Carbon Emission Disclosure and Business Strategies Analysis

VerifiedAdded on 2021/05/31

|14

|2235

|190

Report

AI Summary

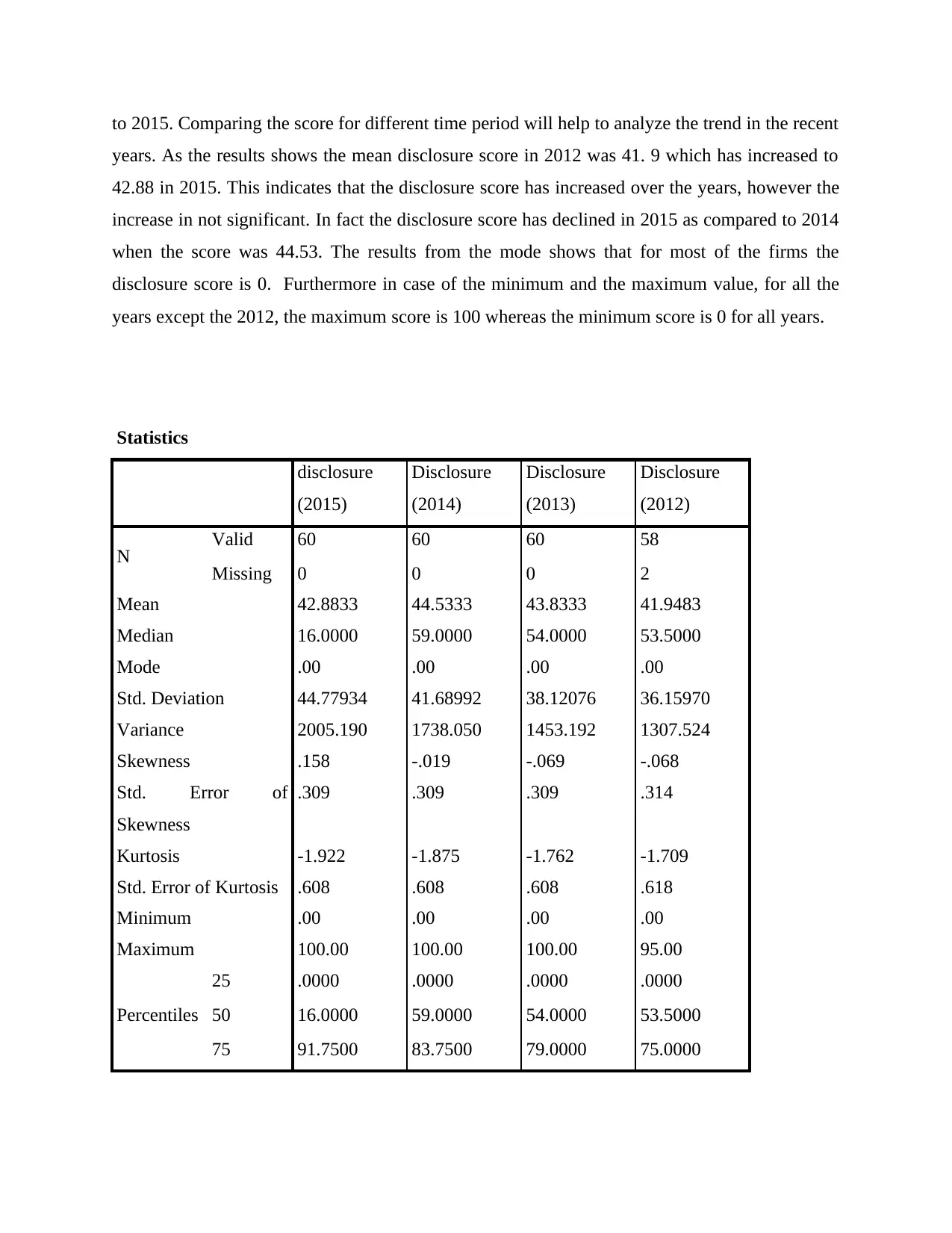

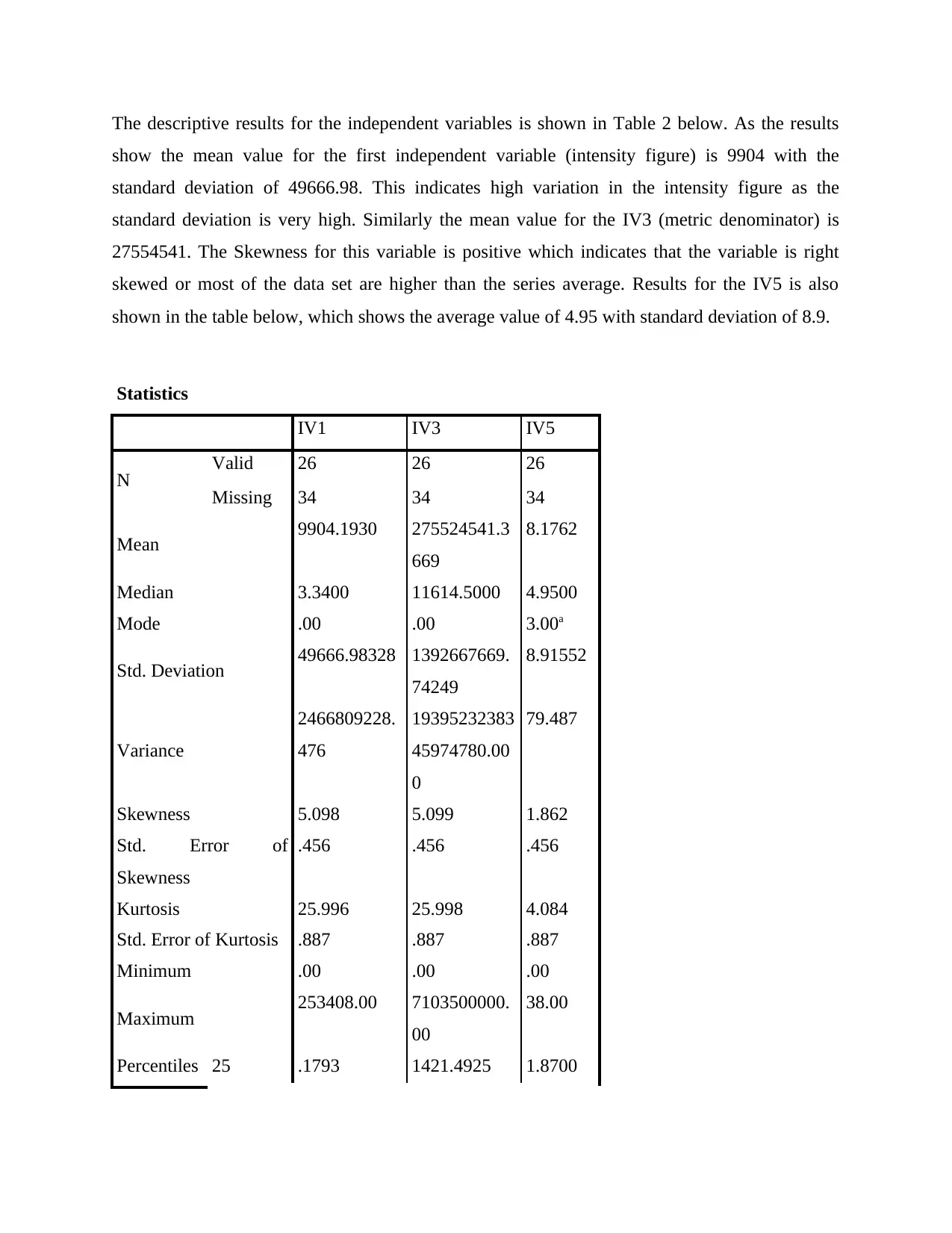

