MGT723 Research: Climate Change, Carbon Emission & Company Size

VerifiedAdded on 2023/06/06

|15

|3336

|369

Report

AI Summary

This research report investigates the relationship between company size (measured by energy consumption) and carbon emissions, considering the influence of climate change policies. It uses data from the CDP survey, focusing on companies in Canada, the United States of America, and Brazil. The study examines variables such as climate change integration, percentage investment in energy, and carbon emission reduction, using descriptive statistical analysis to test the hypothesis that a relationship exists between company size and carbon emissions. The conceptual model highlights the interplay between these variables, with the aim of providing insights applicable to companies across various industries in the Americas, while acknowledging potential limitations due to regional specificities. The report also touches upon stakeholder theory, emphasizing the role of stakeholders in influencing corporate environmental responsibility.

MGT723 Research Project

Semester 2 2018

Assessment Task 2: Data Collection

Student Name: Sai paneendar reddy

Draft Research Question: “Is Carbon emission directly proportional to size of

the company (in terms of energy consumption)?”

Title: Significance of climate change amongst stakeholders of different

companies

Submission Date:

Acknowledgement:

I certify that I have carefully reviewed the university’s academic misconduct policy. I understand that

the source of ideas must be referenced and that quotation marks and a reference are required when

directly quoting anyone else’s words.

Note that you are permitted to change your research question and hypothesis as your research

project develops over the semester. If you make changes you should note, however, that you will

need to update your conceptual model, hypothesis, theoretical constructs and proxy measures

accordingly. Although these not assessed directly, your submission in Task 2 and Task 3 will be

evaluated in the context of your stated conceptual model etc.

Semester 2 2018

Assessment Task 2: Data Collection

Student Name: Sai paneendar reddy

Draft Research Question: “Is Carbon emission directly proportional to size of

the company (in terms of energy consumption)?”

Title: Significance of climate change amongst stakeholders of different

companies

Submission Date:

Acknowledgement:

I certify that I have carefully reviewed the university’s academic misconduct policy. I understand that

the source of ideas must be referenced and that quotation marks and a reference are required when

directly quoting anyone else’s words.

Note that you are permitted to change your research question and hypothesis as your research

project develops over the semester. If you make changes you should note, however, that you will

need to update your conceptual model, hypothesis, theoretical constructs and proxy measures

accordingly. Although these not assessed directly, your submission in Task 2 and Task 3 will be

evaluated in the context of your stated conceptual model etc.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

Various governments around the globe have passed legislation touching on the issue of

climate change. These legislations are expected to reflect on the reduction in the amount of

carbon emissions in the respective countries. The legislations are however dependent on

the implementation by the relevant governments’ agencies and most importantly

compliance from the stakeholders in the climate change agenda.

The size of the company, measured in terms of the energy consumption is a key indicator of

the company’s role in Climate Change. The higher the energy consumption the bigger the

company’s role in climate change.

This research paper investigates the roles that legislation and size of a company in terms of

energy consumption, have in climate change. This is done by citing the case of three

countries in the Americas; Canada, United States of America and Brazil.

2 | P a g e

Various governments around the globe have passed legislation touching on the issue of

climate change. These legislations are expected to reflect on the reduction in the amount of

carbon emissions in the respective countries. The legislations are however dependent on

the implementation by the relevant governments’ agencies and most importantly

compliance from the stakeholders in the climate change agenda.

The size of the company, measured in terms of the energy consumption is a key indicator of

the company’s role in Climate Change. The higher the energy consumption the bigger the

company’s role in climate change.

This research paper investigates the roles that legislation and size of a company in terms of

energy consumption, have in climate change. This is done by citing the case of three

countries in the Americas; Canada, United States of America and Brazil.

2 | P a g e

LITERATURE REVIEW - SUMMARY

Industrial contribution to activities that have fuelled this fast change in ecological conditions

leading to catastrophic implications for the future generations have been since then widely

discussed and addressed across all spheres. Industrial role in curbing climate change is

therefore pose to be one of the prime challenges today (Liesen et al. 2015).

Taking into cognizance the social awareness as well as the real threat to the future

implications, companies have been drawing up strategic policies that work to curb activities

which are identified as the sources of the problem and committing to report on their

activities as checks to such behaviour (Bebbington and Larrinaga 2014).

Greenhouse and carbon emission are one of the main information that many organizations

are expected and encouraged to disclose as per of the carbon disclosure project (CDP). This

is done with the motivation to reveal the strategies and commitment of the firms to reduce

their carbon output which is one of the main avenues by which industries have affected

climate (Hahn, Reimsbach and Schiemann 2015.).

Stakeholder theory deals with the ethical aspect of the managerial division of a business or

any other organization. It is a conceptual frame work for policy making that considers the

moral accountability of the organization and its management (R Edward freeman).

According to the normative theory of identifying stakeholders, any person or a group of

people or another organisation who may or may not be an internal member of the

organization with whom the organization’s interest ally is a stakeholder. They include

consu3mers, shareholders as well as competitors and partners. The first people who come

to mind when considering who holds the stakes at an organization are the shareholders.

However beside the obvious, stakeholders include all whose actions and contributions

influence company performance, like employees, customers and business associates other

than shareholders (Bridoux and Stoelhorst 2014). These people hold the position to

continuously challenge the organisation in how they manage and allocate their resources

thus influencing their operational policies (Herold, Lee and Gunarathne 2018).

The stakeholder salience theory speaks about how stakeholders influence the management

in their decision making process. They argue that stakeholders such as the consumers,

shareholders as well as competitors and partners who may build pressure on certain issues

could influence management to come up with the disclosure data as a testament to their

commitment (de Aguiar and Bebbington 2014).

This can be attributed to the fact that this issues touches all of society including the

stakeholders and the rising concern about climate change and the perceived accountability

of the organizations by the stakeholders places certain expectations from stakeholders onto

the company. The organization in response to these expectations would give first priority to

its stakeholders and align their operational strategy along the interest of the stakeholders

(Herold, Lee, and Gunarathne 2018).

3 | P a g e

Industrial contribution to activities that have fuelled this fast change in ecological conditions

leading to catastrophic implications for the future generations have been since then widely

discussed and addressed across all spheres. Industrial role in curbing climate change is

therefore pose to be one of the prime challenges today (Liesen et al. 2015).

