of the research study refers to

performance of the firm with respect to the carbon emissions and climate change (Kalu,

Buang and Aliagha 2016).

letters and packages. In several types of the other cases the main form of the initiatives is

related to introducing CO2 label on the products. This particular initiative was takin in March

2007 by the UK manufacturers on foods, shirts and detergents. The evaluation of the

packages in the several types of the other incidences are seen to be addressed as per the

actively participating with the “Carbon Trust state” (Rodrik 2014).

The evaluation of the significant nature of the other packages are taken into account

with the number of the factors which are related to carbon footprint. These considerations has

highlighted number of the factors which are seen to be taken into account with using aseptic

carton and aluminium to prevent the impacts of carbon footprints in the environment (Hale

and Roger 2014).

Theoretical Motivation

In general, there are different types the of other theories which are seen to be related

to address the theories associated to carbon footprint. Some of the different types of the

specific theories for the carbon footprint are taken into account with investigating impact of

the carbon risk management and disclosure of the same with non-investor stakeholders. The

quality of the carbon climate change disclosers is seen to be related to the specific aspects of

implementing quality of the climate change disclosures. This particular factor is seen to be

related to the disaggregated carbon risk management and the different types of the disclosure

which are made from the scores of the other sources. There have been significantly less

associated factors for the carbon risk management and ex-ante cost of equity capital and

market value. It has been also discerned that carbon emissions do not provide any additional

information on the non-investor stakeholders over and above carbon risk management. As per

the findings of the previous study the carbon risk management of the research study refers to

performance of the firm with respect to the carbon emissions and climate change (Kalu,

Buang and Aliagha 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CARBON EMISSION AS PER AGENCY THEORY

It needs to be also discerned that the significant factors taken into account for the

carbon emissions are seen to be evident with the consideration of the number of factors

considered with the firm’s efficiency and effectiveness in managing these issues. Several

types of the other aspect of the study are associated to minimise the risks and focus more on

the opportunities. The important purpose of this study has been able to discuss on the firm’s

carbon risk management and climate change performance. Previous research investigations

have been able to discuss the potential issues associated to the climate change disclosures.

These factors are seen to be taken into consideration with the discussion of the “company

size, leverage, profitability, shareholder resolutions, regulatory threats, economic

consequences and institutional investor engagement” (Ben-Amar, Chang and McIlkenny

2017).

Literature Review

Carbon footprint is defined as the overall set of the greenhouse emissions which is

caused by an individual, product and event. The measure of the carbon footprint is able to

consider the total amount of the emission of “carbon dioxide (CO2) and methane (CH4)”.

The “Greenhouse gases (GHGs)” in general are taken into account with the production,

consumption of food, fuels, manufactured goods, materials, wood and land clearance

(Grosjean et al. 2016).

Agency theory is defined as the relationship between agents and principals in

business. This theory has been further seen to be concerned with the unalignment of the goals

or different aversion levels of the risk (Zhang, Zhou and Kung 2015).

The first study of the literature review has been able to discuss the relationship

between environmental performance and disclosures pertaining to the topical type of

environmental performance. The learning related to this has considered disaggregated scores

It needs to be also discerned that the significant factors taken into account for the

carbon emissions are seen to be evident with the consideration of the number of factors

considered with the firm’s efficiency and effectiveness in managing these issues. Several

types of the other aspect of the study are associated to minimise the risks and focus more on

the opportunities. The important purpose of this study has been able to discuss on the firm’s

carbon risk management and climate change performance. Previous research investigations

have been able to discuss the potential issues associated to the climate change disclosures.

These factors are seen to be taken into consideration with the discussion of the “company

size, leverage, profitability, shareholder resolutions, regulatory threats, economic

consequences and institutional investor engagement” (Ben-Amar, Chang and McIlkenny

2017).

Literature Review

Carbon footprint is defined as the overall set of the greenhouse emissions which is

caused by an individual, product and event. The measure of the carbon footprint is able to

consider the total amount of the emission of “carbon dioxide (CO2) and methane (CH4)”.

The “Greenhouse gases (GHGs)” in general are taken into account with the production,

consumption of food, fuels, manufactured goods, materials, wood and land clearance

(Grosjean et al. 2016).

Agency theory is defined as the relationship between agents and principals in

business. This theory has been further seen to be concerned with the unalignment of the goals

or different aversion levels of the risk (Zhang, Zhou and Kung 2015).

