MGT 723 Research Project: Incentives and Carbon Emission Report, 2018

VerifiedAdded on 2023/06/04

|18

|4256

|313

Report

AI Summary

This research report investigates the impact of incentives on corporate carbon emissions, focusing on companies in the USA and Australia. It uses data from the Carbon Disclosure Project (CDP) to analyze the relationship between incentives provided to management for climate change initiatives and the resulting changes in Scope 1 and Scope 2 carbon emissions. The report includes a literature review, theoretical framework, conceptual model, and hypothesis testing using statistical analysis. The findings discuss the implications for both practice and theory, while also acknowledging the limitations of the study and suggesting avenues for further research. The analysis utilizes SPSS software to generate descriptive and inferential statistics, ultimately aiming to determine if a significant relationship exists between carbon emission rates and the incentives offered by companies.

University of Sunshine Coast

At

Australian Technical and Management College

(ATMC)

MGT 723 Research Project

Assessment Task 3: Report

Semester 2, 2018

At

Australian Technical and Management College

(ATMC)

MGT 723 Research Project

Assessment Task 3: Report

Semester 2, 2018

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MGT 723 Research Project

Assignment 3

Acknowledgement:

I certify that I have carefully reviewed the university’s academic misconduct policy. I understand that

the source of ideas must be referenced and that quotation marks and a reference are required when

directly quoting anyone else’s words.

Ashish Tiwari 1113814 2 | P a g e

Assignment 3

Acknowledgement:

I certify that I have carefully reviewed the university’s academic misconduct policy. I understand that

the source of ideas must be referenced and that quotation marks and a reference are required when

directly quoting anyone else’s words.

Ashish Tiwari 1113814 2 | P a g e

MGT 723 Research Project

Assignment 3

Table of Contents

Acknowledgement:................................................................................................................................2

Introduction...........................................................................................................................................4

Literature Review..................................................................................................................................5

Theoretical Framework.........................................................................................................................6

Conceptual Model.................................................................................................................................6

Hypotheses............................................................................................................................................8

Data Analysis – Descriptive....................................................................................................................9

Data Analysis – Inferential...................................................................................................................11

Hypothesis testing...............................................................................................................................12

Discussion............................................................................................................................................13

Limitations...........................................................................................................................................14

Further Research.................................................................................................................................14

References...........................................................................................................................................15

Ashish Tiwari 1113814 3 | P a g e

Assignment 3

Table of Contents

Acknowledgement:................................................................................................................................2

Introduction...........................................................................................................................................4

Literature Review..................................................................................................................................5

Theoretical Framework.........................................................................................................................6

Conceptual Model.................................................................................................................................6

Hypotheses............................................................................................................................................8

Data Analysis – Descriptive....................................................................................................................9

Data Analysis – Inferential...................................................................................................................11

Hypothesis testing...............................................................................................................................12

Discussion............................................................................................................................................13

Limitations...........................................................................................................................................14

Further Research.................................................................................................................................14

References...........................................................................................................................................15

Ashish Tiwari 1113814 3 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MGT 723 Research Project

Assignment 3

Introduction

Corporate responses and the climate changes because of carbon emissions have shifted over for the

last 20 years. In 1990’s, business neglected the concern but recently, greenhouse gases are the main

apprehension towards the environmental degradation. This has not only affected the environment

on a whole but has even affected the climate change issues but with many misconceptions, the

entire issue has fallen back to global warming (Besio and Pronzini 2014). Whether it is burning fossil

fuels or industrial chemicals, the gases trapped creates a radiation and hangs on the overall

temperature. Although, the largest producer of carbon emission is electricity source which is aligned

to 32% of greenhouse emission posing a substantial threat; followed by transportation i.e. 28% of

GHG (Huaman and Jun 2014).

The United States data shows that the total emission has been growing since the 20th century by an

increase of 5%, even though there is a drop but it still rising as a whole for other countries. Carbon

emissions have been the primary root for industrial development (Andrew and Cortese 2011).

Hence, it is important that the nature of carbon emission needs to be examined on a corporate level

as 17% constitute for the GHG threat.

Towards the carbon constrained future, strategies have been developed by corporates for

measuring, assessing, managing and reporting carbon emissions. The threat of climate change has

emerged as a basic response from carbon emissions that has not only intensified the management

and accounting capabilities of GHG but has also, established budgets, baselines and incentivization

for the measurement of actual emissions (Lau and Eng 2014).

The research report studies the carbon emission from the GHG with the use of incentives for urging

the firms to further reveal the extensive information for climate changes. The CDP (Carbon

Disclosure Project) report instil the investors of the present scenario with carbon emission and the

way it would be benefitting the overall financial preformation of the corporates (Caritte, Acha and

Ashish Tiwari 1113814 4 | P a g e

Assignment 3

Introduction

Corporate responses and the climate changes because of carbon emissions have shifted over for the

last 20 years. In 1990’s, business neglected the concern but recently, greenhouse gases are the main

apprehension towards the environmental degradation. This has not only affected the environment

on a whole but has even affected the climate change issues but with many misconceptions, the

entire issue has fallen back to global warming (Besio and Pronzini 2014). Whether it is burning fossil

fuels or industrial chemicals, the gases trapped creates a radiation and hangs on the overall

temperature. Although, the largest producer of carbon emission is electricity source which is aligned

to 32% of greenhouse emission posing a substantial threat; followed by transportation i.e. 28% of

GHG (Huaman and Jun 2014).