Taking into cognizance the social awareness as well as the real threat to the future

implications, companies have been drawing up strategic policies that work to curb activities

which are identified as the sources of the problem and committing to report on their

activities as checks to such behaviour (Bebbington and Larrinaga 2014).

Greenhouse and carbon emission are one of the main information that many organizations

are expected and encouraged to disclose as per of the carbon disclosure project (CDP). This

is done with the motivation to reveal the strategies and commitment of the firms to reduce

their carbon output which is one of the main avenues by which industries have affected

climate (Hahn, Reimsbach and Schiemann 2015.).

Stakeholder theory deals with the ethical aspect of the managerial division of a business or

any other organization. It is a conceptual frame work for policy making that considers the

moral accountability of the organization and its management (R Edward freeman).

According to the normative theory of identifying stakeholders, any person or a group of

people or another organisation who may or may not be an internal member of the

organization with whom the organization’s interest ally is a stakeholder. They include

consu3mers, shareholders as well as competitors and partners. The first people who come

to mind when considering who holds the stakes at an organization are the shareholders.

However beside the obvious, stakeholders include all whose actions and contributions

influence company performance, like employees, customers and business associates other

than shareholders (Bridoux and Stoelhorst 2014). These people hold the position to

continuously challenge the organisation in how they manage and allocate their resources

thus influencing their operational policies (Herold, Lee and Gunarathne 2018).

The stakeholder salience theory speaks about how stakeholders influence the management

in their decision making process. They argue that stakeholders such as the consumers,

shareholders as well as competitors and partners who may build pressure on certain issues

could influence management to come up with the disclosure data as a testament to their

commitment (de Aguiar and Bebbington 2014).

This can be attributed to the fact that this issues touches all of society including the

stakeholders and the rising concern about climate change and the perceived accountability

of the organizations by the stakeholders places certain expectations from stakeholders onto

the company. The organization in response to these expectations would give first priority to

its stakeholders and align their operational strategy along the interest of the stakeholders

(Herold, Lee, and Gunarathne 2018).

3 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

However, none of those have been seen to be consistent. Again, existing research, notable

among which is Schreck and Raithel (2018) shows that firms commit to reporting on

emissions out of the belief that by doing so they would establish image as environmentally

conscious and therefore cater to the growing environmentally conscious consumers in the

market. Liesen (2015). This study in particular makes use of stakeholder theory and

statistical data analysis to explore the problem using empirical research.

The following section shows the conceptual model of the study. The control variable for this

case focuses on the market pressures from consumers that is experienced by the firms and

how they may interact with the size of the firm.

4 | P a g e

among which is Schreck and Raithel (2018) shows that firms commit to reporting on

emissions out of the belief that by doing so they would establish image as environmentally

conscious and therefore cater to the growing environmentally conscious consumers in the

market. Liesen (2015). This study in particular makes use of stakeholder theory and

statistical data analysis to explore the problem using empirical research.

The following section shows the conceptual model of the study. The control variable for this

case focuses on the market pressures from consumers that is experienced by the firms and

how they may interact with the size of the firm.

4 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

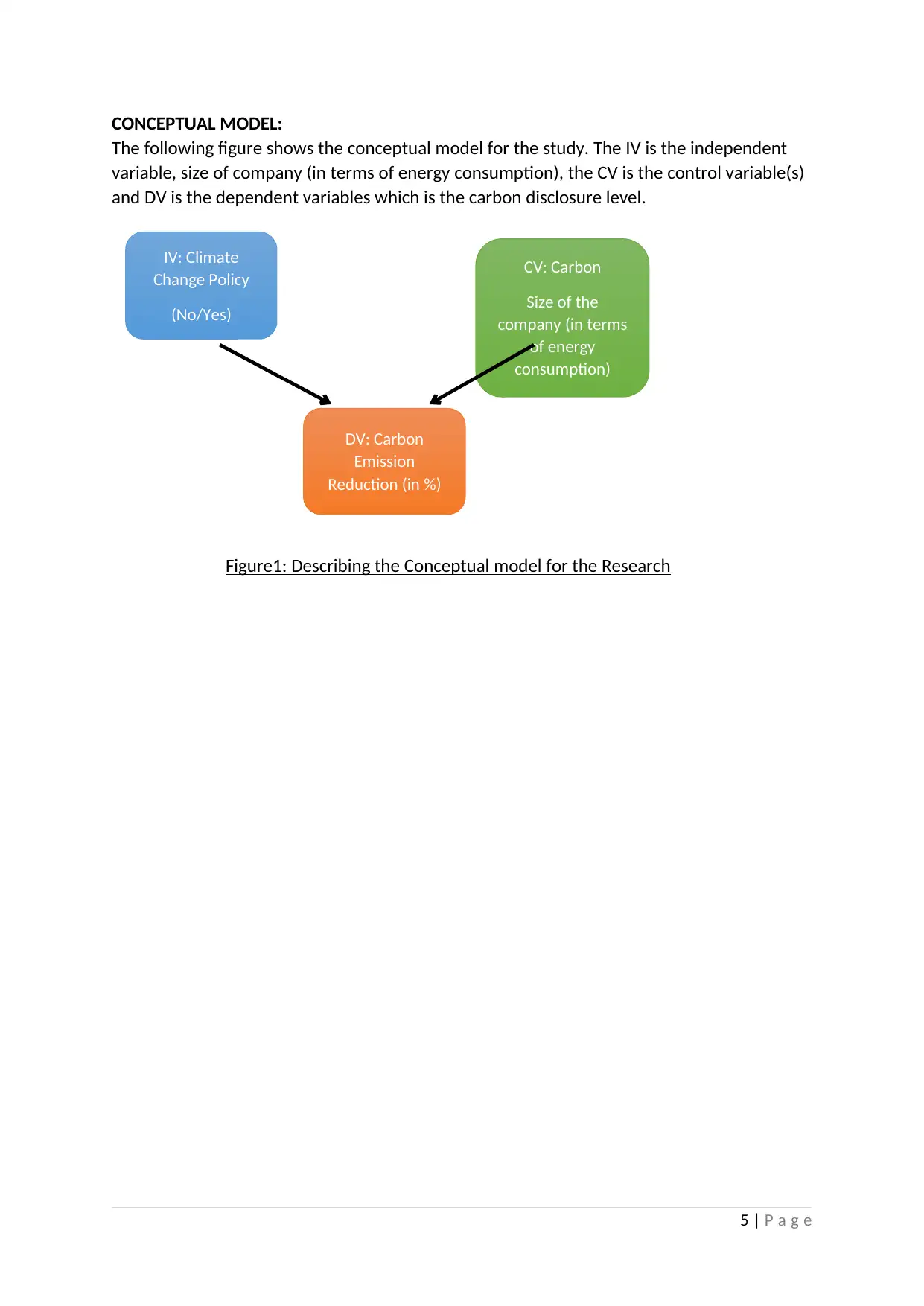

CONCEPTUAL MODEL:

The following figure shows the conceptual model for the study. The IV is the independent

variable, size of company (in terms of energy consumption), the CV is the control variable(s)

and DV is the dependent variables which is the carbon disclosure level.