The first study of the literature review has been able to discuss the relationship

between environmental performance and disclosures pertaining to the topical type of

environmental performance. The learning related to this has considered disaggregated scores

5CARBON EMISSION AS PER AGENCY THEORY

analyses thereby revealing the role of particular carbon risk management practices. The

historical carbon risk management is seen with the measurement of the significant factors

which has enumerated the carbon emission’s intensity and the actual emission. The advantage

of this study has been able to depict the key performance indicators. The limitation for this

seen with less information available (Rehmatulla and Smith 2015).

Some of the other learnings have identified the connection between carbon risk

management and the quality of carbon disclosure. Carbon disclosure project states on the

areas to measure and manage the environmental impacts. The main advantage of this

literature has identified the most comprehensive collection of self-reported environmental

data in the world. The limitation for this is seen to be identified with the cost constraints for

the devices required for reporting on the quality of carbon disclosures (Geels 2014).

The measurement of the carbon footprint has been able to quantify the carbon content

with the relevant portfolio for allocating the carbon emissions of a company. The traditional

portfolio analysis allows the investors to assess the investors to state the reasons related to

address the low carbon footprint. This is mainly due to the underweighted carbon intensive

sectors (Amran, Periasamy and Zulkafli 2014).

Hypotheses

There will be two theoretical aspects explained for the non-financial and financial

disclosures phenomenon. These theories are will be classified with the socio-political theories

and economic-based disclosures. The considerations for the socio-political theories has been

able to assume the disclosure behaviour with the function of political pressure and social

stakeholders. The legitimacy theory is seen to operate within the standards and the norms

which is considered with the social contract.

analyses thereby revealing the role of particular carbon risk management practices. The

historical carbon risk management is seen with the measurement of the significant factors

which has enumerated the carbon emission’s intensity and the actual emission. The advantage

of this study has been able to depict the key performance indicators. The limitation for this

seen with less information available (Rehmatulla and Smith 2015).

Some of the other learnings have identified the connection between carbon risk

management and the quality of carbon disclosure. Carbon disclosure project states on the

areas to measure and manage the environmental impacts. The main advantage of this

literature has identified the most comprehensive collection of self-reported environmental

data in the world. The limitation for this is seen to be identified with the cost constraints for

the devices required for reporting on the quality of carbon disclosures (Geels 2014).

The measurement of the carbon footprint has been able to quantify the carbon content

with the relevant portfolio for allocating the carbon emissions of a company. The traditional

portfolio analysis allows the investors to assess the investors to state the reasons related to

address the low carbon footprint. This is mainly due to the underweighted carbon intensive

sectors (Amran, Periasamy and Zulkafli 2014).

Hypotheses

There will be two theoretical aspects explained for the non-financial and financial

disclosures phenomenon. These theories are will be classified with the socio-political theories

and economic-based disclosures. The considerations for the socio-political theories has been

able to assume the disclosure behaviour with the function of political pressure and social

stakeholders. The legitimacy theory is seen to operate within the standards and the norms

which is considered with the social contract.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CARBON EMISSION AS PER AGENCY THEORY

The investigation and the determinants from the corporate responses are addressed

with the CDP questionnaires and the type of information considered in the responses. The

hypothesis statement will be able to address disagreement with the quality of the disclosures.

The solicit political theories are based on the assumptions to improve the environmental

performance with higher quality of environmental disclosure.

The first hypothesis will be able to provide the relationship between carbon risk

management and the quality of carbon disclosure. The second hypothesis has ascertained the

association between CSR and accounting performance as per the agency theory.

The hypothesis formulated for the research study are listed below as follows:

Null Hypothesis (H01): There does not exist a positive relationship between carbon

risk management and the quality of carbon disclosure

Alternative Hypothesis (H1): There does exists a positive relationship between

carbon risk management and the quality of carbon disclosure

Null Hypothesis (H02): There does not exist a positive relationship for CSR and

accounting performance which is based on agency theory

Alternative Hypothesis (H2): There exists a positive relationship for CSR and

accounting performance which is based on agency theory

Conclusion

As per the practical motivation discussion there has been number of previous article

which are seen to be published by “US Environmental Protection Agency” which has

addressed several issues pertaining to the use of paper, plastic (candy wrappers), glass, cans,

computers, carpet and tires. Several companies and non-profit making academics have been

able to address issues pertaining to mailing letters and packages. The theoretical motivation

The investigation and the determinants from the corporate responses are addressed

with the CDP questionnaires and the type of information considered in the responses. The

hypothesis statement will be able to address disagreement with the quality of the disclosures.