The United States data shows that the total emission has been growing since the 20th century by an

increase of 5%, even though there is a drop but it still rising as a whole for other countries. Carbon

emissions have been the primary root for industrial development (Andrew and Cortese 2011).

Hence, it is important that the nature of carbon emission needs to be examined on a corporate level

as 17% constitute for the GHG threat.

Towards the carbon constrained future, strategies have been developed by corporates for

measuring, assessing, managing and reporting carbon emissions. The threat of climate change has

emerged as a basic response from carbon emissions that has not only intensified the management

and accounting capabilities of GHG but has also, established budgets, baselines and incentivization

for the measurement of actual emissions (Lau and Eng 2014).

The research report studies the carbon emission from the GHG with the use of incentives for urging

the firms to further reveal the extensive information for climate changes. The CDP (Carbon

Disclosure Project) report instil the investors of the present scenario with carbon emission and the

way it would be benefitting the overall financial preformation of the corporates (Caritte, Acha and

Ashish Tiwari 1113814 4 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MGT 723 Research Project

Assignment 3

Shah 2015).The report would be analysed on the handful of corporates with a small sample size and

incentives for carbon accounting to the risks and opportunities faced by the firms.

Literature Review

Carbon emissions focuses on the rate of carbon dioxide emission. As per Elum and Momodu (2017),

oil and gas corporations, automobiles and industrialization in United States and Australia pose a

potential threat to climate change. USA, Australia and Europe later to Kyoto Protocol started

identifying the GHG emissions issues and the responses in market for climate change but the

corporate actions in these areas remained to be ineffective. Later climate change programs –CDP

and GHG Protocol turned out to be elementary reporting for corporate GHG emissions (Hahn,

Reimsbach and Schiemann 2015). For measurement of emissions, the companies were required to

share their GHG performance, so that the corporates could be in a better position to reduce it (Doda

et al. 2016). In this way, the stakeholders of the company could meet the achievements of the

companies reward them and further increase the pressure on the firms to meet the expectations

(Liesen et al. 2015).

The ultimate goal of the investigation was not to extend the pressure on corporates but even to

analyse the GHG emission disclosure for the corporates through stakeholders who are affected but

the firm’s objectives (Hickman 2017). Stakeholders who deal externally have the means to deviate

from the corporate agendas or corporate social responsibility issues (Guenther et al. 2016).

However, for corporates the response needs to be addressed to stakeholders group with the use of

disclosure. Incentive was used as a disclosure tool to minimize the exposure of political and social

environment of the firms (Chauvey et al. 2015).

The corporates have taken the effect of carbon emission not only to climate but also to human

character. For example, Amgen, being a biotechnology company manufactures and advances to

innovative therapeutics”, although, it realizes it new technology usage but also need to follow the

rules and regulations of the country. On the other hand, Rockwell Collins, US company of Aerospace

Ashish Tiwari 1113814 5 | P a g e

Assignment 3

Shah 2015).The report would be analysed on the handful of corporates with a small sample size and

incentives for carbon accounting to the risks and opportunities faced by the firms.

Literature Review

Carbon emissions focuses on the rate of carbon dioxide emission. As per Elum and Momodu (2017),

oil and gas corporations, automobiles and industrialization in United States and Australia pose a

potential threat to climate change. USA, Australia and Europe later to Kyoto Protocol started

identifying the GHG emissions issues and the responses in market for climate change but the

corporate actions in these areas remained to be ineffective. Later climate change programs –CDP

and GHG Protocol turned out to be elementary reporting for corporate GHG emissions (Hahn,

Reimsbach and Schiemann 2015). For measurement of emissions, the companies were required to

share their GHG performance, so that the corporates could be in a better position to reduce it (Doda

et al. 2016). In this way, the stakeholders of the company could meet the achievements of the

companies reward them and further increase the pressure on the firms to meet the expectations

(Liesen et al. 2015).

The ultimate goal of the investigation was not to extend the pressure on corporates but even to

analyse the GHG emission disclosure for the corporates through stakeholders who are affected but

the firm’s objectives (Hickman 2017). Stakeholders who deal externally have the means to deviate

from the corporate agendas or corporate social responsibility issues (Guenther et al. 2016).

However, for corporates the response needs to be addressed to stakeholders group with the use of

disclosure. Incentive was used as a disclosure tool to minimize the exposure of political and social

environment of the firms (Chauvey et al. 2015).

The corporates have taken the effect of carbon emission not only to climate but also to human

character. For example, Amgen, being a biotechnology company manufactures and advances to

innovative therapeutics”, although, it realizes it new technology usage but also need to follow the

rules and regulations of the country. On the other hand, Rockwell Collins, US company of Aerospace

Ashish Tiwari 1113814 5 | P a g e

MGT 723 Research Project

Assignment 3

and defence has been reducing its carbon footprint to an all time low of 26% GHG with continuous

support from Chicago Climate Exchange and data analysis using Lean/ Six Sigma (rockwellcollins.com

2018).

USA and Australia have been actively dealing with the carbon emission problem and aims to reduce

the carbon footprint further in the upcoming years. As the companies in these countries constitutes

to be the mainstay of the people for employment but with the existing approaches, a common

agreement needs to be devised for corresponding assessments. Here, primarily it is to test the

theory of carbon emission with incentives undertaken by the company to the management.