Figure1: Describing the Conceptual model for the Research

5 | P a g e

IV: Climate

Change Policy

(No/Yes)

CV: Carbon

Size of the

company (in terms

of energy

consumption)

DV: Carbon

Emission

Reduction (in %)

The following figure shows the conceptual model for the study. The IV is the independent

variable, size of company (in terms of energy consumption), the CV is the control variable(s)

and DV is the dependent variables which is the carbon disclosure level.

Figure1: Describing the Conceptual model for the Research

5 | P a g e

IV: Climate

Change Policy

(No/Yes)

CV: Carbon

Size of the

company (in terms

of energy

consumption)

DV: Carbon

Emission

Reduction (in %)

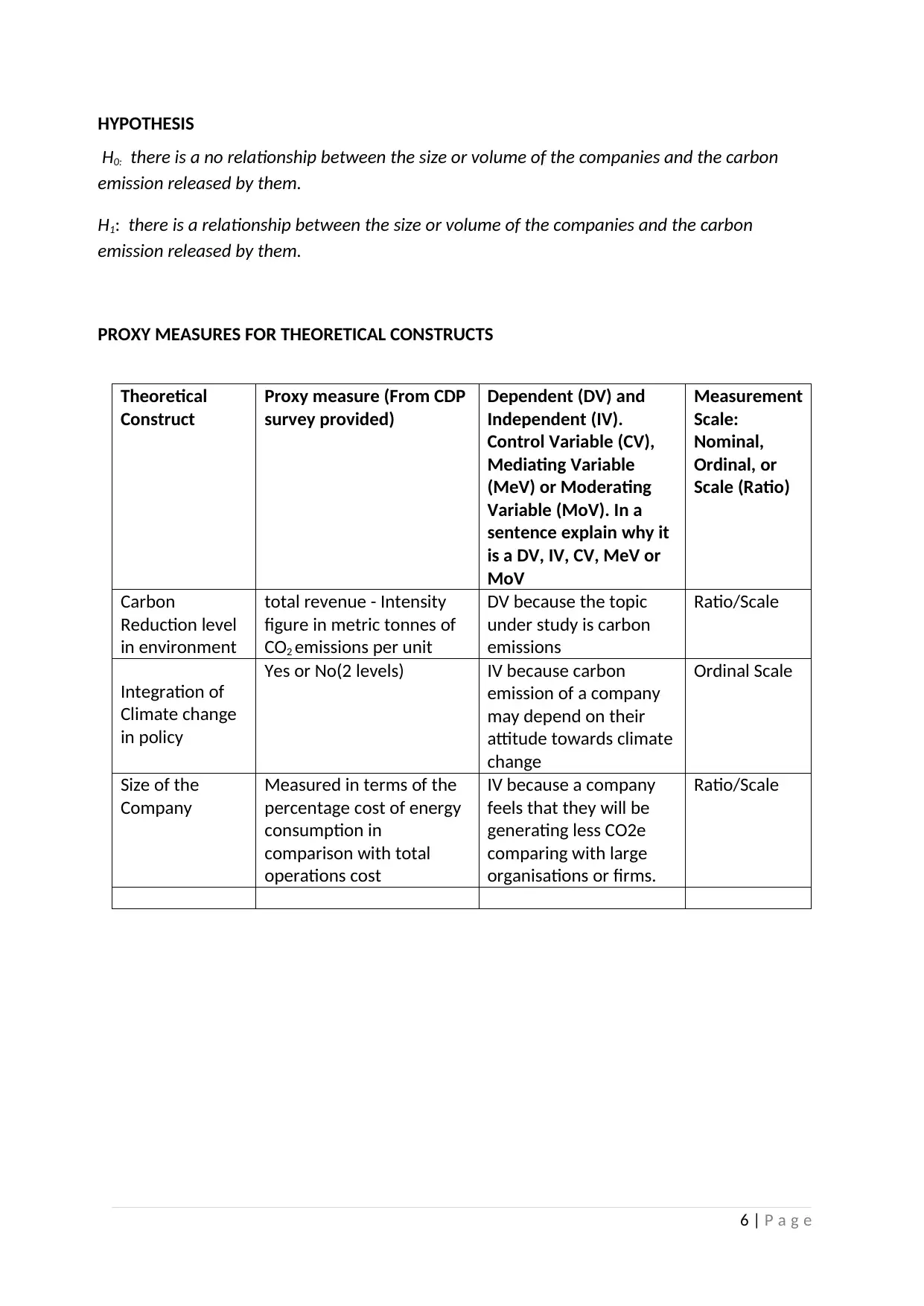

HYPOTHESIS

H0: there is a no relationship between the size or volume of the companies and the carbon

emission released by them.

H1: there is a relationship between the size or volume of the companies and the carbon

emission released by them.

PROXY MEASURES FOR THEORETICAL CONSTRUCTS

Theoretical

Construct

Proxy measure (From CDP

survey provided)

Dependent (DV) and

Independent (IV).

Control Variable (CV),

Mediating Variable

(MeV) or Moderating

Variable (MoV). In a

sentence explain why it

is a DV, IV, CV, MeV or

MoV

Measurement

Scale:

Nominal,

Ordinal, or

Scale (Ratio)

Carbon

Reduction level

in environment

total revenue - Intensity

figure in metric tonnes of

CO2 emissions per unit

DV because the topic

under study is carbon

emissions

Ratio/Scale

Integration of

Climate change

in policy

Yes or No(2 levels) IV because carbon

emission of a company

may depend on their

attitude towards climate

change

Ordinal Scale

Size of the

Company

Measured in terms of the

percentage cost of energy

consumption in

comparison with total

operations cost

IV because a company

feels that they will be

generating less CO2e

comparing with large

organisations or firms.