The solicit political theories are based on the assumptions to improve the environmental

performance with higher quality of environmental disclosure.

The first hypothesis will be able to provide the relationship between carbon risk

management and the quality of carbon disclosure. The second hypothesis has ascertained the

association between CSR and accounting performance as per the agency theory.

The hypothesis formulated for the research study are listed below as follows:

Null Hypothesis (H01): There does not exist a positive relationship between carbon

risk management and the quality of carbon disclosure

Alternative Hypothesis (H1): There does exists a positive relationship between

carbon risk management and the quality of carbon disclosure

Null Hypothesis (H02): There does not exist a positive relationship for CSR and

accounting performance which is based on agency theory

Alternative Hypothesis (H2): There exists a positive relationship for CSR and

accounting performance which is based on agency theory

Conclusion

As per the practical motivation discussion there has been number of previous article

which are seen to be published by “US Environmental Protection Agency” which has

addressed several issues pertaining to the use of paper, plastic (candy wrappers), glass, cans,

computers, carpet and tires. Several companies and non-profit making academics have been

able to address issues pertaining to mailing letters and packages. The theoretical motivation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CARBON EMISSION AS PER AGENCY THEORY

has discerned specific theories for the carbon footprint which are taken into account with

investigating impact of the carbon risk management and disclosure of the same with the non-

investor stakeholders. The quality of the carbon climate change disclosers is seen to be

related to the specific aspects of implementing quality of the climate schange. disclosures.

The hypothesis of the study will be able to determine relationship between carbon risk

management and the quality of carbon disclosure and relationship for CSR and accounting

performance which is based on agency theory.

has discerned specific theories for the carbon footprint which are taken into account with

investigating impact of the carbon risk management and disclosure of the same with the non-

investor stakeholders. The quality of the carbon climate change disclosers is seen to be

related to the specific aspects of implementing quality of the climate schange. disclosures.

The hypothesis of the study will be able to determine relationship between carbon risk

management and the quality of carbon disclosure and relationship for CSR and accounting

performance which is based on agency theory.

8CARBON EMISSION AS PER AGENCY THEORY

Reference List

Amran, A., Periasamy, V. and Zulkafli, A.H., 2014. Determinants of climate change

disclosure by developed and emerging countries in Asia Pacific. Sustainable

Development, 22(3), pp.188-204.

Ben-Amar, W., Chang, M. and McIlkenny, P., 2017. Board gender diversity and corporate

response to sustainability initiatives: evidence from the Carbon Disclosure Project. Journal of

Business Ethics, 142(2), pp.369-383.

Geels, F.W., 2014. Regime resistance against low-carbon transitions: Introducing politics and

power into the multi-level perspective. Theory, Culture & Society, 31(5), pp.21-40.

Golosov, M., Hassler, J., Krusell, P. and Tsyvinski, A., 2014. Optimal taxes on fossil fuel in

general equilibrium. Econometrica, 82(1), pp.41-88.

Grosjean, G., Acworth, W., Flachsland, C. and Marschinski, R., 2016. After monetary policy,

climate policy: is delegation the key to EU ETS reform?. Climate Policy, 16(1), pp.1-25.

Hale, T. and Roger, C., 2014. Orchestration and transnational climate governance. The review

of international organizations, 9(1), pp.59-82.

Jolley, D. and Douglas, K.M., 2014. The social consequences of conspiracism: Exposure to

conspiracy theories decreases intentions to engage in politics and to reduce one's carbon

footprint. British Journal of Psychology, 105(1), pp.35-56.

Kalu, J.U., Buang, A. and Aliagha, G.U., 2016. Determinants of voluntary carbon disclosure

in the corporate real estate sector of Malaysia. Journal of environmental management, 182,

pp.519-524.

Liao, L., Luo, L. and Tang, Q., 2015. Gender diversity, board independence, environmental

committee and greenhouse gas disclosure. The British Accounting Review, 47(4), pp.409-424.

Reference List

Amran, A., Periasamy, V. and Zulkafli, A.H., 2014. Determinants of climate change

disclosure by developed and emerging countries in Asia Pacific. Sustainable

Development, 22(3), pp.188-204.

Ben-Amar, W., Chang, M. and McIlkenny, P., 2017. Board gender diversity and corporate

response to sustainability initiatives: evidence from the Carbon Disclosure Project. Journal of

Business Ethics, 142(2), pp.369-383.