Theoretical Framework

USA and Australia have used the CDP questionnaire with Scope 1 (target) and Scope 2 (reporting)

emissions to analyse the companies emission record on a yearly basis. This reduction initiative has

upstaged the new rules and regulations reducing carbon dioxide emissions. This data will be

examined to revise the rules based on the reduction action performed in metric tonnes CO2e per

unit currency. This environmental strategy will help the regulators to not only set binding limits but

will also help the companies in buying permits to emit when exceeding those set “caps” (Song and

Leng 2012). This research design keeps a tap on the comparison based on the companies carbon

emission reduction rate from different companies of Australia and USA from the industries of

aerospace, mining, electrical, biotechnology, banks and so on.

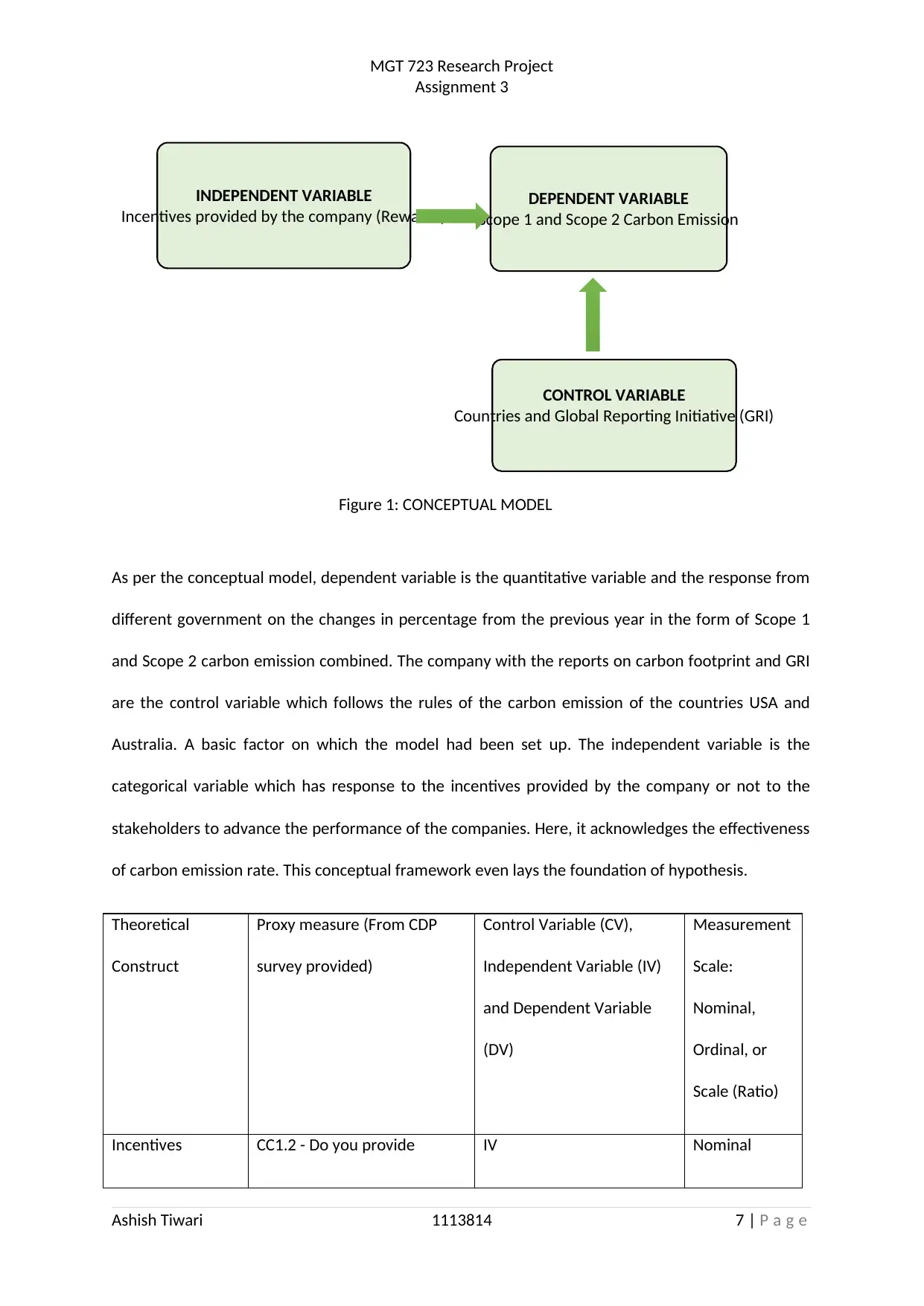

Conceptual Model

The model used for the study highlights the concepts and the variables that are used to identify the

relationship between them and the way it can be underlined with the research presented. Here, the

model specifies the relationship of independent and dependent variable with the effect of control

variable such that the control variable does not change and keeping it constant its effect can be seen

in explanatory and response variables. The model for the report can be given as:

Ashish Tiwari 1113814 6 | P a g e

Assignment 3

and defence has been reducing its carbon footprint to an all time low of 26% GHG with continuous

support from Chicago Climate Exchange and data analysis using Lean/ Six Sigma (rockwellcollins.com

2018).

USA and Australia have been actively dealing with the carbon emission problem and aims to reduce

the carbon footprint further in the upcoming years. As the companies in these countries constitutes

to be the mainstay of the people for employment but with the existing approaches, a common

agreement needs to be devised for corresponding assessments. Here, primarily it is to test the

theory of carbon emission with incentives undertaken by the company to the management.