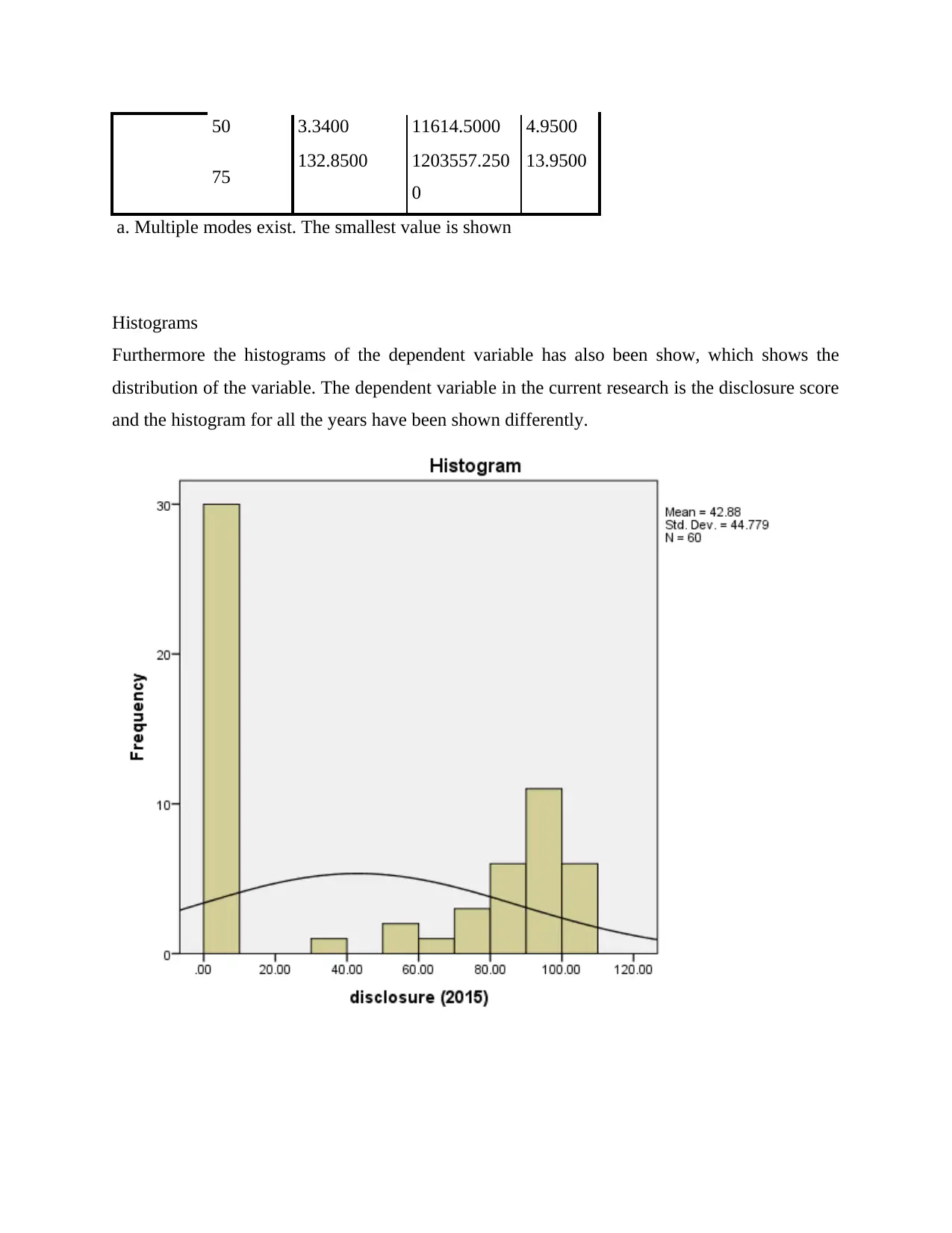

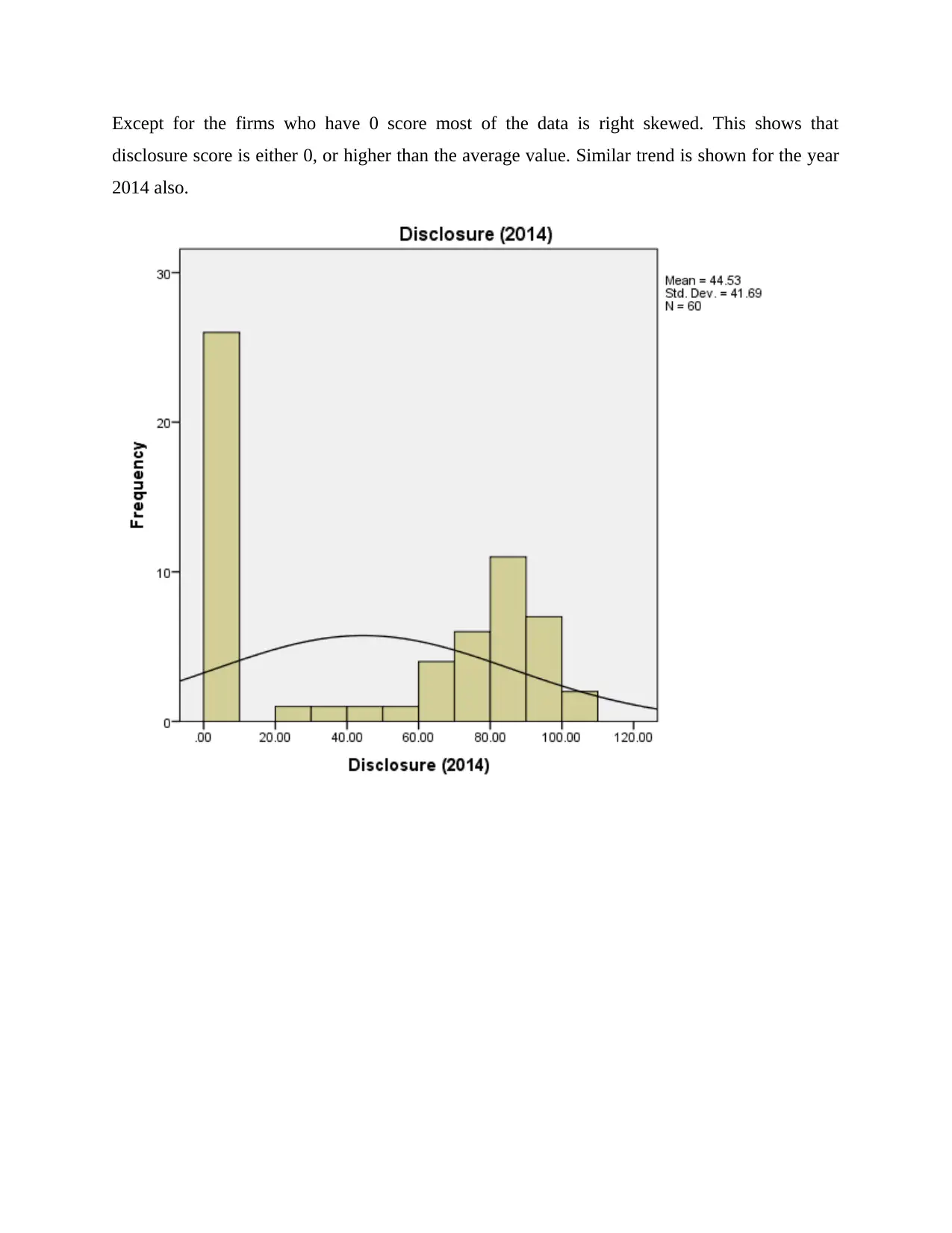

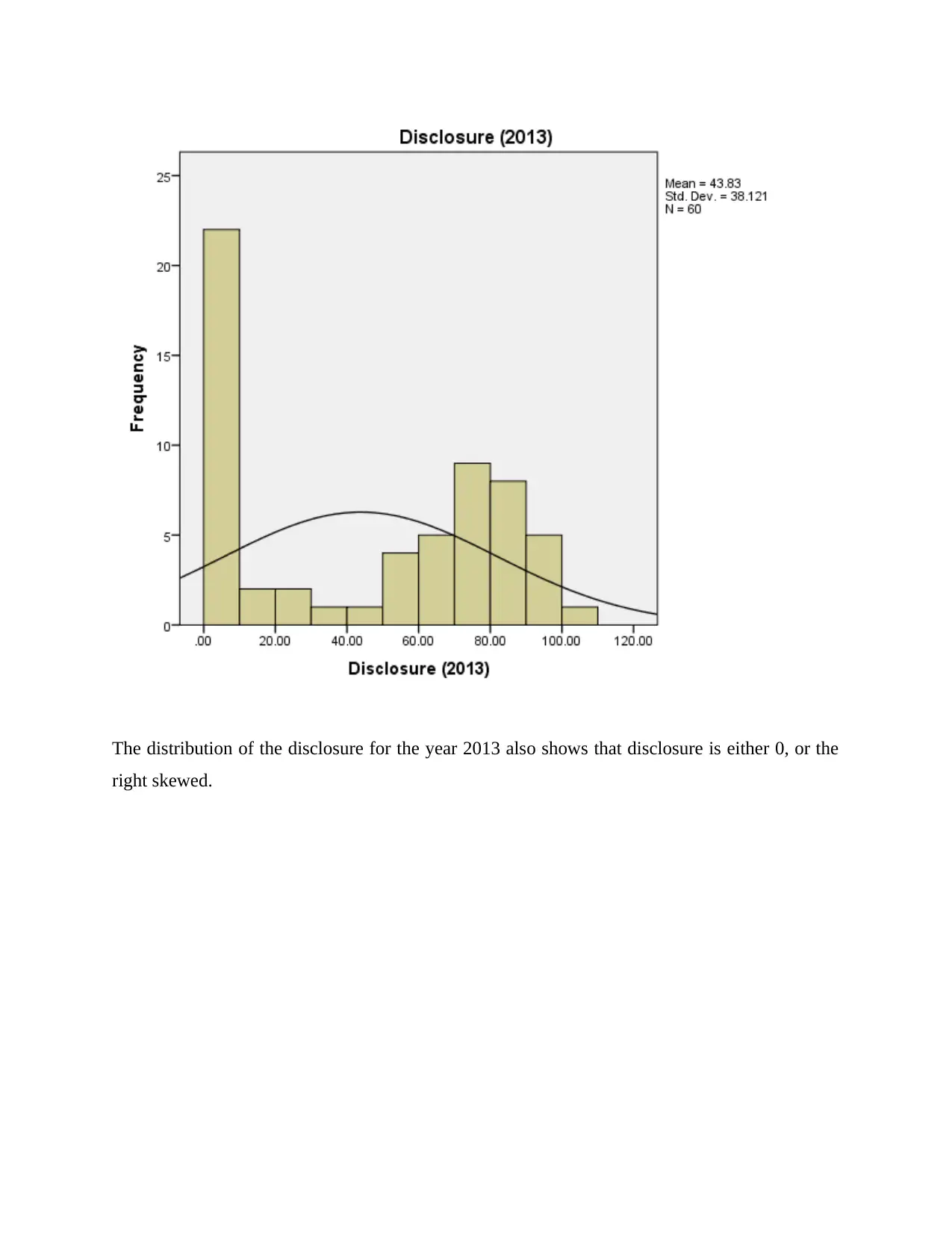

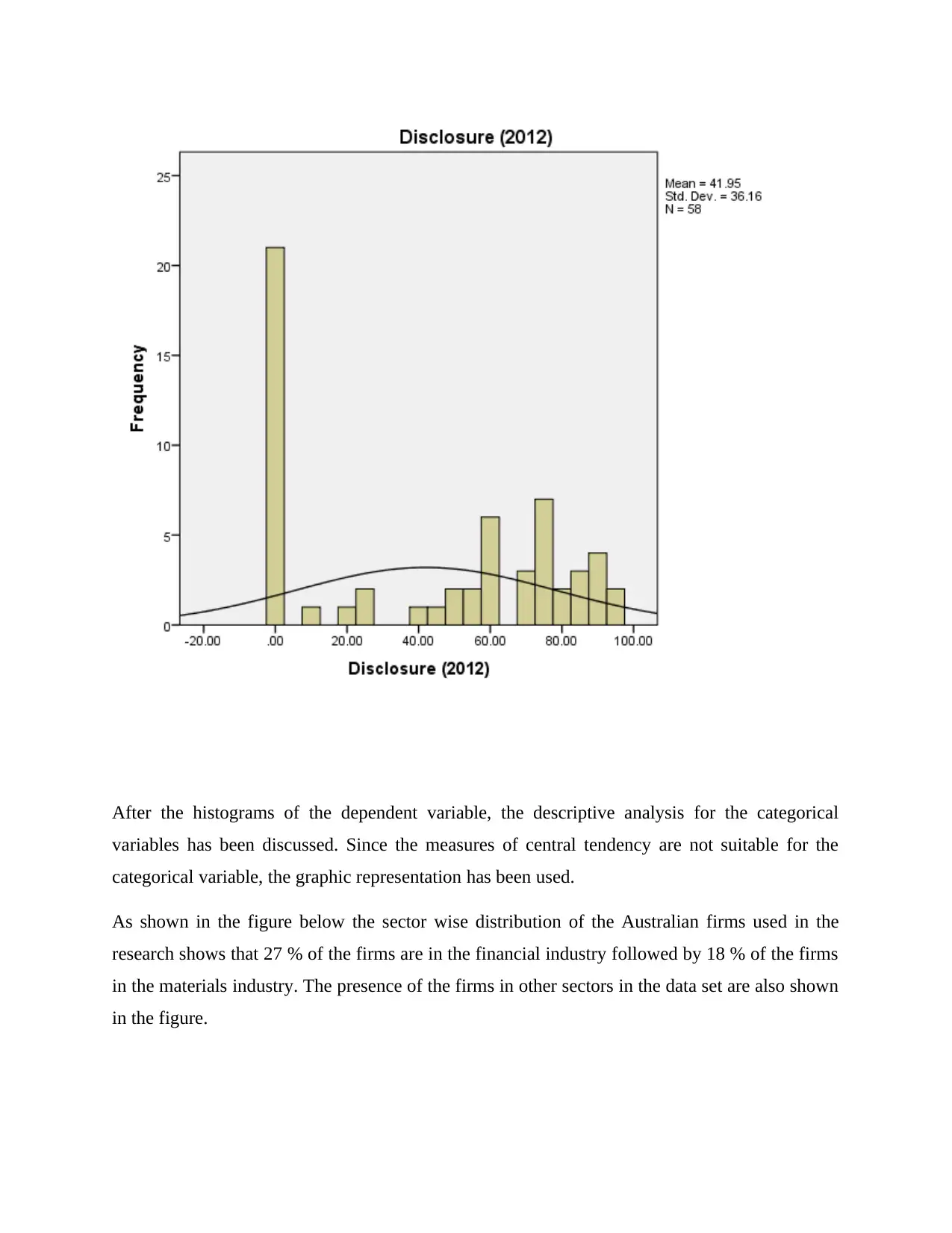

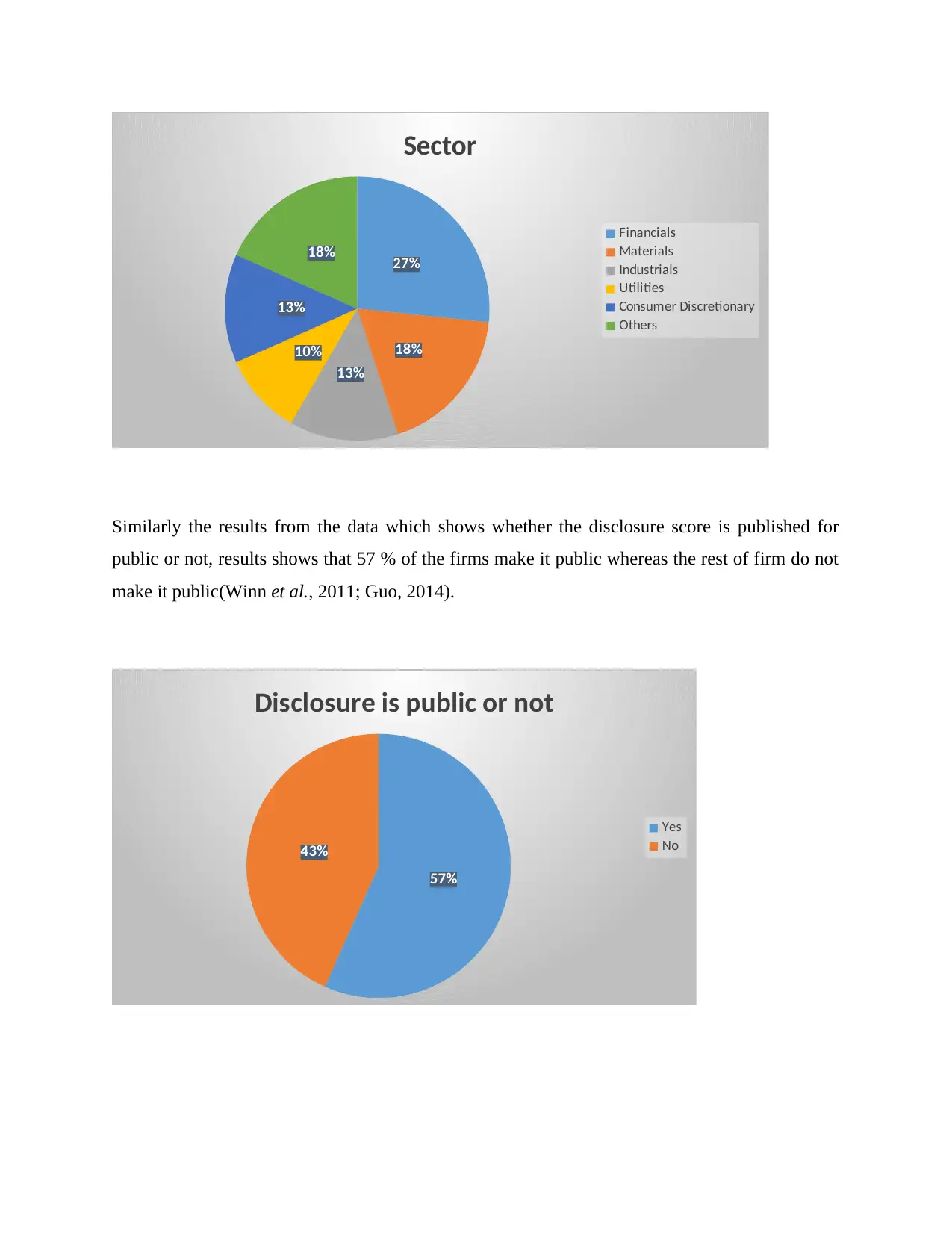