Geels, F.W., 2014. Regime resistance against low-carbon transitions: Introducing politics and

power into the multi-level perspective. Theory, Culture & Society, 31(5), pp.21-40.

Golosov, M., Hassler, J., Krusell, P. and Tsyvinski, A., 2014. Optimal taxes on fossil fuel in

general equilibrium. Econometrica, 82(1), pp.41-88.

Grosjean, G., Acworth, W., Flachsland, C. and Marschinski, R., 2016. After monetary policy,

climate policy: is delegation the key to EU ETS reform?. Climate Policy, 16(1), pp.1-25.

Hale, T. and Roger, C., 2014. Orchestration and transnational climate governance. The review

of international organizations, 9(1), pp.59-82.

Jolley, D. and Douglas, K.M., 2014. The social consequences of conspiracism: Exposure to

conspiracy theories decreases intentions to engage in politics and to reduce one's carbon

footprint. British Journal of Psychology, 105(1), pp.35-56.

Kalu, J.U., Buang, A. and Aliagha, G.U., 2016. Determinants of voluntary carbon disclosure

in the corporate real estate sector of Malaysia. Journal of environmental management, 182,

pp.519-524.

Liao, L., Luo, L. and Tang, Q., 2015. Gender diversity, board independence, environmental

committee and greenhouse gas disclosure. The British Accounting Review, 47(4), pp.409-424.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CARBON EMISSION AS PER AGENCY THEORY

Rehmatulla, N. and Smith, T., 2015. Barriers to energy efficiency in shipping: A triangulated

approach to investigate the principal agent problem. Energy Policy, 84, pp.44-57.

Rodrik, D., 2014. Green industrial policy. Oxford Review of Economic Policy, 30(3), pp.469-

491.

Zhang, N., Zhou, P. and Kung, C.C., 2015. Total-factor carbon emission performance of the

Chinese transportation industry: A bootstrapped non-radial Malmquist index

analysis. Renewable and Sustainable Energy Reviews, 41, pp.584-593.

Rehmatulla, N. and Smith, T., 2015. Barriers to energy efficiency in shipping: A triangulated

approach to investigate the principal agent problem. Energy Policy, 84, pp.44-57.

Rodrik, D., 2014. Green industrial policy. Oxford Review of Economic Policy, 30(3), pp.469-

491.

Zhang, N., Zhou, P. and Kung, C.C., 2015. Total-factor carbon emission performance of the

Chinese transportation industry: A bootstrapped non-radial Malmquist index

analysis. Renewable and Sustainable Energy Reviews, 41, pp.584-593.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CARBON EMISSION AS PER AGENCY THEORY

Appendix

Author Dat

e

Title Journal Type of

Paper

(Theoreti

cal or

Empirica

l)