Theoretical Framework

USA and Australia have used the CDP questionnaire with Scope 1 (target) and Scope 2 (reporting)

emissions to analyse the companies emission record on a yearly basis. This reduction initiative has

upstaged the new rules and regulations reducing carbon dioxide emissions. This data will be

examined to revise the rules based on the reduction action performed in metric tonnes CO2e per

unit currency. This environmental strategy will help the regulators to not only set binding limits but

will also help the companies in buying permits to emit when exceeding those set “caps” (Song and

Leng 2012). This research design keeps a tap on the comparison based on the companies carbon

emission reduction rate from different companies of Australia and USA from the industries of

aerospace, mining, electrical, biotechnology, banks and so on.

Conceptual Model

The model used for the study highlights the concepts and the variables that are used to identify the

relationship between them and the way it can be underlined with the research presented. Here, the

model specifies the relationship of independent and dependent variable with the effect of control

variable such that the control variable does not change and keeping it constant its effect can be seen

in explanatory and response variables. The model for the report can be given as:

Ashish Tiwari 1113814 6 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INDEPENDENT VARIABLE

Incentives provided by the company (Rewards)

DEPENDENT VARIABLE

Scope 1 and Scope 2 Carbon Emission

CONTROL VARIABLE

Countries and Global Reporting Initiative (GRI)

Figure 1: CONCEPTUAL MODEL

MGT 723 Research Project

Assignment 3

As per the conceptual model, dependent variable is the quantitative variable and the response from

different government on the changes in percentage from the previous year in the form of Scope 1

and Scope 2 carbon emission combined. The company with the reports on carbon footprint and GRI

are the control variable which follows the rules of the carbon emission of the countries USA and

Australia. A basic factor on which the model had been set up. The independent variable is the

categorical variable which has response to the incentives provided by the company or not to the

stakeholders to advance the performance of the companies. Here, it acknowledges the effectiveness

of carbon emission rate. This conceptual framework even lays the foundation of hypothesis.

Theoretical

Construct

Proxy measure (From CDP

survey provided)

Control Variable (CV),

Independent Variable (IV)

and Dependent Variable

(DV)

Measurement

Scale:

Nominal,

Ordinal, or

Scale (Ratio)

Incentives CC1.2 - Do you provide IV Nominal

Ashish Tiwari 1113814 7 | P a g e

Incentives provided by the company (Rewards)

DEPENDENT VARIABLE

Scope 1 and Scope 2 Carbon Emission

CONTROL VARIABLE

Countries and Global Reporting Initiative (GRI)

Figure 1: CONCEPTUAL MODEL

MGT 723 Research Project

Assignment 3

As per the conceptual model, dependent variable is the quantitative variable and the response from

different government on the changes in percentage from the previous year in the form of Scope 1

and Scope 2 carbon emission combined. The company with the reports on carbon footprint and GRI

are the control variable which follows the rules of the carbon emission of the countries USA and

Australia. A basic factor on which the model had been set up. The independent variable is the

categorical variable which has response to the incentives provided by the company or not to the

stakeholders to advance the performance of the companies. Here, it acknowledges the effectiveness

of carbon emission rate. This conceptual framework even lays the foundation of hypothesis.

Theoretical

Construct

Proxy measure (From CDP

survey provided)

Control Variable (CV),

Independent Variable (IV)

and Dependent Variable

(DV)

Measurement

Scale:

Nominal,

Ordinal, or

Scale (Ratio)

Incentives CC1.2 - Do you provide IV Nominal

Ashish Tiwari 1113814 7 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MGT 723 Research Project

Assignment 3

incentives for the

management of climate

change issues, including the

attainment of targets? (Yes or

No)

Countries and GRI Countries from USA and

Australia and their industries

CV Nominal

Changes in

percentage of

Carbon Emission

2013 CC12.2 C5 - Please

describe your gross global

combined Scope 1 and 2

emissions for the reporting

year in metric tonnes CO2e

per unit currency total

revenue - % change from

previous year +/-

DV Scale

Table 1: Theoretical Constructs for the conceptual Model

Hypotheses

The changes in carbon emission rate is because of the rules and regulations followed by their

countries. Also, the target set are the national targets to reduce emission. The hypothesis that can

be generated from the conceptual model is:

H0: Null Hypothesis: There is no significant relationship between carbon emission and the incentives

provided by the companies to the management for the climate change issues.

H1: Alternate Hypothesis: There is significant relationship between carbon emission and the

incentives provided by the companies to the management for the climate change issues.

Ashish Tiwari 1113814 8 | P a g e

Assignment 3

incentives for the

management of climate

change issues, including the

attainment of targets? (Yes or

No)

Countries and GRI Countries from USA and

Australia and their industries

CV Nominal

Changes in

percentage of

Carbon Emission

2013 CC12.2 C5 - Please

describe your gross global

combined Scope 1 and 2

emissions for the reporting

year in metric tonnes CO2e

per unit currency total

revenue - % change from

previous year +/-

DV Scale

Table 1: Theoretical Constructs for the conceptual Model

Hypotheses

The changes in carbon emission rate is because of the rules and regulations followed by their

countries. Also, the target set are the national targets to reduce emission. The hypothesis that can

be generated from the conceptual model is:

H0: Null Hypothesis: There is no significant relationship between carbon emission and the incentives

provided by the companies to the management for the climate change issues.

H1: Alternate Hypothesis: There is significant relationship between carbon emission and the

incentives provided by the companies to the management for the climate change issues.