Ratio/Scale

6 | P a g e

H0: there is a no relationship between the size or volume of the companies and the carbon

emission released by them.

H1: there is a relationship between the size or volume of the companies and the carbon

emission released by them.

PROXY MEASURES FOR THEORETICAL CONSTRUCTS

Theoretical

Construct

Proxy measure (From CDP

survey provided)

Dependent (DV) and

Independent (IV).

Control Variable (CV),

Mediating Variable

(MeV) or Moderating

Variable (MoV). In a

sentence explain why it

is a DV, IV, CV, MeV or

MoV

Measurement

Scale:

Nominal,

Ordinal, or

Scale (Ratio)

Carbon

Reduction level

in environment

total revenue - Intensity

figure in metric tonnes of

CO2 emissions per unit

DV because the topic

under study is carbon

emissions

Ratio/Scale

Integration of

Climate change

in policy

Yes or No(2 levels) IV because carbon

emission of a company

may depend on their

attitude towards climate

change

Ordinal Scale

Size of the

Company

Measured in terms of the

percentage cost of energy

consumption in

comparison with total

operations cost

IV because a company

feels that they will be

generating less CO2e

comparing with large

organisations or firms.

Ratio/Scale

6 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

DATA ANALYSIS - DESCRIPTIVE

The sample data contains information on firms from all the industries that were available in

the original dataset of the CDP Survey. The decision to include all the available industries

was informed by the acknowledgement that every industry is a contributor to climate

change.

An industry might be at the final stage in the cycle of a product, such as at a shopping mall,

but the industry remains responsible for the other stages that the product has gone

through. These stages start from the raw material stage all through to the supply chain.

Therefore this research considers all the firms form all the available industries in the

analysis.

The sample data has six different variables; Account Name, Country, GRI, Climate Change

Integration, Percentage Investment in Energy and Carbon Emission Reduction.

The Account Name Variable represents the name of the firm or company whose data is

being collected for analysis. In this research, this variable will be a control variable (CV).

The Country Variable represent the country in which the firm or company is located. For the

purpose of this research paper, consideration has been given to the Americas. The data was

collected for countries that are located in the following countries in the Americas; Canada,

United States of America and Brazil. These four countries represent the four biggest

economies in the Americas. The countries are high industrialized, hence making climate

change an issue of interest in these countries. In this research, this variable will be a control

variable (CV).

The GRI variable represents the nature of industry in which the firm operates. The research

covers all the available industries from the CDP Survey dataset. This is aimed at get the net

effect on all industries. In this research, this variable will be a control variable (CV).

The Climate Change Integration variable represents the integration of the climate change

agenda and policies into the operations of the firm or company in question. This variable

represents information on whether this has been done or not. In this research, this variable

will be an Independent Variable (IV)

The Percentage Investment in Energy is variable that is representative of the size of the firm

or company. This variable measures the size of the company by its rate of energy

consumption. The higher the rate energy consumption of the company the larger the part

the company has to play in climate change. The variable represents the percentage of the

company’s total operational cost was spent on energy. In this research, this variable will be

an Independent Variable (IV).

The Carbon Emission Reduction variable represents the percentage reduction in carbon

emissions between for the year 2012. The research considers one year as the period of

study for the trend in carbon emissions for the firms and company’s in question. In this

research, this variable will be the Dependent Variable (DV).

The results from the analysis represented in this paper can generally be considered as

reliable and applicable for all the firms and companies in the Americas regardless of which

industry the fall. The conclusions are however limited to the Americas and can only be

applied to other regions in the world with extreme caution. The Americas may have political

7 | P a g e

The sample data contains information on firms from all the industries that were available in

the original dataset of the CDP Survey. The decision to include all the available industries

was informed by the acknowledgement that every industry is a contributor to climate

change.

An industry might be at the final stage in the cycle of a product, such as at a shopping mall,

but the industry remains responsible for the other stages that the product has gone

through. These stages start from the raw material stage all through to the supply chain.

Therefore this research considers all the firms form all the available industries in the

analysis.

The sample data has six different variables; Account Name, Country, GRI, Climate Change

Integration, Percentage Investment in Energy and Carbon Emission Reduction.

The Account Name Variable represents the name of the firm or company whose data is

being collected for analysis. In this research, this variable will be a control variable (CV).

The Country Variable represent the country in which the firm or company is located. For the

purpose of this research paper, consideration has been given to the Americas. The data was

collected for countries that are located in the following countries in the Americas; Canada,

United States of America and Brazil. These four countries represent the four biggest

economies in the Americas. The countries are high industrialized, hence making climate

change an issue of interest in these countries. In this research, this variable will be a control

variable (CV).

The GRI variable represents the nature of industry in which the firm operates. The research

covers all the available industries from the CDP Survey dataset. This is aimed at get the net

effect on all industries. In this research, this variable will be a control variable (CV).

The Climate Change Integration variable represents the integration of the climate change

agenda and policies into the operations of the firm or company in question. This variable

represents information on whether this has been done or not. In this research, this variable

will be an Independent Variable (IV)

The Percentage Investment in Energy is variable that is representative of the size of the firm

or company. This variable measures the size of the company by its rate of energy

consumption. The higher the rate energy consumption of the company the larger the part

the company has to play in climate change. The variable represents the percentage of the

company’s total operational cost was spent on energy. In this research, this variable will be

an Independent Variable (IV).

The Carbon Emission Reduction variable represents the percentage reduction in carbon

emissions between for the year 2012. The research considers one year as the period of

study for the trend in carbon emissions for the firms and company’s in question. In this

research, this variable will be the Dependent Variable (DV).

The results from the analysis represented in this paper can generally be considered as

reliable and applicable for all the firms and companies in the Americas regardless of which

industry the fall. The conclusions are however limited to the Americas and can only be

applied to other regions in the world with extreme caution. The Americas may have political

7 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

environment, social environment or economic environment that is specific for that region

and significantly different from other regions globally.

However, the choice of countries (that is: Canada, United States of America and Brazil) does

represent both Developed and Developing worlds. This can therefore allow the conclusions

from the analysis in this research paper to be applicable globally to some extent.