If

empirical

, research

method

and

sample

If

empirical,

dependen

t and

independe

nt

variables

100-word

summary

of

contributio

n to the

research

question

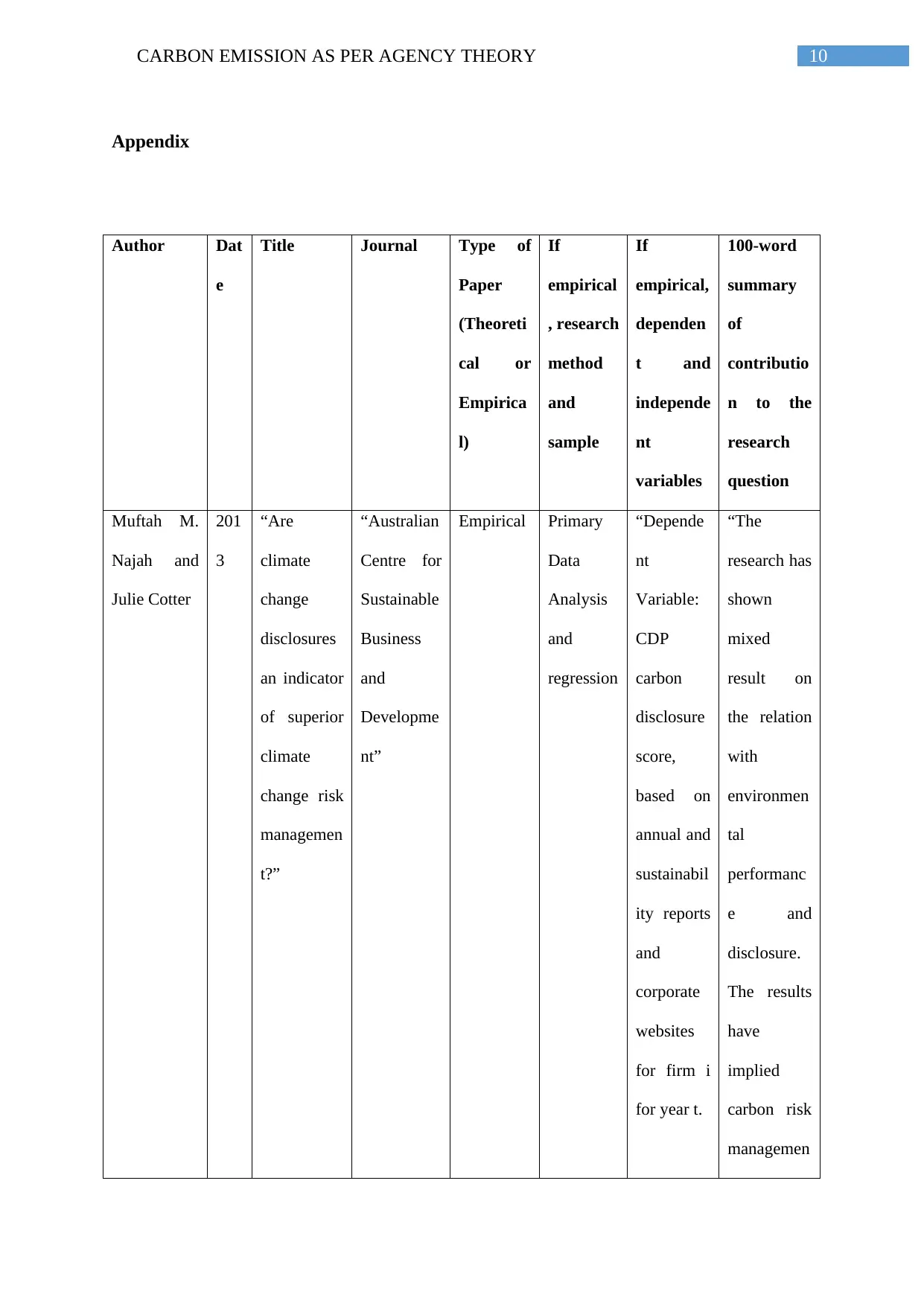

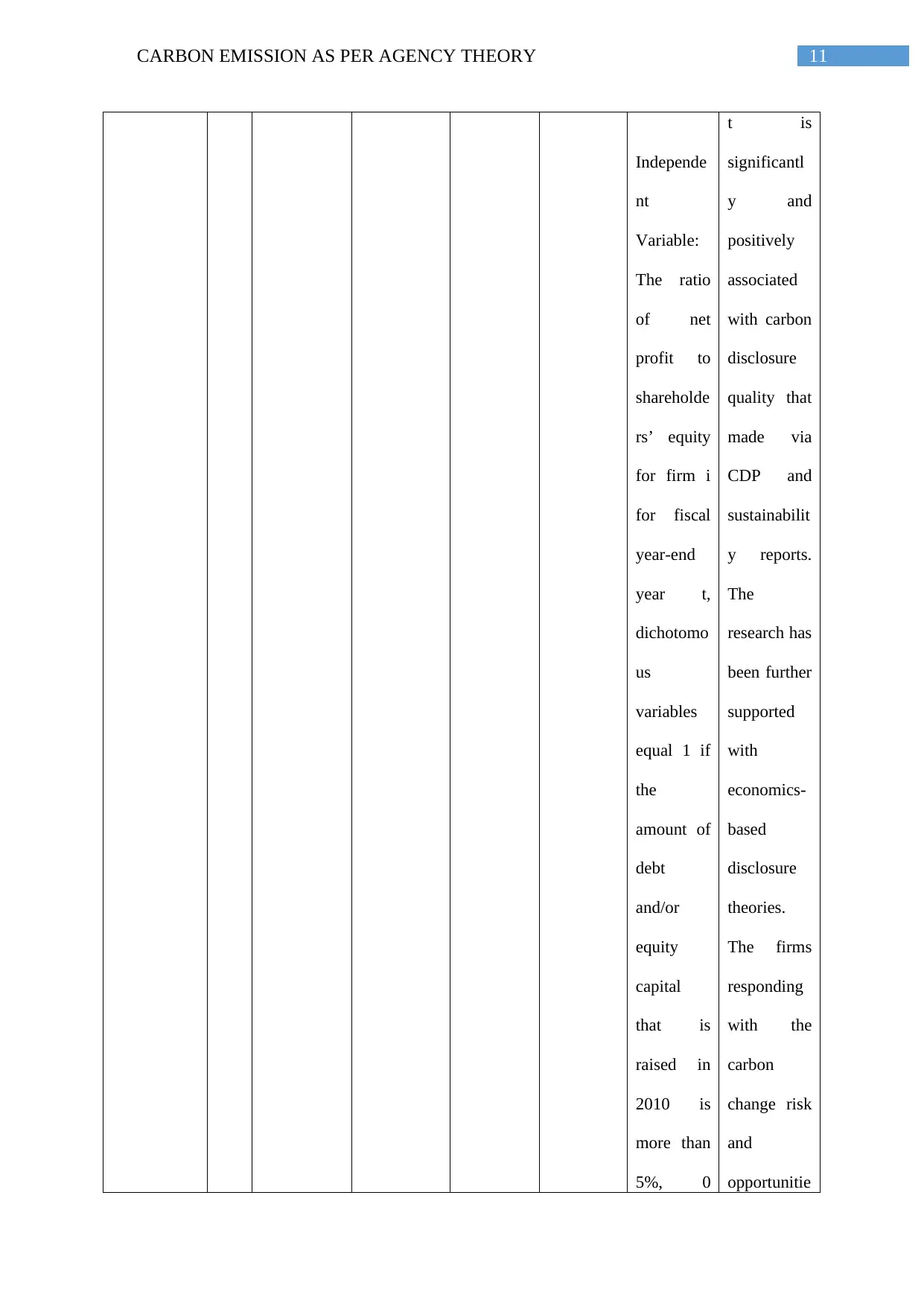

Muftah M.

Najah and

Julie Cotter

201

3

“Are

climate

change

disclosures

an indicator

of superior

climate

change risk

managemen

t?”

“Australian

Centre for

Sustainable

Business

and

Developme

nt”

Empirical Primary

Data

Analysis

and

regression

“Depende

nt

Variable:

CDP

carbon

disclosure

score,

based on

annual and

sustainabil

ity reports

and

corporate

websites

for firm i

for year t.

“The

research has

shown

mixed

result on

the relation

with

environmen

tal

performanc

e and

disclosure.

The results

have

implied

carbon risk

managemen

Appendix

Author Dat

e

Title Journal Type of

Paper

(Theoreti

cal or

Empirica

l)

If

empirical

, research

method

and

sample

If

empirical,

dependen

t and

independe

nt

variables

100-word

summary

of

contributio

n to the

research

question

Muftah M.

Najah and

Julie Cotter

201

3

“Are

climate

change

disclosures

an indicator

of superior

climate

change risk

managemen

t?”

“Australian

Centre for

Sustainable

Business

and

Developme

nt”

Empirical Primary

Data

Analysis

and

regression

“Depende

nt

Variable:

CDP

carbon

disclosure

score,

based on

annual and