Ashish Tiwari 1113814 8 | P a g e

MGT 723 Research Project

Assignment 3

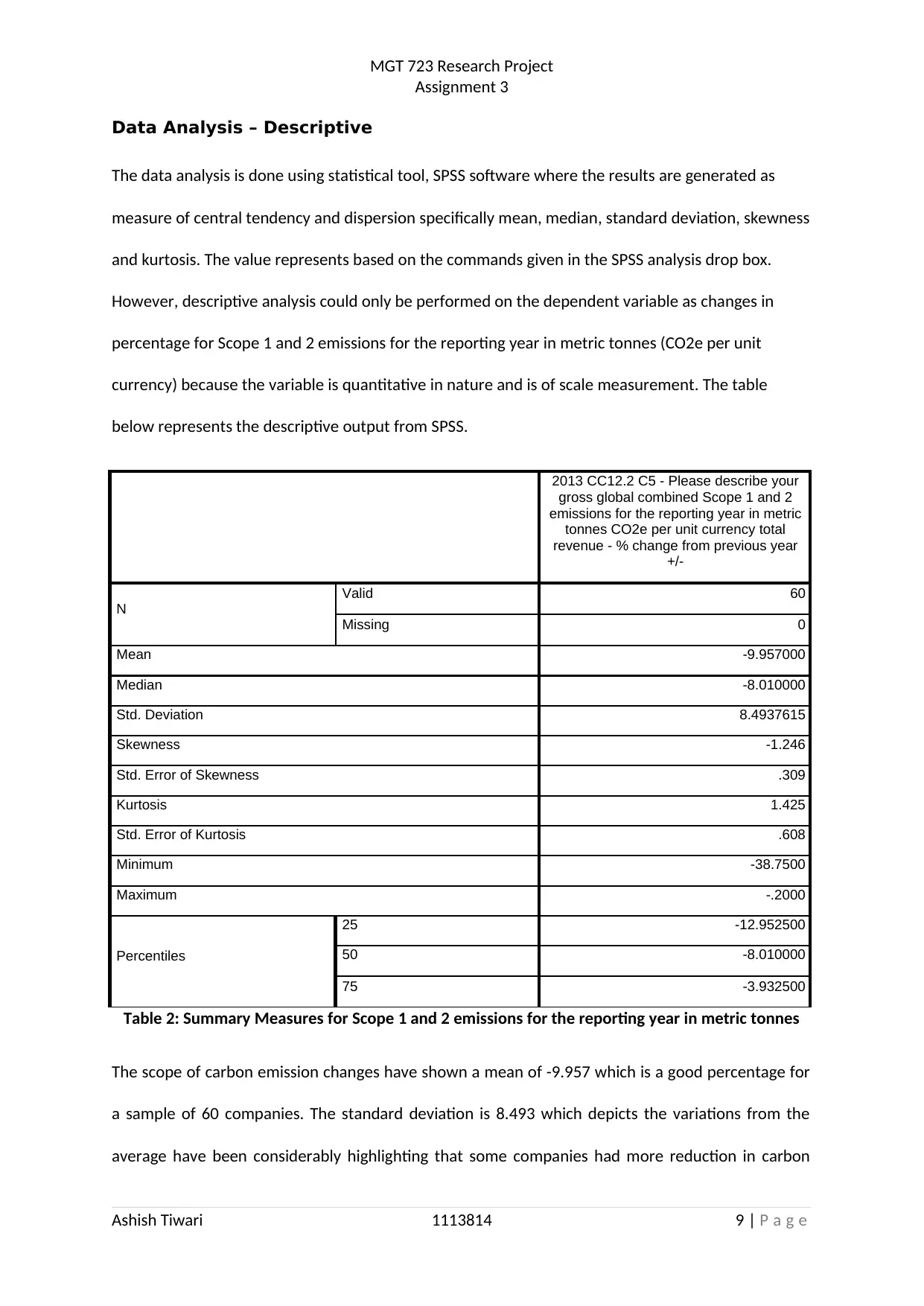

Data Analysis – Descriptive

The data analysis is done using statistical tool, SPSS software where the results are generated as

measure of central tendency and dispersion specifically mean, median, standard deviation, skewness

and kurtosis. The value represents based on the commands given in the SPSS analysis drop box.

However, descriptive analysis could only be performed on the dependent variable as changes in

percentage for Scope 1 and 2 emissions for the reporting year in metric tonnes (CO2e per unit

currency) because the variable is quantitative in nature and is of scale measurement. The table

below represents the descriptive output from SPSS.

2013 CC12.2 C5 - Please describe your

gross global combined Scope 1 and 2

emissions for the reporting year in metric

tonnes CO2e per unit currency total

revenue - % change from previous year

+/-

N

Valid 60

Missing 0

Mean -9.957000

Median -8.010000

Std. Deviation 8.4937615

Skewness -1.246

Std. Error of Skewness .309

Kurtosis 1.425

Std. Error of Kurtosis .608

Minimum -38.7500

Maximum -.2000

Percentiles

25 -12.952500

50 -8.010000

75 -3.932500

Table 2: Summary Measures for Scope 1 and 2 emissions for the reporting year in metric tonnes

The scope of carbon emission changes have shown a mean of -9.957 which is a good percentage for

a sample of 60 companies. The standard deviation is 8.493 which depicts the variations from the

average have been considerably highlighting that some companies had more reduction in carbon

Ashish Tiwari 1113814 9 | P a g e

Assignment 3

Data Analysis – Descriptive

The data analysis is done using statistical tool, SPSS software where the results are generated as

measure of central tendency and dispersion specifically mean, median, standard deviation, skewness

and kurtosis. The value represents based on the commands given in the SPSS analysis drop box.