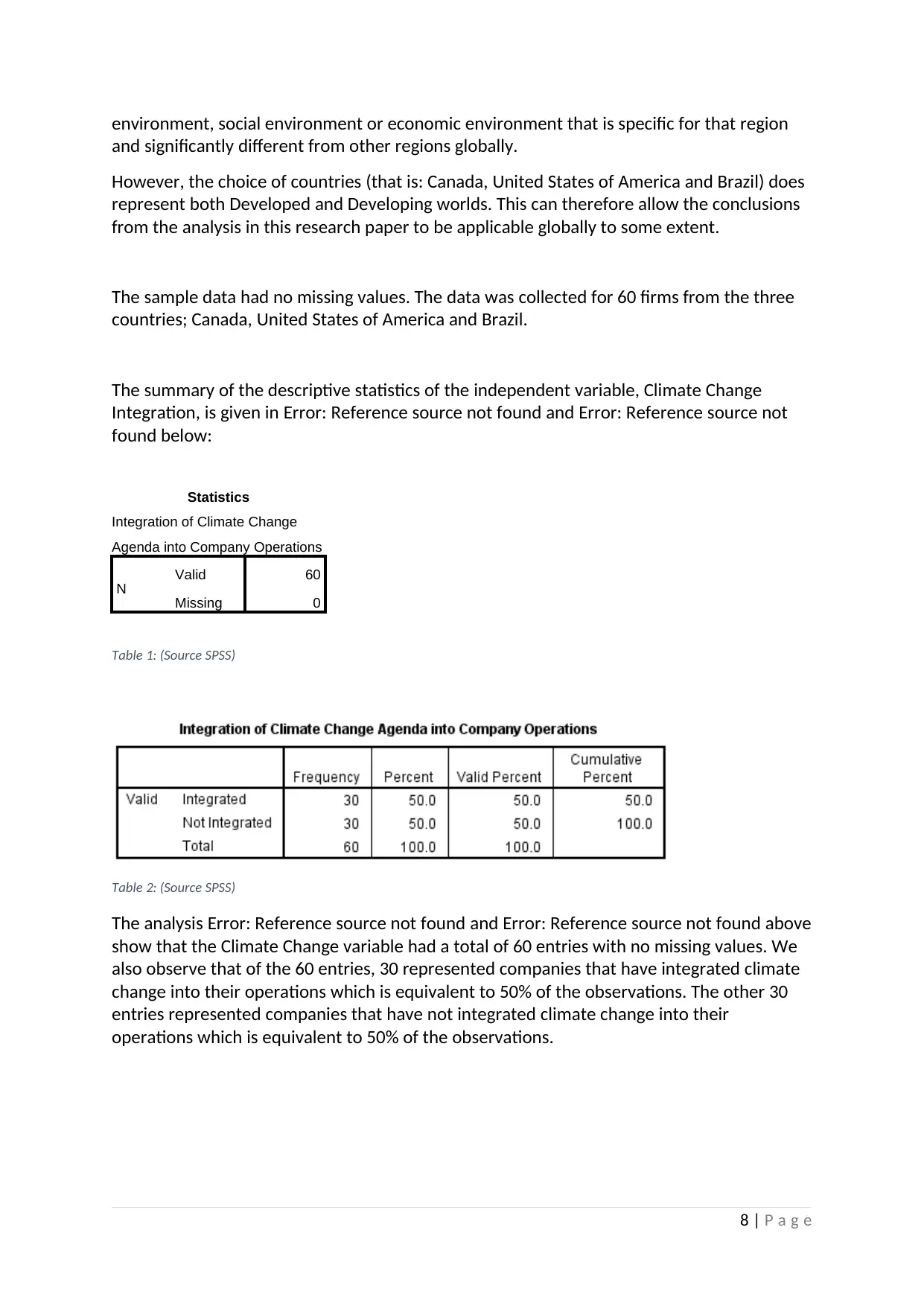

The sample data had no missing values. The data was collected for 60 firms from the three

countries; Canada, United States of America and Brazil.

The summary of the descriptive statistics of the independent variable, Climate Change

Integration, is given in Error: Reference source not found and Error: Reference source not

found below:

Statistics

Integration of Climate Change

Agenda into Company Operations

N Valid 60

Missing 0

Table 1: (Source SPSS)

Table 2: (Source SPSS)