sustainabil

ity reports

and

corporate

websites

for firm i

for year t.

“The

research has

shown

mixed

result on

the relation

with

environmen

tal

performanc

e and

disclosure.

The results

have

implied

carbon risk

managemen

11CARBON EMISSION AS PER AGENCY THEORY

Independe

nt

Variable:

The ratio

of net

profit to

shareholde

rs’ equity

for firm i

for fiscal

year-end

year t,

dichotomo

us

variables

equal 1 if

the

amount of

debt

and/or

equity

capital

that is

raised in

2010 is

more than

5%, 0

t is

significantl

y and

positively

associated

with carbon

disclosure

quality that

made via

CDP and

sustainabilit

y reports.

The

research has

been further

supported

with

economics-

based

disclosure

theories.

The firms

responding

with the

carbon

change risk

and

opportunitie

Independe

nt

Variable:

The ratio

of net

profit to

shareholde

rs’ equity

for firm i

for fiscal

year-end

year t,

dichotomo

us

variables

equal 1 if

the

amount of

debt

and/or

equity

capital

that is

raised in

2010 is

more than

5%, 0

t is

significantl

y and

positively

associated

with carbon

disclosure

quality that

made via

CDP and

sustainabilit

y reports.

The

research has

been further

supported

with

economics-

based

disclosure

theories.

The firms

responding

with the

carbon

change risk

and

opportunitie

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.