However, descriptive analysis could only be performed on the dependent variable as changes in

percentage for Scope 1 and 2 emissions for the reporting year in metric tonnes (CO2e per unit

currency) because the variable is quantitative in nature and is of scale measurement. The table

below represents the descriptive output from SPSS.

2013 CC12.2 C5 - Please describe your

gross global combined Scope 1 and 2

emissions for the reporting year in metric

tonnes CO2e per unit currency total

revenue - % change from previous year

+/-

N

Valid 60

Missing 0

Mean -9.957000

Median -8.010000

Std. Deviation 8.4937615

Skewness -1.246

Std. Error of Skewness .309

Kurtosis 1.425

Std. Error of Kurtosis .608

Minimum -38.7500

Maximum -.2000

Percentiles

25 -12.952500

50 -8.010000

75 -3.932500

Table 2: Summary Measures for Scope 1 and 2 emissions for the reporting year in metric tonnes

The scope of carbon emission changes have shown a mean of -9.957 which is a good percentage for

a sample of 60 companies. The standard deviation is 8.493 which depicts the variations from the

average have been considerably highlighting that some companies had more reduction in carbon

Ashish Tiwari 1113814 9 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MGT 723 Research Project

Assignment 3

emission. This can be further strengthened by percentile scores, a 25th percentile score depicts the

major changes does in this part which is -12.952 followed by 50th percentile and later by 75th

percentile. The skewness and kurtosis of the distribution is negatively skewed and is leptokurtic in

nature depicting that mean , median and mode are not equal and mode > median > mean.

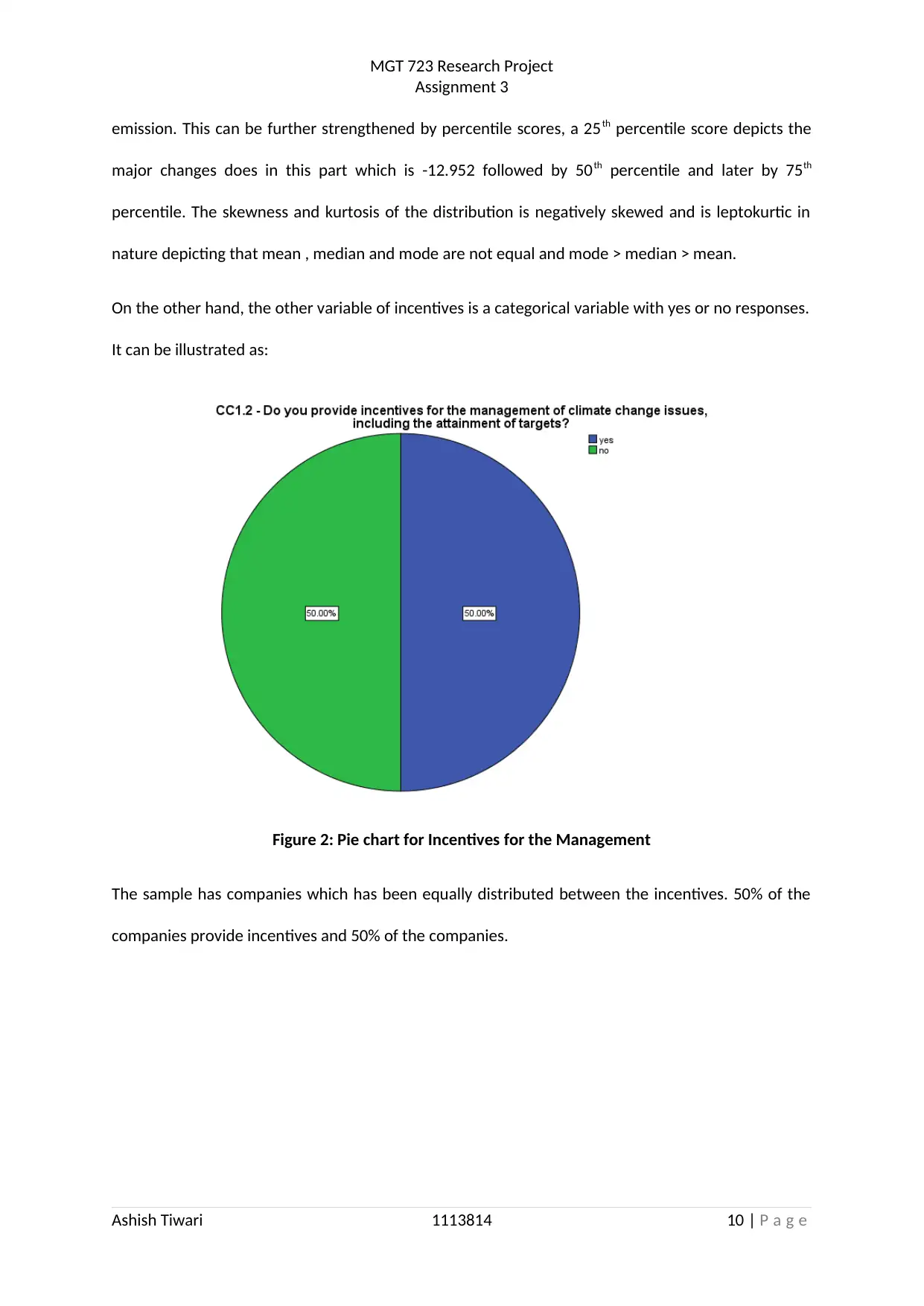

On the other hand, the other variable of incentives is a categorical variable with yes or no responses.