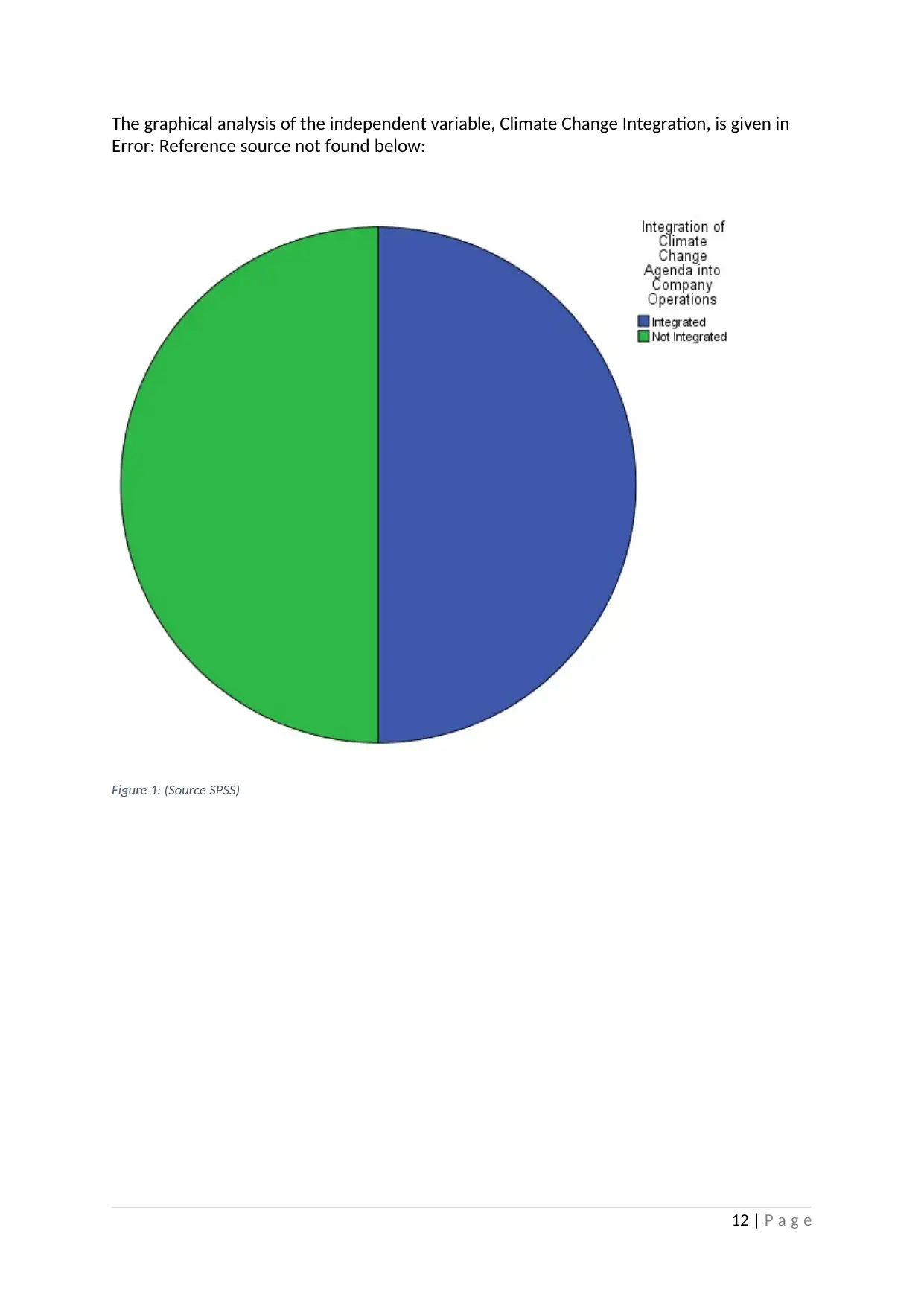

The analysis Error: Reference source not found and Error: Reference source not found above

show that the Climate Change variable had a total of 60 entries with no missing values. We

also observe that of the 60 entries, 30 represented companies that have integrated climate

change into their operations which is equivalent to 50% of the observations. The other 30

entries represented companies that have not integrated climate change into their

operations which is equivalent to 50% of the observations.

8 | P a g e

and significantly different from other regions globally.

However, the choice of countries (that is: Canada, United States of America and Brazil) does

represent both Developed and Developing worlds. This can therefore allow the conclusions

from the analysis in this research paper to be applicable globally to some extent.

The sample data had no missing values. The data was collected for 60 firms from the three

countries; Canada, United States of America and Brazil.

The summary of the descriptive statistics of the independent variable, Climate Change

Integration, is given in Error: Reference source not found and Error: Reference source not

found below:

Statistics

Integration of Climate Change

Agenda into Company Operations

N Valid 60

Missing 0

Table 1: (Source SPSS)

Table 2: (Source SPSS)

The analysis Error: Reference source not found and Error: Reference source not found above

show that the Climate Change variable had a total of 60 entries with no missing values. We

also observe that of the 60 entries, 30 represented companies that have integrated climate

change into their operations which is equivalent to 50% of the observations. The other 30

entries represented companies that have not integrated climate change into their

operations which is equivalent to 50% of the observations.

8 | P a g e

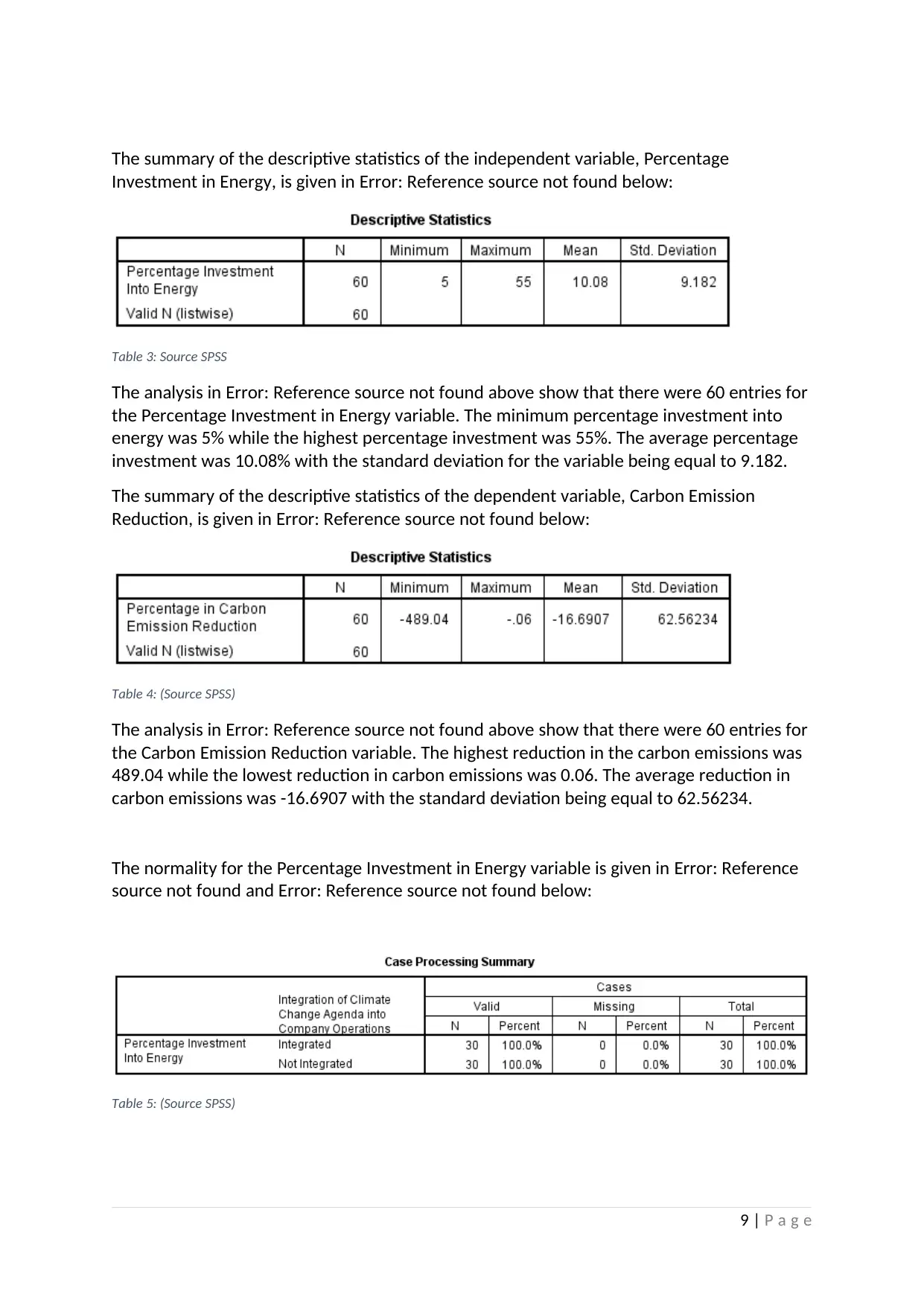

The summary of the descriptive statistics of the independent variable, Percentage

Investment in Energy, is given in Error: Reference source not found below:

Table 3: Source SPSS

The analysis in Error: Reference source not found above show that there were 60 entries for

the Percentage Investment in Energy variable. The minimum percentage investment into

energy was 5% while the highest percentage investment was 55%. The average percentage

investment was 10.08% with the standard deviation for the variable being equal to 9.182.