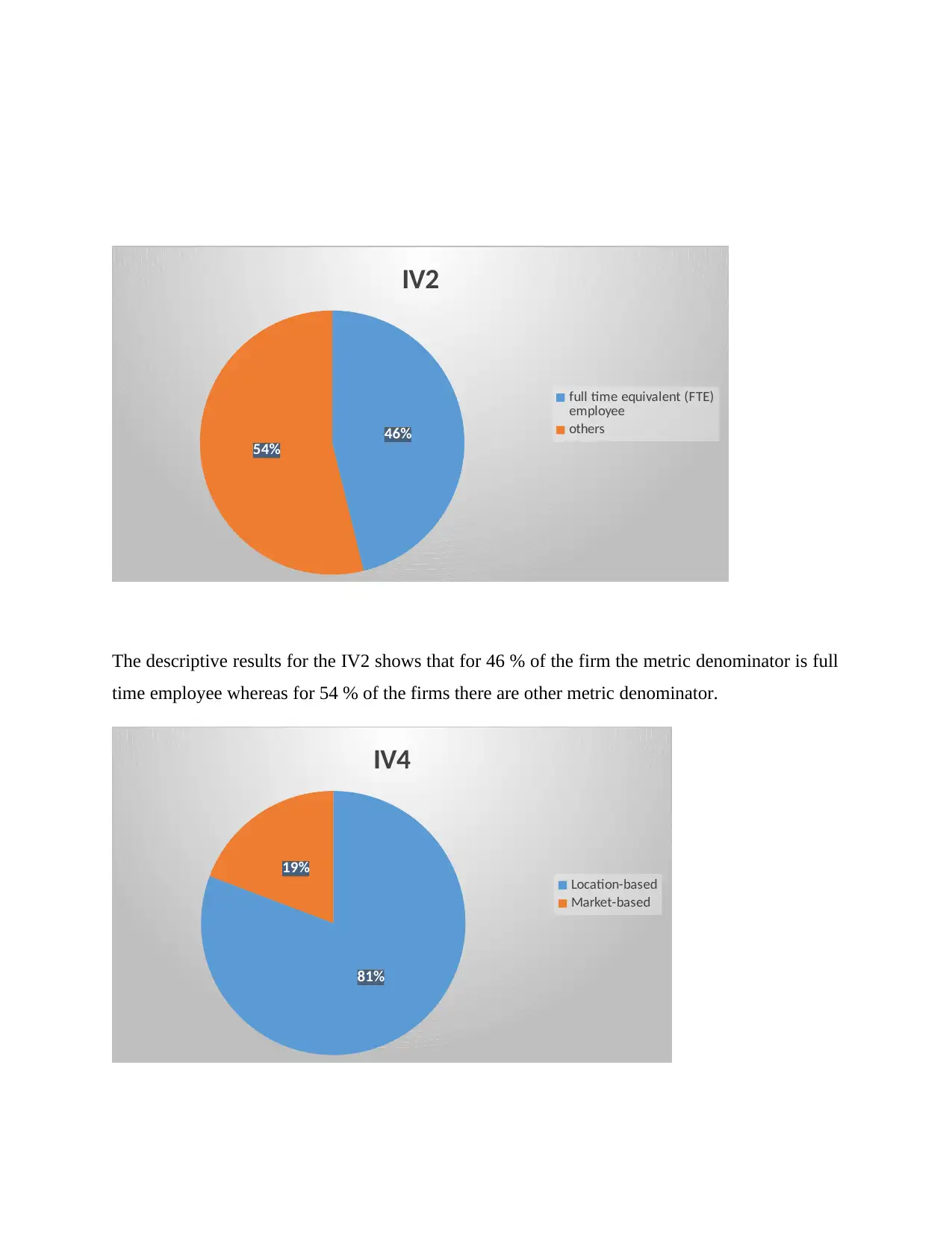

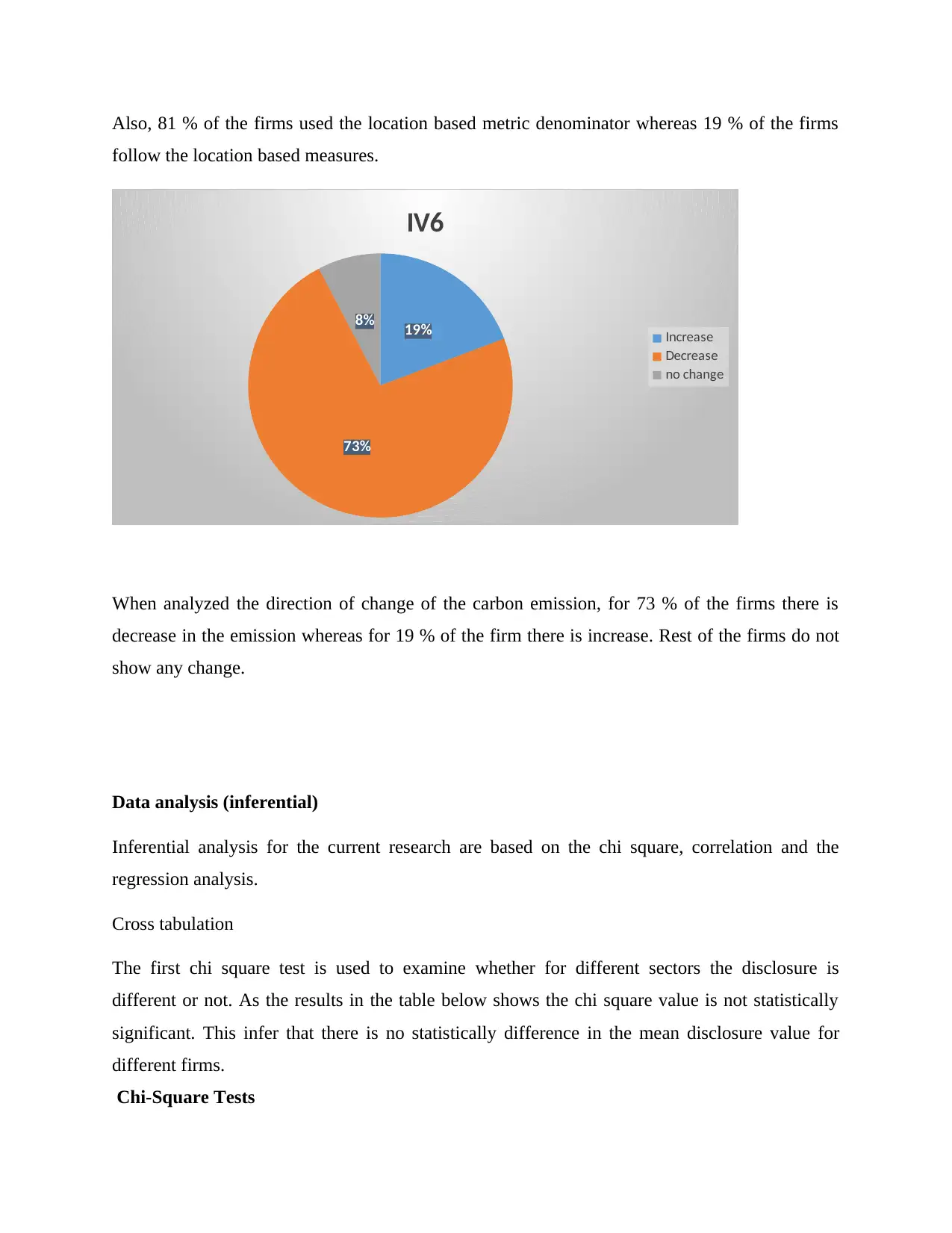

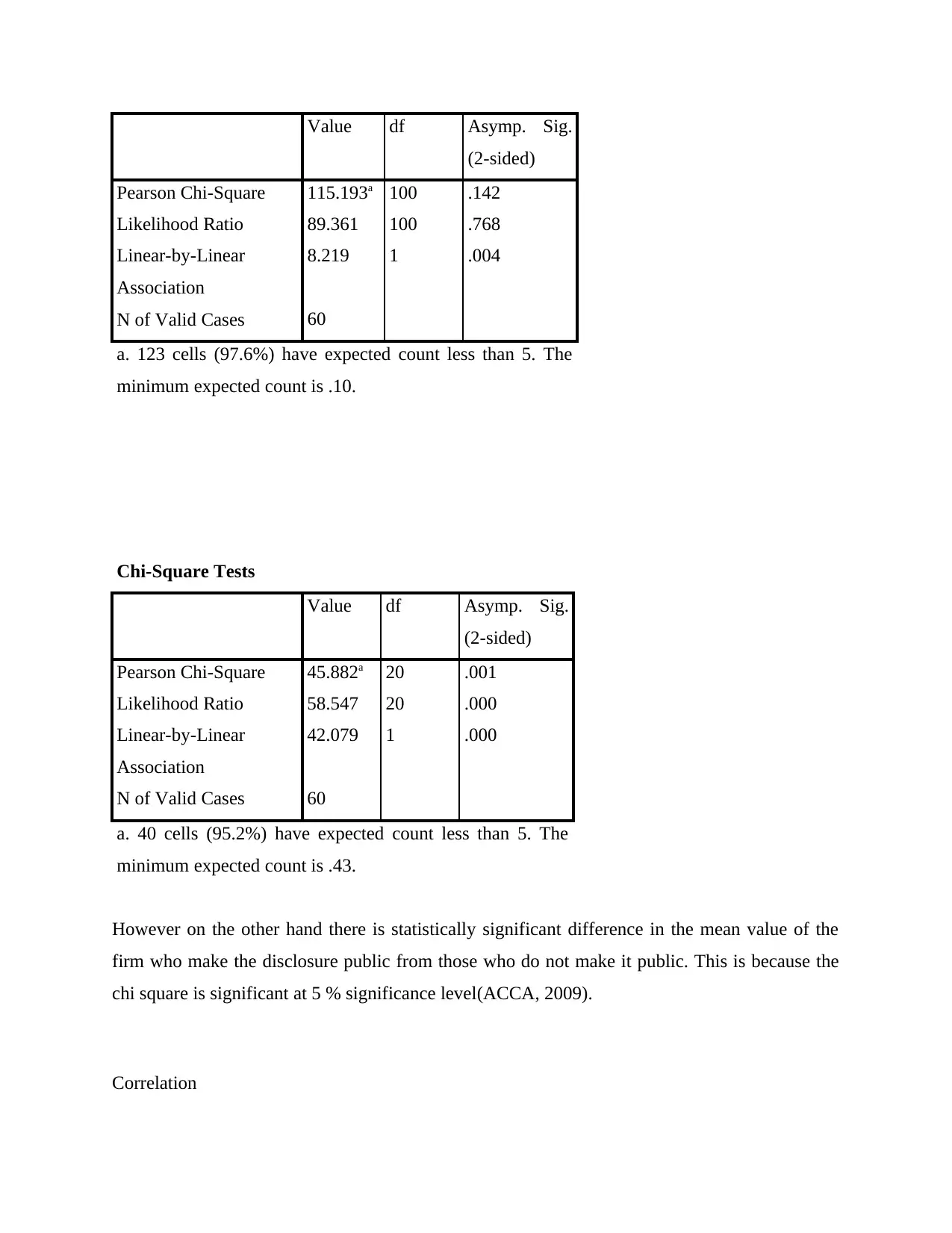

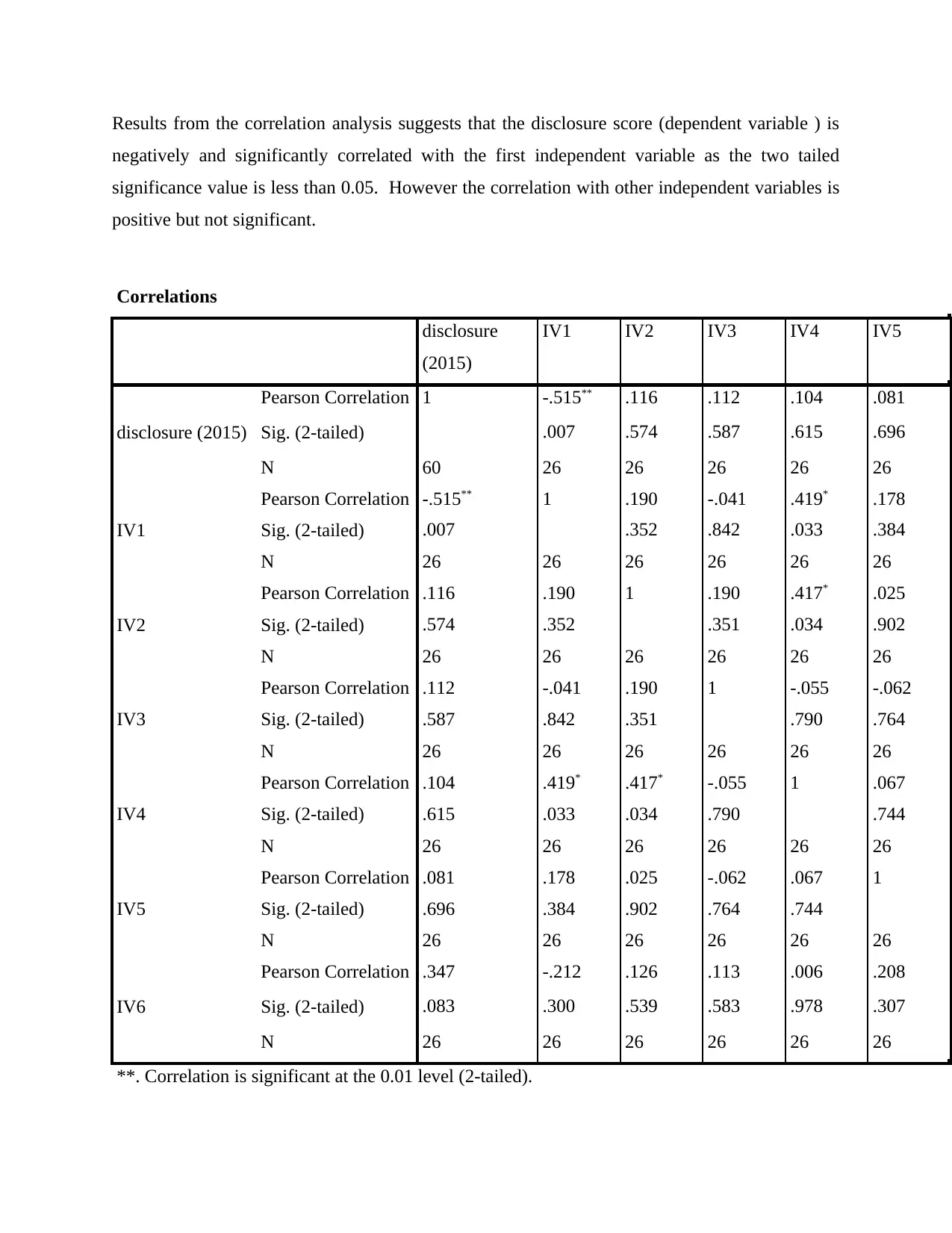

This report investigates the relationship between voluntary carbon emission disclosures of Australian firms and their climate change business strategies, framed within the context of agency theory. The study, based on a sample of 60 firms, analyzes data from 2012 to 2015, employing descriptive, correlational, and regression analyses. Descriptive statistics reveal an increasing, though not always significant, trend in disclosure scores. Inferential analysis, including chi-square, correlation, and regression, examines the impact of various independent variables on disclosure scores. The findings indicate a negative and significant correlation between disclosure scores and an intensity figure, while a regression model highlights the significance of specific independent variables like the intensity figure and a sector variable. The report offers insights into the determinants of carbon emission disclosures and their connection to business strategies, which can help firms and regulators to deal with climate change.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.