It can be illustrated as:

Figure 2: Pie chart for Incentives for the Management

The sample has companies which has been equally distributed between the incentives. 50% of the

companies provide incentives and 50% of the companies.

Ashish Tiwari 1113814 10 | P a g e

Assignment 3

emission. This can be further strengthened by percentile scores, a 25th percentile score depicts the

major changes does in this part which is -12.952 followed by 50th percentile and later by 75th

percentile. The skewness and kurtosis of the distribution is negatively skewed and is leptokurtic in

nature depicting that mean , median and mode are not equal and mode > median > mean.

On the other hand, the other variable of incentives is a categorical variable with yes or no responses.

It can be illustrated as:

Figure 2: Pie chart for Incentives for the Management

The sample has companies which has been equally distributed between the incentives. 50% of the

companies provide incentives and 50% of the companies.

Ashish Tiwari 1113814 10 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MGT 723 Research Project

Assignment 3

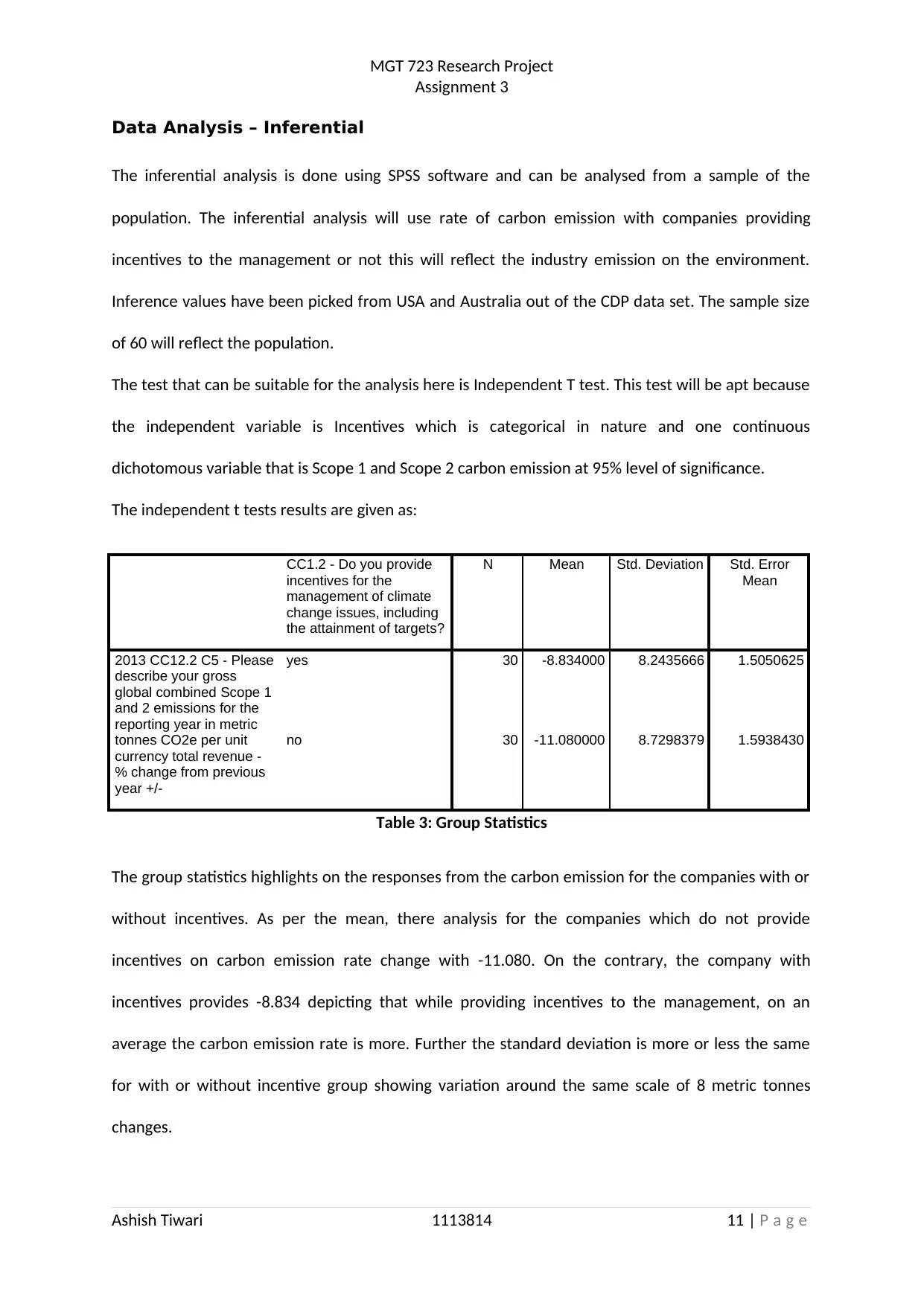

Data Analysis – Inferential

The inferential analysis is done using SPSS software and can be analysed from a sample of the

population. The inferential analysis will use rate of carbon emission with companies providing

incentives to the management or not this will reflect the industry emission on the environment.

Inference values have been picked from USA and Australia out of the CDP data set. The sample size

of 60 will reflect the population.