The summary of the descriptive statistics of the dependent variable, Carbon Emission

Reduction, is given in Error: Reference source not found below:

Table 4: (Source SPSS)

The analysis in Error: Reference source not found above show that there were 60 entries for

the Carbon Emission Reduction variable. The highest reduction in the carbon emissions was

489.04 while the lowest reduction in carbon emissions was 0.06. The average reduction in

carbon emissions was -16.6907 with the standard deviation being equal to 62.56234.

The normality for the Percentage Investment in Energy variable is given in Error: Reference

source not found and Error: Reference source not found below:

Table 5: (Source SPSS)

9 | P a g e

Investment in Energy, is given in Error: Reference source not found below:

Table 3: Source SPSS

The analysis in Error: Reference source not found above show that there were 60 entries for

the Percentage Investment in Energy variable. The minimum percentage investment into

energy was 5% while the highest percentage investment was 55%. The average percentage

investment was 10.08% with the standard deviation for the variable being equal to 9.182.

The summary of the descriptive statistics of the dependent variable, Carbon Emission

Reduction, is given in Error: Reference source not found below:

Table 4: (Source SPSS)

The analysis in Error: Reference source not found above show that there were 60 entries for

the Carbon Emission Reduction variable. The highest reduction in the carbon emissions was

489.04 while the lowest reduction in carbon emissions was 0.06. The average reduction in

carbon emissions was -16.6907 with the standard deviation being equal to 62.56234.

The normality for the Percentage Investment in Energy variable is given in Error: Reference

source not found and Error: Reference source not found below:

Table 5: (Source SPSS)

9 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

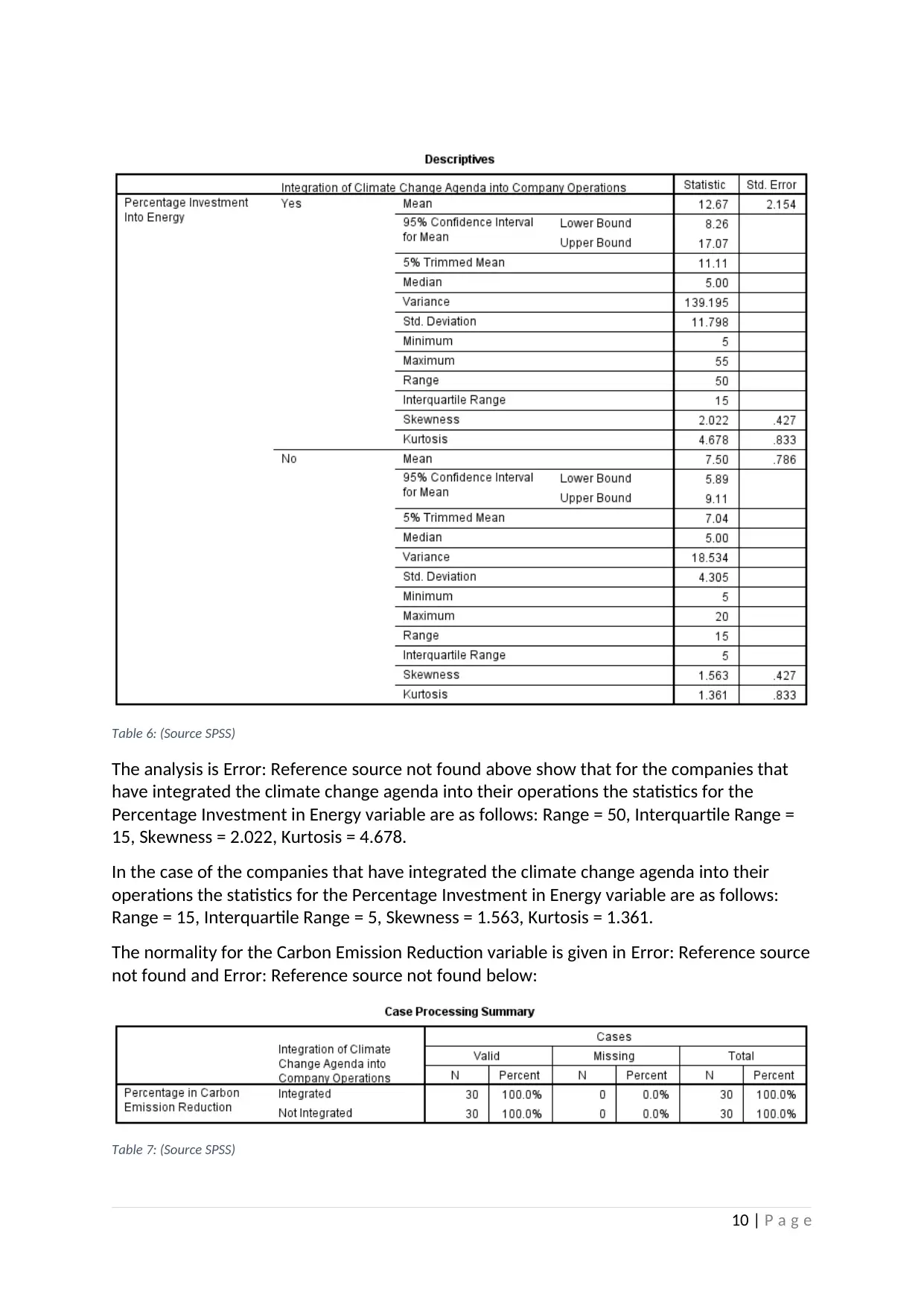

Table 6: (Source SPSS)

The analysis is Error: Reference source not found above show that for the companies that

have integrated the climate change agenda into their operations the statistics for the

Percentage Investment in Energy variable are as follows: Range = 50, Interquartile Range =

15, Skewness = 2.022, Kurtosis = 4.678.