The test that can be suitable for the analysis here is Independent T test. This test will be apt because

the independent variable is Incentives which is categorical in nature and one continuous

dichotomous variable that is Scope 1 and Scope 2 carbon emission at 95% level of significance.

The independent t tests results are given as:

CC1.2 - Do you provide

incentives for the

management of climate

change issues, including

the attainment of targets?

N Mean Std. Deviation Std. Error

Mean

2013 CC12.2 C5 - Please

describe your gross

global combined Scope 1

and 2 emissions for the

reporting year in metric

tonnes CO2e per unit

currency total revenue -

% change from previous

year +/-

yes 30 -8.834000 8.2435666 1.5050625

no 30 -11.080000 8.7298379 1.5938430

Table 3: Group Statistics

The group statistics highlights on the responses from the carbon emission for the companies with or

without incentives. As per the mean, there analysis for the companies which do not provide

incentives on carbon emission rate change with -11.080. On the contrary, the company with

incentives provides -8.834 depicting that while providing incentives to the management, on an

average the carbon emission rate is more. Further the standard deviation is more or less the same

for with or without incentive group showing variation around the same scale of 8 metric tonnes

changes.

Ashish Tiwari 1113814 11 | P a g e

Assignment 3

Data Analysis – Inferential

The inferential analysis is done using SPSS software and can be analysed from a sample of the

population. The inferential analysis will use rate of carbon emission with companies providing

incentives to the management or not this will reflect the industry emission on the environment.

Inference values have been picked from USA and Australia out of the CDP data set. The sample size

of 60 will reflect the population.

The test that can be suitable for the analysis here is Independent T test. This test will be apt because

the independent variable is Incentives which is categorical in nature and one continuous

dichotomous variable that is Scope 1 and Scope 2 carbon emission at 95% level of significance.

The independent t tests results are given as:

CC1.2 - Do you provide

incentives for the

management of climate

change issues, including

the attainment of targets?

N Mean Std. Deviation Std. Error

Mean

2013 CC12.2 C5 - Please

describe your gross

global combined Scope 1

and 2 emissions for the

reporting year in metric

tonnes CO2e per unit

currency total revenue -

% change from previous

year +/-

yes 30 -8.834000 8.2435666 1.5050625

no 30 -11.080000 8.7298379 1.5938430

Table 3: Group Statistics

The group statistics highlights on the responses from the carbon emission for the companies with or

without incentives. As per the mean, there analysis for the companies which do not provide

incentives on carbon emission rate change with -11.080. On the contrary, the company with

incentives provides -8.834 depicting that while providing incentives to the management, on an

average the carbon emission rate is more. Further the standard deviation is more or less the same

for with or without incentive group showing variation around the same scale of 8 metric tonnes

changes.

Ashish Tiwari 1113814 11 | P a g e

MGT 723 Research Project

Assignment 3

Levene's

Test for

Equality

of

Variances

t-test for Equality of Means

F Sig. t df Sig.

(2-

tailed

)

Mean

Difference

Std. Error

Difference

95%

Confidenc

e Interval

of the

Difference

Lower Upper

2013

CC12.2

C5 -

Please

describe

your gross

global

combined

Scope 1

and 2

emissions

for the

reporting

year in

metric

tonnes

CO2e per

unit

currency

total

revenue -

% change

from

previous

year +/-

Equal

variances

assumed

.00

6

.93

8

1.02

5 58 .310 2.246000

0

2.192156

2

-

2.1420773

6.634077

3

Equal

variances

not

assumed

1.02

5

57.81

1 .310 2.246000

0

2.192156

2

-

2.1423836

6.634383

6

Table 4: Independent Sample t- test

The independent t test for equal variances assumed would be taken as both the groups have equal

number of sample seize with around 8 metric tonnes as standard deviation. The lower and upper

bound of carbon emission rate changes are from -2.14 to 6.634 with standard error difference of

2.192.

Hypothesis testing

The hypothesis will be set statistically for the independent t – test to be taken is given as:

H0: μ1 = μ2 (no significant population mean difference between carbon emission and the incentives

provided by the companies)

Ashish Tiwari 1113814 12 | P a g e

Assignment 3

Levene's

Test for

Equality

of

Variances

t-test for Equality of Means

F Sig. t df Sig.

(2-

tailed

)

Mean

Difference

Std. Error

Difference

95%

Confidenc

e Interval

of the

Difference

Lower Upper

2013

CC12.2

C5 -

Please

describe

your gross

global

combined

Scope 1

and 2

emissions

for the

reporting

year in

metric

tonnes

CO2e per

unit

currency

total

revenue -

% change

from

previous

year +/-

Equal

variances

assumed

.00

6

.93

8

1.02

5 58 .310 2.246000

0

2.192156

2

-

2.1420773

6.634077

3

Equal

variances

not

assumed

1.02

5

57.81

1 .310 2.246000

0

2.192156

2

-

2.1423836

6.634383

6

Table 4: Independent Sample t- test

The independent t test for equal variances assumed would be taken as both the groups have equal

number of sample seize with around 8 metric tonnes as standard deviation. The lower and upper

bound of carbon emission rate changes are from -2.14 to 6.634 with standard error difference of

2.192.

Hypothesis testing

The hypothesis will be set statistically for the independent t – test to be taken is given as:

H0: μ1 = μ2 (no significant population mean difference between carbon emission and the incentives

provided by the companies)

Ashish Tiwari 1113814 12 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.