In the case of the companies that have integrated the climate change agenda into their

operations the statistics for the Percentage Investment in Energy variable are as follows:

Range = 15, Interquartile Range = 5, Skewness = 1.563, Kurtosis = 1.361.

The normality for the Carbon Emission Reduction variable is given in Error: Reference source

not found and Error: Reference source not found below:

Table 7: (Source SPSS)

10 | P a g e

The analysis is Error: Reference source not found above show that for the companies that

have integrated the climate change agenda into their operations the statistics for the

Percentage Investment in Energy variable are as follows: Range = 50, Interquartile Range =

15, Skewness = 2.022, Kurtosis = 4.678.

In the case of the companies that have integrated the climate change agenda into their

operations the statistics for the Percentage Investment in Energy variable are as follows:

Range = 15, Interquartile Range = 5, Skewness = 1.563, Kurtosis = 1.361.

The normality for the Carbon Emission Reduction variable is given in Error: Reference source

not found and Error: Reference source not found below:

Table 7: (Source SPSS)

10 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

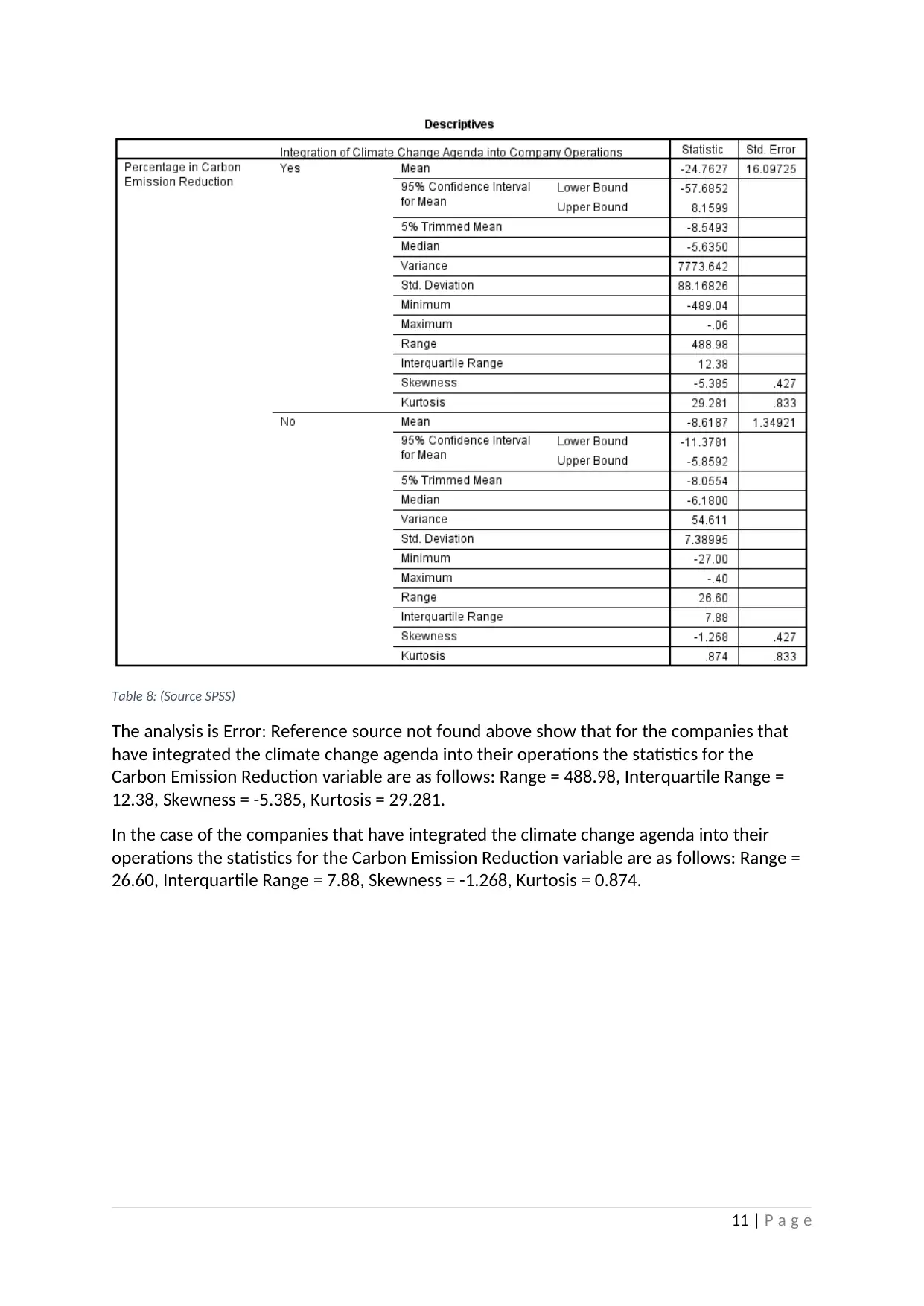

Table 8: (Source SPSS)

The analysis is Error: Reference source not found above show that for the companies that

have integrated the climate change agenda into their operations the statistics for the

Carbon Emission Reduction variable are as follows: Range = 488.98, Interquartile Range =

12.38, Skewness = -5.385, Kurtosis = 29.281.

In the case of the companies that have integrated the climate change agenda into their

operations the statistics for the Carbon Emission Reduction variable are as follows: Range =

26.60, Interquartile Range = 7.88, Skewness = -1.268, Kurtosis = 0.874.

11 | P a g e

The analysis is Error: Reference source not found above show that for the companies that

have integrated the climate change agenda into their operations the statistics for the

Carbon Emission Reduction variable are as follows: Range = 488.98, Interquartile Range =

12.38, Skewness = -5.385, Kurtosis = 29.281.

In the case of the companies that have integrated the climate change agenda into their

operations the statistics for the Carbon Emission Reduction variable are as follows: Range =

26.60, Interquartile Range = 7.88, Skewness = -1.268, Kurtosis = 0.874.

11 | P a g e

The graphical analysis of the independent variable, Climate Change Integration, is given in

Error: Reference source not found below:

Figure 1: (Source SPSS)

12 | P a g e

Error: Reference source not found below:

Figure 1: (Source SPSS)

12 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.